- Lecture

Содержание

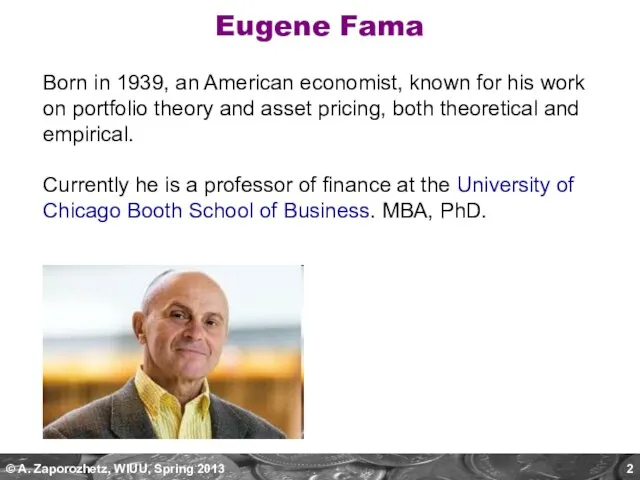

- 2. Eugene Fama Born in 1939, an American economist, known for his work on portfolio theory and

- 3. Eugene Fama E. Fama is most often thought of as the father of efficient market hypothesis

- 4. GSS, Gross security selection = ract - rCAPM = CFDR + NSS CFDR, Compensation for diversifiable

- 5. NSS, Net security selection = GSS – CFDR NSS is the effect of “smart” selection of

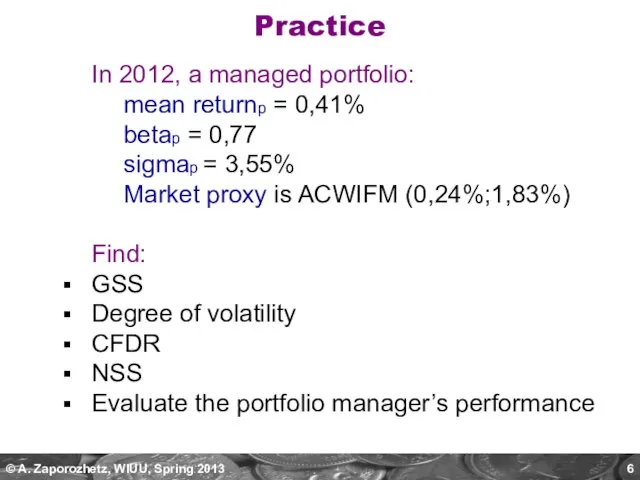

- 6. In 2012, a managed portfolio: mean returnp = 0,41% betap = 0,77 sigmap = 3,55% Market

- 8. Скачать презентацию

И.П.Кулибин

И.П.Кулибин Иммобилайзер Pandect IS-250 - противоугонное средство нового поколения, наделяющее автомобиль противоугонными и противоразбойными функ

Иммобилайзер Pandect IS-250 - противоугонное средство нового поколения, наделяющее автомобиль противоугонными и противоразбойными функ Источники энергии

Источники энергии Предлоги

Предлоги Разработка проекта сварочного участка по изготовлению сварной конструкции патрубок приемный

Разработка проекта сварочного участка по изготовлению сварной конструкции патрубок приемный Экологическое просвещение населения средствами информационных технологий

Экологическое просвещение населения средствами информационных технологий Клички и прозвища

Клички и прозвища Повышение эффективности системы социальной поддержки Работников АО НИИАС

Повышение эффективности системы социальной поддержки Работников АО НИИАС Источники и системы теплоснабжения

Источники и системы теплоснабжения «Это был не век поэзии, а целая ее эпоха.» (И. Эренбург)

«Это был не век поэзии, а целая ее эпоха.» (И. Эренбург) Презентация гимназии KITEE

Презентация гимназии KITEE Презентация на тему Заимствованные слова

Презентация на тему Заимствованные слова  История возникновения и развития зимних видов спорта

История возникновения и развития зимних видов спорта Депозитарная деятельность на рынке ценных бумаг

Депозитарная деятельность на рынке ценных бумаг Организационные структуры управления

Организационные структуры управления Результаты опытной эксплуатации сети цифрового телевидения Курской области

Результаты опытной эксплуатации сети цифрового телевидения Курской области Истоки Киевской Руси

Истоки Киевской Руси Организация педагогического споровождения детей сирот и детей, оставшихся без попечения родителей

Организация педагогического споровождения детей сирот и детей, оставшихся без попечения родителей Проект на тему: "Изучение видового состава и контроль за сохранностью хвойных насаждений на территории села Ладомировка"

Проект на тему: "Изучение видового состава и контроль за сохранностью хвойных насаждений на территории села Ладомировка" Кукла из фетра

Кукла из фетра Различные виды деревьев в стихотворениях Сергея Есенина

Различные виды деревьев в стихотворениях Сергея Есенина Сорта яблони

Сорта яблони Совместная программа /Joint Project «Национальные меньшинства в Российской Федерации: развитие языков, культуры, средств массовой инфор

Совместная программа /Joint Project «Национальные меньшинства в Российской Федерации: развитие языков, культуры, средств массовой инфор Типові лексичні та орфографічні помилки в українській мові

Типові лексичні та орфографічні помилки в українській мові Старинные русские игрушки

Старинные русские игрушки Особенности контрактов со спортсменом и тренером. Лекция 10

Особенности контрактов со спортсменом и тренером. Лекция 10 Нора Галь

Нора Галь Отчетпо методической работе МБОУ «СОШ № 22» за 2010 – 2011 учебный год»

Отчетпо методической работе МБОУ «СОШ № 22» за 2010 – 2011 учебный год»