- Perfect Conpetition and the supply Curve

Содержание

- 2. What a perfectly competitive market is and the characteristics of a perfectly competitive industry How a

- 3. Perfect Competition A price-taking producer is a producer whose actions have no effect on the market

- 4. Two Necessary Conditions for Perfect Competition For an industry to be perfectly competitive, it must contain

- 5. Free Entry and Exit There is free entry and exit into and from an industry when

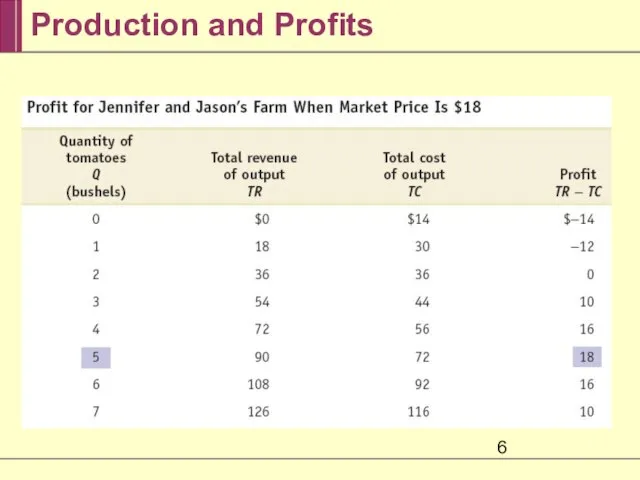

- 6. Production and Profits

- 7. Using Marginal Analysis to Choose the Profit-Maximizing Quantity of Output Marginal revenue is the change in

- 8. The Optimal Output Rule The optimal output rule says that profit is maximized by producing the

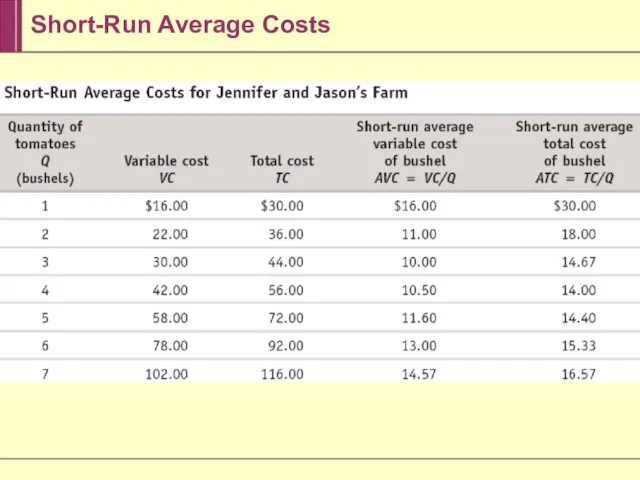

- 9. Short-Run Costs for Jennifer and Jason’s Farm

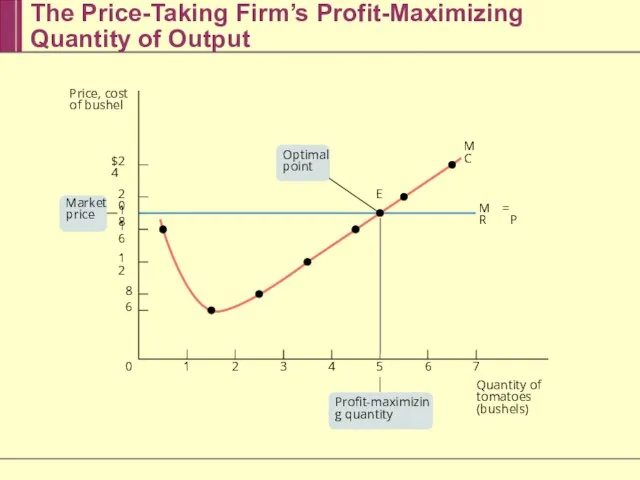

- 10. Marginal Analysis Leads to Profit-Maximizing Quantity of Output The price-taking firm’s optimal output rule says that

- 11. The Price-Taking Firm’s Profit-Maximizing Quantity of Output 7 6 5 4 3 2 1 0 $24

- 12. When Is Production Profitable? If TR > TC, the firm is profitable. If TR = TC,

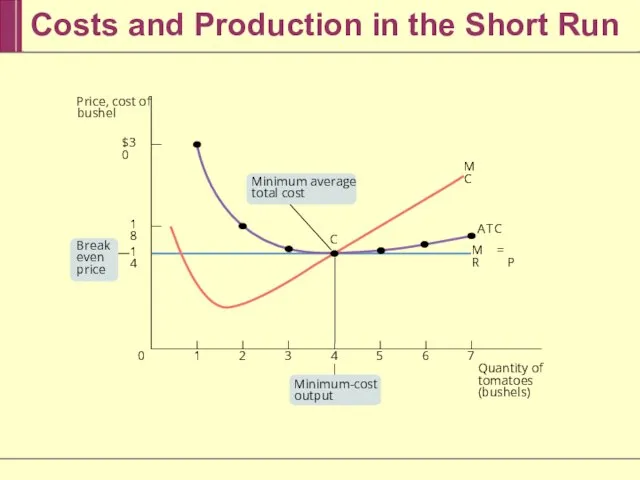

- 13. Short-Run Average Costs

- 14. Costs and Production in the Short Run 7 6 5 4 3 2 1 0 $30

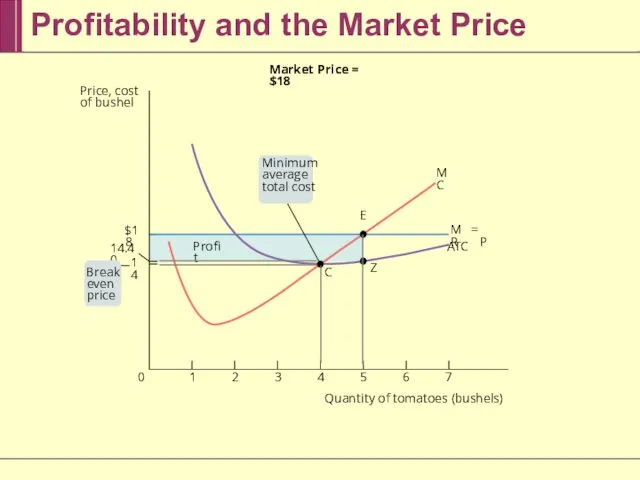

- 15. Profitability and the Market Price 7 6 5 4 3 2 1 0 MC Profit A

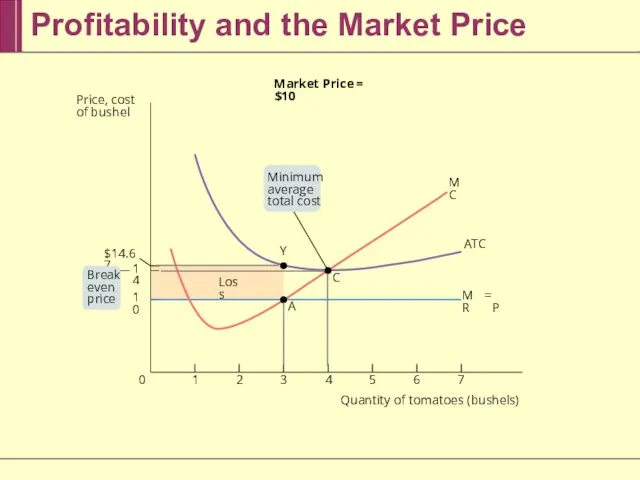

- 16. Profitability and the Market Price 7 6 5 4 3 2 1 0 MC Loss A

- 17. Profit, Break-Even or Loss The break-even price of a price-taking firm is the market price at

- 18. The Short-Run Individual Supply Curve 7 6 5 4 3 3.5 2 1 0 $18 16

- 19. Summary of the Competitive Firm’s Profitability and Production Conditions

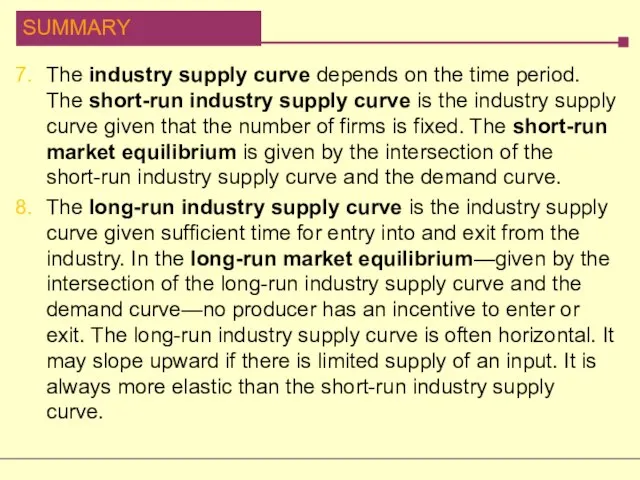

- 20. Industry Supply Curve The industry supply curve shows the relationship between the price of a good

- 21. The Long-Run Industry Supply Curve A market is in long-run market equilibrium when the quantity supplied

- 22. The Short-Run Market Equilibrium 700 600 500 400 300 200 0 $26 22 18 14 10

- 23. The Long-Run Market Equilibrium Quantity of tomatoes (bushels) 6 5 4 4.5 3 0 $18 16

- 24. The Effect of an Increase in Demand in the Short Run and the Long Run MC

- 25. Comparing the Short-Run and Long-Run Industry Supply Curves The long-run industry supply curve is always flatter

- 26. Conclusions Three conclusions about the cost of production and efficiency in the long-run equilibrium of a

- 27. In a perfectly competitive market all producers are price-taking producers and all consumers are price-taking consumers.

- 28. A producer chooses output according to the optimal output rule: produce the quantity at which marginal

- 29. Fixed cost is irrelevant to the firm’s optimal short-run production decision, which depends on its shut-down

- 30. The industry supply curve depends on the time period. The short-run industry supply curve is the

- 32. Скачать презентацию

Слайд 3Perfect Competition

A price-taking producer is a producer whose actions have no effect

Perfect Competition

A price-taking producer is a producer whose actions have no effect

Слайд 4Two Necessary Conditions for Perfect Competition

For an industry to be perfectly competitive,

Two Necessary Conditions for Perfect Competition

For an industry to be perfectly competitive,

Слайд 5Free Entry and Exit

There is free entry and exit into and from

Free Entry and Exit

There is free entry and exit into and from

Слайд 6Production and Profits

Production and Profits

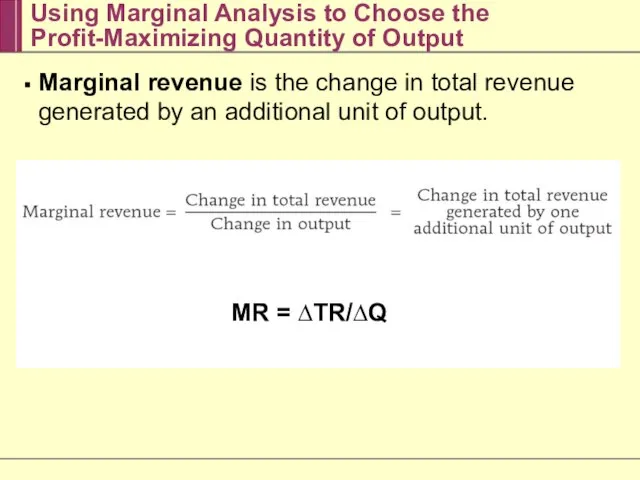

Слайд 7Using Marginal Analysis to Choose the Profit-Maximizing Quantity of Output

Marginal revenue is

Using Marginal Analysis to Choose the Profit-Maximizing Quantity of Output

Marginal revenue is

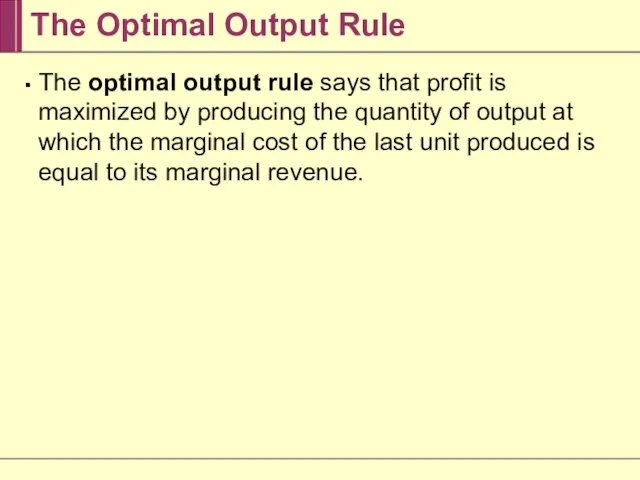

Слайд 8The Optimal Output Rule

The optimal output rule says that profit is maximized

The Optimal Output Rule

The optimal output rule says that profit is maximized

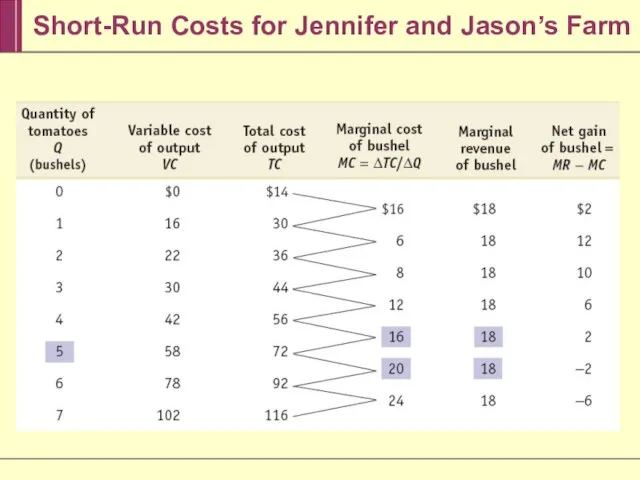

Слайд 9Short-Run Costs for Jennifer and Jason’s Farm

Short-Run Costs for Jennifer and Jason’s Farm

Слайд 10Marginal Analysis Leads to Profit-Maximizing Quantity of Output

The price-taking firm’s optimal output

Marginal Analysis Leads to Profit-Maximizing Quantity of Output

The price-taking firm’s optimal output

Слайд 11The Price-Taking Firm’s Profit-Maximizing Quantity of Output

7

6

5

4

3

2

1

0

$24

20

18

16

12

8

6

Price, cost of bushel

Quantity of tomatoes

The Price-Taking Firm’s Profit-Maximizing Quantity of Output

7

6

5

4

3

2

1

0

$24

20

18

16

12

8

6

Price, cost of bushel

Quantity of tomatoes

Слайд 12When Is Production Profitable?

If TR > TC, the firm is profitable.

If TR

When Is Production Profitable?

If TR > TC, the firm is profitable.

If TR

Слайд 13Short-Run Average Costs

Short-Run Average Costs

Слайд 14Costs and Production in the Short Run

7

6

5

4

3

2

1

0

$30

18

14

MC

A

T

C

MR

=

P

C

Break even price

Minimum-cost output

Price,

Costs and Production in the Short Run

7

6

5

4

3

2

1

0

$30

18

14

MC

A

T

C

MR

=

P

C

Break even price

Minimum-cost output

Price,

Слайд 15Profitability and the Market Price

7

6

5

4

3

2

1

0

MC

Profit

A

T

C

MR

=

P

C

Z

E

Market Price = $18

14

14.40

$18

Price, cost of

Profitability and the Market Price

7

6

5

4

3

2

1

0

MC

Profit

A

T

C

MR

=

P

C

Z

E

Market Price = $18

14

14.40

$18

Price, cost of

Слайд 16Profitability and the Market Price

7

6

5

4

3

2

1

0

MC

Loss

A

T

C

MR

=

P

C

A

Y

Market Price = $10

14

10

$14.67

Price, cost of

Profitability and the Market Price

7

6

5

4

3

2

1

0

MC

Loss

A

T

C

MR

=

P

C

A

Y

Market Price = $10

14

10

$14.67

Price, cost of

Слайд 17Profit, Break-Even or Loss

The break-even price of a price-taking firm is the

Profit, Break-Even or Loss

The break-even price of a price-taking firm is the

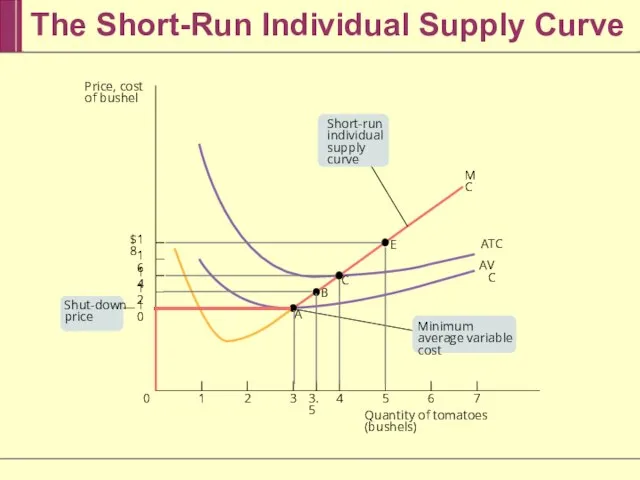

Слайд 18The Short-Run Individual Supply Curve

7

6

5

4

3

3.5

2

1

0

$18

16

14

12

10

MC

A

T

C

A

VC

C

B

A

E

Minimum average variable cost

Short-run individual supply curve

Shut-down price

Price,

The Short-Run Individual Supply Curve

7

6

5

4

3

3.5

2

1

0

$18

16

14

12

10

MC

A

T

C

A

VC

C

B

A

E

Minimum average variable cost

Short-run individual supply curve

Shut-down price

Price,

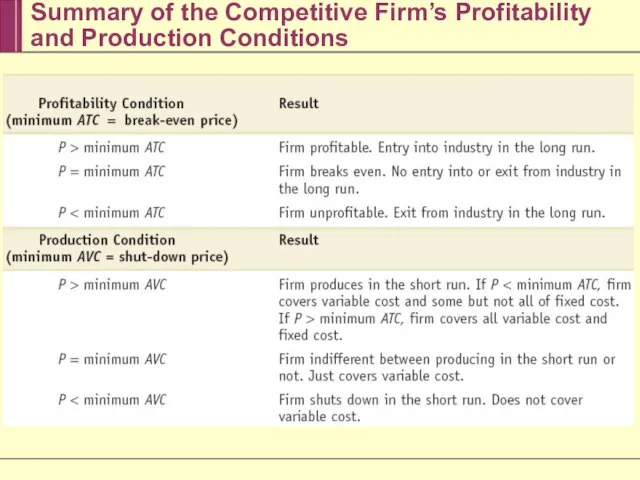

Слайд 19Summary of the Competitive Firm’s Profitability and Production Conditions

Summary of the Competitive Firm’s Profitability and Production Conditions

Слайд 20Industry Supply Curve

The industry supply curve shows the relationship between the price

Industry Supply Curve

The industry supply curve shows the relationship between the price

Слайд 21The Long-Run Industry Supply Curve

A market is in long-run market equilibrium when

The Long-Run Industry Supply Curve

A market is in long-run market equilibrium when

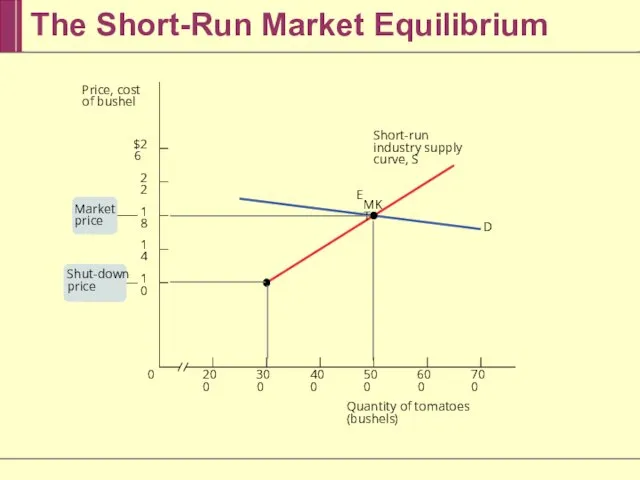

Слайд 22The Short-Run Market Equilibrium

700

600

500

400

300

200

0

$26

22

18

14

10

D

Short-run industry supply curve, S

E

MKT

Shut-down price

Price, cost of bushel

Quantity

The Short-Run Market Equilibrium

700

600

500

400

300

200

0

$26

22

18

14

10

D

Short-run industry supply curve, S

E

MKT

Shut-down price

Price, cost of bushel

Quantity

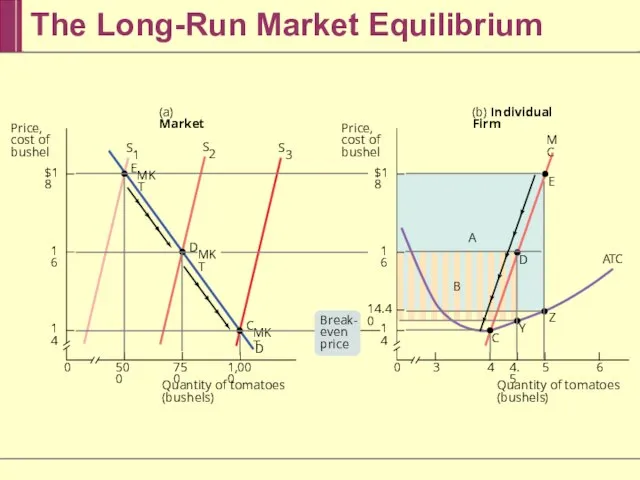

Слайд 23The Long-Run Market Equilibrium

Quantity of tomatoes (bushels)

6

5

4

4.5

3

0

$18

16

14

1,000

750

500

0

$18

16

14

D

E

C

D

Y

Z

MC

A

T

C

A

B

(a) Market

(b) Individual Firm

14.40

E

D

C

MKT

S

1

S

3

S

2

Price, cost of

The Long-Run Market Equilibrium

Quantity of tomatoes (bushels)

6

5

4

4.5

3

0

$18

16

14

1,000

750

500

0

$18

16

14

D

E

C

D

Y

Z

MC

A

T

C

A

B

(a) Market

(b) Individual Firm

14.40

E

D

C

MKT

S

1

S

3

S

2

Price, cost of

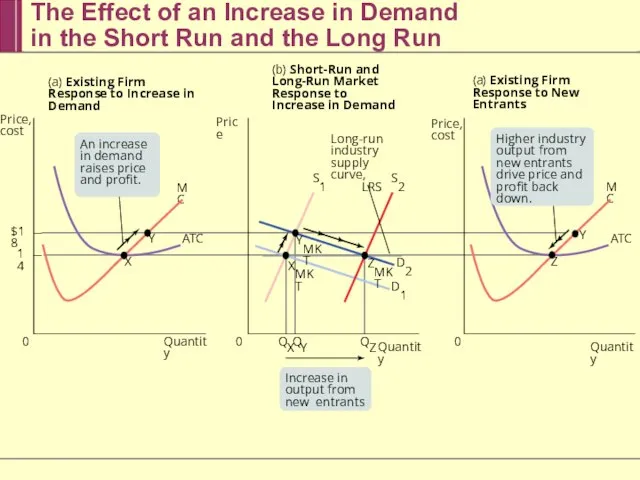

Слайд 24The Effect of an Increase in Demand

in the Short Run and the

The Effect of an Increase in Demand in the Short Run and the

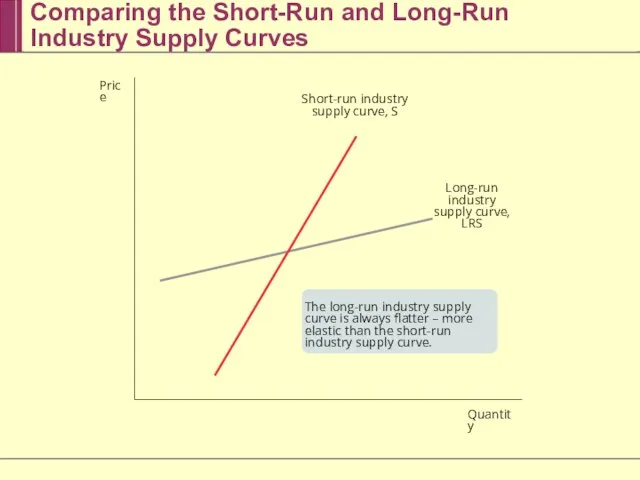

Слайд 25Comparing the Short-Run and Long-Run

Industry Supply Curves

The long-run industry supply curve

Comparing the Short-Run and Long-Run

Industry Supply Curves

The long-run industry supply curve

Слайд 26Conclusions

Three conclusions about the cost of production and efficiency in the long-run

Conclusions

Three conclusions about the cost of production and efficiency in the long-run

Слайд 27In a perfectly competitive market all producers are price-taking producers and all

In a perfectly competitive market all producers are price-taking producers and all

Слайд 28A producer chooses output according to the optimal output rule: produce the

A producer chooses output according to the optimal output rule: produce the

Слайд 29Fixed cost is irrelevant to the firm’s optimal short-run production decision, which

Fixed cost is irrelevant to the firm’s optimal short-run production decision, which

Слайд 30The industry supply curve depends on the time period. The short-run industry

The industry supply curve depends on the time period. The short-run industry

Итоговая аттестация пилотного класса в рамках реализации ФГОС НОО

Итоговая аттестация пилотного класса в рамках реализации ФГОС НОО Достоевский Ф.М

Достоевский Ф.М Вредные привычки у детей. Консультация для родителей

Вредные привычки у детей. Консультация для родителей ТКС

ТКС Измерение удельной теплоемкости твердого тела

Измерение удельной теплоемкости твердого тела «Деревня…

«Деревня… Церкви Ленинграда в годы Советской власти

Церкви Ленинграда в годы Советской власти Условия и механизмы функционирования рынка информационных услуг и продуктов

Условия и механизмы функционирования рынка информационных услуг и продуктов Презентация на тему Жизнь и творчество И.К. Айвазовского

Презентация на тему Жизнь и творчество И.К. Айвазовского Это – Кинематограф!

Это – Кинематограф! Классификация видов групп однородной продукции и их характеристики

Классификация видов групп однородной продукции и их характеристики Погрузочно-доставочная машина LH514L

Погрузочно-доставочная машина LH514L Удивительная

Удивительная Лекция 3 Общение как социально-психологический механизм

Лекция 3 Общение как социально-психологический механизм Организация и техническое оснащение работ по приготовлению, хранению, подготовке к реализации горячих соусов

Организация и техническое оснащение работ по приготовлению, хранению, подготовке к реализации горячих соусов Кривая Филлипса: выбор между безработицей и инфляцией

Кривая Филлипса: выбор между безработицей и инфляцией ГИА по русскому языку

ГИА по русскому языку Тема 5 (Форми дежави)

Тема 5 (Форми дежави) собственность эк 11

собственность эк 11 Найбільші біржі світу. 9 клас

Найбільші біржі світу. 9 клас АЙСБЕРГ

АЙСБЕРГ Система оценки эффективности исполнителя и удовлетворенности клиента качеством сервиса по выполненным заявкам

Система оценки эффективности исполнителя и удовлетворенности клиента качеством сервиса по выполненным заявкам Product Placement

Product Placement Мои жизненные ценности

Мои жизненные ценности 2022-10-6 Резолюция № 1 (1)

2022-10-6 Резолюция № 1 (1) Классические технологии хитрости на экзамене

Классические технологии хитрости на экзамене Презентация на тему Освоение культурного наследия Многоканальная модель освоения культурного наследия

Презентация на тему Освоение культурного наследия Многоканальная модель освоения культурного наследия  Malsharuashylyq

Malsharuashylyq