- Presentation On discipline: the English language On Revenue Account

Содержание

- 2. THE CONTENT INTRODUCTION 1. The nature and purpose of income statement 2. The shape and structure

- 3. The aim of the report is to study the report on incomes and businesses. In accordance

- 4. The information report can be used to: evaluate the effectiveness of the management apparatus; forecasting activities

- 5. A report on the results of financial and economic activity is reduced to the disclosure of

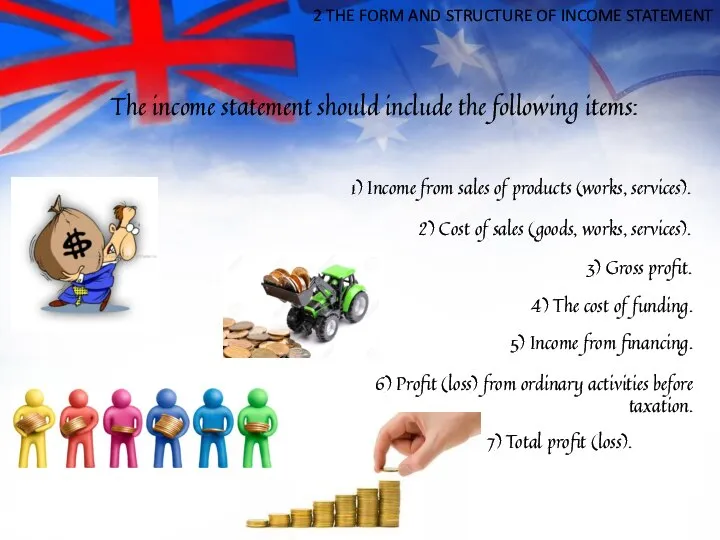

- 6. 2 THE FORM AND STRUCTURE OF INCOME STATEMENT The income statement should include the following items:

- 7. The income statement is one of the main forms of reporting, is necessarily present in periodic

- 8. REFERENCES 1. Babaev A. Y. "Accounting" - Moscow: unity, 2003. 2. Kozlova E. P., Babchenko, T.

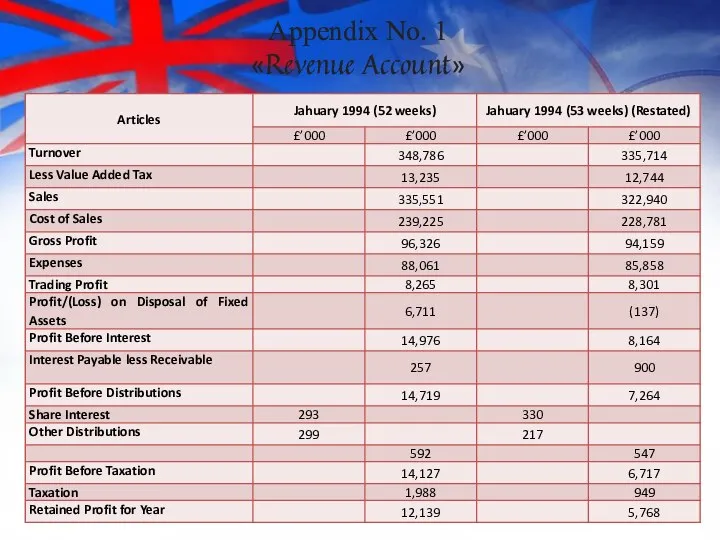

- 9. Appendix No. 1 «Revenue Account»

- 11. Скачать презентацию

Слайд 3The aim of the report is to study the report on incomes

The aim of the report is to study the report on incomes

Слайд 4The information report can be used to:

evaluate the effectiveness of the management

The information report can be used to:

evaluate the effectiveness of the management

Слайд 5A report on the results of financial and economic activity is reduced

A report on the results of financial and economic activity is reduced

Слайд 62 THE FORM AND STRUCTURE OF INCOME STATEMENT

The income statement should include

2 THE FORM AND STRUCTURE OF INCOME STATEMENT

The income statement should include

Слайд 7 The income statement is one of the main forms of reporting, is

The income statement is one of the main forms of reporting, is

Слайд 8REFERENCES

1. Babaev A. Y. "Accounting" - Moscow: unity, 2003.

2. Kozlova E. P.,

REFERENCES

1. Babaev A. Y. "Accounting" - Moscow: unity, 2003.

2. Kozlova E. P.,

Слайд 9Appendix No. 1

«Revenue Account»

Appendix No. 1

«Revenue Account»

Circus (2)

Circus (2) Quest Pirate Ship

Quest Pirate Ship Decorate Your Turkey

Decorate Your Turkey Speech synthesis

Speech synthesis Passive voice

Passive voice About me

About me Nothern reptiles - dragons

Nothern reptiles - dragons Modal verbs: must, have to, can, could, be allowed to

Modal verbs: must, have to, can, could, be allowed to Sample Loch Ness by helgabel

Sample Loch Ness by helgabel Winter Book

Winter Book Will London by helgabel

Will London by helgabel Complete the verb-noun collocations with the nouns below

Complete the verb-noun collocations with the nouns below Правила чтения согласных и гласных звуков английского языка

Правила чтения согласных и гласных звуков английского языка Areas of London

Areas of London Terms to keep clear. Ensemble. Genre. Form

Terms to keep clear. Ensemble. Genre. Form Методические рекомендации 2022

Методические рекомендации 2022 What are americans said to be?

What are americans said to be? Презентация на тему My family (5 класс)

Презентация на тему My family (5 класс)  New words

New words Connectors and linkers: reason, result and purpose

Connectors and linkers: reason, result and purpose At the supermarket

At the supermarket A. Conan Doyle (1859—1930)

A. Conan Doyle (1859—1930) Мнение о книге

Мнение о книге Презентация на тему Club of English Ladies and Gentlemen

Презентация на тему Club of English Ladies and Gentlemen  Treasure maps

Treasure maps Hidden animals (игра)

Hidden animals (игра) What's the weather like today?

What's the weather like today? What color do you like

What color do you like