- taxes 2021 BATIS

Содержание

- 2. Chapter 1: TAXATION AND ITS ECONOMIC EFFECTS Overview of Taxation Principles A tax (from the Latin

- 3. Tax Collection In modern taxation systems, governments levy taxes in money; but in-kind and corvée taxation

- 4. Purposes of Taxation Purposes of Taxation The levying of taxes aims to raise revenue to fund

- 5. Economic Effects of Taxation Economic Effects of Taxation Imposition of taxes may have the following effects:

- 6. Tax Incidence Tax incidence is the division of the burden of a tax between buyers and

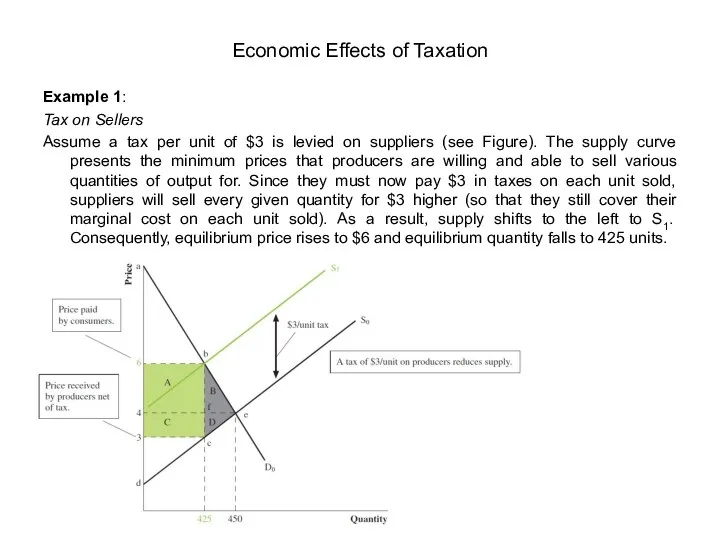

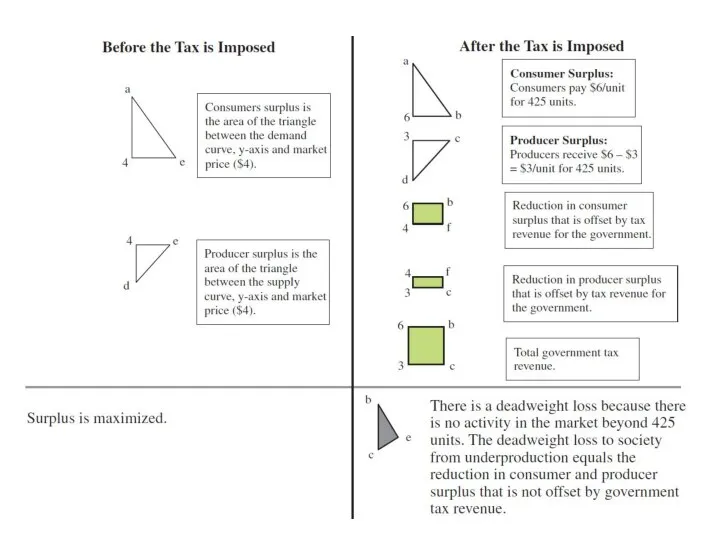

- 7. Example 1: Tax on Sellers Assume a tax per unit of $3 is levied on suppliers

- 9. Consumers purchase 425 units and pay $6/unit. Effectively prices paid by consumers have gone up by

- 10. Example 2: Why taxes result in deadweight losses Imagine that Joe cleans Jane’s house each week

- 11. Example 3: Tax on Buyers Now assume that instead of being levied upon producers, the same

- 12. The impact of a tax on a market outcome is the same whether the tax is

- 13. Tax Incidence and Elasticity of Demand The division of the tax between buyers and sellers depends

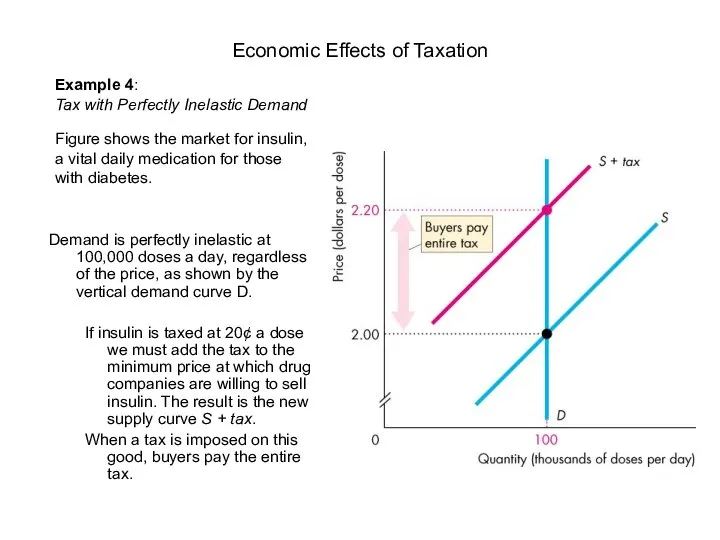

- 14. Economic Effects of Taxation

- 15. Demand is perfectly inelastic at 100,000 doses a day, regardless of the price, as shown by

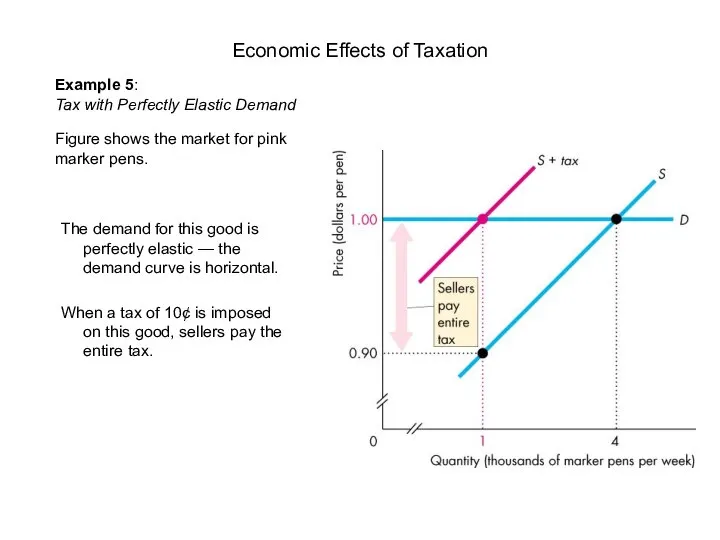

- 16. The demand for this good is perfectly elastic — the demand curve is horizontal. When a

- 17. Tax Incidence and Elasticity of Supply The division of the tax between buyers and sellers also

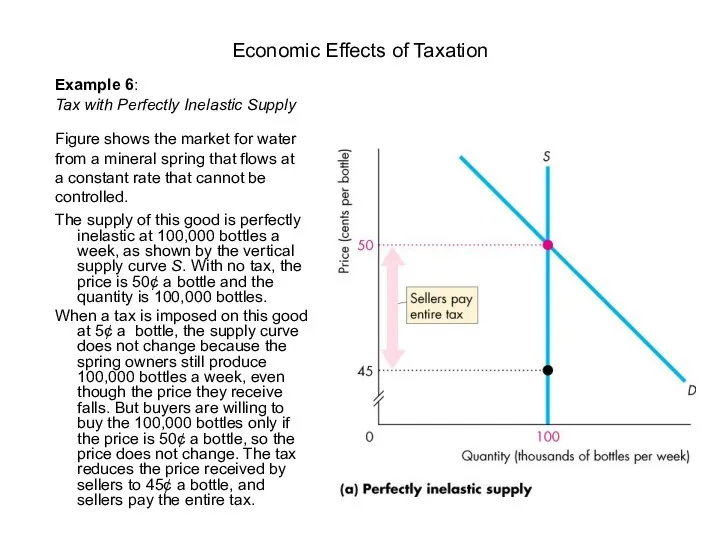

- 19. The supply of this good is perfectly inelastic at 100,000 bottles a week, as shown by

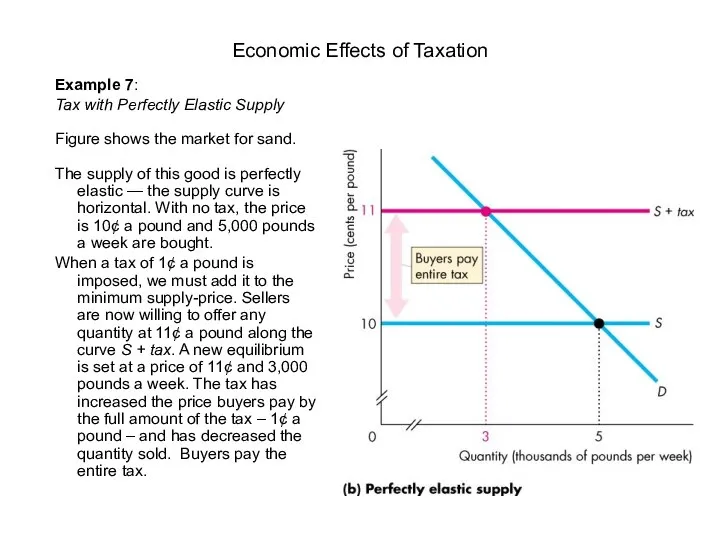

- 20. The supply of this good is perfectly elastic — the supply curve is horizontal. With no

- 21. Example 8: The burden of tax Depending on the circumstance, the burden of tax can fall

- 22. In the tobacco example, the tax burden falls on the most inelastic side of the market.

- 23. When a tax is introduced in a market with an inelastic supply (see Fig. A) —

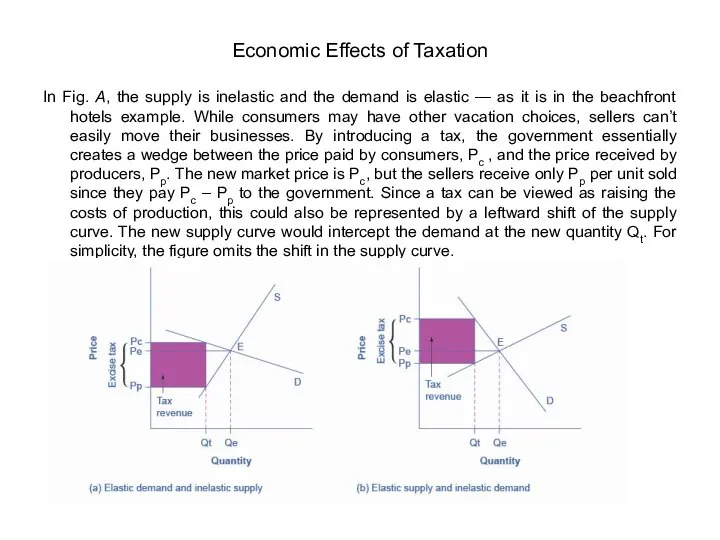

- 24. In Fig. A, the supply is inelastic and the demand is elastic — as it is

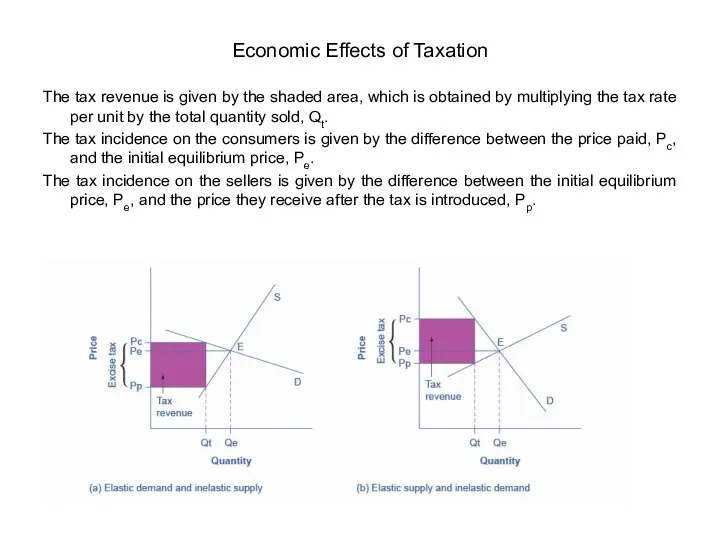

- 25. The tax revenue is given by the shaded area, which is obtained by multiplying the tax

- 26. In figure A, the tax burden falls disproportionately on the sellers, and a larger proportion of

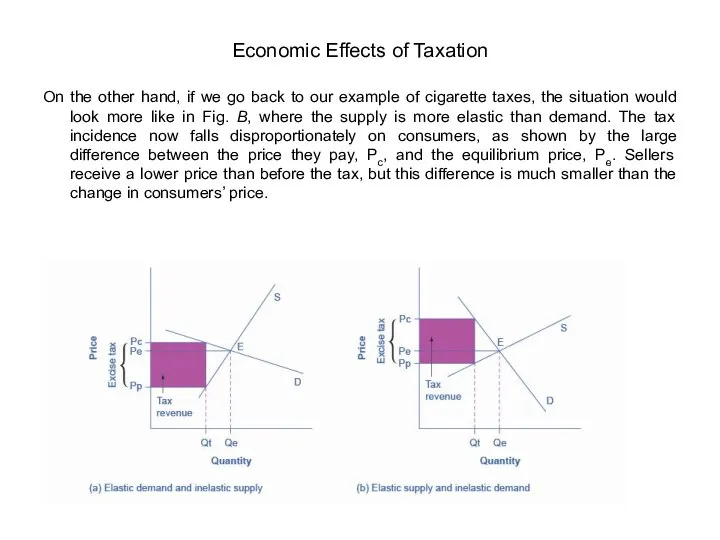

- 27. On the other hand, if we go back to our example of cigarette taxes, the situation

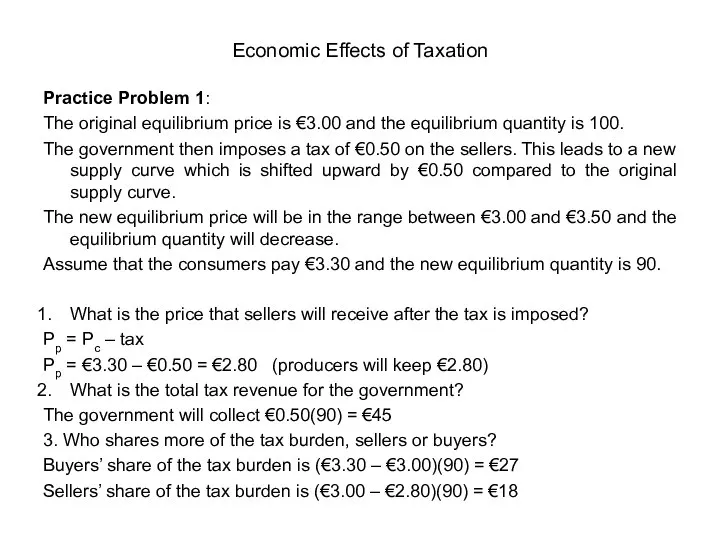

- 28. Practice Problem 1: The original equilibrium price is €3.00 and the equilibrium quantity is 100. The

- 29. Other economic effects of taxation Redistribution of Income This effect is felt most in developing countries.

- 30. Other economic effects of taxation A Reduction in Incentive It may be argued that increased taxation

- 31. Other economic effects of taxation 3. A Reduction in Business Activity Entrepreneurs undertake investment in anticipation

- 32. Other economic effects of taxation 4. Effects on the Ability to Work, Save and Invest Imposition

- 33. Other economic effects of taxation It is suggested that effects of taxes upon the willingness to

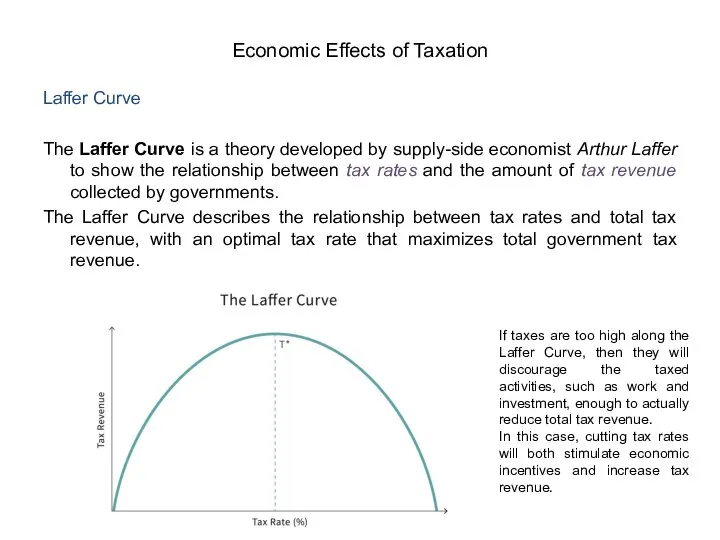

- 34. Laffer Curve The Laffer Curve is a theory developed by supply-side economist Arthur Laffer to show

- 35. Chapter 2: BASIC PRINCIPLES OF TAXATION Goals of an Ideal Taxing System Principles of taxation vary

- 36. 1. Equality Taxpayers should bear a fair level of tax relative to their economic positions (e.g.,

- 37. Vertical equity: When taxpayers are in different economic positions, the taxpayer with the greatest ability to

- 38. 2. Certainty Taxpayer knows when, how, and how much tax is paid. It would protect the

- 39. Tax Base Taxes are computed by multiplying the tax rate by the tax base, that is:

- 40. Tax Deduction Tax deduction is a reduction of income that is able to be taxed and

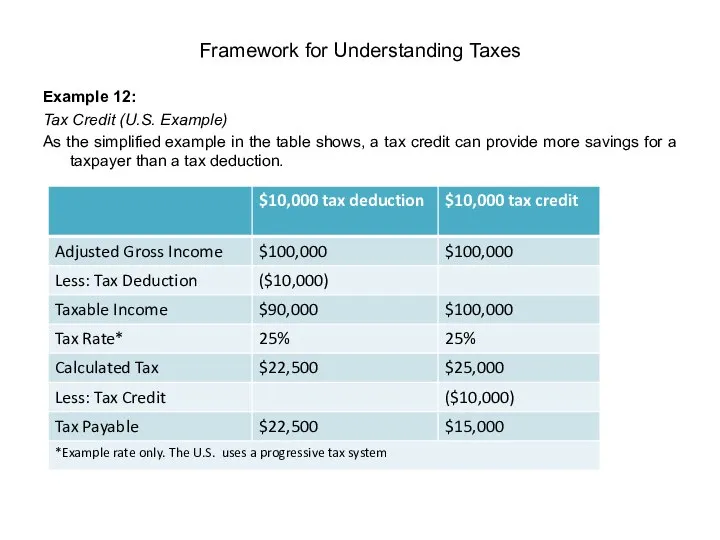

- 41. Example 12: Tax Credit (U.S. Example) As the simplified example in the table shows, a tax

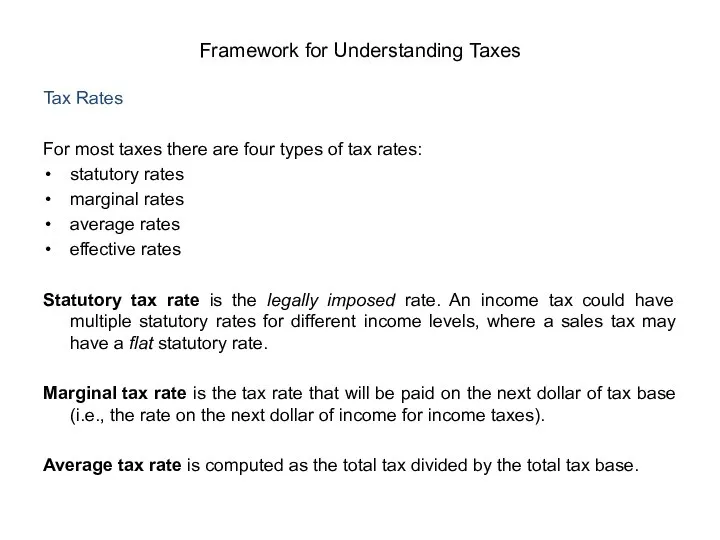

- 42. Tax Rates For most taxes there are four types of tax rates: statutory rates marginal rates

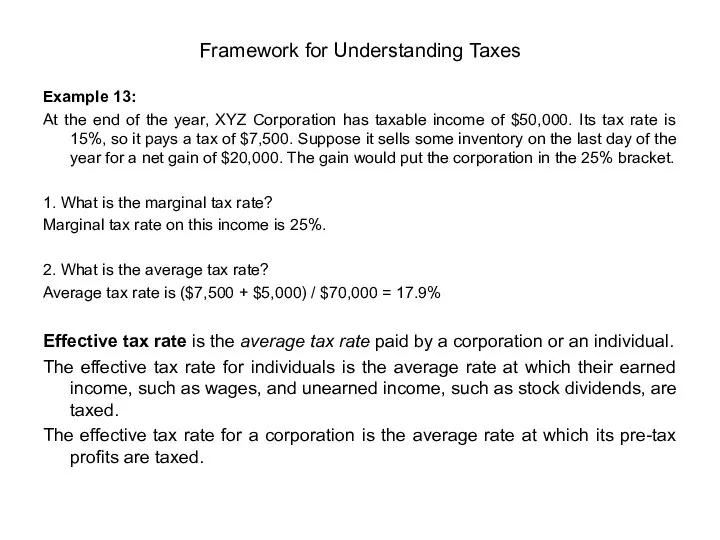

- 43. Example 13: At the end of the year, XYZ Corporation has taxable income of $50,000. Its

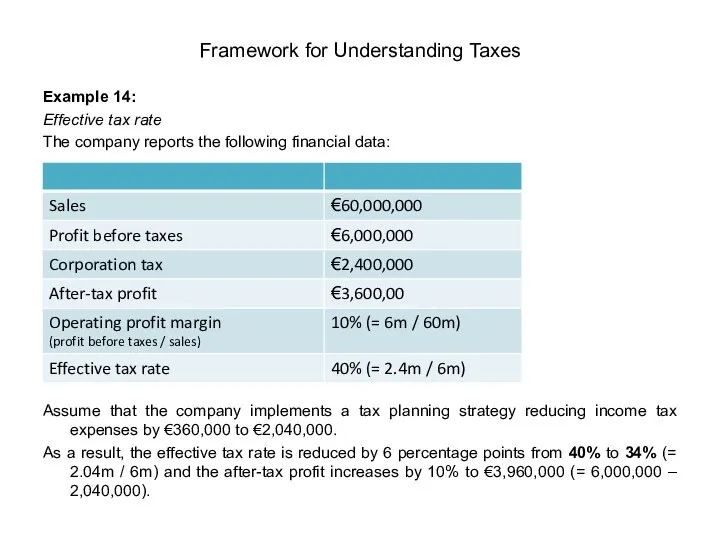

- 44. Example 14: Effective tax rate The company reports the following financial data: Assume that the company

- 45. Effective Tax Rate vs. Marginal Tax Rate The effective tax rate is a more accurate representation

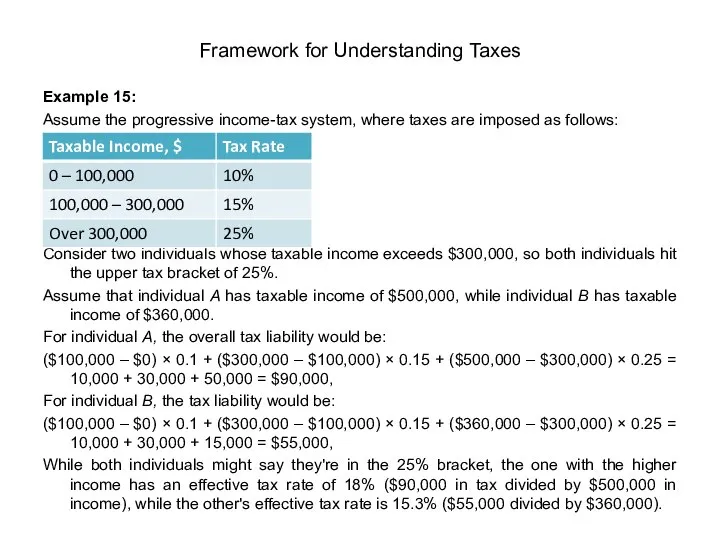

- 46. Example 15: Assume the progressive income-tax system, where taxes are imposed as follows: Consider two individuals

- 47. Tax Rate Structures In most tax jurisdictions, a tax rate structure applies to ordinary income (such

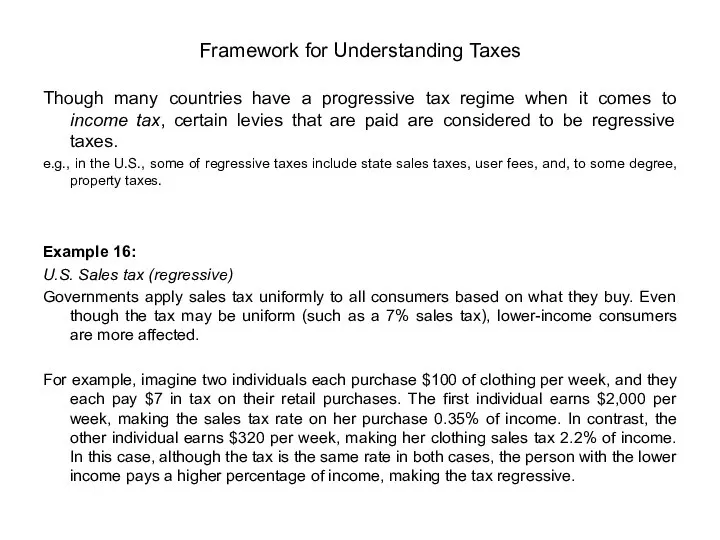

- 48. Though many countries have a progressive tax regime when it comes to income tax, certain levies

- 49. Example 17: U.S. User Fees (regressive) User fees levied by the U.S. government are another form

- 50. Other examples of regressive taxes Gambling taxes Those on low incomes have a high propensity to

- 51. A progressive tax system is one in which the average tax rate (taxes paid ÷ personal

- 52. Example 20: Calculation of Tax Due on Taxable Income (progressive tax structure) In a progressive rate

- 53. A proportional tax system (a.k.a., flat tax system) is the one in which a tax imposed

- 54. Important Principles and Concepts in Tax Law Most tax systems have developed around fundamental concepts that

- 55. Entity Principle Under the entity principle, an entity (such as a corporation) and its owners (for

- 56. Arm’s Length Principle The condition or the fact that the parties to a transaction are independent

- 57. Example 24: Arm’s Length Principle Assume that in Example 23 the corporation pays its entire $250,000

- 58. Example 25: Arm’s Length Test Assume that an entrepreneur sells an asset to his corporation, and

- 59. Arm’s Length Principle: Business Expenses Ordinary and necessary business expenses are deductible only to the extent

- 60. Example 27: Business Deductions Assume John hired four part-time employees and paid them $10 an hour

- 61. All-Inclusive Income Principle This principle basically means that if some simple tests are met, then receipt

- 62. Example 28: Realization Principle A corporation owns two assets that have gone up in value. It

- 63. Business Purpose Concept Relates to tax deductions. Here, business expenses are deductible only if they have

- 64. Tax-Benefit Rule Under the tax-benefit rule, if a taxpayer receives a refund of an item for

- 65. Substance over Form Doctrine Under the doctrine of substance over form, even when the form of

- 66. Pay-As-You-Earn Concept (PAYE) Taxpayers must pay part of their estimated annual tax liability throughout the year,

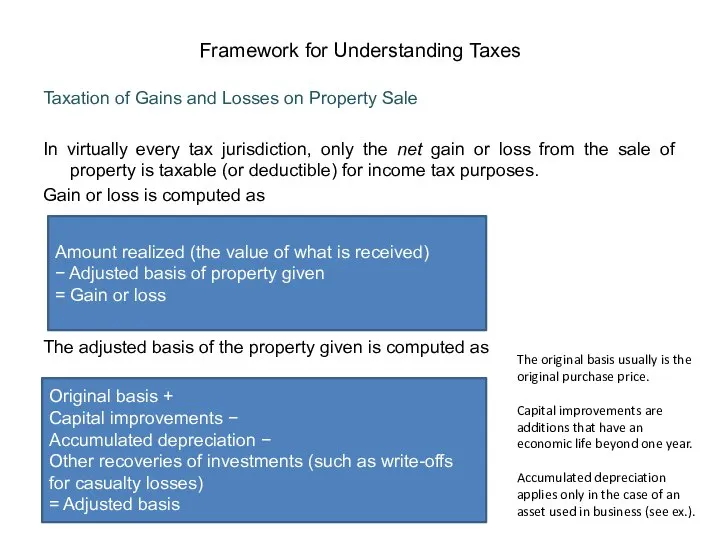

- 67. Taxation of Gains and Losses on Property Sale In virtually every tax jurisdiction, only the net

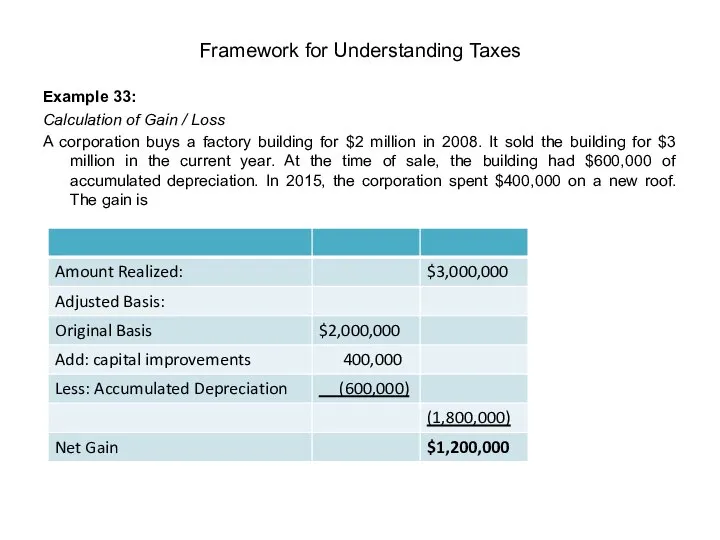

- 68. Example 33: Calculation of Gain / Loss A corporation buys a factory building for $2 million

- 69. Chapter 3: PERSONAL INCOME TAX Definition of Personal Income Tax According to OECD, tax on personal

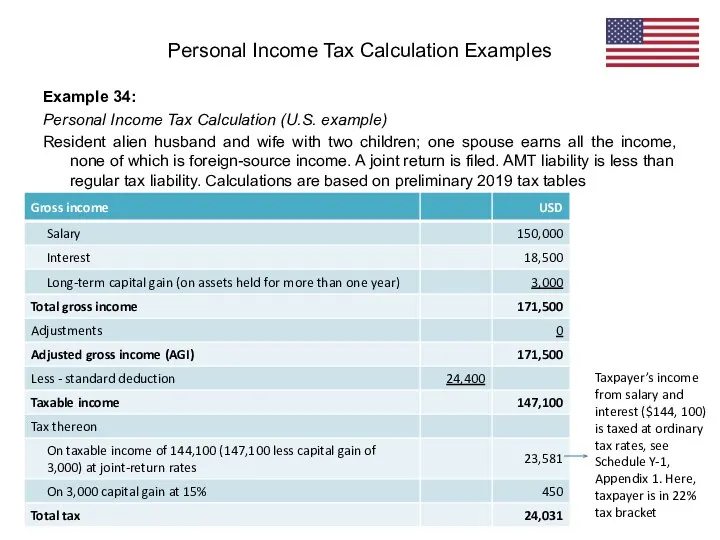

- 70. Example 34: Personal Income Tax Calculation (U.S. example) Resident alien husband and wife with two children;

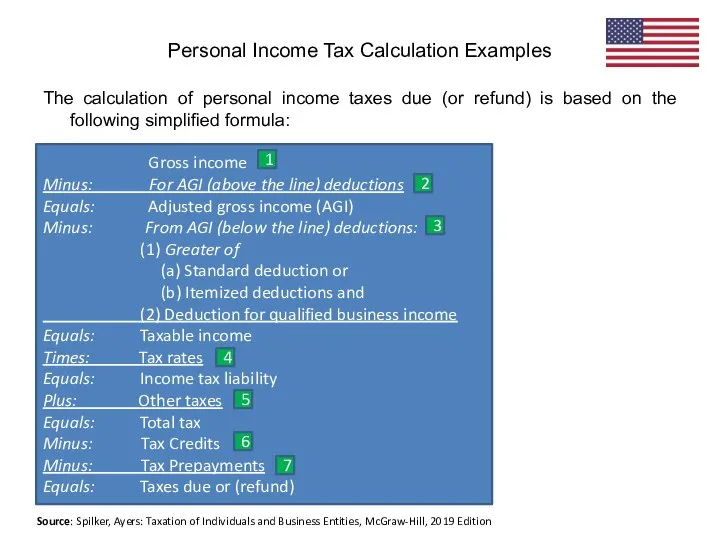

- 71. The calculation of personal income taxes due (or refund) is based on the following simplified formula:

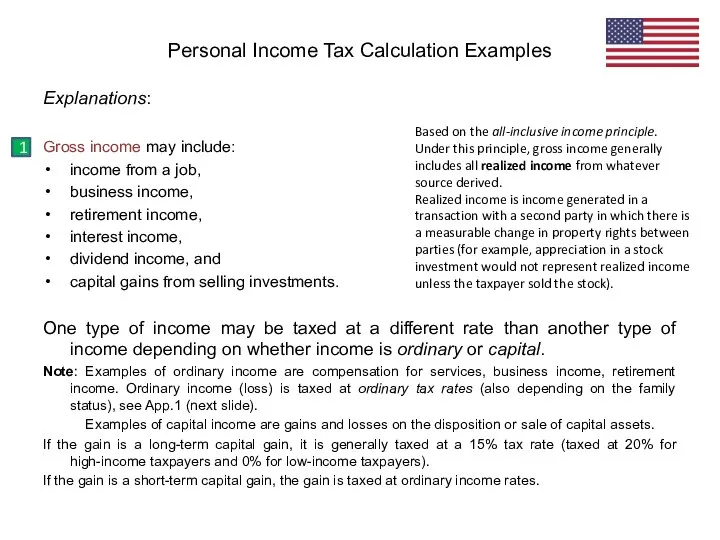

- 72. Explanations: Gross income may include: income from a job, business income, retirement income, interest income, dividend

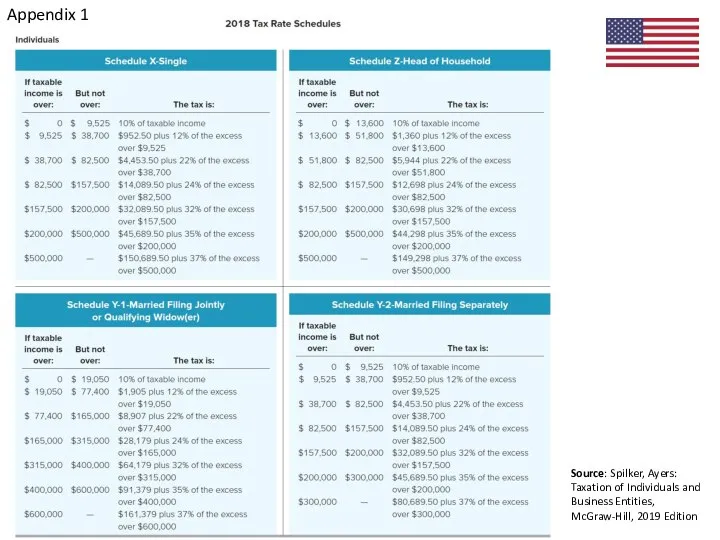

- 73. Appendix 1 Source: Spilker, Ayers: Taxation of Individuals and Business Entities, McGraw-Hill, 2019 Edition

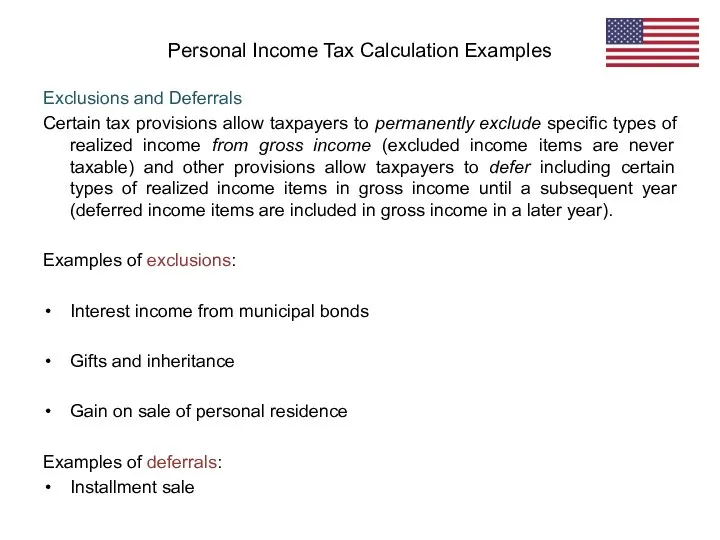

- 74. Exclusions and Deferrals Certain tax provisions allow taxpayers to permanently exclude specific types of realized income

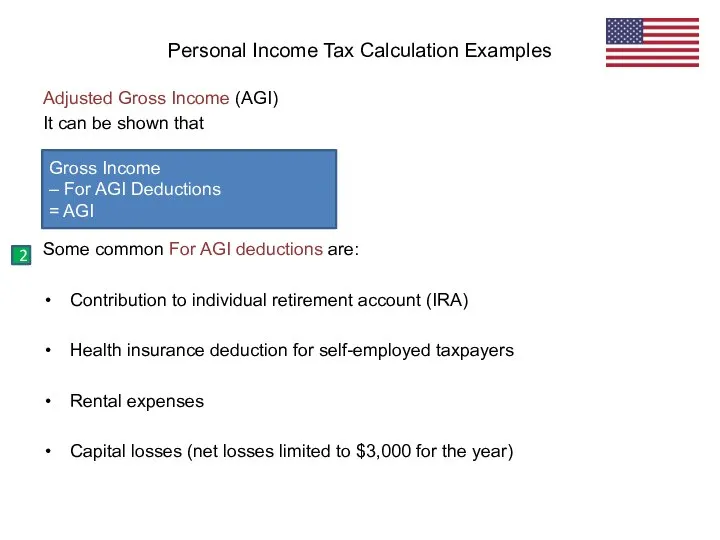

- 75. Adjusted Gross Income (AGI) It can be shown that Some common For AGI deductions are: Contribution

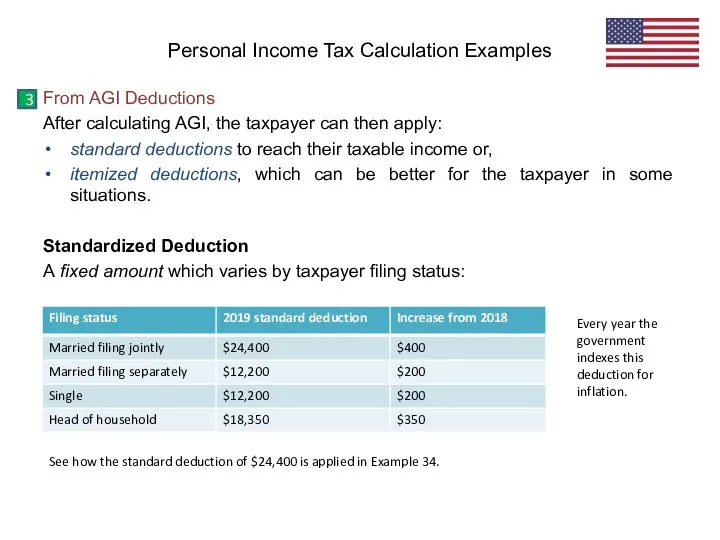

- 76. From AGI Deductions After calculating AGI, the taxpayer can then apply: standard deductions to reach their

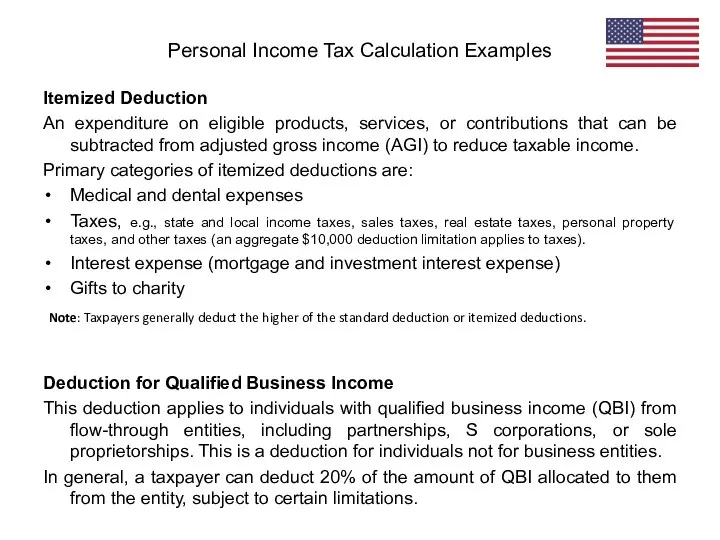

- 77. Itemized Deduction An expenditure on eligible products, services, or contributions that can be subtracted from adjusted

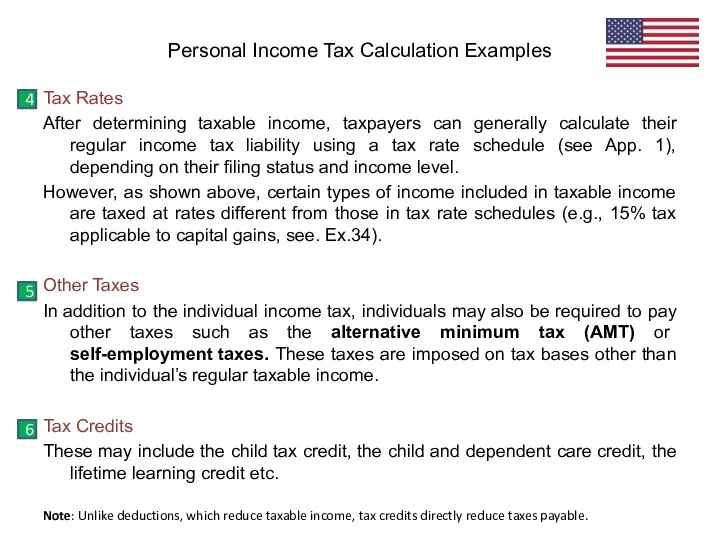

- 78. Tax Rates After determining taxable income, taxpayers can generally calculate their regular income tax liability using

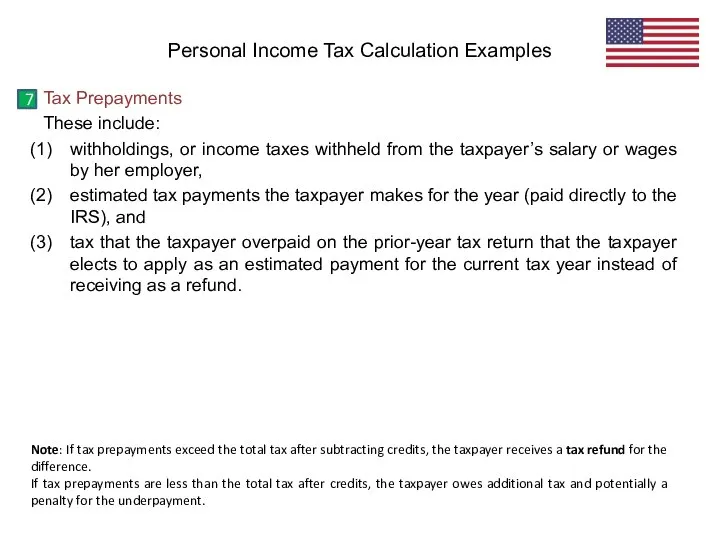

- 79. Tax Prepayments These include: withholdings, or income taxes withheld from the taxpayer’s salary or wages by

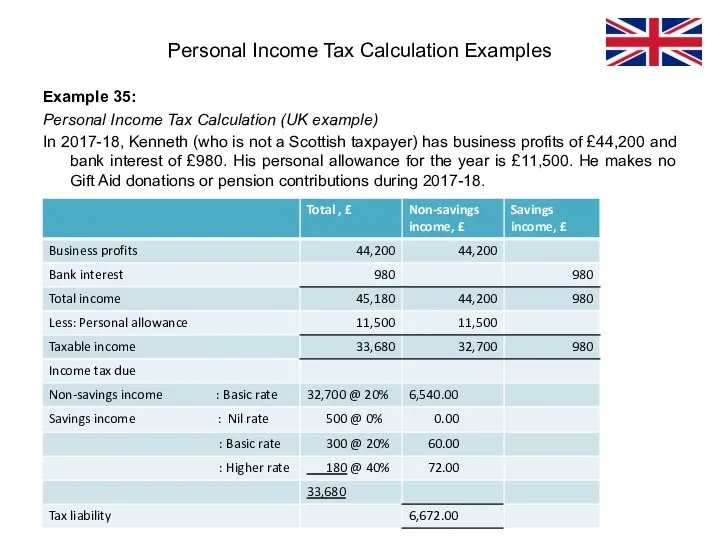

- 80. Example 35: Personal Income Tax Calculation (UK example) In 2017-18, Kenneth (who is not a Scottish

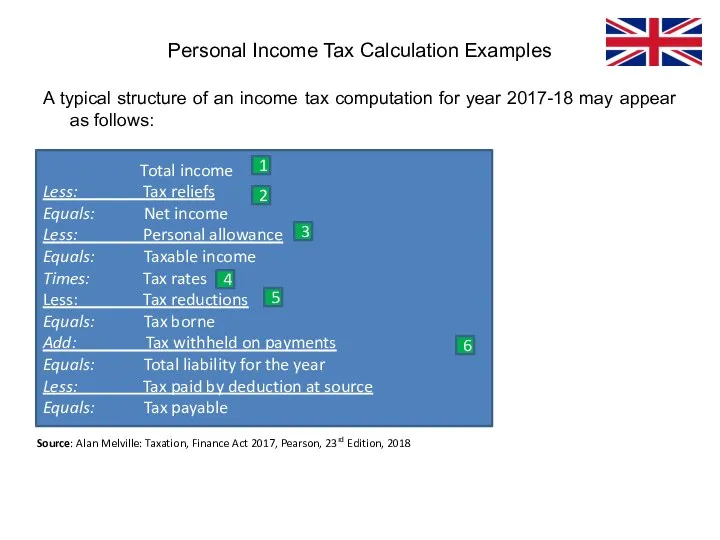

- 81. A typical structure of an income tax computation for year 2017-18 may appear as follows: Personal

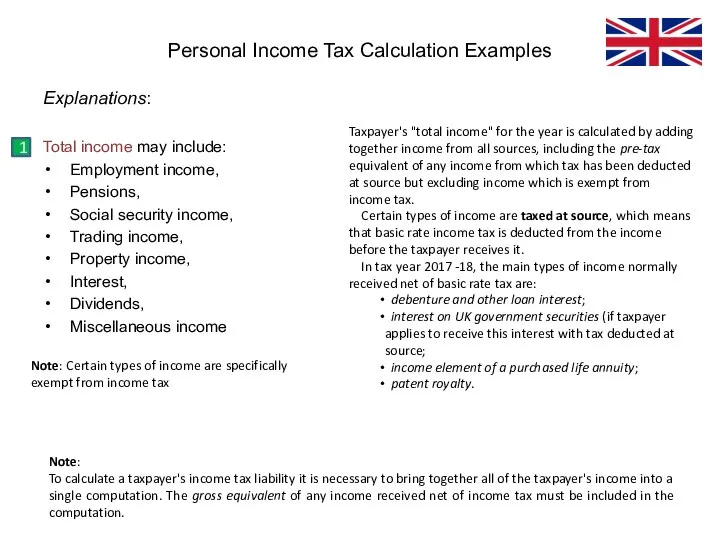

- 82. Explanations: Total income may include: Employment income, Pensions, Social security income, Trading income, Property income, Interest,

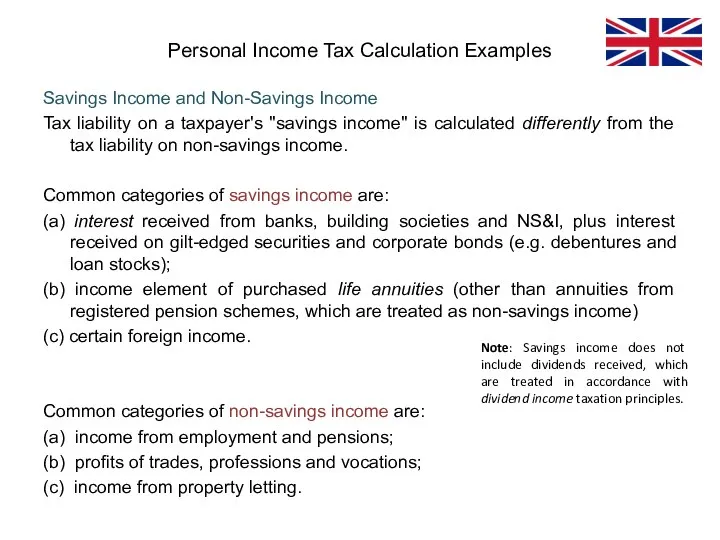

- 83. Savings Income and Non-Savings Income Tax liability on a taxpayer's "savings income" is calculated differently from

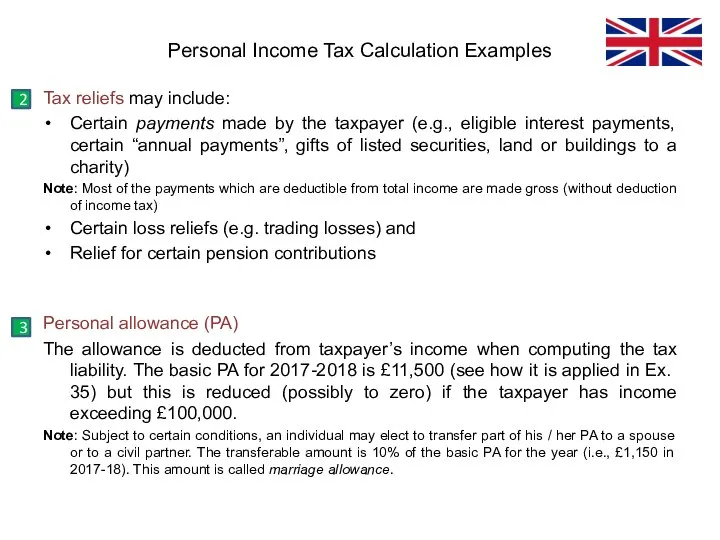

- 84. Tax reliefs may include: Certain payments made by the taxpayer (e.g., eligible interest payments, certain “annual

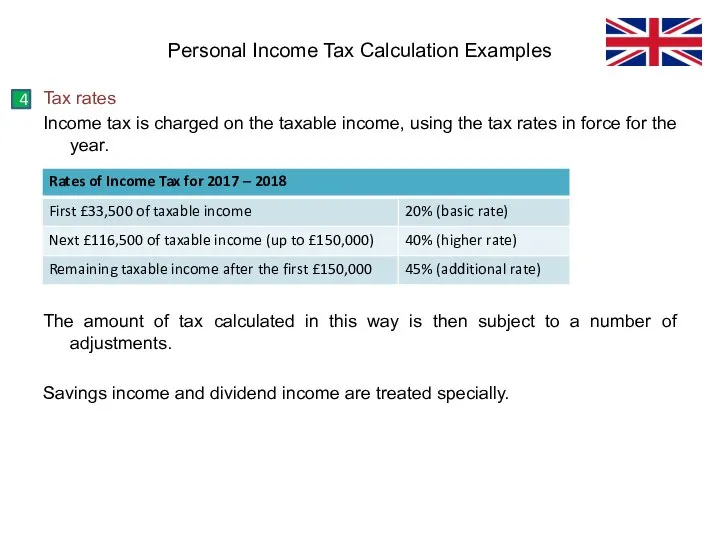

- 85. Tax rates Income tax is charged on the taxable income, using the tax rates in force

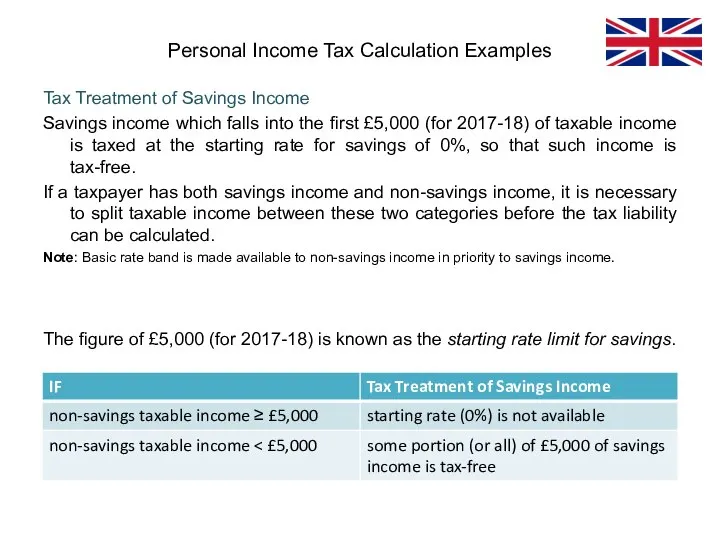

- 86. Tax Treatment of Savings Income Savings income which falls into the first £5,000 (for 2017-18) of

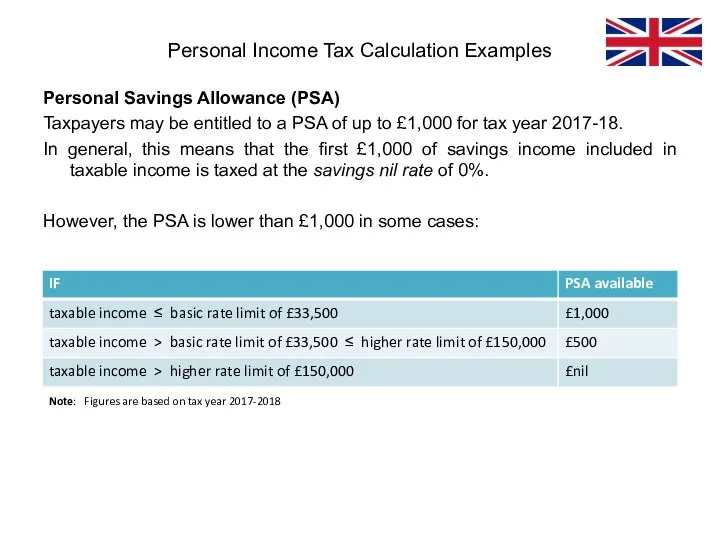

- 87. Personal Savings Allowance (PSA) Taxpayers may be entitled to a PSA of up to £1,000 for

- 88. Example 36: Personal Income Tax Calculation (UK example) In 2017-18, Robert has business profits of £39,700

- 89. Example 37: Personal Income Tax Calculation (UK example) In 2017-18, Roberta has rental income of £15,700

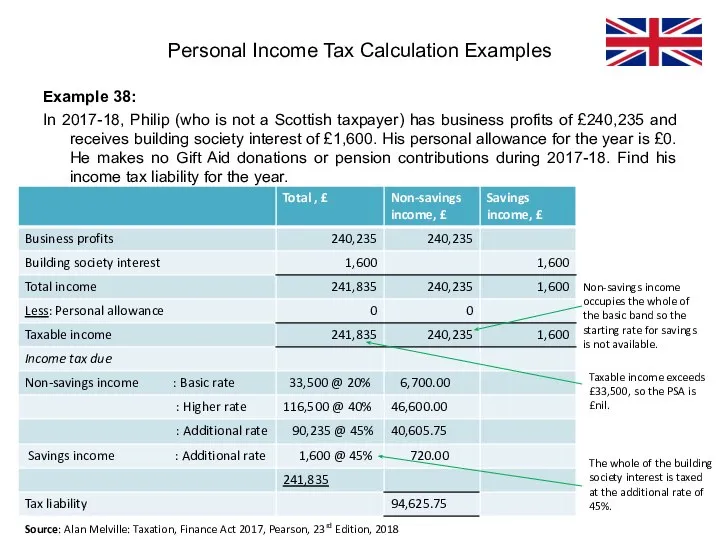

- 90. Example 38: In 2017-18, Philip (who is not a Scottish taxpayer) has business profits of £240,235

- 91. Chapter 4: TAXATION OF INVESTMENT INCOME Definition of Investment Income Investment income is income that comes

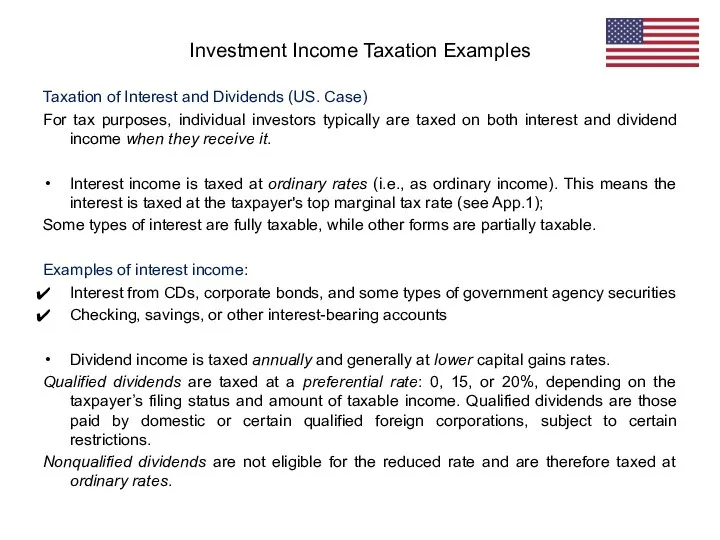

- 92. Taxation of Interest and Dividends (US. Case) For tax purposes, individual investors typically are taxed on

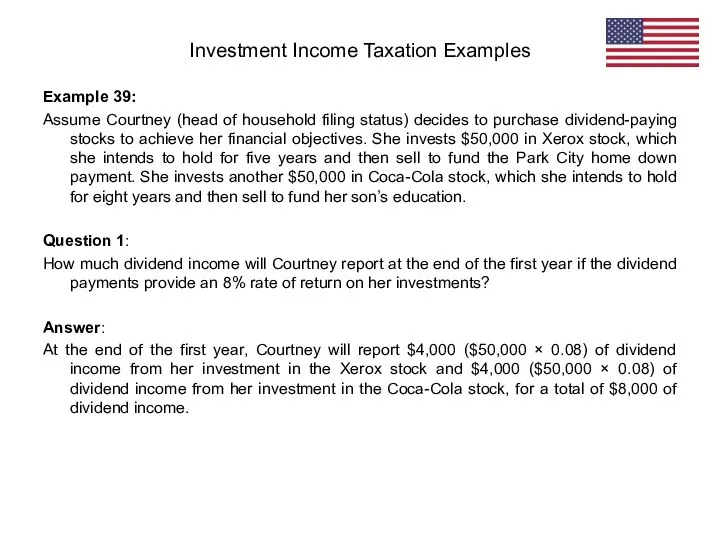

- 93. Example 39: Assume Courtney (head of household filing status) decides to purchase dividend-paying stocks to achieve

- 94. Example 39: Assume Courtney (head of household filing status) decides to purchase dividend-paying stocks to achieve

- 95. Example 39: Assume Courtney (head of household filing status) decides to purchase dividend-paying stocks to achieve

- 96. Taxation of Capital Gains and Losses (US. Case) A capital gains tax is a tax on

- 97. FIFO method and Specific Identification Method When taxpayers sell a capital asset, e.g., stock, they may

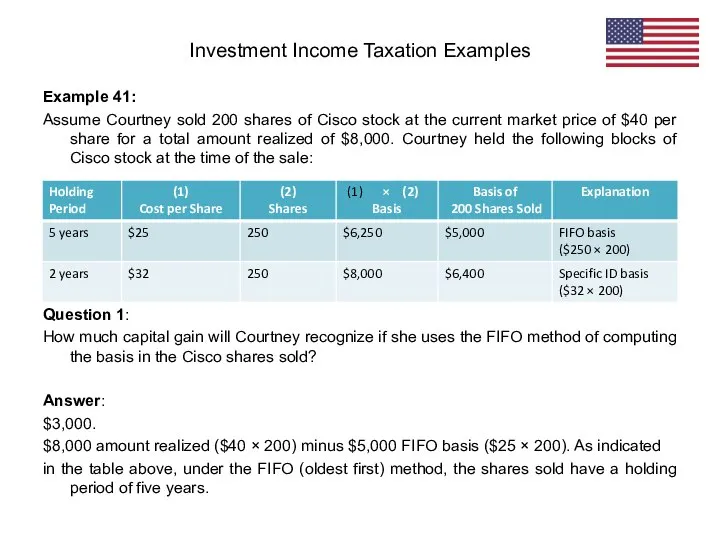

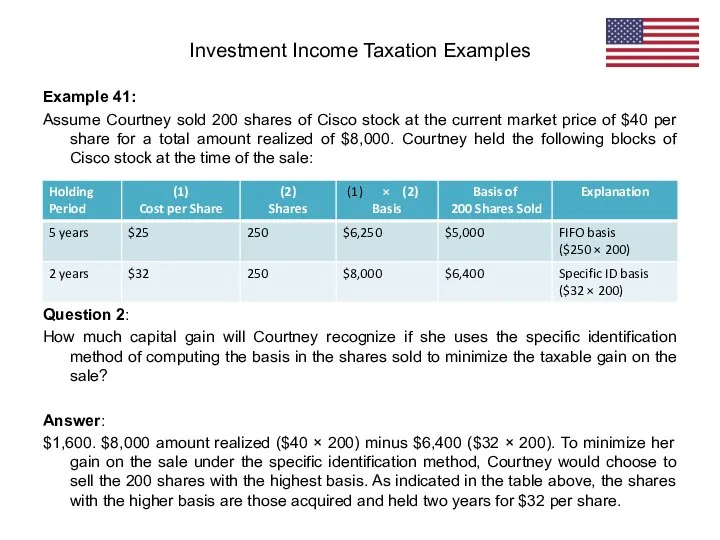

- 98. Example 41: Assume Courtney sold 200 shares of Cisco stock at the current market price of

- 99. Example 41: Assume Courtney sold 200 shares of Cisco stock at the current market price of

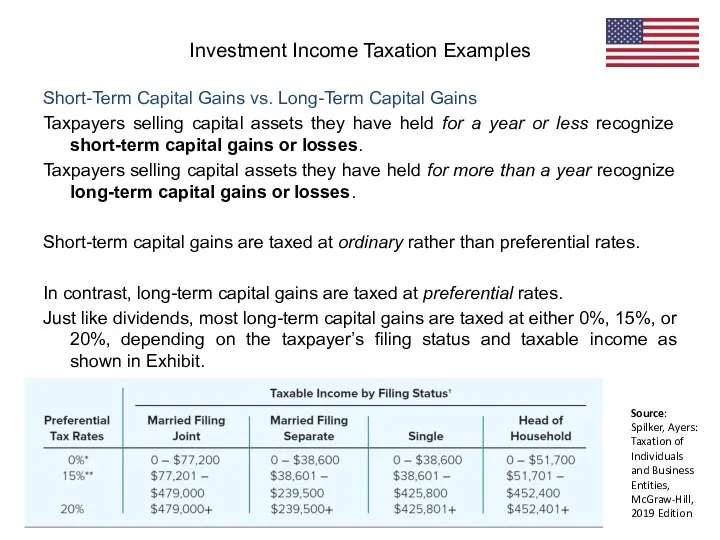

- 100. Short-Term Capital Gains vs. Long-Term Capital Gains Taxpayers selling capital assets they have held for a

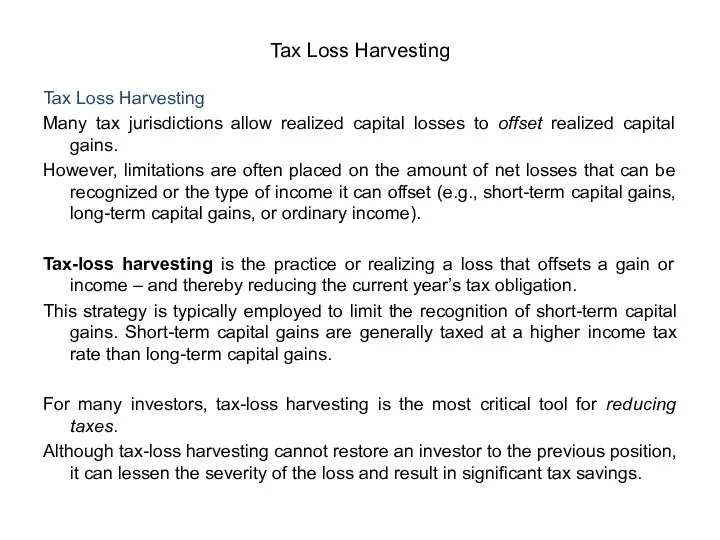

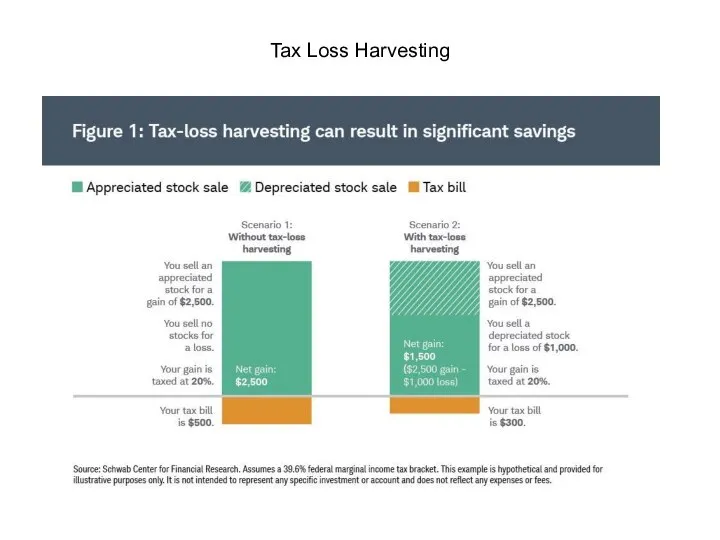

- 101. Tax Loss Harvesting Many tax jurisdictions allow realized capital losses to offset realized capital gains. However,

- 102. Tax Loss Harvesting Example 41a: Eduardo has a €1,000,000 portfolio held in a taxable account. The

- 103. Tax Loss Harvesting Example 41a: Eduardo has a €1,000,000 portfolio held in a taxable account. The

- 104. Tax Loss Harvesting

- 105. Taxation of Interest and Dividends (UK Case) Interest received by a taxpayer is charged to income

- 106. Example 42: In 2017-18, Alfred had business profits of £15,870 and received net debenture interest of

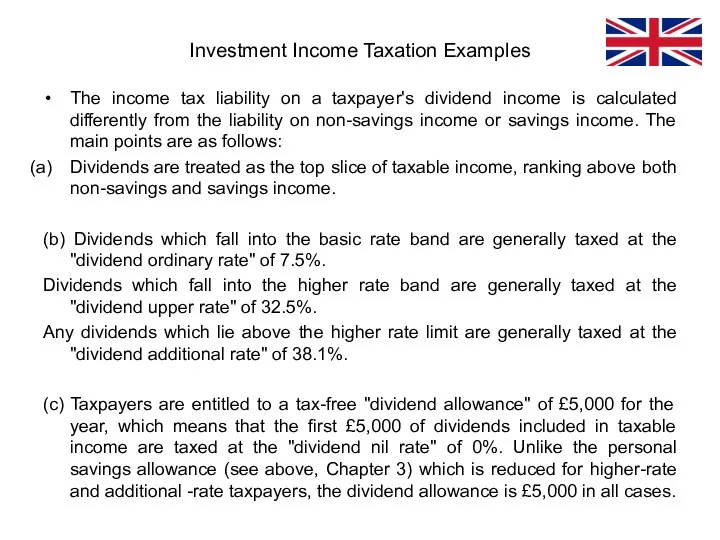

- 107. The income tax liability on a taxpayer's dividend income is calculated differently from the liability on

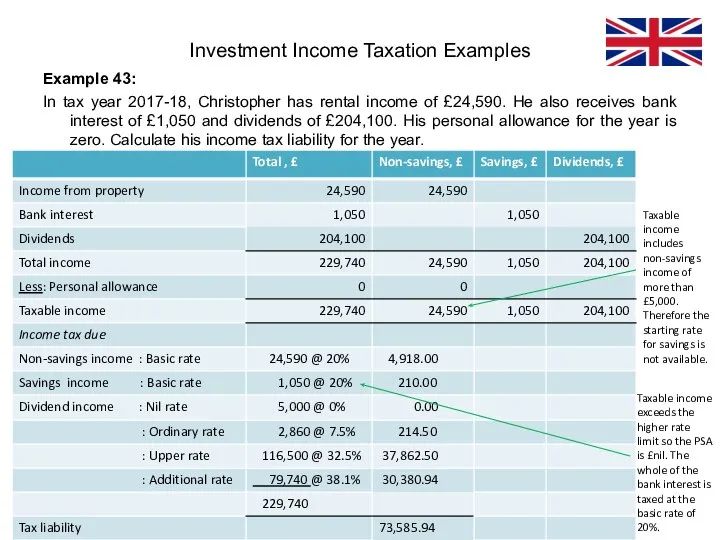

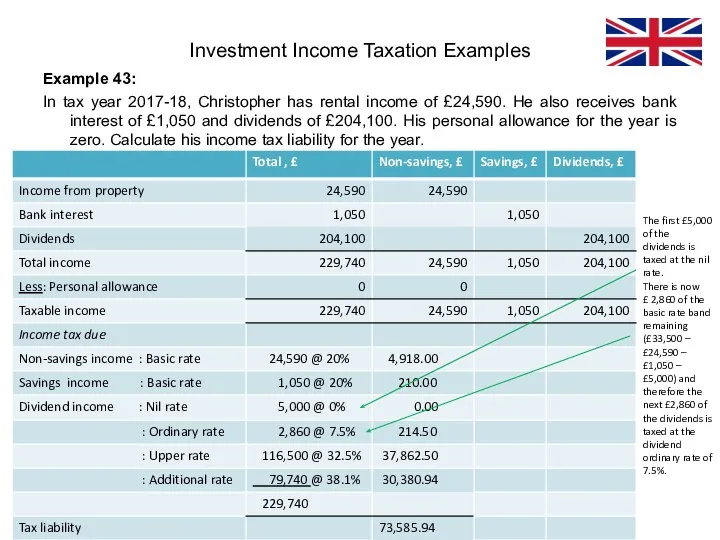

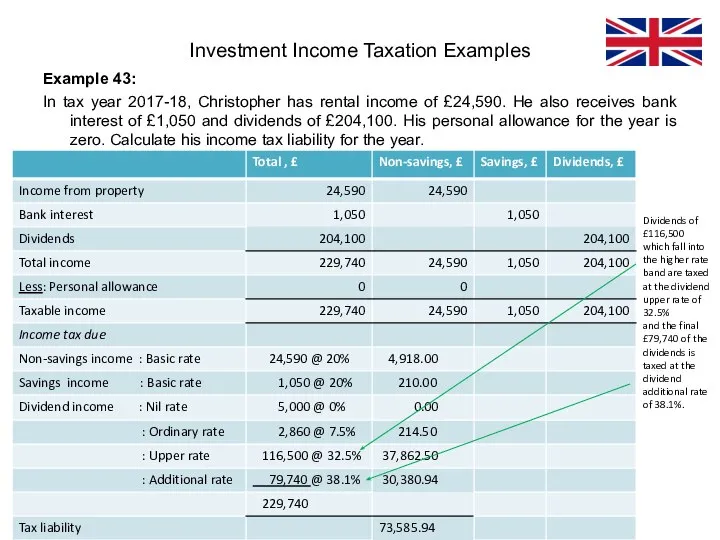

- 108. Example 43: In tax year 2017-18, Christopher has rental income of £24,590. He also receives bank

- 109. Example 43: In tax year 2017-18, Christopher has rental income of £24,590. He also receives bank

- 110. Example 43: In tax year 2017-18, Christopher has rental income of £24,590. He also receives bank

- 111. Capital Gains Tax (UK Case) For tax year 2017-18, there are two main rates of capital

- 112. Capital Gains Tax: Basis of Assessment A person's CGT liability for a tax year is based

- 113. (c) If there are net gains for the year, these are reduced first by any unrelieved

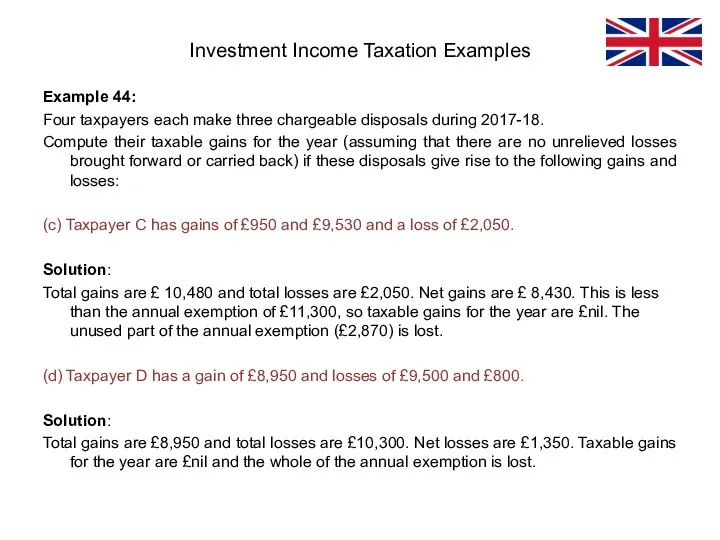

- 114. Example 44: Four taxpayers each make three chargeable disposals during 2017-18. Compute their taxable gains for

- 115. Example 44: Four taxpayers each make three chargeable disposals during 2017-18. Compute their taxable gains for

- 116. Calculation of Capital Gains Tax Payable CGT rates are applied to the taxable gains which remain

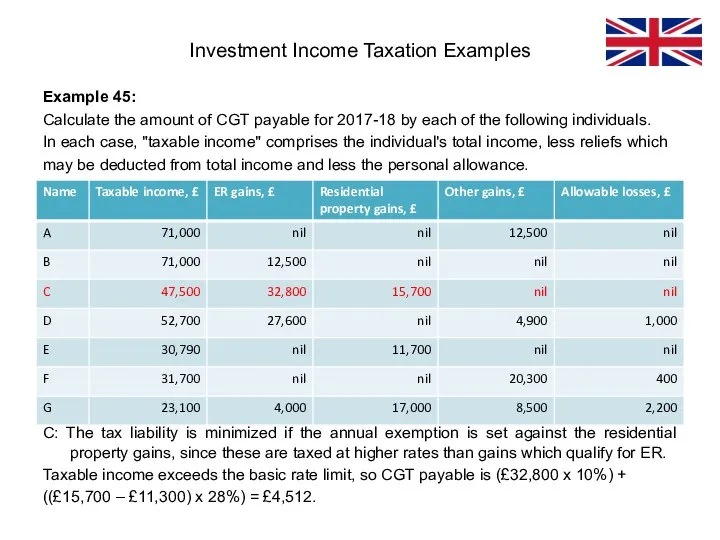

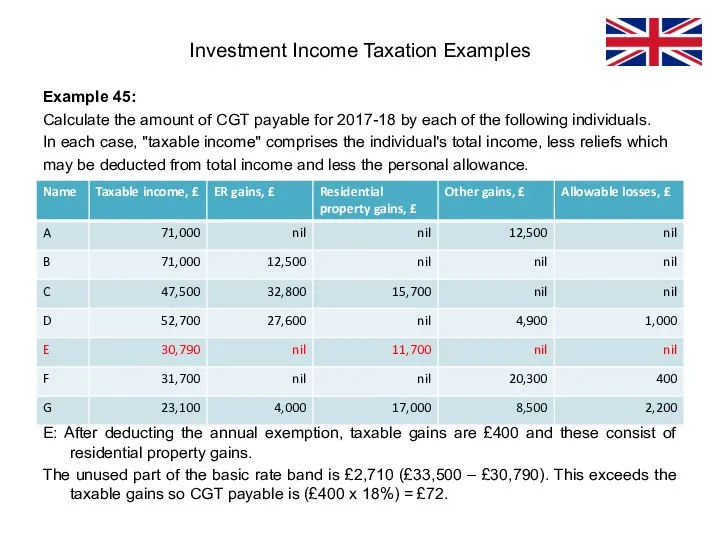

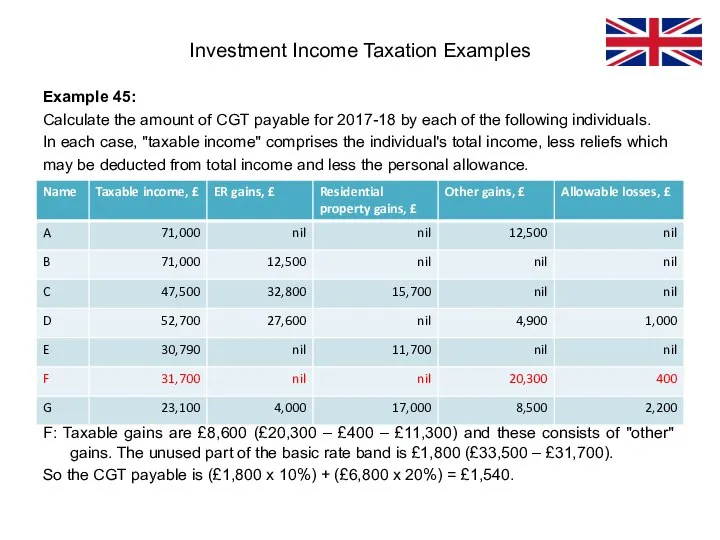

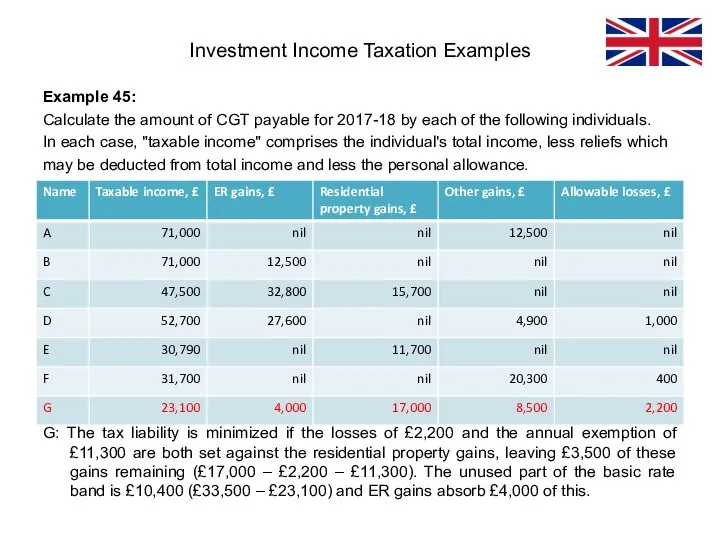

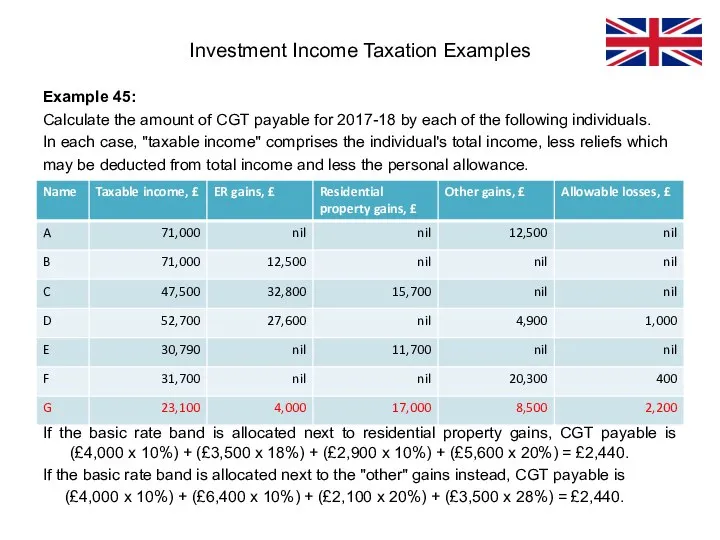

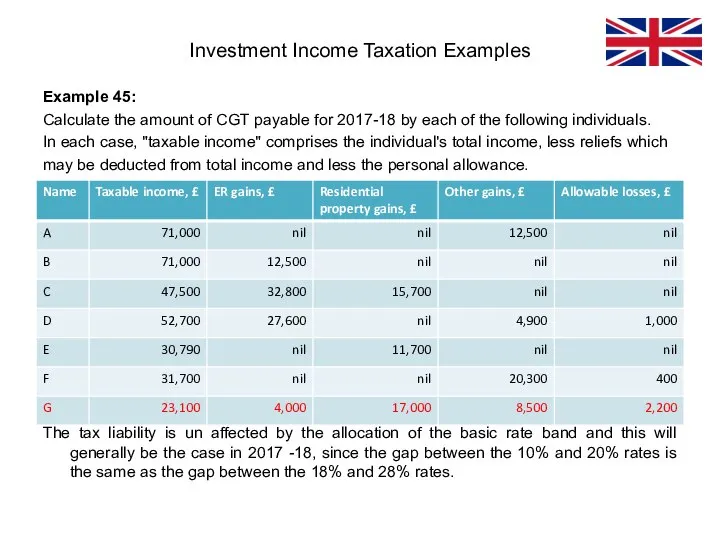

- 117. Example 45: Calculate the amount of CGT payable for 2017-18 by each of the following individuals.

- 118. Example 45: Calculate the amount of CGT payable for 2017-18 by each of the following individuals.

- 119. Example 45: Calculate the amount of CGT payable for 2017-18 by each of the following individuals.

- 120. Example 45: Calculate the amount of CGT payable for 2017-18 by each of the following individuals.

- 121. Example 45: Calculate the amount of CGT payable for 2017-18 by each of the following individuals.

- 122. Example 45: Calculate the amount of CGT payable for 2017-18 by each of the following individuals.

- 123. Example 45: Calculate the amount of CGT payable for 2017-18 by each of the following individuals.

- 124. Example 45: Calculate the amount of CGT payable for 2017-18 by each of the following individuals.

- 125. Example 45: Calculate the amount of CGT payable for 2017-18 by each of the following individuals.

- 126. Effect of Taxes on Investment Returns After-Tax Accumulations and Returns for Taxable Accounts Taxes on investment

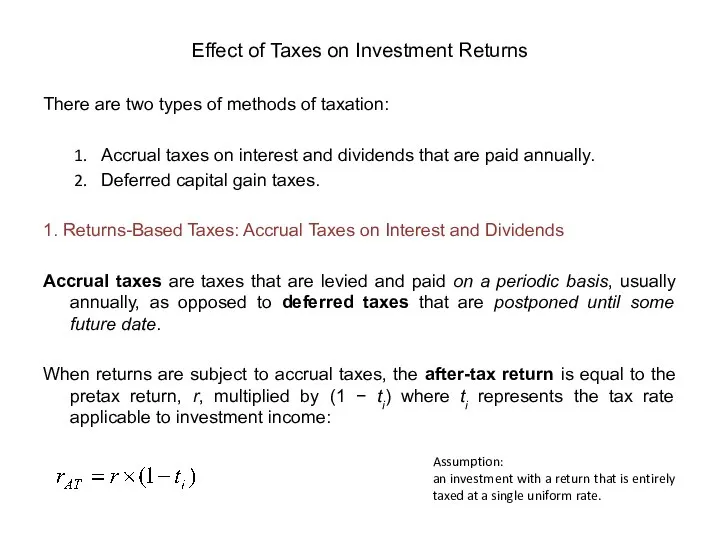

- 127. Effect of Taxes on Investment Returns There are two types of methods of taxation: Accrual taxes

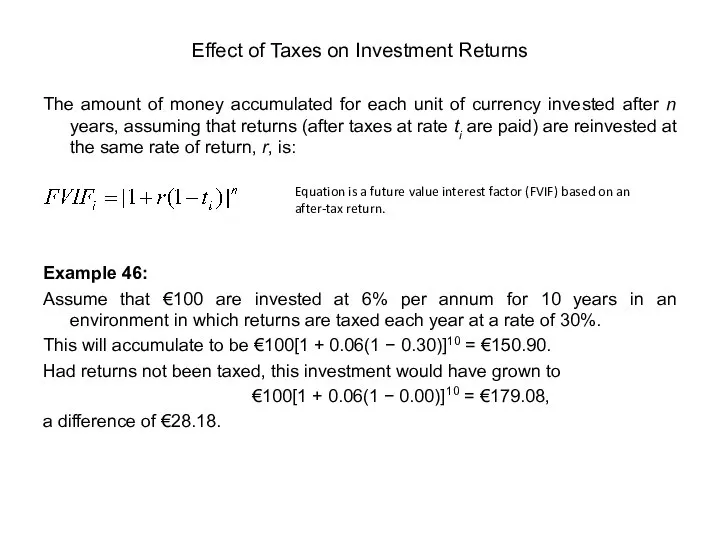

- 128. Effect of Taxes on Investment Returns The amount of money accumulated for each unit of currency

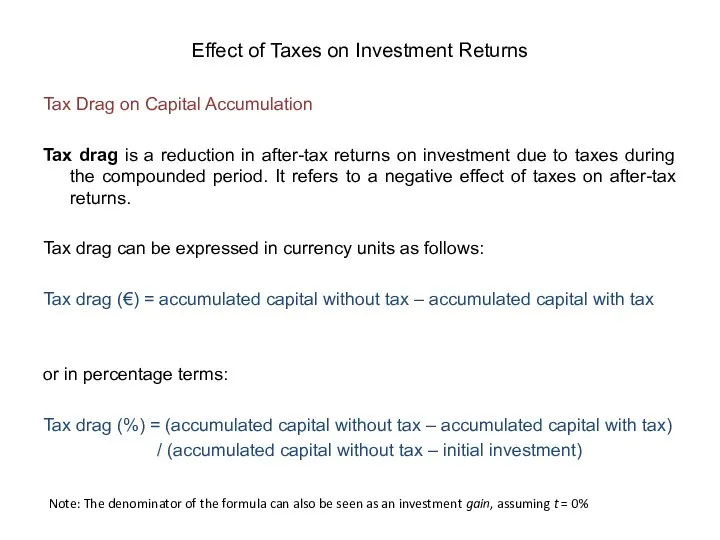

- 129. Effect of Taxes on Investment Returns Tax Drag on Capital Accumulation Tax drag is a reduction

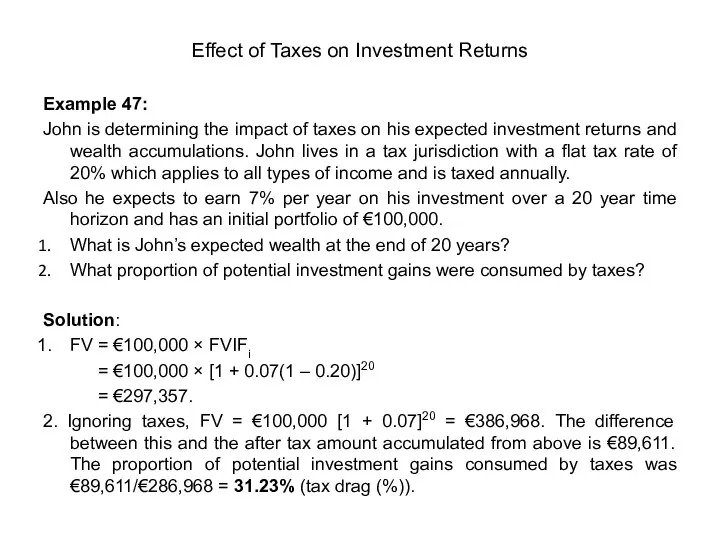

- 130. Effect of Taxes on Investment Returns Example 47: John is determining the impact of taxes on

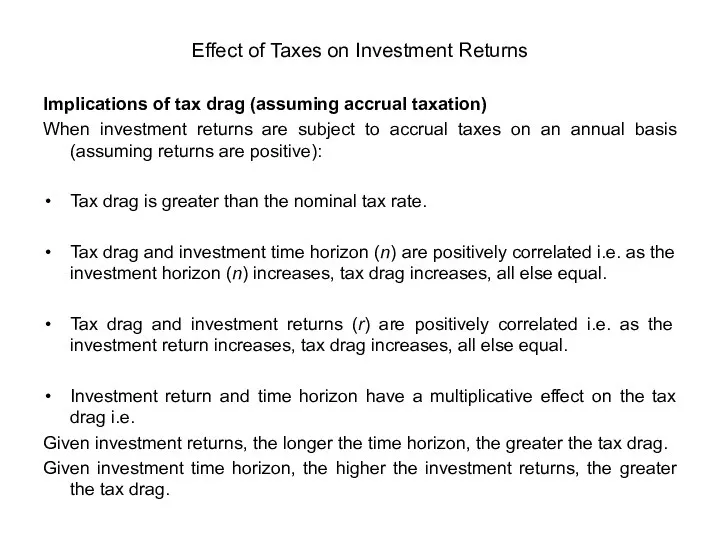

- 131. Effect of Taxes on Investment Returns Implications of tax drag (assuming accrual taxation) When investment returns

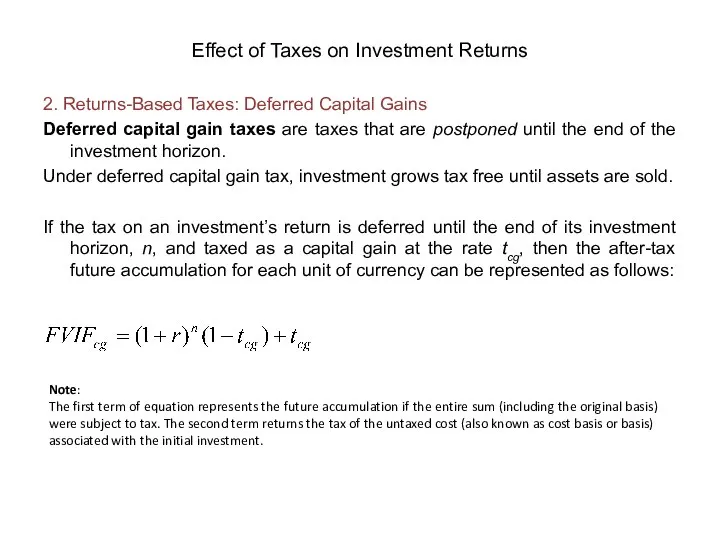

- 132. Effect of Taxes on Investment Returns 2. Returns-Based Taxes: Deferred Capital Gains Deferred capital gain taxes

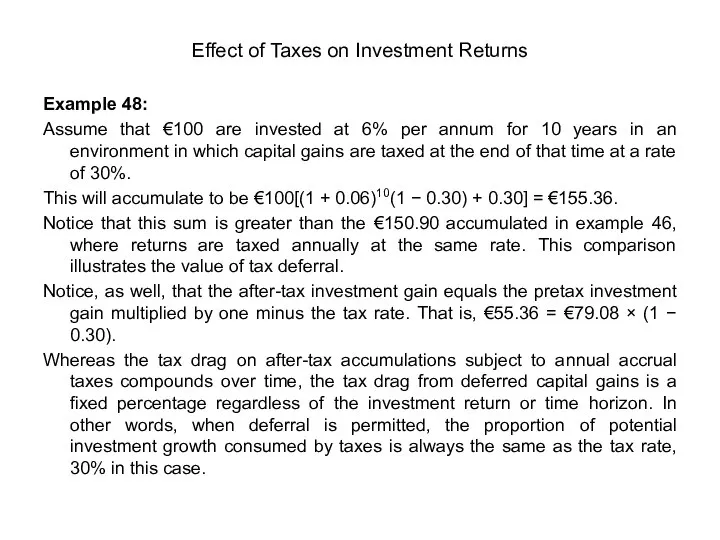

- 133. Effect of Taxes on Investment Returns Example 48: Assume that €100 are invested at 6% per

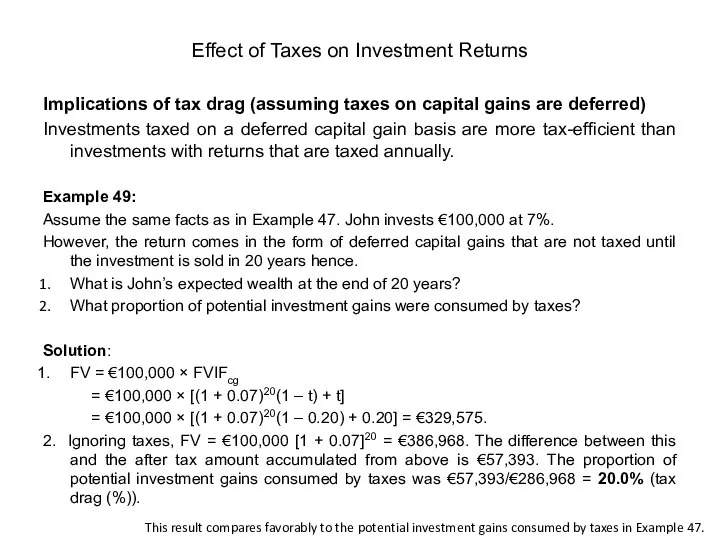

- 134. Effect of Taxes on Investment Returns Implications of tax drag (assuming taxes on capital gains are

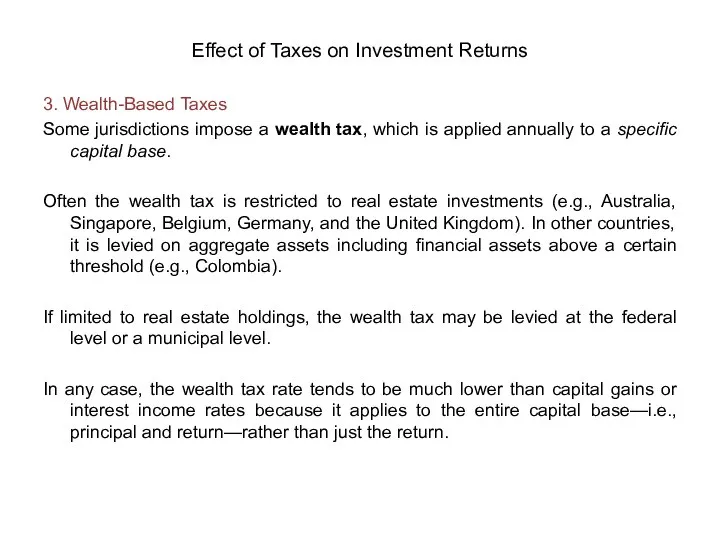

- 135. Effect of Taxes on Investment Returns 3. Wealth-Based Taxes Some jurisdictions impose a wealth tax, which

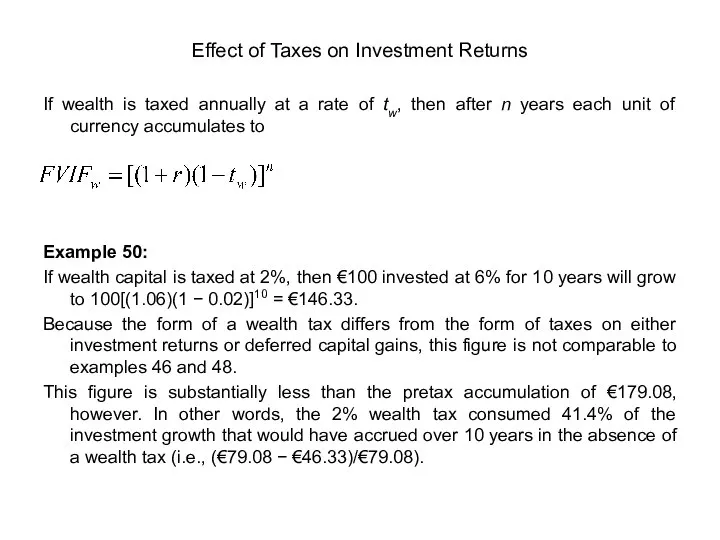

- 136. Effect of Taxes on Investment Returns If wealth is taxed annually at a rate of tw,

- 137. Effect of Taxes on Investment Returns Implications of tax drag (assuming tax on wealth) Tax drag

- 138. Effect of Taxes on Investment Returns Example 51: Olga lives in a country that imposes a

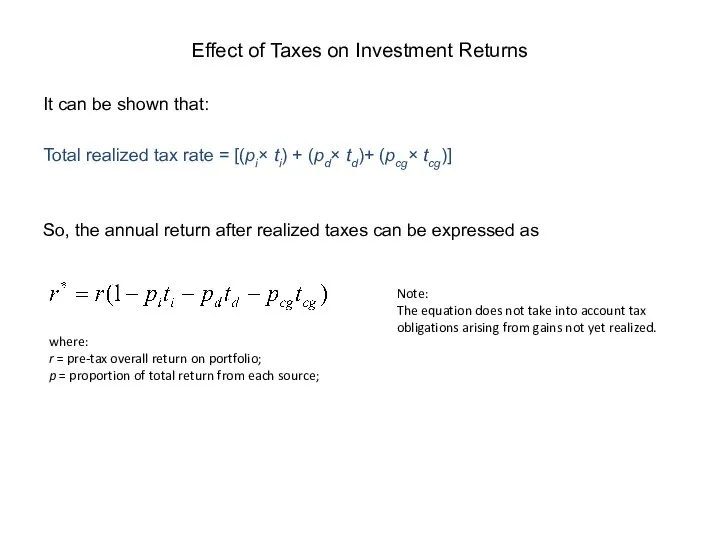

- 139. Effect of Taxes on Investment Returns Blended Taxing Environments In reality, investment portfolios are subject to

- 140. Effect of Taxes on Investment Returns It can be shown that: Total realized tax rate =

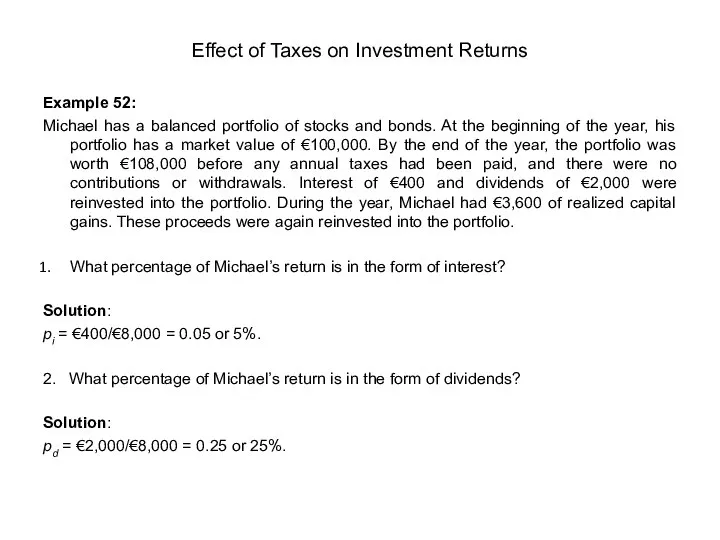

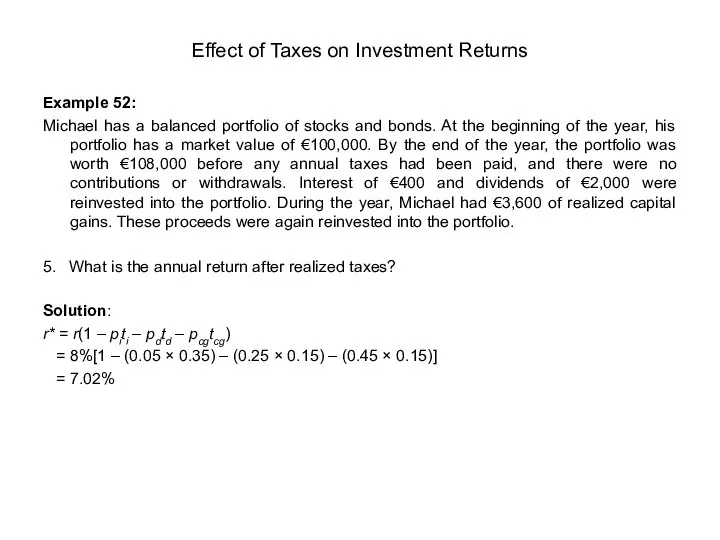

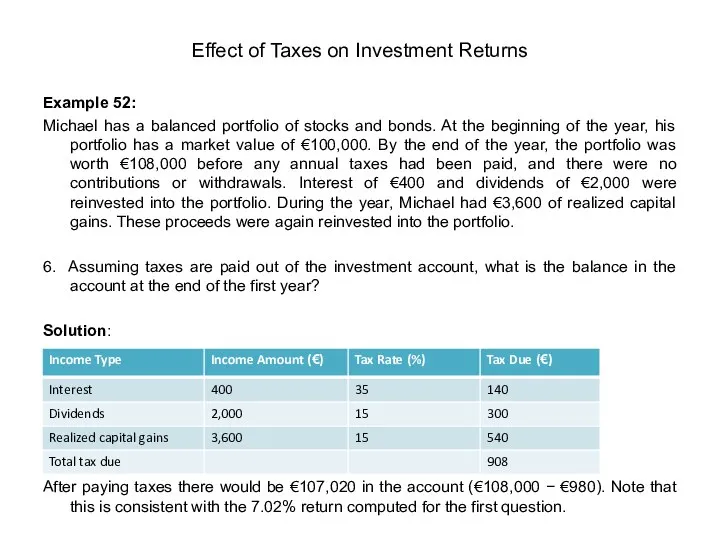

- 141. Effect of Taxes on Investment Returns Example 52: Michael has a balanced portfolio of stocks and

- 142. Effect of Taxes on Investment Returns Example 52: Michael has a balanced portfolio of stocks and

- 143. Effect of Taxes on Investment Returns Example 52: Michael has a balanced portfolio of stocks and

- 144. Effect of Taxes on Investment Returns Example 52: Michael has a balanced portfolio of stocks and

- 145. Chapter 5: CORPORATION TAX Definition of Corporate Tax Corporate tax (a.k.a. corporation tax) is a direct

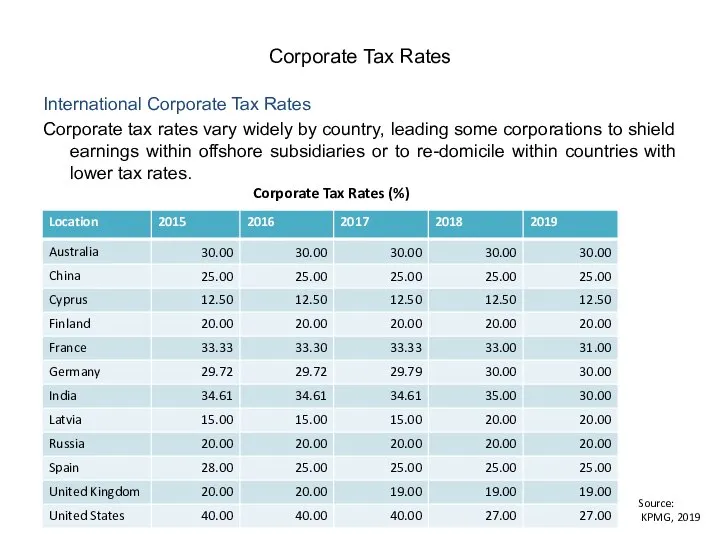

- 146. Corporate Tax Rates International Corporate Tax Rates Corporate tax rates vary widely by country, leading some

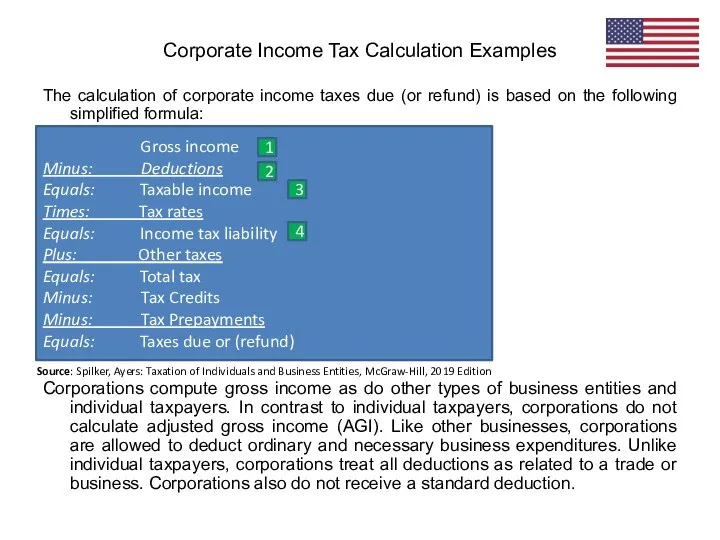

- 147. The calculation of corporate income taxes due (or refund) is based on the following simplified formula:

- 148. Explanations: Gross income may include: gross profit from inventory sales (sales minus cost of goods sold),

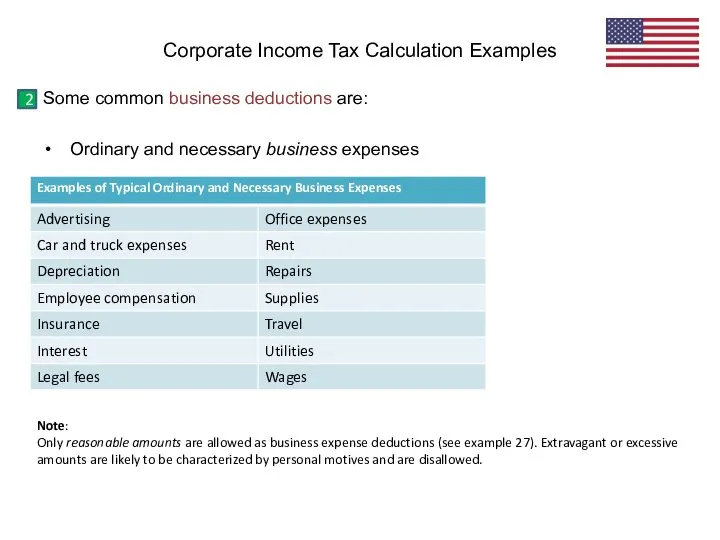

- 149. Some common business deductions are: Ordinary and necessary business expenses Corporate Income Tax Calculation Examples 2

- 150. Some limitations on business deductions: Capital expenditures (e.g., expenditures for tangible assets such as buildings, machinery,

- 151. Business interest expense Deduction for business interest expense is limited to the sum of business interest

- 152. Computing corporate taxable income To compute taxable income, most corporations begin with book (financial reporting) income

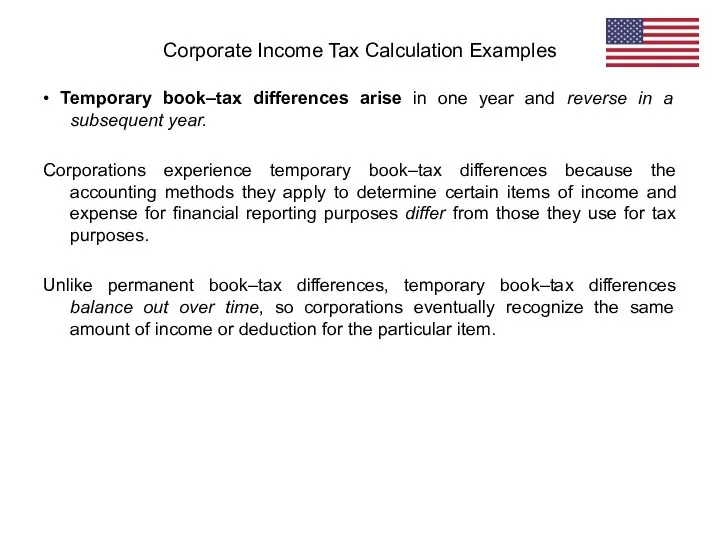

- 153. In addition to the favorable/unfavorable distinction, book–tax differences can be categorized as permanent or temporary. •

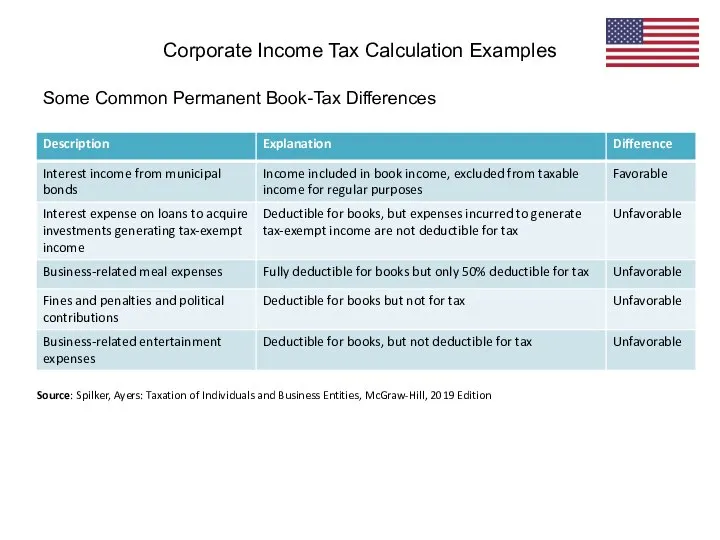

- 154. Some Common Permanent Book-Tax Differences Corporate Income Tax Calculation Examples Source: Spilker, Ayers: Taxation of Individuals

- 155. • Temporary book–tax differences arise in one year and reverse in a subsequent year. Corporations experience

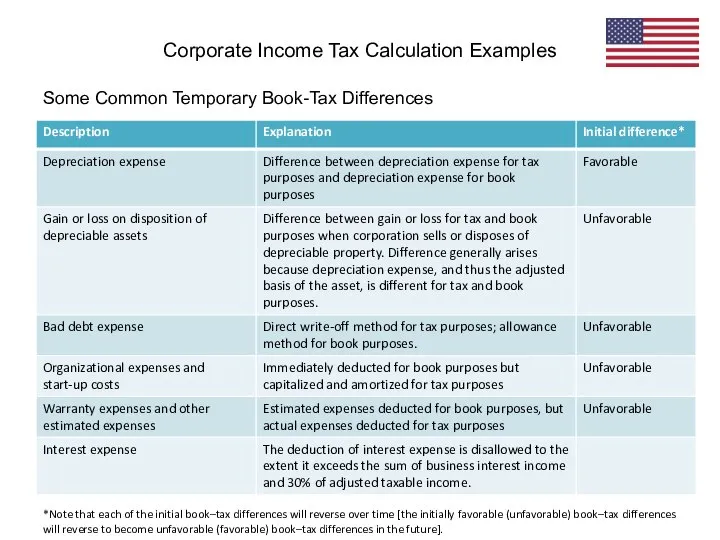

- 156. Some Common Temporary Book-Tax Differences Corporate Income Tax Calculation Examples *Note that each of the initial

- 157. Corporate-Specific Deductions and Book-Tax Differences Net Capital Losses For corporations, all net capital gains (long- and

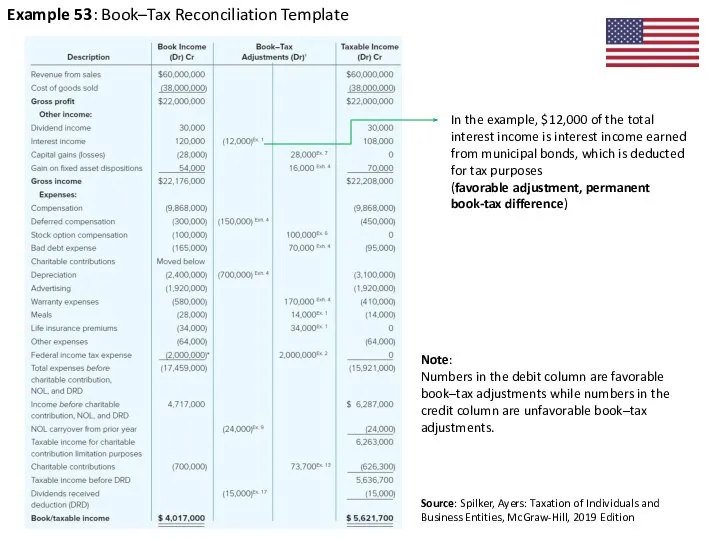

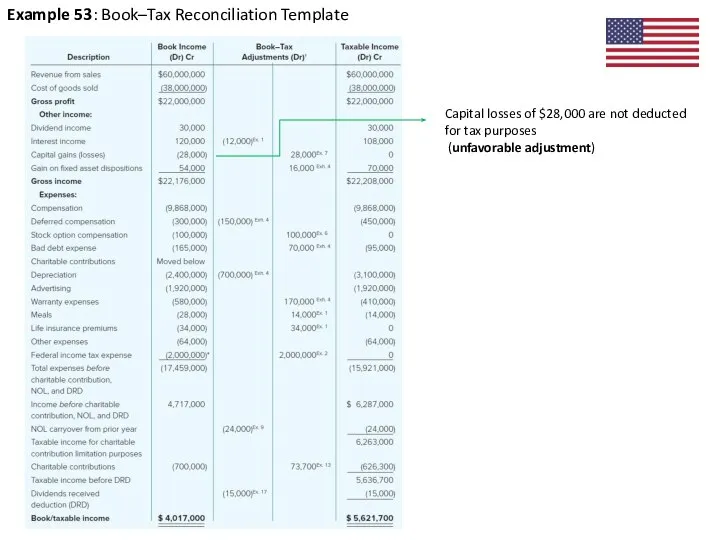

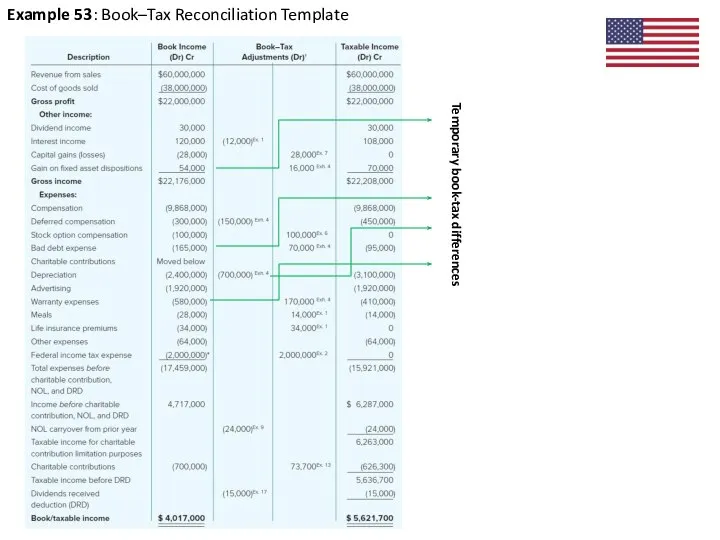

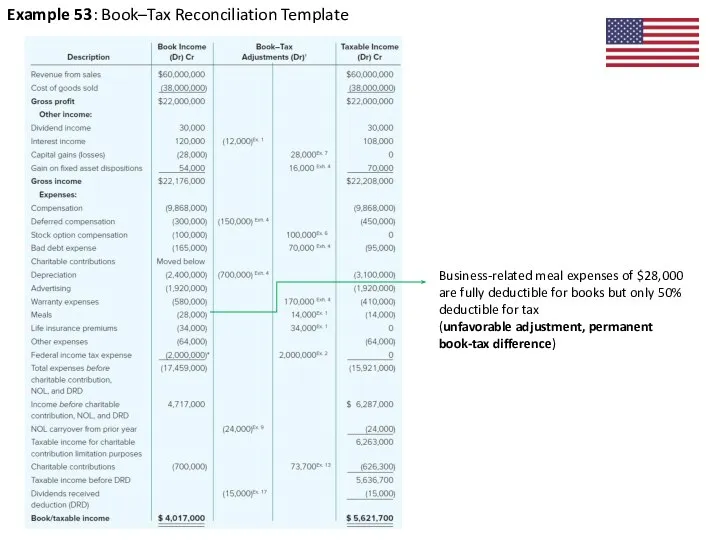

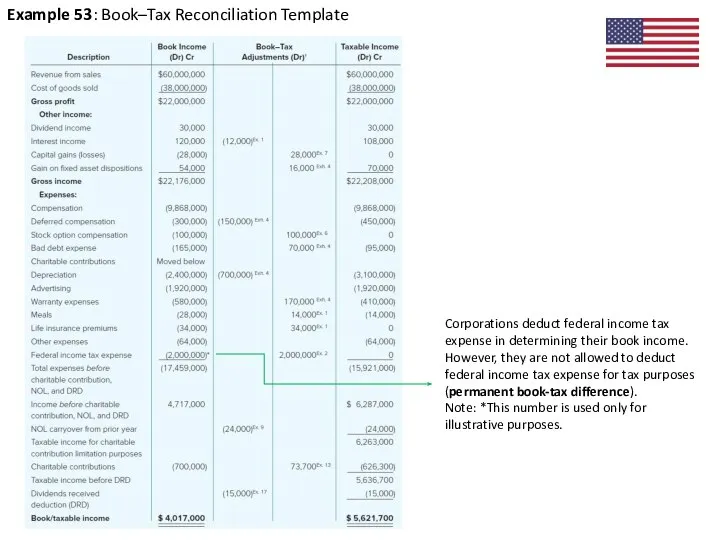

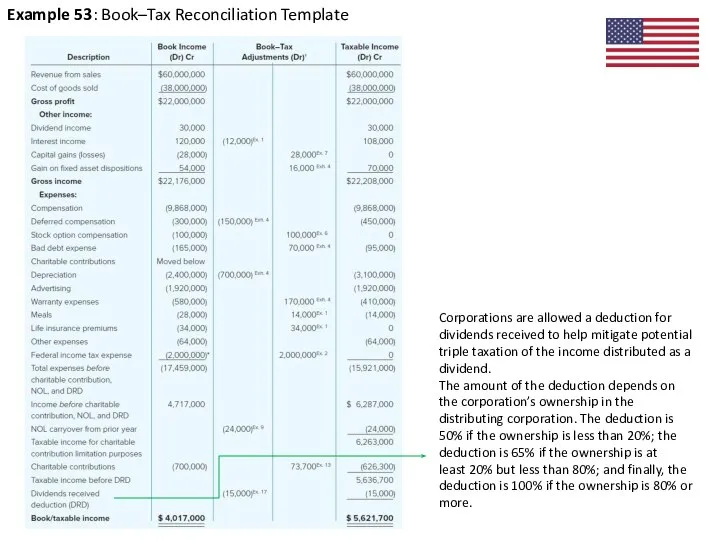

- 158. Example 53: Book–Tax Reconciliation Template Source: Spilker, Ayers: Taxation of Individuals and Business Entities, McGraw-Hill, 2019

- 159. Example 53: Book–Tax Reconciliation Template Capital losses of $28,000 are not deducted for tax purposes (unfavorable

- 160. Example 53: Book–Tax Reconciliation Template Initial estimated fair value of stock options is deducted in books,

- 161. Example 53: Book–Tax Reconciliation Template Temporary book-tax differences

- 162. Example 53: Book–Tax Reconciliation Template Business-related meal expenses of $28,000 are fully deductible for books but

- 163. Example 53: Book–Tax Reconciliation Template Corporations deduct federal income tax expense in determining their book income.

- 164. Example 53: Book–Tax Reconciliation Template Corporations are allowed a deduction for dividends received to help mitigate

- 165. Corporate income tax liability: When corporations calculate their taxable income, they compute their tax liability using

- 166. Scope of Corporation Tax (U.K. case) A company's taxable total profits include both its income and

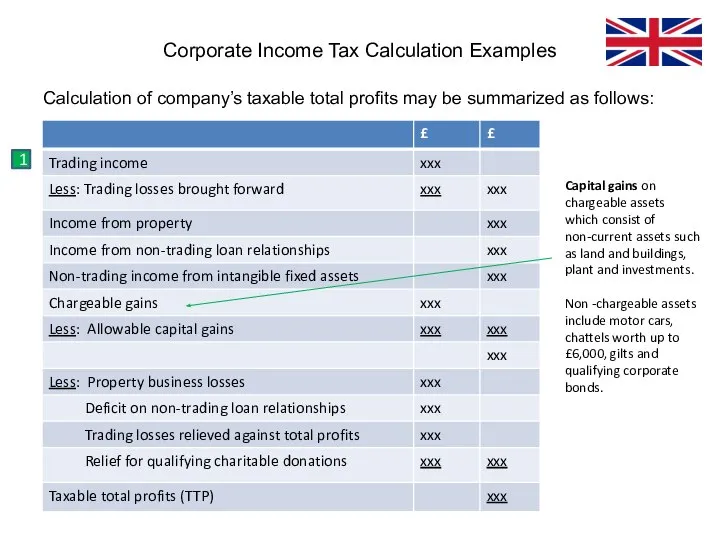

- 167. Calculation of company’s taxable total profits may be summarized as follows: Corporate Income Tax Calculation Examples

- 168. Calculation of company’s taxable total profits may be summarized as follows: Corporate Income Tax Calculation Examples

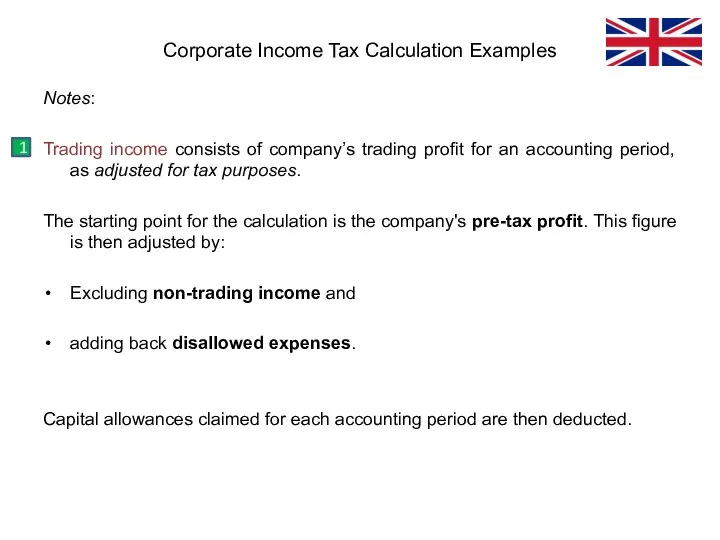

- 169. Notes: Trading income consists of company’s trading profit for an accounting period, as adjusted for tax

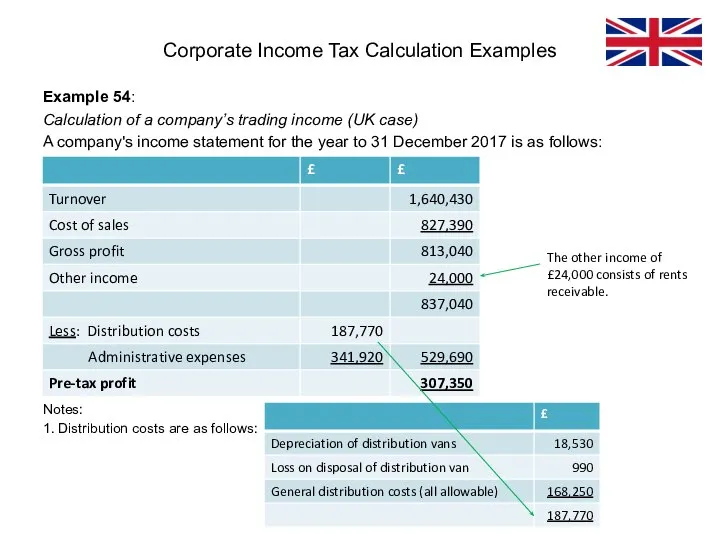

- 170. Example 54: Calculation of a company’s trading income (UK case) A company's income statement for the

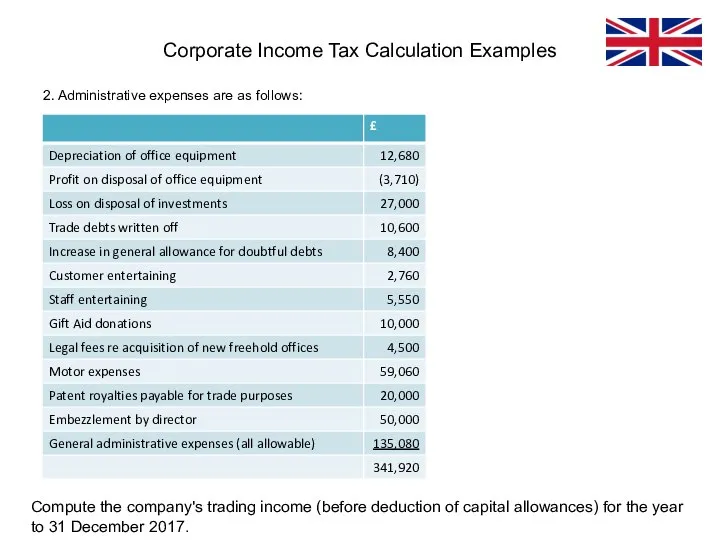

- 171. 2. Administrative expenses are as follows: Corporate Income Tax Calculation Examples Compute the company's trading income

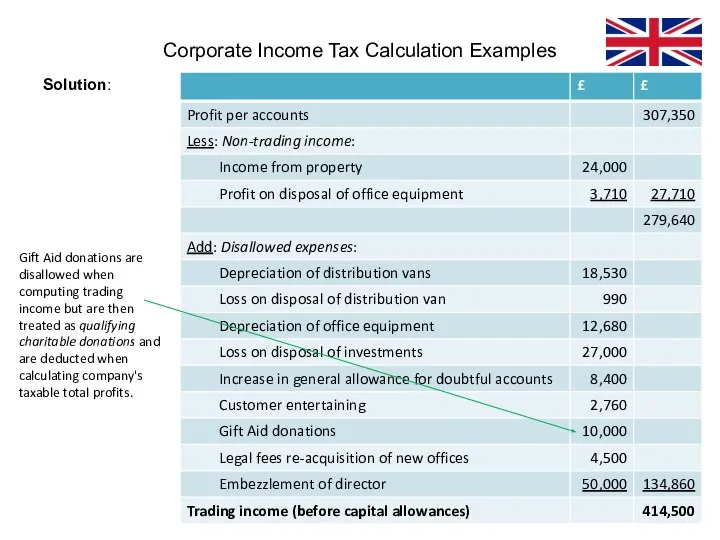

- 172. Solution: Corporate Income Tax Calculation Examples Gift Aid donations are disallowed when computing trading income but

- 173. Solution: Corporate Income Tax Calculation Examples Losses caused by the dishonesty of a director are disallowed.

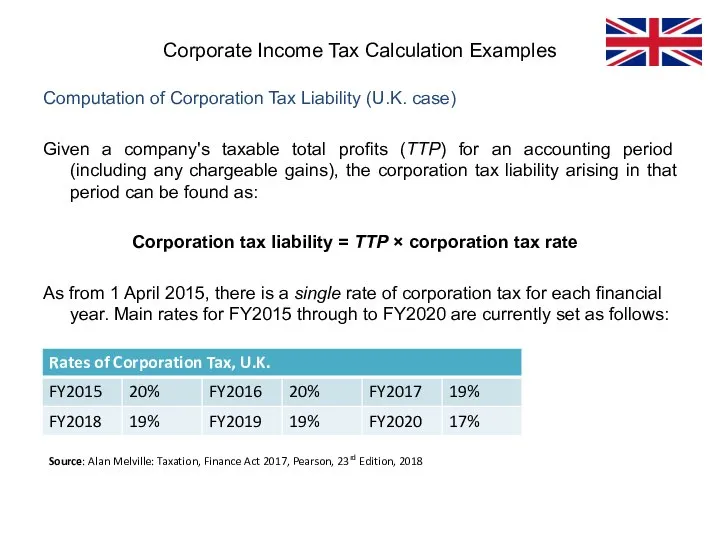

- 174. Computation of Corporation Tax Liability (U.K. case) Given a company's taxable total profits (TTP) for an

- 175. Chapter 6: INDIRECT TAXES: VALUE-ADDED TAX Definition of Value Added Tax Value added tax (VAT) is

- 176. Map of countries and territories by their VAT status VAT No VAT

- 177. Standard VAT or sales tax rate

- 178. Value Added Tax Rates in Europe

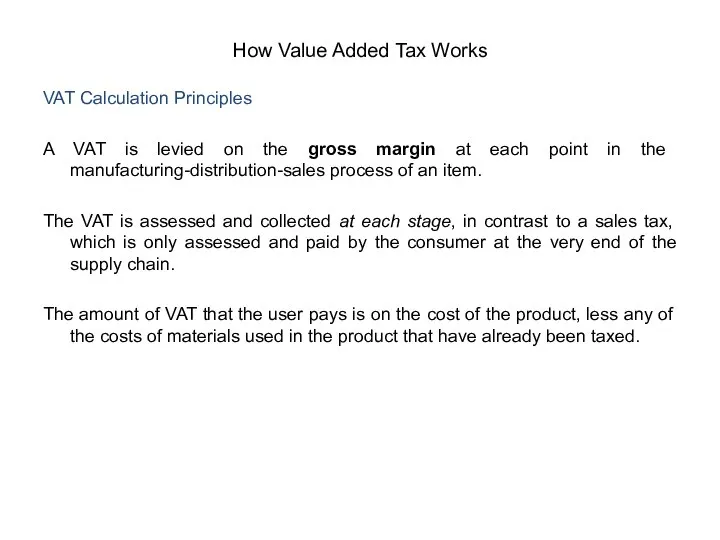

- 179. VAT Calculation Principles A VAT is levied on the gross margin at each point in the

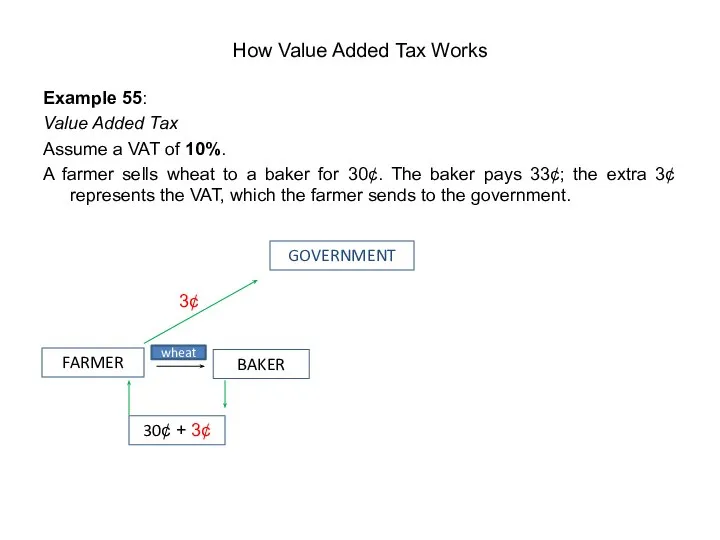

- 180. Example 55: Value Added Tax Assume a VAT of 10%. A farmer sells wheat to a

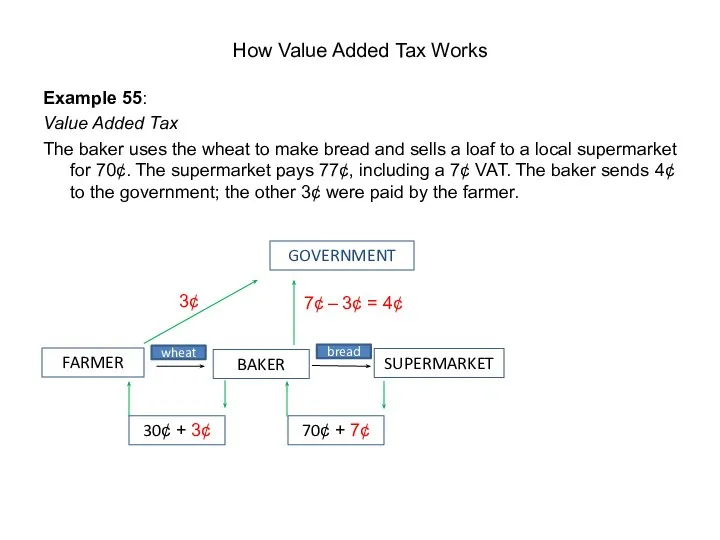

- 181. Example 55: Value Added Tax The baker uses the wheat to make bread and sells a

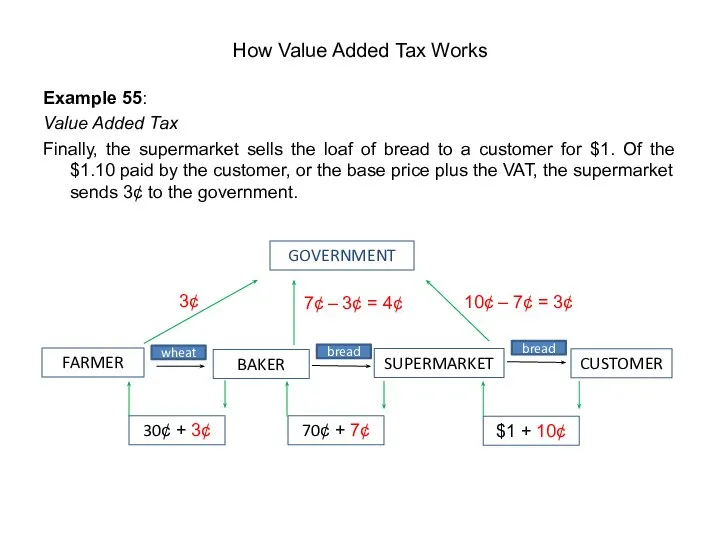

- 182. Example 55: Value Added Tax Finally, the supermarket sells the loaf of bread to a customer

- 183. VAT vs. Sales Tax Sales tax is assessed only once at the final stage of the

- 184. VAT: Advantages Adoption of a regressive tax system, such as VAT, gives people a stronger incentive

- 185. VAT: Disadvantages Unlike the income tax rate, which varies at different levels of income, VAT is

- 186. Value Added Tax (U.K. case) The basic principle of VAT is that tax should be charged

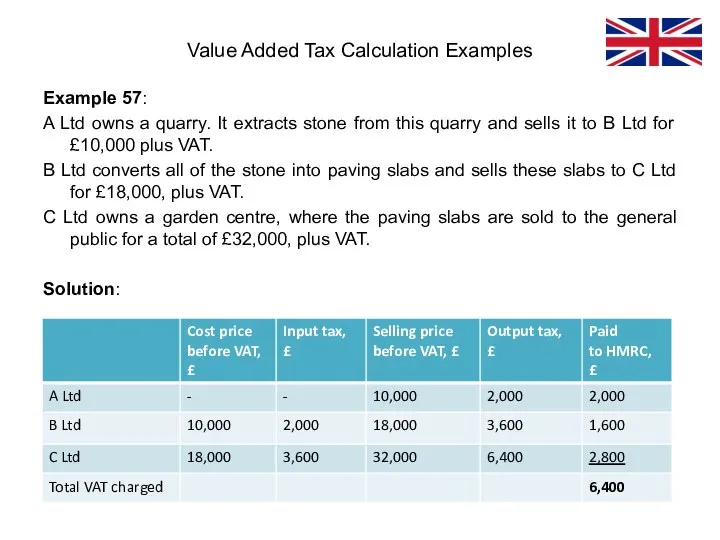

- 187. Example 57: A Ltd owns a quarry. It extracts stone from this quarry and sells it

- 188. Example 57: A Ltd owns a quarry. It extracts stone from this quarry and sells it

- 189. Chapter 7: INTERNATIONAL TAXATION ASPECTS Taxation Systems Countries that tax income generally use one of two

- 191. Taxation of income Under source jurisdiction a country levies taxes on all income generated within its

- 192. Double Taxation Conflicts Interaction of country tax systems can result in tax conflicts in which two

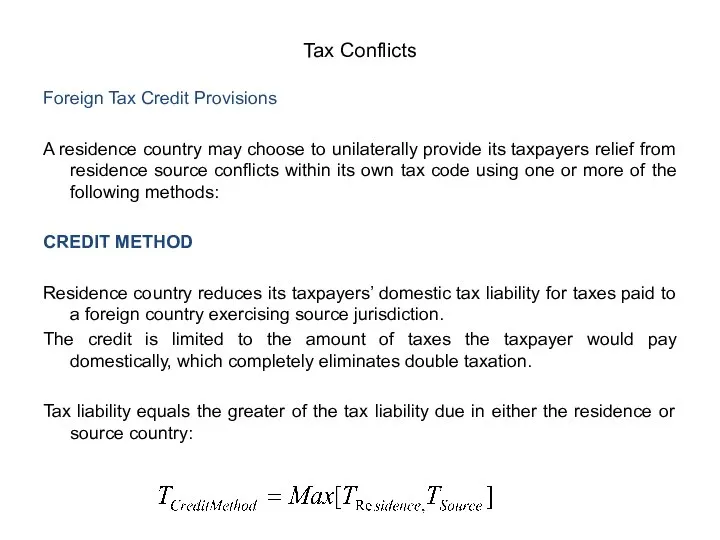

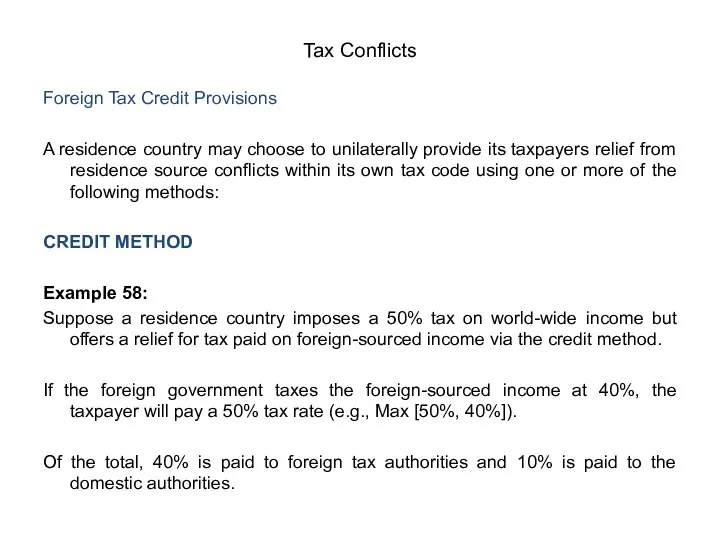

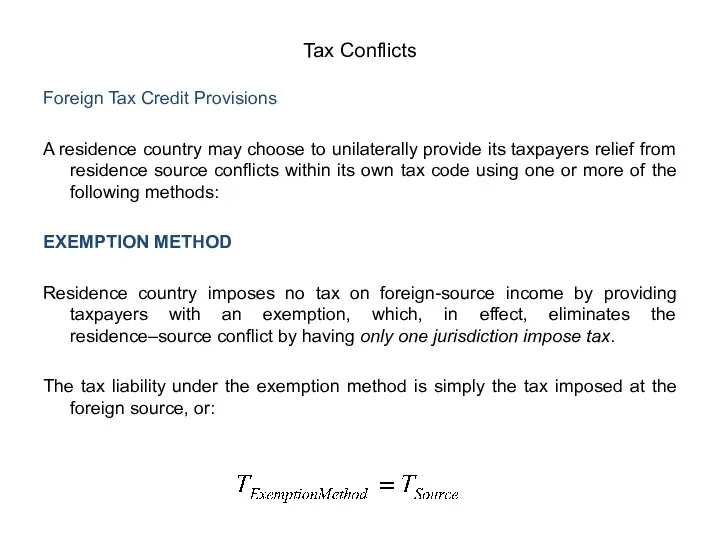

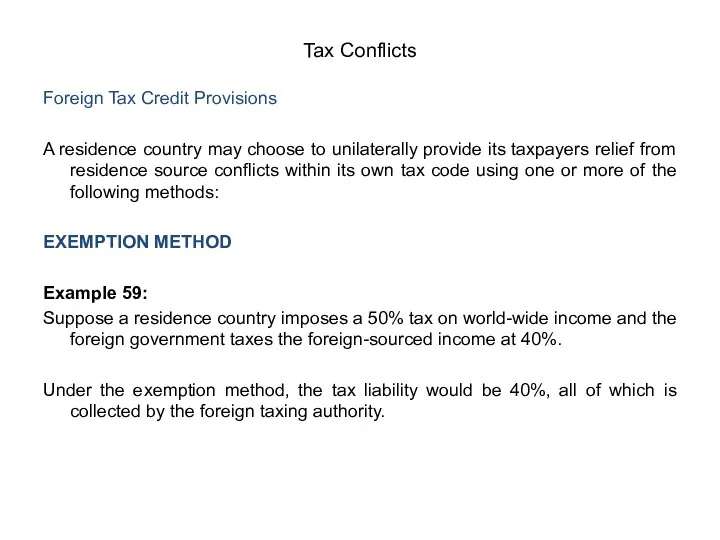

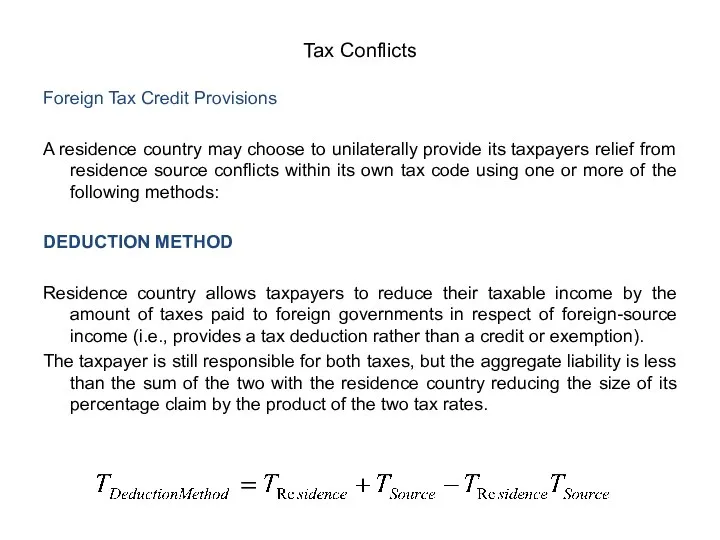

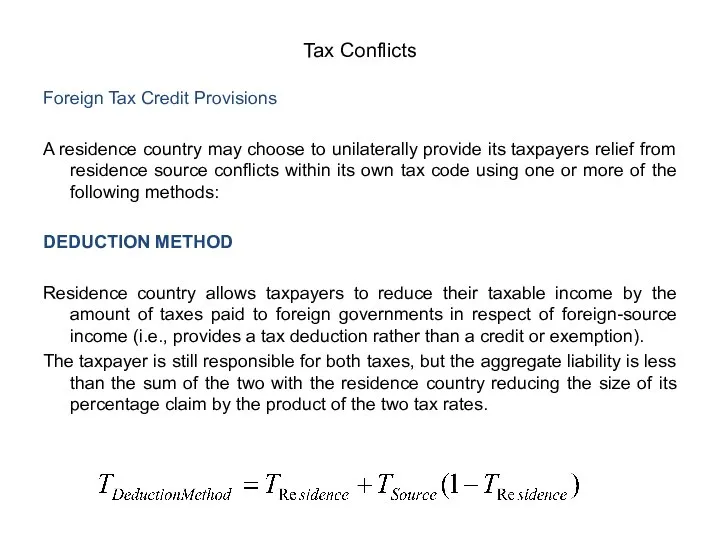

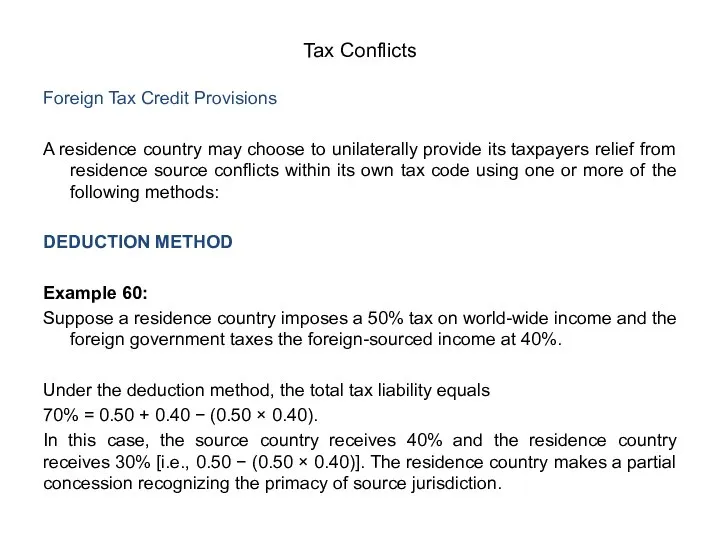

- 193. Foreign Tax Credit Provisions A residence country may choose to unilaterally provide its taxpayers relief from

- 194. Foreign Tax Credit Provisions A residence country may choose to unilaterally provide its taxpayers relief from

- 195. Foreign Tax Credit Provisions A residence country may choose to unilaterally provide its taxpayers relief from

- 196. Foreign Tax Credit Provisions A residence country may choose to unilaterally provide its taxpayers relief from

- 197. Foreign Tax Credit Provisions A residence country may choose to unilaterally provide its taxpayers relief from

- 198. Foreign Tax Credit Provisions A residence country may choose to unilaterally provide its taxpayers relief from

- 199. Foreign Tax Credit Provisions A residence country may choose to unilaterally provide its taxpayers relief from

- 200. Foreign Tax Credit Provisions A residence country may choose to unilaterally provide its taxpayers relief from

- 201. Double Taxation Treaties Relief from double taxation may be provided through a double taxation treaty (DTT)

- 202. Double Taxation Treaties In addition to residence–source conflicts, DTTs resolve residence–residence conflicts. A resident is taxable

- 203. Tax Avoidance vs. Tax Evasion Tax avoidance (a.k.a. “tax minimization”) uses legal means to lower the

- 204. Current Trends in International Transparency and Information Exchange Most countries attempt to maximize the amount of

- 205. Current Trends in International Transparency and Information Exchange Most countries attempt to maximize the amount of

- 206. Current Trends in International Transparency and Information Exchange Most countries attempt to maximize the amount of

- 207. Common Tax Evasion Schemes Falsifying information on tax return This occurs when a taxpayer understates its

- 208. Transfer Pricing Transfer pricing is an accounting practice that represents the price that one division in

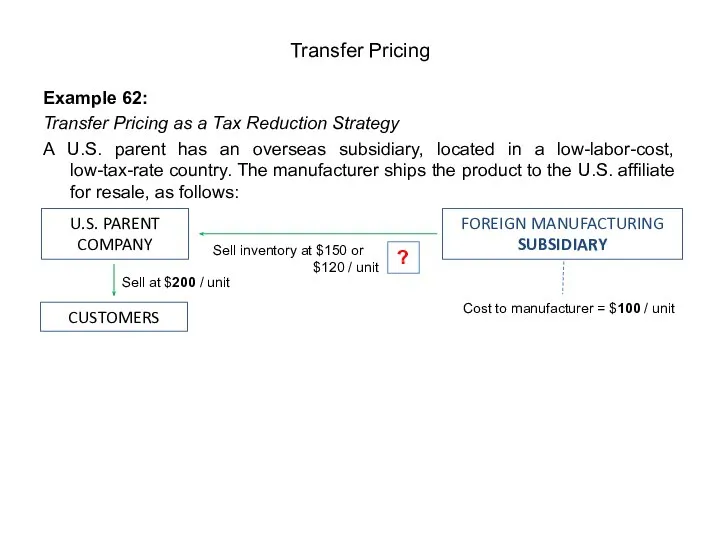

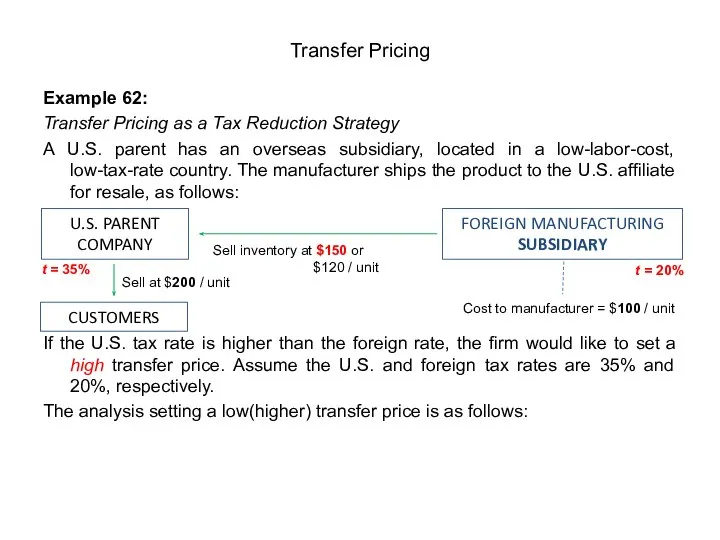

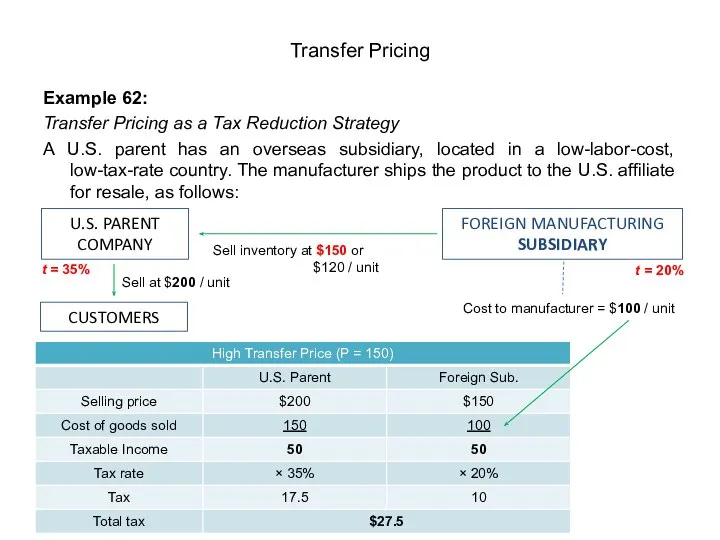

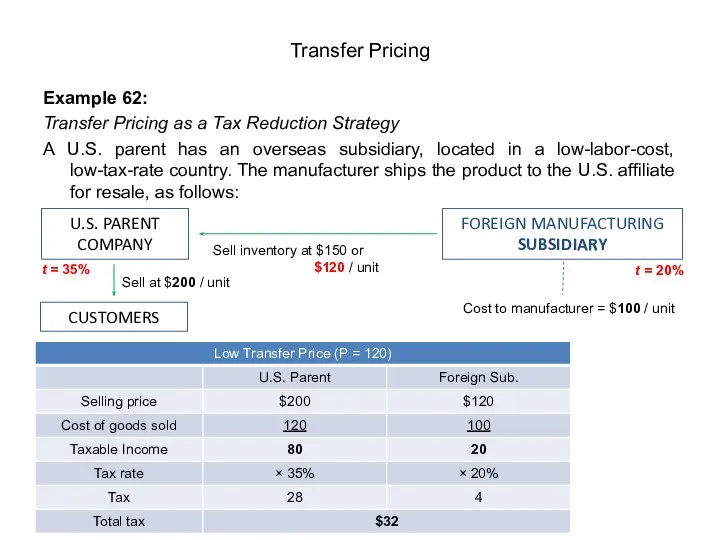

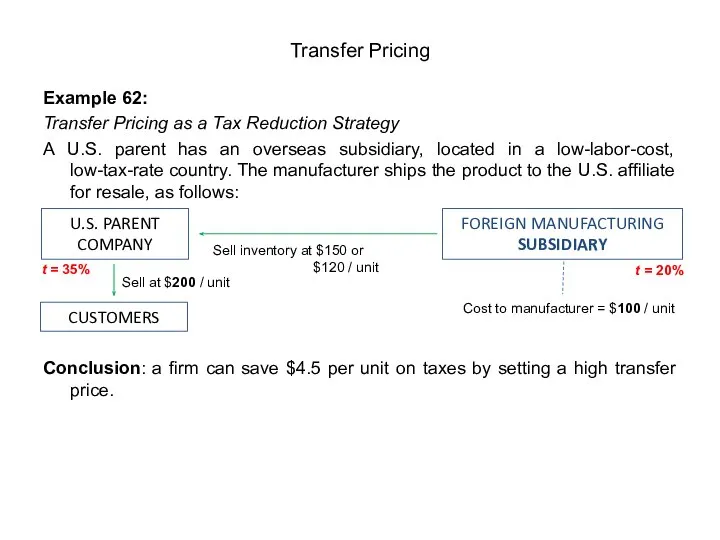

- 209. Example 62: Transfer Pricing as a Tax Reduction Strategy A U.S. parent has an overseas subsidiary,

- 210. Example 62: Transfer Pricing as a Tax Reduction Strategy A U.S. parent has an overseas subsidiary,

- 211. Example 62: Transfer Pricing as a Tax Reduction Strategy A U.S. parent has an overseas subsidiary,

- 212. Example 62: Transfer Pricing as a Tax Reduction Strategy A U.S. parent has an overseas subsidiary,

- 213. Example 62: Transfer Pricing as a Tax Reduction Strategy A U.S. parent has an overseas subsidiary,

- 214. Transfer Pricing via Tax Haven Transfer pricing is a technique used by multinational corporations to shift

- 215. Tax Haven A tax haven (a.k.a., offshore financial center) is a tax jurisdiction with very low

- 217. Скачать презентацию

Слайд 3Tax Collection

In modern taxation systems, governments levy taxes in money; but in-kind

Tax Collection

In modern taxation systems, governments levy taxes in money; but in-kind

Слайд 4Purposes of Taxation

Purposes of Taxation

The levying of taxes aims to

raise revenue

Purposes of Taxation

Purposes of Taxation

The levying of taxes aims to

raise revenue

Слайд 5Economic Effects of Taxation

Economic Effects of Taxation

Imposition of taxes may have the

Economic Effects of Taxation

Economic Effects of Taxation

Imposition of taxes may have the

Слайд 6Tax Incidence

Tax incidence is the division of the burden of a tax

Tax Incidence

Tax incidence is the division of the burden of a tax

Слайд 7Example 1:

Tax on Sellers

Assume a tax per unit of $3 is levied

Example 1:

Tax on Sellers

Assume a tax per unit of $3 is levied

Слайд 9Consumers purchase 425 units and pay $6/unit. Effectively prices paid by consumers

Consumers purchase 425 units and pay $6/unit. Effectively prices paid by consumers

Слайд 10Example 2:

Why taxes result in deadweight losses

Imagine that Joe cleans Jane’s house

Example 2:

Why taxes result in deadweight losses

Imagine that Joe cleans Jane’s house

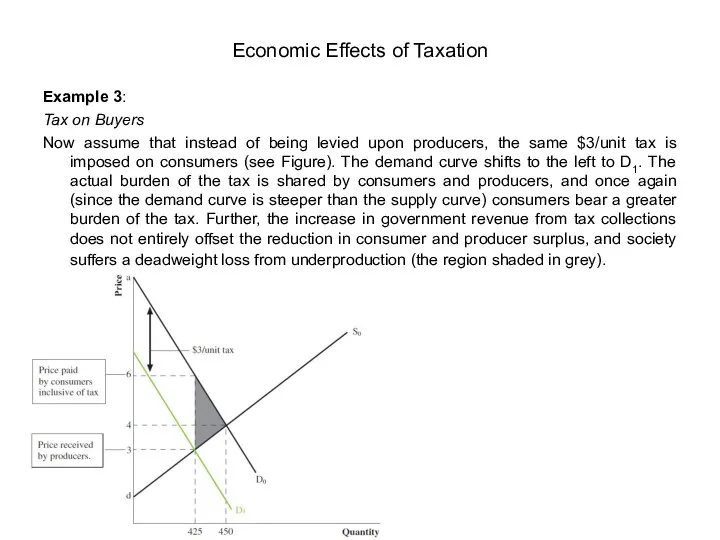

Слайд 11Example 3:

Tax on Buyers

Now assume that instead of being levied upon producers,

Example 3:

Tax on Buyers

Now assume that instead of being levied upon producers,

Слайд 12The impact of a tax on a market outcome is the same

The impact of a tax on a market outcome is the same

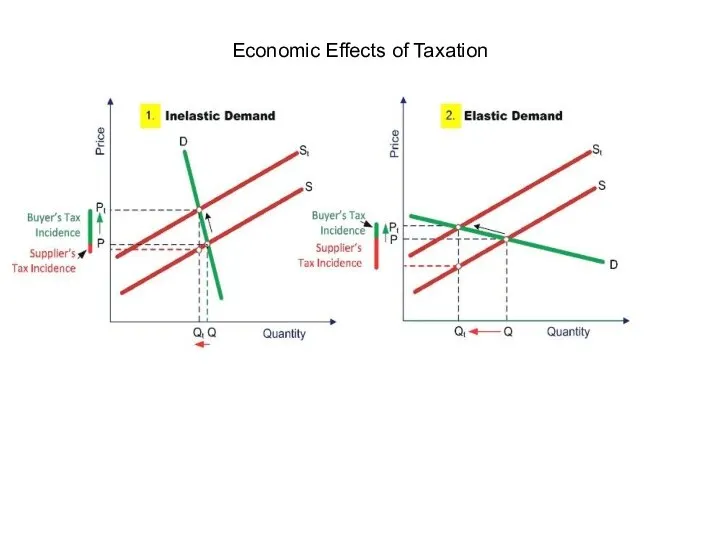

Слайд 13Tax Incidence and Elasticity of Demand

The division of the tax between buyers

Tax Incidence and Elasticity of Demand

The division of the tax between buyers

Слайд 14Economic Effects of Taxation

Economic Effects of Taxation

Слайд 15Demand is perfectly inelastic at 100,000 doses a day, regardless of the

Demand is perfectly inelastic at 100,000 doses a day, regardless of the

Слайд 16The demand for this good is perfectly elastic — the demand curve

The demand for this good is perfectly elastic — the demand curve

Слайд 17Tax Incidence and Elasticity of Supply

The division of the tax between buyers

Tax Incidence and Elasticity of Supply

The division of the tax between buyers

Слайд 19The supply of this good is perfectly inelastic at 100,000 bottles a

The supply of this good is perfectly inelastic at 100,000 bottles a

Слайд 20The supply of this good is perfectly elastic — the supply curve

The supply of this good is perfectly elastic — the supply curve

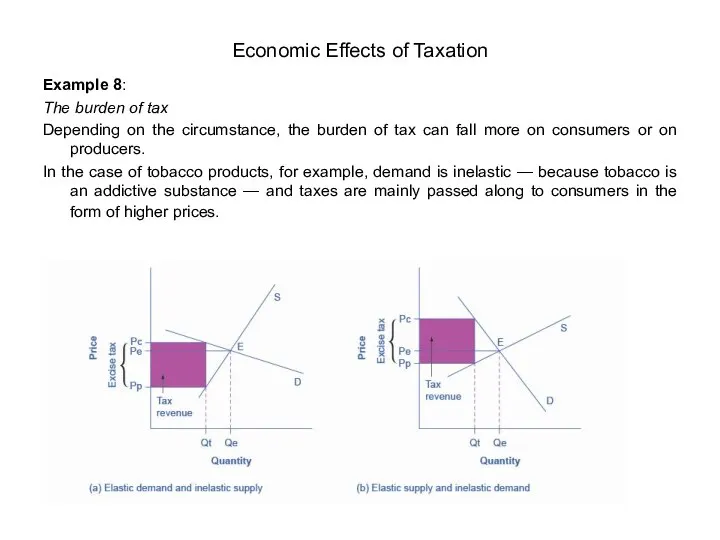

Слайд 21Example 8:

The burden of tax

Depending on the circumstance, the burden of tax

Example 8:

The burden of tax

Depending on the circumstance, the burden of tax

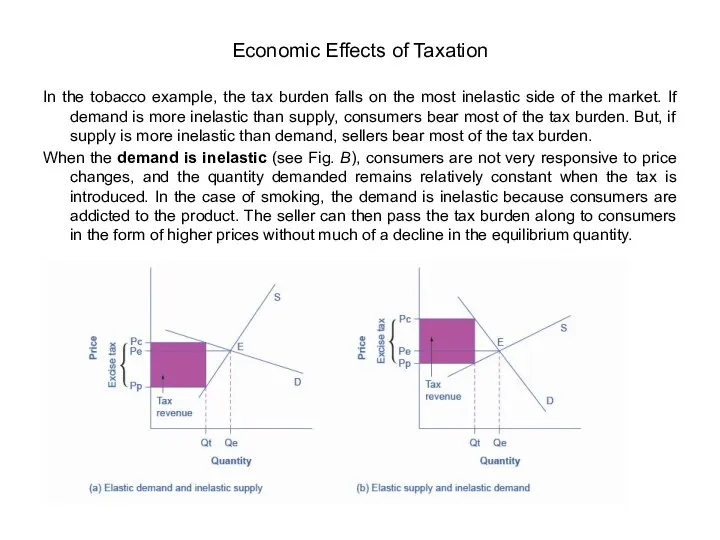

Слайд 22In the tobacco example, the tax burden falls on the most inelastic

In the tobacco example, the tax burden falls on the most inelastic

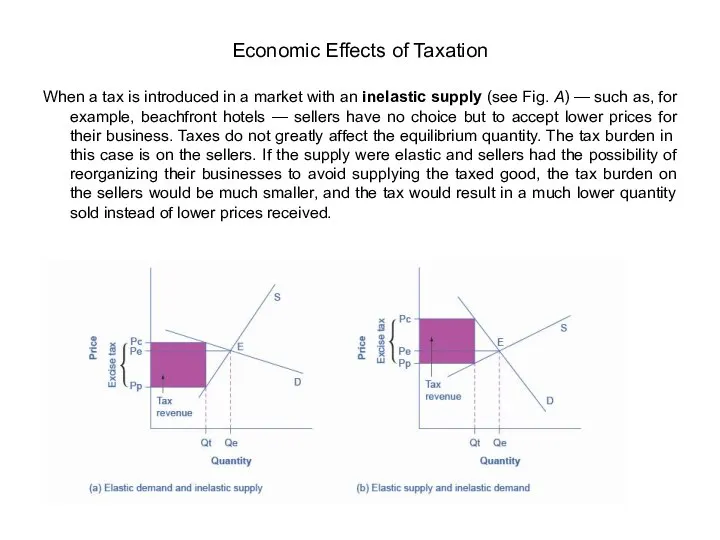

Слайд 23When a tax is introduced in a market with an inelastic supply

When a tax is introduced in a market with an inelastic supply

Слайд 24In Fig. A, the supply is inelastic and the demand is elastic

In Fig. A, the supply is inelastic and the demand is elastic

Слайд 25The tax revenue is given by the shaded area, which is obtained

The tax revenue is given by the shaded area, which is obtained

Слайд 26In figure A, the tax burden falls disproportionately on the sellers, and

In figure A, the tax burden falls disproportionately on the sellers, and

Слайд 27On the other hand, if we go back to our example of

On the other hand, if we go back to our example of

Слайд 28Practice Problem 1:

The original equilibrium price is €3.00 and the equilibrium quantity

Practice Problem 1:

The original equilibrium price is €3.00 and the equilibrium quantity

Слайд 29Other economic effects of taxation

Redistribution of Income

This effect is felt most in

Other economic effects of taxation

Redistribution of Income

This effect is felt most in

Слайд 30Other economic effects of taxation

A Reduction in Incentive

It may be argued that

Other economic effects of taxation

A Reduction in Incentive

It may be argued that

Слайд 31Other economic effects of taxation

3. A Reduction in Business Activity

Entrepreneurs undertake investment

Other economic effects of taxation

3. A Reduction in Business Activity

Entrepreneurs undertake investment

Слайд 32Other economic effects of taxation

4. Effects on the Ability to Work, Save

Other economic effects of taxation

4. Effects on the Ability to Work, Save

Слайд 33Other economic effects of taxation

It is suggested that effects of taxes upon

Other economic effects of taxation

It is suggested that effects of taxes upon

Слайд 34Laffer Curve

The Laffer Curve is a theory developed by supply-side economist Arthur

Laffer Curve

The Laffer Curve is a theory developed by supply-side economist Arthur

Слайд 35Chapter 2: BASIC PRINCIPLES OF TAXATION

Goals of an Ideal Taxing System

Principles of

Chapter 2: BASIC PRINCIPLES OF TAXATION

Goals of an Ideal Taxing System

Principles of

Слайд 361. Equality

Taxpayers should bear a fair level of tax relative to their

1. Equality

Taxpayers should bear a fair level of tax relative to their

Слайд 37Vertical equity:

When taxpayers are in different economic positions, the taxpayer with the

Vertical equity:

When taxpayers are in different economic positions, the taxpayer with the

Слайд 382. Certainty

Taxpayer knows when, how, and how much tax is paid.

It

2. Certainty

Taxpayer knows when, how, and how much tax is paid.

It

Слайд 39Tax Base

Taxes are computed by multiplying the tax rate by the tax

Tax Base

Taxes are computed by multiplying the tax rate by the tax

Слайд 40Tax Deduction

Tax deduction is a reduction of income that is able to

Tax Deduction

Tax deduction is a reduction of income that is able to

Слайд 41Example 12:

Tax Credit (U.S. Example)

As the simplified example in the table shows,

Example 12:

Tax Credit (U.S. Example)

As the simplified example in the table shows,

Слайд 42Tax Rates

For most taxes there are four types of tax rates:

statutory rates

marginal

Tax Rates

For most taxes there are four types of tax rates:

statutory rates

marginal

Слайд 43Example 13:

At the end of the year, XYZ Corporation has taxable income

Example 13:

At the end of the year, XYZ Corporation has taxable income

Слайд 44Example 14:

Effective tax rate

The company reports the following financial data:

Assume that the

Example 14:

Effective tax rate

The company reports the following financial data:

Assume that the

Слайд 45Effective Tax Rate vs. Marginal Tax Rate

The effective tax rate is a

Effective Tax Rate vs. Marginal Tax Rate

The effective tax rate is a

Слайд 46Example 15:

Assume the progressive income-tax system, where taxes are imposed as follows:

Example 15:

Assume the progressive income-tax system, where taxes are imposed as follows:

Слайд 47Tax Rate Structures

In most tax jurisdictions, a tax rate structure applies to

Tax Rate Structures

In most tax jurisdictions, a tax rate structure applies to

Слайд 48Though many countries have a progressive tax regime when it comes to

Though many countries have a progressive tax regime when it comes to

Слайд 49Example 17:

U.S. User Fees (regressive)

User fees levied by the U.S. government are

Example 17:

U.S. User Fees (regressive)

User fees levied by the U.S. government are

Слайд 50Other examples of regressive taxes

Gambling taxes

Those on low incomes have a

Other examples of regressive taxes

Gambling taxes

Those on low incomes have a

Слайд 51A progressive tax system is one in which the average tax rate

A progressive tax system is one in which the average tax rate

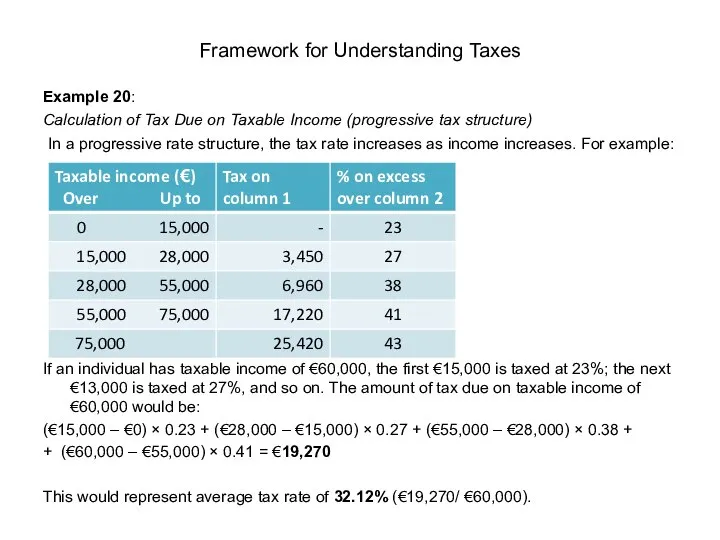

Слайд 52Example 20:

Calculation of Tax Due on Taxable Income (progressive tax structure)

In

Example 20:

Calculation of Tax Due on Taxable Income (progressive tax structure)

In

Слайд 53A proportional tax system (a.k.a., flat tax system) is the one in

A proportional tax system (a.k.a., flat tax system) is the one in

Слайд 54Important Principles and Concepts in Tax Law

Most tax systems have developed around

Important Principles and Concepts in Tax Law

Most tax systems have developed around

Слайд 55Entity Principle

Under the entity principle, an entity (such as a corporation)

Entity Principle

Under the entity principle, an entity (such as a corporation)

Слайд 56Arm’s Length Principle

The condition or the fact that the parties to

Arm’s Length Principle

The condition or the fact that the parties to

Слайд 57Example 24:

Arm’s Length Principle

Assume that in Example 23 the corporation pays its

Example 24:

Arm’s Length Principle

Assume that in Example 23 the corporation pays its

Слайд 58Example 25:

Arm’s Length Test

Assume that an entrepreneur sells an asset to his

Example 25:

Arm’s Length Test

Assume that an entrepreneur sells an asset to his

Слайд 59Arm’s Length Principle: Business Expenses

Ordinary and necessary business expenses are deductible only

Arm’s Length Principle: Business Expenses

Ordinary and necessary business expenses are deductible only

Слайд 60Example 27:

Business Deductions

Assume John hired four part-time employees and paid them $10

Example 27:

Business Deductions

Assume John hired four part-time employees and paid them $10

Слайд 61All-Inclusive Income Principle

This principle basically means that if some simple tests

All-Inclusive Income Principle

This principle basically means that if some simple tests

Слайд 62Example 28:

Realization Principle

A corporation owns two assets that have gone up in

Example 28:

Realization Principle

A corporation owns two assets that have gone up in

Слайд 63Business Purpose Concept

Relates to tax deductions.

Here, business expenses are deductible only if

Business Purpose Concept

Relates to tax deductions.

Here, business expenses are deductible only if

Слайд 64Tax-Benefit Rule

Under the tax-benefit rule, if a taxpayer receives a refund of

Tax-Benefit Rule

Under the tax-benefit rule, if a taxpayer receives a refund of

Слайд 65Substance over Form Doctrine

Under the doctrine of substance over form, even when

Substance over Form Doctrine

Under the doctrine of substance over form, even when

Слайд 66Pay-As-You-Earn Concept (PAYE)

Taxpayers must pay part of their estimated annual tax liability

Pay-As-You-Earn Concept (PAYE)

Taxpayers must pay part of their estimated annual tax liability

Слайд 67Taxation of Gains and Losses on Property Sale

In virtually every tax jurisdiction,

Taxation of Gains and Losses on Property Sale

In virtually every tax jurisdiction,

Слайд 68Example 33:

Calculation of Gain / Loss

A corporation buys a factory building for

Example 33:

Calculation of Gain / Loss

A corporation buys a factory building for

Слайд 69Chapter 3: PERSONAL INCOME TAX

Definition of Personal Income Tax

According to OECD, tax

Chapter 3: PERSONAL INCOME TAX

Definition of Personal Income Tax

According to OECD, tax

Слайд 70Example 34:

Personal Income Tax Calculation (U.S. example)

Resident alien husband and wife with

Example 34:

Personal Income Tax Calculation (U.S. example)

Resident alien husband and wife with

Слайд 71The calculation of personal income taxes due (or refund) is based on

The calculation of personal income taxes due (or refund) is based on

Слайд 72Explanations:

Gross income may include:

income from a job,

business income,

retirement income,

interest

Explanations:

Gross income may include:

income from a job,

business income,

retirement income,

interest

Слайд 73Appendix 1

Source: Spilker, Ayers: Taxation of Individuals and Business Entities, McGraw-Hill, 2019

Appendix 1

Source: Spilker, Ayers: Taxation of Individuals and Business Entities, McGraw-Hill, 2019

Слайд 74Exclusions and Deferrals

Certain tax provisions allow taxpayers to permanently exclude specific types

Exclusions and Deferrals

Certain tax provisions allow taxpayers to permanently exclude specific types

Слайд 75Adjusted Gross Income (AGI)

It can be shown that

Some common For AGI

Adjusted Gross Income (AGI)

It can be shown that

Some common For AGI

Слайд 76From AGI Deductions

After calculating AGI, the taxpayer can then apply:

standard deductions to

From AGI Deductions

After calculating AGI, the taxpayer can then apply:

standard deductions to

Слайд 77Itemized Deduction

An expenditure on eligible products, services, or contributions that can be

Itemized Deduction

An expenditure on eligible products, services, or contributions that can be

Слайд 78Tax Rates

After determining taxable income, taxpayers can generally calculate their regular

Tax Rates

After determining taxable income, taxpayers can generally calculate their regular

Слайд 79Tax Prepayments

These include:

withholdings, or income taxes withheld from the taxpayer’s

Tax Prepayments

These include:

withholdings, or income taxes withheld from the taxpayer’s

Слайд 80Example 35:

Personal Income Tax Calculation (UK example)

In 2017-18, Kenneth (who is not

Example 35:

Personal Income Tax Calculation (UK example)

In 2017-18, Kenneth (who is not

Слайд 81A typical structure of an income tax computation for year 2017-18 may

A typical structure of an income tax computation for year 2017-18 may

Слайд 82Explanations:

Total income may include:

Employment income,

Pensions,

Social security income,

Trading income,

Property

Explanations:

Total income may include:

Employment income,

Pensions,

Social security income,

Trading income,

Property

Слайд 83Savings Income and Non-Savings Income

Tax liability on a taxpayer's "savings income"

Savings Income and Non-Savings Income

Tax liability on a taxpayer's "savings income"

Слайд 84Tax reliefs may include:

Certain payments made by the taxpayer (e.g., eligible interest

Tax reliefs may include:

Certain payments made by the taxpayer (e.g., eligible interest

Слайд 85Tax rates

Income tax is charged on the taxable income, using the tax

Tax rates

Income tax is charged on the taxable income, using the tax

Слайд 86Tax Treatment of Savings Income

Savings income which falls into the first £5,000

Tax Treatment of Savings Income

Savings income which falls into the first £5,000

Слайд 87Personal Savings Allowance (PSA)

Taxpayers may be entitled to a PSA of up

Personal Savings Allowance (PSA)

Taxpayers may be entitled to a PSA of up

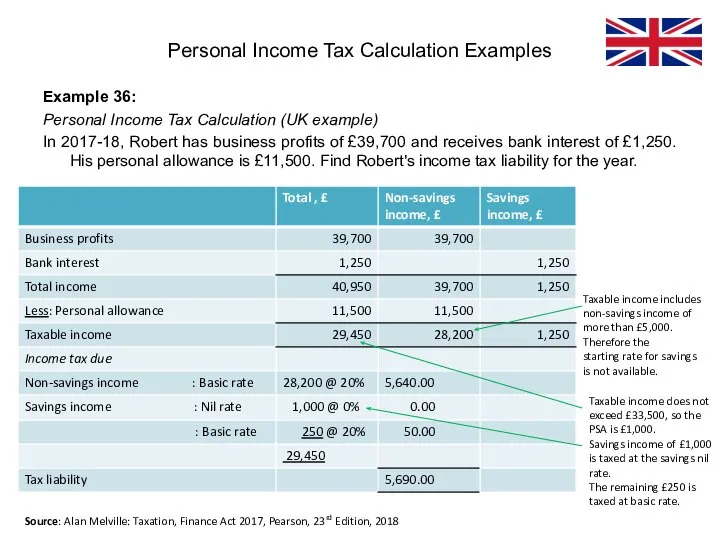

Слайд 88Example 36:

Personal Income Tax Calculation (UK example)

In 2017-18, Robert has business profits

Example 36:

Personal Income Tax Calculation (UK example)

In 2017-18, Robert has business profits

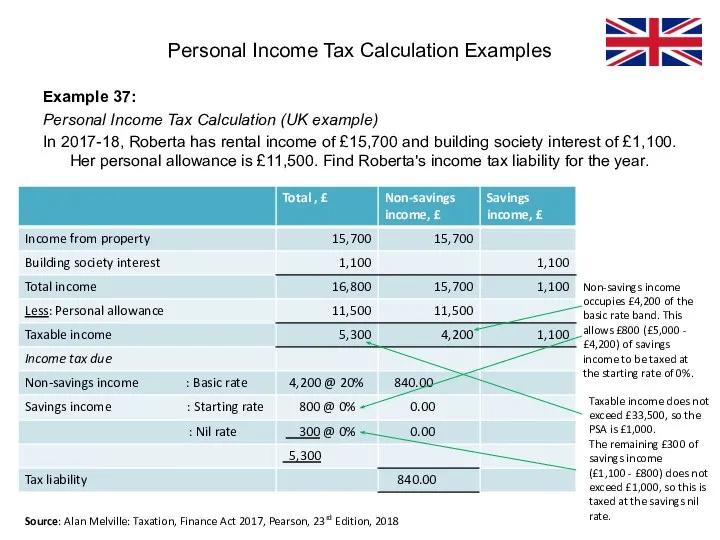

Слайд 89Example 37:

Personal Income Tax Calculation (UK example)

In 2017-18, Roberta has rental income

Example 37:

Personal Income Tax Calculation (UK example)

In 2017-18, Roberta has rental income

Слайд 90Example 38:

In 2017-18, Philip (who is not a Scottish taxpayer) has business

Example 38:

In 2017-18, Philip (who is not a Scottish taxpayer) has business

Слайд 91Chapter 4: TAXATION OF INVESTMENT INCOME

Definition of Investment Income

Investment income is income

Chapter 4: TAXATION OF INVESTMENT INCOME

Definition of Investment Income

Investment income is income

Слайд 92Taxation of Interest and Dividends (US. Case)

For tax purposes, individual investors typically

Taxation of Interest and Dividends (US. Case)

For tax purposes, individual investors typically

Слайд 93Example 39:

Assume Courtney (head of household filing status) decides to purchase dividend-paying

Example 39:

Assume Courtney (head of household filing status) decides to purchase dividend-paying

Слайд 94Example 39:

Assume Courtney (head of household filing status) decides to purchase dividend-paying

Example 39:

Assume Courtney (head of household filing status) decides to purchase dividend-paying

Слайд 95Example 39:

Assume Courtney (head of household filing status) decides to purchase dividend-paying

Example 39:

Assume Courtney (head of household filing status) decides to purchase dividend-paying

Слайд 96Taxation of Capital Gains and Losses (US. Case)

A capital gains tax is

Taxation of Capital Gains and Losses (US. Case)

A capital gains tax is

Слайд 97FIFO method and Specific Identification Method

When taxpayers sell a capital asset, e.g.,

FIFO method and Specific Identification Method

When taxpayers sell a capital asset, e.g.,

Слайд 98Example 41:

Assume Courtney sold 200 shares of Cisco stock at the current

Example 41:

Assume Courtney sold 200 shares of Cisco stock at the current

Слайд 99Example 41:

Assume Courtney sold 200 shares of Cisco stock at the current

Example 41:

Assume Courtney sold 200 shares of Cisco stock at the current

Слайд 100Short-Term Capital Gains vs. Long-Term Capital Gains

Taxpayers selling capital assets they have

Short-Term Capital Gains vs. Long-Term Capital Gains

Taxpayers selling capital assets they have

Слайд 101Tax Loss Harvesting

Many tax jurisdictions allow realized capital losses to offset realized

Tax Loss Harvesting

Many tax jurisdictions allow realized capital losses to offset realized

Слайд 102Tax Loss Harvesting

Example 41a:

Eduardo has a €1,000,000 portfolio held in a taxable

Tax Loss Harvesting

Example 41a:

Eduardo has a €1,000,000 portfolio held in a taxable

Слайд 103Tax Loss Harvesting

Example 41a:

Eduardo has a €1,000,000 portfolio held in a taxable

Tax Loss Harvesting

Example 41a:

Eduardo has a €1,000,000 portfolio held in a taxable

Слайд 104Tax Loss Harvesting

Tax Loss Harvesting

Слайд 105Taxation of Interest and Dividends (UK Case)

Interest received by a taxpayer is

Taxation of Interest and Dividends (UK Case)

Interest received by a taxpayer is

Слайд 106Example 42:

In 2017-18, Alfred had business profits of £15,870 and received net

Example 42:

In 2017-18, Alfred had business profits of £15,870 and received net

Слайд 107The income tax liability on a taxpayer's dividend income is calculated differently

The income tax liability on a taxpayer's dividend income is calculated differently

Слайд 108Example 43:

In tax year 2017-18, Christopher has rental income of £24,590. He

Example 43:

In tax year 2017-18, Christopher has rental income of £24,590. He

Слайд 109Example 43:

In tax year 2017-18, Christopher has rental income of £24,590. He

Example 43:

In tax year 2017-18, Christopher has rental income of £24,590. He

Слайд 110Example 43:

In tax year 2017-18, Christopher has rental income of £24,590. He

Example 43:

In tax year 2017-18, Christopher has rental income of £24,590. He

Слайд 111Capital Gains Tax (UK Case)

For tax year 2017-18, there are two main

Capital Gains Tax (UK Case)

For tax year 2017-18, there are two main

Слайд 112Capital Gains Tax: Basis of Assessment

A person's CGT liability for a tax

Capital Gains Tax: Basis of Assessment

A person's CGT liability for a tax

Слайд 113(c) If there are net gains for the year, these are reduced

(c) If there are net gains for the year, these are reduced

Слайд 114Example 44:

Four taxpayers each make three chargeable disposals during 2017-18.

Compute their

Example 44:

Four taxpayers each make three chargeable disposals during 2017-18.

Compute their

Слайд 115Example 44:

Four taxpayers each make three chargeable disposals during 2017-18.

Compute their

Example 44:

Four taxpayers each make three chargeable disposals during 2017-18.

Compute their

Слайд 116Calculation of Capital Gains Tax Payable

CGT rates are applied to the taxable

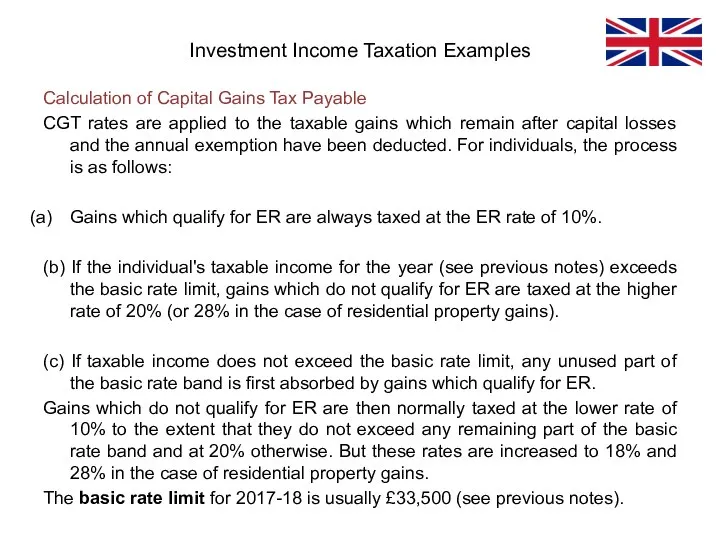

Calculation of Capital Gains Tax Payable

CGT rates are applied to the taxable

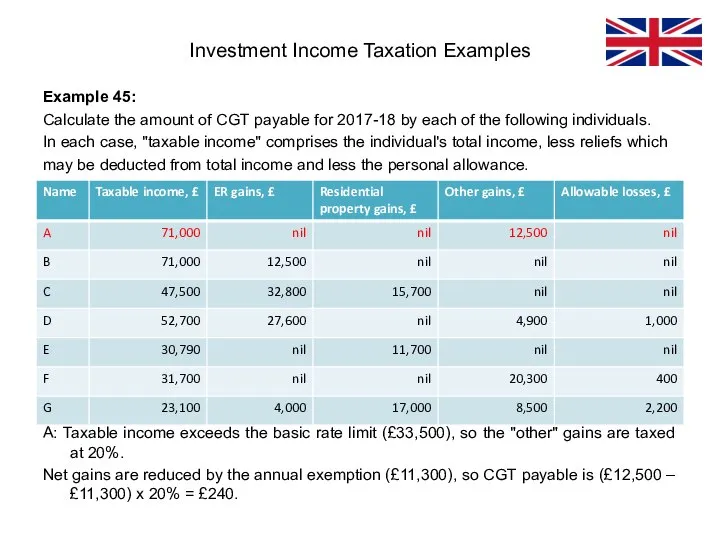

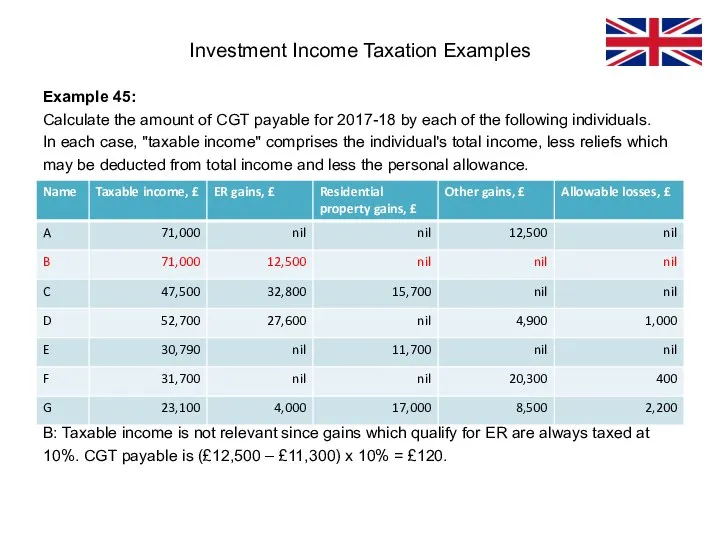

Слайд 117Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Слайд 118Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Слайд 119Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Слайд 120Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Слайд 121Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Слайд 122Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Слайд 123Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Слайд 124Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Слайд 125Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Example 45:

Calculate the amount of CGT payable for 2017-18 by each of

Слайд 126Effect of Taxes on Investment Returns

After-Tax Accumulations and Returns for Taxable Accounts

Taxes

Effect of Taxes on Investment Returns

After-Tax Accumulations and Returns for Taxable Accounts

Taxes

Слайд 127Effect of Taxes on Investment Returns

There are two types of methods of

Effect of Taxes on Investment Returns

There are two types of methods of

Слайд 128Effect of Taxes on Investment Returns

The amount of money accumulated for each

Effect of Taxes on Investment Returns

The amount of money accumulated for each

Слайд 129Effect of Taxes on Investment Returns

Tax Drag on Capital Accumulation

Tax drag is

Effect of Taxes on Investment Returns

Tax Drag on Capital Accumulation

Tax drag is

Слайд 130Effect of Taxes on Investment Returns

Example 47:

John is determining the impact of

Effect of Taxes on Investment Returns

Example 47:

John is determining the impact of

Слайд 131Effect of Taxes on Investment Returns

Implications of tax drag (assuming accrual taxation)

When

Effect of Taxes on Investment Returns

Implications of tax drag (assuming accrual taxation)

When

Слайд 132Effect of Taxes on Investment Returns

2. Returns-Based Taxes: Deferred Capital Gains

Deferred capital

Effect of Taxes on Investment Returns

2. Returns-Based Taxes: Deferred Capital Gains

Deferred capital

Слайд 133Effect of Taxes on Investment Returns

Example 48:

Assume that €100 are invested at

Effect of Taxes on Investment Returns

Example 48:

Assume that €100 are invested at

Слайд 134Effect of Taxes on Investment Returns

Implications of tax drag (assuming taxes on

Effect of Taxes on Investment Returns

Implications of tax drag (assuming taxes on

Слайд 135Effect of Taxes on Investment Returns

3. Wealth-Based Taxes

Some jurisdictions impose a wealth

Effect of Taxes on Investment Returns

3. Wealth-Based Taxes

Some jurisdictions impose a wealth

Слайд 136Effect of Taxes on Investment Returns

If wealth is taxed annually at a

Effect of Taxes on Investment Returns

If wealth is taxed annually at a

Слайд 137Effect of Taxes on Investment Returns

Implications of tax drag (assuming tax on

Effect of Taxes on Investment Returns

Implications of tax drag (assuming tax on

Слайд 138Effect of Taxes on Investment Returns

Example 51:

Olga lives in a country that

Effect of Taxes on Investment Returns

Example 51:

Olga lives in a country that

Слайд 139Effect of Taxes on Investment Returns

Blended Taxing Environments

In reality, investment portfolios are

Effect of Taxes on Investment Returns

Blended Taxing Environments

In reality, investment portfolios are

Слайд 140Effect of Taxes on Investment Returns

It can be shown that:

Total realized tax

Effect of Taxes on Investment Returns

It can be shown that:

Total realized tax

Слайд 141Effect of Taxes on Investment Returns

Example 52:

Michael has a balanced portfolio of

Effect of Taxes on Investment Returns

Example 52:

Michael has a balanced portfolio of

Слайд 142Effect of Taxes on Investment Returns

Example 52:

Michael has a balanced portfolio of

Effect of Taxes on Investment Returns

Example 52:

Michael has a balanced portfolio of

Слайд 143Effect of Taxes on Investment Returns

Example 52:

Michael has a balanced portfolio of

Effect of Taxes on Investment Returns

Example 52:

Michael has a balanced portfolio of

Слайд 144Effect of Taxes on Investment Returns

Example 52:

Michael has a balanced portfolio of

Effect of Taxes on Investment Returns

Example 52:

Michael has a balanced portfolio of

Слайд 145Chapter 5: CORPORATION TAX

Definition of Corporate Tax

Corporate tax (a.k.a. corporation tax) is

Chapter 5: CORPORATION TAX

Definition of Corporate Tax

Corporate tax (a.k.a. corporation tax) is

Слайд 146Corporate Tax Rates

International Corporate Tax Rates

Corporate tax rates vary widely by country,

Corporate Tax Rates

International Corporate Tax Rates

Corporate tax rates vary widely by country,

Слайд 147The calculation of corporate income taxes due (or refund) is based on

The calculation of corporate income taxes due (or refund) is based on

Слайд 148Explanations:

Gross income may include:

gross profit from inventory sales (sales minus cost of

Explanations:

Gross income may include:

gross profit from inventory sales (sales minus cost of

Слайд 149Some common business deductions are:

Ordinary and necessary business expenses

Corporate Income Tax Calculation

Some common business deductions are:

Ordinary and necessary business expenses

Corporate Income Tax Calculation

Слайд 150Some limitations on business deductions:

Capital expenditures (e.g., expenditures for tangible assets such

Some limitations on business deductions:

Capital expenditures (e.g., expenditures for tangible assets such

Слайд 151Business interest expense

Deduction for business interest expense is limited to the

Business interest expense

Deduction for business interest expense is limited to the

Слайд 152Computing corporate taxable income

To compute taxable income, most corporations begin with

Computing corporate taxable income

To compute taxable income, most corporations begin with

Слайд 153In addition to the favorable/unfavorable distinction, book–tax differences can be categorized as

In addition to the favorable/unfavorable distinction, book–tax differences can be categorized as

Слайд 154Some Common Permanent Book-Tax Differences

Corporate Income Tax Calculation Examples

Source: Spilker, Ayers: Taxation

Some Common Permanent Book-Tax Differences

Corporate Income Tax Calculation Examples

Source: Spilker, Ayers: Taxation

Слайд 155• Temporary book–tax differences arise in one year and reverse in a

• Temporary book–tax differences arise in one year and reverse in a

Слайд 156Some Common Temporary Book-Tax Differences

Corporate Income Tax Calculation Examples

*Note that each of

Some Common Temporary Book-Tax Differences

Corporate Income Tax Calculation Examples

*Note that each of

Слайд 157Corporate-Specific Deductions and Book-Tax Differences

Net Capital Losses

For corporations, all net capital gains

Corporate-Specific Deductions and Book-Tax Differences

Net Capital Losses

For corporations, all net capital gains

Слайд 158Example 53: Book–Tax Reconciliation Template

Source: Spilker, Ayers: Taxation of Individuals and Business

Example 53: Book–Tax Reconciliation Template

Source: Spilker, Ayers: Taxation of Individuals and Business

Слайд 159Example 53: Book–Tax Reconciliation Template

Capital losses of $28,000 are not deducted for

Example 53: Book–Tax Reconciliation Template

Capital losses of $28,000 are not deducted for

Слайд 160Example 53: Book–Tax Reconciliation Template

Initial estimated fair value of stock options is

Example 53: Book–Tax Reconciliation Template

Initial estimated fair value of stock options is

Слайд 161Example 53: Book–Tax Reconciliation Template

Temporary book-tax differences

Example 53: Book–Tax Reconciliation Template

Temporary book-tax differences

Слайд 162Example 53: Book–Tax Reconciliation Template

Business-related meal expenses of $28,000 are fully deductible

Example 53: Book–Tax Reconciliation Template

Business-related meal expenses of $28,000 are fully deductible

Слайд 163Example 53: Book–Tax Reconciliation Template

Corporations deduct federal income tax expense in determining

Example 53: Book–Tax Reconciliation Template

Corporations deduct federal income tax expense in determining

Слайд 164Example 53: Book–Tax Reconciliation Template

Corporations are allowed a deduction for dividends received

Example 53: Book–Tax Reconciliation Template

Corporations are allowed a deduction for dividends received

Слайд 165Corporate income tax liability:

When corporations calculate their taxable income, they compute their

Corporate income tax liability:

When corporations calculate their taxable income, they compute their

Слайд 166Scope of Corporation Tax (U.K. case)

A company's taxable total profits include both

Scope of Corporation Tax (U.K. case)

A company's taxable total profits include both

Слайд 167Calculation of company’s taxable total profits may be summarized as follows:

Corporate Income

Calculation of company’s taxable total profits may be summarized as follows:

Corporate Income

Слайд 168Calculation of company’s taxable total profits may be summarized as follows:

Corporate Income

Calculation of company’s taxable total profits may be summarized as follows:

Corporate Income

Слайд 169Notes:

Trading income consists of company’s trading profit for an accounting period, as

Notes:

Trading income consists of company’s trading profit for an accounting period, as

Слайд 170Example 54:

Calculation of a company’s trading income (UK case)

A company's income statement

Example 54:

Calculation of a company’s trading income (UK case)

A company's income statement

Слайд 1712. Administrative expenses are as follows:

Corporate Income Tax Calculation Examples

Compute the company's

2. Administrative expenses are as follows:

Corporate Income Tax Calculation Examples

Compute the company's

Слайд 172Solution:

Corporate Income Tax Calculation Examples

Gift Aid donations are disallowed when computing trading

Solution:

Corporate Income Tax Calculation Examples

Gift Aid donations are disallowed when computing trading

Слайд 173Solution:

Corporate Income Tax Calculation Examples

Losses caused by the dishonesty of a director

Solution:

Corporate Income Tax Calculation Examples

Losses caused by the dishonesty of a director

Слайд 174Computation of Corporation Tax Liability (U.K. case)

Given a company's taxable total profits

Computation of Corporation Tax Liability (U.K. case)

Given a company's taxable total profits

Слайд 175Chapter 6: INDIRECT TAXES: VALUE-ADDED TAX

Definition of Value Added Tax

Value added tax

Chapter 6: INDIRECT TAXES: VALUE-ADDED TAX

Definition of Value Added Tax

Value added tax

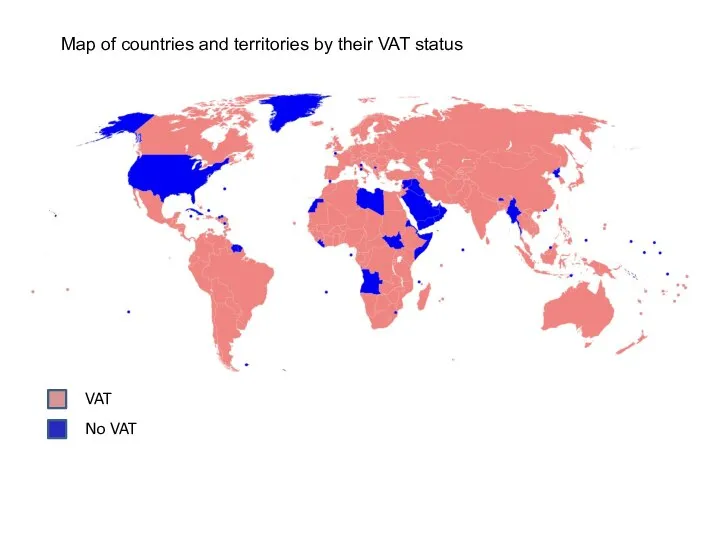

Слайд 176Map of countries and territories by their VAT status

VAT

No VAT

Map of countries and territories by their VAT status

VAT

No VAT

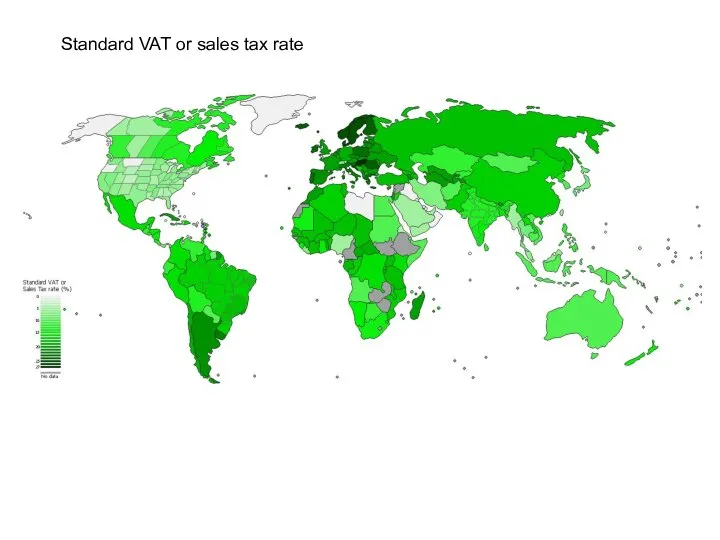

Слайд 177Standard VAT or sales tax rate

Standard VAT or sales tax rate

Слайд 178Value Added Tax Rates in Europe

Value Added Tax Rates in Europe

Слайд 179VAT Calculation Principles

A VAT is levied on the gross margin at each

VAT Calculation Principles

A VAT is levied on the gross margin at each

Слайд 180Example 55:

Value Added Tax

Assume a VAT of 10%.

A farmer sells wheat

Example 55:

Value Added Tax

Assume a VAT of 10%.

A farmer sells wheat

Слайд 181Example 55:

Value Added Tax

The baker uses the wheat to make bread and

Example 55:

Value Added Tax

The baker uses the wheat to make bread and

Слайд 182Example 55:

Value Added Tax

Finally, the supermarket sells the loaf of bread to

Example 55:

Value Added Tax

Finally, the supermarket sells the loaf of bread to

Слайд 183VAT vs. Sales Tax

Sales tax is assessed only once at the final

VAT vs. Sales Tax

Sales tax is assessed only once at the final

Слайд 184VAT: Advantages

Adoption of a regressive tax system, such as VAT, gives people

VAT: Advantages

Adoption of a regressive tax system, such as VAT, gives people

Слайд 185VAT: Disadvantages

Unlike the income tax rate, which varies at different levels of

VAT: Disadvantages

Unlike the income tax rate, which varies at different levels of

Слайд 186Value Added Tax (U.K. case)

The basic principle of VAT is that tax

Value Added Tax (U.K. case)

The basic principle of VAT is that tax

Слайд 187Example 57:

A Ltd owns a quarry. It extracts stone from this quarry

Example 57:

A Ltd owns a quarry. It extracts stone from this quarry

Слайд 188Example 57:

A Ltd owns a quarry. It extracts stone from this quarry

Example 57:

A Ltd owns a quarry. It extracts stone from this quarry

Слайд 189Chapter 7: INTERNATIONAL TAXATION ASPECTS

Taxation Systems

Countries that tax income generally use one

Chapter 7: INTERNATIONAL TAXATION ASPECTS

Taxation Systems

Countries that tax income generally use one

Слайд 191Taxation of income

Under source jurisdiction a country levies taxes on all income

Taxation of income

Under source jurisdiction a country levies taxes on all income

Слайд 192Double Taxation Conflicts

Interaction of country tax systems can result in tax conflicts

Double Taxation Conflicts

Interaction of country tax systems can result in tax conflicts

Слайд 193Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Слайд 194Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Слайд 195Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Слайд 196Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Слайд 197Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Слайд 198Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Слайд 199Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Слайд 200Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Foreign Tax Credit Provisions

A residence country may choose to unilaterally provide its

Слайд 201Double Taxation Treaties

Relief from double taxation may be provided through a double

Double Taxation Treaties

Relief from double taxation may be provided through a double

Слайд 202Double Taxation Treaties

In addition to residence–source conflicts, DTTs resolve residence–residence conflicts.

A

Double Taxation Treaties

In addition to residence–source conflicts, DTTs resolve residence–residence conflicts.

A

Слайд 203Tax Avoidance vs. Tax Evasion

Tax avoidance (a.k.a. “tax minimization”) uses legal means

Tax Avoidance vs. Tax Evasion

Tax avoidance (a.k.a. “tax minimization”) uses legal means

Слайд 204Current Trends in International Transparency and Information Exchange

Most countries attempt to maximize

Current Trends in International Transparency and Information Exchange

Most countries attempt to maximize

Слайд 205Current Trends in International Transparency and Information Exchange

Most countries attempt to maximize

Current Trends in International Transparency and Information Exchange

Most countries attempt to maximize

Слайд 206Current Trends in International Transparency and Information Exchange

Most countries attempt to maximize

Current Trends in International Transparency and Information Exchange

Most countries attempt to maximize

Слайд 207Common Tax Evasion Schemes

Falsifying information on tax return

This occurs when a taxpayer

Common Tax Evasion Schemes

Falsifying information on tax return

This occurs when a taxpayer

Слайд 208Transfer Pricing

Transfer pricing is an accounting practice that represents the price that

Transfer Pricing

Transfer pricing is an accounting practice that represents the price that

Слайд 209Example 62:

Transfer Pricing as a Tax Reduction Strategy

A U.S. parent has

Example 62:

Transfer Pricing as a Tax Reduction Strategy

A U.S. parent has

Слайд 210Example 62:

Transfer Pricing as a Tax Reduction Strategy

A U.S. parent has

Example 62:

Transfer Pricing as a Tax Reduction Strategy

A U.S. parent has

Слайд 211Example 62:

Transfer Pricing as a Tax Reduction Strategy

A U.S. parent has

Example 62:

Transfer Pricing as a Tax Reduction Strategy

A U.S. parent has

Слайд 212Example 62:

Transfer Pricing as a Tax Reduction Strategy

A U.S. parent has

Example 62:

Transfer Pricing as a Tax Reduction Strategy

A U.S. parent has

Слайд 213Example 62:

Transfer Pricing as a Tax Reduction Strategy

A U.S. parent has

Example 62:

Transfer Pricing as a Tax Reduction Strategy

A U.S. parent has

Слайд 214Transfer Pricing via Tax Haven

Transfer pricing is a technique used by multinational

Transfer Pricing via Tax Haven

Transfer pricing is a technique used by multinational

Слайд 215Tax Haven

A tax haven (a.k.a., offshore financial center) is a tax jurisdiction

Tax Haven

A tax haven (a.k.a., offshore financial center) is a tax jurisdiction

Food. Еда

Food. Еда Fonetika Fairyland

Fonetika Fairyland Verb to be

Verb to be Verbs. Numbers. Dates

Verbs. Numbers. Dates Adjective to + verb

Adjective to + verb Winter - Зима

Winter - Зима Sunshine Sight Word Puzzles

Sunshine Sight Word Puzzles Sports

Sports Can I help

Can I help Combination of words

Combination of words Description of the picture

Description of the picture Let's dance. Game

Let's dance. Game Глаголы. Найди верный перевод

Глаголы. Найди верный перевод Distant lesson

Distant lesson Набор карандашей

Набор карандашей Our Future Profession Учитель английского языка МБОУ «Новотроицкая СОШ», Альметьевский район

Our Future Profession Учитель английского языка МБОУ «Новотроицкая СОШ», Альметьевский район Conversation topics Do you think that films can be educational?

Conversation topics Do you think that films can be educational? Как начать изучать английский

Как начать изучать английский Prepositions

Prepositions There is or There are?

There is or There are? Plural

Plural Презентация на тему THE TOWER OF LONDON

Презентация на тему THE TOWER OF LONDON  Grammar

Grammar Буквосочетание ow

Буквосочетание ow Dangerous in driving a car

Dangerous in driving a car Grammar 4.2

Grammar 4.2 Кафедра учителей английского языка МОУ лицея №14 г.Ставрополя

Кафедра учителей английского языка МОУ лицея №14 г.Ставрополя Morphology

Morphology