- Accounts Receivable Management

Содержание

- 2. After studying this theme, you should be able to: List the key factors that can be

- 3. Credit and Collection Policies Analyzing the Credit Applicant

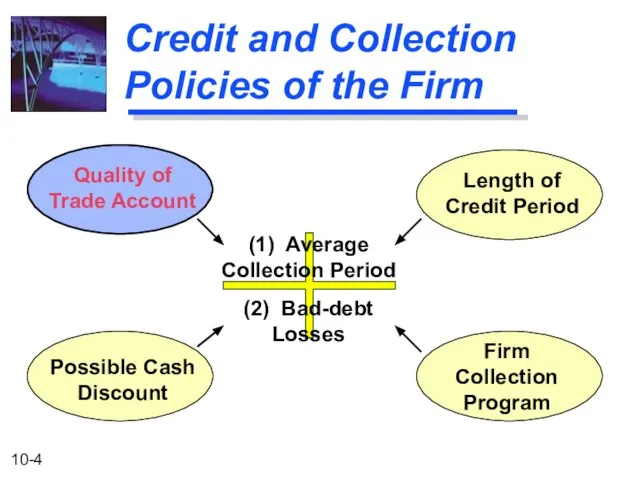

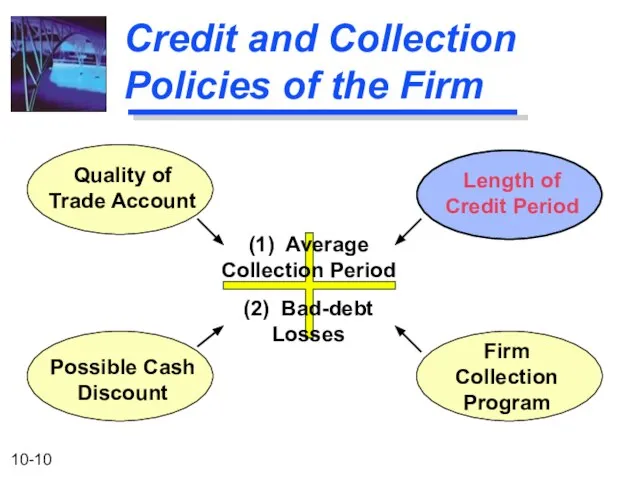

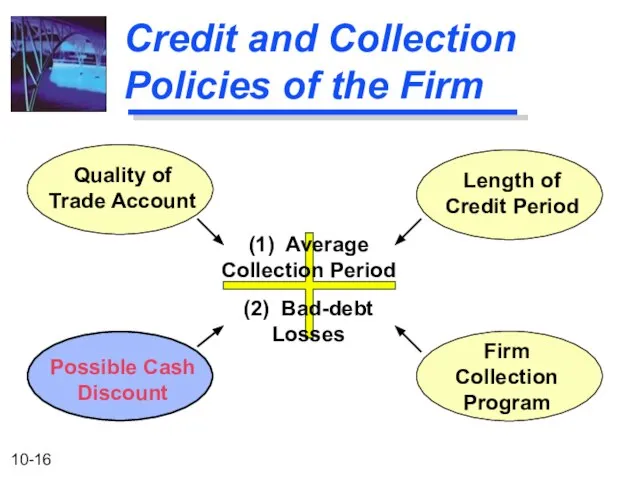

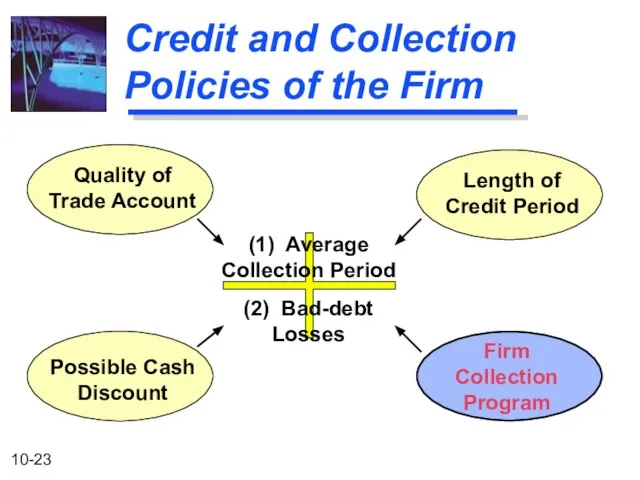

- 4. Credit and Collection Policies of the Firm (1) Average Collection Period (2) Bad-debt Losses Quality of

- 5. Credit Standards The financial manager should continually lower the firm’s credit standards as long as profitability

- 6. Credit Standards A larger credit department Additional clerical work Servicing additional accounts Bad-debt losses Opportunity costs

- 7. Example of Relaxing Credit Standards Basket Wonders is not operating at full capacity and wants to

- 8. Example of Relaxing Credit Standards Additional annual credit sales of $120,000 and an average collection period

- 9. Example of Relaxing Credit Standards Profitability of ($5 contribution) x (4,800 units) = additional sales $24,000

- 10. Credit and Collection Policies of the Firm (1) Average Collection Period (2) Bad-debt Losses Quality of

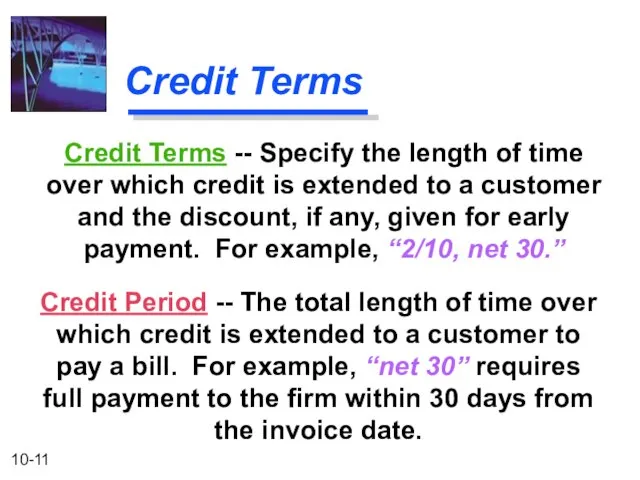

- 11. Credit Terms Credit Period -- The total length of time over which credit is extended to

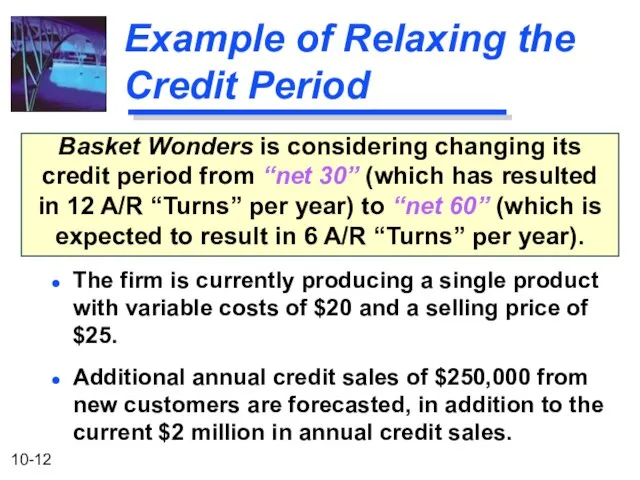

- 12. Example of Relaxing the Credit Period Basket Wonders is considering changing its credit period from “net

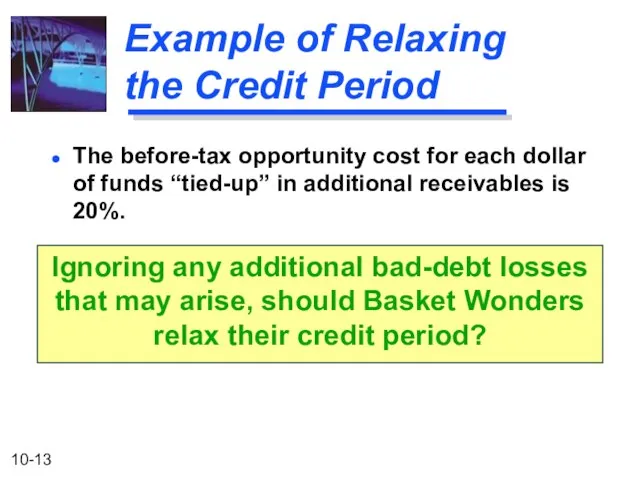

- 13. Example of Relaxing the Credit Period The before-tax opportunity cost for each dollar of funds “tied-up”

- 14. Example of Relaxing the Credit Period Profitability of ($5 contribution)x(10,000 units) = additional sales $50,000 Additional

- 15. Example of Relaxing the Credit Period New ($2,000,000 sales) / (6 Turns) = receivable level $333,333

- 16. Credit and Collection Policies of the Firm (1) Average Collection Period (2) Bad-debt Losses Quality of

- 17. Credit Terms Cash Discount -- A percent (%) reduction in sales or purchase price allowed for

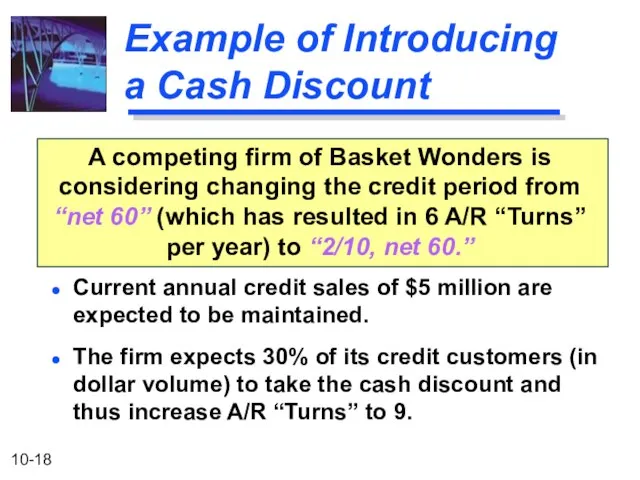

- 18. Example of Introducing a Cash Discount A competing firm of Basket Wonders is considering changing the

- 19. The before-tax opportunity cost for each dollar of funds “tied-up” in additional receivables is 20%. Ignoring

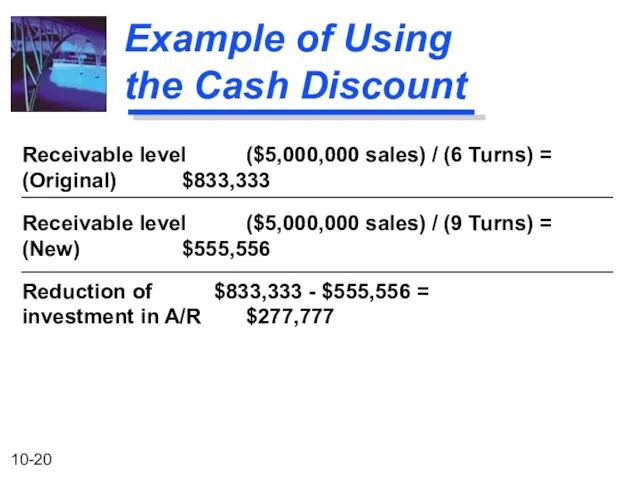

- 20. Example of Using the Cash Discount Receivable level ($5,000,000 sales) / (6 Turns) = (Original) $833,333

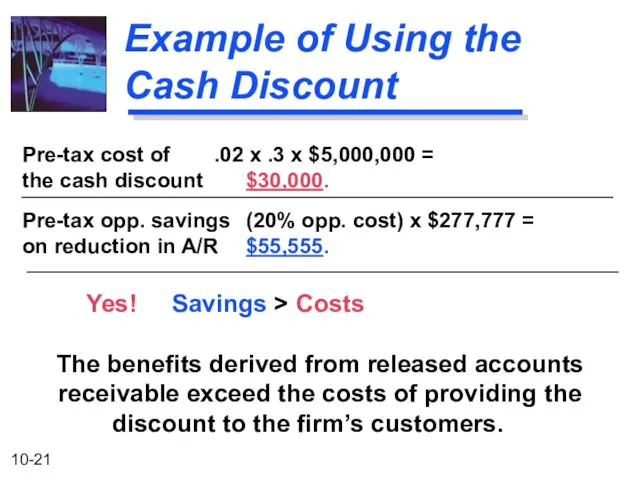

- 21. Pre-tax cost of .02 x .3 x $5,000,000 = the cash discount $30,000. Pre-tax opp. savings

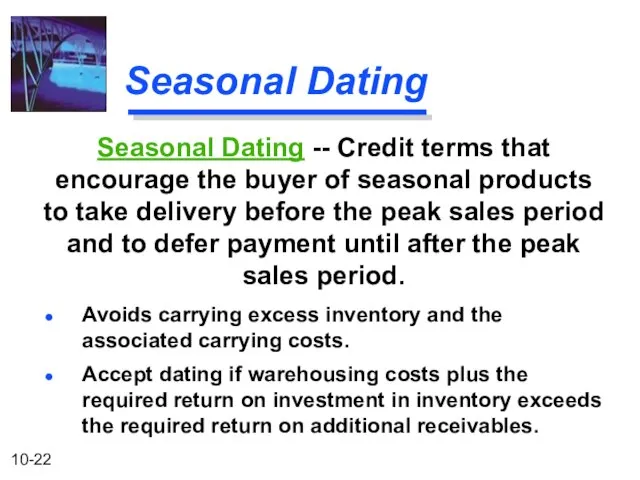

- 22. Seasonal Dating Avoids carrying excess inventory and the associated carrying costs. Accept dating if warehousing costs

- 23. Credit and Collection Policies of the Firm (1) Average Collection Period (2) Bad-debt Losses Quality of

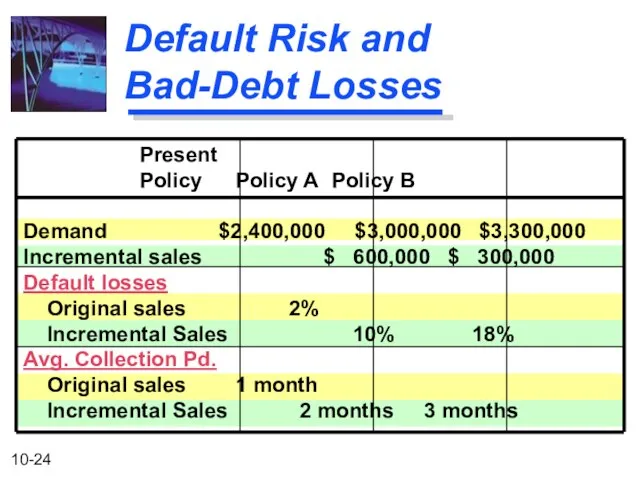

- 24. Default Risk and Bad-Debt Losses Present Policy Policy A Policy B Demand $2,400,000 $3,000,000 $3,300,000 Incremental

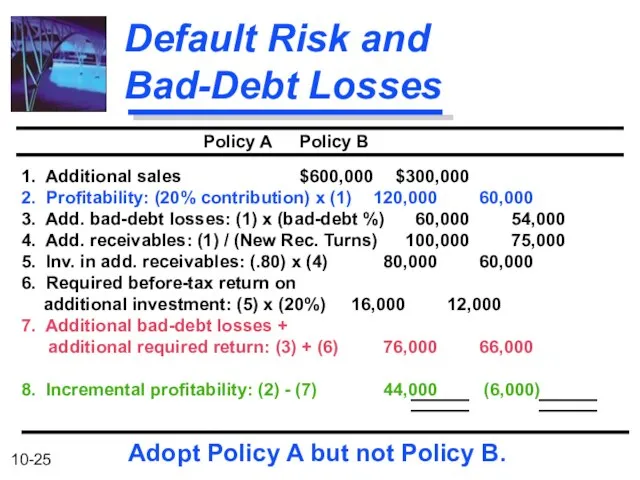

- 25. Default Risk and Bad-Debt Losses Policy A Policy B 1. Additional sales $600,000 $300,000 2. Profitability:

- 27. Скачать презентацию

Слайд 3Credit and Collection Policies

Analyzing the Credit Applicant

Credit and Collection Policies

Analyzing the Credit Applicant

Слайд 4Credit and Collection Policies of the Firm

(1) Average

Collection Period

(2) Bad-debt

Losses

Quality of

Trade

Credit and Collection Policies of the Firm

(1) Average

Collection Period

(2) Bad-debt

Losses

Quality of

Trade

Слайд 5Credit Standards

The financial manager should continually lower the firm’s credit standards as

Credit Standards

The financial manager should continually lower the firm’s credit standards as

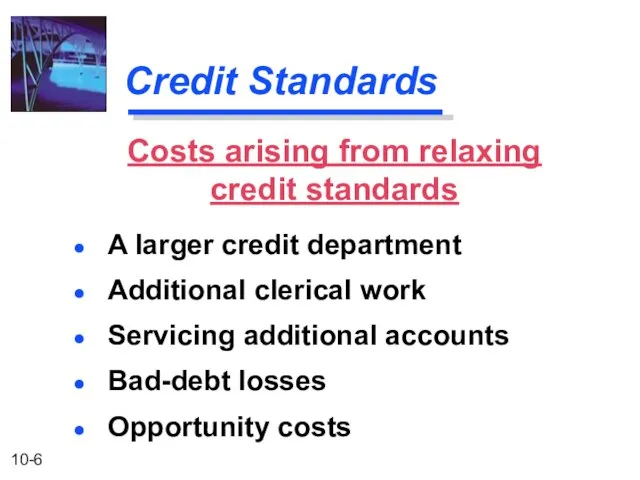

Слайд 6Credit Standards

A larger credit department

Additional clerical work

Servicing additional accounts

Bad-debt losses

Opportunity costs

Costs arising

Credit Standards

A larger credit department

Additional clerical work

Servicing additional accounts

Bad-debt losses

Opportunity costs

Costs arising

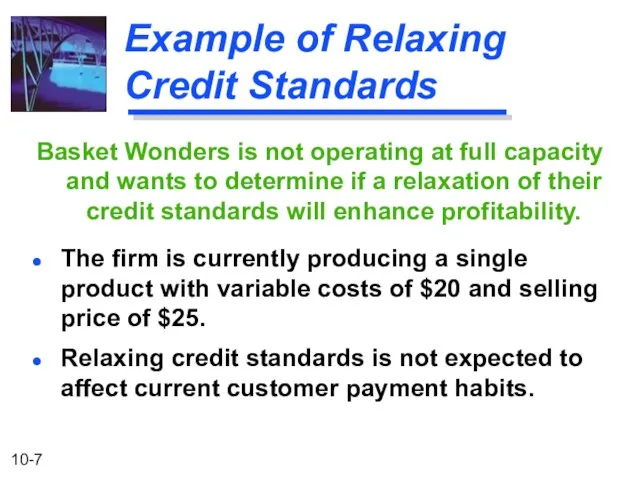

Слайд 7Example of Relaxing Credit Standards

Basket Wonders is not operating at full capacity

Example of Relaxing Credit Standards

Basket Wonders is not operating at full capacity

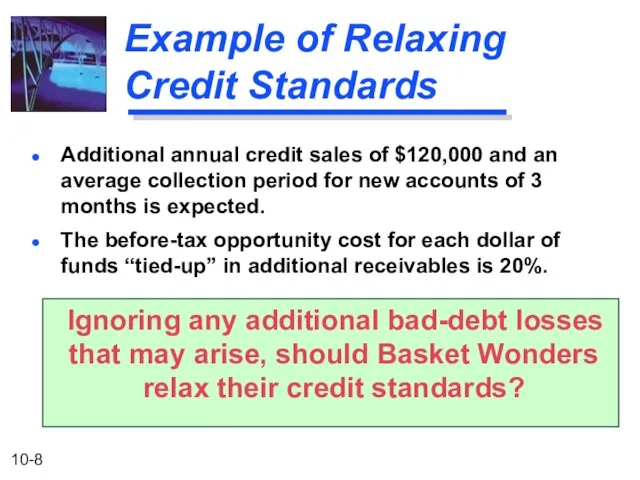

Слайд 8Example of Relaxing Credit Standards

Additional annual credit sales of $120,000 and an

Example of Relaxing Credit Standards

Additional annual credit sales of $120,000 and an

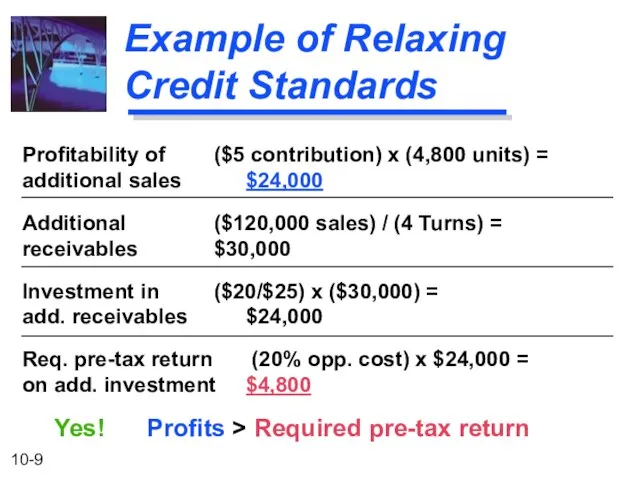

Слайд 9Example of Relaxing Credit Standards

Profitability of ($5 contribution) x (4,800 units) =

additional

Example of Relaxing Credit Standards

Profitability of ($5 contribution) x (4,800 units) =

additional

Слайд 10Credit and Collection Policies of the Firm

(1) Average

Collection Period

(2) Bad-debt

Losses

Quality of

Trade

Credit and Collection Policies of the Firm

(1) Average

Collection Period

(2) Bad-debt

Losses

Quality of

Trade

Слайд 11Credit Terms

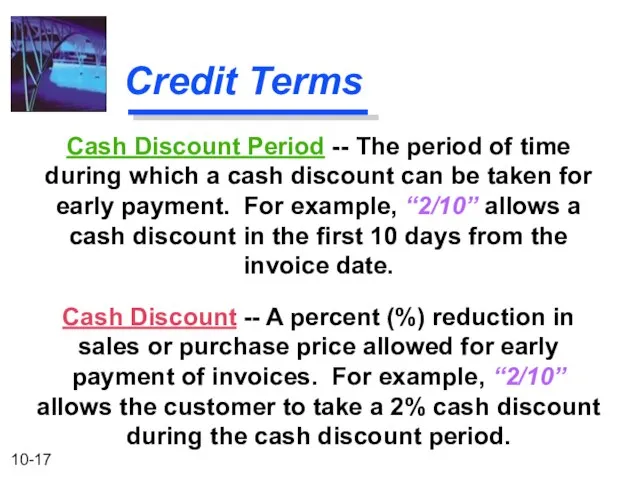

Credit Period -- The total length of time over which credit

Credit Terms

Credit Period -- The total length of time over which credit

Слайд 12Example of Relaxing the Credit Period

Basket Wonders is considering changing its credit

Example of Relaxing the Credit Period

Basket Wonders is considering changing its credit

Слайд 13Example of Relaxing the Credit Period

The before-tax opportunity cost for each dollar

Example of Relaxing the Credit Period

The before-tax opportunity cost for each dollar

Слайд 14Example of Relaxing the Credit Period

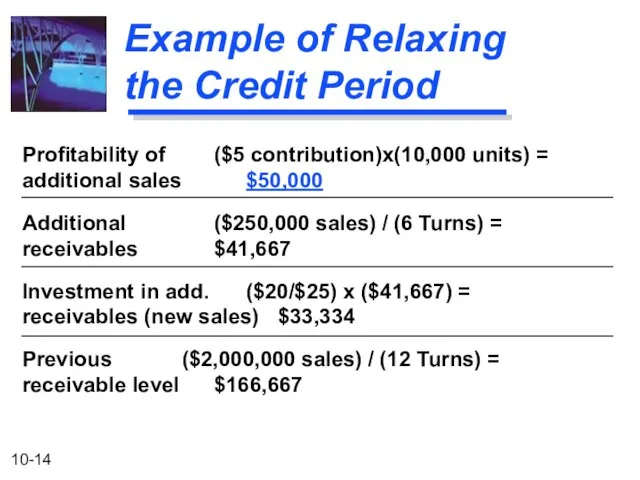

Profitability of ($5 contribution)x(10,000 units) =

additional sales $50,000

Additional

Example of Relaxing the Credit Period

Profitability of ($5 contribution)x(10,000 units) =

additional sales $50,000

Additional

Слайд 15Example of Relaxing the Credit Period

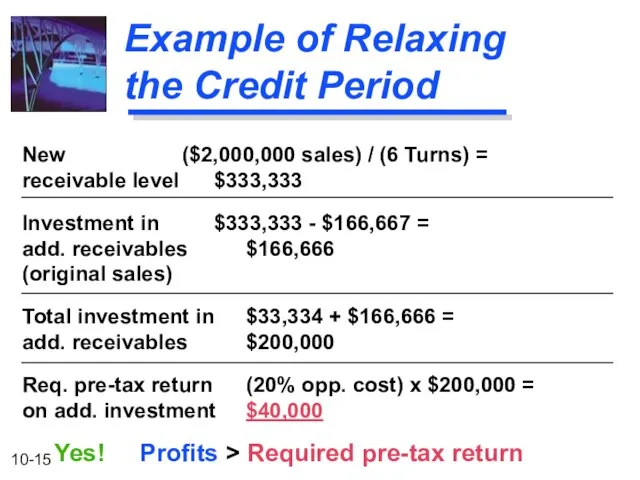

New ($2,000,000 sales) / (6 Turns) =

receivable

Example of Relaxing the Credit Period

New ($2,000,000 sales) / (6 Turns) =

receivable

Слайд 16Credit and Collection Policies of the Firm

(1) Average

Collection Period

(2) Bad-debt

Losses

Quality of

Trade

Credit and Collection Policies of the Firm

(1) Average

Collection Period

(2) Bad-debt

Losses

Quality of

Trade

Слайд 17Credit Terms

Cash Discount -- A percent (%) reduction in sales or purchase

Credit Terms

Cash Discount -- A percent (%) reduction in sales or purchase

Слайд 18Example of Introducing a Cash Discount

A competing firm of Basket Wonders is

Example of Introducing a Cash Discount

A competing firm of Basket Wonders is

Слайд 19The before-tax opportunity cost for each dollar of funds “tied-up” in additional

The before-tax opportunity cost for each dollar of funds “tied-up” in additional

Слайд 20Example of Using the Cash Discount

Receivable level ($5,000,000 sales) / (6 Turns)

Example of Using the Cash Discount

Receivable level ($5,000,000 sales) / (6 Turns)

Слайд 21Pre-tax cost of .02 x .3 x $5,000,000 =

the cash discount $30,000.

Pre-tax

Pre-tax cost of .02 x .3 x $5,000,000 =

the cash discount $30,000.

Pre-tax

Слайд 22Seasonal Dating

Avoids carrying excess inventory and the associated carrying costs.

Accept dating if

Seasonal Dating

Avoids carrying excess inventory and the associated carrying costs.

Accept dating if

Слайд 23Credit and Collection Policies of the Firm

(1) Average

Collection Period

(2) Bad-debt

Losses

Quality of

Trade

Credit and Collection Policies of the Firm

(1) Average

Collection Period

(2) Bad-debt

Losses

Quality of

Trade

Слайд 24Default Risk and Bad-Debt Losses

Present

Policy Policy A Policy B

Demand $2,400,000 $3,000,000 $3,300,000

Incremental

Default Risk and Bad-Debt Losses

Present

Policy Policy A Policy B

Demand $2,400,000 $3,000,000 $3,300,000

Incremental

Слайд 25Default Risk and Bad-Debt Losses

Policy A Policy B

1. Additional sales $600,000 $300,000

2.

Default Risk and Bad-Debt Losses

Policy A Policy B

1. Additional sales $600,000 $300,000

2.

Основні і оборотні фонди залізничного тарнспорту. Лекція 7

Основні і оборотні фонди залізничного тарнспорту. Лекція 7 Педагогика лек 7 -2022

Педагогика лек 7 -2022 Информационное обеспечение системы обязательного медицинского страхования

Информационное обеспечение системы обязательного медицинского страхования Презентация на тему Основные понятия генетики

Презентация на тему Основные понятия генетики Азбука плавания

Азбука плавания Современные и перспективные технологии разработки прикладных систем

Современные и перспективные технологии разработки прикладных систем Профориентационная работа Профориентационная работа с учащимися.

Профориентационная работа Профориентационная работа с учащимися. Как возникло франкское государство

Как возникло франкское государство Презентация на тему 300 лет Нижегородской губернии

Презентация на тему 300 лет Нижегородской губернии  Презентация на тему Моя будущая профессия

Презентация на тему Моя будущая профессия  Мощные производители из наиболее развитых провинций - Цзянсу

Мощные производители из наиболее развитых провинций - Цзянсу Права человека

Права человека Презентация на тему Электроёмкость

Презентация на тему Электроёмкость KazakhParty-ға қош келдіңіз. Үйлену тойы

KazakhParty-ға қош келдіңіз. Үйлену тойы ДискретизацияСверткаДПФ

ДискретизацияСверткаДПФ Использование компьютерного тестирования на уроках английского языка

Использование компьютерного тестирования на уроках английского языка Микропроцессоры

Микропроцессоры Дети@Mail.Ru

Дети@Mail.Ru Печенье Oreo

Печенье Oreo Пути активизации устной речи на уроках английского языка в рамках коммуникативной методики обучения

Пути активизации устной речи на уроках английского языка в рамках коммуникативной методики обучения Загадки деда мороза

Загадки деда мороза Chanel- один из самых влиятельных французских домов моды

Chanel- один из самых влиятельных французских домов моды психология упр 2

психология упр 2 Регламент на автовыставку

Регламент на автовыставку Результаты учебной деятельности за 2010-2011 учебный год

Результаты учебной деятельности за 2010-2011 учебный год Экологические кризисы 9 класс

Экологические кризисы 9 класс Обеспечение безопасности детей при работе в Интернет

Обеспечение безопасности детей при работе в Интернет Управление бизнес-проектами в коммуникациях

Управление бизнес-проектами в коммуникациях