- The Design of the tax system

Содержание

- 2. “In this world nothing is certain but death and taxes.” . . . Benjamin Franklin Taxes

- 3. “In this world nothing is certain but death and taxes.” . . . Benjamin Franklin 1789

- 4. Figure 1 Government Revenue as a Percentage of GDP Copyright © 2004 South-Western 0 5 10

- 5. Table 1 Central Government Tax Revenue as a Percent of GDP Copyright©2004 South-Western

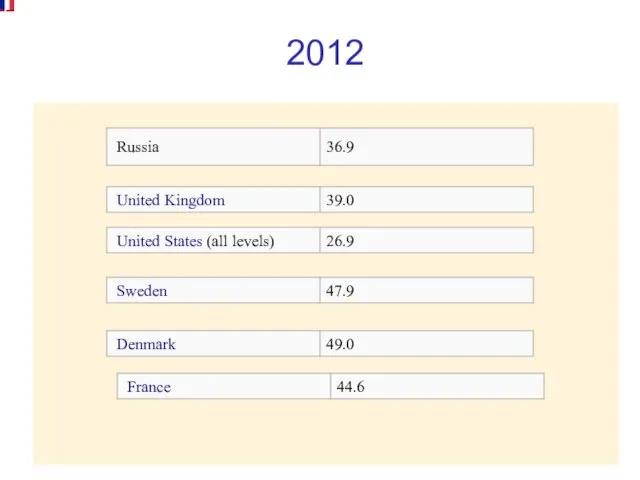

- 6. 2012

- 7. The Federal Government The U.S. federal government collects about two-thirds of the taxes in our economy.

- 8. The Federal Government The largest source of revenue for the federal government is the individual income

- 9. The Federal Government Individual Income Taxes The marginal tax rate is the tax rate applied to

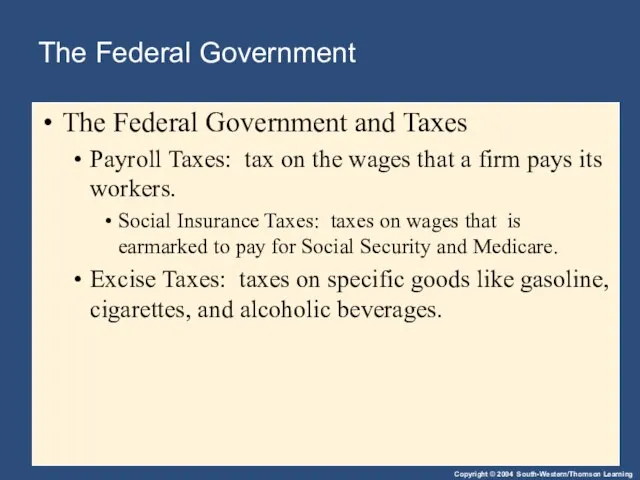

- 10. The Federal Government The Federal Government and Taxes Payroll Taxes: tax on the wages that a

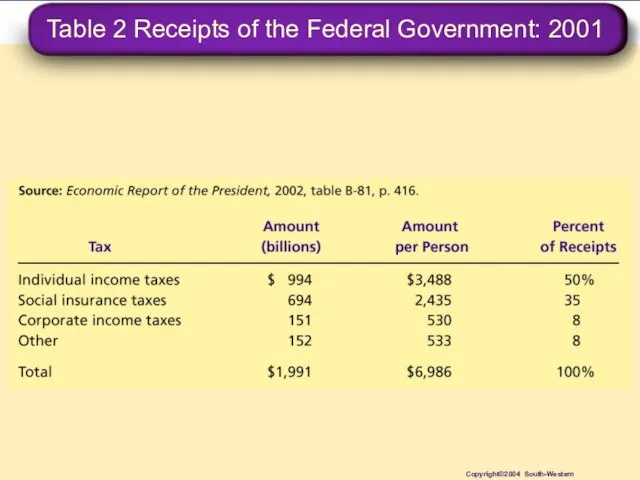

- 11. Table 2 Receipts of the Federal Government: 2001 Copyright©2004 South-Western

- 12. Receipts of the Federal Government...

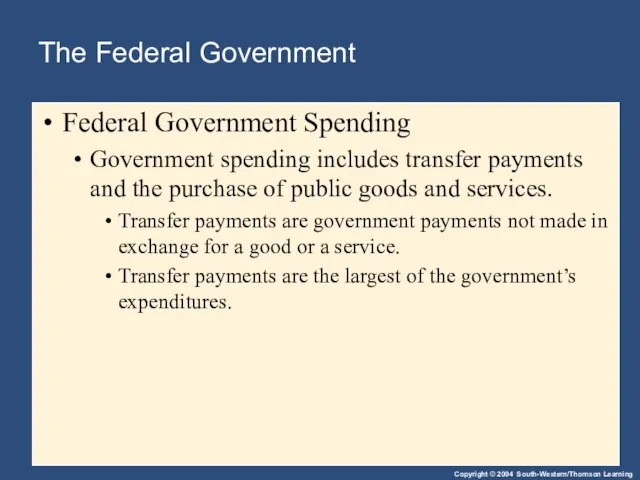

- 13. The Federal Government Federal Government Spending Government spending includes transfer payments and the purchase of public

- 14. The Federal Government Federal Government Spending Expense Category: Social Security National Defense Income Security Net Interest

- 15. The Federal Government Budget Surplus A budget surplus is an excess of government receipts over government

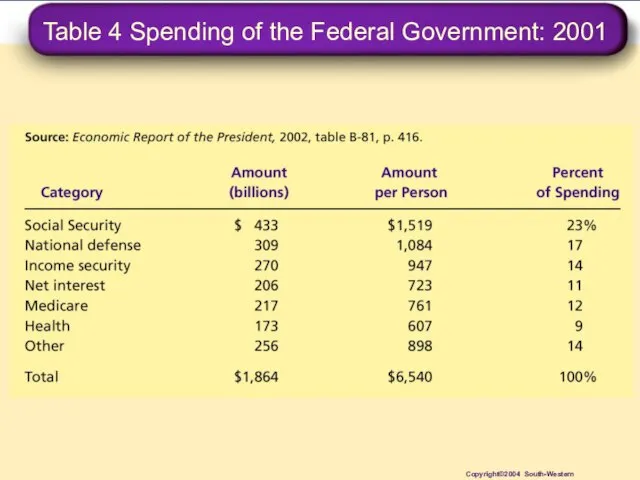

- 16. Table 4 Spending of the Federal Government: 2001 Copyright©2004 South-Western

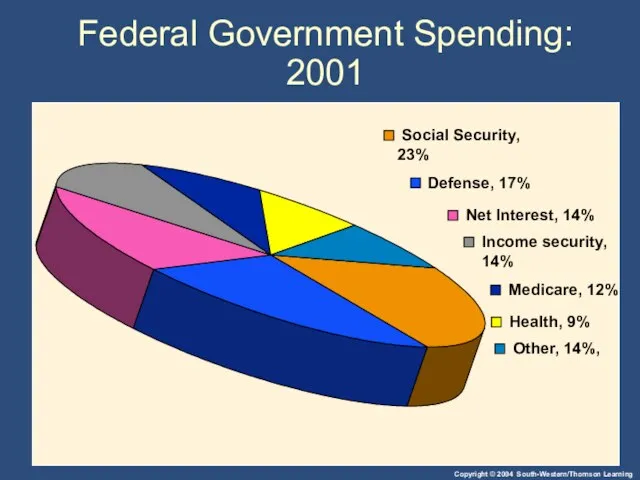

- 17. Federal Government Spending: 2001

- 18. The Federal Government Financial Conditions of the Federal Budget A budget deficit occurs when there is

- 19. State and Local Governments State and local governments collect about 40 percent of taxes paid.

- 20. State and Local Government Receipts Sales Taxes Property Taxes Individual Income Taxes Corporate Income Taxes Federal

- 21. Table 5 Receipts of State and Local Governments: 1999 Copyright©2004 South-Western

- 22. State and Local Government Spending Education Public Welfare Highways Other

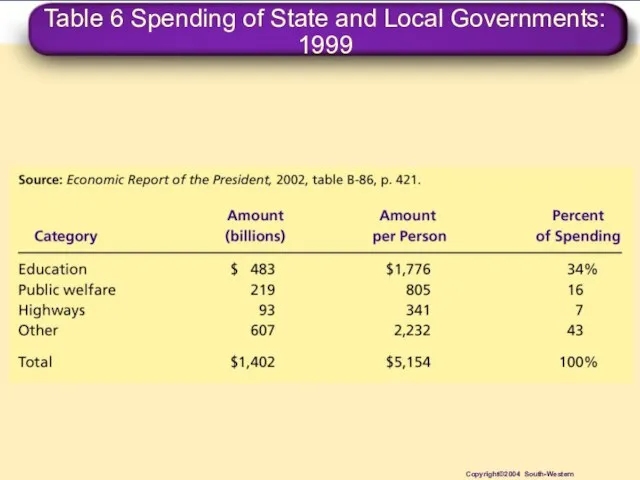

- 23. Table 6 Spending of State and Local Governments: 1999 Copyright©2004 South-Western

- 24. TAXES AND EFFICIENCY Policymakers have two objectives in designing a tax system... Efficiency Equity

- 25. TAXES AND EFFICIENCY One tax system is more efficient than another if it raises the same

- 26. TAXES AND EFFICIENCY The Cost of Taxes to Taxpayers The tax payment itself Deadweight losses Administrative

- 27. Deadweight Losses Because taxes distort incentives, they entail deadweight losses. The deadweight loss of a tax

- 28. Administrative Burdens Complying with tax laws creates additional deadweight losses. Taxpayers lose additional time and money

- 29. Marginal Tax Rates versus Average Tax Rates The average tax rate is total taxes paid divided

- 30. Lump-Sum Taxes A lump-sum tax is a tax that is the same amount for every person,

- 31. TAXES AND EQUITY How should the burden of taxes be divided among the population? How do

- 33. TAXES AND EQUITY Principles of Taxation Benefits principle Ability-to-pay principle $

- 34. Benefits Principle The benefits principle is the idea that people should pay taxes based on the

- 35. Ability-to-Pay Principle The ability-to-pay principle is the idea that taxes should be levied on a person

- 36. Ability-to-Pay Principle Vertical equity is the idea that taxpayers with a greater ability to pay taxes

- 37. Ability-to-Pay Principle Vertical Equity and Alternative Tax Systems A proportional tax is one for which high-income

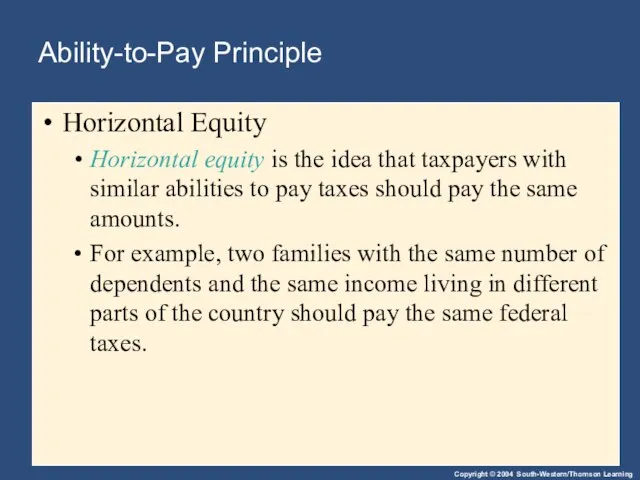

- 38. Ability-to-Pay Principle Horizontal Equity Horizontal equity is the idea that taxpayers with similar abilities to pay

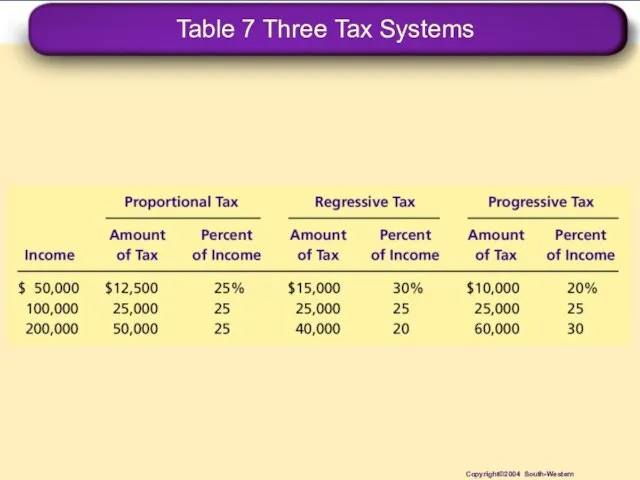

- 39. Table 7 Three Tax Systems Copyright©2004 South-Western

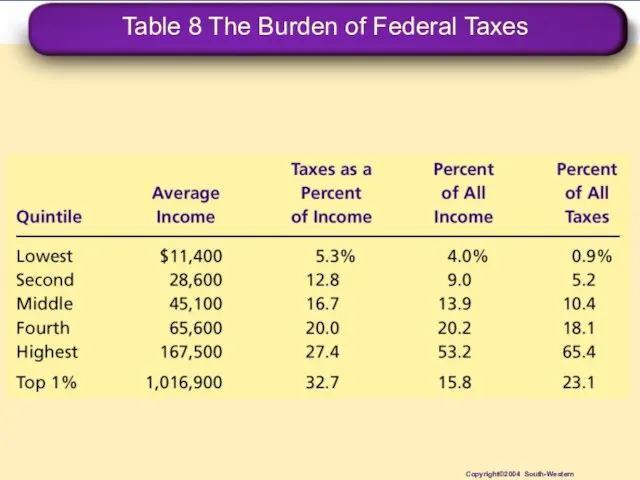

- 40. Table 8 The Burden of Federal Taxes Copyright©2004 South-Western

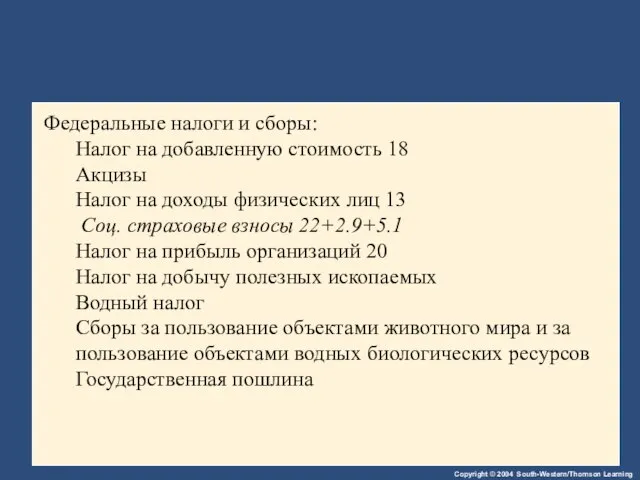

- 42. Федеральные налоги и сборы: Налог на добавленную стоимость 18 Акцизы Налог на доходы физических лиц 13

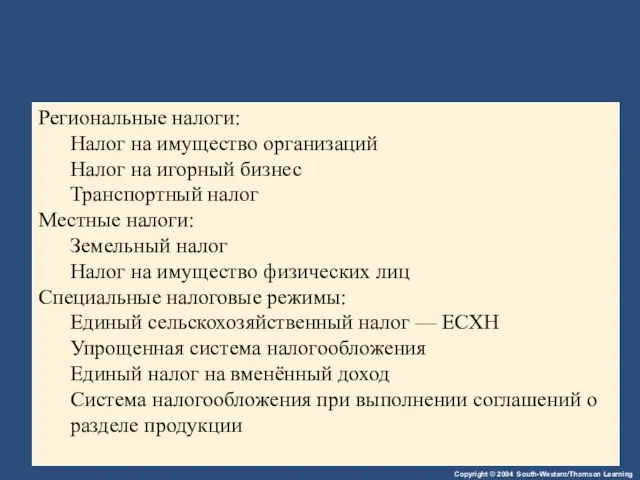

- 43. Региональные налоги: Налог на имущество организаций Налог на игорный бизнес Транспортный налог Местные налоги: Земельный налог

- 44. CASE STUDY: Horizontal Equity and the Marriage Tax Marriage affects the tax liability of a couple

- 45. Tax Incidence and Tax Equity The difficulty in formulating tax policy is balancing the often conflicting

- 46. Tax Incidence and Tax Equity Flypaper Theory of Tax Incidence According to the flypaper theory, the

- 47. Summary The U.S. government raises revenue using various taxes. Income taxes and payroll taxes raise the

- 48. Summary Equity and efficiency are the two most important goals of the tax system. The efficiency

- 49. Summary According to the benefits principle, it is fair for people to pay taxes based on

- 51. Скачать презентацию

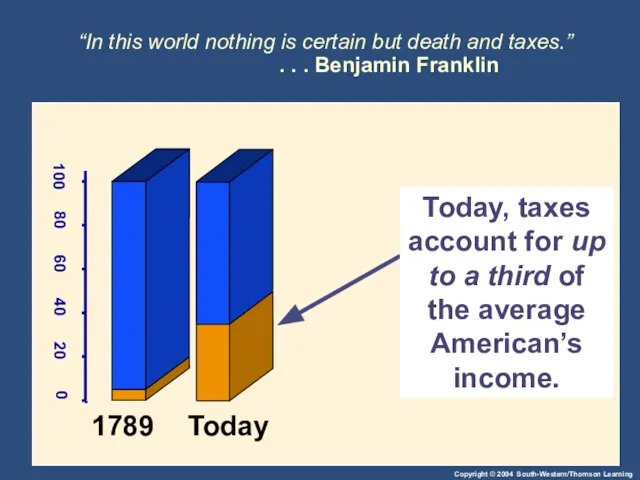

Слайд 3“In this world nothing is certain but death and taxes.”

. .

“In this world nothing is certain but death and taxes.” . .

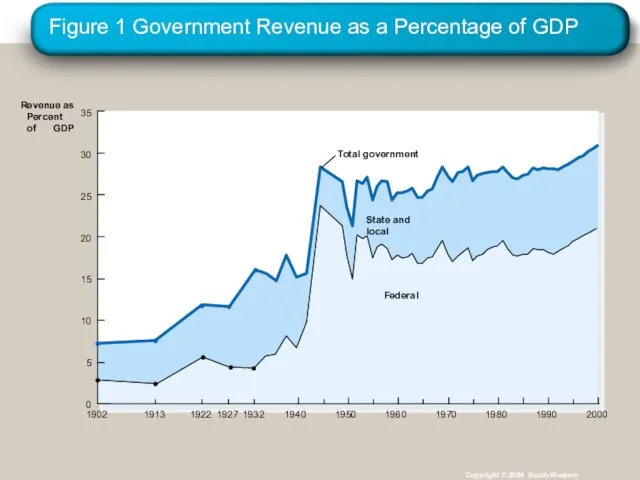

Слайд 4Figure 1 Government Revenue as a Percentage of GDP

Copyright © 2004 South-Western

0

5

10

15

20

25

30

35

Revenue

Figure 1 Government Revenue as a Percentage of GDP

Copyright © 2004 South-Western

0

5

10

15

20

25

30

35

Revenue

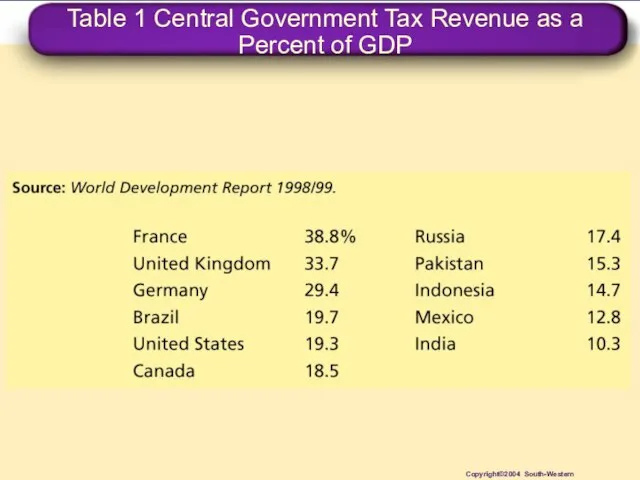

Слайд 5Table 1 Central Government Tax Revenue as a Percent of GDP

Copyright©2004 South-Western

Table 1 Central Government Tax Revenue as a Percent of GDP

Copyright©2004 South-Western

Слайд 62012

2012

Слайд 7The Federal Government

The U.S. federal government collects about two-thirds of the

The Federal Government

The U.S. federal government collects about two-thirds of the

Слайд 8The Federal Government

The largest source of revenue for the federal government

The Federal Government

The largest source of revenue for the federal government

Слайд 9The Federal Government

Individual Income Taxes

The marginal tax rate is the tax

The Federal Government

Individual Income Taxes

The marginal tax rate is the tax

Слайд 10The Federal Government

The Federal Government and Taxes

Payroll Taxes: tax on

The Federal Government

The Federal Government and Taxes

Payroll Taxes: tax on

Слайд 11Table 2 Receipts of the Federal Government: 2001

Copyright©2004 South-Western

Table 2 Receipts of the Federal Government: 2001

Copyright©2004 South-Western

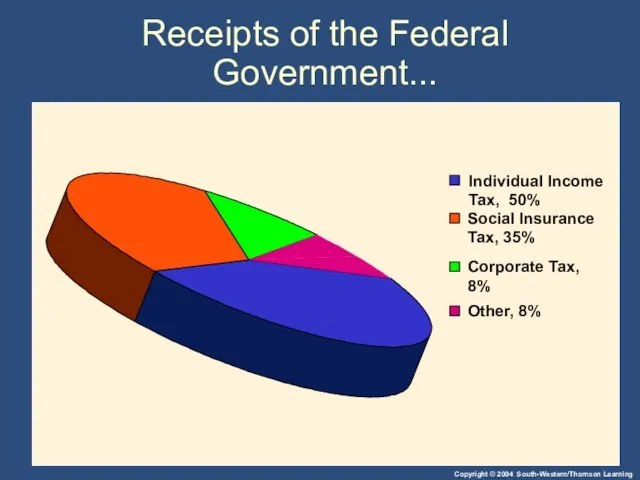

Слайд 12Receipts of the Federal Government...

Receipts of the Federal Government...

Слайд 13The Federal Government

Federal Government Spending

Government spending includes transfer payments and the

The Federal Government

Federal Government Spending

Government spending includes transfer payments and the

Слайд 14The Federal Government

Federal Government Spending

Expense Category:

Social Security

National Defense

Income Security

Net Interest

Medicare

Health

Other

The Federal Government

Federal Government Spending

Expense Category:

Social Security

National Defense

Income Security

Net Interest

Medicare

Health

Other

Слайд 15The Federal Government

Budget Surplus

A budget surplus is an excess of government receipts

The Federal Government

Budget Surplus

A budget surplus is an excess of government receipts

Слайд 16Table 4 Spending of the Federal Government: 2001

Copyright©2004 South-Western

Table 4 Spending of the Federal Government: 2001

Copyright©2004 South-Western

Слайд 17Federal Government Spending: 2001

Federal Government Spending: 2001

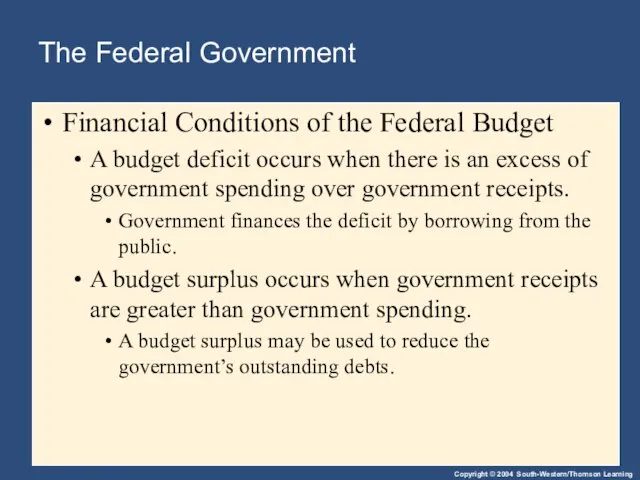

Слайд 18The Federal Government

Financial Conditions of the Federal Budget

A budget deficit occurs when

The Federal Government

Financial Conditions of the Federal Budget

A budget deficit occurs when

Слайд 19State and Local Governments

State and local governments collect about 40 percent of

State and Local Governments

State and local governments collect about 40 percent of

Слайд 20State and Local Government

Receipts

Sales Taxes

Property Taxes

Individual Income Taxes

Corporate Income Taxes

Federal government

Other

Taxes

$

State and Local Government

Receipts

Sales Taxes

Property Taxes

Individual Income Taxes

Corporate Income Taxes

Federal government

Other

Taxes

$

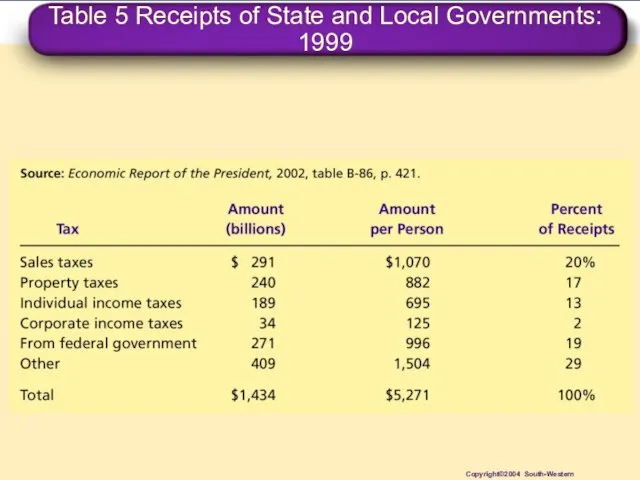

Слайд 21Table 5 Receipts of State and Local Governments: 1999

Copyright©2004 South-Western

Table 5 Receipts of State and Local Governments: 1999

Copyright©2004 South-Western

Слайд 22State and Local Government

Spending

Education

Public Welfare

Highways

Other

State and Local Government

Spending

Education

Public Welfare

Highways

Other

Слайд 23Table 6 Spending of State and Local Governments: 1999

Copyright©2004 South-Western

Table 6 Spending of State and Local Governments: 1999

Copyright©2004 South-Western

Слайд 24TAXES AND EFFICIENCY

Policymakers have two objectives in designing a tax system...

Efficiency

Equity

TAXES AND EFFICIENCY

Policymakers have two objectives in designing a tax system...

Efficiency

Equity

Слайд 25TAXES AND EFFICIENCY

One tax system is more efficient than another if it

TAXES AND EFFICIENCY

One tax system is more efficient than another if it

Слайд 26TAXES AND EFFICIENCY

The Cost of Taxes to Taxpayers

The tax payment itself

Deadweight

TAXES AND EFFICIENCY

The Cost of Taxes to Taxpayers

The tax payment itself

Deadweight

Слайд 27Deadweight Losses

Because taxes distort incentives, they entail deadweight losses.

The deadweight loss of

Deadweight Losses

Because taxes distort incentives, they entail deadweight losses.

The deadweight loss of

Слайд 28Administrative Burdens

Complying with tax laws creates additional deadweight losses.

Taxpayers lose additional

Administrative Burdens

Complying with tax laws creates additional deadweight losses.

Taxpayers lose additional

Слайд 29Marginal Tax Rates versus Average Tax Rates

The average tax rate is total

Marginal Tax Rates versus Average Tax Rates

The average tax rate is total

Слайд 30Lump-Sum Taxes

A lump-sum tax is a tax that is the same amount

Lump-Sum Taxes

A lump-sum tax is a tax that is the same amount

Слайд 31TAXES AND EQUITY

How should the burden of taxes be divided among the

TAXES AND EQUITY

How should the burden of taxes be divided among the

Слайд 33TAXES AND EQUITY

Principles of Taxation

Benefits principle

Ability-to-pay principle

$

TAXES AND EQUITY

Principles of Taxation

Benefits principle

Ability-to-pay principle

$

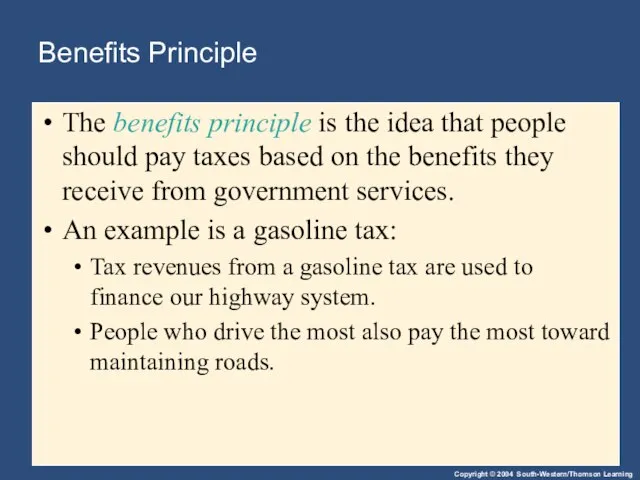

Слайд 34Benefits Principle

The benefits principle is the idea that people should pay taxes

Benefits Principle

The benefits principle is the idea that people should pay taxes

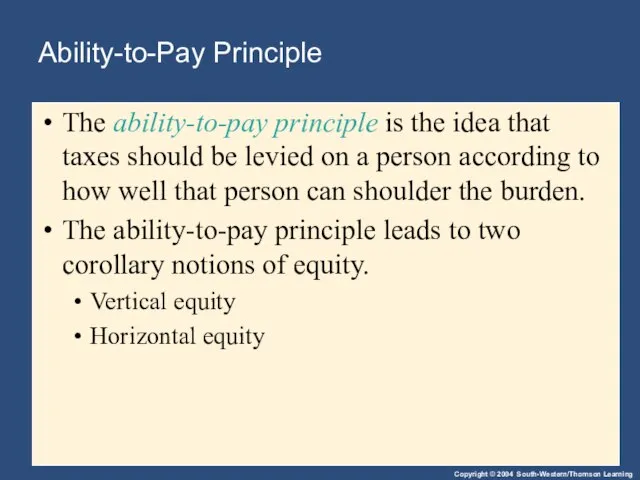

Слайд 35Ability-to-Pay Principle

The ability-to-pay principle is the idea that taxes should be levied

Ability-to-Pay Principle

The ability-to-pay principle is the idea that taxes should be levied

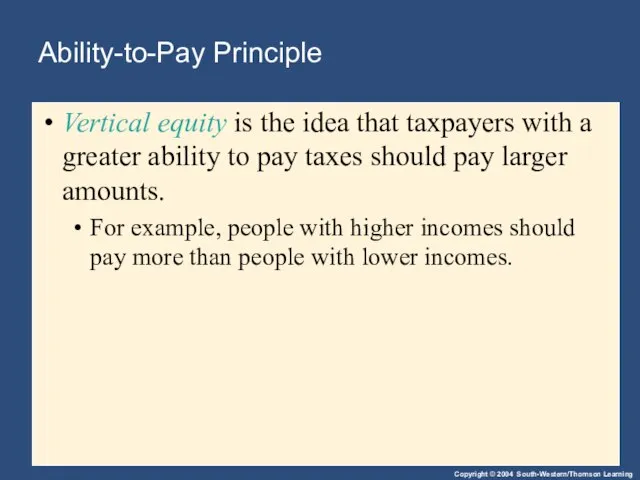

Слайд 36Ability-to-Pay Principle

Vertical equity is the idea that taxpayers with a greater ability

Ability-to-Pay Principle

Vertical equity is the idea that taxpayers with a greater ability

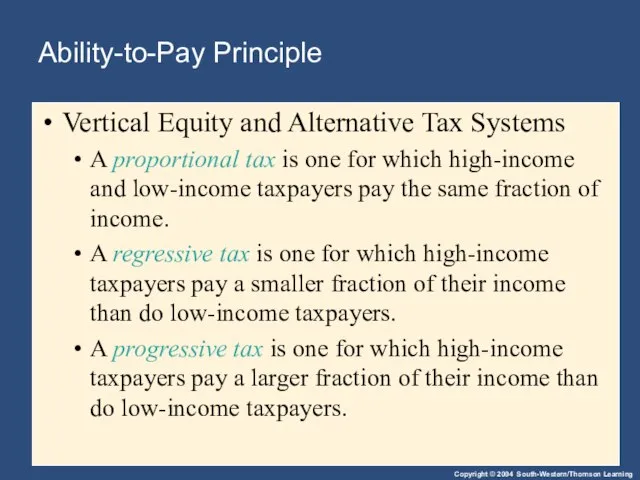

Слайд 37Ability-to-Pay Principle

Vertical Equity and Alternative Tax Systems

A proportional tax is one

Ability-to-Pay Principle

Vertical Equity and Alternative Tax Systems

A proportional tax is one

Слайд 38Ability-to-Pay Principle

Horizontal Equity

Horizontal equity is the idea that taxpayers with similar

Ability-to-Pay Principle

Horizontal Equity

Horizontal equity is the idea that taxpayers with similar

Слайд 39Table 7 Three Tax Systems

Copyright©2004 South-Western

Table 7 Three Tax Systems

Copyright©2004 South-Western

Слайд 40Table 8 The Burden of Federal Taxes

Copyright©2004 South-Western

Table 8 The Burden of Federal Taxes

Copyright©2004 South-Western

Слайд 42Федеральные налоги и сборы:

Налог на добавленную стоимость 18

Акцизы

Налог на доходы физических лиц

Федеральные налоги и сборы:

Налог на добавленную стоимость 18

Акцизы

Налог на доходы физических лиц

Слайд 43Региональные налоги:

Налог на имущество организаций

Налог на игорный бизнес

Транспортный налог

Местные налоги:

Земельный налог

Налог на

Региональные налоги:

Налог на имущество организаций

Налог на игорный бизнес

Транспортный налог

Местные налоги:

Земельный налог

Налог на

Слайд 44CASE STUDY: Horizontal Equity and the Marriage Tax

Marriage affects the tax liability

CASE STUDY: Horizontal Equity and the Marriage Tax

Marriage affects the tax liability

Слайд 45Tax Incidence and Tax Equity

The difficulty in formulating tax policy is balancing

Tax Incidence and Tax Equity

The difficulty in formulating tax policy is balancing

Слайд 46Tax Incidence and Tax Equity

Flypaper Theory of Tax Incidence

According to the

Tax Incidence and Tax Equity

Flypaper Theory of Tax Incidence

According to the

Слайд 47Summary

The U.S. government raises revenue using various taxes.

Income taxes and payroll taxes

Summary

The U.S. government raises revenue using various taxes.

Income taxes and payroll taxes

Слайд 48Summary

Equity and efficiency are the two most important goals of the tax

Summary

Equity and efficiency are the two most important goals of the tax

Слайд 49Summary

According to the benefits principle, it is fair for people to pay

Summary

According to the benefits principle, it is fair for people to pay

Презентация на тему Пожар в лесу

Презентация на тему Пожар в лесу Огорсад иль садород?

Огорсад иль садород? Числа от 1 до 10

Числа от 1 до 10 Деятельностный подход на уроках математики

Деятельностный подход на уроках математики Transformation of a Drawing

Transformation of a Drawing Староакульшетская школа

Староакульшетская школа Шахматные фигуры и начальная позиция (урок № 7)

Шахматные фигуры и начальная позиция (урок № 7) Информация, ее виды и свойства

Информация, ее виды и свойства Какую роль играет вкус,зрение,обоняние в жизнедеятельности человека

Какую роль играет вкус,зрение,обоняние в жизнедеятельности человека Лабынкырский чёрт

Лабынкырский чёрт "Основы религиозных культур и светской этики"

"Основы религиозных культур и светской этики" Презентация на тему Корненожки. Амеба обыкновенная

Презентация на тему Корненожки. Амеба обыкновенная Керамзитовый завод Козульки

Керамзитовый завод Козульки Планерка обработчиков

Планерка обработчиков 20121009_duhovnost

20121009_duhovnost Части речи 3 класс

Части речи 3 класс Стратегический менеджмент в условиях спонтанных изменений

Стратегический менеджмент в условиях спонтанных изменений Протоколы маршрутизации

Протоколы маршрутизации  Презентация на тему Многогранники и их различия

Презентация на тему Многогранники и их различия Эквадор

Эквадор Золотое правило НРАВСТВЕННОСТИ

Золотое правило НРАВСТВЕННОСТИ Липецкий государственный технический университет Кафедра прикладной механики

Липецкий государственный технический университет Кафедра прикладной механики ЗАГАДКА МЁБИУСА

ЗАГАДКА МЁБИУСА Russia is my motherland

Russia is my motherland Многообразие органических веществ

Многообразие органических веществ Классификация химических реакций (11 класс)

Классификация химических реакций (11 класс) Фредерик Уинслоу Тейлор. Ду́глас Мак-Гре́гор Теория Х

Фредерик Уинслоу Тейлор. Ду́глас Мак-Гре́гор Теория Х Педагогика лек6 -2022

Педагогика лек6 -2022