- Taxation in the United States of America

Содержание

- 2. PLAN The tax system of USA Payroll taxes Property taxes Income taxes Sales taxes Excise taxes

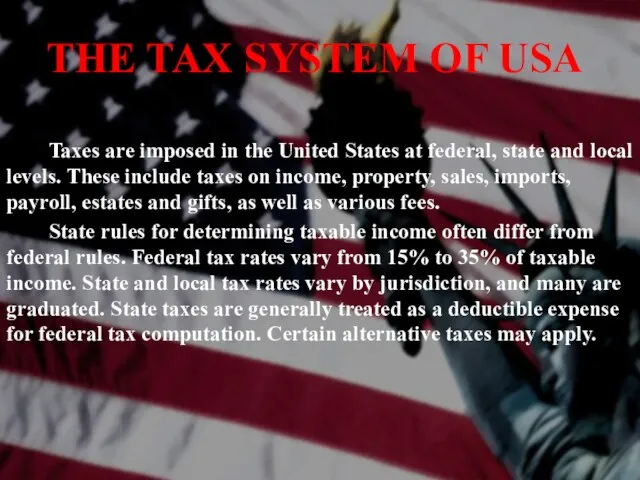

- 3. THE TAX SYSTEM OF USA Taxes are imposed in the United States at federal, state and

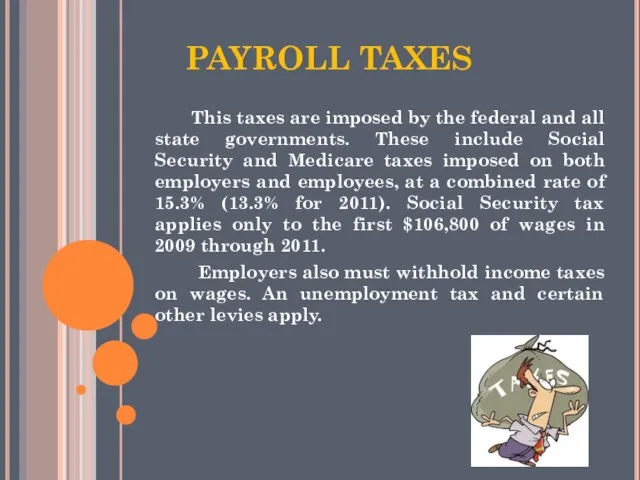

- 4. PAYROLL TAXES This taxes are imposed by the federal and all state governments. These include Social

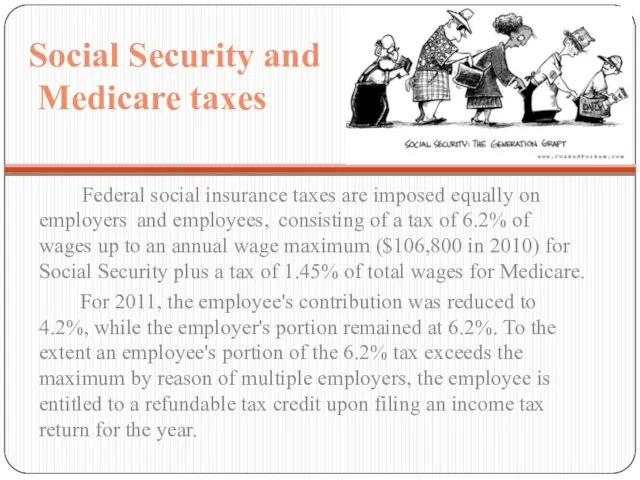

- 5. Social Security and Medicare taxes Federal social insurance taxes are imposed equally on employers and employees,

- 6. TAXES Employers are subject to unemployment taxes by the federal and all state governments. The tax

- 7. Property taxes Property taxes are imposed by most local governments and many special purpose authorities based

- 8. Income tax The U.S. income tax system imposes a tax based on income on individuals, corporations,

- 9. Income tax rates differ at the federal and state levels for corporations and individuals. Individuals are

- 10. Sales taxes Sales taxes are imposed on the price at retail sale of many goods and

- 11. The United States imposes tariffs or customs duties on the import of many types of goods

- 12. EXCISE TAXES Excise taxes may be imposed on the sales price of goods or on a

- 13. Estate and gift taxes Estate and gift taxes in the United States are imposed by the

- 14. Licenses and occupational taxes Many jurisdictions within the United States impose taxes or fees on the

- 16. Скачать презентацию

Слайд 2PLAN

The tax system of USA

Payroll taxes

Property taxes

Income taxes

Sales taxes

Excise taxes

Estate and gift

PLAN

The tax system of USA

Payroll taxes

Property taxes

Income taxes

Sales taxes

Excise taxes

Estate and gift

Слайд 3 THE TAX SYSTEM OF USA

Taxes are imposed in the United States at

THE TAX SYSTEM OF USA

Taxes are imposed in the United States at

Слайд 4PAYROLL TAXES

This taxes are imposed by the federal and all state

PAYROLL TAXES

This taxes are imposed by the federal and all state

Слайд 5Social Security and

Medicare taxes

Federal social insurance taxes are imposed equally

Social Security and

Medicare taxes

Federal social insurance taxes are imposed equally

Слайд 6 TAXES

Employers are subject to unemployment taxes by the federal and all

TAXES

Employers are subject to unemployment taxes by the federal and all

Слайд 7Property taxes

Property taxes are imposed by most local governments and many special purpose

Property taxes

Property taxes are imposed by most local governments and many special purpose

Слайд 8Income tax

The U.S. income tax system imposes a tax based

Income tax

The U.S. income tax system imposes a tax based

Слайд 9 Income tax rates differ at the federal and state levels for

Income tax rates differ at the federal and state levels for

Слайд 10Sales taxes

Sales taxes are imposed on the price at retail sale

Sales taxes

Sales taxes are imposed on the price at retail sale

Слайд 11 The United States imposes tariffs or customs duties on the import

The United States imposes tariffs or customs duties on the import

Слайд 12EXCISE TAXES

Excise taxes may be imposed on the sales price of goods

EXCISE TAXES

Excise taxes may be imposed on the sales price of goods

Слайд 13Estate and gift taxes

Estate and gift taxes in the United States

Estate and gift taxes

Estate and gift taxes in the United States

Слайд 14Licenses and

occupational taxes

Many jurisdictions within the United States impose taxes

Licenses and

occupational taxes

Many jurisdictions within the United States impose taxes

Ли́зинг (англ. leasing от англ. to lease — сдать в аренду)

Ли́зинг (англ. leasing от англ. to lease — сдать в аренду) Электронные деньги и формы их использования

Электронные деньги и формы их использования 21 лютого - День рідної мови

21 лютого - День рідної мови Сертификация и качественные испытания в области пожарной безопасности

Сертификация и качественные испытания в области пожарной безопасности Презентация на тему Юрий Долгорукий

Презентация на тему Юрий Долгорукий  Russian Surginet

Russian Surginet Презентация на тему Значение физических упражнений для формирования скелета и мышц

Презентация на тему Значение физических упражнений для формирования скелета и мышц  Conditionals

Conditionals МОУ «Маловская средняя общеобразовательная школа» Проект «ЕГЭ на 100 баллов!» Выполнил: учитель истории Загдаева Н.А. 2010 год

МОУ «Маловская средняя общеобразовательная школа» Проект «ЕГЭ на 100 баллов!» Выполнил: учитель истории Загдаева Н.А. 2010 год Старинные зимние обычаи и праздники, «Рождество», «Святки»

Старинные зимние обычаи и праздники, «Рождество», «Святки» Презентация рекламного агентства Ambitica

Презентация рекламного агентства Ambitica «AstorFest 2009» К иїв 13-14 Жовтня

«AstorFest 2009» К иїв 13-14 Жовтня Шаблон_отчет_маркетинг_еженедльный_внутренний

Шаблон_отчет_маркетинг_еженедльный_внутренний Бел_ пчёл из син_ туч_ Вылета_ рой летуч_. Не гуд_ и не куса_, На ладошк_ тёпл_ та_.

Бел_ пчёл из син_ туч_ Вылета_ рой летуч_. Не гуд_ и не куса_, На ладошк_ тёпл_ та_. Переходные формы в эволюции

Переходные формы в эволюции Электронное управление. Проблемы и пути их решения

Электронное управление. Проблемы и пути их решения День космонавтики (4 класс)

День космонавтики (4 класс) Финансовые отношения

Финансовые отношения Звонки в центры чрезвычайных ситуаций

Звонки в центры чрезвычайных ситуаций ПРОДУКТЫ ДЛЯ ЧАСТНЫХ КЛИЕНТОВ

ПРОДУКТЫ ДЛЯ ЧАСТНЫХ КЛИЕНТОВ Рукописная книга

Рукописная книга Продолжите предложения:

Продолжите предложения: УЧЕТ ВНЕБЮДЖЕТНЫХ ДОХОДОВ БЮДЖЕТНЫХ УЧРЕЖДЕНИЙ РЕСТРУКТУРИЗАЦИЯ БЮДЖЕТНЫХ УЧРЕЖДЕНИЙ Сентябрь, 2003 А.Ковалевская

УЧЕТ ВНЕБЮДЖЕТНЫХ ДОХОДОВ БЮДЖЕТНЫХ УЧРЕЖДЕНИЙ РЕСТРУКТУРИЗАЦИЯ БЮДЖЕТНЫХ УЧРЕЖДЕНИЙ Сентябрь, 2003 А.Ковалевская Эмоции

Эмоции Состязание юных Математиков

Состязание юных Математиков Наиболее важные основные особенности пешего туризма по равнинной местности

Наиболее важные основные особенности пешего туризма по равнинной местности Межличностные конфликты, их конструктивное решение

Межличностные конфликты, их конструктивное решение Основы безопасности информационных систем

Основы безопасности информационных систем