- Financial Planning

Содержание

- 2. Task of financial planning Cover a short time span Take a long term perspective Focus on

- 3. Financial plan Adaptable tool for management to use to achieve its strategic goals Translation of strategic

- 4. Goals of financial planning Three important uses: Forecast the amount and sources of financing that will

- 5. What answers should Financial planning give to the manager? What is the size of financial funds

- 6. Financial planning Long term – more than 3 years Medium-term – for 1-3 years Short-term -

- 7. Financial Planning The projection of sales, income, and assets based on alternative production and marketing strategies,

- 8. Steps to get AFN – simple one-pass forecast balance sheet method Calculate RE with the data

- 9. Steps in Financial Forecasting Forecast sales Project the assets needed to support sales Project internally generated

- 10. 2013 Balance Sheet (Millions of $)

- 11. 2013 Income Statement (Millions of $)

- 12. AFN (Additional Funds Needed): Key Assumptions Operating at full capacity in 2013. Each type of asset

- 13. Assets Sales 0 1,000 2,000 1,250 2,500 A*/S0 = $1,000/$2,000 = 0.5 = $1,250/$2,500. Δ Assets

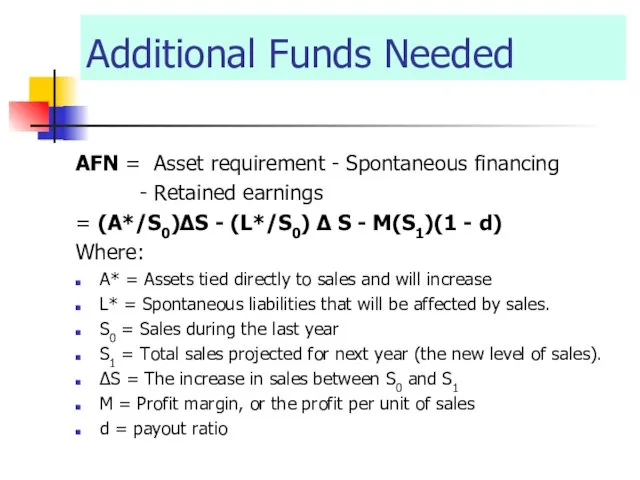

- 14. Additional Funds Needed AFN = Asset requirement - Spontaneous financing - Retained earnings = (A*/S0)ΔS -

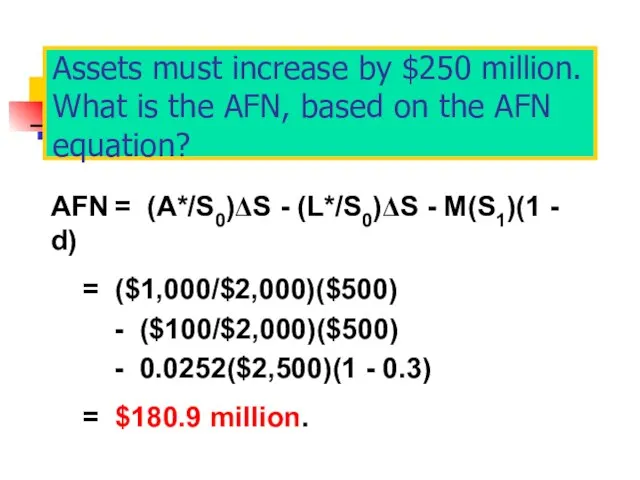

- 15. Assets must increase by $250 million. What is the AFN, based on the AFN equation? AFN

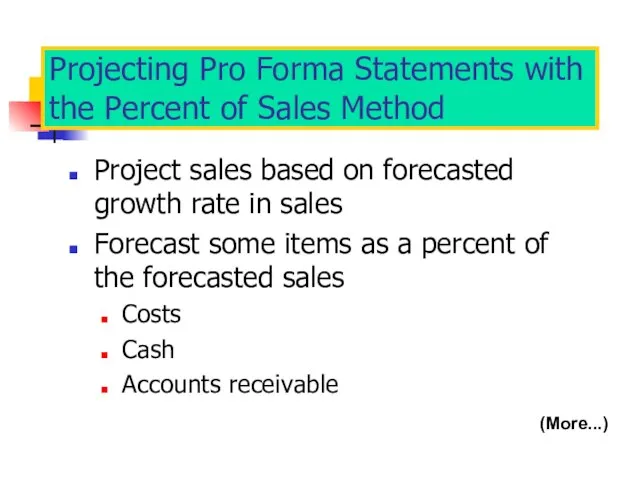

- 16. Projecting Pro Forma Statements with the Percent of Sales Method Project sales based on forecasted growth

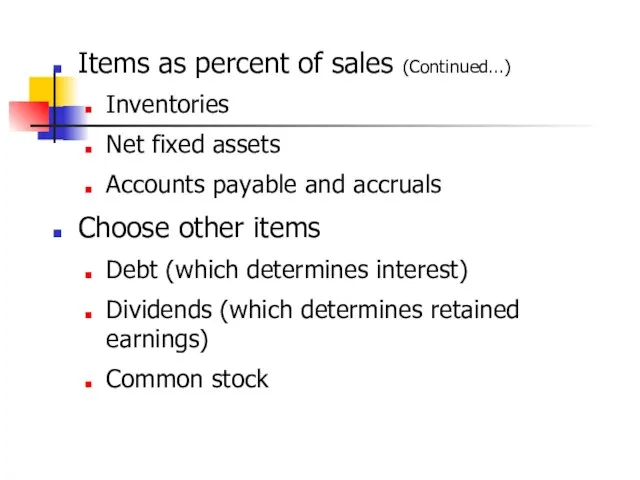

- 17. Items as percent of sales (Continued...) Inventories Net fixed assets Accounts payable and accruals Choose other

- 18. Percent of Sales: Inputs

- 19. Other Inputs

- 20. 2014 1st Pass Income Statement

- 21. 2014 1st Pass Balance Sheet (Assets) Forecasted assets are a percent of forecasted sales.

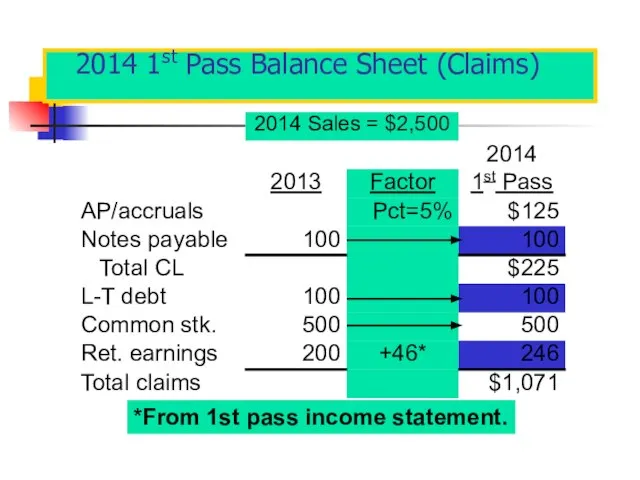

- 22. 2014 1st Pass Balance Sheet (Claims) *From 1st pass income statement.

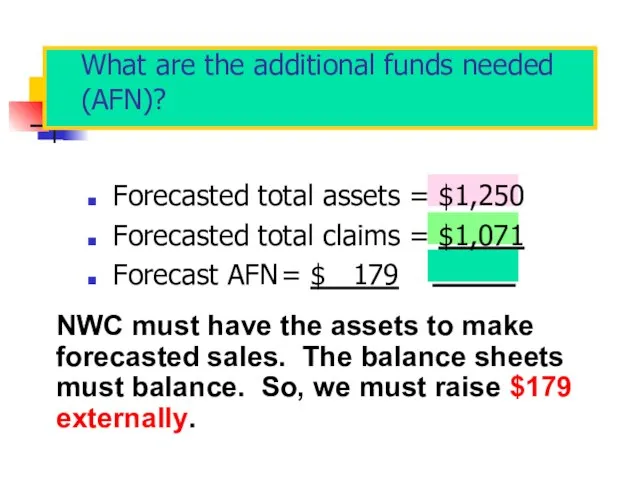

- 23. What are the additional funds needed (AFN)? Forecasted total assets = $1,250 Forecasted total claims =

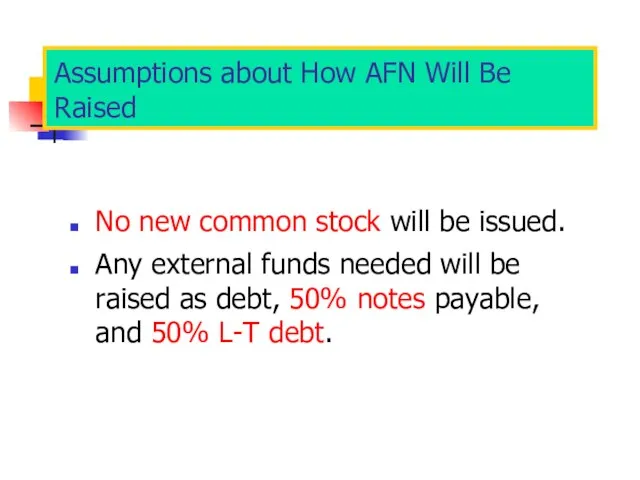

- 24. Assumptions about How AFN Will Be Raised No new common stock will be issued. Any external

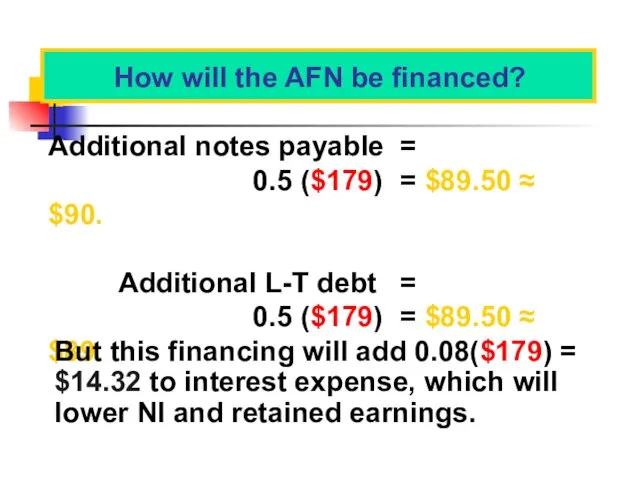

- 25. How will the AFN be financed? Additional notes payable = 0.5 ($179) = $89.50 ≈ $90.

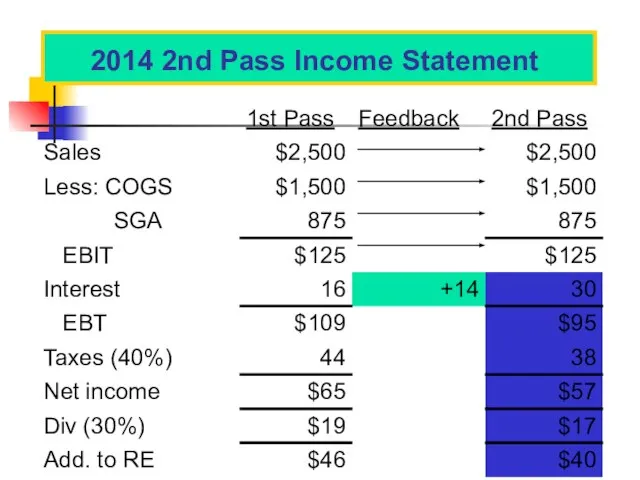

- 26. 2014 2nd Pass Income Statement

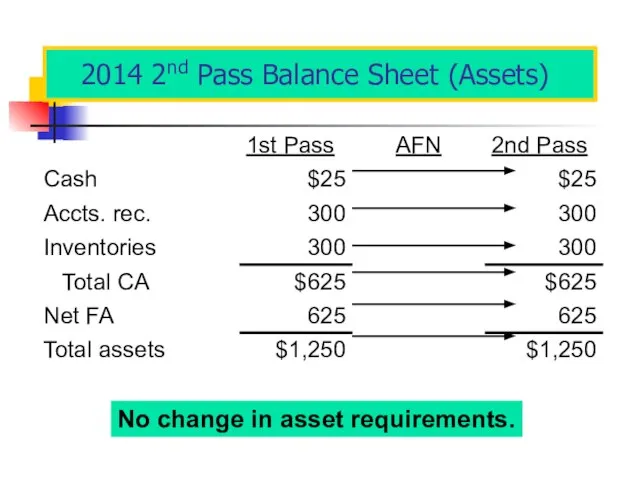

- 27. 2014 2nd Pass Balance Sheet (Assets) No change in asset requirements.

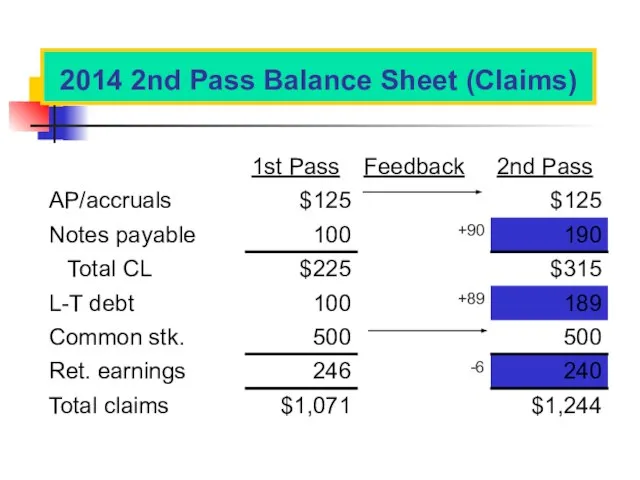

- 28. 2014 2nd Pass Balance Sheet (Claims)

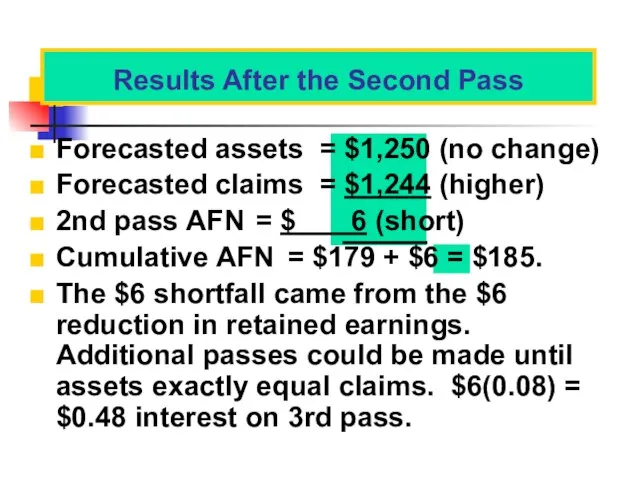

- 29. Forecasted assets = $1,250 (no change) Forecasted claims = $1,244 (higher) 2nd pass AFN = $

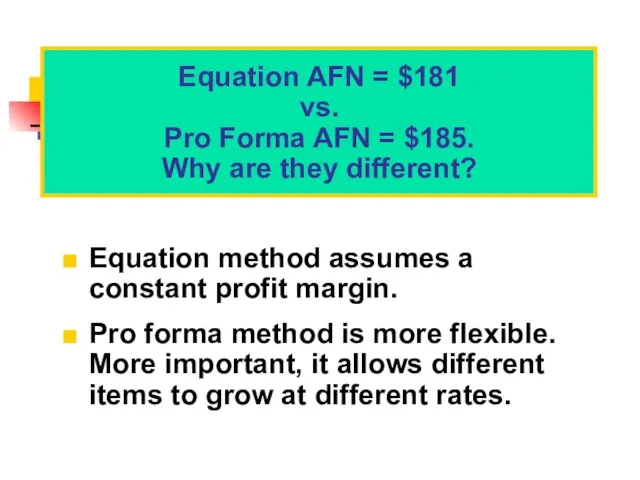

- 30. Equation method assumes a constant profit margin. Pro forma method is more flexible. More important, it

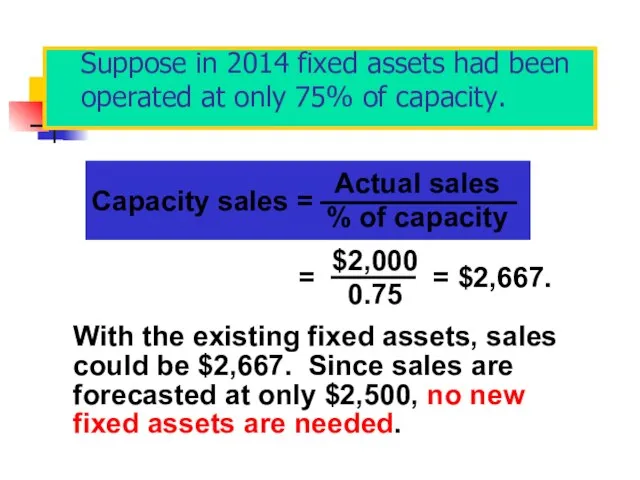

- 31. Suppose in 2014 fixed assets had been operated at only 75% of capacity. With the existing

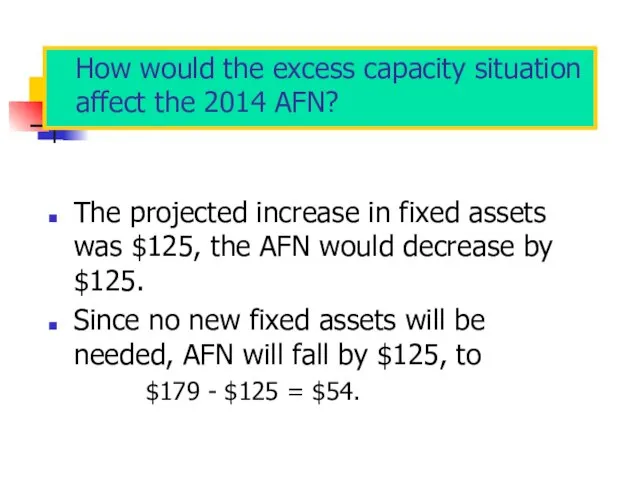

- 32. How would the excess capacity situation affect the 2014 AFN? The projected increase in fixed assets

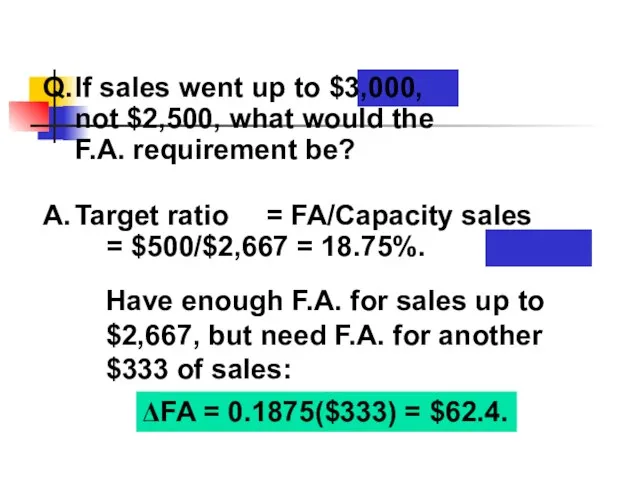

- 33. Q. If sales went up to $3,000, not $2,500, what would the F.A. requirement be? A.

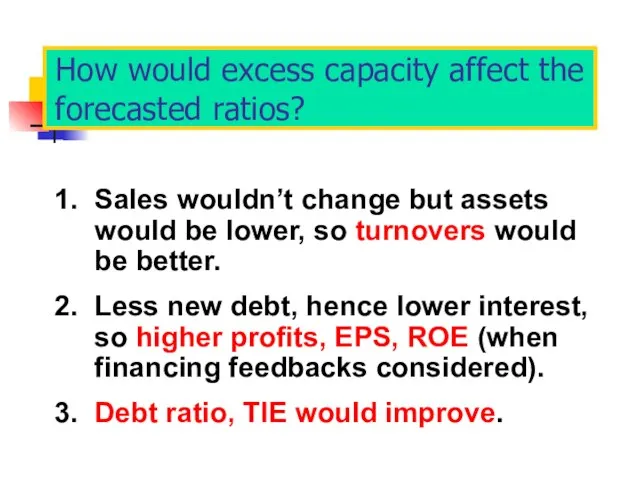

- 34. How would excess capacity affect the forecasted ratios? 1. Sales wouldn’t change but assets would be

- 35. Regression Analysis for Asset Forecasting Get historical data on a good company, then fit a regression

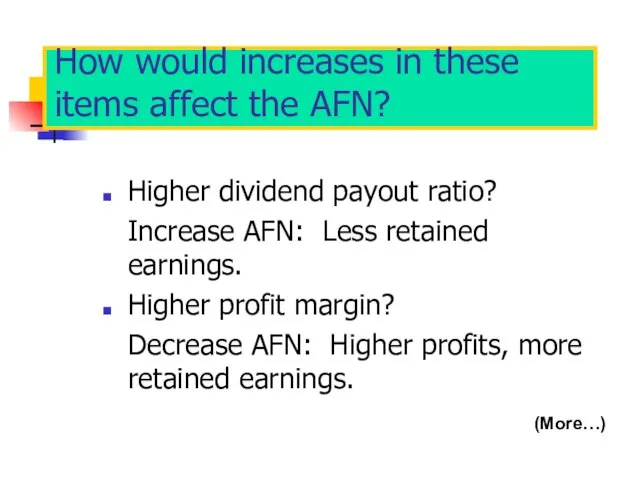

- 36. How would increases in these items affect the AFN? Higher dividend payout ratio? Increase AFN: Less

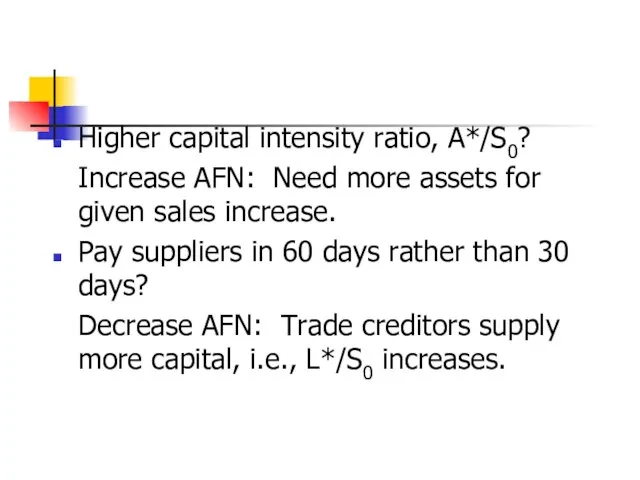

- 37. Higher capital intensity ratio, A*/S0? Increase AFN: Need more assets for given sales increase. Pay suppliers

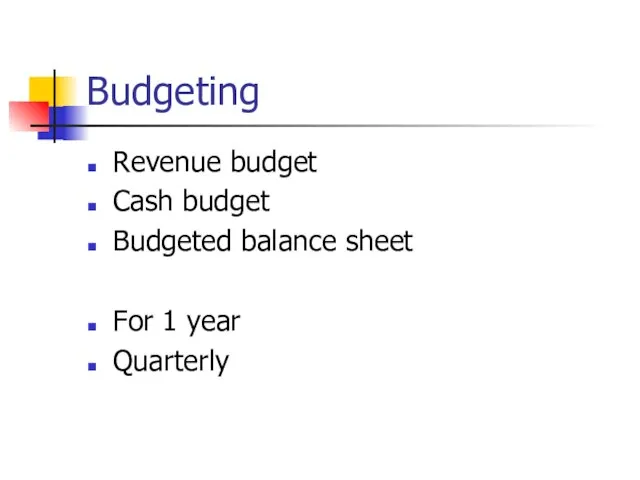

- 38. Budgeting Revenue budget Cash budget Budgeted balance sheet For 1 year Quarterly

- 40. Скачать презентацию

Слайд 3Financial plan

Adaptable tool for management to use to achieve its strategic goals

Translation

Financial plan

Adaptable tool for management to use to achieve its strategic goals

Translation

Слайд 4Goals of financial planning

Three important uses:

Forecast the amount and sources of financing

Goals of financial planning

Three important uses:

Forecast the amount and sources of financing

Слайд 5What answers should Financial planning give to the manager?

What is the size

What answers should Financial planning give to the manager?

What is the size

Слайд 6Financial planning

Long term – more than 3 years

Medium-term – for 1-3 years

Short-term

Financial planning

Long term – more than 3 years

Medium-term – for 1-3 years

Short-term

Слайд 7Financial Planning

The projection of sales, income, and assets based on alternative production

Financial Planning

The projection of sales, income, and assets based on alternative production

Слайд 8Steps to get AFN – simple one-pass forecast balance sheet method

Calculate RE

Steps to get AFN – simple one-pass forecast balance sheet method

Calculate RE

Слайд 9Steps in Financial Forecasting

Forecast sales

Project the assets needed to support sales

Project internally

Steps in Financial Forecasting

Forecast sales

Project the assets needed to support sales

Project internally

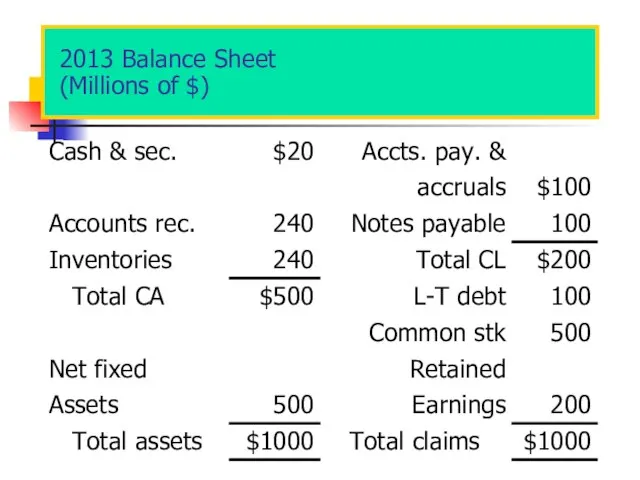

Слайд 102013 Balance Sheet

(Millions of $)

2013 Balance Sheet

(Millions of $)

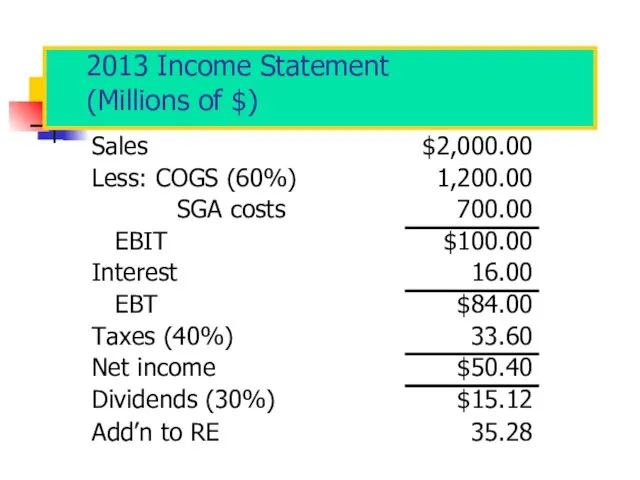

Слайд 112013 Income Statement

(Millions of $)

2013 Income Statement

(Millions of $)

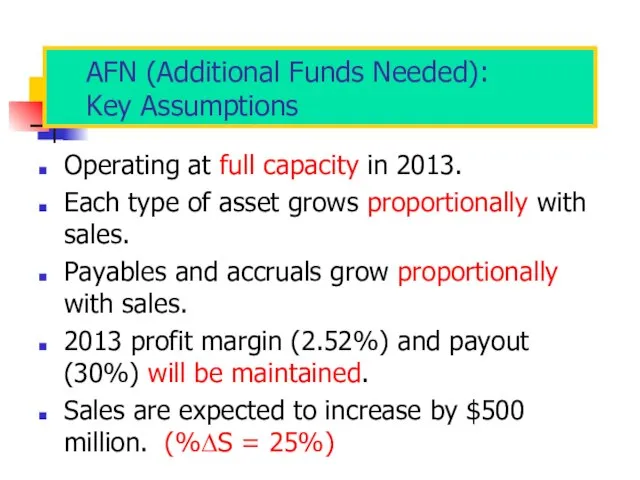

Слайд 12AFN (Additional Funds Needed):

Key Assumptions

Operating at full capacity in 2013.

Each type of

AFN (Additional Funds Needed):

Key Assumptions

Operating at full capacity in 2013.

Each type of

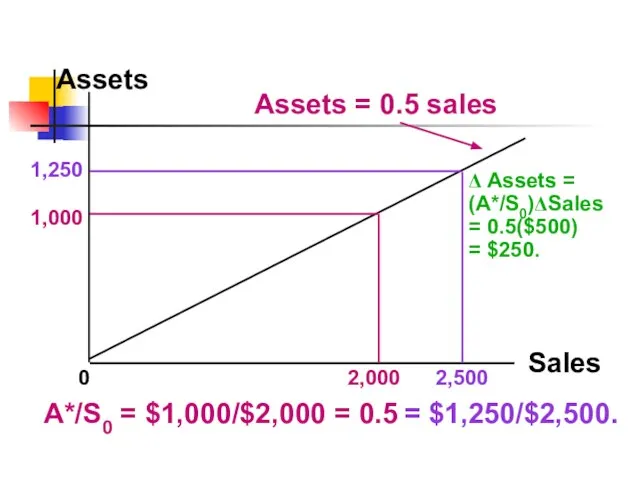

Слайд 13Assets

Sales

0

1,000

2,000

1,250

2,500

A*/S0 = $1,000/$2,000 = 0.5

= $1,250/$2,500.

Δ Assets =

(A*/S0)ΔSales

= 0.5($500)

= $250.

Assets = 0.5

Assets

Sales

0

1,000

2,000

1,250

2,500

A*/S0 = $1,000/$2,000 = 0.5

= $1,250/$2,500.

Δ Assets =

(A*/S0)ΔSales

= 0.5($500)

= $250.

Assets = 0.5

Слайд 14Additional Funds Needed

AFN = Asset requirement - Spontaneous financing

- Retained earnings

= (A*/S0)ΔS

Additional Funds Needed

AFN = Asset requirement - Spontaneous financing

- Retained earnings

= (A*/S0)ΔS

Слайд 15Assets must increase by $250 million. What is the AFN, based on

Assets must increase by $250 million. What is the AFN, based on

Слайд 16Projecting Pro Forma Statements with the Percent of Sales Method

Project sales based

Projecting Pro Forma Statements with the Percent of Sales Method

Project sales based

Слайд 17Items as percent of sales (Continued...)

Inventories

Net fixed assets

Accounts payable and accruals

Choose other

Items as percent of sales (Continued...)

Inventories

Net fixed assets

Accounts payable and accruals

Choose other

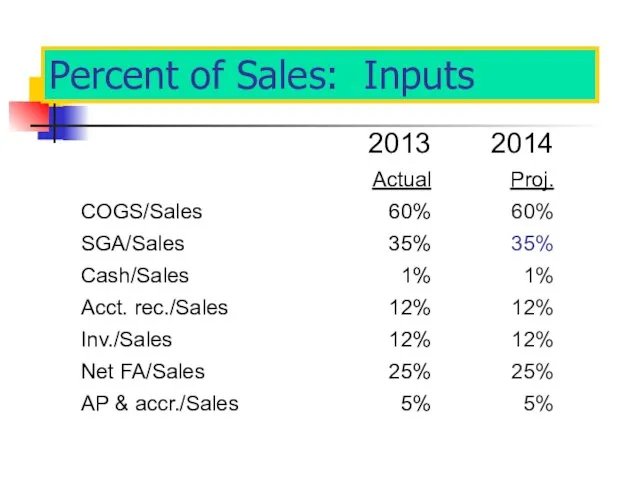

Слайд 18Percent of Sales: Inputs

Percent of Sales: Inputs

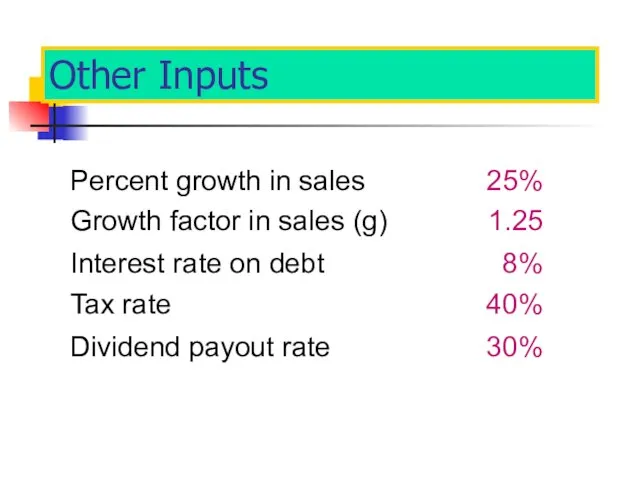

Слайд 19Other Inputs

Other Inputs

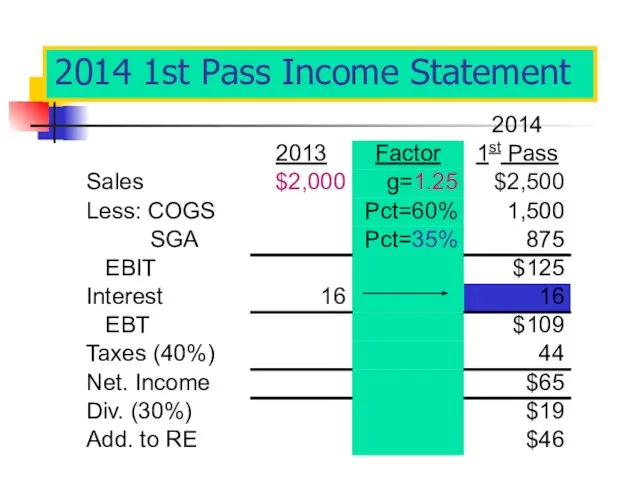

Слайд 202014 1st Pass Income Statement

2014 1st Pass Income Statement

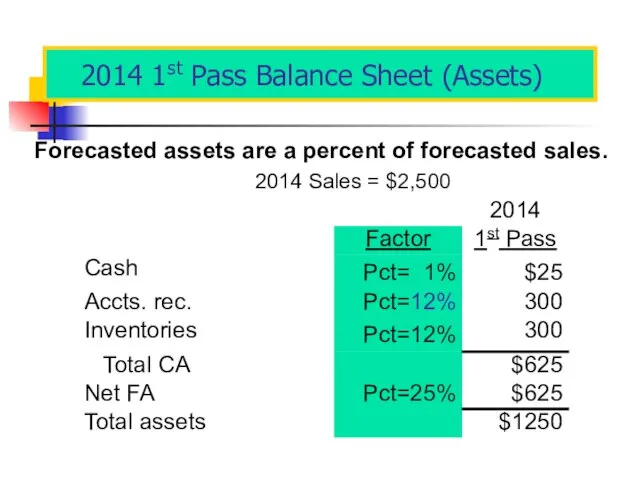

Слайд 212014 1st Pass Balance Sheet (Assets)

Forecasted assets are a percent of forecasted

2014 1st Pass Balance Sheet (Assets)

Forecasted assets are a percent of forecasted

Слайд 222014 1st Pass Balance Sheet (Claims)

*From 1st pass income statement.

2014 1st Pass Balance Sheet (Claims)

*From 1st pass income statement.

Слайд 23What are the additional funds needed (AFN)?

Forecasted total assets = $1,250

Forecasted total claims =

What are the additional funds needed (AFN)?

Forecasted total assets = $1,250

Forecasted total claims =

Слайд 24Assumptions about How AFN Will Be Raised

No new common stock will be

Assumptions about How AFN Will Be Raised

No new common stock will be

Слайд 25How will the AFN be financed?

Additional notes payable =

0.5 ($179) = $89.50 ≈

How will the AFN be financed?

Additional notes payable =

0.5 ($179) = $89.50 ≈

Слайд 262014 2nd Pass Income Statement

2014 2nd Pass Income Statement

Слайд 272014 2nd Pass Balance Sheet (Assets)

No change in asset requirements.

2014 2nd Pass Balance Sheet (Assets)

No change in asset requirements.

Слайд 282014 2nd Pass Balance Sheet (Claims)

2014 2nd Pass Balance Sheet (Claims)

Слайд 29Forecasted assets = $1,250 (no change)

Forecasted claims = $1,244 (higher)

2nd pass AFN = $ 6

Forecasted assets = $1,250 (no change)

Forecasted claims = $1,244 (higher)

2nd pass AFN = $ 6

Слайд 30Equation method assumes a constant profit margin.

Pro forma method is more flexible.

Equation method assumes a constant profit margin.

Pro forma method is more flexible.

Слайд 31Suppose in 2014 fixed assets had been operated at only 75% of

Suppose in 2014 fixed assets had been operated at only 75% of

Слайд 32How would the excess capacity situation affect the 2014 AFN?

The projected increase

How would the excess capacity situation affect the 2014 AFN?

The projected increase

Слайд 33Q. If sales went up to $3,000,

not $2,500, what would the

F.A.

Q. If sales went up to $3,000,

not $2,500, what would the

F.A.

Слайд 34How would excess capacity affect the forecasted ratios?

1. Sales wouldn’t change but assets

How would excess capacity affect the forecasted ratios?

1. Sales wouldn’t change but assets

Слайд 35Regression Analysis for Asset Forecasting

Get historical data on a good company, then

Regression Analysis for Asset Forecasting

Get historical data on a good company, then

Слайд 36How would increases in these items affect the AFN?

Higher dividend payout ratio?

Increase

How would increases in these items affect the AFN?

Higher dividend payout ratio?

Increase

Слайд 37Higher capital intensity ratio, A*/S0?

Increase AFN: Need more assets for given sales

Higher capital intensity ratio, A*/S0?

Increase AFN: Need more assets for given sales

Слайд 38Budgeting

Revenue budget

Cash budget

Budgeted balance sheet

For 1 year

Quarterly

Budgeting

Revenue budget

Cash budget

Budgeted balance sheet

For 1 year

Quarterly

Clever

Clever Праздничные народные гулянья. Урок изобразительного искусства. 5 класс

Праздничные народные гулянья. Урок изобразительного искусства. 5 класс Тöс ле эчеҥи члендер

Тöс ле эчеҥи члендер ЕГЭ 2010 задачи С1-С6

ЕГЭ 2010 задачи С1-С6 Справка о МТО

Справка о МТО Учебно-методическое обеспечение современного образования подростков

Учебно-методическое обеспечение современного образования подростков Размещение бытового газоборудования в квартирах

Размещение бытового газоборудования в квартирах Нормы, закрепленные в статьях 163,165,166 УК РФ

Нормы, закрепленные в статьях 163,165,166 УК РФ Геометрическая оптика

Геометрическая оптика CashFlow

CashFlow ВРЕМЕННОЕ ПЛОМБИРОВАНИЕ КОРНЕВЫХ КАНАЛОВ

ВРЕМЕННОЕ ПЛОМБИРОВАНИЕ КОРНЕВЫХ КАНАЛОВ Экваториальные леса Южной Америки

Экваториальные леса Южной Америки Презентация на тему Формула здоровья

Презентация на тему Формула здоровья  Неомодерн в архитектуре Ростова

Неомодерн в архитектуре Ростова Производительность МП и ее тестирование

Производительность МП и ее тестирование Внешность человека

Внешность человека Золотое содержание в национальной валюте. Финансы и кредит

Золотое содержание в национальной валюте. Финансы и кредит Сервис Взаимозачет

Сервис Взаимозачет Логарифмическая функция

Логарифмическая функция  Оценка и анализ финансовых рисков

Оценка и анализ финансовых рисков Договор транспортной экспедиции

Договор транспортной экспедиции Бюджетное учреждение здравоохранения Омской Области «Таврическая центральная районная больница»

Бюджетное учреждение здравоохранения Омской Области «Таврическая центральная районная больница» Развитие образа Снегурочки в искусстве

Развитие образа Снегурочки в искусстве Архитектура Серебряного века России

Архитектура Серебряного века России Презентация на тему Рождество в Великобритании

Презентация на тему Рождество в Великобритании  Решение уравнения в 1 классе

Решение уравнения в 1 классе Презентация на тему Русский язык среди других славянских языков

Презентация на тему Русский язык среди других славянских языков Умей бороться честно. Что такое допинг

Умей бороться честно. Что такое допинг