- Session 1.2_Time Value of Money

Содержание

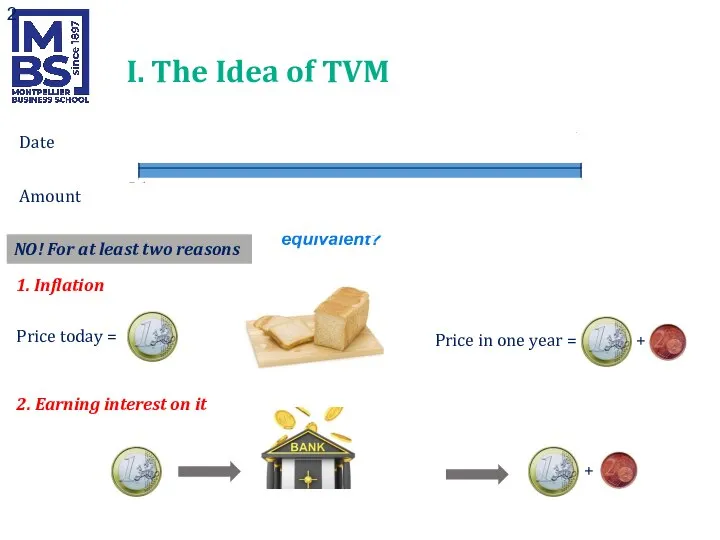

- 2. I. The Idea of TVM € 1 Date Amount 0 (today) € 1 1 (end of

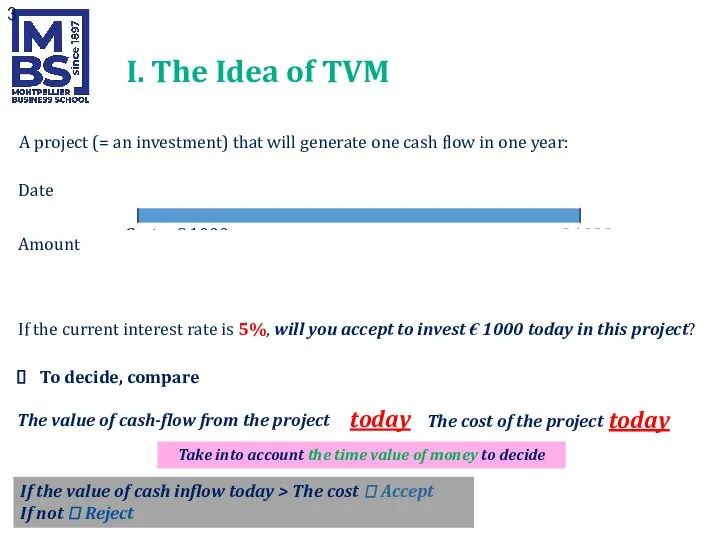

- 3. A project (= an investment) that will generate one cash flow in one year: I. The

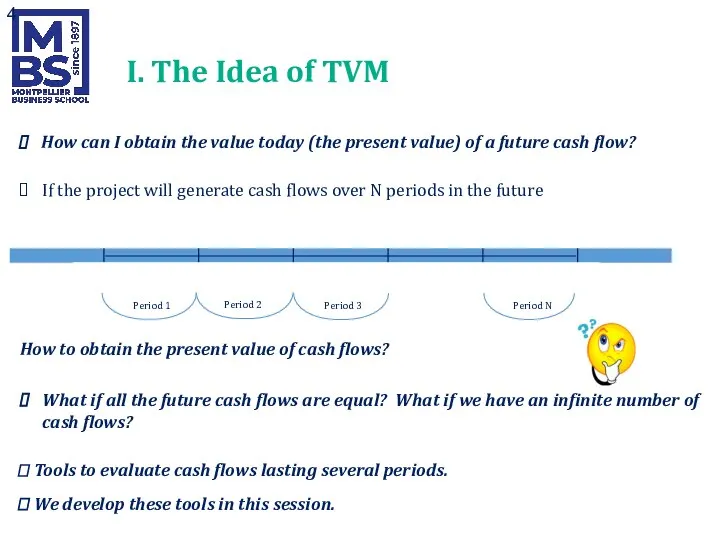

- 4. I. The Idea of TVM How can I obtain the value today (the present value) of

- 5. II. The Three Rules of Time Travel Financial decisions ? Comparing or combining cash flows that

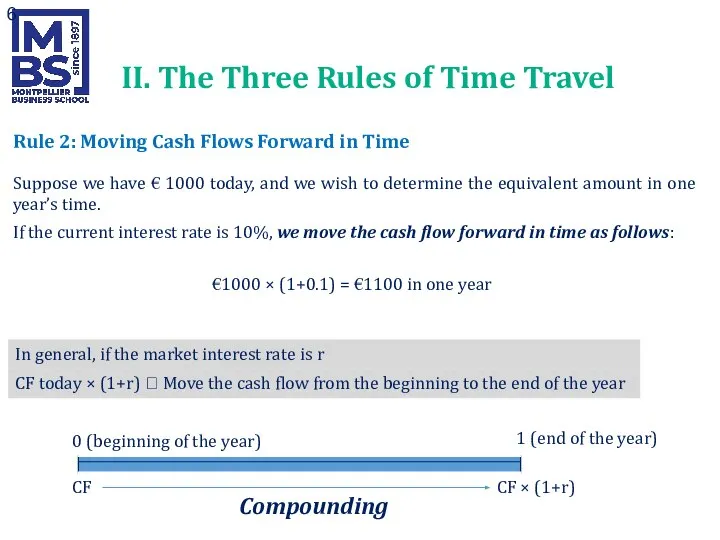

- 6. II. The Three Rules of Time Travel Rule 2: Moving Cash Flows Forward in Time Suppose

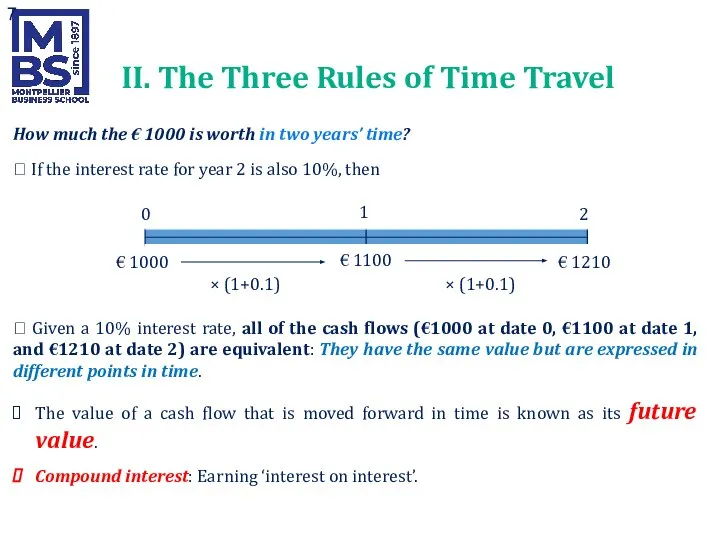

- 7. II. The Three Rules of Time Travel 0 1 2 € 1000 € 1100 € 1210

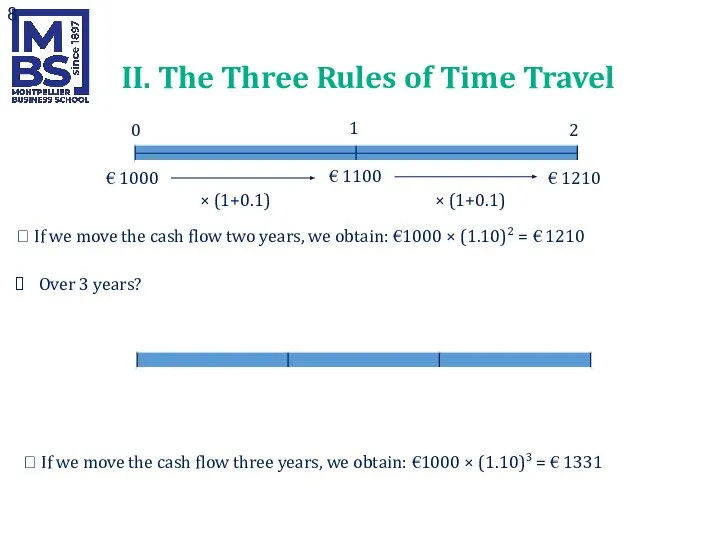

- 8. 0 1 2 € 1000 € 1100 € 1210 × (1+0.1) × (1+0.1) ? If we

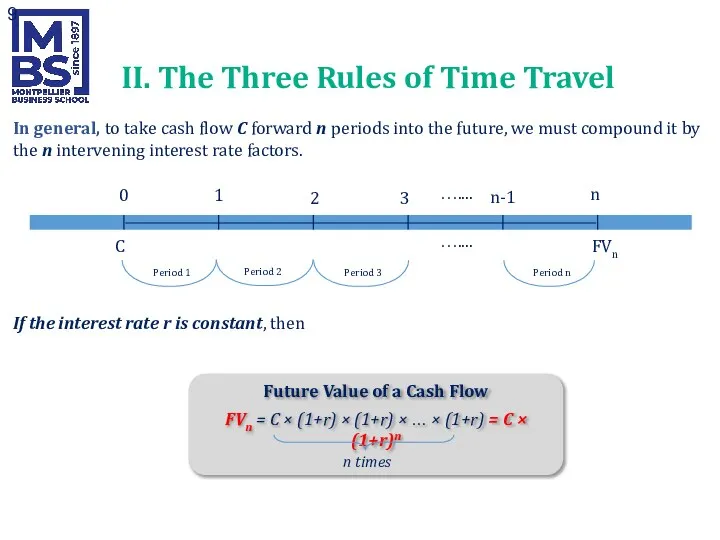

- 9. In general, to take cash flow C forward n periods into the future, we must compound

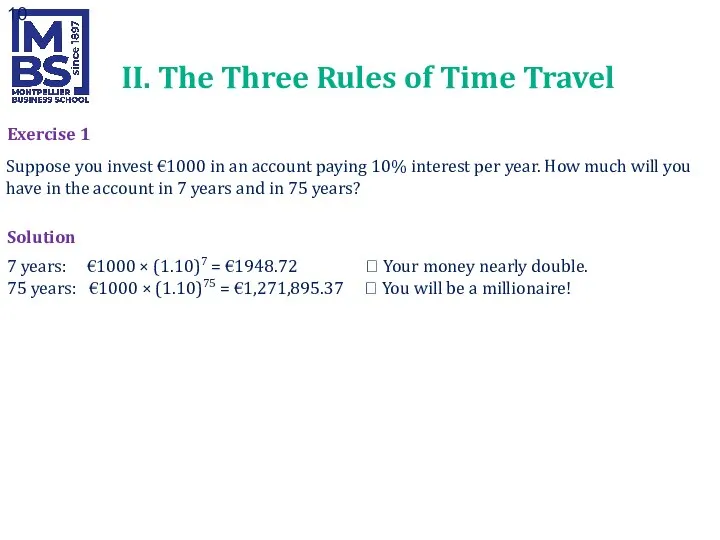

- 10. II. The Three Rules of Time Travel Exercise 1 Suppose you invest €1000 in an account

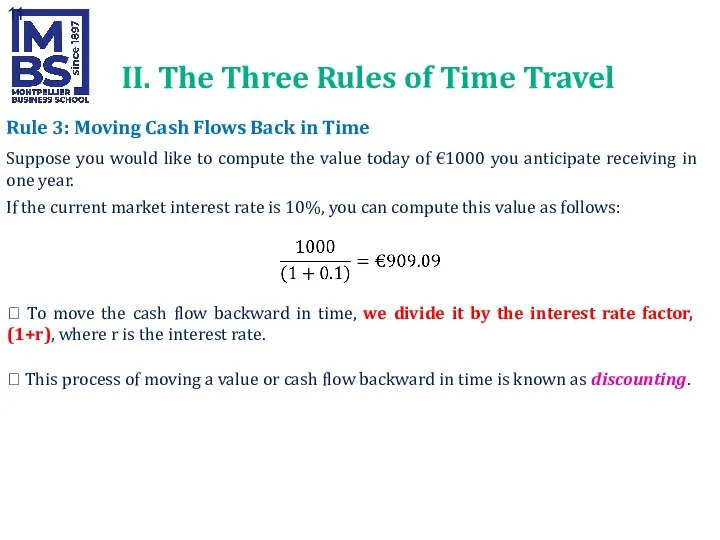

- 11. Rule 3: Moving Cash Flows Back in Time Suppose you would like to compute the value

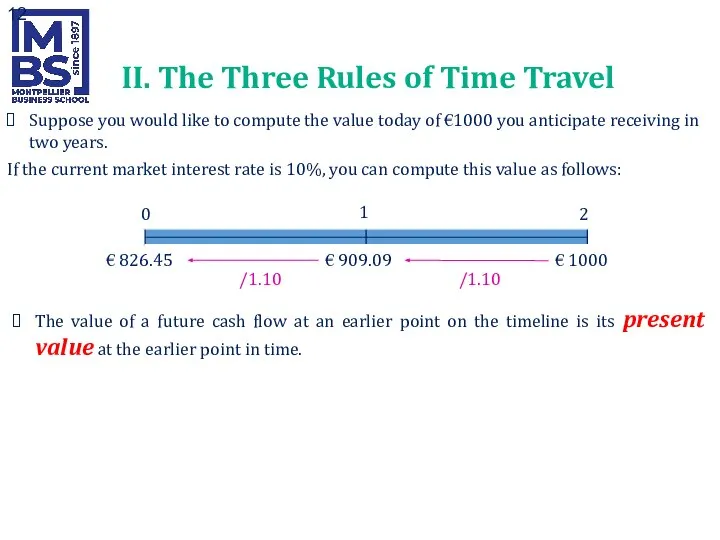

- 12. 0 1 2 € 826.45 € 909.09 € 1000 /1.10 /1.10 II. The Three Rules of

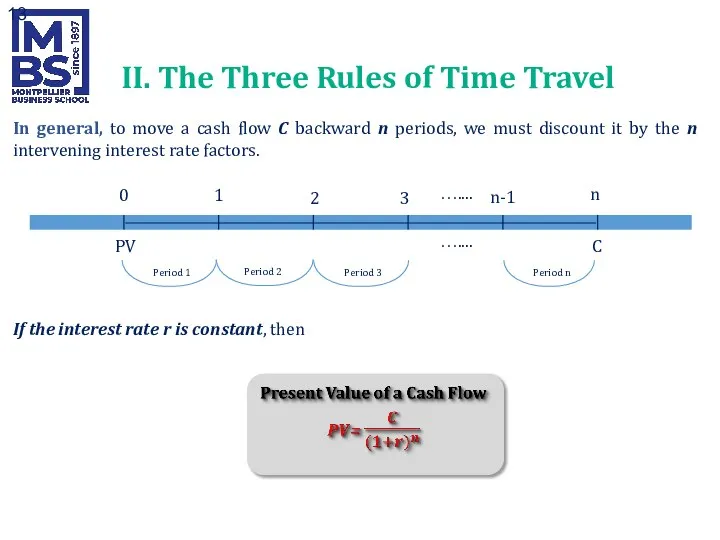

- 13. In general, to move a cash flow C backward n periods, we must discount it by

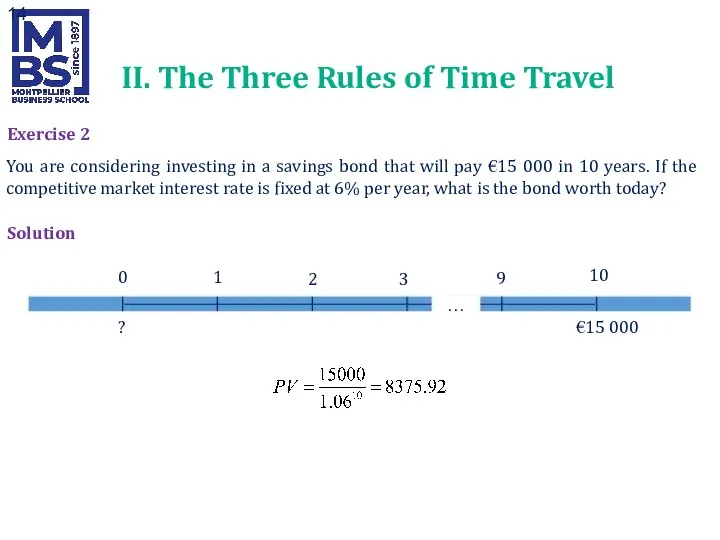

- 14. Exercise 2 You are considering investing in a savings bond that will pay €15 000 in

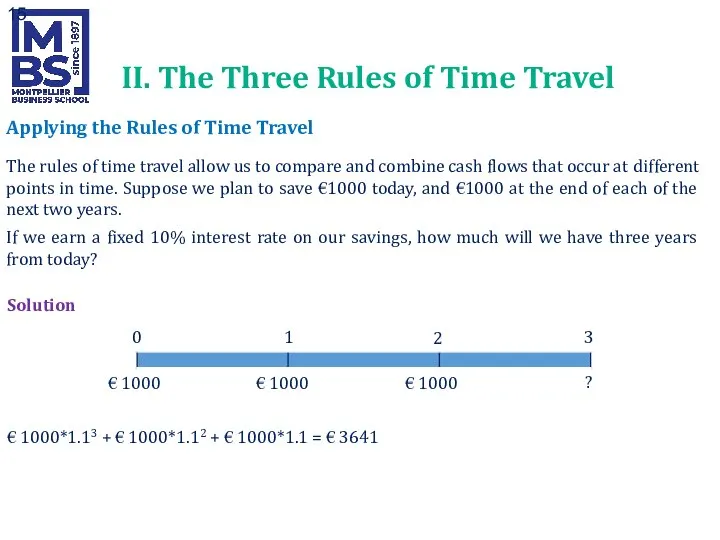

- 15. Applying the Rules of Time Travel The rules of time travel allow us to compare and

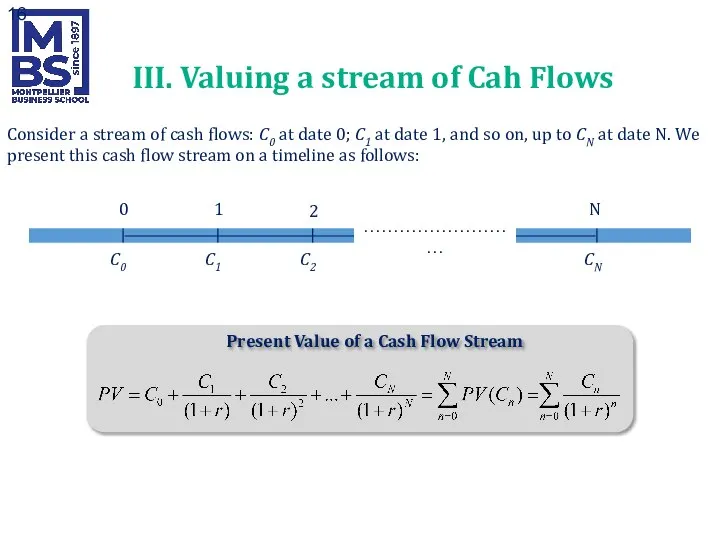

- 16. III. Valuing a stream of Cah Flows Consider a stream of cash flows: C0 at date

- 18. Скачать презентацию

Слайд 3A project (= an investment) that will generate one cash flow in

A project (= an investment) that will generate one cash flow in

Слайд 4I. The Idea of TVM

How can I obtain the value today (the

I. The Idea of TVM

How can I obtain the value today (the

Слайд 5II. The Three Rules of Time Travel

Financial decisions ? Comparing or combining

II. The Three Rules of Time Travel

Financial decisions ? Comparing or combining

Слайд 6II. The Three Rules of Time Travel

Rule 2: Moving Cash Flows Forward

II. The Three Rules of Time Travel

Rule 2: Moving Cash Flows Forward

Слайд 7II. The Three Rules of Time Travel

0

1

2

€ 1000

€ 1100

€ 1210

× (1+0.1)

× (1+0.1)

How

II. The Three Rules of Time Travel

0

1

2

€ 1000

€ 1100

€ 1210

× (1+0.1)

× (1+0.1)

How

Слайд 80

1

2

€ 1000

€ 1100

€ 1210

× (1+0.1)

× (1+0.1)

? If we move the cash flow

0

1

2

€ 1000

€ 1100

€ 1210

× (1+0.1)

× (1+0.1)

? If we move the cash flow

Слайд 9In general, to take cash flow C forward n periods into the

In general, to take cash flow C forward n periods into the

Слайд 10II. The Three Rules of Time Travel

Exercise 1

Suppose you invest €1000 in

II. The Three Rules of Time Travel

Exercise 1

Suppose you invest €1000 in

Слайд 11Rule 3: Moving Cash Flows Back in Time

Suppose you would like to

Rule 3: Moving Cash Flows Back in Time

Suppose you would like to

Слайд 120

1

2

€ 826.45

€ 909.09

€ 1000

/1.10

/1.10

II. The Three Rules of Time Travel

Suppose you would

0

1

2

€ 826.45

€ 909.09

€ 1000

/1.10

/1.10

II. The Three Rules of Time Travel

Suppose you would

Слайд 13In general, to move a cash flow C backward n periods, we

In general, to move a cash flow C backward n periods, we

Слайд 14Exercise 2

You are considering investing in a savings bond that will pay

Exercise 2

You are considering investing in a savings bond that will pay

Слайд 15Applying the Rules of Time Travel

The rules of time travel allow us

Applying the Rules of Time Travel

The rules of time travel allow us

Слайд 16III. Valuing a stream of Cah Flows

Consider a stream of cash flows:

III. Valuing a stream of Cah Flows

Consider a stream of cash flows:

Структура живой воды 4 класс

Структура живой воды 4 класс Мировой туризм.

Мировой туризм. Система работы по развитию профессиональной компетентности педагога дополнительного образования в ЦДТ Вахитовского района г. Ка

Система работы по развитию профессиональной компетентности педагога дополнительного образования в ЦДТ Вахитовского района г. Ка Прожектор. Применение и устройство

Прожектор. Применение и устройство Семь Чудес Света

Семь Чудес Света Leisure Activities

Leisure Activities Двугранный угол. Угол между плоскостями

Двугранный угол. Угол между плоскостями Презентація

Презентація "Типы телосложений, осанка, силуэт"

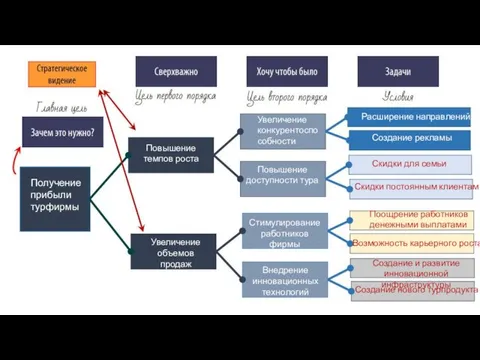

"Типы телосложений, осанка, силуэт" Стратегическое видение. Получение прибыли турфирмы

Стратегическое видение. Получение прибыли турфирмы Инновационные процессы в образовании. (Модуль 2. Политико-экономический контекст инноваций в XX- XX веках)

Инновационные процессы в образовании. (Модуль 2. Политико-экономический контекст инноваций в XX- XX веках) КОМПОЗИЦИЯ

КОМПОЗИЦИЯ Национальное агентство развития квалификаций

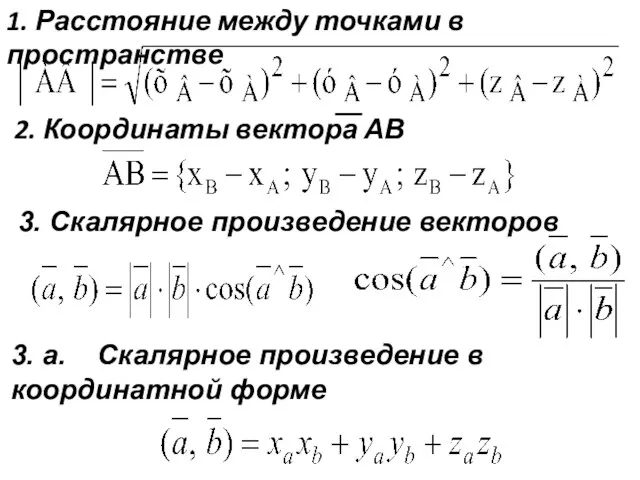

Национальное агентство развития квалификаций Расстояние между точками в пространстве

Расстояние между точками в пространстве  Мультимедийная презентация:«Интеграция предметов гуманитарно-эстетического цикла на уроках литературы»(из опыта работы)2008 г

Мультимедийная презентация:«Интеграция предметов гуманитарно-эстетического цикла на уроках литературы»(из опыта работы)2008 г Стратегическое планирование

Стратегическое планирование МОУ «СОШ с.Прималкинского»Прохладненского района КБРПровела учитель: Мешкова Н.В.

МОУ «СОШ с.Прималкинского»Прохладненского района КБРПровела учитель: Мешкова Н.В. Технологическая карта

Технологическая карта "Он нас от смерти защитил"

"Он нас от смерти защитил" Подросток и закон

Подросток и закон Витамины. Их виды и значение для человека.

Витамины. Их виды и значение для человека. Доступ к среде передачи

Доступ к среде передачи Зубная паста с углём

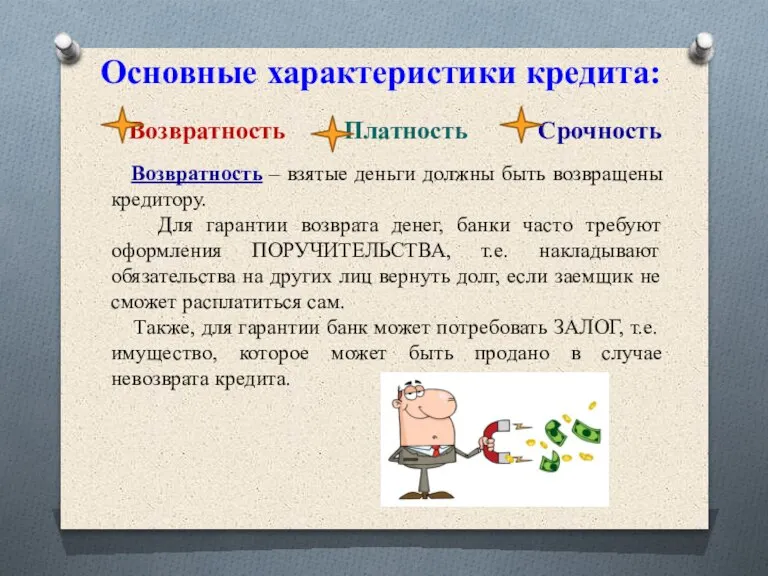

Зубная паста с углём Характеристики кредита

Характеристики кредита О состоянии детского дорожно-транспортного травматизма в Удмуртской Республике по итогам 2010 года.

О состоянии детского дорожно-транспортного травматизма в Удмуртской Республике по итогам 2010 года. Грабеж. Задания для выполнения

Грабеж. Задания для выполнения Транспорт будущего

Транспорт будущего Жидкие дисперсии полимеров Salcare

Жидкие дисперсии полимеров Salcare