- Risk and its treatment

Содержание

- 2. Agenda Definitions of Risk Chance of Loss Peril and Hazard Classification of Risk Major Personal Risks

- 3. Definitions of Risk Traditional Definition of Risk: Uncertainty concerning the occurrence of a loss In the

- 4. Loss Exposure: Any situation or circumstance in which a loss is possible, regardless of whether a

- 5. Chance of Loss Chance of loss: The probability that an event will occur Objective probability refers

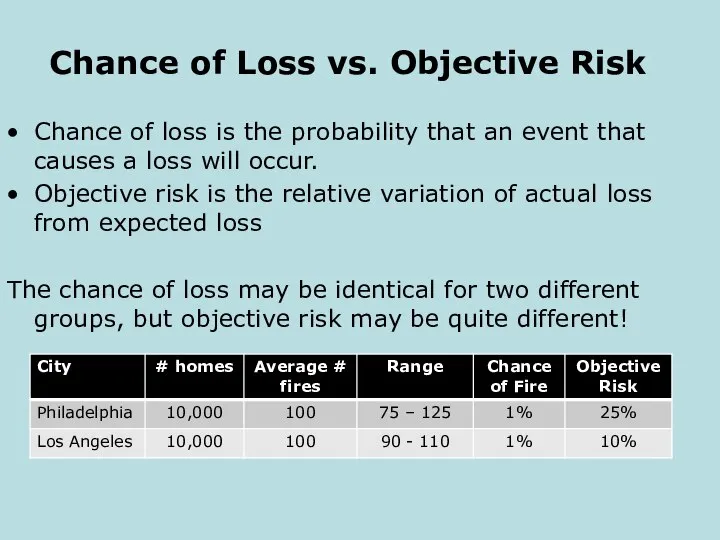

- 6. Chance of Loss vs. Objective Risk Chance of loss is the probability that an event that

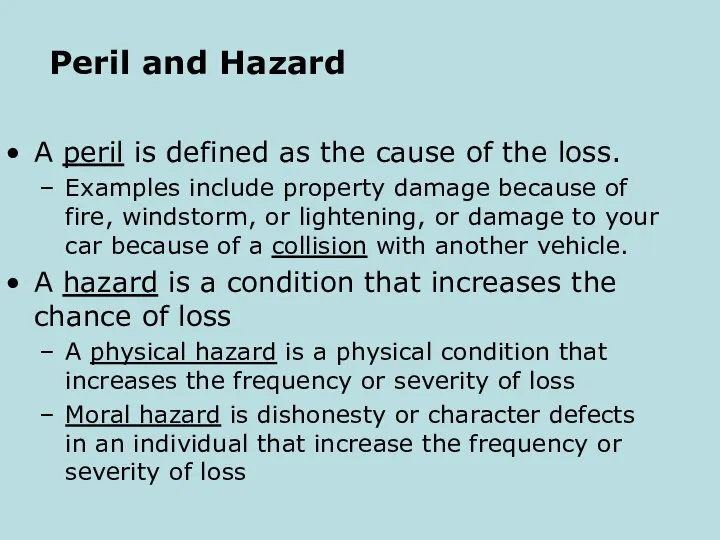

- 7. Peril and Hazard A peril is defined as the cause of the loss. Examples include property

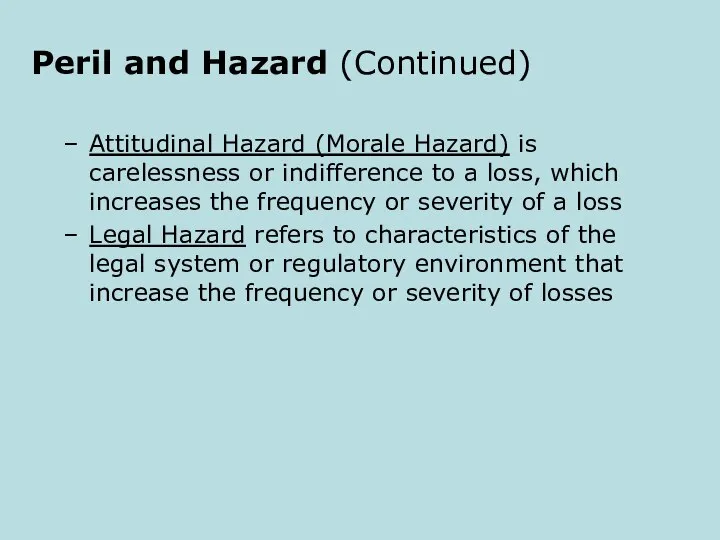

- 8. Peril and Hazard (Continued) Attitudinal Hazard (Morale Hazard) is carelessness or indifference to a loss, which

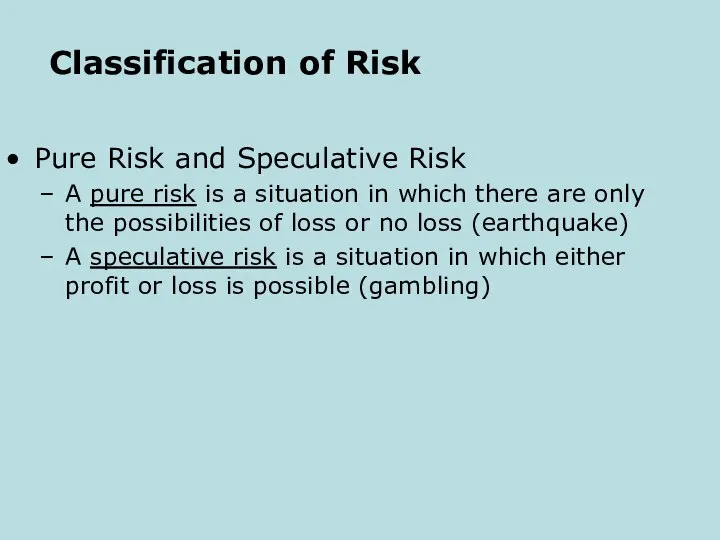

- 9. Classification of Risk Pure Risk and Speculative Risk A pure risk is a situation in which

- 10. Classification of Risk (Continued) Diversifiable Risk and Nondiversifiable Risk A diversifiable risk affects only individuals or

- 11. Classification of Risk (Continued) Enterprise risk encompasses all major risks faced by a business firm, which

- 12. Classification of Risk (Continued) Enterprise Risk Management combines into a single unified treatment program all major

- 13. Classification of Risk (Continued) As long as all risks are not perfectly correlated, the firm can

- 14. Classification of Risk (Continued) Systemic risk is the risk of collapse of an entire system or

- 15. Major Personal Risks Personal risks are risks that directly affect an individual or family. They involve

- 16. Exhibit 1.1 Total Savings and Investments Reported by Retirees, Among Those Responding (not including value of

- 17. Major Personal Risks (Continued) Property risks involve the possibility of losses associated with the destruction or

- 18. Major Personal Risks (Continued) Liability risks involve the possibility of being held legally liable for bodily

- 19. Major Commercial Risks Firms face a variety of pure risks that can have serious financial consequences

- 20. Major Commercial Risks (Continued) Other risks faced by business firms include: Human resources exposures, such as

- 21. Burden of Risk on Society The presence of risk results in three major burdens on society:

- 22. Techniques for Managing Risk Risk Control refers to techniques that reduce the frequency or severity of

- 23. Techniques for Managing Risk (Continued) Risk Financing refers to techniques that provide for payment of losses

- 24. Techniques for Managing Risk (Continued) Self Insurance is a special form of planned retention by which

- 26. Скачать презентацию

Слайд 2Agenda

Definitions of Risk

Chance of Loss

Peril and Hazard

Classification of Risk

Major Personal Risks and

Agenda

Definitions of Risk

Chance of Loss

Peril and Hazard

Classification of Risk

Major Personal Risks and

Слайд 3Definitions of Risk

Traditional Definition of Risk: Uncertainty concerning the occurrence of a

Definitions of Risk

Traditional Definition of Risk: Uncertainty concerning the occurrence of a

Слайд 4Loss Exposure: Any situation or circumstance in which a loss is possible,

Loss Exposure: Any situation or circumstance in which a loss is possible,

Слайд 5Chance of Loss

Chance of loss: The probability that an event will occur

Objective

Chance of Loss

Chance of loss: The probability that an event will occur

Objective

Слайд 6Chance of Loss vs. Objective Risk

Chance of loss is the probability that

Chance of Loss vs. Objective Risk

Chance of loss is the probability that

Слайд 7Peril and Hazard

A peril is defined as the cause of the loss.

Examples

Peril and Hazard

A peril is defined as the cause of the loss.

Examples

Слайд 8Peril and Hazard (Continued)

Attitudinal Hazard (Morale Hazard) is carelessness or indifference to

Peril and Hazard (Continued)

Attitudinal Hazard (Morale Hazard) is carelessness or indifference to

Слайд 9Classification of Risk

Pure Risk and Speculative Risk

A pure risk is a situation

Classification of Risk

Pure Risk and Speculative Risk

A pure risk is a situation

Слайд 10Classification of Risk (Continued)

Diversifiable Risk and Nondiversifiable Risk

A diversifiable risk affects only

Classification of Risk (Continued)

Diversifiable Risk and Nondiversifiable Risk

A diversifiable risk affects only

Слайд 11Classification of Risk (Continued)

Enterprise risk encompasses all major risks faced by a

Classification of Risk (Continued)

Enterprise risk encompasses all major risks faced by a

Слайд 12Classification of Risk (Continued)

Enterprise Risk Management combines into a single unified treatment

Classification of Risk (Continued)

Enterprise Risk Management combines into a single unified treatment

Слайд 13Classification of Risk (Continued)

As long as all risks are not perfectly correlated,

Classification of Risk (Continued)

As long as all risks are not perfectly correlated,

Слайд 14Classification of Risk (Continued)

Systemic risk is the risk of collapse of an

Classification of Risk (Continued)

Systemic risk is the risk of collapse of an

Слайд 15Major Personal Risks

Personal risks are risks that directly affect an individual or

Major Personal Risks

Personal risks are risks that directly affect an individual or

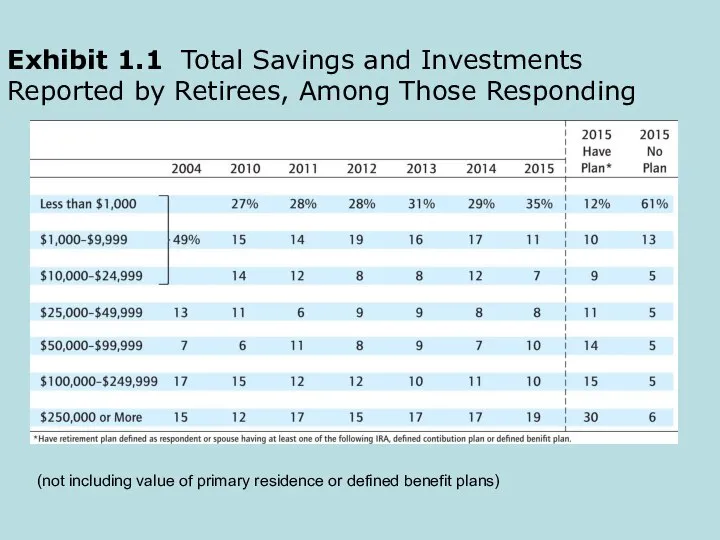

Слайд 16Exhibit 1.1 Total Savings and Investments Reported by Retirees, Among Those Responding

(not

Exhibit 1.1 Total Savings and Investments Reported by Retirees, Among Those Responding

(not

Слайд 17Major Personal Risks (Continued)

Property risks involve the possibility of losses associated with

Major Personal Risks (Continued)

Property risks involve the possibility of losses associated with

Слайд 18Major Personal Risks (Continued)

Liability risks involve the possibility of being held legally

Major Personal Risks (Continued)

Liability risks involve the possibility of being held legally

Слайд 19Major Commercial Risks

Firms face a variety of pure risks that can have

Major Commercial Risks

Firms face a variety of pure risks that can have

Слайд 20Major Commercial Risks (Continued)

Other risks faced by business firms include:

Human resources

Major Commercial Risks (Continued)

Other risks faced by business firms include:

Human resources

Слайд 21Burden of Risk on Society

The presence of risk results in three major

Burden of Risk on Society

The presence of risk results in three major

Слайд 22Techniques for Managing Risk

Risk Control refers to techniques that reduce the frequency

Techniques for Managing Risk

Risk Control refers to techniques that reduce the frequency

Слайд 23Techniques for Managing Risk (Continued)

Risk Financing refers to techniques that provide for

Techniques for Managing Risk (Continued)

Risk Financing refers to techniques that provide for

Слайд 24Techniques for Managing Risk (Continued)

Self Insurance is a special form of planned

Techniques for Managing Risk (Continued)

Self Insurance is a special form of planned

Маршрут твоей жизни. Твоя возможность показать себя!

Маршрут твоей жизни. Твоя возможность показать себя! Башкирский государственный университет. Магистратура по социологии с применением дистанционных технологий обучения

Башкирский государственный университет. Магистратура по социологии с применением дистанционных технологий обучения Курсовой проект. Сборка, разборка сцепления

Курсовой проект. Сборка, разборка сцепления Регенерация дождевого червя

Регенерация дождевого червя Турклуб УрФУ Романтик. Психологический климат туристской группы

Турклуб УрФУ Романтик. Психологический климат туристской группы Энергосбережение, как способ модернизации экономики

Энергосбережение, как способ модернизации экономики Праздничные народные гулянья. 1 часть

Праздничные народные гулянья. 1 часть Презентация по английскому my working day

Презентация по английскому my working day Билеты для зачета

Билеты для зачета Разрушенные и восстановленные храмы. Церковь Вознесения. Христова в Орлецах

Разрушенные и восстановленные храмы. Церковь Вознесения. Христова в Орлецах Зачем нужен сайт?

Зачем нужен сайт? Выразительность русской речи

Выразительность русской речи Презентация на тему Транспорт и проезжая часть

Презентация на тему Транспорт и проезжая часть  Cовместное развлекательно-познавательное мероприятие Свет материнской любви

Cовместное развлекательно-познавательное мероприятие Свет материнской любви Оперативное общение в новом формате

Оперативное общение в новом формате Презентация на тему Из истории денег

Презентация на тему Из истории денег Мой дом Петропавловск-Камчатский

Мой дом Петропавловск-Камчатский Троянские программы и защита от них

Троянские программы и защита от них Сложение и вычитание чисел с переходом через 10. Единицы измерения длины – см и дм.

Сложение и вычитание чисел с переходом через 10. Единицы измерения длины – см и дм. Загадки о Санкт – Петербурге для детей 5-7 лет

Загадки о Санкт – Петербурге для детей 5-7 лет В.р.б.и, т.трад., п.л.то, учител., к.н.ки, вернуть, корабл., к.ртофель.

В.р.б.и, т.трад., п.л.то, учител., к.н.ки, вернуть, корабл., к.ртофель. Общественное движение: либералы и консерваторы

Общественное движение: либералы и консерваторы Русский язык как развивающееся явление

Русский язык как развивающееся явление Volumes of Revolution

Volumes of Revolution  Машины переменного тока. Трансформаторы

Машины переменного тока. Трансформаторы Портфолио ВОСПИТАТЕЛЯ ДЕТСКОГО САДА

Портфолио ВОСПИТАТЕЛЯ ДЕТСКОГО САДА Опрос прохожих. Команда Black Sect + 220

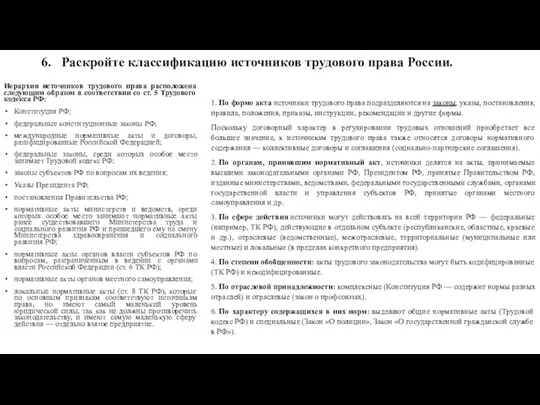

Опрос прохожих. Команда Black Sect + 220 Иерархия источников трудового права. Ответы на вопросы 5,13,16

Иерархия источников трудового права. Ответы на вопросы 5,13,16