- Financial reporting system

Содержание

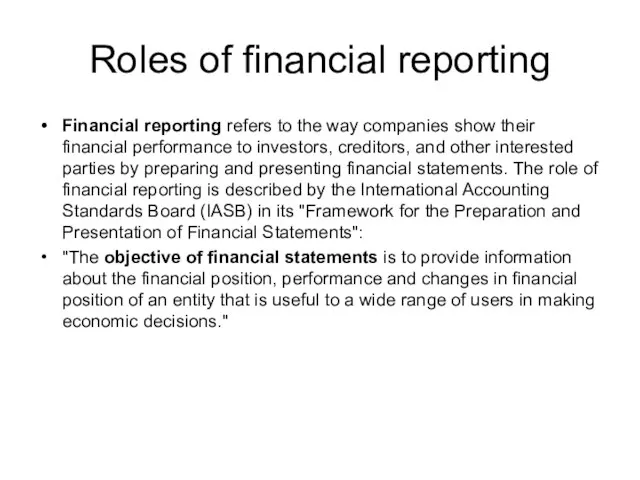

- 2. Roles of financial reporting Financial reporting refers to the way companies show their financial performance to

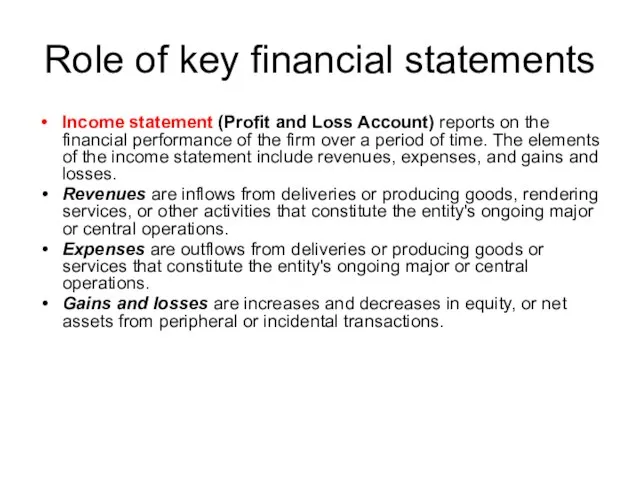

- 3. Role of key financial statements Income statement (Profit and Loss Account) reports on the financial performance

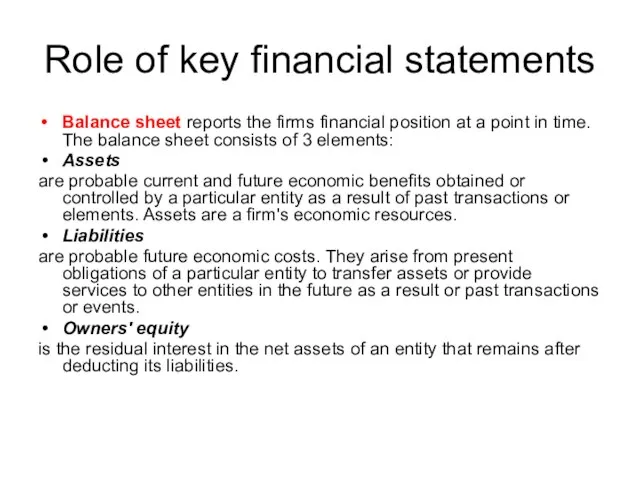

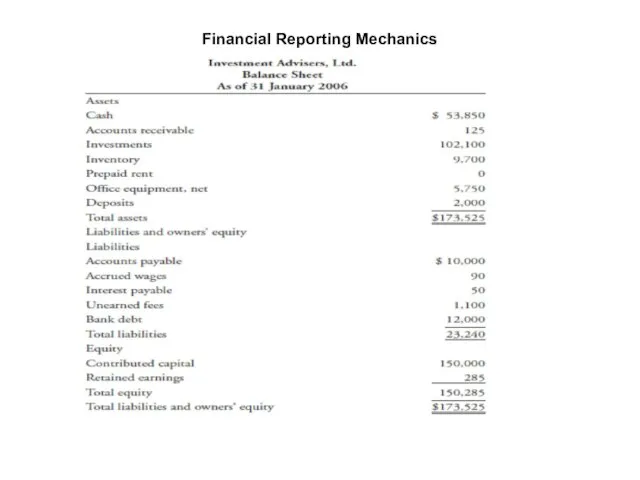

- 4. Role of key financial statements Balance sheet reports the firms financial position at a point in

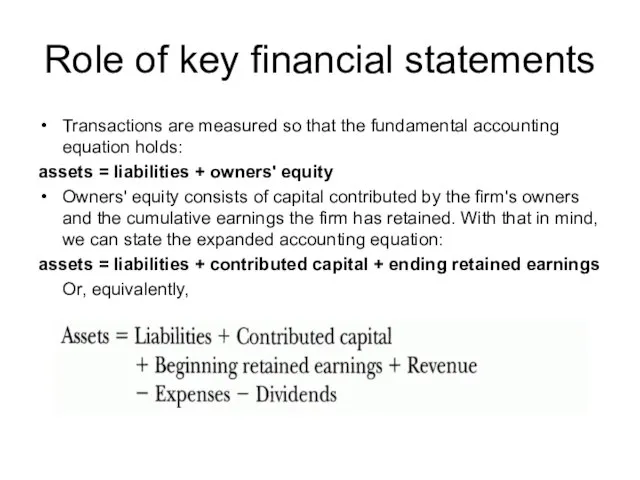

- 5. Role of key financial statements Transactions are measured so that the fundamental accounting equation holds: assets

- 6. Role of key financial statements Cash flow statement reports the company's cash receipts and payments. These

- 7. Financial statement notes and supplementary information Financial statement notes (footnotes) include disclosures that provide further details

- 8. Financial statement notes and supplementary information Supplementary schedules contain additional information. Examples of such disclosures include:

- 9. Objective of audits of financial statements Audit is an independent review of an entity's financial statements.

- 10. Objective of audits of financial statements The standard auditor's opinion contains 3 parts and states that:

- 11. Objective of audits of financial statements An unqualified opinion indicates that the auditor believes the statements

- 12. General requirements for financial statements International Accounting Standard (lAS) No.1 defines which financial statements are required

- 13. General requirements for financial statements Fair presentation as faithfully representing the effects of the entity's transactions

- 14. General requirements for financial statements PRINCIPLES OF PRESENTATION: 1)Aggregation of similar items and separation of dissimilar

- 15. Qualitative characteristics of financial statements: Financial statements should be: 1)understandable; 2)relevant; 3)reliable; 4)comparable. Understandability: Users with

- 16. Qualitative characteristics of financial statements: Reliability: Information is reliable if it reflects economic reality, is unbiased,

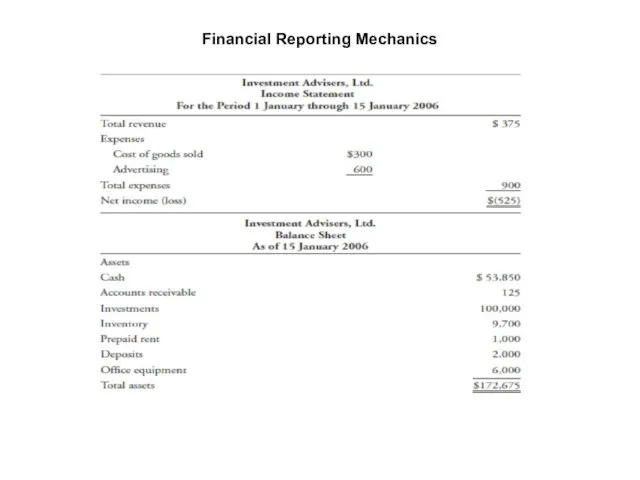

- 17. Financial Reporting Mechanics Business Activities for Investment Advisers, Ltd. 31 December 2005 File documents with regulatory

- 18. Financial Reporting Mechanics

- 19. Financial Reporting Mechanics 2 January 2006 Set up a $100,000 investment account and purchase a portfolio

- 20. Financial Reporting Mechanics

- 21. Financial Reporting Mechanics 3 January 2006 Purchase office equipment for $6,000 in cash. The equipment has

- 22. Financial Reporting Mechanics

- 23. Financial Reporting Mechanics

- 24. Financial Reporting Mechanics 10 January 2006 Purchase and receive 500 books at a cost of $20

- 25. Financial Reporting Mechanics

- 26. Financial Reporting Mechanics

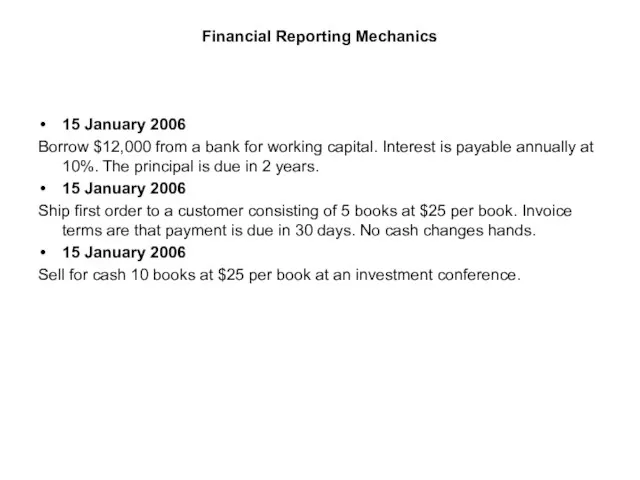

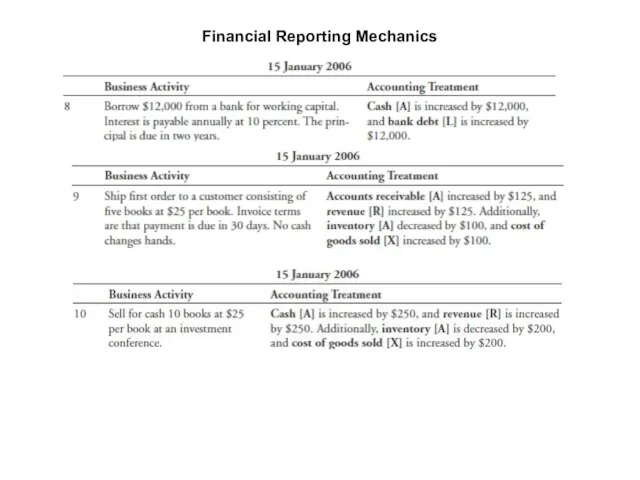

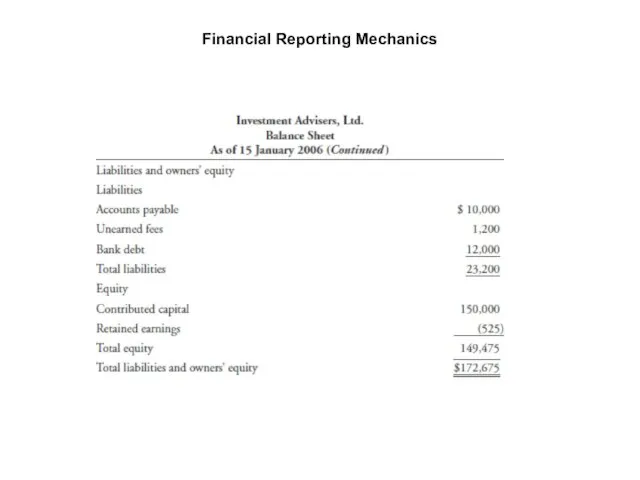

- 27. Financial Reporting Mechanics 15 January 2006 Borrow $12,000 from a bank for working capital. Interest is

- 28. Financial Reporting Mechanics

- 29. Financial Reporting Mechanics

- 30. Financial Reporting Mechanics

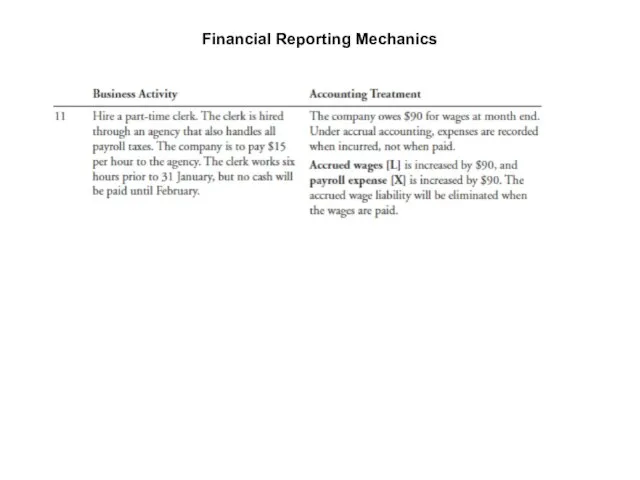

- 31. Financial Reporting Mechanics 30 January 2006 Hire a part-time clerk. The clerk is hired through an

- 32. Financial Reporting Mechanics

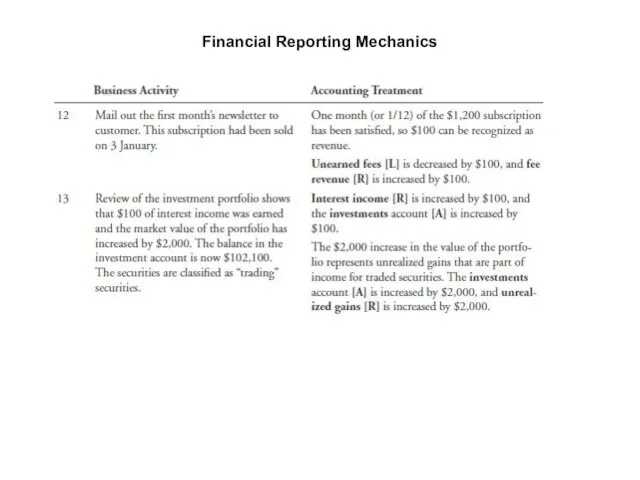

- 33. Financial Reporting Mechanics 31 January 2006 Mail out the first month’s newsletter to customer. This subscription

- 34. Financial Reporting Mechanics

- 35. Financial Reporting Mechanics

- 36. Financial Reporting Mechanics

- 37. Financial Reporting Mechanics Items 3a, 4a, and 8a reflect adjustments relating to items 3, 4, and

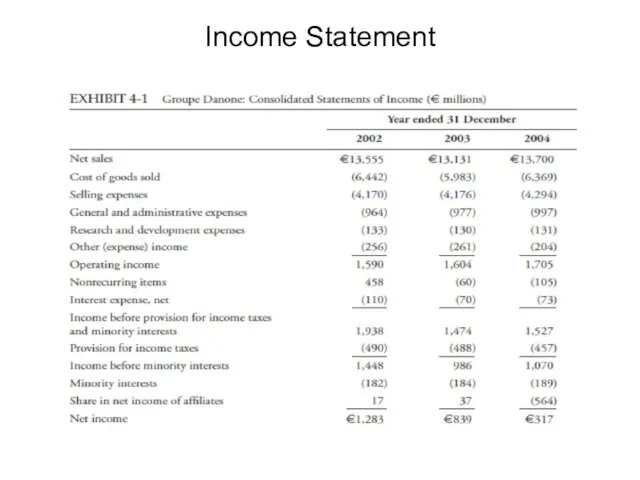

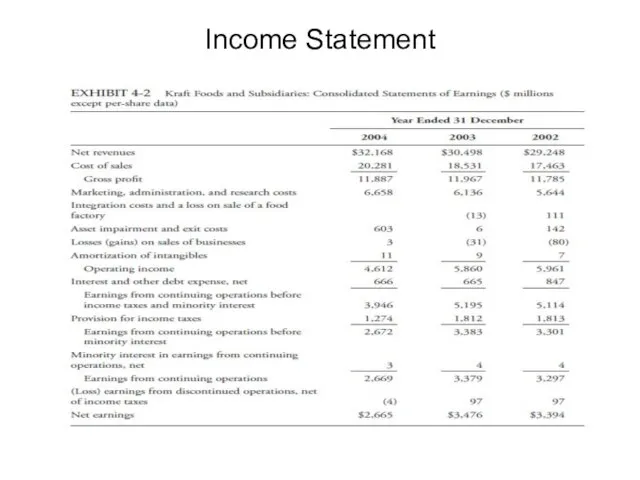

- 38. Income Statement Income statement presents information on the financial results of a company’s business activities over

- 39. Income Statement

- 40. Income Statement

- 41. Revenue Recognition A fundamental principle of accrual accounting is that revenue is recognized when it is

- 42. Revenue Recognition International Accounting Standards Board (IASB) provides that revenue for the sale of goods is

- 43. Expense Recognition Under the IASB Framework, expenses are “ decreases in economic benefits during the accounting

- 44. Expense Recognition Period costs , expenditures that less directly match the timing of revenues, are reflected

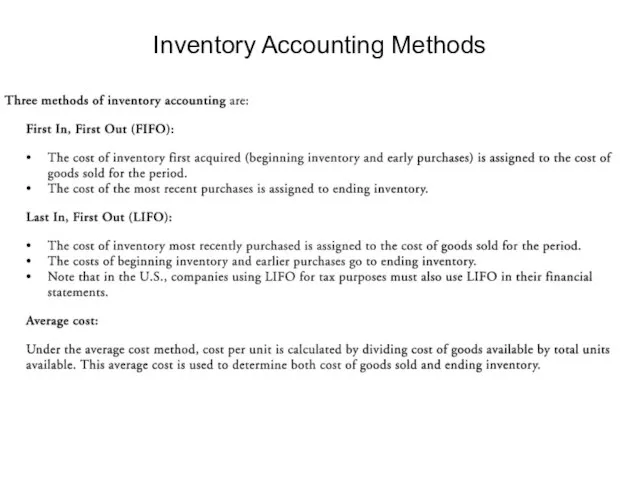

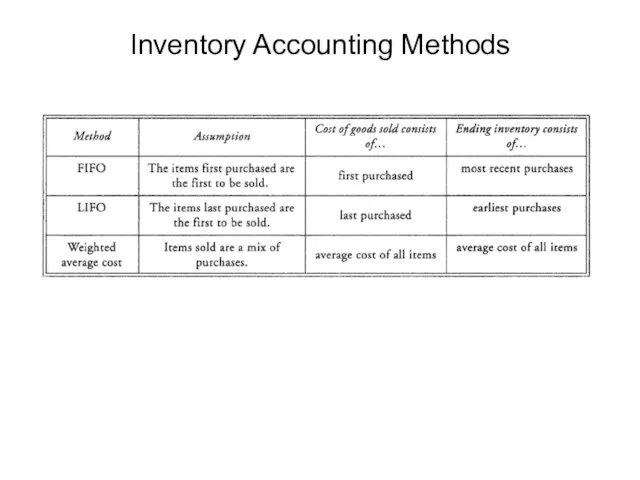

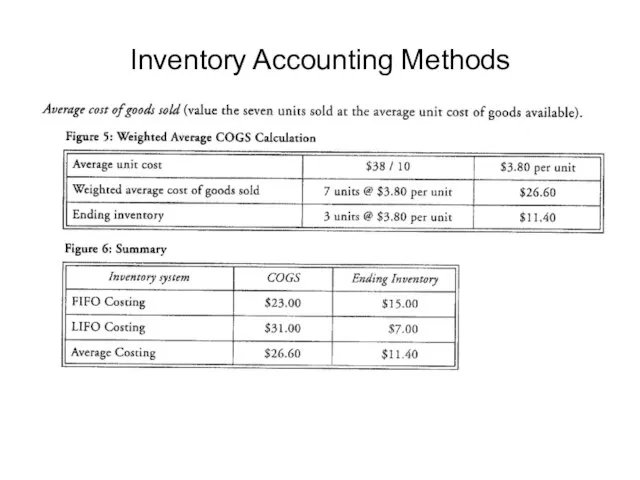

- 45. Inventory Accounting Methods

- 46. Inventory Accounting Methods

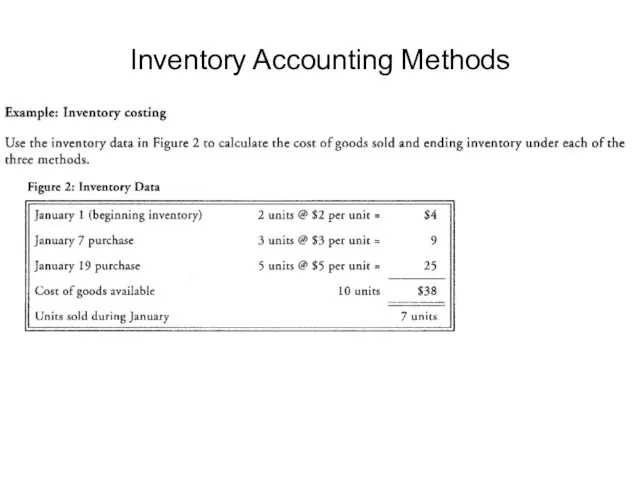

- 47. Inventory Accounting Methods

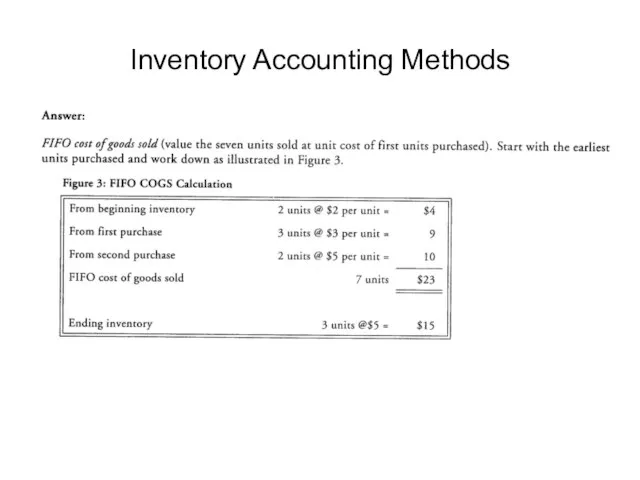

- 48. Inventory Accounting Methods

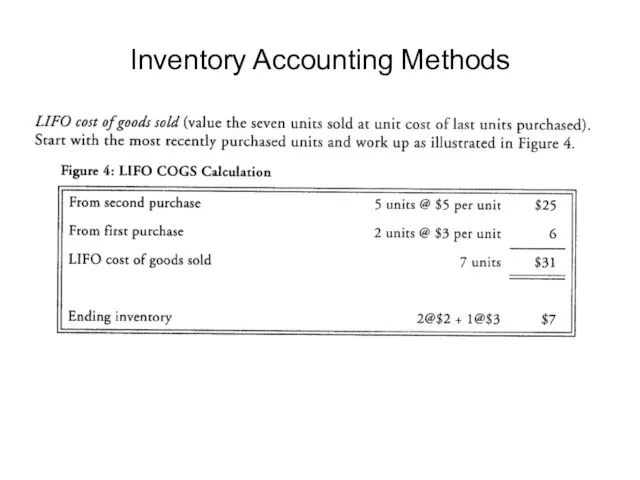

- 49. Inventory Accounting Methods

- 50. Inventory Accounting Methods

- 52. Скачать презентацию

Слайд 3Role of key financial statements

Income statement (Profit and Loss Account) reports on

Role of key financial statements

Income statement (Profit and Loss Account) reports on

Слайд 4Role of key financial statements

Balance sheet reports the firms financial position at

Role of key financial statements

Balance sheet reports the firms financial position at

Слайд 5Role of key financial statements

Transactions are measured so that the fundamental accounting

Role of key financial statements

Transactions are measured so that the fundamental accounting

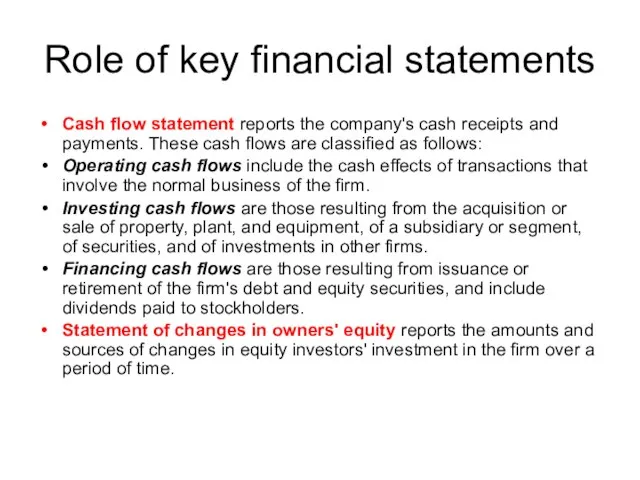

Слайд 6Role of key financial statements

Cash flow statement reports the company's cash receipts

Role of key financial statements

Cash flow statement reports the company's cash receipts

Слайд 7Financial statement notes and supplementary information

Financial statement notes (footnotes) include disclosures that

Financial statement notes and supplementary information

Financial statement notes (footnotes) include disclosures that

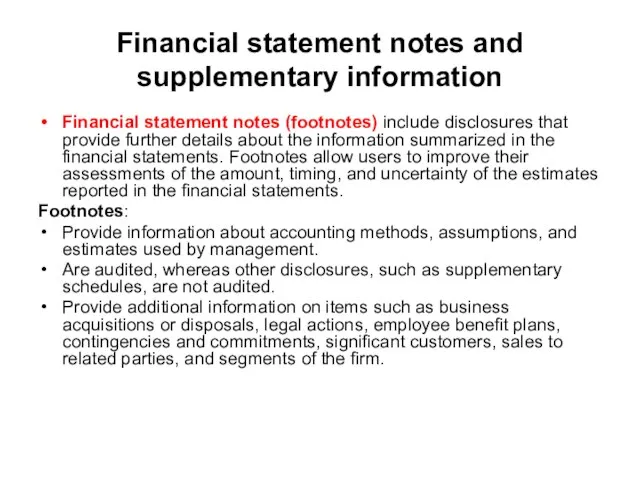

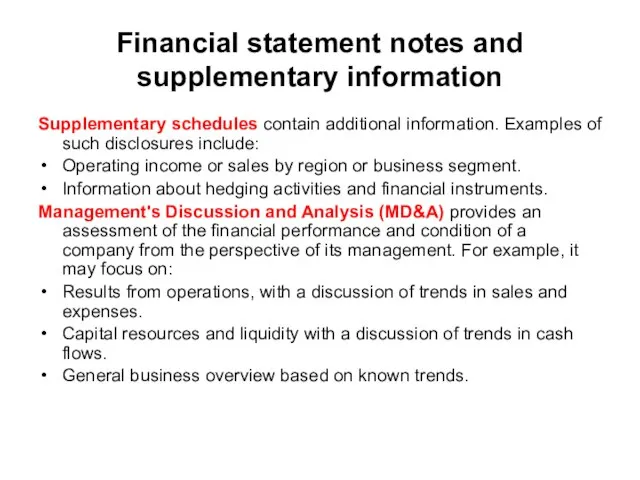

Слайд 8Financial statement notes and supplementary information

Supplementary schedules contain additional information. Examples of

Financial statement notes and supplementary information

Supplementary schedules contain additional information. Examples of

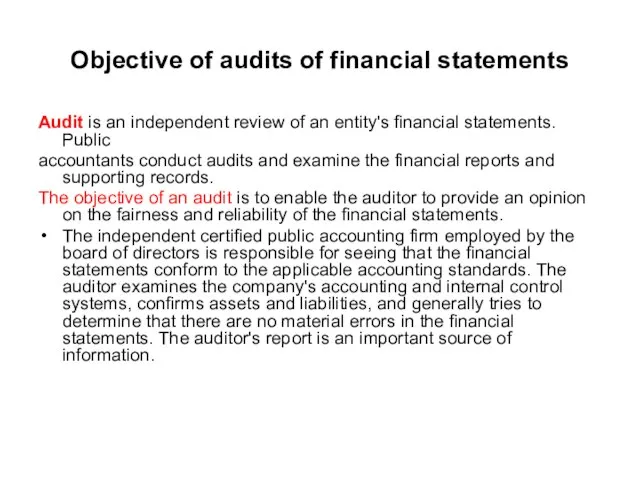

Слайд 9Objective of audits of financial statements

Audit is an independent review of an

Objective of audits of financial statements

Audit is an independent review of an

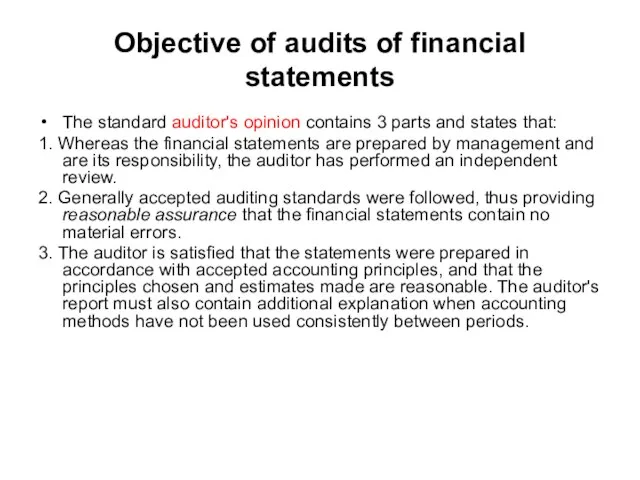

Слайд 10Objective of audits of financial statements

The standard auditor's opinion contains 3 parts

Objective of audits of financial statements

The standard auditor's opinion contains 3 parts

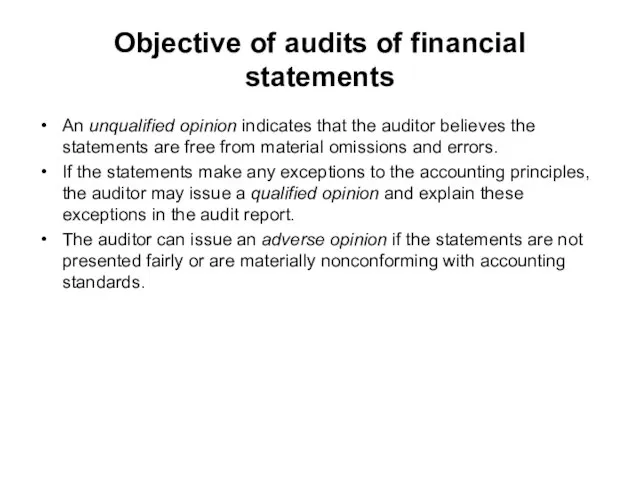

Слайд 11Objective of audits of financial statements

An unqualified opinion indicates that the auditor

Objective of audits of financial statements

An unqualified opinion indicates that the auditor

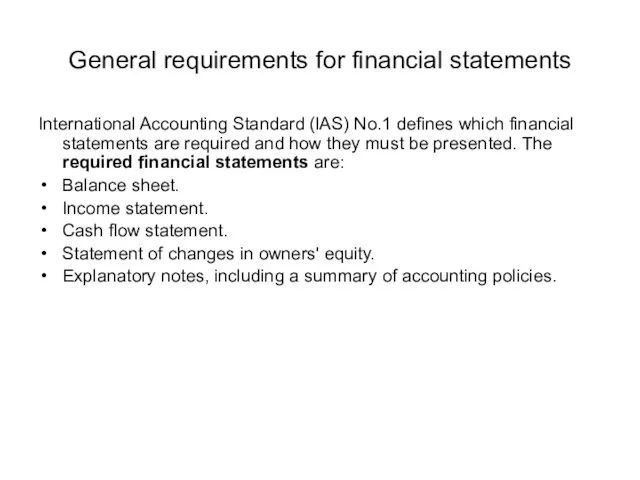

Слайд 12General requirements for financial statements

International Accounting Standard (lAS) No.1 defines which financial

General requirements for financial statements

International Accounting Standard (lAS) No.1 defines which financial

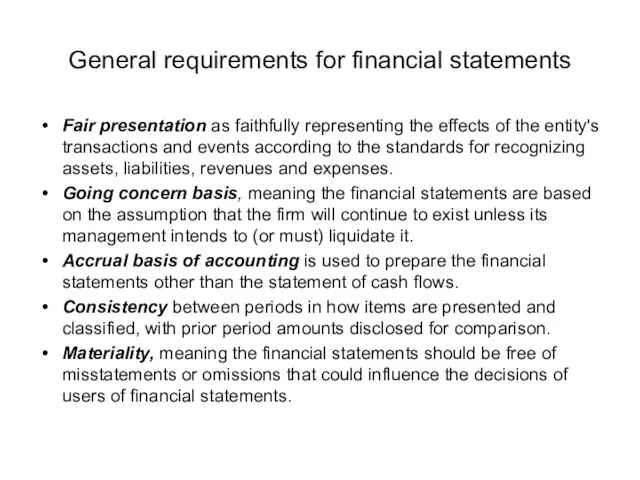

Слайд 13General requirements for financial statements

Fair presentation as faithfully representing the effects of

General requirements for financial statements

Fair presentation as faithfully representing the effects of

Слайд 14General requirements for financial statements

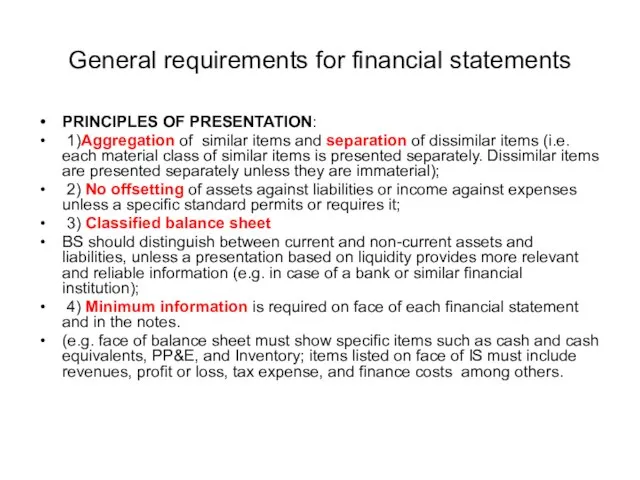

PRINCIPLES OF PRESENTATION:

1)Aggregation of similar items and

General requirements for financial statements

PRINCIPLES OF PRESENTATION:

1)Aggregation of similar items and

Слайд 15Qualitative characteristics of financial statements:

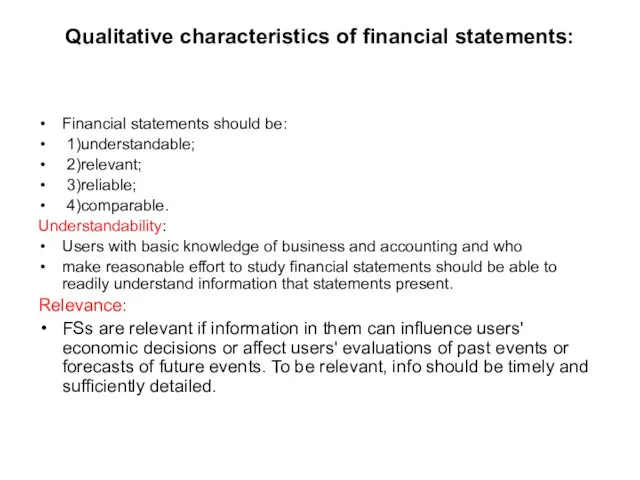

Financial statements should be:

1)understandable;

2)relevant;

3)reliable;

4)comparable.

Understandability:

Users

Qualitative characteristics of financial statements:

Financial statements should be:

1)understandable;

2)relevant;

3)reliable;

4)comparable.

Understandability:

Users

Слайд 16Qualitative characteristics of financial statements:

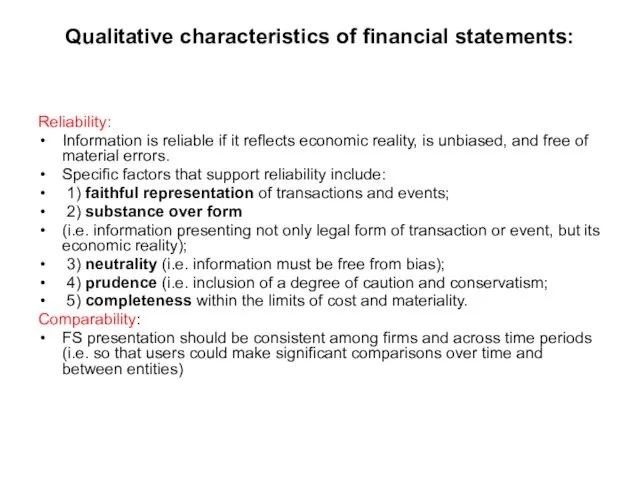

Reliability:

Information is reliable if it reflects economic reality,

Qualitative characteristics of financial statements:

Reliability:

Information is reliable if it reflects economic reality,

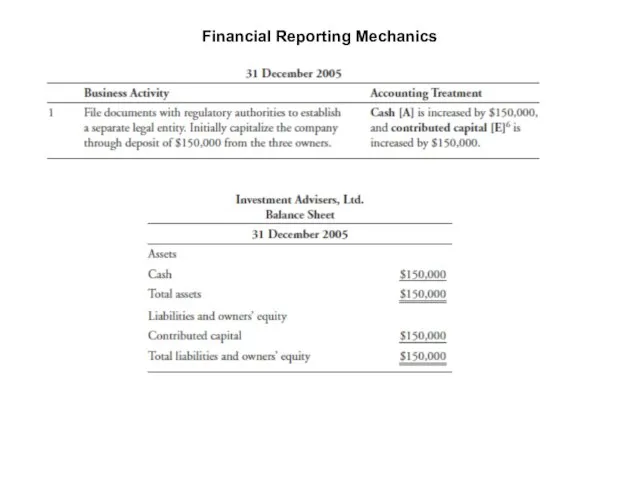

Слайд 17Financial Reporting Mechanics

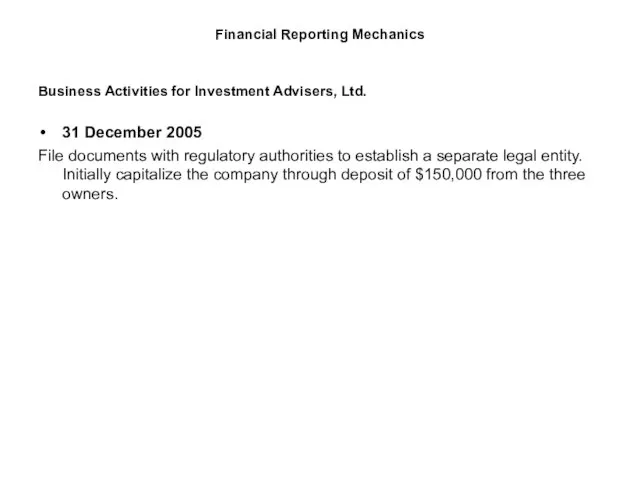

Business Activities for Investment Advisers, Ltd.

31 December 2005

File documents

Financial Reporting Mechanics

Business Activities for Investment Advisers, Ltd.

31 December 2005

File documents

Слайд 18Financial Reporting Mechanics

Financial Reporting Mechanics

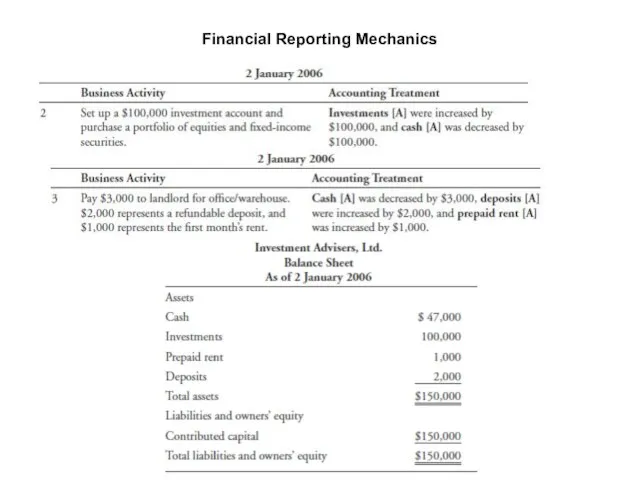

Слайд 19Financial Reporting Mechanics

2 January 2006

Set up a $100,000 investment account and

Financial Reporting Mechanics

2 January 2006

Set up a $100,000 investment account and

Слайд 20Financial Reporting Mechanics

Financial Reporting Mechanics

Слайд 21Financial Reporting Mechanics

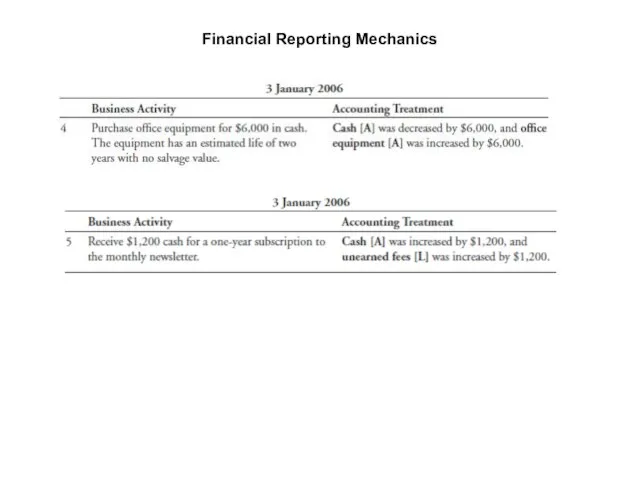

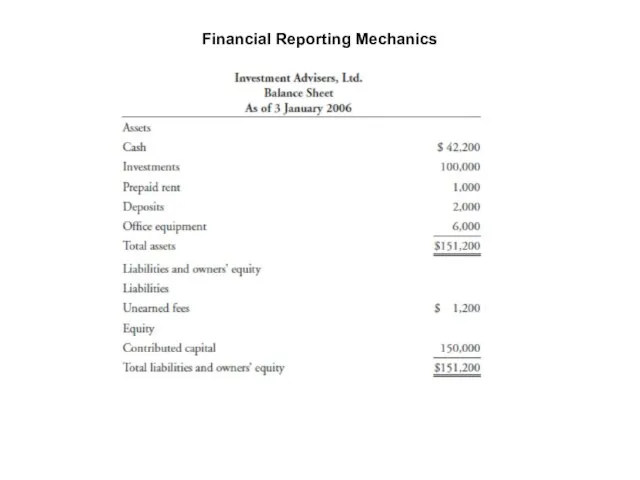

3 January 2006

Purchase office equipment for $6,000 in cash. The

Financial Reporting Mechanics

3 January 2006

Purchase office equipment for $6,000 in cash. The

Слайд 22Financial Reporting Mechanics

Financial Reporting Mechanics

Слайд 23Financial Reporting Mechanics

Financial Reporting Mechanics

Слайд 24Financial Reporting Mechanics

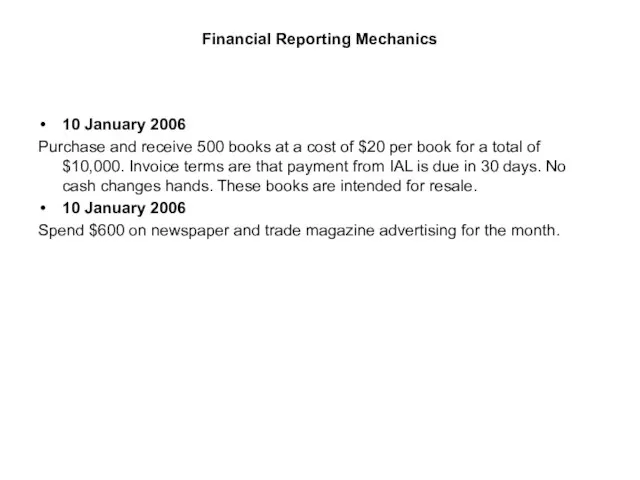

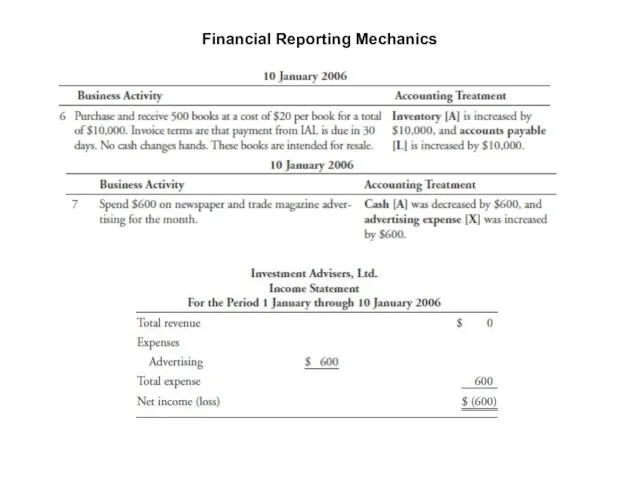

10 January 2006

Purchase and receive 500 books at a cost

Financial Reporting Mechanics

10 January 2006

Purchase and receive 500 books at a cost

Слайд 25Financial Reporting Mechanics

Financial Reporting Mechanics

Слайд 26Financial Reporting Mechanics

Financial Reporting Mechanics

Слайд 27Financial Reporting Mechanics

15 January 2006

Borrow $12,000 from a bank for working capital.

Financial Reporting Mechanics

15 January 2006

Borrow $12,000 from a bank for working capital.

Слайд 28Financial Reporting Mechanics

Financial Reporting Mechanics

Слайд 29Financial Reporting Mechanics

Financial Reporting Mechanics

Слайд 30Financial Reporting Mechanics

Financial Reporting Mechanics

Слайд 31Financial Reporting Mechanics

30 January 2006

Hire a part-time clerk. The clerk is hired

Financial Reporting Mechanics

30 January 2006

Hire a part-time clerk. The clerk is hired

Слайд 32Financial Reporting Mechanics

Financial Reporting Mechanics

Слайд 33Financial Reporting Mechanics

31 January 2006

Mail out the first month’s newsletter to customer.

Financial Reporting Mechanics

31 January 2006

Mail out the first month’s newsletter to customer.

Слайд 34Financial Reporting Mechanics

Financial Reporting Mechanics

Слайд 35Financial Reporting Mechanics

Financial Reporting Mechanics

Слайд 36Financial Reporting Mechanics

Financial Reporting Mechanics

Слайд 37Financial Reporting Mechanics

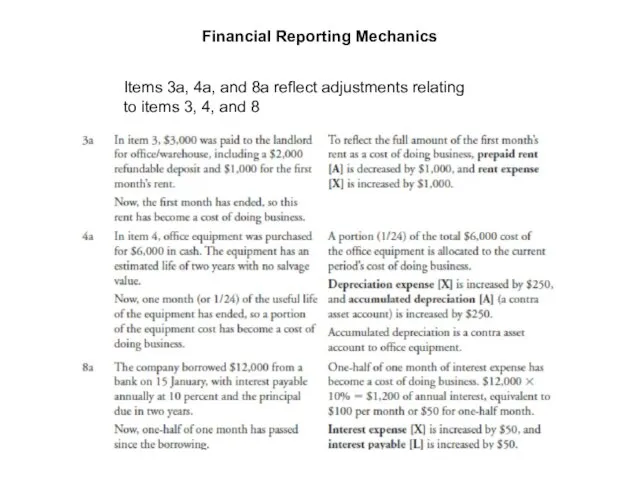

Items 3a, 4a, and 8a reflect adjustments relating to items

Financial Reporting Mechanics

Items 3a, 4a, and 8a reflect adjustments relating to items

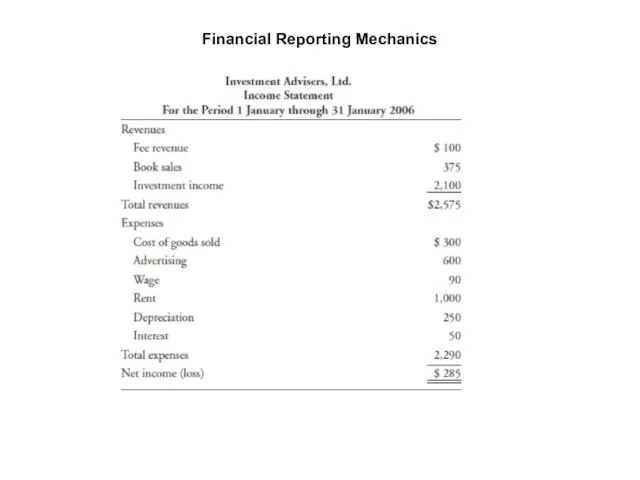

Слайд 38Income Statement

Income statement presents information on the financial results of a company’s

Income Statement

Income statement presents information on the financial results of a company’s

Слайд 39Income Statement

Income Statement

Слайд 40Income Statement

Income Statement

Слайд 41Revenue Recognition

A fundamental principle of accrual accounting is that revenue is recognized

Revenue Recognition

A fundamental principle of accrual accounting is that revenue is recognized

Слайд 42Revenue Recognition

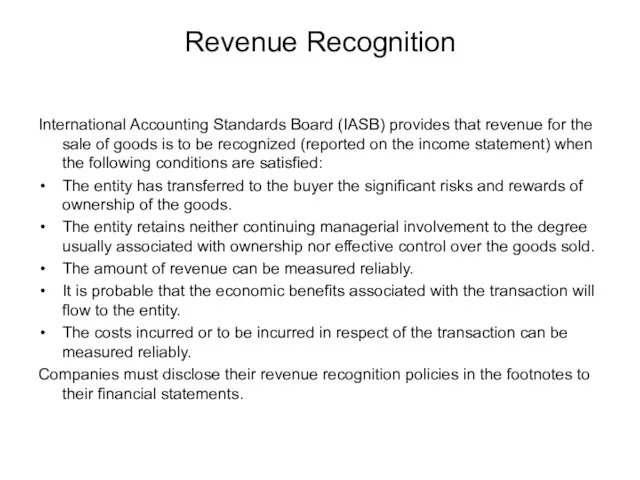

International Accounting Standards Board (IASB) provides that revenue for the sale

Revenue Recognition

International Accounting Standards Board (IASB) provides that revenue for the sale

Слайд 43Expense Recognition

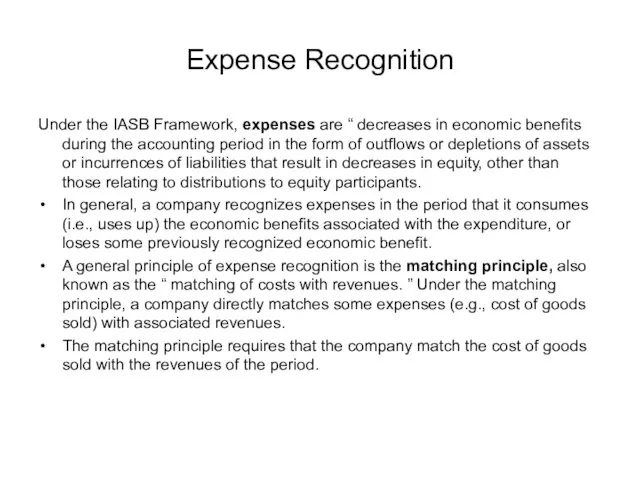

Under the IASB Framework, expenses are “ decreases in economic benefits

Expense Recognition

Under the IASB Framework, expenses are “ decreases in economic benefits

Слайд 44Expense Recognition

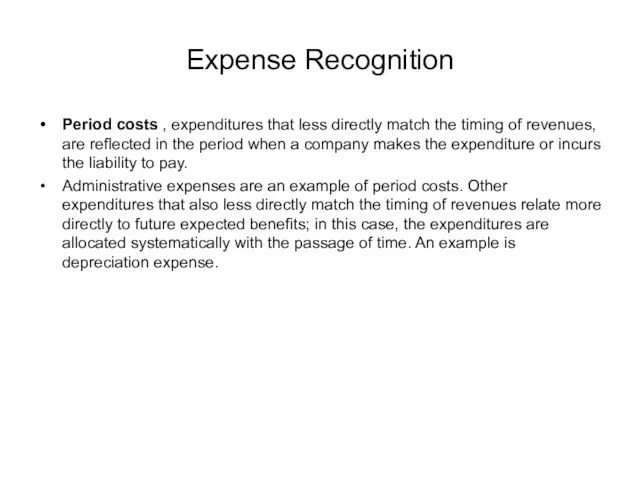

Period costs , expenditures that less directly match the timing of

Expense Recognition

Period costs , expenditures that less directly match the timing of

Слайд 45Inventory Accounting Methods

Inventory Accounting Methods

Слайд 46Inventory Accounting Methods

Inventory Accounting Methods

Слайд 47Inventory Accounting Methods

Inventory Accounting Methods

Слайд 48Inventory Accounting Methods

Inventory Accounting Methods

Слайд 49Inventory Accounting Methods

Inventory Accounting Methods

Слайд 50Inventory Accounting Methods

Inventory Accounting Methods

Как бы ни был красив Шираз, Он не лучше рязанских раздолий.

Как бы ни был красив Шираз, Он не лучше рязанских раздолий. Презентация на тему Объёмы тел

Презентация на тему Объёмы тел Презентация на тему Прямая и обратная пропорциональные зависимости (6 класс)

Презентация на тему Прямая и обратная пропорциональные зависимости (6 класс) Интерьер и внутреннее убранства крестьянской избы

Интерьер и внутреннее убранства крестьянской избы …. и в поте лица твоего будешь есть хлеб.

…. и в поте лица твоего будешь есть хлеб. Спаситель Петербурга

Спаситель Петербурга МП

МП Группа компаний Интегрика

Группа компаний Интегрика СПЕЦИФИЧНОЕ ПРИЛОЖЕНИЕ КЛИМАТА И МИНЕРАЛЬНыХ ВОД ВО ВРЕМЯ ЛЕЧЕНИЯ И ВОССТAНОВЛЕНИЯ АНДРОЛОГИЧЕСКИХ И ГИНЕКОЛОГИЧЕСКИХ ЗАБОЛЕВ

СПЕЦИФИЧНОЕ ПРИЛОЖЕНИЕ КЛИМАТА И МИНЕРАЛЬНыХ ВОД ВО ВРЕМЯ ЛЕЧЕНИЯ И ВОССТAНОВЛЕНИЯ АНДРОЛОГИЧЕСКИХ И ГИНЕКОЛОГИЧЕСКИХ ЗАБОЛЕВ Цветочная лавка AMSTERDAM. Коммерческое предложение

Цветочная лавка AMSTERDAM. Коммерческое предложение ABBYY и «Просвещение» – новые возможности для изучения английского языка!

ABBYY и «Просвещение» – новые возможности для изучения английского языка! Фотоальбом

Фотоальбом Начинается урок, Он пойдёт ребятам впрок. Постарайтесь всё понять И очень многое узнать.

Начинается урок, Он пойдёт ребятам впрок. Постарайтесь всё понять И очень многое узнать. Вологодское Кружево

Вологодское Кружево Сводная по мерчендайзингу. Октябрь 2022

Сводная по мерчендайзингу. Октябрь 2022 Считай, экономь и плати!Правовые аспекты взаимоотношений между гражданами, исполнителями коммунальных услуг и ресурсоснабжающе

Считай, экономь и плати!Правовые аспекты взаимоотношений между гражданами, исполнителями коммунальных услуг и ресурсоснабжающе Государственная власть и государственное управления

Государственная власть и государственное управления Исследование антиоксидантной активности фитопрепарата «Тигровый глаз - орто»

Исследование антиоксидантной активности фитопрепарата «Тигровый глаз - орто» Поволжский экономический район

Поволжский экономический район РАСЧЕТ ПРОЧНОСТИ НОРМАЛЬНЫХ СЕЧЕНИЙ

РАСЧЕТ ПРОЧНОСТИ НОРМАЛЬНЫХ СЕЧЕНИЙ  Забавные загадки по физике

Забавные загадки по физике Понятие об имени прилагательном

Понятие об имени прилагательном Условия осуществления образовательной деятельности

Условия осуществления образовательной деятельности математика

математика Я познаю мир

Я познаю мир Коренной перелом в Великой Отечественной войне

Коренной перелом в Великой Отечественной войне Трехслойные сэндвич-панелиМП ТСП

Трехслойные сэндвич-панелиМП ТСП Славянский регион

Славянский регион