- Corporate Governance: A Review of Current

Содержание

- 2. Sources of Research Agenda Finance Agency theory – investigation of different corporate governance practices and firm

- 3. Research Effectiveness may be based on a number of different dimensions of corporate governance, ranging from

- 4. Research Board characteristics and composition Resource dependency approach Transaction costs theory Role and effects of independence

- 5. Research Board processes Effects of duality of CEO role Stewardship theory Executive compensation Managerial stock ownership

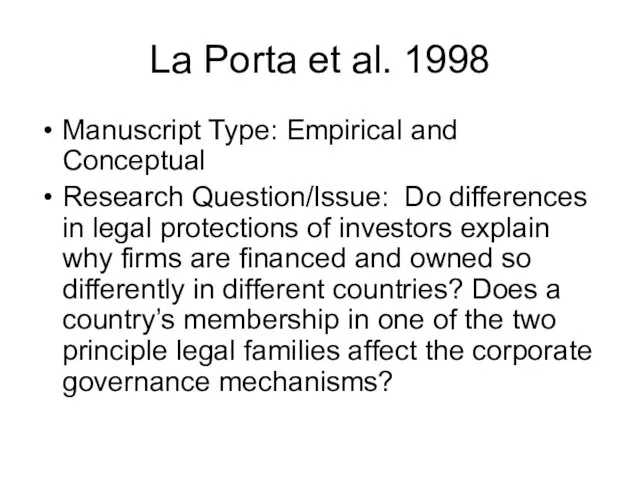

- 6. La Porta et al. 1998 Manuscript Type: Empirical and Conceptual Research Question/Issue: Do differences in legal

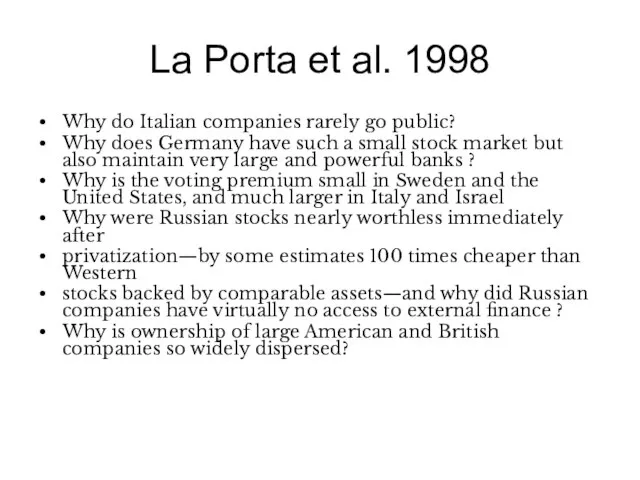

- 7. La Porta et al. 1998 Why do Italian companies rarely go public? Why does Germany have

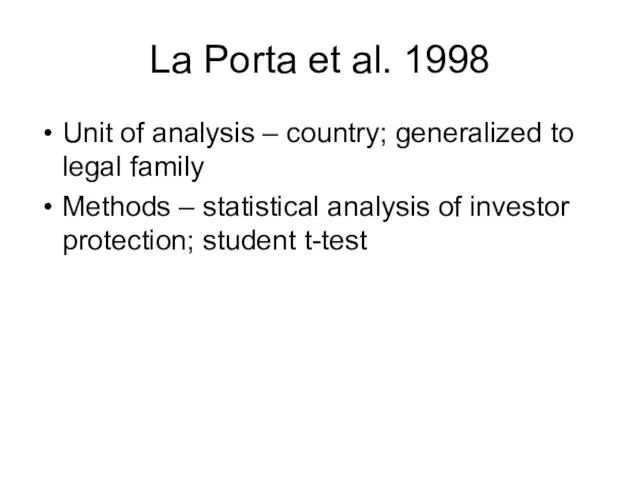

- 8. La Porta et al. 1998 Unit of analysis – country; generalized to legal family Methods –

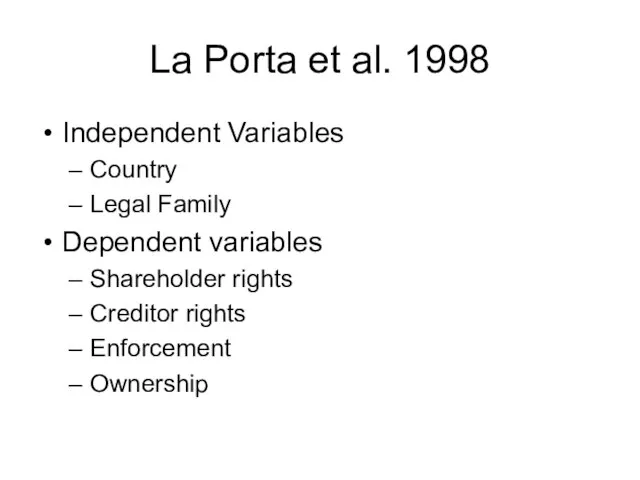

- 9. La Porta et al. 1998 Independent Variables Country Legal Family Dependent variables Shareholder rights Creditor rights

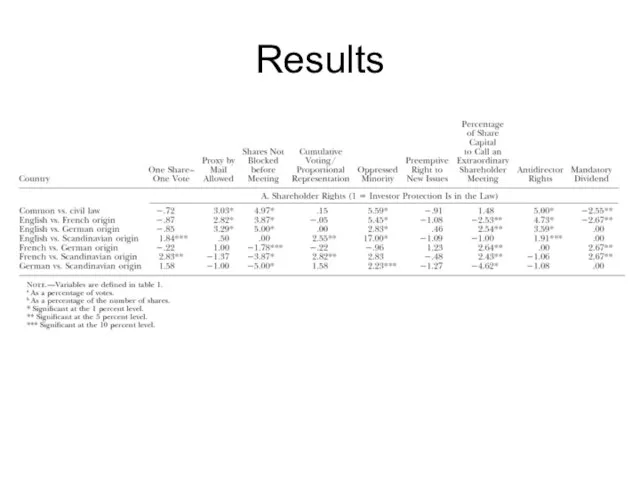

- 10. Results

- 11. La Porta et al. 1998 Research Findings/Results: The results show that common-law countries generally have the

- 12. Shleifer and Vishny 1997 Agency problem Contracts Managerial Discretion Incentive Contracts Evidence on agency problem –

- 13. Shleifer and Vishny 1997 Finance without governance – reputation Legal Enforcement of Rights Large Investors Takeovers

- 14. Shleifer and Vishny 1997 Debt versus equity choice LBO Cooperatives and State ownership

- 15. La Porta et al. 1999 Studied ownership structures of large corporations in 27 wealthy economies to

- 16. Yermack 1996 Smaller boards of directors are more efficient than larger boards Theory Large boards have

- 17. Jensen 1993 Claims that since 1973 technological, political, regulatory, and economic forces have been changing the

- 18. Jensen 1993 IC systems have failed to require managers to make decisions to properly manage the

- 20. Скачать презентацию

Слайд 2Sources of Research Agenda

Finance

Agency theory – investigation of different corporate governance practices

Sources of Research Agenda

Finance

Agency theory – investigation of different corporate governance practices

Слайд 3Research

Effectiveness may be based on a number of different dimensions of corporate

Research

Effectiveness may be based on a number of different dimensions of corporate

Слайд 4Research

Board characteristics and composition

Resource dependency approach

Transaction costs theory

Role and effects of

Research

Board characteristics and composition

Resource dependency approach

Transaction costs theory

Role and effects of

Слайд 5Research

Board processes

Effects of duality of CEO role

Stewardship theory

Executive compensation

Managerial stock

Research

Board processes

Effects of duality of CEO role

Stewardship theory

Executive compensation

Managerial stock

Слайд 6La Porta et al. 1998

Manuscript Type: Empirical and Conceptual

Research Question/Issue: Do differences

La Porta et al. 1998

Manuscript Type: Empirical and Conceptual

Research Question/Issue: Do differences

Слайд 7La Porta et al. 1998

Why do Italian companies rarely go public?

Why does

La Porta et al. 1998

Why do Italian companies rarely go public?

Why does

Слайд 8La Porta et al. 1998

Unit of analysis – country; generalized to legal

La Porta et al. 1998

Unit of analysis – country; generalized to legal

Слайд 9La Porta et al. 1998

Independent Variables

Country

Legal Family

Dependent variables

Shareholder rights

Creditor rights

Enforcement

Ownership

La Porta et al. 1998

Independent Variables

Country

Legal Family

Dependent variables

Shareholder rights

Creditor rights

Enforcement

Ownership

Слайд 10Results

Results

Слайд 11La Porta et al. 1998

Research Findings/Results: The results show that common-law countries

La Porta et al. 1998

Research Findings/Results: The results show that common-law countries

Слайд 12Shleifer and Vishny 1997

Agency problem

Contracts

Managerial Discretion

Incentive Contracts

Evidence on agency problem – does

Shleifer and Vishny 1997

Agency problem

Contracts

Managerial Discretion

Incentive Contracts

Evidence on agency problem – does

Слайд 13Shleifer and Vishny 1997

Finance without governance – reputation

Legal Enforcement of Rights

Large Investors

Takeovers

Large

Shleifer and Vishny 1997

Finance without governance – reputation

Legal Enforcement of Rights

Large Investors

Takeovers

Large

Слайд 14Shleifer and Vishny 1997

Debt versus equity choice

LBO

Cooperatives and State ownership

Shleifer and Vishny 1997

Debt versus equity choice

LBO

Cooperatives and State ownership

Слайд 15La Porta et al. 1999

Studied ownership structures of large corporations in 27

La Porta et al. 1999

Studied ownership structures of large corporations in 27

Слайд 16Yermack 1996

Smaller boards of directors are more efficient than larger boards

Theory

Large boards

Yermack 1996

Smaller boards of directors are more efficient than larger boards

Theory

Large boards

Слайд 17Jensen 1993

Claims that since 1973 technological, political, regulatory, and economic forces have

Jensen 1993

Claims that since 1973 technological, political, regulatory, and economic forces have

Слайд 18Jensen 1993

IC systems have failed to require managers to make decisions to

Jensen 1993

IC systems have failed to require managers to make decisions to

ПОРТФОЛИО ВОСПИТАТЕЛЯ

ПОРТФОЛИО ВОСПИТАТЕЛЯ Презентация на тему Минойская цивилизация

Презентация на тему Минойская цивилизация  PHIL 1- Lecture 3 - Week 3 moodle

PHIL 1- Lecture 3 - Week 3 moodle Железнодорожный тоннель

Железнодорожный тоннель FINANCIAL ANALYSIS AND

FINANCIAL ANALYSIS AND Использование проектной методики в обучении иностранному языку

Использование проектной методики в обучении иностранному языку Система права

Система права Гигиена питания

Гигиена питания Гигиена коз и овец

Гигиена коз и овец Использование ФЦИОР на уроках физики

Использование ФЦИОР на уроках физики Налоговый вычет по ценным бумагам

Налоговый вычет по ценным бумагам Доли федеральных телеканалов при национальном и региональном размещении рекламы

Доли федеральных телеканалов при национальном и региональном размещении рекламы Презентация WasteVEM процесса

Презентация WasteVEM процесса Фея Флора. Богиня цветов и весны. С приходом весны властвовала над всеми живыми существами. Имя образовано от flos ("цветок"). По леген

Фея Флора. Богиня цветов и весны. С приходом весны властвовала над всеми живыми существами. Имя образовано от flos ("цветок"). По леген Старшов Петр Павлович

Старшов Петр Павлович Классицизм в литературе

Классицизм в литературе Методическая тема

Методическая тема He’s. She

He’s. She Программа коррекции синдрова эмоционального выгорания и повышения стрессоустойчивости личности

Программа коррекции синдрова эмоционального выгорания и повышения стрессоустойчивости личности Пирог Ленивец

Пирог Ленивец Учебный семинар «Формирование универсальных учебных действий на уроках в начальной школе»

Учебный семинар «Формирование универсальных учебных действий на уроках в начальной школе» Диалог о вредной привычке.

Диалог о вредной привычке. Права та обовязки споживачів

Права та обовязки споживачів Mother teresa

Mother teresa Удаление третьих моляров верхней и нижней челюсти. Ретенция и дистопия зубов мудрости

Удаление третьих моляров верхней и нижней челюсти. Ретенция и дистопия зубов мудрости Мыс өндіріс қалдықтарынан түсті металл тұздарын алуды жобалау

Мыс өндіріс қалдықтарынан түсті металл тұздарын алуды жобалау Персональное предложение по регистрации товарного знака Баранкино для ИП (ООО) Под ключ

Персональное предложение по регистрации товарного знака Баранкино для ИП (ООО) Под ключ Семь дней недели

Семь дней недели