- Behind the supply Inputs and costs

Содержание

- 2. The importance of the firm’s production function, the relationship between quantity of inputs and quantity of

- 3. The Production Function A production function is the relationship between the quantity of inputs a firm

- 4. Inputs and Output The long run is the time period in which all inputs can be

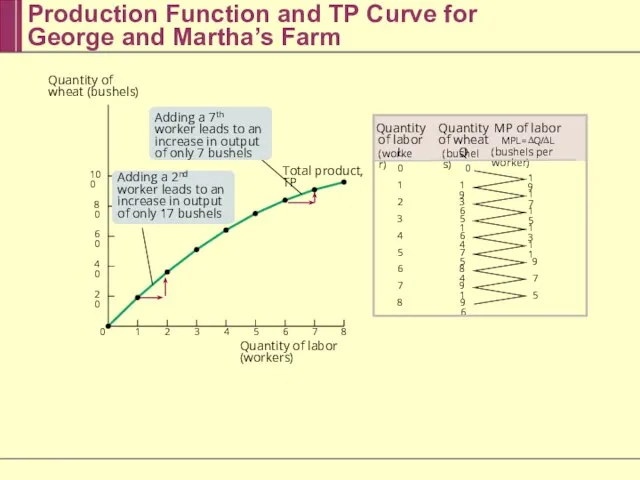

- 5. Production Function and TP Curve for George and Martha’s Farm 0 1 2 3 4 5

- 6. The marginal product of an input is the additional quantity of output that is produced by

- 7. Diminishing Returns to an Input There are diminishing returns to an input when an increase in

- 8. Marginal Product of Labor Curve Marginal product of labor, MPL 7 8 6 5 4 3

- 9. (a) Total Product Curves (b) Marginal Product Curves Marginal product of labor (bushels per worker) Quantity

- 10. From the Production Function to Cost Curves A fixed cost is a cost that does not

- 11. Total Cost Curve The total cost of producing a given quantity of output is the sum

- 12. Total Cost Curve for George and Martha’s Farm 19 36 51 64 75 84 91 96

- 13. The Mythical Man-Month Quantity of labor (programmers) TP MPL 0 0 Quantity of labor (programmers) Marginal

- 14. Two Key Concepts: Marginal Cost and Average Cost As in the case of marginal product, marginal

- 15. Costs at Selena’s Gourmet Salsas

- 16. Total Cost and Marginal Cost Curves for Selena’s Gourmet Salsas $250 200 150 100 50 Cost

- 17. Why is the Marginal Cost Curve Upward Sloping? Because there are diminishing returns to inputs in

- 18. Average Cost Average total cost, often referred to simply as average cost, is total cost divided

- 19. Average Cost Average variable cost is the variable cost per unit of output. AVC = VC/Q=

- 20. Average Total Cost Curve Increasing output has two opposing effects on average total cost: The spreading

- 21. Average Costs for Selena’s Gourmet Salsas

- 22. Average Total Cost Curve for Selena’s Gourmet Salsas Average total cost, ATC M 7 8 9

- 23. Putting the Four Cost Curves Together Note that: Marginal cost is upward sloping due to diminishing

- 24. Marginal Cost and Average Cost Curves for Selena’s Gourmet Salsas $250 200 150 100 50 7

- 25. General Principles That Are Always True About a Firm’s Marginal and Average Total Cost Curves The

- 26. The Relationship Between the Average Total Cost and the Marginal Cost Curves Cost of unit Quantity

- 27. Does the Marginal Cost Curve Always Slope Upward? In practice, marginal cost curves often slope downward

- 28. More Realistic Cost Curves MC A T C A VC Cost of unit Quantity 2. …

- 29. Short-Run versus Long-Run Costs In the short run, fixed cost is completely outside the control of

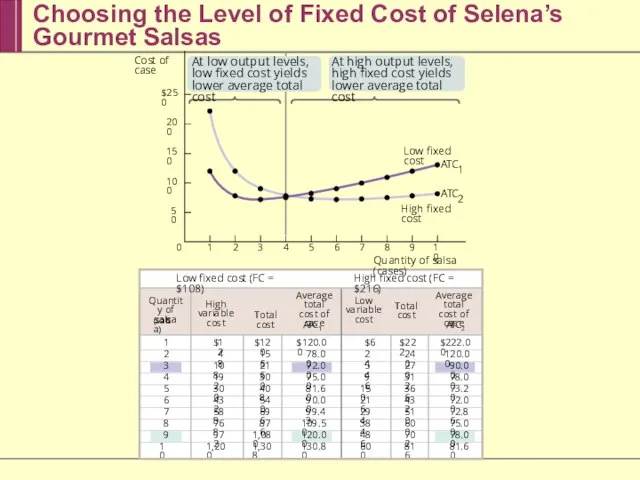

- 30. Choosing the Level of Fixed Cost of Selena’s Gourmet Salsas $250 200 150 100 50 Cost

- 31. The long-run average total cost curve shows the relationship between output and average total cost when

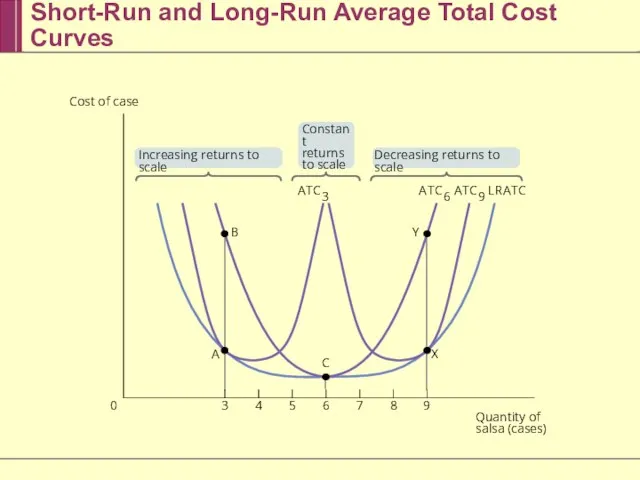

- 32. Short-Run and Long-Run Average Total Cost Curves B A T C 6 A T C 9

- 33. Returns to Scale There are increasing returns to scale (economies of scale) when long-run average total

- 34. The relationship between inputs and output is a producer’s production function. In the short run, the

- 35. Average total cost, total cost divided by quantity of output, is the cost of the average

- 37. Скачать презентацию

Слайд 3The Production Function

A production function is the relationship between the quantity of

The Production Function

A production function is the relationship between the quantity of

Слайд 4Inputs and Output

The long run is the time period in which all

Inputs and Output

The long run is the time period in which all

Слайд 5Production Function and TP Curve for

George and Martha’s Farm

0

1

2

3

4

5

6

7

8

19

17

15

13

11

9

7

5

0

19

36

51

64

75

84

91

96

Quantity of labor L

(worker)

Quantity

Production Function and TP Curve for

George and Martha’s Farm

0

1

2

3

4

5

6

7

8

19

17

15

13

11

9

7

5

0

19

36

51

64

75

84

91

96

Quantity of labor L

(worker)

Quantity

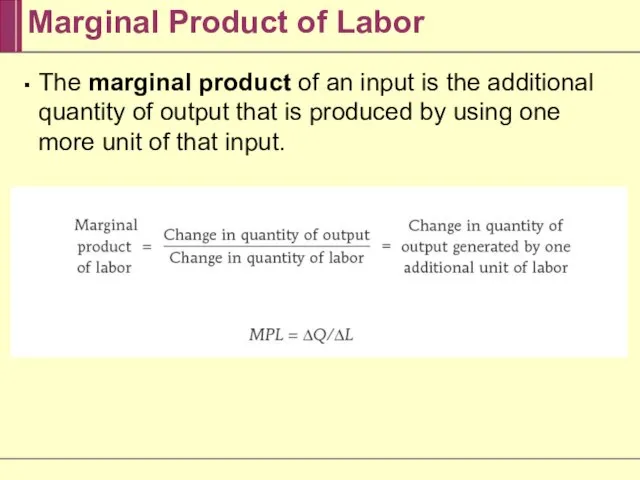

Слайд 6The marginal product of an input is the additional quantity of output

The marginal product of an input is the additional quantity of output

Слайд 7Diminishing Returns to an Input

There are diminishing returns to an input when

Diminishing Returns to an Input

There are diminishing returns to an input when

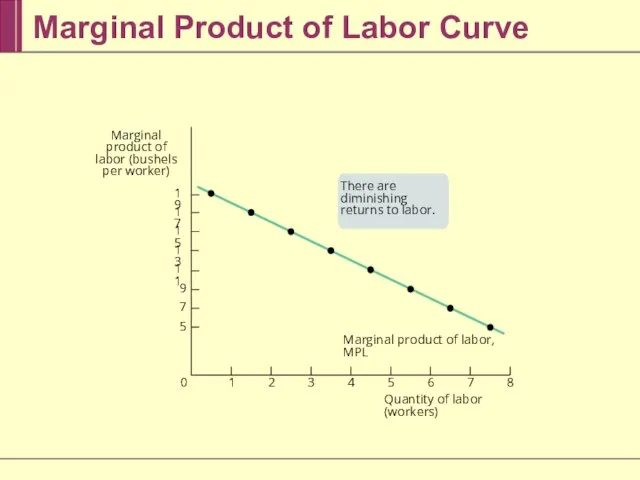

Слайд 8Marginal Product of Labor Curve

Marginal product of labor, MPL

7

8

6

5

4

3

2

1

0

19

17

15

13

11

9

7

5

Marginal product of labor

Marginal Product of Labor Curve

Marginal product of labor, MPL

7

8

6

5

4

3

2

1

0

19

17

15

13

11

9

7

5

Marginal product of labor

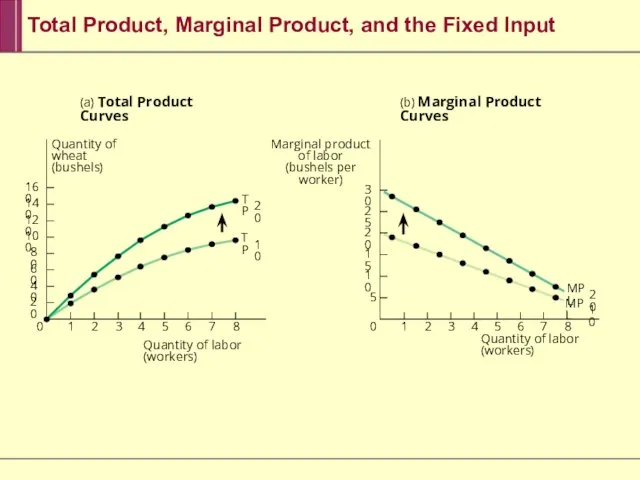

Слайд 9(a) Total Product Curves

(b) Marginal Product Curves

Marginal product of labor

(bushels per

(a) Total Product Curves

(b) Marginal Product Curves

Marginal product of labor

(bushels per

Слайд 10From the Production Function to Cost Curves

A fixed cost is a cost

From the Production Function to Cost Curves

A fixed cost is a cost

Слайд 11Total Cost Curve

The total cost of producing a given quantity of output

Total Cost Curve

The total cost of producing a given quantity of output

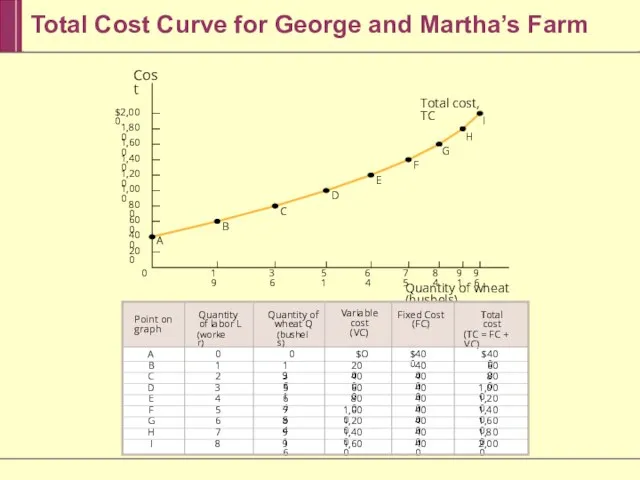

Слайд 12Total Cost Curve for George and Martha’s Farm

19

36

51

64

75

84

91

96

0

$2,000

1,800

1,600

1,400

1,200

1,000

800

600

400

200

Cost

Quantity of wheat (bushels)

A

B

C

D

E

F

G

Total cost,

Total Cost Curve for George and Martha’s Farm

19

36

51

64

75

84

91

96

0

$2,000

1,800

1,600

1,400

1,200

1,000

800

600

400

200

Cost

Quantity of wheat (bushels)

A

B

C

D

E

F

G

Total cost,

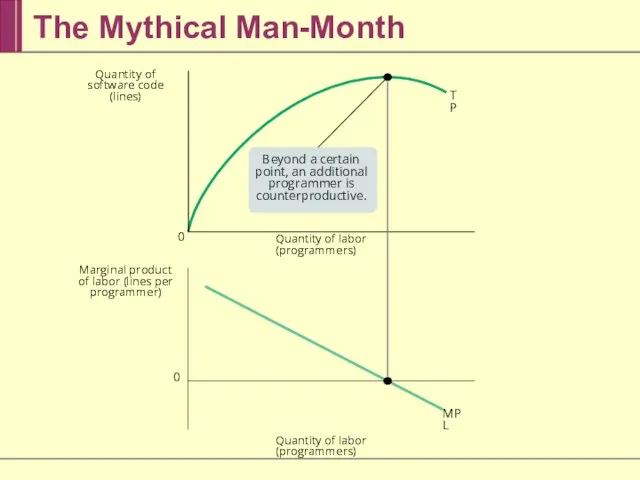

Слайд 13The Mythical Man-Month

Quantity of labor (programmers)

TP

MPL

0

0

Quantity of labor (programmers)

Marginal product of labor

The Mythical Man-Month

Quantity of labor (programmers)

TP

MPL

0

0

Quantity of labor (programmers)

Marginal product of labor

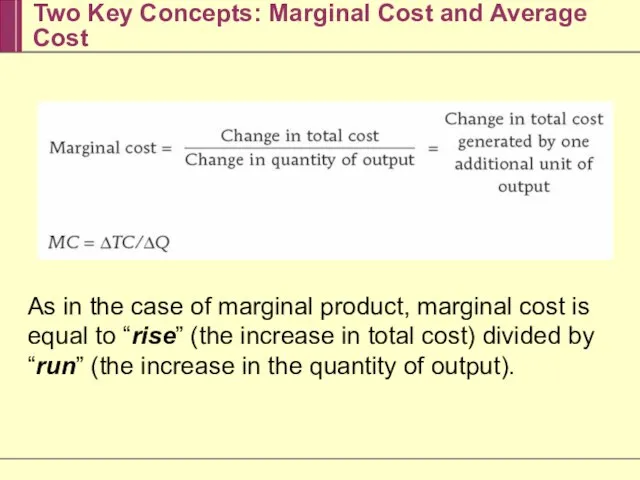

Слайд 14Two Key Concepts: Marginal Cost and Average Cost

As in the case of

Two Key Concepts: Marginal Cost and Average Cost

As in the case of

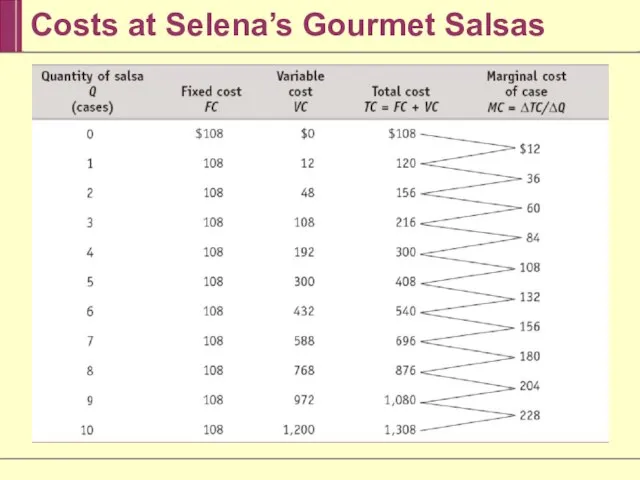

Слайд 15Costs at Selena’s Gourmet Salsas

Costs at Selena’s Gourmet Salsas

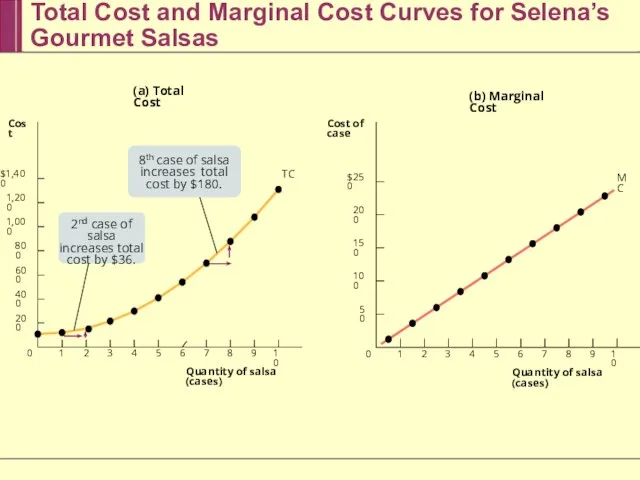

Слайд 16Total Cost and Marginal Cost Curves for Selena’s Gourmet Salsas

$250

200

150

100

50

Cost of case

7

8

9

10

6

5

4

3

2

1

0

$1,400

1,200

1,000

800

600

400

200

Cost

Quantity

Total Cost and Marginal Cost Curves for Selena’s Gourmet Salsas

$250

200

150

100

50

Cost of case

7

8

9

10

6

5

4

3

2

1

0

$1,400

1,200

1,000

800

600

400

200

Cost

Quantity

Слайд 17Why is the Marginal Cost Curve Upward Sloping?

Because there are diminishing returns

Why is the Marginal Cost Curve Upward Sloping?

Because there are diminishing returns

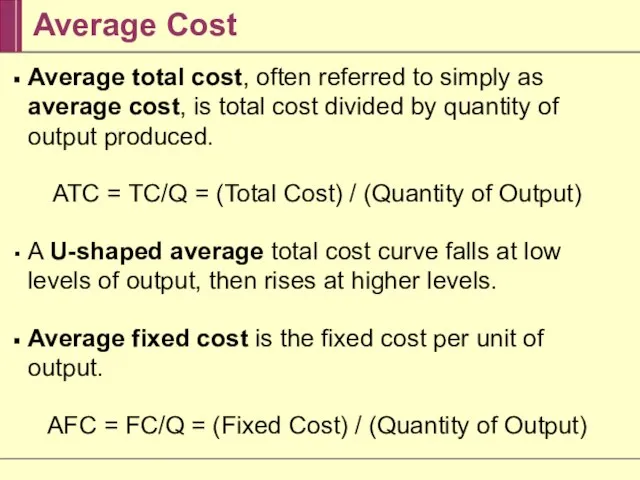

Слайд 18Average Cost

Average total cost, often referred to simply as average cost, is

Average Cost

Average total cost, often referred to simply as average cost, is

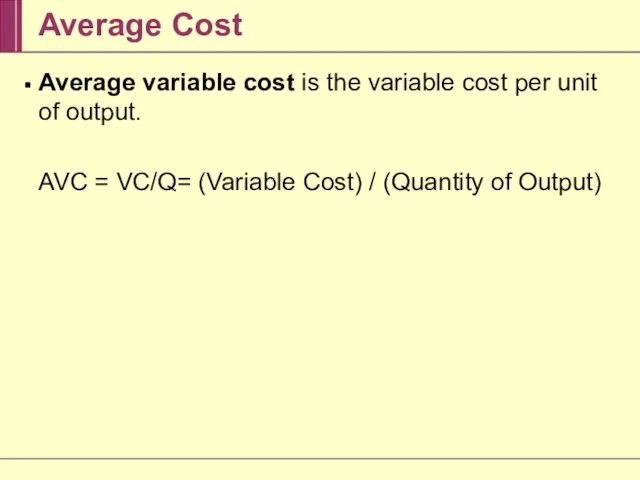

Слайд 19Average Cost

Average variable cost is the variable cost per unit of output.

Average Cost

Average variable cost is the variable cost per unit of output.

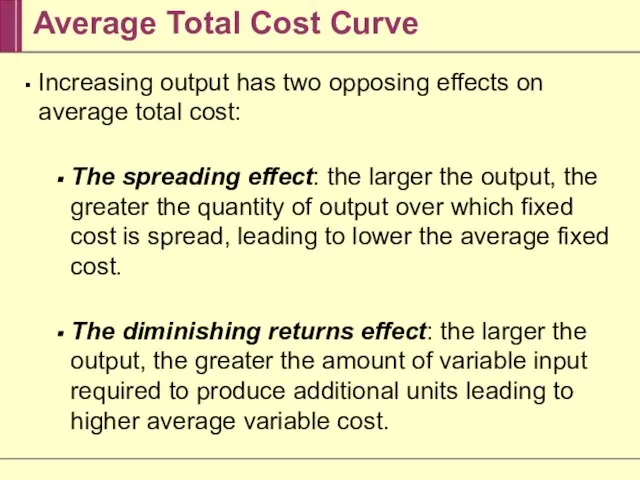

Слайд 20Average Total Cost Curve

Increasing output has two opposing effects on average total

Average Total Cost Curve

Increasing output has two opposing effects on average total

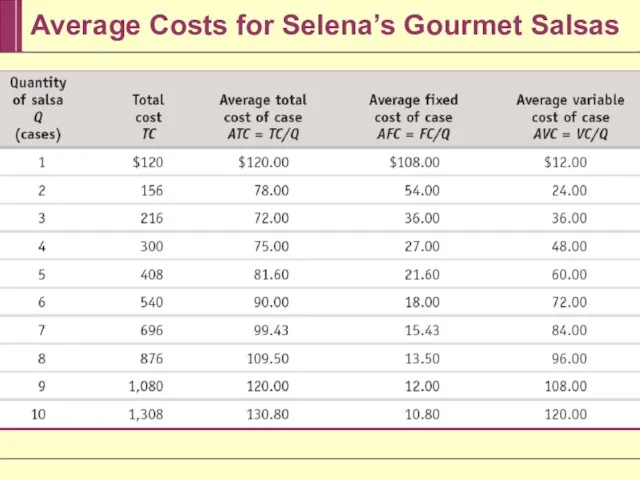

Слайд 21Average Costs for Selena’s Gourmet Salsas

Average Costs for Selena’s Gourmet Salsas

Слайд 22Average Total Cost Curve for Selena’s Gourmet Salsas

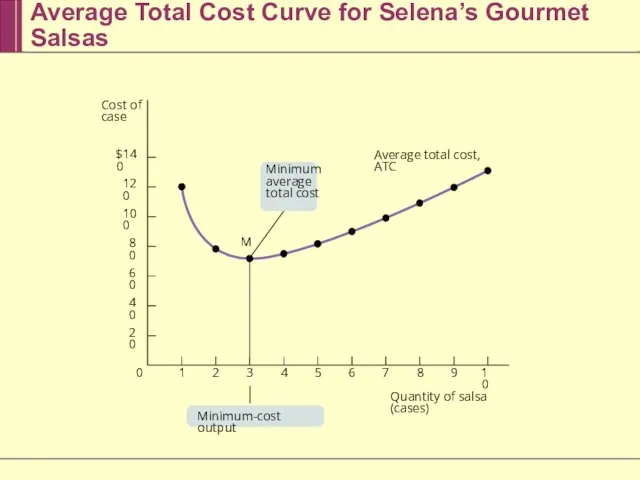

Average total cost, ATC

M

7

8

9

10

6

5

4

3

2

1

0

$140

120

100

80

60

40

20

Minimum average

Average Total Cost Curve for Selena’s Gourmet Salsas

Average total cost, ATC

M

7

8

9

10

6

5

4

3

2

1

0

$140

120

100

80

60

40

20

Minimum average

Слайд 23Putting the Four Cost Curves Together

Note that:

Marginal cost is upward sloping due

Putting the Four Cost Curves Together

Note that:

Marginal cost is upward sloping due

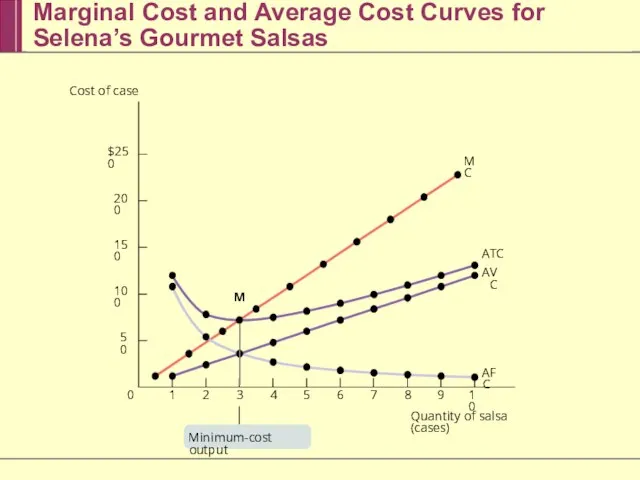

Слайд 24Marginal Cost and Average Cost Curves for Selena’s Gourmet Salsas

$250

200

150

100

50

7

8

9

10

6

5

4

3

2

1

M

0

MC

A

T

C

A

VC

AFC

Minimum-cost output

Cost of

Marginal Cost and Average Cost Curves for Selena’s Gourmet Salsas

$250

200

150

100

50

7

8

9

10

6

5

4

3

2

1

M

0

MC

A

T

C

A

VC

AFC

Minimum-cost output

Cost of

Слайд 25General Principles That Are Always True About a Firm’s Marginal and Average

General Principles That Are Always True About a Firm’s Marginal and Average

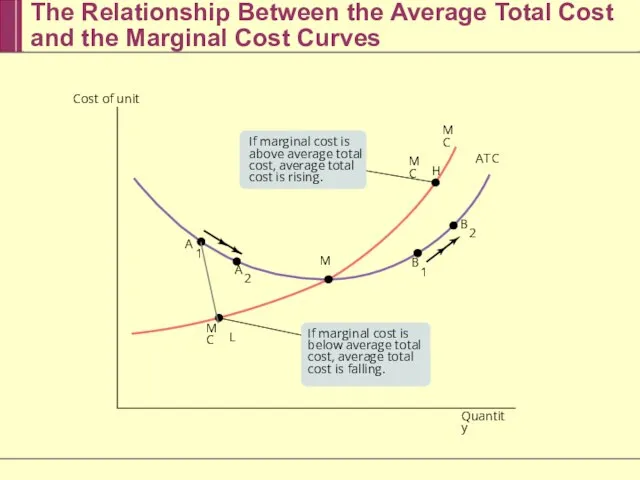

Слайд 26The Relationship Between the Average Total Cost and the Marginal Cost Curves

Cost

The Relationship Between the Average Total Cost and the Marginal Cost Curves

Cost

Слайд 27Does the Marginal Cost Curve Always Slope Upward?

In practice, marginal cost curves

Does the Marginal Cost Curve Always Slope Upward?

In practice, marginal cost curves

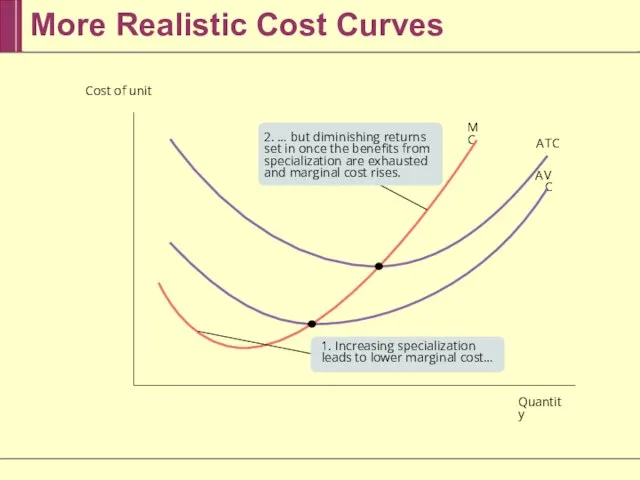

Слайд 28More Realistic Cost Curves

MC

A

T

C

A

VC

Cost of unit

Quantity

2. … but diminishing returns set in

More Realistic Cost Curves

MC

A

T

C

A

VC

Cost of unit

Quantity

2. … but diminishing returns set in

Слайд 29Short-Run versus Long-Run Costs

In the short run, fixed cost is completely outside

Short-Run versus Long-Run Costs

In the short run, fixed cost is completely outside

Слайд 30Choosing the Level of Fixed Cost of Selena’s Gourmet Salsas

$250

200

150

100

50

Cost of case

Quantity

Choosing the Level of Fixed Cost of Selena’s Gourmet Salsas

$250

200

150

100

50

Cost of case

Quantity

Слайд 31The long-run average total cost curve shows the relationship between output and

The long-run average total cost curve shows the relationship between output and

Слайд 32Short-Run and Long-Run Average Total Cost Curves

B

A

T

C

6

A

T

C

9

A

T

C

3

L

R

A

T

C

3

5

8

4

7

0

6

9

Increasing returns to scale

Decreasing returns to

Short-Run and Long-Run Average Total Cost Curves

B

A

T

C

6

A

T

C

9

A

T

C

3

L

R

A

T

C

3

5

8

4

7

0

6

9

Increasing returns to scale

Decreasing returns to

Слайд 33Returns to Scale

There are increasing returns to scale (economies of scale) when

Returns to Scale

There are increasing returns to scale (economies of scale) when

Слайд 34The relationship between inputs and output is a producer’s production function. In

The relationship between inputs and output is a producer’s production function. In

Слайд 35Average total cost, total cost divided by quantity of output, is the

Average total cost, total cost divided by quantity of output, is the

Итоговая аттестация пилотного класса в рамках реализации ФГОС НОО

Итоговая аттестация пилотного класса в рамках реализации ФГОС НОО Достоевский Ф.М

Достоевский Ф.М Вредные привычки у детей. Консультация для родителей

Вредные привычки у детей. Консультация для родителей ТКС

ТКС Измерение удельной теплоемкости твердого тела

Измерение удельной теплоемкости твердого тела «Деревня…

«Деревня… Церкви Ленинграда в годы Советской власти

Церкви Ленинграда в годы Советской власти Условия и механизмы функционирования рынка информационных услуг и продуктов

Условия и механизмы функционирования рынка информационных услуг и продуктов Презентация на тему Жизнь и творчество И.К. Айвазовского

Презентация на тему Жизнь и творчество И.К. Айвазовского Это – Кинематограф!

Это – Кинематограф! Классификация видов групп однородной продукции и их характеристики

Классификация видов групп однородной продукции и их характеристики Погрузочно-доставочная машина LH514L

Погрузочно-доставочная машина LH514L Удивительная

Удивительная Лекция 3 Общение как социально-психологический механизм

Лекция 3 Общение как социально-психологический механизм Организация и техническое оснащение работ по приготовлению, хранению, подготовке к реализации горячих соусов

Организация и техническое оснащение работ по приготовлению, хранению, подготовке к реализации горячих соусов Кривая Филлипса: выбор между безработицей и инфляцией

Кривая Филлипса: выбор между безработицей и инфляцией ГИА по русскому языку

ГИА по русскому языку Тема 5 (Форми дежави)

Тема 5 (Форми дежави) собственность эк 11

собственность эк 11 Найбільші біржі світу. 9 клас

Найбільші біржі світу. 9 клас АЙСБЕРГ

АЙСБЕРГ Система оценки эффективности исполнителя и удовлетворенности клиента качеством сервиса по выполненным заявкам

Система оценки эффективности исполнителя и удовлетворенности клиента качеством сервиса по выполненным заявкам Product Placement

Product Placement Мои жизненные ценности

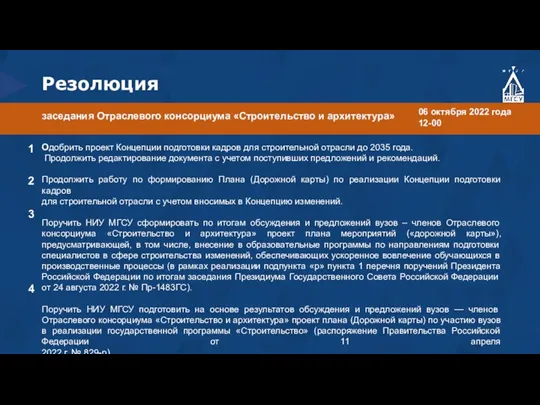

Мои жизненные ценности 2022-10-6 Резолюция № 1 (1)

2022-10-6 Резолюция № 1 (1) Классические технологии хитрости на экзамене

Классические технологии хитрости на экзамене Презентация на тему Освоение культурного наследия Многоканальная модель освоения культурного наследия

Презентация на тему Освоение культурного наследия Многоканальная модель освоения культурного наследия  Malsharuashylyq

Malsharuashylyq