- FOREIGN EXCHANGE RISK FINANCIAL INSTITUTIONS MANAGEMENT

Содержание

- 2. AGENDA: FOREX RISK Sources of foreign exchange risk and FX trading activities; FX risk and hedging:

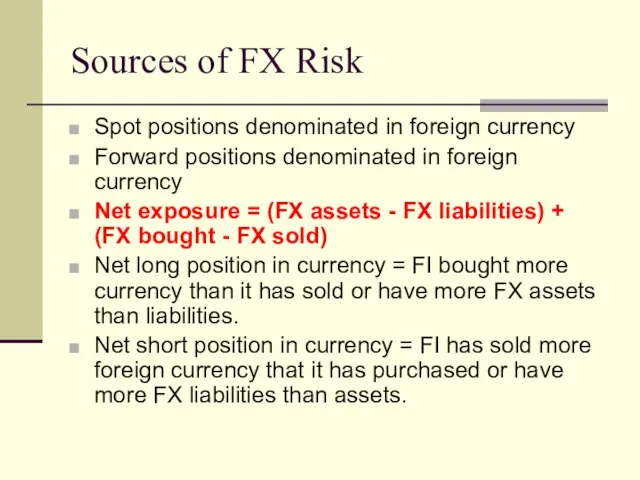

- 3. Sources of FX Risk Spot positions denominated in foreign currency Forward positions denominated in foreign currency

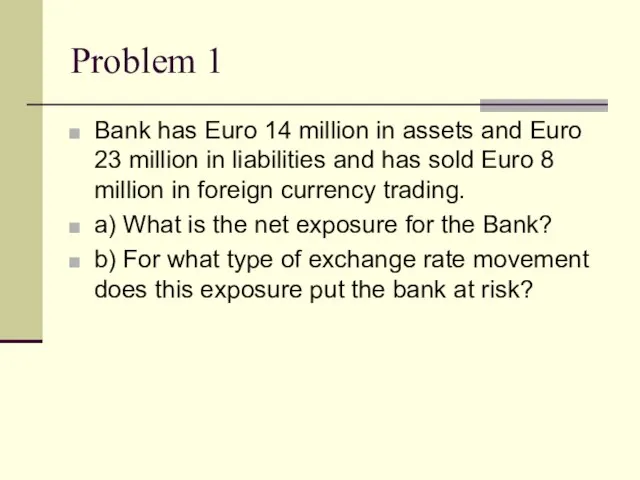

- 4. Problem 1 Bank has Euro 14 million in assets and Euro 23 million in liabilities and

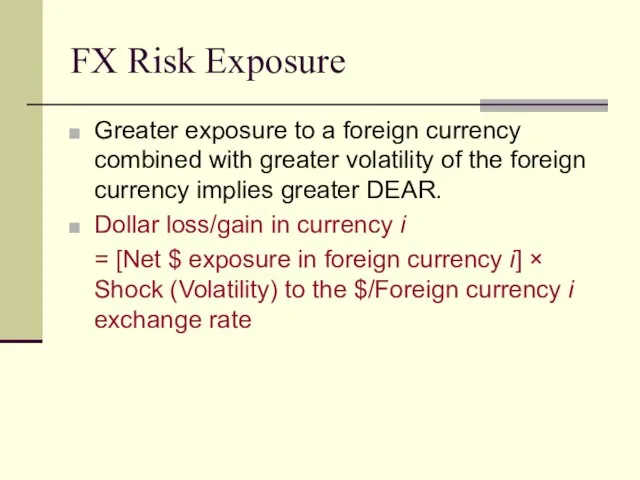

- 5. FX Risk Exposure Greater exposure to a foreign currency combined with greater volatility of the foreign

- 6. Trading Activities Basically 4 trading activities: Purchase and sale of currencies to complete international transactions. Facilitating

- 7. Foreign Assets & Liabilities Mismatches between foreign asset and liability portfolios. Ability to raise funds from

- 8. Return and Risk of Foreign Investments Returns are affected by: Spread between costs and revenues Changes

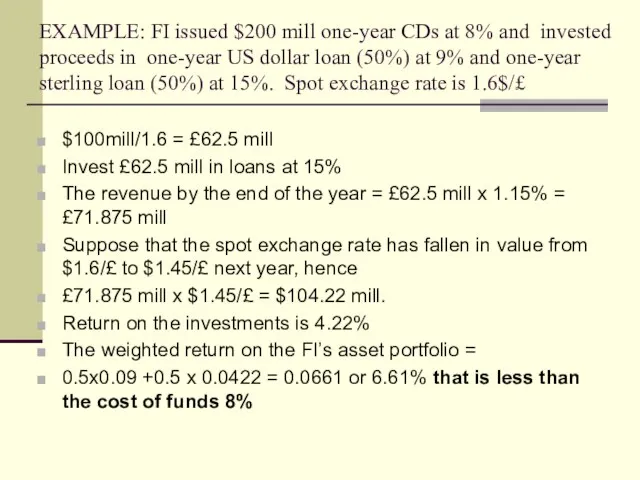

- 9. EXAMPLE: FI issued $200 mill one-year CDs at 8% and invested proceeds in one-year US dollar

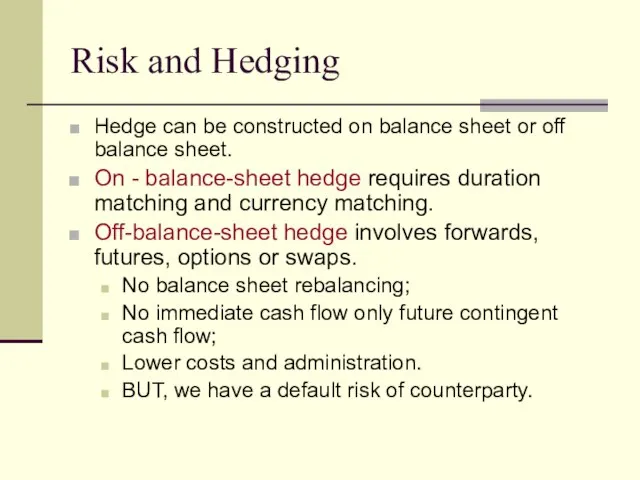

- 10. Risk and Hedging Hedge can be constructed on balance sheet or off balance sheet. On -

- 11. On balance sheet hedging We match maturities and currency foreign asset-liability book: $100 mill UK loans

- 12. £ appreciation to $1.70/£, the return on British loan is equal to 22.188% £ Cost of

- 13. Off balance sheet hedge with forward contracts $100mill/$1.6/£ = £62.5 mill Invested £62.5 mill in loans

- 14. Specifications of the FX futures Six months in the March quarterly cycle (Mar, Jun, Sep, Dec)

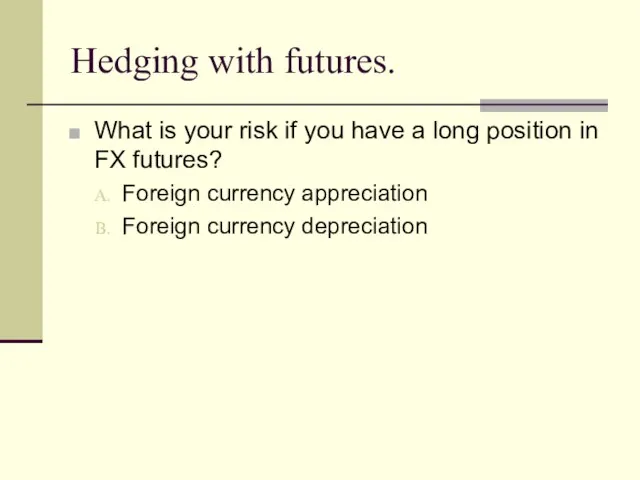

- 15. Hedging with futures. What is your risk if you have a long position in FX futures?

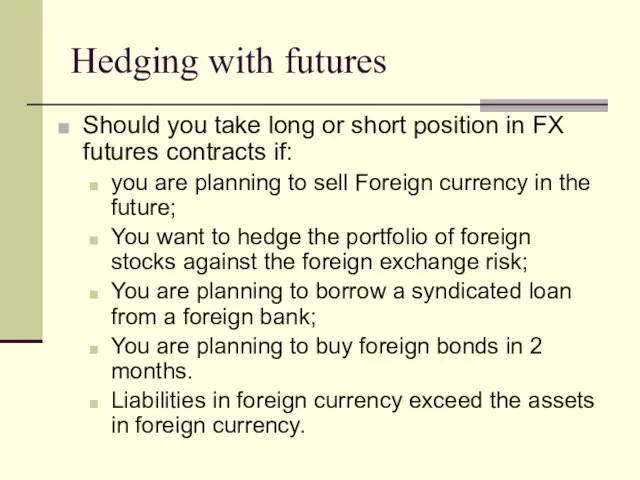

- 16. Hedging with futures Should you take long or short position in FX futures contracts if: you

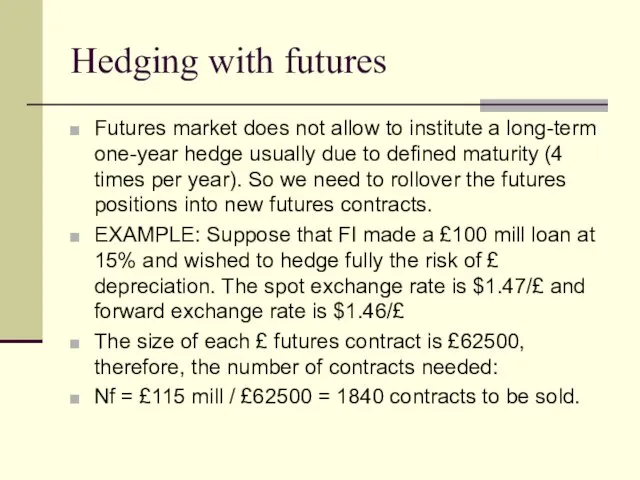

- 17. Hedging with futures Futures market does not allow to institute a long-term one-year hedge usually due

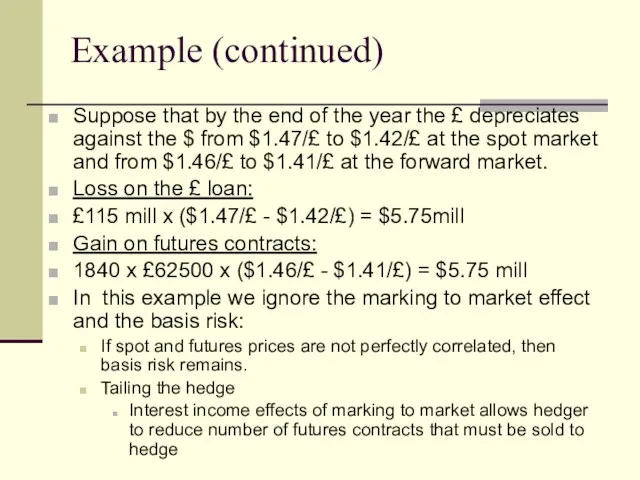

- 18. Example (continued) Suppose that by the end of the year the £ depreciates against the $

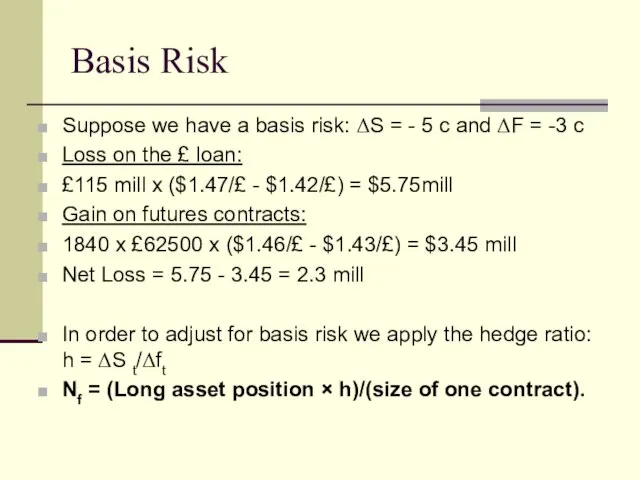

- 19. Basis Risk Suppose we have a basis risk: ΔS = - 5 c and ΔF =

- 20. Example (continued) H = 0.5/0.3 = 1.66 Nf = (£115mill x 1.66) / £62500 = 3054.4

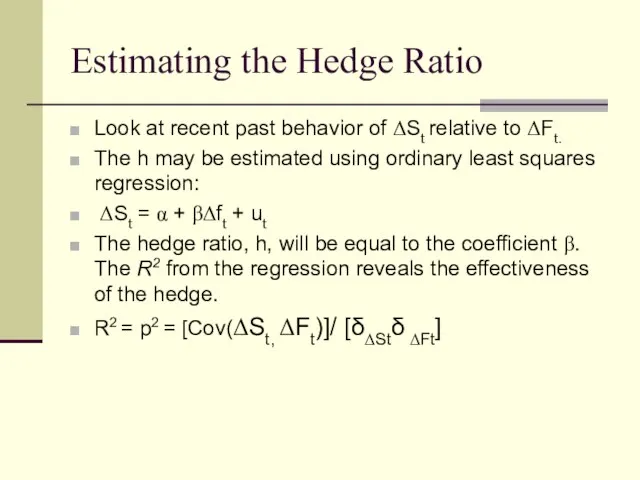

- 21. Estimating the Hedge Ratio Look at recent past behavior of ΔSt relative to ΔFt. The h

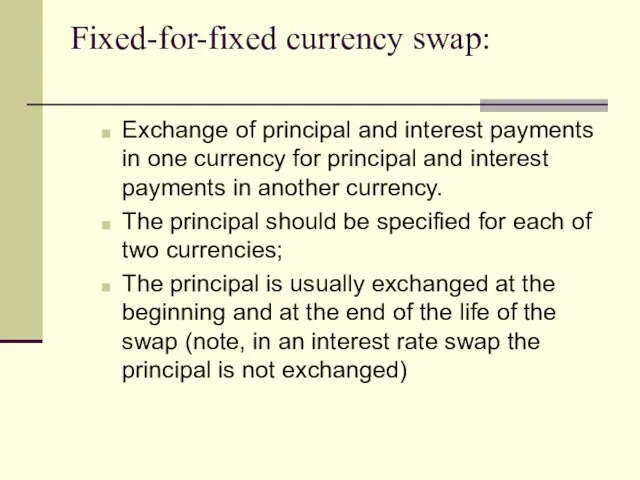

- 22. Fixed-for-fixed currency swap: Exchange of principal and interest payments in one currency for principal and interest

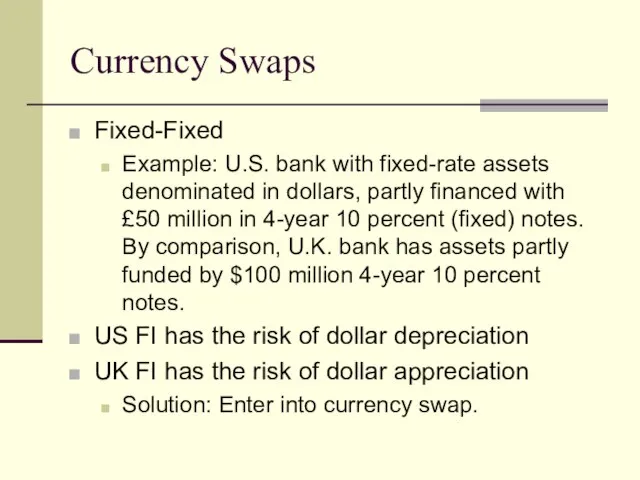

- 23. Currency Swaps Fixed-Fixed Example: U.S. bank with fixed-rate assets denominated in dollars, partly financed with £50

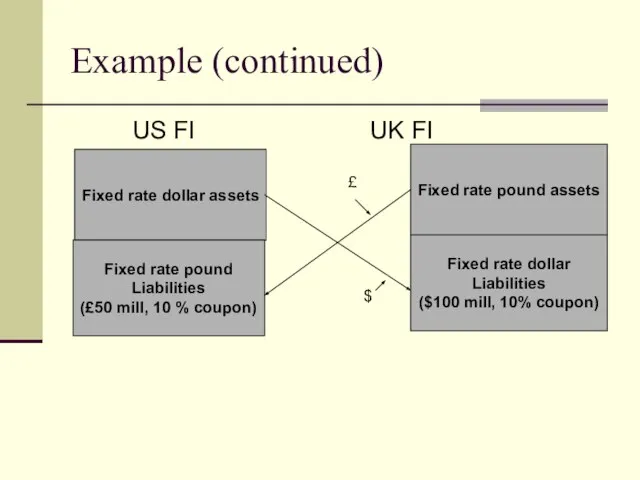

- 24. Example (continued) US FI UK FI Fixed rate dollar assets Fixed rate pound Liabilities (£50 mill,

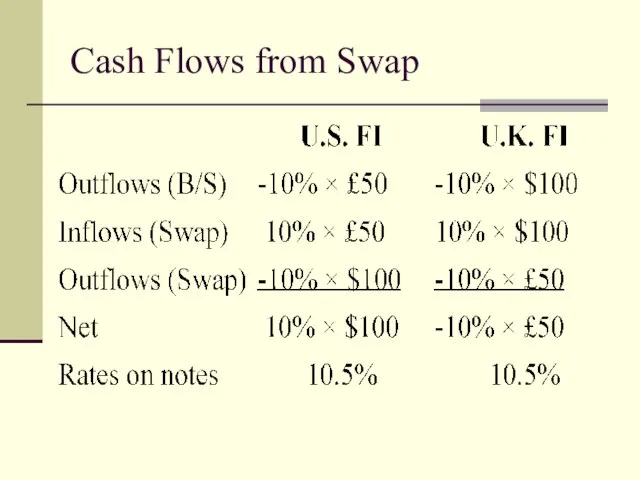

- 25. Cash Flows from Swap

- 26. Fixed-Floating + Currency Fixed-Floating currency swaps. Allows hedging of interest rate and currency exposures simultaneously Example:

- 27. Example (continued) US FI UK FI Floating rate short term $ assets Fixed rate 4 year

- 29. Скачать презентацию

Слайд 3Sources of FX Risk

Spot positions denominated in foreign currency

Forward positions denominated in

Sources of FX Risk

Spot positions denominated in foreign currency

Forward positions denominated in

Слайд 4Problem 1

Bank has Euro 14 million in assets and Euro 23 million

Problem 1

Bank has Euro 14 million in assets and Euro 23 million

Слайд 5FX Risk Exposure

Greater exposure to a foreign currency combined with greater volatility

FX Risk Exposure

Greater exposure to a foreign currency combined with greater volatility

Слайд 6Trading Activities

Basically 4 trading activities:

Purchase and sale of currencies to complete international

Trading Activities

Basically 4 trading activities:

Purchase and sale of currencies to complete international

Слайд 7Foreign Assets & Liabilities

Mismatches between foreign asset and liability portfolios.

Ability to

Foreign Assets & Liabilities

Mismatches between foreign asset and liability portfolios.

Ability to

Слайд 8Return and Risk of

Foreign Investments

Returns are affected by:

Spread between costs and

Return and Risk of

Foreign Investments

Returns are affected by:

Spread between costs and

Слайд 9EXAMPLE: FI issued $200 mill one-year CDs at 8% and invested proceeds

EXAMPLE: FI issued $200 mill one-year CDs at 8% and invested proceeds

Слайд 10Risk and Hedging

Hedge can be constructed on balance sheet or off balance

Risk and Hedging

Hedge can be constructed on balance sheet or off balance

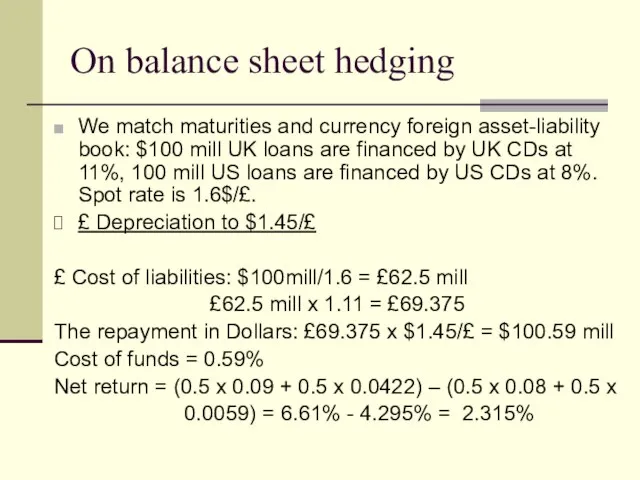

Слайд 11On balance sheet hedging

We match maturities and currency foreign asset-liability book: $100

On balance sheet hedging

We match maturities and currency foreign asset-liability book: $100

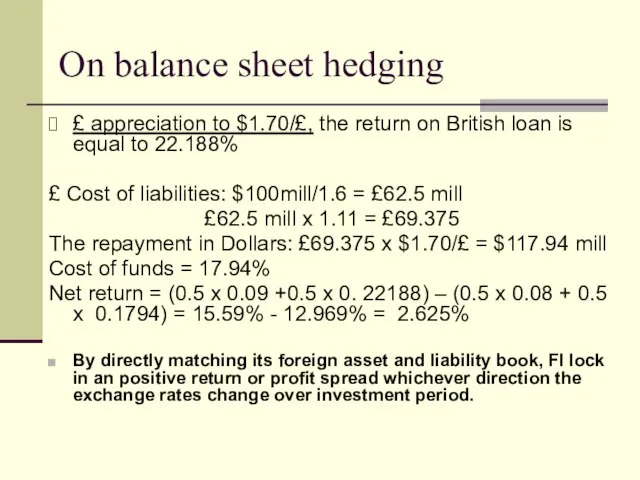

Слайд 12

£ appreciation to $1.70/£, the return on British loan is equal

£ appreciation to $1.70/£, the return on British loan is equal

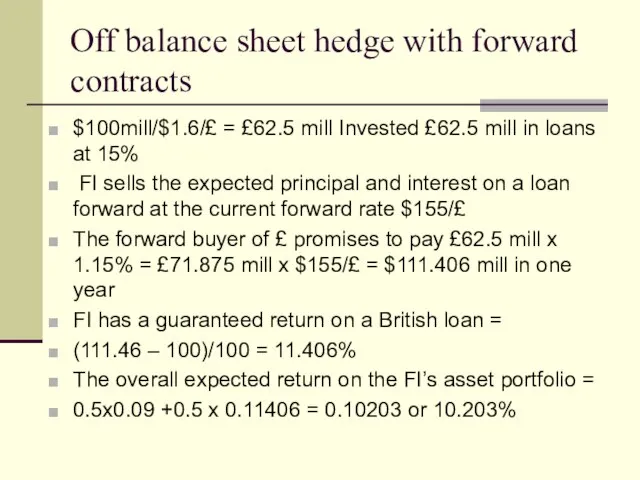

Слайд 13Off balance sheet hedge with forward contracts

$100mill/$1.6/£ = £62.5 mill Invested £62.5

Off balance sheet hedge with forward contracts

$100mill/$1.6/£ = £62.5 mill Invested £62.5

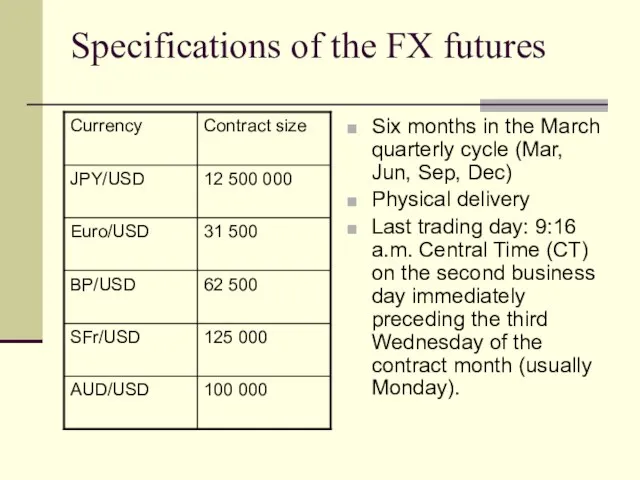

Слайд 14Specifications of the FX futures

Six months in the March quarterly cycle (Mar,

Specifications of the FX futures

Six months in the March quarterly cycle (Mar,

Слайд 15Hedging with futures.

What is your risk if you have a long position

Hedging with futures.

What is your risk if you have a long position

Слайд 16Hedging with futures

Should you take long or short position in FX futures

Hedging with futures

Should you take long or short position in FX futures

Слайд 17Hedging with futures

Futures market does not allow to institute a long-term one-year

Hedging with futures

Futures market does not allow to institute a long-term one-year

Слайд 18Example (continued)

Suppose that by the end of the year the £ depreciates

Example (continued)

Suppose that by the end of the year the £ depreciates

Слайд 19Basis Risk

Suppose we have a basis risk: ΔS = - 5 c

Basis Risk

Suppose we have a basis risk: ΔS = - 5 c

Слайд 20Example (continued)

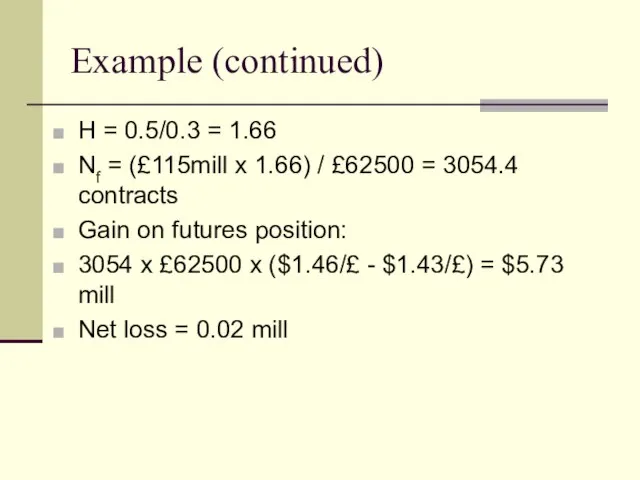

H = 0.5/0.3 = 1.66

Nf = (£115mill x 1.66) /

Example (continued)

H = 0.5/0.3 = 1.66

Nf = (£115mill x 1.66) /

Слайд 21Estimating the Hedge Ratio

Look at recent past behavior of ΔSt relative to

Estimating the Hedge Ratio

Look at recent past behavior of ΔSt relative to

Слайд 22Fixed-for-fixed currency swap:

Exchange of principal and interest payments in one currency

Fixed-for-fixed currency swap:

Exchange of principal and interest payments in one currency

Слайд 23Currency Swaps

Fixed-Fixed

Example: U.S. bank with fixed-rate assets denominated in dollars, partly

Currency Swaps

Fixed-Fixed

Example: U.S. bank with fixed-rate assets denominated in dollars, partly

Слайд 24Example (continued)

US FI UK FI

Fixed rate dollar assets

Fixed rate pound

Example (continued)

US FI UK FI

Fixed rate dollar assets

Fixed rate pound

Слайд 25Cash Flows from Swap

Cash Flows from Swap

Слайд 26Fixed-Floating + Currency

Fixed-Floating currency swaps.

Allows hedging of interest rate and currency exposures

Fixed-Floating + Currency

Fixed-Floating currency swaps.

Allows hedging of interest rate and currency exposures

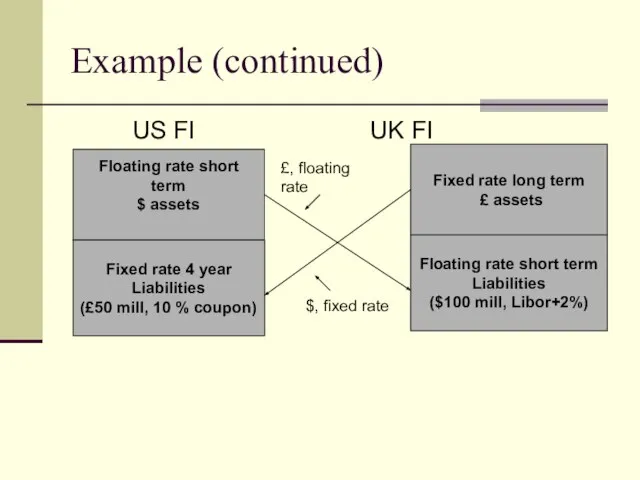

Слайд 27Example (continued)

US FI UK FI

Floating rate short term

$ assets

Fixed rate

Example (continued)

US FI UK FI

Floating rate short term

$ assets

Fixed rate

Фермы

Фермы Искусство барокко. Архитектура и скульптура

Искусство барокко. Архитектура и скульптура Использование элементов блог-технологии в языковой подготовке студентов колледжа

Использование элементов блог-технологии в языковой подготовке студентов колледжа Новая роль библиотекаря в новой библиотеке

Новая роль библиотекаря в новой библиотеке Шартлы теләк фигыль

Шартлы теләк фигыль УРОК В СООТВЕТСТВИИ С ФГОС

УРОК В СООТВЕТСТВИИ С ФГОС Исповедь. Таинства церкви

Исповедь. Таинства церкви Тема 5.3. Классификация способов сварки

Тема 5.3. Классификация способов сварки Сложение натуральных чисел и его свойства

Сложение натуральных чисел и его свойства Презентация на тему Сентиментализм и классицизм. Сравнительная характеристика

Презентация на тему Сентиментализм и классицизм. Сравнительная характеристика Ценные бумаги

Ценные бумаги Деяние. Главная мысль

Деяние. Главная мысль Роль портрета в литературном произведении Урок- практикум по рассказу В.Г. Короленко «В дурном обществе»

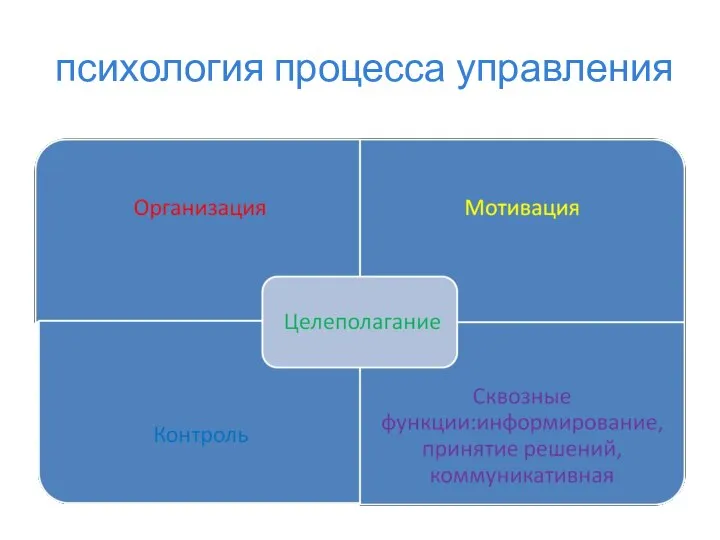

Роль портрета в литературном произведении Урок- практикум по рассказу В.Г. Короленко «В дурном обществе» Психология процесса управления

Психология процесса управления ФЕДЕРАЛЬНЫЙ ГОСУДАРСТВЕННЫЙ ОБРАЗОВАТЕЛЬНЫЙ СТАНДАРТ второго поколения

ФЕДЕРАЛЬНЫЙ ГОСУДАРСТВЕННЫЙ ОБРАЗОВАТЕЛЬНЫЙ СТАНДАРТ второго поколения Правила расчет стоимости стандартного турпакета

Правила расчет стоимости стандартного турпакета Салями Италии

Салями Италии Военные походы фараонов

Военные походы фараонов Изобарический процесс

Изобарический процесс Благодійний проект “Подих Життя”

Благодійний проект “Подих Життя” Дисциплина «Контракты в международной торговле» тема: «Структура и особенности договора коммерческой концессии/франчайзинга»

Дисциплина «Контракты в международной торговле» тема: «Структура и особенности договора коммерческой концессии/франчайзинга» Художники Сенгилеевского района

Художники Сенгилеевского района О развитии территориального общественного самоуправления в Архангельской области

О развитии территориального общественного самоуправления в Архангельской области Однородные и неоднородные определения

Однородные и неоднородные определения Публичный отчёто деятельности школы за 2009 – 2010 учебный год

Публичный отчёто деятельности школы за 2009 – 2010 учебный год  История открытия

История открытия Пьер Огю́ст Ренуа́р

Пьер Огю́ст Ренуа́р Спрос. Величина спроса. Эластичность спроса.

Спрос. Величина спроса. Эластичность спроса.