- Principles of Pharmacoeconomics

Содержание

- 2. Cost Determination Lecture 2

- 3. Objectives Compare and contrast direct, indirect, and intangible costs Describe the relationship between marginal and average

- 4. Objectives Given a specific perspective, identify all relevant costs that should be included in an analysis

- 5. Cost Data Measurement of resource use

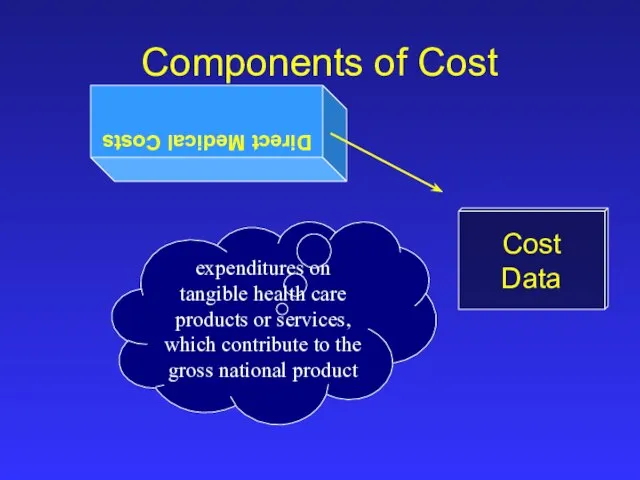

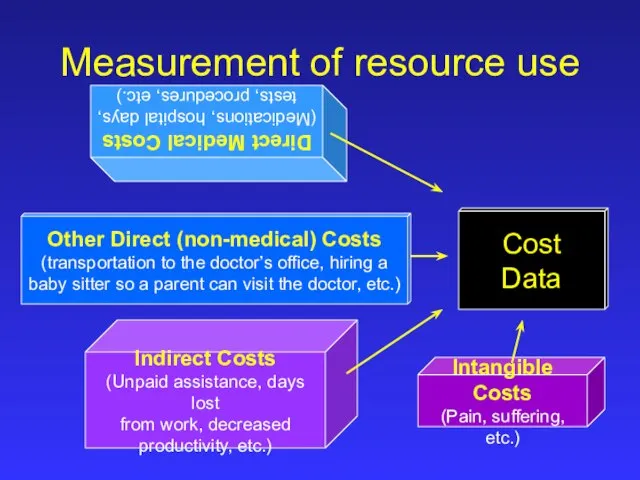

- 6. Direct Medical Costs Cost Data Components of Cost expenditures on tangible health care products or services,

- 7. Direct Medical Costs (Medications, hospital days, tests, procedures, etc.) Cost Data Components of Cost

- 8. Other Direct (non-medical) Costs Cost Data Components of Cost expenditures on tangible products or services, which

- 9. Cost Data Components of Cost Other Direct (non-medical) Costs (transportation to the doctor’s office, hiring a

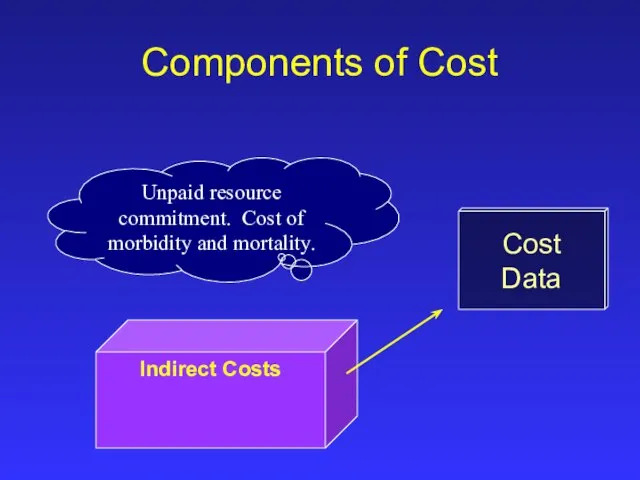

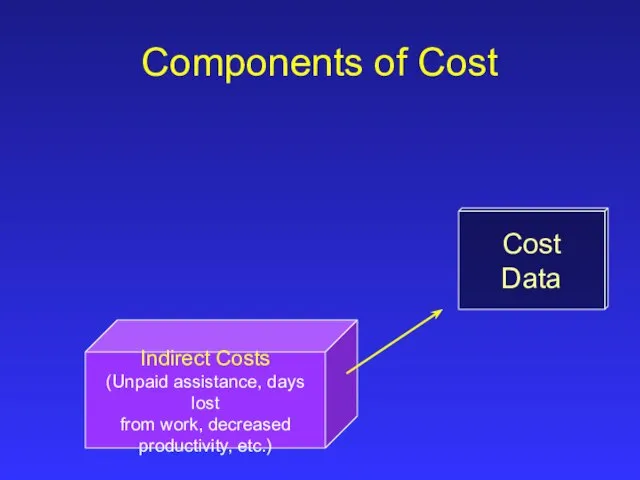

- 10. Cost Data Components of Cost Indirect Costs Unpaid resource commitment. Cost of morbidity and mortality.

- 11. Cost Data Components of Cost Indirect Costs (Unpaid assistance, days lost from work, decreased productivity, etc.)

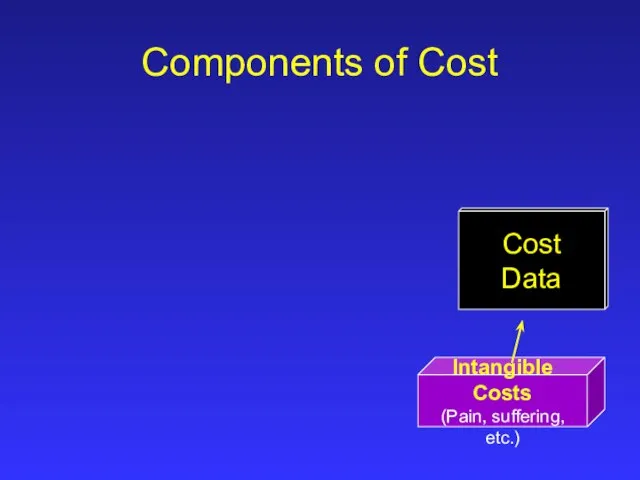

- 12. Intangible Costs (Pain, suffering, etc.) Cost Data Components of Cost

- 13. Direct Medical Costs (Medications, hospital days, tests, procedures, etc.) Intangible Costs (Pain, suffering, etc.) Cost Data

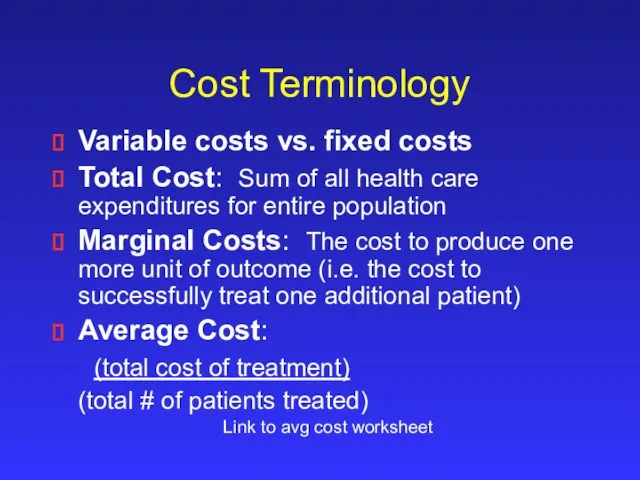

- 14. Cost Terminology Variable costs vs. fixed costs Total Cost: Sum of all health care expenditures for

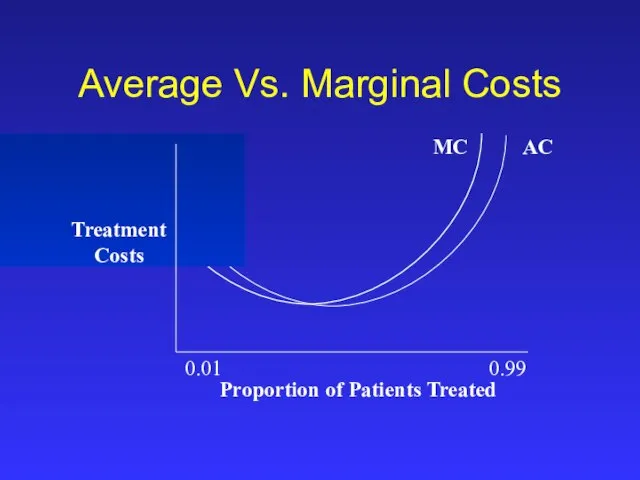

- 15. AC MC Treatment Costs Average Vs. Marginal Costs Proportion of Patients Treated 0.01 0.99

- 16. Specifying the Inputs Develop comprehensive list of ALL relevant inputs (i.e. resources consumed) to produce a

- 17. Payer Perspective Direct Indirect Asthma management service

- 18. Hospitalizations Laboratory costs Medications Medical devises Physician / pharmacist fees Payer Perspective Direct Indirect Asthma management

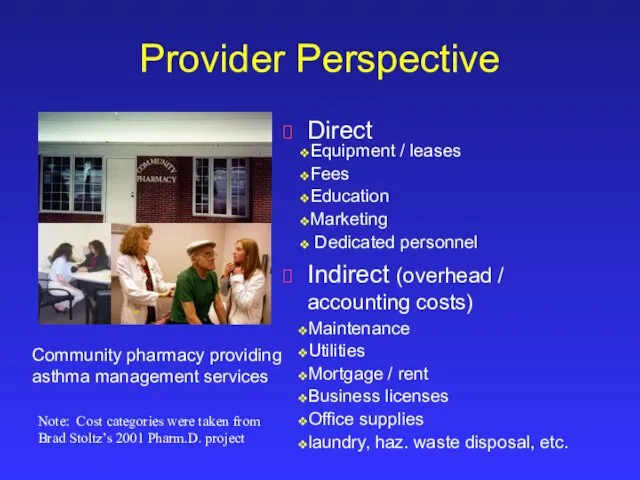

- 19. Direct Indirect (overhead / accounting costs) Provider Perspective Community pharmacy providing asthma management services Note: Cost

- 20. Direct Indirect (overhead / accounting costs) Maintenance Utilities Mortgage / rent Business licenses Office supplies laundry,

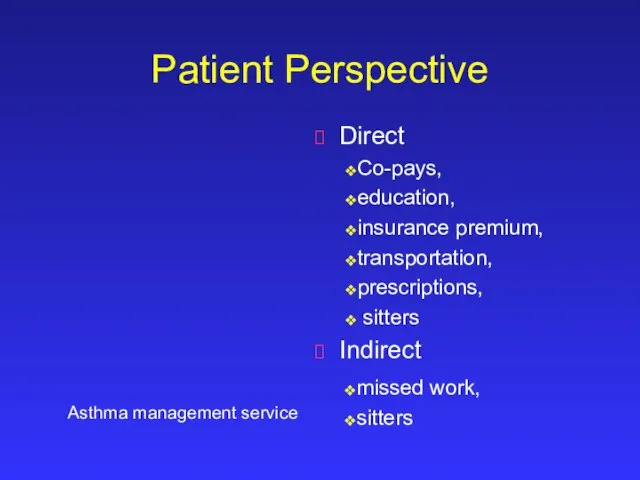

- 21. Patient Perspective Direct Indirect Asthma management service

- 22. Co-pays, education, insurance premium, transportation, prescriptions, sitters missed work, sitters Patient Perspective Direct Indirect Asthma management

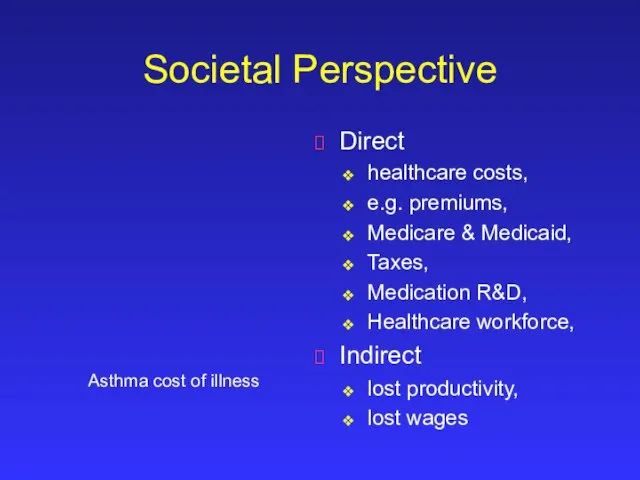

- 23. Societal Perspective Direct Indirect Asthma management service

- 24. healthcare costs, e.g. premiums, Medicare & Medicaid, Taxes, Medication R&D, Healthcare workforce, lost productivity, lost wages

- 25. Counting Units Determine the unit of use for a given resource (e.g., hospital day, single lab

- 26. Assigning Dollar Values Opportunity costs Vs. market price Personnel time / costs Medication costs Physician and

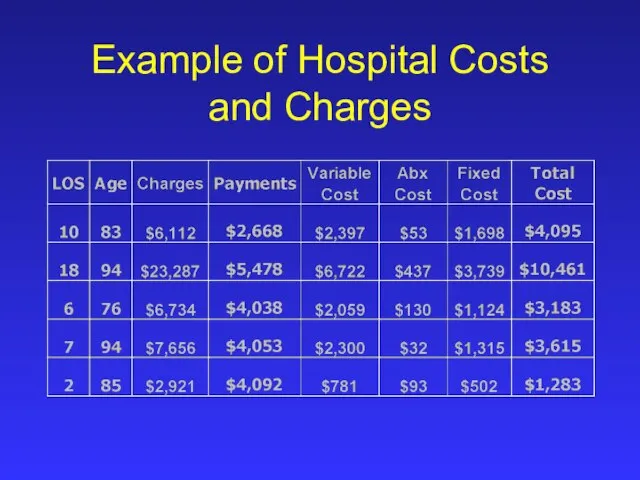

- 27. Example of Hospital Costs and Charges

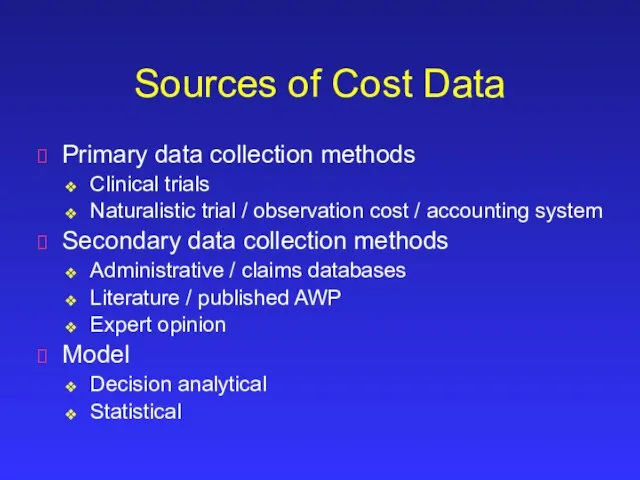

- 28. Sources of Cost Data Primary data collection methods Clinical trials Naturalistic trial / observation cost /

- 29. Adjusting for Differences in the Timing of Costs A cost or benefit today is not equivalent

- 30. Discounting Now Past Future Account for Inflation Discount future costs

- 31. Taken from: http://www.orst.edu/dept/pol_sci/fac/sahr/mill00.htm without permission

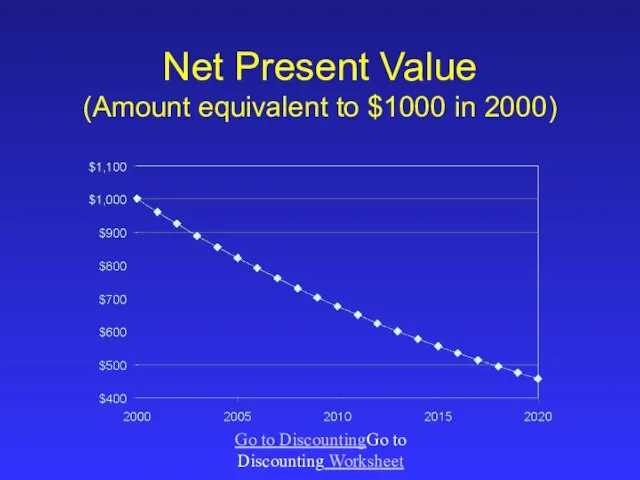

- 32. Net Present Value (Amount equivalent to $1000 in 2000) Go to DiscountingGo to Discounting Worksheet

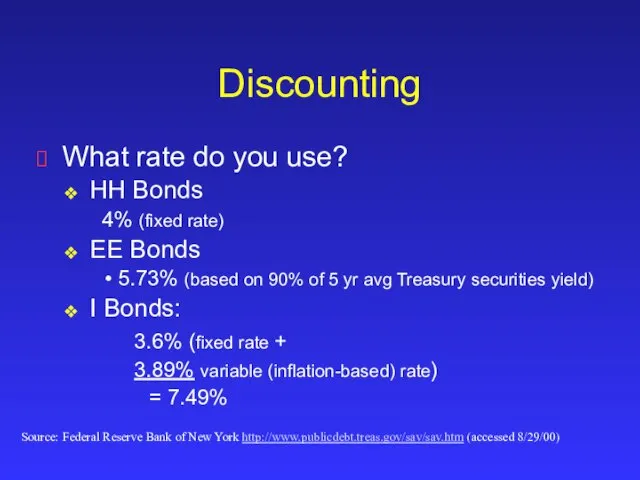

- 33. Discounting What rate do you use? HH Bonds 4% (fixed rate) EE Bonds 5.73% (based on

- 34. Allowing for Uncertainty What if the type and number of resources included in the analysis change?

- 35. Purchase cable service Do not purchase cable service Example Need a TV Purchase a 32” TV

- 37. Скачать презентацию

Слайд 3Objectives

Compare and contrast direct, indirect, and intangible costs

Describe the relationship between marginal

Objectives

Compare and contrast direct, indirect, and intangible costs

Describe the relationship between marginal

Слайд 4Objectives

Given a specific perspective, identify all relevant costs that should be included

Objectives

Given a specific perspective, identify all relevant costs that should be included

Слайд 5Cost

Data

Measurement of resource use

Cost

Data

Measurement of resource use

Слайд 6Direct Medical Costs

Cost

Data

Components of Cost

expenditures on tangible health care products

Direct Medical Costs

Cost

Data

Components of Cost

expenditures on tangible health care products

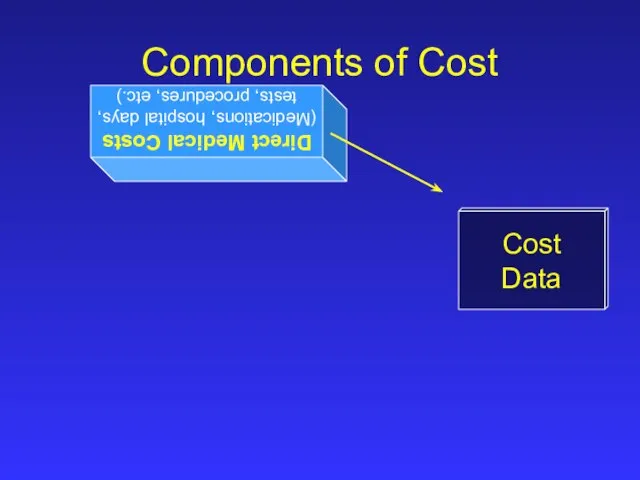

Слайд 7Direct Medical Costs

(Medications, hospital days,

tests, procedures, etc.)

Cost

Data

Components of Cost

Direct Medical Costs

(Medications, hospital days,

tests, procedures, etc.)

Cost

Data

Components of Cost

Слайд 8Other Direct (non-medical) Costs

Cost

Data

Components of Cost

expenditures on tangible products or services,

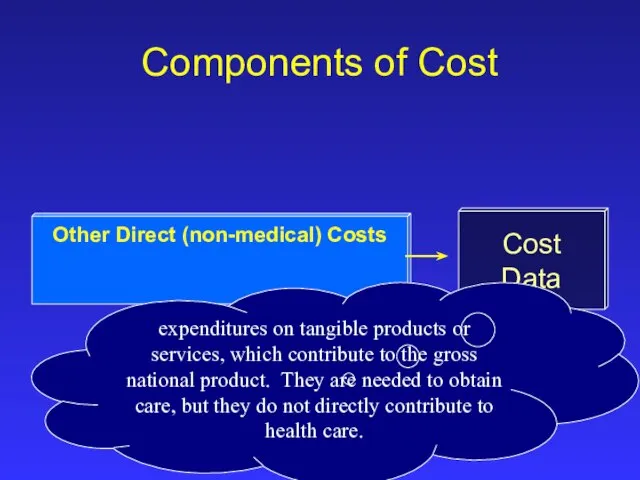

Other Direct (non-medical) Costs

Cost

Data

Components of Cost

expenditures on tangible products or services,

Слайд 9Cost

Data

Components of Cost

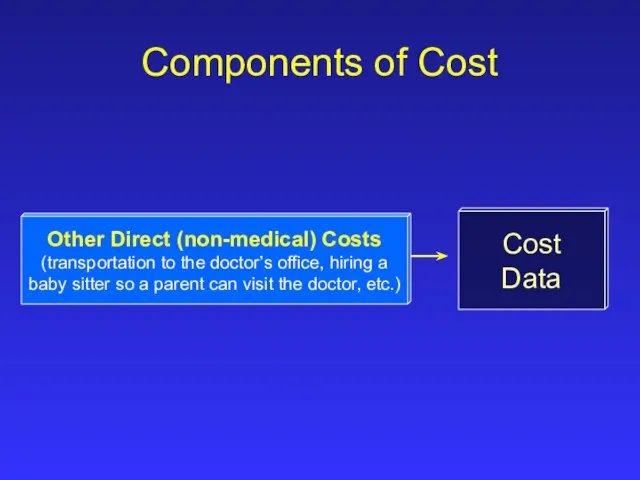

Other Direct (non-medical) Costs

(transportation to the doctor’s office, hiring

Cost

Data

Components of Cost

Other Direct (non-medical) Costs

(transportation to the doctor’s office, hiring

Слайд 10Cost

Data

Components of Cost

Indirect Costs

Unpaid resource commitment. Cost of morbidity and mortality.

Cost

Data

Components of Cost

Indirect Costs

Unpaid resource commitment. Cost of morbidity and mortality.

Слайд 11Cost

Data

Components of Cost

Indirect Costs

(Unpaid assistance, days lost

from work, decreased

productivity,

Cost

Data

Components of Cost

Indirect Costs

(Unpaid assistance, days lost

from work, decreased

productivity,

Слайд 12Intangible Costs

(Pain, suffering, etc.)

Cost

Data

Components of Cost

Intangible Costs

(Pain, suffering, etc.)

Cost

Data

Components of Cost

Слайд 13Direct Medical Costs

(Medications, hospital days,

tests, procedures, etc.)

Intangible Costs

(Pain, suffering, etc.)

Cost

Direct Medical Costs

(Medications, hospital days,

tests, procedures, etc.)

Intangible Costs

(Pain, suffering, etc.)

Cost

Слайд 14Cost Terminology

Variable costs vs. fixed costs

Total Cost: Sum of all health care

Cost Terminology

Variable costs vs. fixed costs

Total Cost: Sum of all health care

Слайд 15AC

MC

Treatment

Costs

Average Vs. Marginal Costs

Proportion of Patients Treated

0.01 0.99

AC

MC

Treatment

Costs

Average Vs. Marginal Costs

Proportion of Patients Treated

0.01 0.99

Слайд 16Specifying the Inputs

Develop comprehensive list of ALL relevant inputs (i.e. resources consumed)

Specifying the Inputs

Develop comprehensive list of ALL relevant inputs (i.e. resources consumed)

Слайд 17Payer Perspective

Direct

Indirect

Asthma management service

Payer Perspective

Direct

Indirect

Asthma management service

Слайд 18Hospitalizations

Laboratory costs

Medications

Medical devises

Physician / pharmacist fees

Payer Perspective

Direct

Indirect

Asthma management service

?

Laboratory costs

Medications

Medical devises

Physician / pharmacist fees

Payer Perspective

Direct

Indirect

Asthma management service

?

Слайд 19Direct

Indirect (overhead / accounting costs)

Provider Perspective

Community pharmacy providing

asthma management services

Note: Cost

Direct

Indirect (overhead / accounting costs)

Provider Perspective

Community pharmacy providing

asthma management services

Note: Cost

Слайд 20Direct

Indirect (overhead / accounting costs)

Maintenance

Utilities

Mortgage / rent

Business licenses

Office supplies

laundry, haz. waste

Direct

Indirect (overhead / accounting costs)

Maintenance

Utilities

Mortgage / rent

Business licenses

Office supplies

laundry, haz. waste

Слайд 21Patient Perspective

Direct

Indirect

Asthma management service

Patient Perspective

Direct

Indirect

Asthma management service

Слайд 22Co-pays,

education,

insurance premium,

transportation,

prescriptions,

sitters

missed work,

sitters

Patient Perspective

Direct

Indirect

Asthma management

education,

insurance premium,

transportation,

prescriptions,

sitters

missed work,

sitters

Patient Perspective

Direct

Indirect

Asthma management

Слайд 23Societal Perspective

Direct

Indirect

Asthma management service

Societal Perspective

Direct

Indirect

Asthma management service

Слайд 24healthcare costs,

e.g. premiums,

Medicare & Medicaid,

Taxes,

Medication R&D,

Healthcare workforce,

lost productivity,

e.g. premiums,

Medicare & Medicaid,

Taxes,

Medication R&D,

Healthcare workforce,

lost productivity,

Слайд 25Counting Units

Determine the unit of use for a given resource (e.g., hospital

Counting Units

Determine the unit of use for a given resource (e.g., hospital

Слайд 26Assigning Dollar Values

Opportunity costs Vs. market price

Personnel time / costs

Medication costs

Physician and

Assigning Dollar Values

Opportunity costs Vs. market price

Personnel time / costs

Medication costs

Physician and

Слайд 27Example of Hospital Costs and Charges

Example of Hospital Costs and Charges

Слайд 28Sources of Cost Data

Primary data collection methods

Clinical trials

Naturalistic trial / observation cost

Sources of Cost Data

Primary data collection methods

Clinical trials

Naturalistic trial / observation cost

Слайд 29Adjusting for Differences in

the Timing of Costs

A cost or benefit today

Adjusting for Differences in

the Timing of Costs

A cost or benefit today

Слайд 30Discounting

Now

Past

Future

Account for Inflation

Discount future costs

Discounting

Now

Past

Future

Account for Inflation

Discount future costs

Слайд 31Taken from: http://www.orst.edu/dept/pol_sci/fac/sahr/mill00.htm without permission

Taken from: http://www.orst.edu/dept/pol_sci/fac/sahr/mill00.htm without permission

Слайд 32Net Present Value

(Amount equivalent to $1000 in 2000)

Go to DiscountingGo to

Net Present Value

(Amount equivalent to $1000 in 2000)

Go to DiscountingGo to

Слайд 33Discounting

What rate do you use?

HH Bonds

4% (fixed rate)

EE Bonds

5.73% (based on 90%

Discounting

What rate do you use?

HH Bonds

4% (fixed rate)

EE Bonds

5.73% (based on 90%

Слайд 34Allowing for Uncertainty

What if the type and number of resources included in

Allowing for Uncertainty

What if the type and number of resources included in

Слайд 35Purchase cable

service

Do not purchase

cable service

Example

Need

a TV

Purchase a

32” TV

Purchase a

20”

Purchase cable

service

Do not purchase

cable service

Example

Need

a TV

Purchase a

32” TV

Purchase a

20”

Удержания из страховых пенсий

Удержания из страховых пенсий Инспекторский и приемочный контроль на предприятиях железнодорожного машиностроения

Инспекторский и приемочный контроль на предприятиях железнодорожного машиностроения Лермонтов Михаил Юрьевич

Лермонтов Михаил Юрьевич Презентация на тему Архитектура классицизма в России

Презентация на тему Архитектура классицизма в России  Кузнецов Павел Варфоломеевич

Кузнецов Павел Варфоломеевич Перспективы разработки источников вторичного электропитания для ракетно-космической и авиационной техники

Перспективы разработки источников вторичного электропитания для ракетно-космической и авиационной техники Человек и закон. Конкурс лучших детективов имени Шерлока Холмса

Человек и закон. Конкурс лучших детективов имени Шерлока Холмса Реконструкция системы водоснабжения п. Гирей, Краснодарского края

Реконструкция системы водоснабжения п. Гирей, Краснодарского края Легко и просто создать мультфильм

Легко и просто создать мультфильм Человек. Индивидуальность

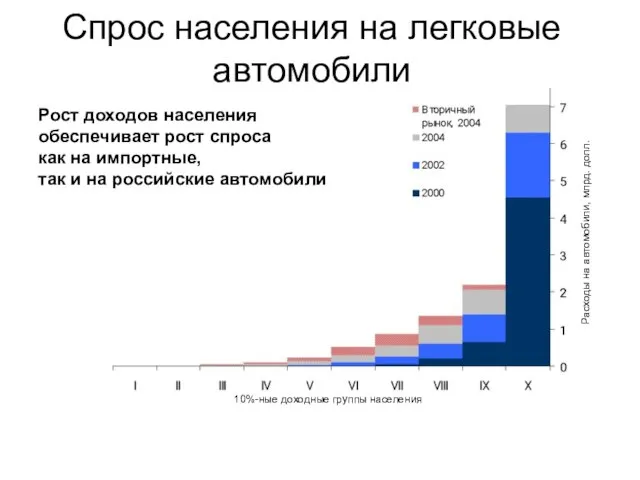

Человек. Индивидуальность Спрос населения на легковые автомобили

Спрос населения на легковые автомобили тенденции туристического спроса

тенденции туристического спроса "Как найти общий язык с ребёнком"

"Как найти общий язык с ребёнком" Основная деятельность компании- лидогенерация

Основная деятельность компании- лидогенерация 20141104_2_osobo_okhranyaemye_prirodnye_territorii_u._o

20141104_2_osobo_okhranyaemye_prirodnye_territorii_u._o Ветлуга моя

Ветлуга моя Уходит старый год, Шуршит его последняя страница, Пусть лучшее, что было не уйдёт, А худшее не сможет повториться.

Уходит старый год, Шуршит его последняя страница, Пусть лучшее, что было не уйдёт, А худшее не сможет повториться. Транспорт веществ в растительном организме

Транспорт веществ в растительном организме ПЕРМЯКОВ АНТОН ЕВГЕНЬЕВИЧ

ПЕРМЯКОВ АНТОН ЕВГЕНЬЕВИЧ Презентация на тему Зевс

Презентация на тему Зевс Совершенствование методов работы старшей школы по индивидуальным учебным планам

Совершенствование методов работы старшей школы по индивидуальным учебным планам Прокуратура РФ

Прокуратура РФ Угадай мелодию Щелкунчик

Угадай мелодию Щелкунчик Презентация на тему Возникновение средневековых городов

Презентация на тему Возникновение средневековых городов  Глобальные сети

Глобальные сети Агитационное искусство периода Первой мировой войны

Агитационное искусство периода Первой мировой войны 20140111_chudesa_sveta

20140111_chudesa_sveta Понятие о внутрикорпоративных коммуникациях

Понятие о внутрикорпоративных коммуникациях