- Econometrics

Содержание

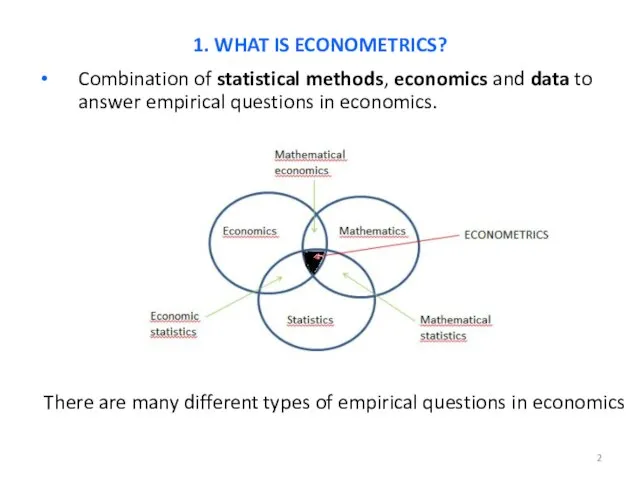

- 2. Combination of statistical methods, economics and data to answer empirical questions in economics. 1. WHAT IS

- 3. Estimation of economic relationships: - Demand and supply equations; - Production functions; - Wage equations, etc.

- 4. Econometrics is relevant in virtually every branch of applied economics: finance, labor, health, industrial, macro, development,

- 5. The research process in applied econometrics is not simply linear, but it has “loops”. That is,

- 6. Step 1: Empirical question(s) Learning-by-doing (LBD) is the process by which the cost of producing a

- 7. Step 2: Collection of data There are different of datasets that can be collected to study

- 8. Step 3: Specification of the Econometric Model An Econometric Model is an economic model where we

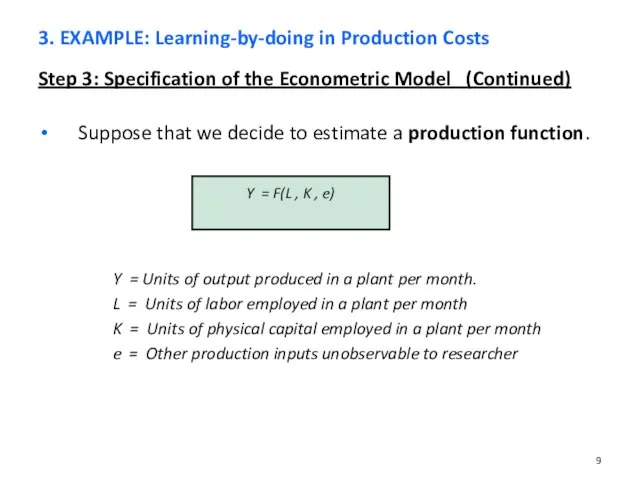

- 9. Step 3: Specification of the Econometric Model (Continued) Suppose that we decide to estimate a production

- 10. Step 3: Specification of the Econometric Model (Continued) An important specification assumption is the choice of

- 11. Step 3: Specification of the econometric model (continued) Dealing with the unobservable (or error term or

- 12. Step 4: Estimation, validation, hypotheses testing, prediction We want to estimate the parameters β in the

- 13. Different types of datasets have their own issues, advantages and limitations. Some econometric methods may be

- 14. Cross-Sectional Data A cross-sectional dataset is a sample of individuals, or households, or firms, or cities,

- 15. Time Series Data A time series dataset consists of observations on a variable or several variables

- 16. Pooled cross sections Suppose that we have a sequence of cross sections of the same variables

- 17. Panel Data In panel data we have a group of individuals (or households, firms, countries, …)

- 18. Most empirical questions in economics are associated to the identification of CAUSAL EFFECTS. The notion of

- 19. In most applications, we can not hold ALL the relevant factors constant. There is an immense

- 20. Does it mean that we cannot identify causal effects? Not necessarily. In fact, there are cases

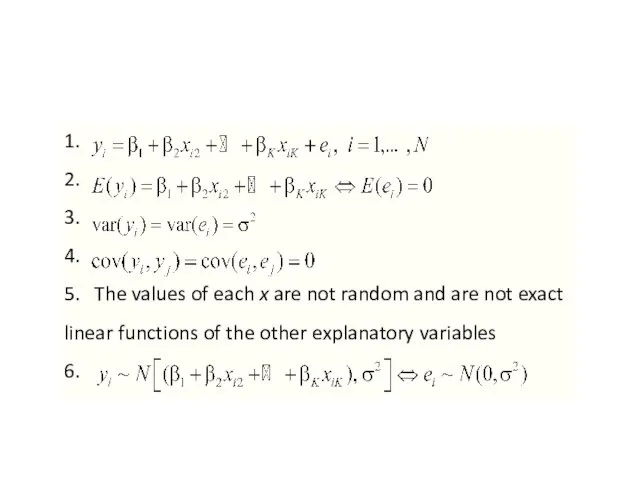

- 21. We make two assumptions about the explanatory variables: The explanatory variables are not random variables We

- 22. We make two assumptions about the explanatory variables (Continued): Any one of the explanatory variables is

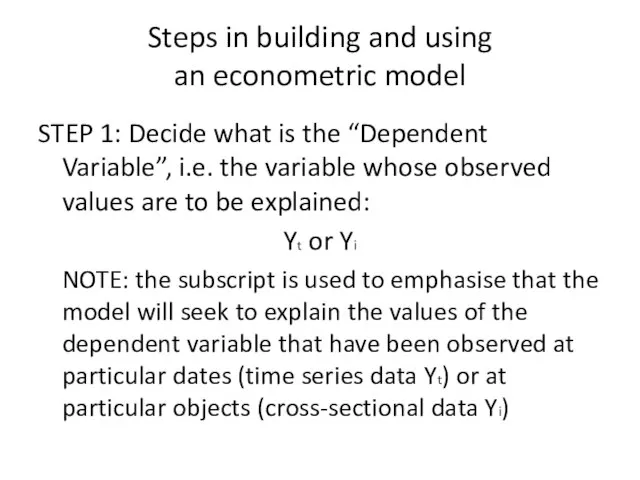

- 24. Steps in building and using an econometric model STEP 1: Decide what is the “Dependent Variable”,

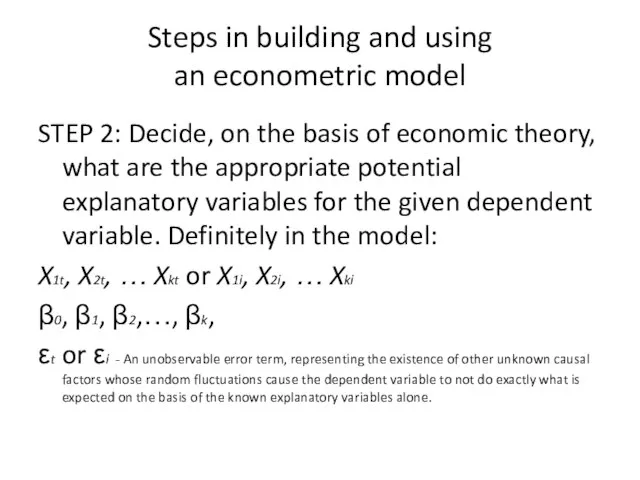

- 25. Steps in building and using an econometric model STEP 2: Decide, on the basis of economic

- 26. Steps in building and using an econometric model STEP 3: Note the anticipated signs of the

- 27. Steps in building and using an econometric model STEP 4: Decide the data sample NOTE: n

- 28. Steps in building and using an econometric model STEP 5: Estimate the model: Using the Ordinary

- 29. Steps in building and using an econometric model STEP 6: Assess the diagnostic statistics: [Remember: econometrics

- 30. Steps in building and using an econometric model STEP 7: Interpret the results: [Remember: econometrics can

- 32. Скачать презентацию

Слайд 3Estimation of economic relationships:

- Demand and supply equations;

- Production functions;

- Wage

Estimation of economic relationships:

- Demand and supply equations;

- Production functions;

- Wage

Слайд 4Econometrics is relevant in virtually every branch of applied economics: finance, labor,

Econometrics is relevant in virtually every branch of applied economics: finance, labor,

Слайд 5The research process in applied econometrics is not simply linear, but it

The research process in applied econometrics is not simply linear, but it

Слайд 6Step 1: Empirical question(s)

Learning-by-doing (LBD) is the process by which the cost

Step 1: Empirical question(s)

Learning-by-doing (LBD) is the process by which the cost

Слайд 7Step 2: Collection of data

There are different of datasets that can be

Step 2: Collection of data

There are different of datasets that can be

Слайд 8Step 3: Specification of the Econometric Model

An Econometric Model is an economic

Step 3: Specification of the Econometric Model

An Econometric Model is an economic

Слайд 9Step 3: Specification of the Econometric Model (Continued)

Suppose that we decide

Step 3: Specification of the Econometric Model (Continued)

Suppose that we decide

Слайд 10Step 3: Specification of the Econometric Model (Continued)

An important specification assumption

Step 3: Specification of the Econometric Model (Continued)

An important specification assumption

Слайд 11Step 3: Specification of the econometric model (continued)

Dealing with the unobservable (or

Step 3: Specification of the econometric model (continued)

Dealing with the unobservable (or

Слайд 12Step 4: Estimation, validation, hypotheses testing, prediction

We want to estimate the parameters

Step 4: Estimation, validation, hypotheses testing, prediction

We want to estimate the parameters

Слайд 13Different types of datasets have their own issues, advantages and limitations.

Some econometric

Different types of datasets have their own issues, advantages and limitations.

Some econometric

Слайд 14Cross-Sectional Data

A cross-sectional dataset is a sample of individuals, or households, or

Cross-Sectional Data

A cross-sectional dataset is a sample of individuals, or households, or

Слайд 15Time Series Data

A time series dataset consists of observations on a variable

Time Series Data

A time series dataset consists of observations on a variable

Слайд 16Pooled cross sections

Suppose that we have a sequence of cross sections of

Pooled cross sections

Suppose that we have a sequence of cross sections of

Слайд 17Panel Data

In panel data we have a group of individuals (or households,

Panel Data

In panel data we have a group of individuals (or households,

Слайд 18Most empirical questions in economics are associated to the identification of CAUSAL

Most empirical questions in economics are associated to the identification of CAUSAL

Слайд 19In most applications, we can not hold ALL the relevant factors constant.

In most applications, we can not hold ALL the relevant factors constant.

Слайд 20Does it mean that we cannot identify causal effects?

Not necessarily. In

Does it mean that we cannot identify causal effects?

Not necessarily. In

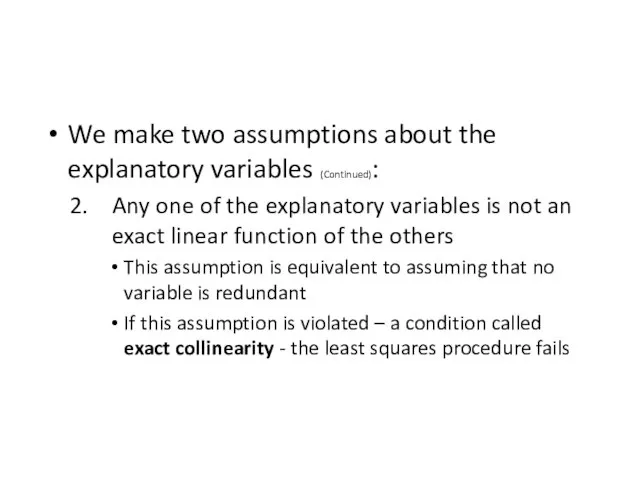

Слайд 21We make two assumptions about the explanatory variables:

The explanatory variables are not

The explanatory variables are not

Слайд 22We make two assumptions about the explanatory variables (Continued):

Any one of

Any one of

Слайд 24

Steps in building and using

an econometric model

STEP 1: Decide what is

Steps in building and using

an econometric model

STEP 1: Decide what is

Слайд 25

Steps in building and using

an econometric model

STEP 2: Decide, on the

Steps in building and using

an econometric model

STEP 2: Decide, on the

Слайд 26

Steps in building and using

an econometric model

STEP 3: Note the anticipated

Steps in building and using

an econometric model

STEP 3: Note the anticipated

Слайд 27

Steps in building and using

an econometric model

STEP 4: Decide the data

Steps in building and using

an econometric model

STEP 4: Decide the data

Слайд 28

Steps in building and using

an econometric model

STEP 5: Estimate the model:

Using

Steps in building and using

an econometric model

STEP 5: Estimate the model:

Using

Слайд 29

Steps in building and using

an econometric model

STEP 6: Assess the diagnostic

Steps in building and using

an econometric model

STEP 6: Assess the diagnostic

Слайд 30

Steps in building and using

an econometric model

STEP 7: Interpret the results:

[Remember:

Steps in building and using

an econometric model

STEP 7: Interpret the results:

[Remember:

Слова с сочетаниями ЖИ-ШИ

Слова с сочетаниями ЖИ-ШИ Цвет. Основы цветоведения

Цвет. Основы цветоведения О компании PR-Агентство "Медиастиль" предоставляет высококвалифицированные услуги в сфере связей с общественностью. Область нашей

О компании PR-Агентство "Медиастиль" предоставляет высококвалифицированные услуги в сфере связей с общественностью. Область нашей  Литеййное производство

Литеййное производство Роль писателя в совершенствовании языка

Роль писателя в совершенствовании языка Презентация на тему Первые христиане и их учение

Презентация на тему Первые христиане и их учение Древние образы в современных народных игрушках

Древние образы в современных народных игрушках СМЕСИТЕЛИ

СМЕСИТЕЛИ Воспитание Россиянина в условиях поликультурного образования

Воспитание Россиянина в условиях поликультурного образования Принципы воспитания (физического)

Принципы воспитания (физического)  Презентация на тему Деление десятичных дробей

Презентация на тему Деление десятичных дробей Школа будущего

Школа будущего Козловская Диана. Грамоты

Козловская Диана. Грамоты Великая Отечественная война в Заполярье

Великая Отечественная война в Заполярье www.sales.ua

www.sales.ua «Оно оказывает значительное целебное воздействие, укрепляет желудок, останавливает рвоту, возбуждает аппетит и очищает кровь; спо

«Оно оказывает значительное целебное воздействие, укрепляет желудок, останавливает рвоту, возбуждает аппетит и очищает кровь; спо Урок по творчеству шведской писательницы А.Линдгрен.

Урок по творчеству шведской писательницы А.Линдгрен. Афродита

Афродита «Кукла моей бабушки»

«Кукла моей бабушки» Мой дедушка - участник Второй Мировой Войны

Мой дедушка - участник Второй Мировой Войны Результаты итоговой аттестации за курс средней школы

Результаты итоговой аттестации за курс средней школы Облака. Наша идея

Облака. Наша идея Ключи от форта Математика

Ключи от форта Математика Воскресенские (Иверские) ворота

Воскресенские (Иверские) ворота Новгородский государственный университет им. Ярослава Мудрого. Кафедра отраслевого менеджмента

Новгородский государственный университет им. Ярослава Мудрого. Кафедра отраслевого менеджмента Эстетическое воспитание

Эстетическое воспитание Дом мод

Дом мод Фразеологизмы и их особенности

Фразеологизмы и их особенности