- Taxation in the UK

Содержание

- 2. Taxation in the United Kingdom may involve payments to a minimum of two different levels of

- 3. THE TAX YEAR The tax year in the UK, which applies to income tax and other

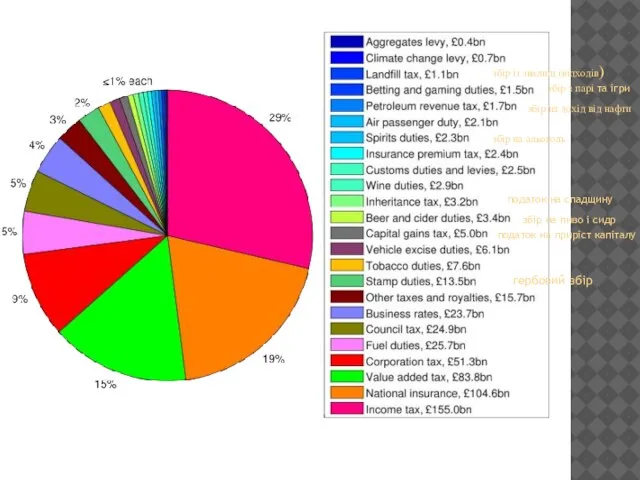

- 4. гербовий збір податок на приріст капіталу збір на пиво і сидр податок на спадщину збір на

- 5. INCOME TAX Income tax forms the single largest source of revenues collected by the government. Each

- 6. Different rates of income tax (as of 2010-2011):

- 7. NATIONAL INSURANCE CONTRIBUTIONS The second largest source of government revenues is National Insurance contributions (NICs). NICs

- 8. VALUE ADDED TAX On 4 January 2011 VAT was raised from 17, 5% to 20% The

- 9. CORPORATION TAX Corporation tax forms the fourth-largest source of government revenue (after income, NIC, and VAT).

- 10. FUEL DUTY The UK there is a fuel duty that is applied to all Hydrocarbon fuels,

- 11. COUNCIL TAX Council Tax is the system of local taxation used in England, Scotland and Wales

- 12. CLIMATE CHANGE LEVY The climate change levy (CCL) is a tax on energy delivered to non-domestic

- 14. Скачать презентацию

Слайд 3THE TAX YEAR

The tax year in the UK, which applies to income

THE TAX YEAR

The tax year in the UK, which applies to income

Слайд 4гербовий збір

податок на приріст капіталу

збір на пиво і сидр

податок на спадщину

збір на

гербовий збір

податок на приріст капіталу

збір на пиво і сидр

податок на спадщину

збір на

Слайд 5INCOME TAX

Income tax forms the single largest source of revenues collected by

INCOME TAX

Income tax forms the single largest source of revenues collected by

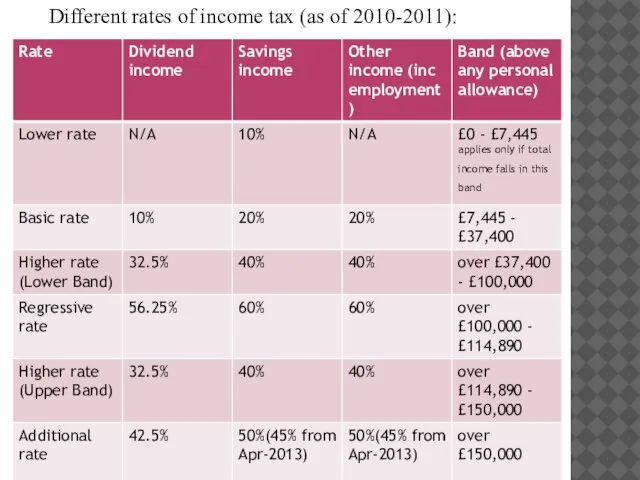

Слайд 6Different rates of income tax (as of 2010-2011):

Different rates of income tax (as of 2010-2011):

Слайд 7NATIONAL INSURANCE CONTRIBUTIONS

The second largest source of government revenues is National Insurance

NATIONAL INSURANCE CONTRIBUTIONS

The second largest source of government revenues is National Insurance

Слайд 8VALUE ADDED TAX

On 4 January 2011 VAT was raised from 17, 5%

VALUE ADDED TAX

On 4 January 2011 VAT was raised from 17, 5%

Слайд 9CORPORATION TAX

Corporation tax forms the fourth-largest source of government revenue (after income,

CORPORATION TAX

Corporation tax forms the fourth-largest source of government revenue (after income,

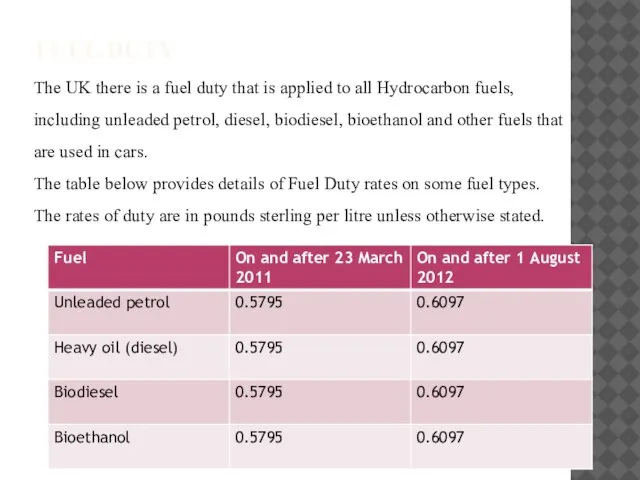

Слайд 10FUEL DUTY

The UK there is a fuel duty that is applied to

FUEL DUTY

The UK there is a fuel duty that is applied to

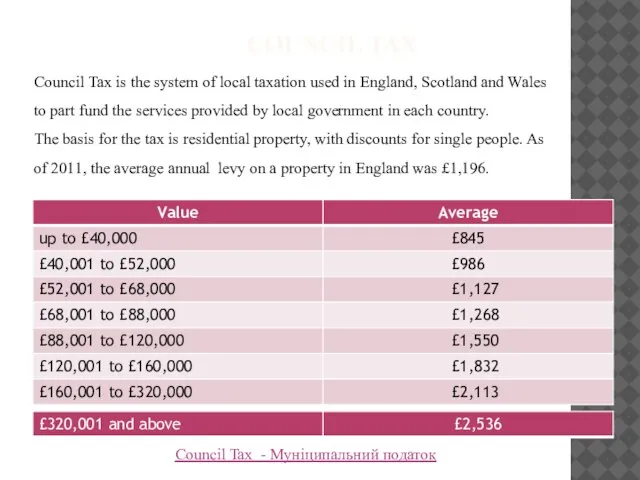

Слайд 11 COUNCIL TAX

Council Tax is the system of local taxation used in

COUNCIL TAX

Council Tax is the system of local taxation used in

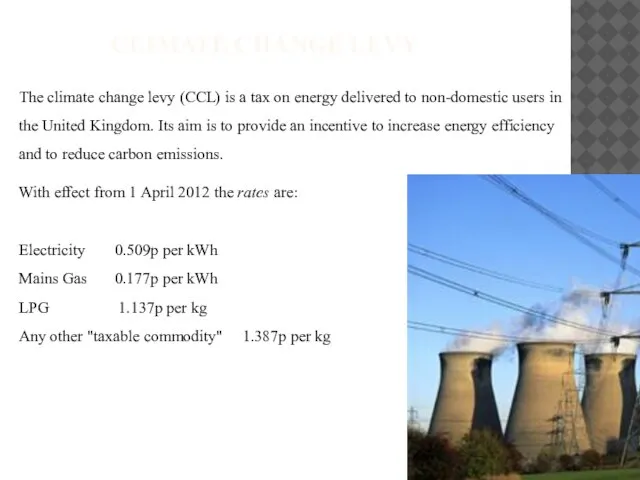

Слайд 12CLIMATE CHANGE LEVY

The climate change levy (CCL) is a tax on energy

CLIMATE CHANGE LEVY

The climate change levy (CCL) is a tax on energy

Animals vocabulary review by herber

Animals vocabulary review by herber Методы решения текстовых задач

Методы решения текстовых задач Социальные функции и социальный механизм действия права

Социальные функции и социальный механизм действия права Понятие, признаки и структура норм права

Понятие, признаки и структура норм права На пути к жизненному успеху

На пути к жизненному успеху Ацетилен и его гомологи

Ацетилен и его гомологи die Schweiz

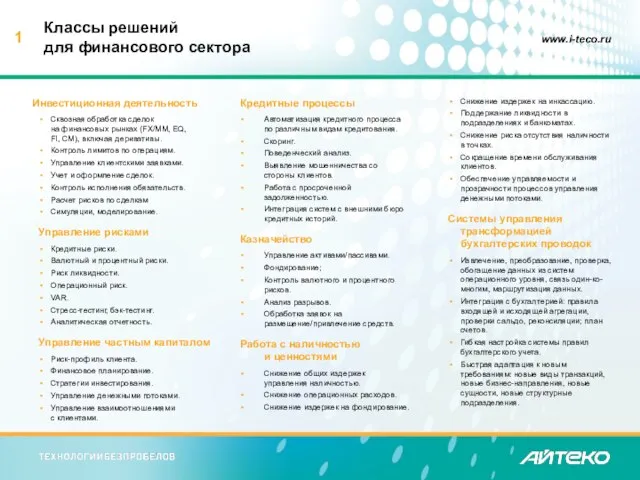

die Schweiz Классы решений для финансового сектора

Классы решений для финансового сектора Отчёт учителя английского языка Полуэктовой Е.С. за март- июнь 2012г.

Отчёт учителя английского языка Полуэктовой Е.С. за март- июнь 2012г. 40 ГОДИНИ СПЕЦИАЛНОСТ “ИНФОРМАТИКА” Ние сме във времето и времето е в нас... [Васил Левски]

40 ГОДИНИ СПЕЦИАЛНОСТ “ИНФОРМАТИКА” Ние сме във времето и времето е в нас... [Васил Левски] Презентация на тему Модификационная изменчивость 9 - 10 класс

Презентация на тему Модификационная изменчивость 9 - 10 класс Великие ученые

Великие ученые ГОУ ВПО ХМАО-Югры «Ханты-Мансийская государственная медицинская академия»

ГОУ ВПО ХМАО-Югры «Ханты-Мансийская государственная медицинская академия» Статистика рынка Казахстана с точки зрения карточных интернет транзакций

Статистика рынка Казахстана с точки зрения карточных интернет транзакций Щи

Щи Продвижение в социальных сетях и реклама в блогах

Продвижение в социальных сетях и реклама в блогах Отчет о ходе реализации целевой программы Калининградской области «Развитие здравоохранения Калининградской области на период

Отчет о ходе реализации целевой программы Калининградской области «Развитие здравоохранения Калининградской области на период  Презентация на тему Ферменты

Презентация на тему Ферменты Что мы знаем о местоимении?

Что мы знаем о местоимении? Работы в технике айрисфолдинг

Работы в технике айрисфолдинг Психосексуальное развитие детей и подростков

Психосексуальное развитие детей и подростков О ФОРМИРОВАНИИ АРХИВНОГО ФОНДА ДАННЫХ О СОСТОЯНИИ ОКРУЖАЮЩЕЙ СРЕДЫ, ЕЕ ЗАГРЯЗНЕНИИ

О ФОРМИРОВАНИИ АРХИВНОГО ФОНДА ДАННЫХ О СОСТОЯНИИ ОКРУЖАЮЩЕЙ СРЕДЫ, ЕЕ ЗАГРЯЗНЕНИИ «Социальная реабилитация людей с особенностями психофизического развития и организация временной занятости молодежи».

«Социальная реабилитация людей с особенностями психофизического развития и организация временной занятости молодежи». Тема:

Тема: Создание индивидуального стиля заказчика по мотивам ретро-стилей 50-70 годов ХХ века

Создание индивидуального стиля заказчика по мотивам ретро-стилей 50-70 годов ХХ века Надежность технологической системы

Надежность технологической системы Bed_Wars

Bed_Wars Эрнест Хемингуэй. Старик и море

Эрнест Хемингуэй. Старик и море