- FINANCIAL ANALYSIS AND

Содержание

- 2. INTRODUCTION

- 3. FINANCIAL MODEL OF A COMPANY

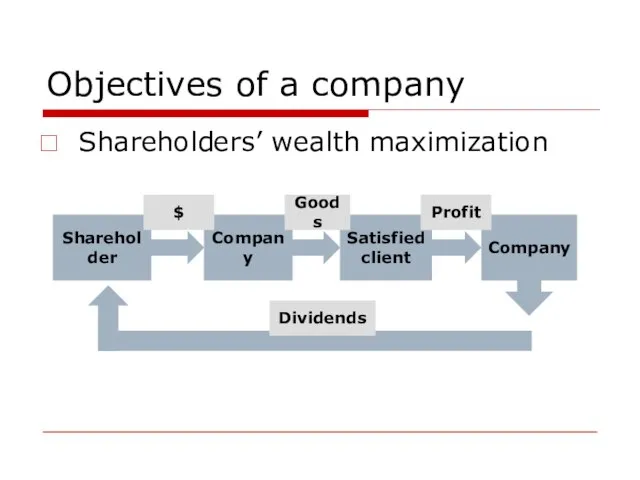

- 4. Objectives of a company Shareholders’ wealth maximization

- 5. Objectives of a company Stakeholders’ income increase: Shareholders Employees Managers Suppliers Clients Society

- 6. Functions of a financial manager Activity spheres of a financial manager: Strategic management – general objectives

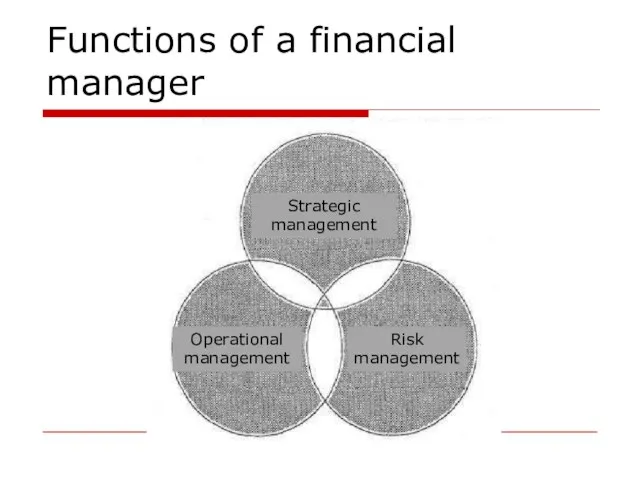

- 7. Functions of a financial manager

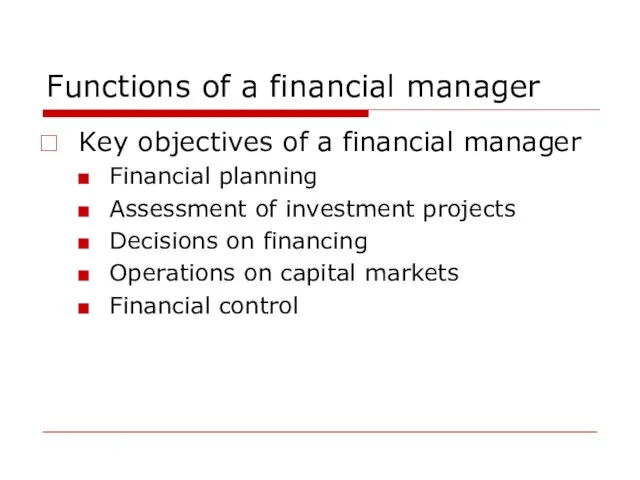

- 8. Functions of a financial manager Key objectives of a financial manager Financial planning Assessment of investment

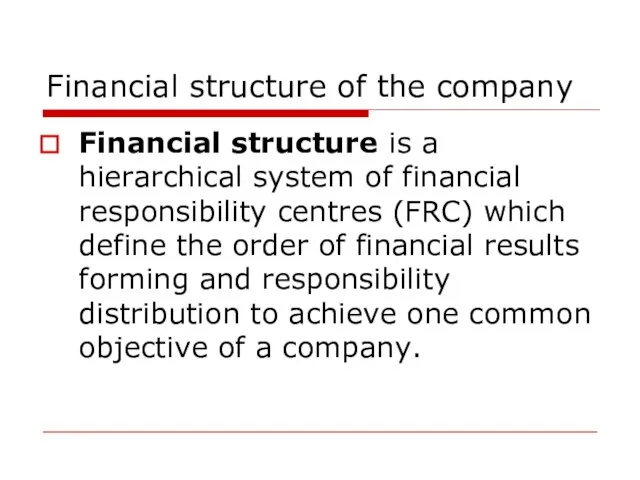

- 9. Financial structure of the company Financial structure is a hierarchical system of financial responsibility centres (FRC)

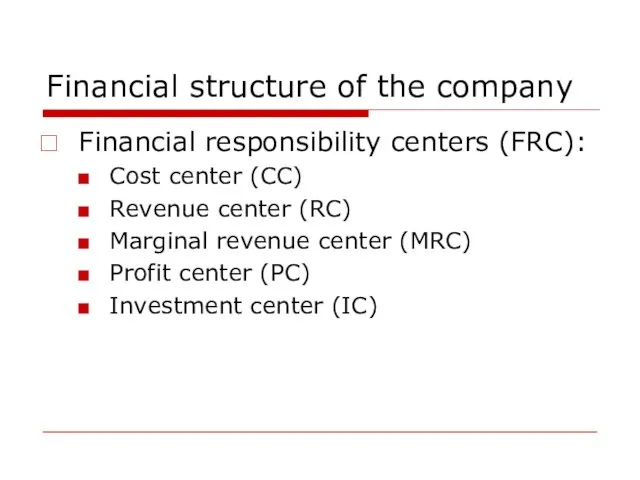

- 10. Financial structure of the company Financial responsibility centers (FRC): Cost center (CC) Revenue center (RC) Marginal

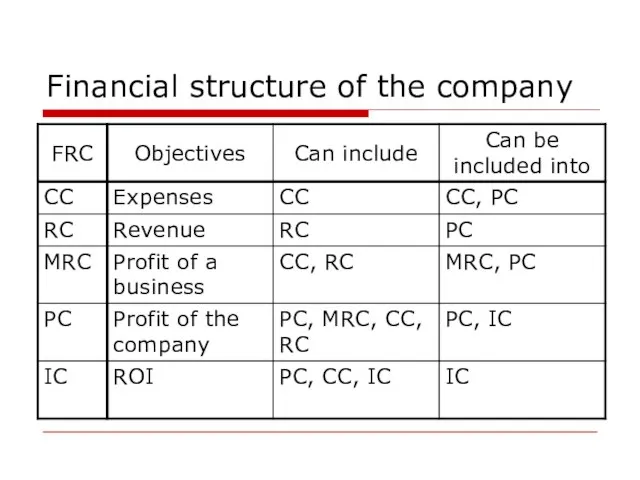

- 11. Financial structure of the company

- 12. Financial structure of the company How to from a financial structure: Organizational approach Process approach Define

- 13. Organizational approach An organizational structure is a mainly hierarchical concept of subordination of entities that collaborate

- 14. Organizational approach Functional organization

- 15. Organizational approach Functional organization

- 16. Organizational approach Projectized organization

- 17. Organizational approach Projectized organization

- 18. Organizational approach Matrix organization

- 19. Organizational approach Matrix organization

- 20. Organizational approach Financial structure PC Director + Fin.Director CC Manufacturing Workshop 1 Workshop 2 PC Enterprises

- 21. Organizational approach Differences between organizational and financial structures

- 22. Process approach A process is an activity which transforms input into output. A business process is

- 23. Process scheme

- 24. Process approach Business-process types: Main Supporting Development Corporate management

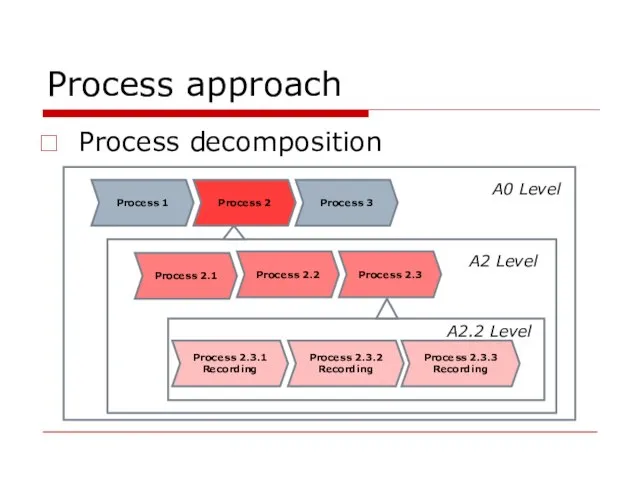

- 25. Process approach Process decomposition Process 1 Process 2 Process 3 Process 2.1 Process 2.2 Process 2.3

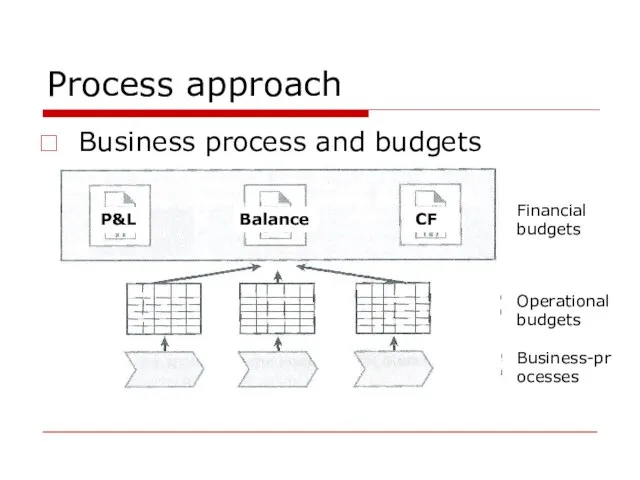

- 26. Process approach Business process and budgets P&L Balance CF Financial budgets Operational budgets Business-processes

- 27. BASIC PRINCIPLES OF FINANCIAL MANAGEMENT

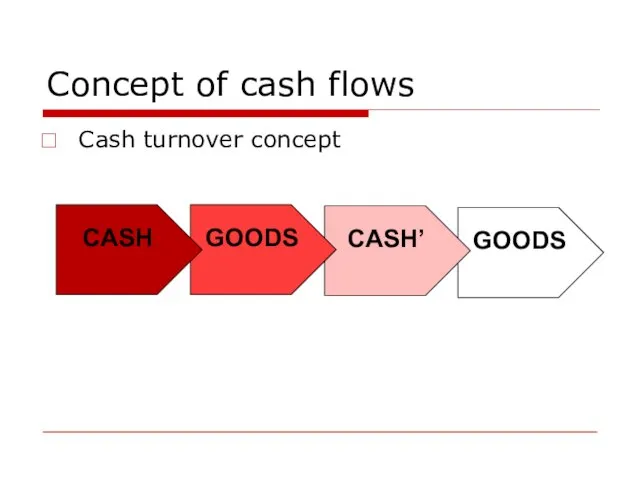

- 28. Concept of cash flows Cash turnover concept

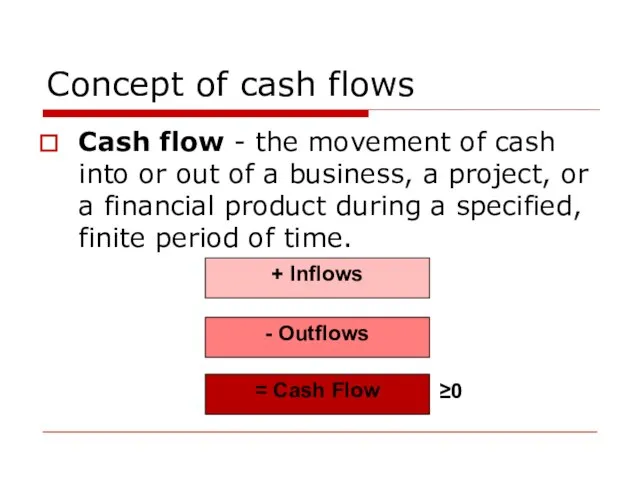

- 29. Concept of cash flows Cash flow - the movement of cash into or out of a

- 30. Relationship between risk & profit Nothing ventured, nothing gained Britain’s Special Air Service motto: Who dares,

- 31. ACCOUNTING SYSTEMS

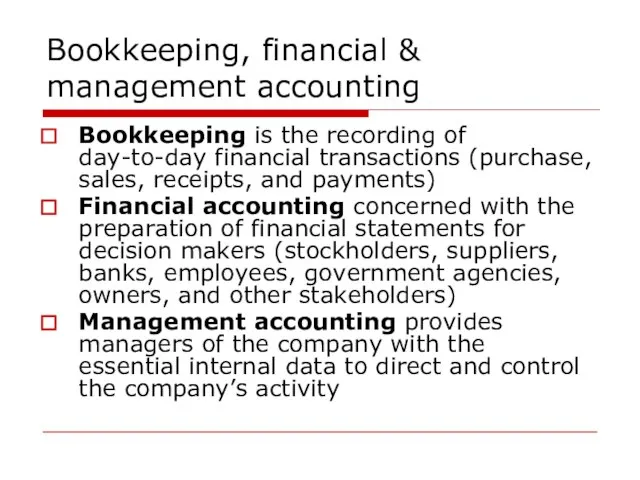

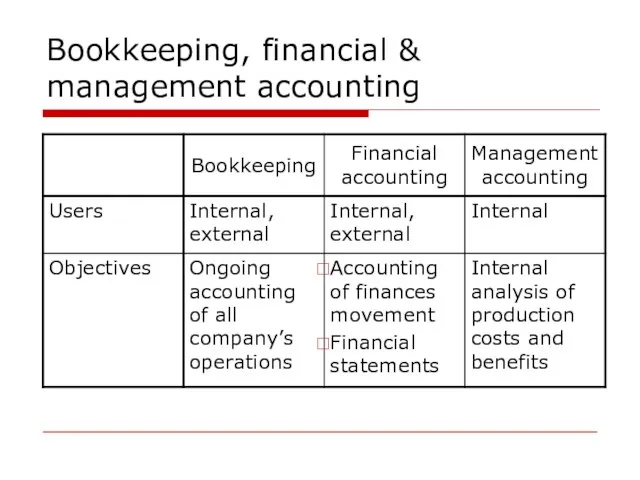

- 32. Bookkeeping, financial & management accounting Bookkeeping is the recording of day-to-day financial transactions (purchase, sales, receipts,

- 33. Bookkeeping, financial & management accounting

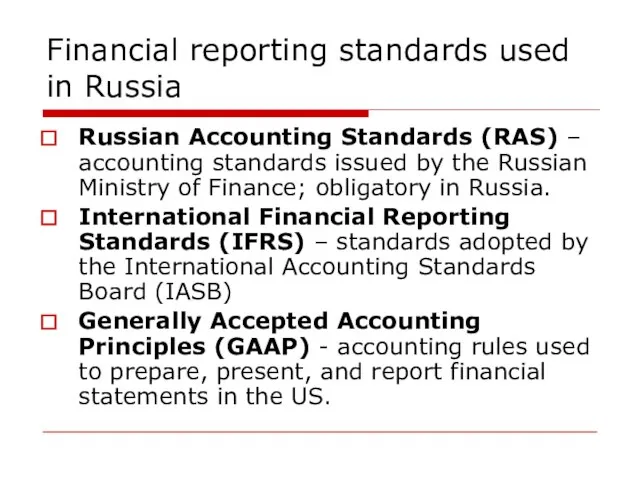

- 34. Financial reporting standards used in Russia Russian Accounting Standards (RAS) – accounting standards issued by the

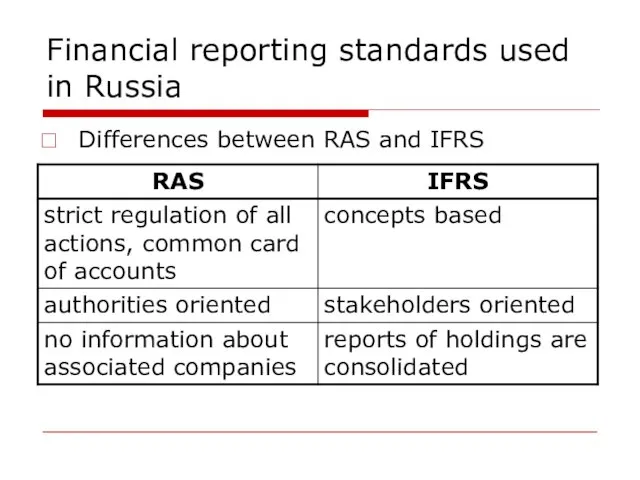

- 35. Financial reporting standards used in Russia Differences between RAS and IFRS

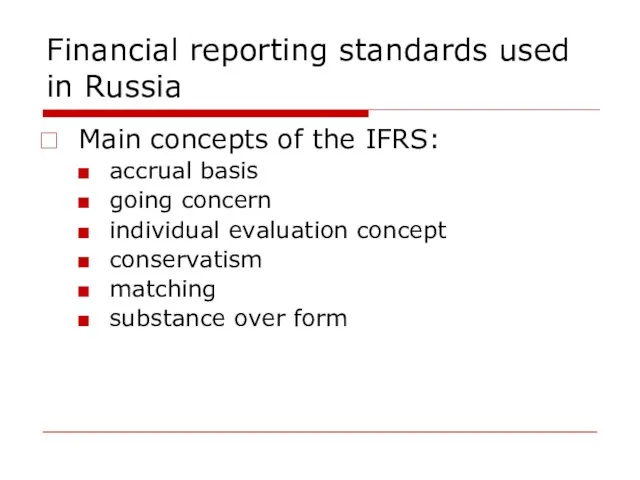

- 36. Financial reporting standards used in Russia Main concepts of the IFRS: accrual basis going concern individual

- 37. FINANCIAL STATEMENTS

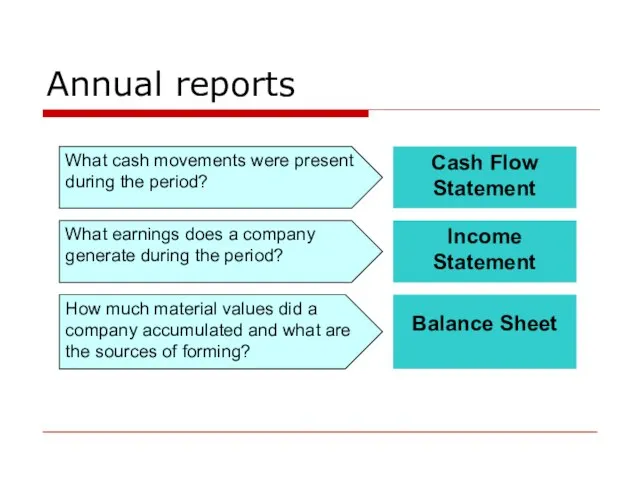

- 38. Annual reports

- 39. BALANCE SHEET

- 40. Loan capital Invested capital EQUITY & LIABILITIES? Where from? ASSETS What? Structure of assets & liabilities

- 41. Structure of assets & liabilities Balance equation Total Assets = Total Liabilities & Equity = FA

- 42. Structure of assets & liabilities Fixed assets: land plant & equipment transport long-term financial investments license

- 43. Structure of assets & liabilities Current assets: cash inventories work-in-process accounts receivable short-term financial investments pre-paid

- 44. Structure of assets & liabilities Equity: shareholders’ equity retained earnings additional capital reserves

- 45. Structure of assets & liabilities Loan capital: long-term liabilities (longer than 12 months) short-term liabilities loans

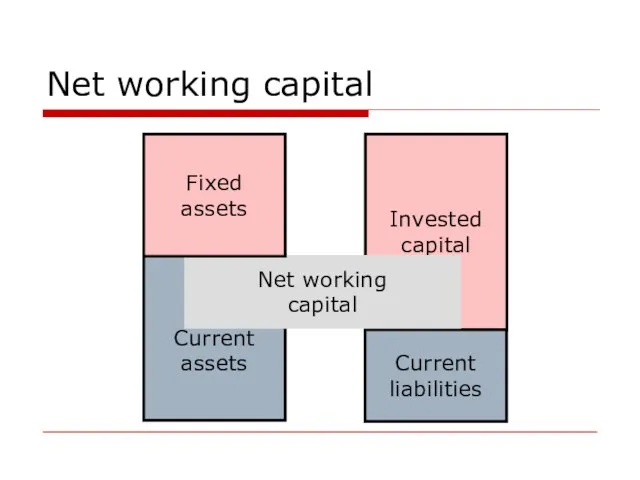

- 46. Net working capital Invested capital Current assets Current liabilities Net working capital Fixed assets

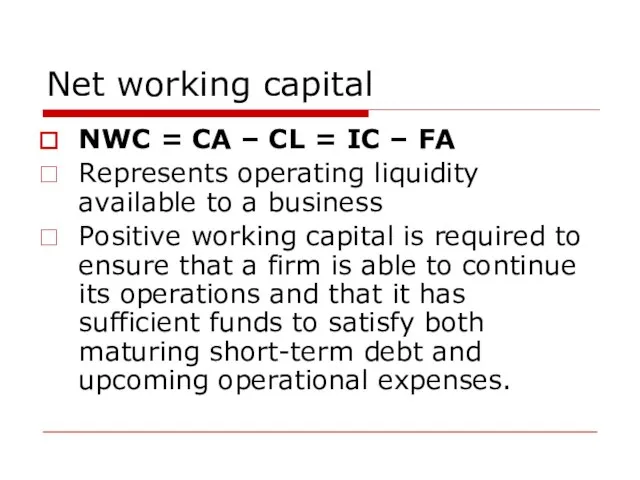

- 47. Net working capital NWC = CA – CL = IC – FA Represents operating liquidity available

- 48. INCOME STATEMENT

- 49. Income statement Receipts: Sales Interests Payments for services Rent … Disbursements: Cost of sales Salaries &

- 50. Income statement

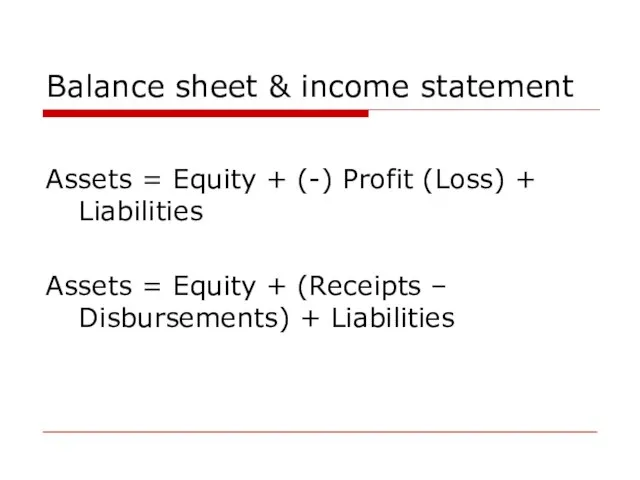

- 51. Balance sheet & income statement

- 52. Balance sheet & income statement Assets = Equity + (-) Profit (Loss) + Liabilities Assets =

- 53. STATEMENT OF CASH FLOWS

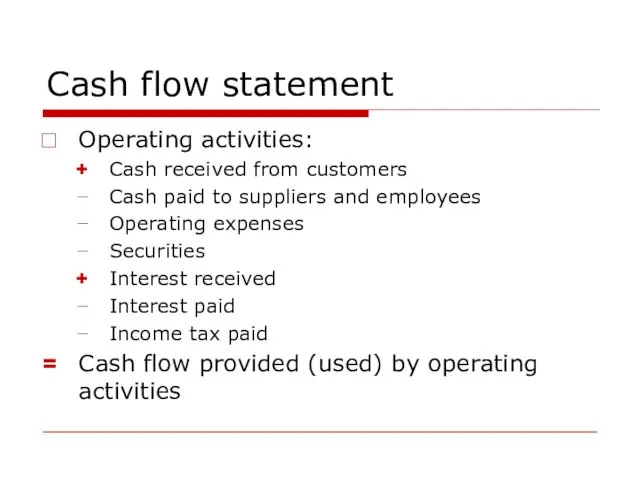

- 54. Cash flow statement Operating activities: Cash received from customers Cash paid to suppliers and employees Operating

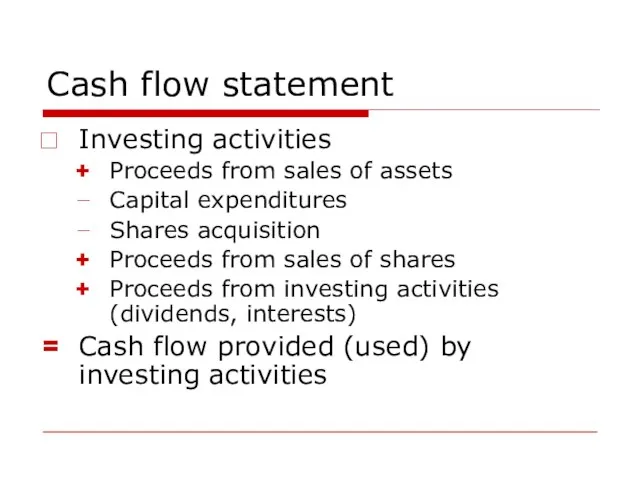

- 55. Cash flow statement Investing activities Proceeds from sales of assets Capital expenditures Shares acquisition Proceeds from

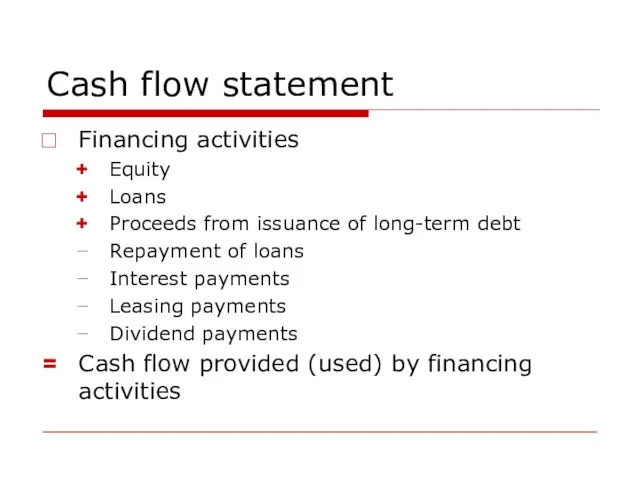

- 56. Cash flow statement Financing activities Equity Loans Proceeds from issuance of long-term debt Repayment of loans

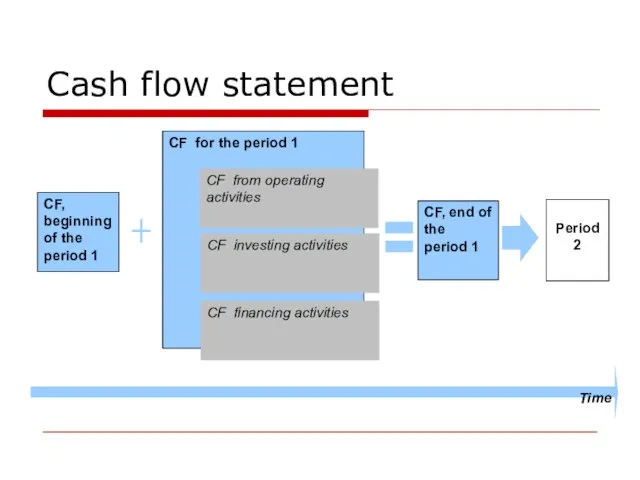

- 57. Cash flow statement

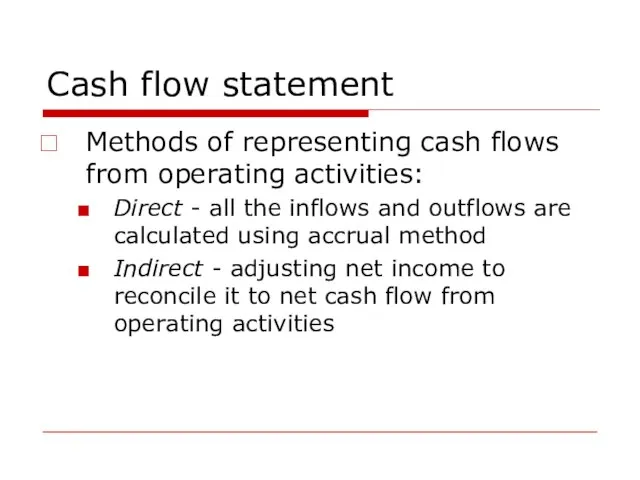

- 58. Cash flow statement Methods of representing cash flows from operating activities: Direct - all the inflows

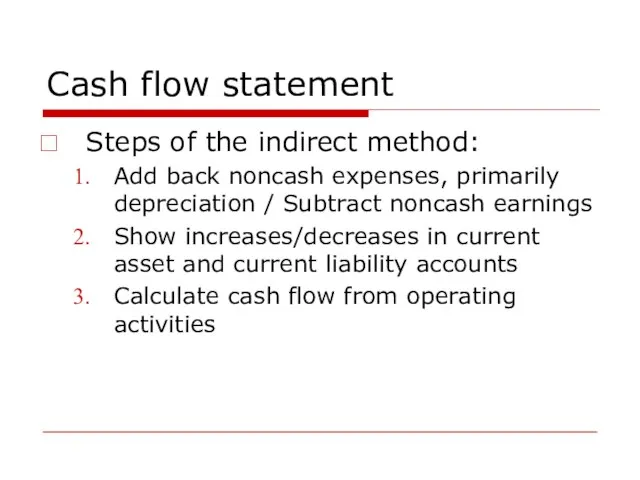

- 59. Cash flow statement Steps of the indirect method: Add back noncash expenses, primarily depreciation / Subtract

- 60. Cash flow statement Signs for adjustments (indirect method) ? Current assets ? Current liabilities Noncash earnings

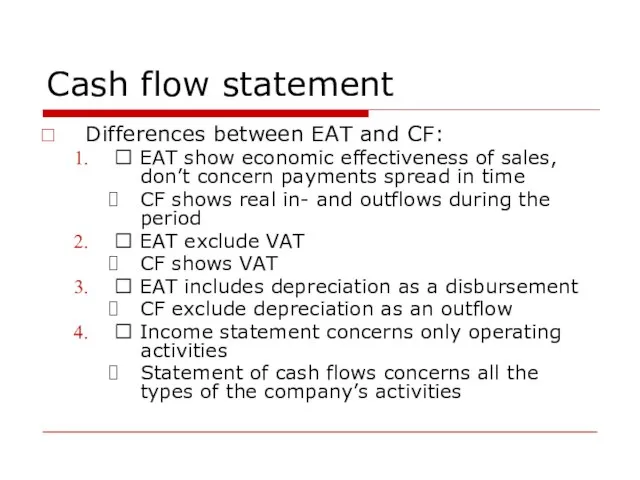

- 61. Cash flow statement Differences between EAT and CF: ? EAT show economic effectiveness of sales, don’t

- 62. FINANCIAL ANALYSIS

- 63. BASIC PRINCIPLES

- 64. Financial ratios A financial ratio is a relationship that indicates something about a firm’s activities and

- 65. Financial ratios Successful financial ratio analysis: Requires only representative sample of possible ratios A financial ratio

- 66. Financial ratios Advantages of financial ratios: Possible to compare companies and projects of different sizes Just

- 67. Financial ratios Disadvantages of financial ratios: Strongly depend on accuracy of reports Don’t analyze absolute values

- 68. Financial ratios Users of financial analysis results:

- 69. FIVE GROUPS OF FINANCIAL RAIOS

- 70. Financial ratios Five groups of financial ratios Profitability Liquidity Activity Financial leverage Market based

- 71. Liquidity ratios Liquidity ratios indicate a firm’s ability to meet short-term financial obligations. Current ratio=Current assets

- 72. Liquidity ratios Aging schedule

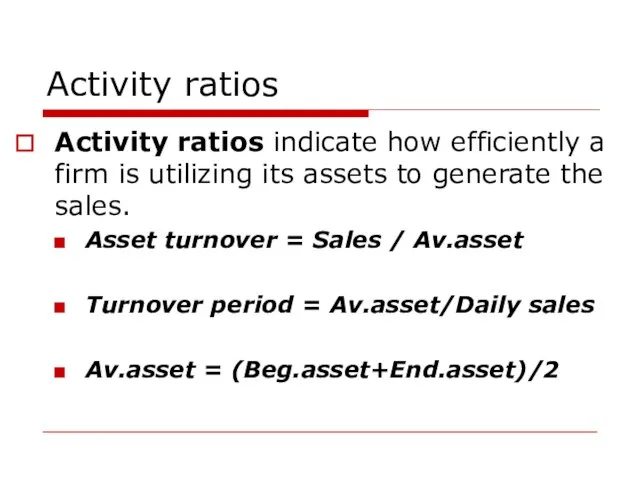

- 73. Activity ratios Activity ratios indicate how efficiently a firm is utilizing its assets to generate the

- 74. Activity ratios Average collection period = Accounts receivable/ (Annual credit sales/365) Inventory turnover = Costs of

- 75. Financial leverage ratios Financial leverage ratios measure the degree to which a firm is financing its

- 76. Financial leverage ratios Financial leverage rule: if the rate of return on equity exceed the cost

- 77. Profitability ratios Profitability ratios measure the total effectiveness of a company’s management in generating profits. Gross

- 78. Market-based ratios Market-based ratios measure the market’s (investor’s) assessment of the risk and performance of a

- 79. SOME METHODS OF FINANCIAL ANALYSIS

- 80. Methods of financial analysis Vertical analysis – structure analysis of a company’s statements Horizontal analysis –

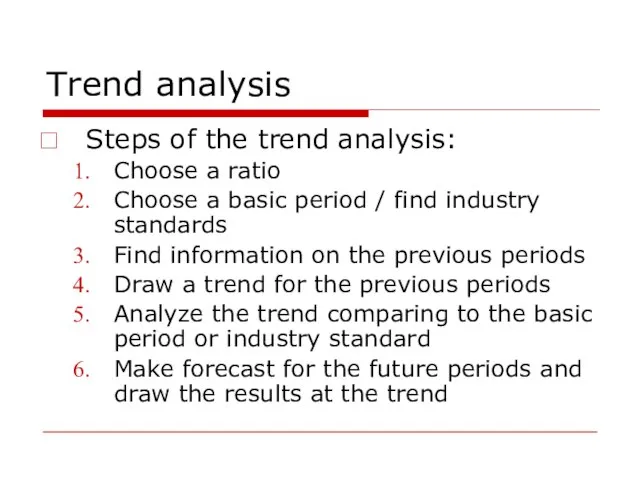

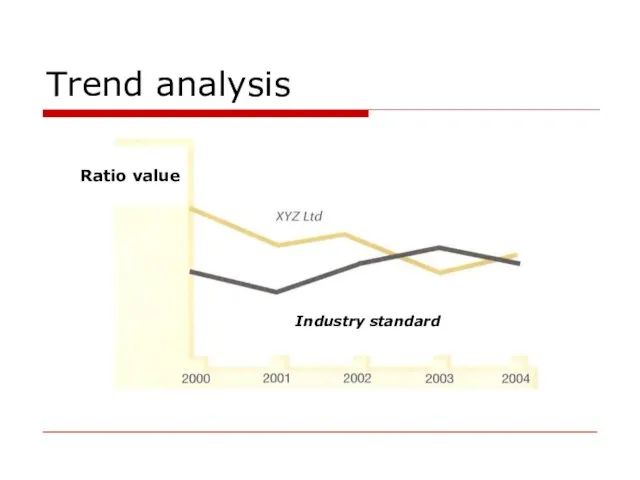

- 81. Trend analysis Steps of the trend analysis: Choose a ratio Choose a basic period / find

- 82. Trend analysis Ratio value Industry standard

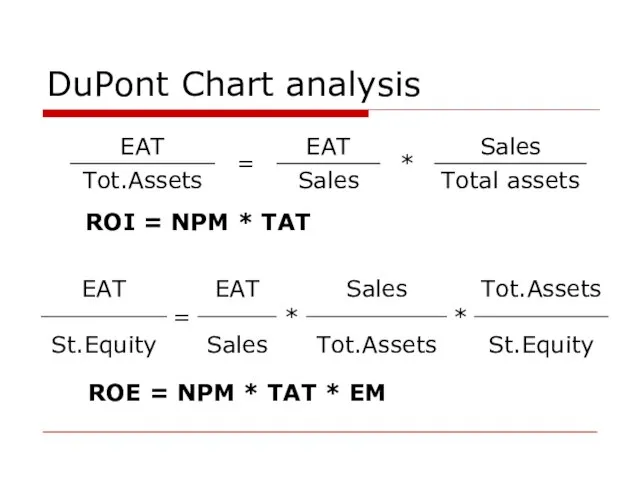

- 83. DuPont Chart analysis ROI = NPM * TAT ROE = NPM * TAT * EM

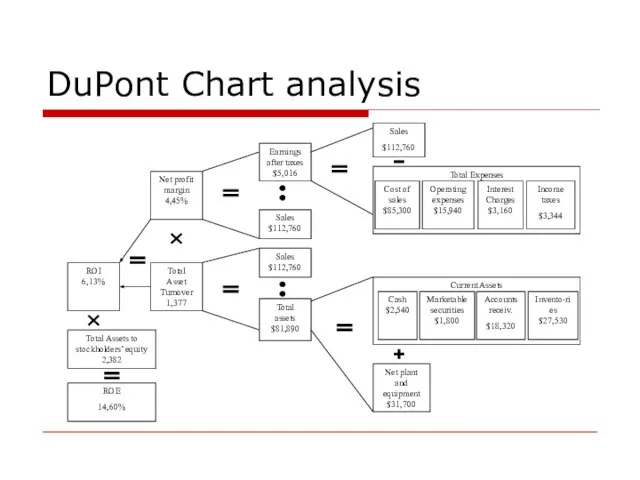

- 84. DuPont Chart analysis Net profit margin 4,45% Total Asset Turnover 1,377 Earnings after taxes $5,016 Sales

- 85. Factor analysis

- 86. Factor analysis

- 87. Z-analysis

- 88. CASH FLOW MANAGEMENT

- 89. NET CASH FLOW

- 90. Cash as a company’s working capital

- 91. Cash as a company’s working capital Cash volume depends on: Production phase Sales Collection of accounts

- 92. Cash as a company’s working capital Control of a cash rest Cash rest, RUR External limit

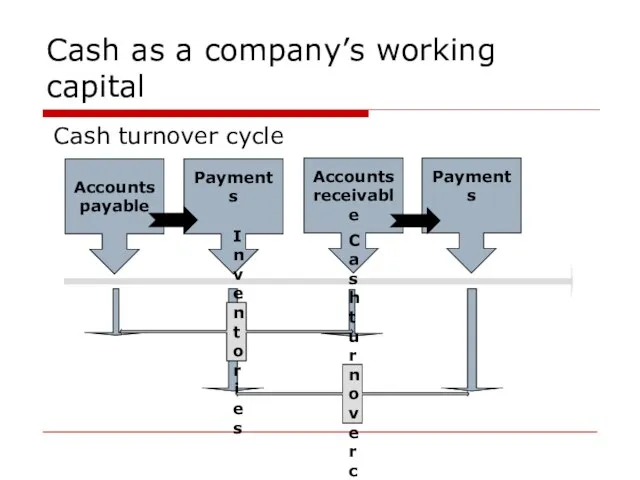

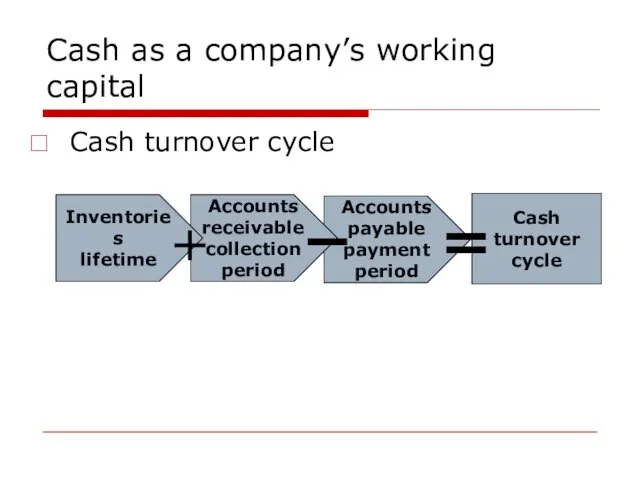

- 93. Cash as a company’s working capital Cash turnover cycle

- 94. Accounts payable payment period Accounts receivable collection period Cash as a company’s working capital Cash turnover

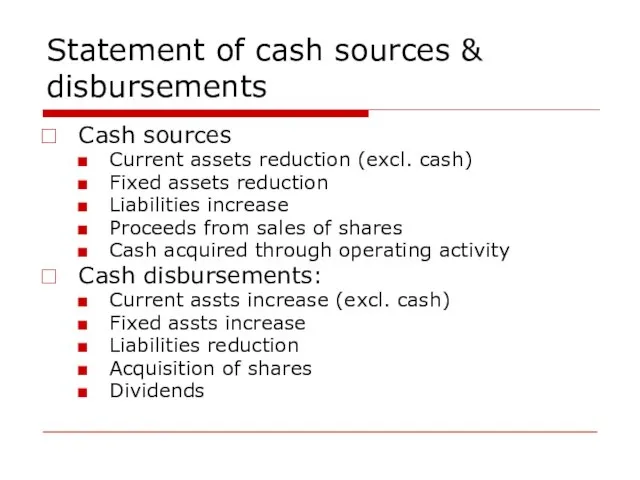

- 95. Statement of cash sources & disbursements Cash sources Current assets reduction (excl. cash) Fixed assets reduction

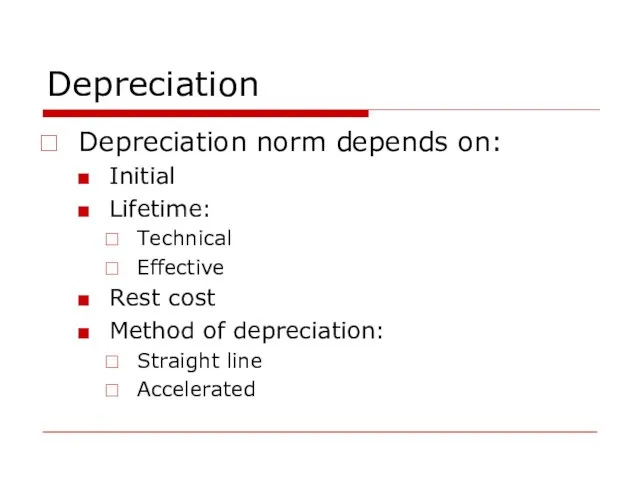

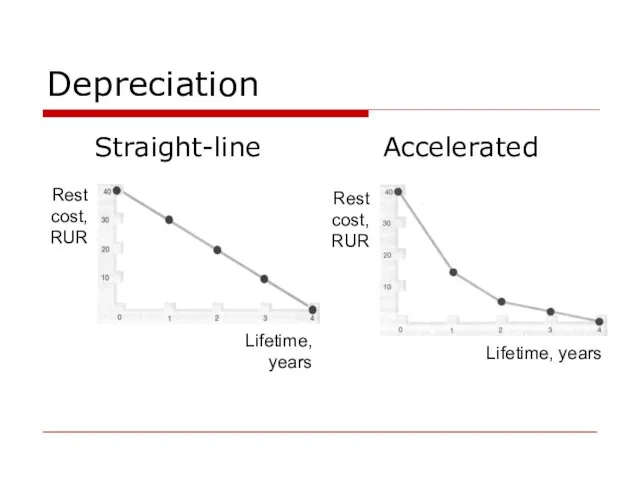

- 96. Depreciation Depreciation norm depends on: Initial Lifetime: Technical Effective Rest cost Method of depreciation: Straight line

- 97. Depreciation Straight-line Accelerated

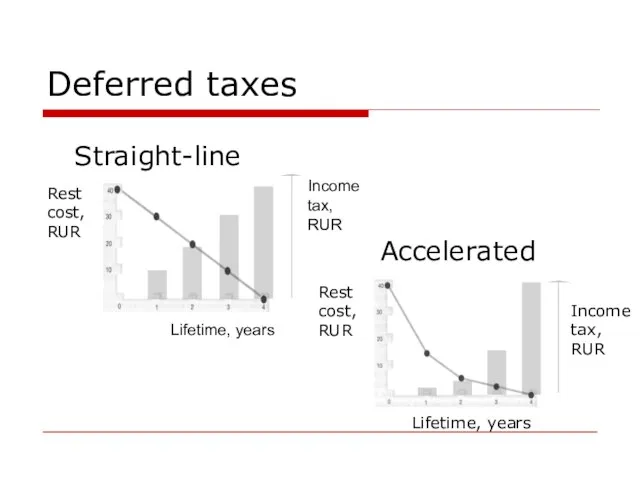

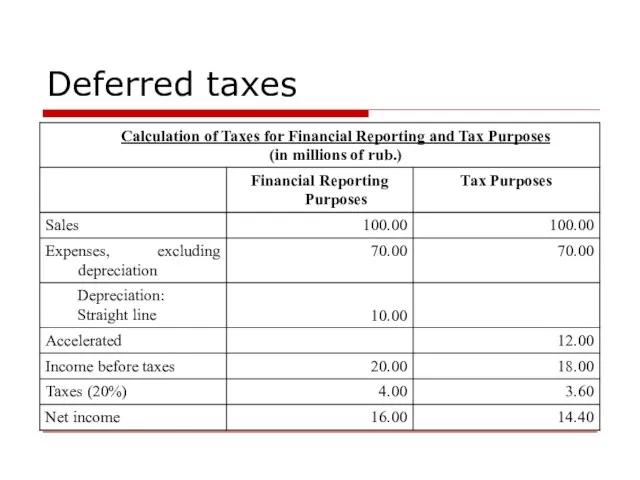

- 98. Deferred taxes Straight-line Accelerated

- 99. Deferred taxes

- 100. CASH FLOW FORECASTING

- 101. Forecasting of financial statements 5 steps: Define basic data for forecasting: external income tax rate interest

- 102. Forecasting of financial statements internal: investments policy external financing policy accounting policy dividend policy planned profitability

- 103. Forecasting of financial statements Forecast the volume of sales bottom-up forecasting statistics analysis marketing analysis Forecast

- 104. Forecasting of financial statements Analysis of pro forma financial statements Cash flows Additional financing & sources

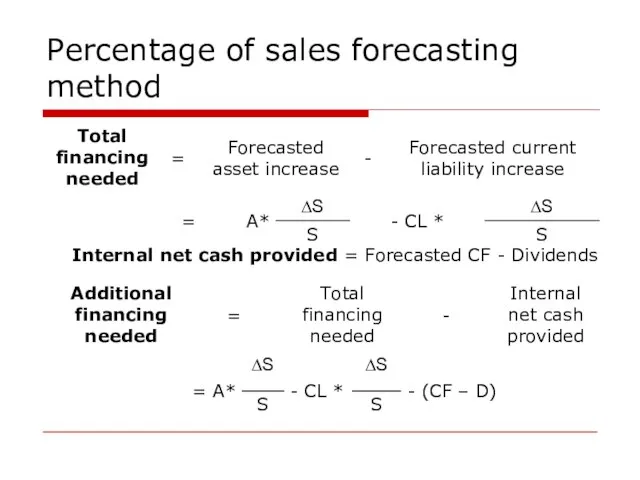

- 105. Percentage of sales forecasting method The percentage of sales forecasting method: permits a company to forecast

- 106. Percentage of sales forecasting method Internal net cash provided = Forecasted CF - Dividends

- 107. Percentage of sales forecasting method To support the sales increase the management of the company has

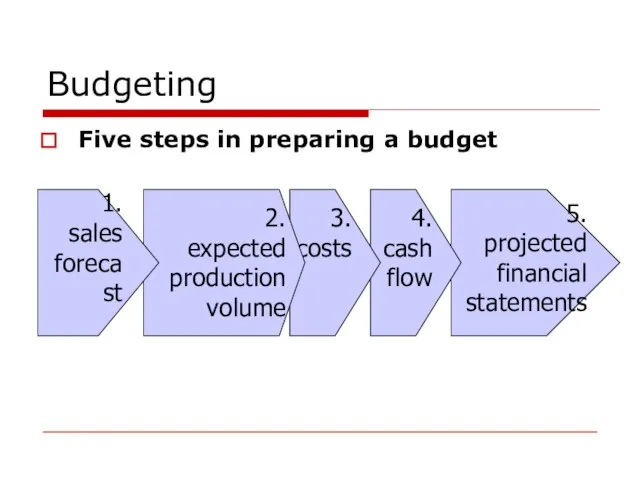

- 108. Budgeting Five steps in preparing a budget

- 109. COSTS PLANNING

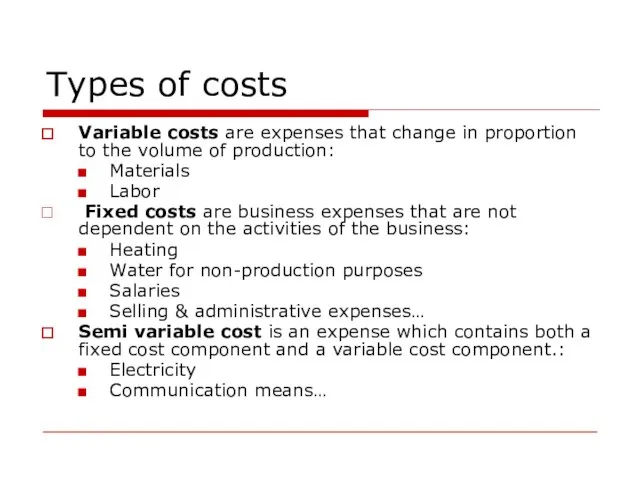

- 110. Types of costs Variable costs are expenses that change in proportion to the volume of production:

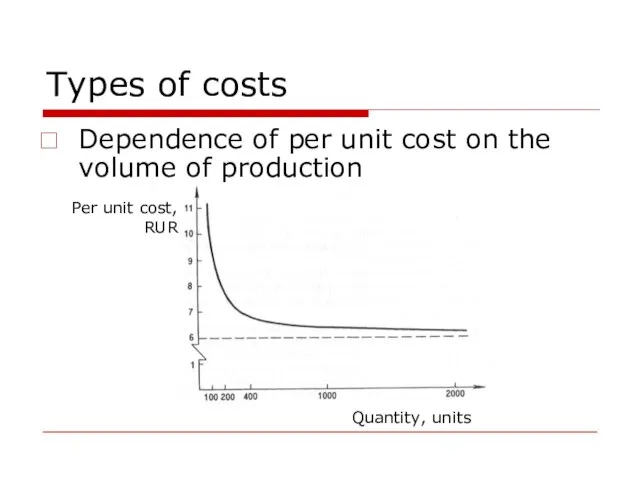

- 111. Types of costs Dependence of per unit cost on the volume of production Per unit cost,

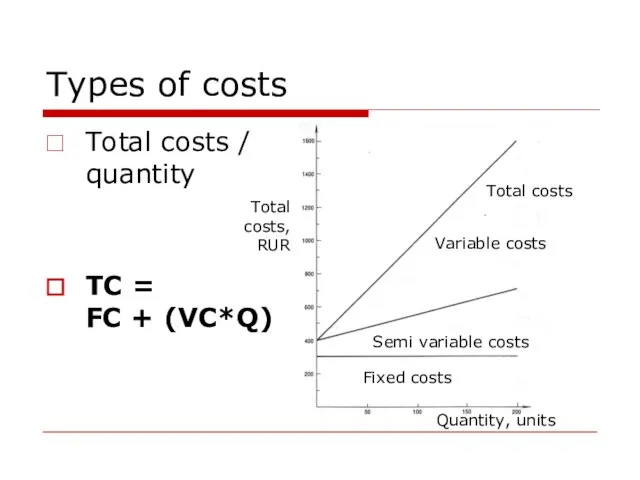

- 112. Types of costs Total costs / quantity TC = FC + (VC*Q) Total costs, RUR Quantity,

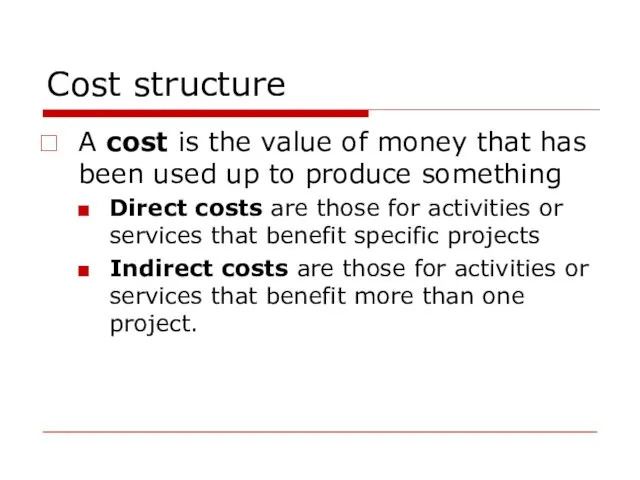

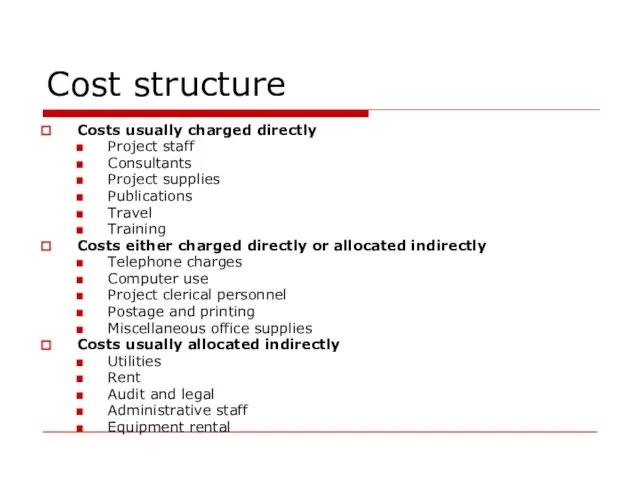

- 113. Cost structure A cost is the value of money that has been used up to produce

- 114. Cost structure Costs usually charged directly Project staff Consultants Project supplies Publications Travel Training Costs either

- 116. Скачать презентацию

Слайд 3FINANCIAL MODEL OF A COMPANY

FINANCIAL MODEL OF A COMPANY

Слайд 4Objectives of a company

Shareholders’ wealth maximization

Objectives of a company

Shareholders’ wealth maximization

Слайд 5Objectives of a company

Stakeholders’ income increase:

Shareholders

Employees

Managers

Suppliers

Clients

Society

Objectives of a company

Stakeholders’ income increase:

Shareholders

Employees

Managers

Suppliers

Clients

Society

Слайд 6Functions of a financial manager

Activity spheres of a financial manager:

Strategic management –

Functions of a financial manager

Activity spheres of a financial manager:

Strategic management –

Слайд 7Functions of a financial manager

Functions of a financial manager

Слайд 8Functions of a financial manager

Key objectives of a financial manager

Financial planning

Assessment of

Functions of a financial manager

Key objectives of a financial manager

Financial planning

Assessment of

Слайд 9Financial structure of the company

Financial structure is a hierarchical system of financial

Financial structure of the company

Financial structure is a hierarchical system of financial

Слайд 10Financial structure of the company

Financial responsibility centers (FRC):

Cost center (CC)

Revenue center (RC)

Marginal

Financial structure of the company

Financial responsibility centers (FRC):

Cost center (CC)

Revenue center (RC)

Marginal

Слайд 11Financial structure of the company

Financial structure of the company

Слайд 12Financial structure of the company

How to from a financial structure:

Organizational approach

Process approach

Define

Financial structure of the company

How to from a financial structure:

Organizational approach

Process approach

Define

Слайд 13Organizational approach

An organizational structure is a mainly hierarchical concept of subordination of

Organizational approach

An organizational structure is a mainly hierarchical concept of subordination of

Слайд 14Organizational approach

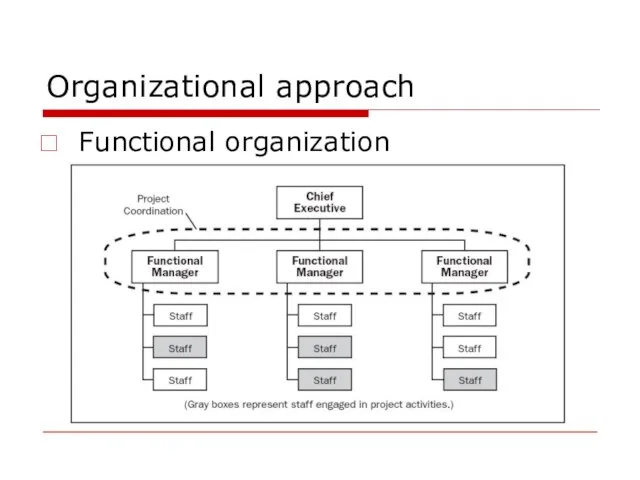

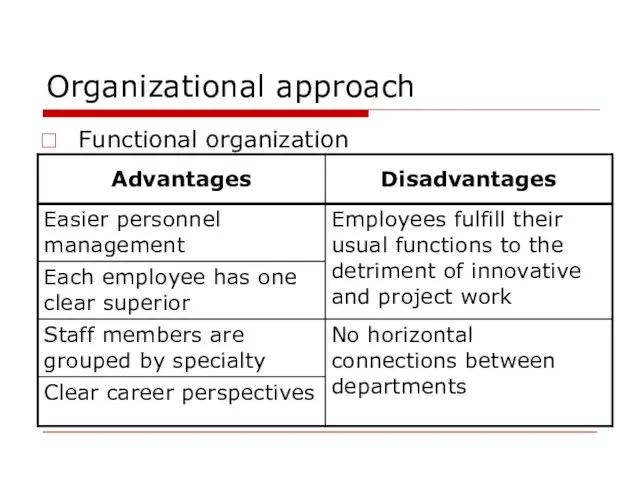

Functional organization

Organizational approach

Functional organization

Слайд 15Organizational approach

Functional organization

Organizational approach

Functional organization

Слайд 16Organizational approach

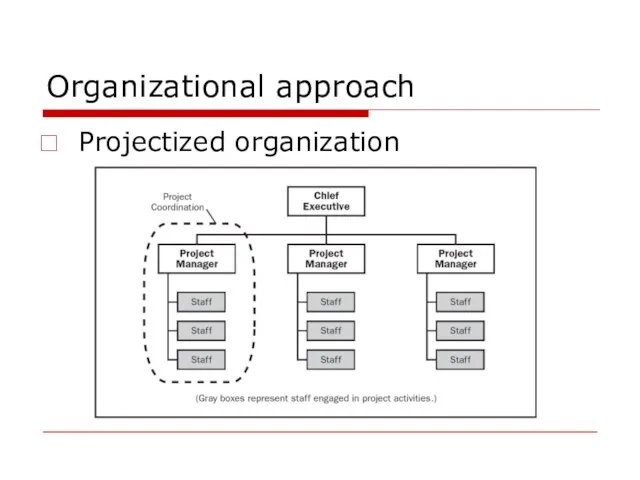

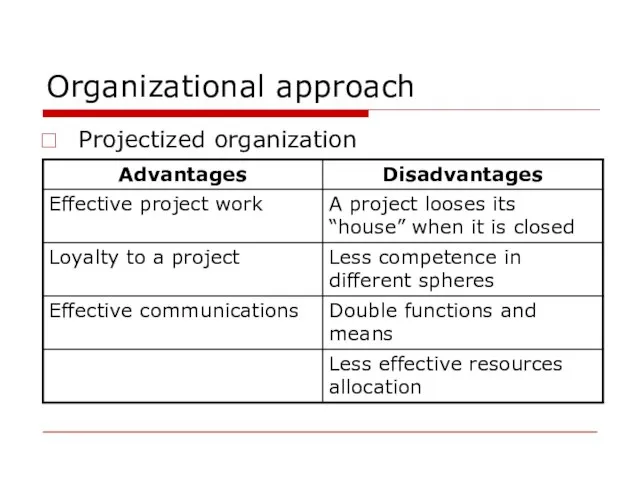

Projectized organization

Organizational approach

Projectized organization

Слайд 17Organizational approach

Projectized organization

Organizational approach

Projectized organization

Слайд 18Organizational approach

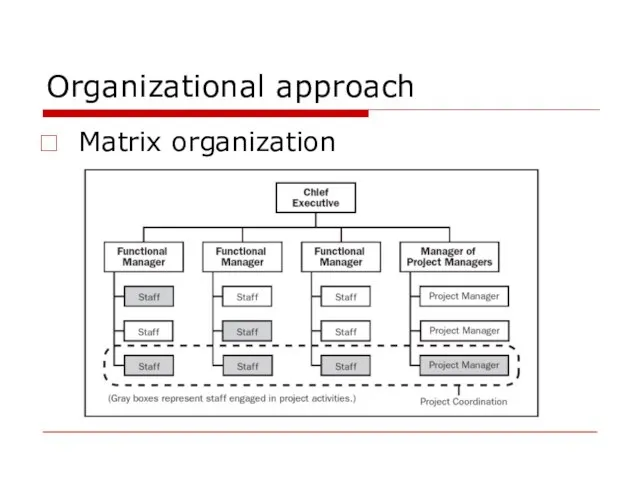

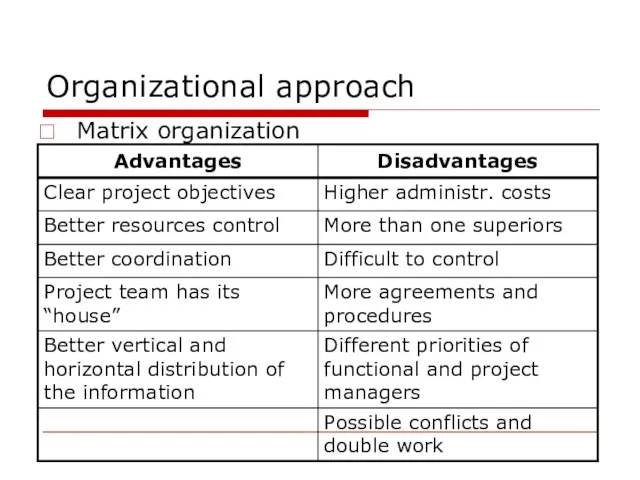

Matrix organization

Organizational approach

Matrix organization

Слайд 19Organizational approach

Matrix organization

Organizational approach

Matrix organization

Слайд 20Organizational approach

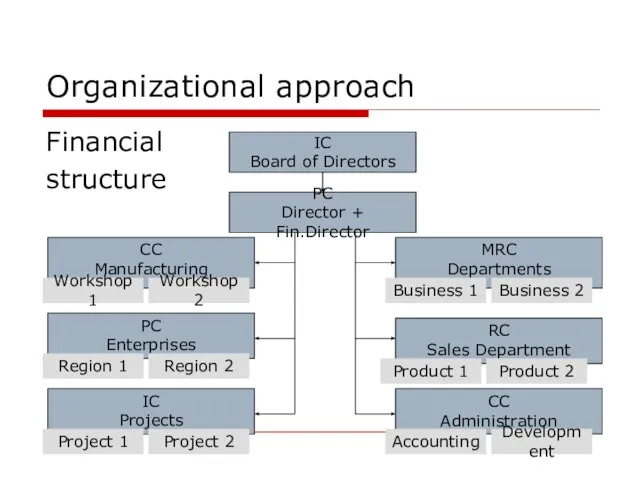

Financial

structure

PC

Director + Fin.Director

CC

Manufacturing

Workshop 1

Workshop 2

PC

Enterprises

Region 1

Region 2

MRC

Departments

Business 1

Business 2

RC

Sales Department

CC

Administration

Accounting

Development

IC

Projects

Project

Organizational approach

Financial

structure

PC

Director + Fin.Director

CC

Manufacturing

Workshop 1

Workshop 2

PC

Enterprises

Region 1

Region 2

MRC

Departments

Business 1

Business 2

RC

Sales Department

CC

Administration

Accounting

Development

IC

Projects

Project

Слайд 21Organizational approach

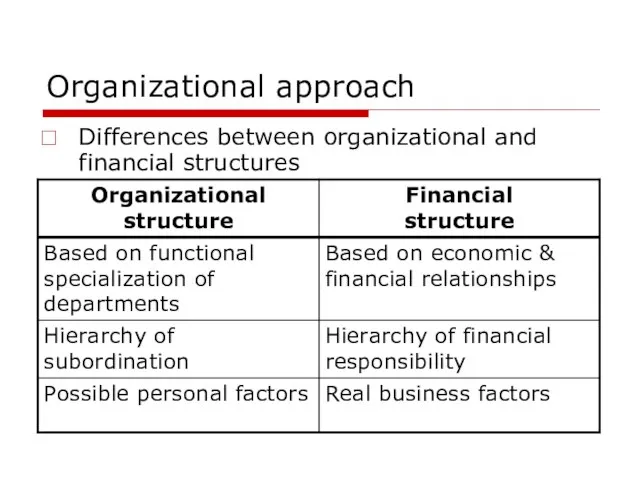

Differences between organizational and financial structures

Organizational approach

Differences between organizational and financial structures

Слайд 22Process approach

A process is an activity which transforms input into output.

A business

Process approach

A process is an activity which transforms input into output.

A business

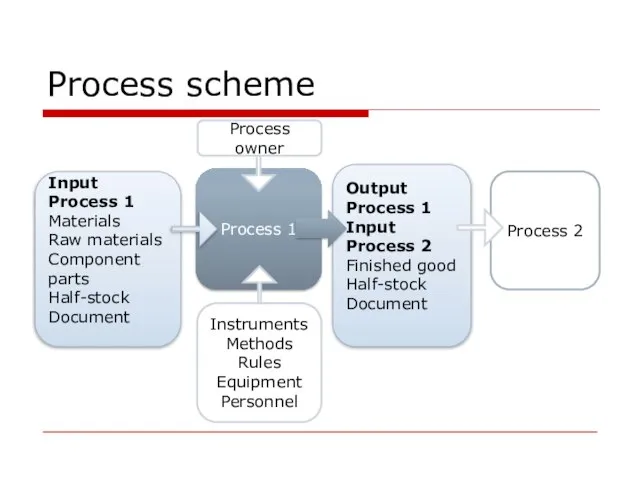

Слайд 23Process scheme

Process scheme

Слайд 24Process approach

Business-process types:

Main

Supporting

Development

Corporate management

Process approach

Business-process types:

Main

Supporting

Development

Corporate management

Слайд 25Process approach

Process decomposition

Process 1

Process 2

Process 3

Process 2.1

Process 2.2

Process 2.3

Process 2.3.1

Recording

Process 2.3.2

Recording

Process 2.3.3

Recording

A0

Process approach

Process decomposition

Process 1

Process 2

Process 3

Process 2.1

Process 2.2

Process 2.3

Process 2.3.1

Recording

Process 2.3.2

Recording

Process 2.3.3

Recording

A0

Слайд 26Process approach

Business process and budgets

P&L

Balance

CF

Financial budgets

Operational budgets

Business-processes

Process approach

Business process and budgets

P&L

Balance

CF

Financial budgets

Operational budgets

Business-processes

Слайд 27BASIC PRINCIPLES OF FINANCIAL MANAGEMENT

BASIC PRINCIPLES OF FINANCIAL MANAGEMENT

Слайд 28Concept of cash flows

Cash turnover concept

Concept of cash flows

Cash turnover concept

Слайд 29Concept of cash flows

Cash flow - the movement of cash into or

Concept of cash flows

Cash flow - the movement of cash into or

Слайд 30Relationship between risk & profit

Nothing ventured, nothing gained

Britain’s Special Air Service

Relationship between risk & profit

Nothing ventured, nothing gained

Britain’s Special Air Service

Слайд 31ACCOUNTING SYSTEMS

ACCOUNTING SYSTEMS

Слайд 32Bookkeeping, financial & management accounting

Bookkeeping is the recording of day-to-day financial transactions

Bookkeeping, financial & management accounting

Bookkeeping is the recording of day-to-day financial transactions

Слайд 33Bookkeeping, financial & management accounting

Bookkeeping, financial & management accounting

Слайд 34Financial reporting standards used in Russia

Russian Accounting Standards (RAS) – accounting standards

Financial reporting standards used in Russia

Russian Accounting Standards (RAS) – accounting standards

Слайд 35Financial reporting standards used in Russia

Differences between RAS and IFRS

Financial reporting standards used in Russia

Differences between RAS and IFRS

Слайд 36Financial reporting standards used in Russia

Main concepts of the IFRS:

accrual basis

going

Financial reporting standards used in Russia

Main concepts of the IFRS:

accrual basis

going

Слайд 37FINANCIAL STATEMENTS

FINANCIAL STATEMENTS

Слайд 38Annual reports

Annual reports

Слайд 39BALANCE SHEET

BALANCE SHEET

Слайд 40Loan

capital

Invested

capital

EQUITY &

LIABILITIES?

Where from?

ASSETS

What?

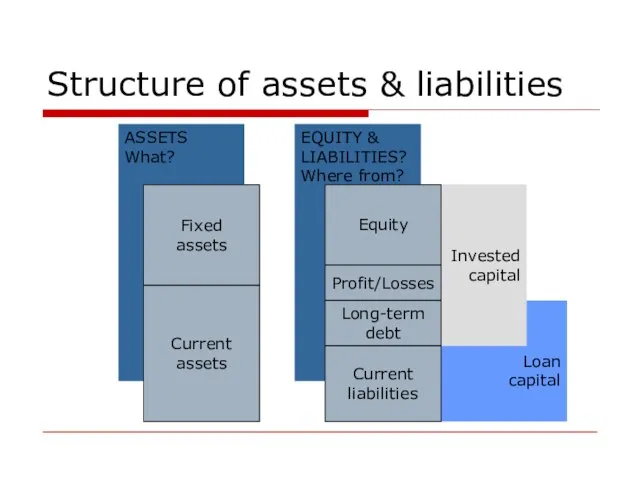

Structure of assets & liabilities

Fixed

assets

Current

assets

Equity

Profit/Losses

Long-term

debt

Current

liabilities

Invested

capital

EQUITY &

LIABILITIES?

Where from?

ASSETS

What?

Structure of assets & liabilities

Fixed

assets

Current

assets

Equity

Profit/Losses

Long-term

debt

Current

liabilities

Слайд 41Structure of assets & liabilities

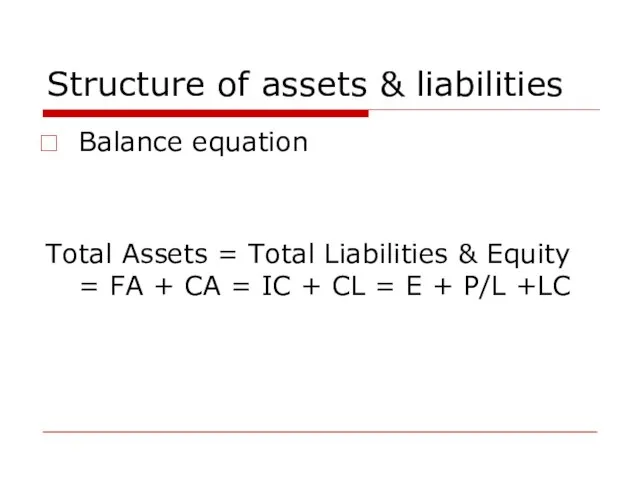

Balance equation

Total Assets = Total Liabilities & Equity

Structure of assets & liabilities

Balance equation

Total Assets = Total Liabilities & Equity

Слайд 42Structure of assets & liabilities

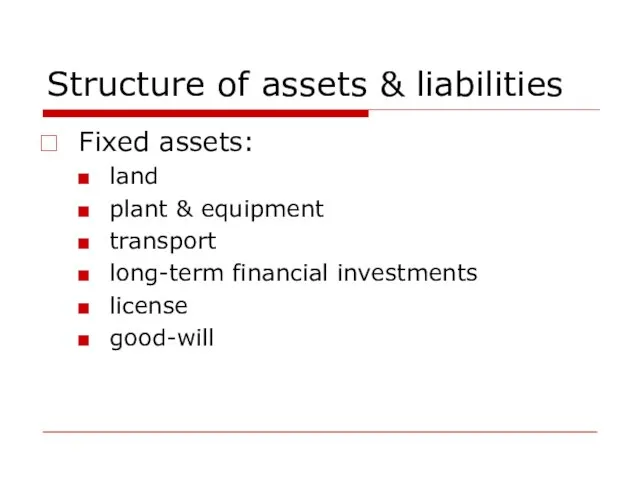

Fixed assets:

land

plant & equipment

transport

long-term financial investments

license

good-will

Structure of assets & liabilities

Fixed assets:

land

plant & equipment

transport

long-term financial investments

license

good-will

Слайд 43Structure of assets & liabilities

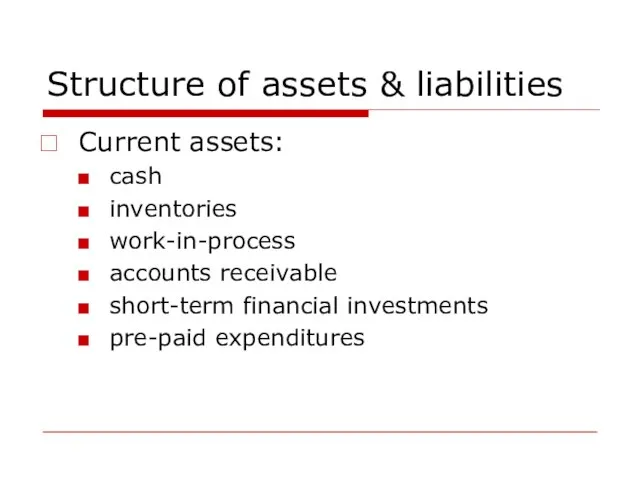

Current assets:

cash

inventories

work-in-process

accounts receivable

short-term financial investments

pre-paid expenditures

Structure of assets & liabilities

Current assets:

cash

inventories

work-in-process

accounts receivable

short-term financial investments

pre-paid expenditures

Слайд 44Structure of assets & liabilities

Equity:

shareholders’ equity

retained earnings

additional capital

reserves

Structure of assets & liabilities

Equity:

shareholders’ equity

retained earnings

additional capital

reserves

Слайд 45Structure of assets & liabilities

Loan capital:

long-term liabilities (longer than 12 months)

short-term liabilities

loans

Structure of assets & liabilities

Loan capital:

long-term liabilities (longer than 12 months)

short-term liabilities

loans

Слайд 46Net working capital

Invested

capital

Current

assets

Current

liabilities

Net working

capital

Fixed

assets

Net working capital

Invested

capital

Current

assets

Current

liabilities

Net working

capital

Fixed

assets

Слайд 47Net working capital

NWC = CA – CL = IC – FA

Represents operating

Net working capital

NWC = CA – CL = IC – FA

Represents operating

Слайд 48INCOME STATEMENT

INCOME STATEMENT

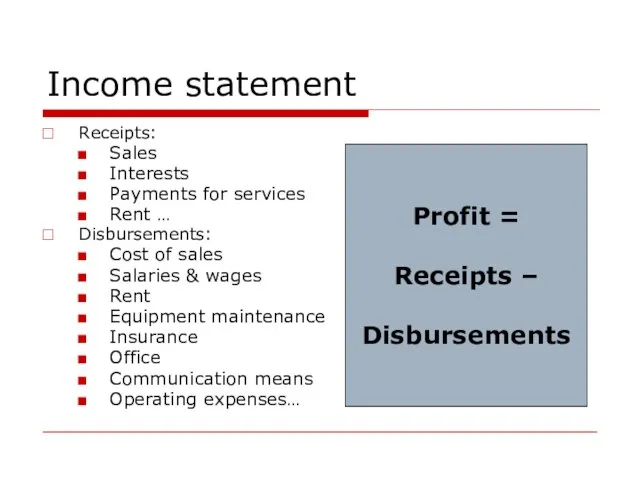

Слайд 49Income statement

Receipts:

Sales

Interests

Payments for services

Rent …

Disbursements:

Cost of sales

Salaries & wages

Rent

Equipment maintenance

Insurance

Office

Communication means

Operating expenses…

Profit

Income statement

Receipts:

Sales

Interests

Payments for services

Rent …

Disbursements:

Cost of sales

Salaries & wages

Rent

Equipment maintenance

Insurance

Office

Communication means

Operating expenses…

Profit

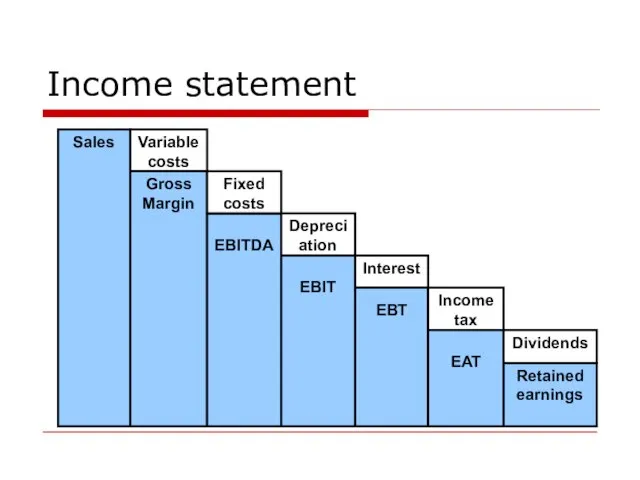

Слайд 50Income statement

Income statement

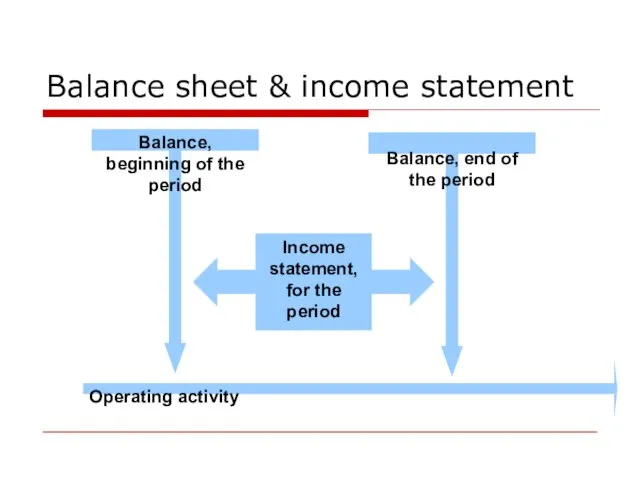

Слайд 51Balance sheet & income statement

Balance sheet & income statement

Слайд 52Balance sheet & income statement

Assets = Equity + (-) Profit (Loss) +

Balance sheet & income statement

Assets = Equity + (-) Profit (Loss) +

Слайд 53STATEMENT OF CASH FLOWS

STATEMENT OF CASH FLOWS

Слайд 54Cash flow statement

Operating activities:

Cash received from customers

Cash paid to suppliers and employees

Cash flow statement

Operating activities:

Cash received from customers

Cash paid to suppliers and employees

Слайд 55Cash flow statement

Investing activities

Proceeds from sales of assets

Capital expenditures

Shares acquisition

Proceeds from sales

Cash flow statement

Investing activities

Proceeds from sales of assets

Capital expenditures

Shares acquisition

Proceeds from sales

Слайд 56Cash flow statement

Financing activities

Equity

Loans

Proceeds from issuance of long-term debt

Repayment of loans

Interest

Cash flow statement

Financing activities

Equity

Loans

Proceeds from issuance of long-term debt

Repayment of loans

Interest

Слайд 57Cash flow statement

Cash flow statement

Слайд 58Cash flow statement

Methods of representing cash flows from operating activities:

Direct -

Cash flow statement

Methods of representing cash flows from operating activities:

Direct -

Слайд 59Cash flow statement

Steps of the indirect method:

Add back noncash expenses, primarily depreciation

Cash flow statement

Steps of the indirect method:

Add back noncash expenses, primarily depreciation

Слайд 60Cash flow statement

Signs for adjustments (indirect method)

? Current assets

? Current liabilities

Noncash earnings

?

Cash flow statement

Signs for adjustments (indirect method)

? Current assets

? Current liabilities

Noncash earnings

?

Слайд 61Cash flow statement

Differences between EAT and CF:

? EAT show economic effectiveness of

Cash flow statement

Differences between EAT and CF:

? EAT show economic effectiveness of

Слайд 62FINANCIAL ANALYSIS

FINANCIAL ANALYSIS

Слайд 63BASIC PRINCIPLES

BASIC PRINCIPLES

Слайд 64Financial ratios

A financial ratio is a relationship that indicates something about a

Financial ratios

A financial ratio is a relationship that indicates something about a

Слайд 65Financial ratios

Successful financial ratio analysis:

Requires only representative sample of possible ratios

A financial

Financial ratios

Successful financial ratio analysis:

Requires only representative sample of possible ratios

A financial

Слайд 66Financial ratios

Advantages of financial ratios:

Possible to compare companies and projects of different

Financial ratios

Advantages of financial ratios:

Possible to compare companies and projects of different

Слайд 67Financial ratios

Disadvantages of financial ratios:

Strongly depend on accuracy of reports

Don’t analyze absolute

Financial ratios

Disadvantages of financial ratios:

Strongly depend on accuracy of reports

Don’t analyze absolute

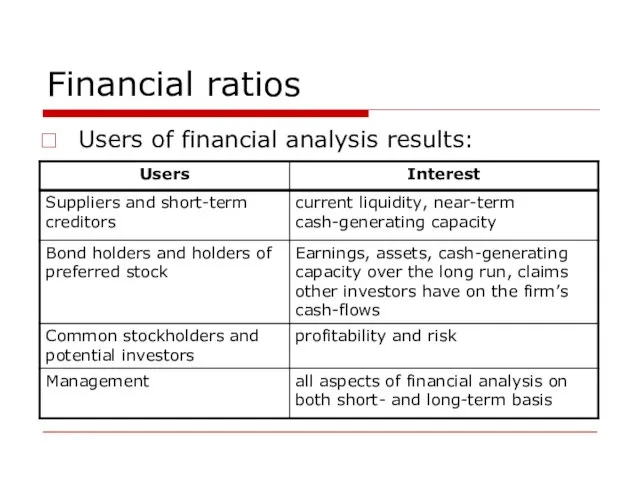

Слайд 68Financial ratios

Users of financial analysis results:

Financial ratios

Users of financial analysis results:

Слайд 69FIVE GROUPS OF FINANCIAL RAIOS

FIVE GROUPS OF FINANCIAL RAIOS

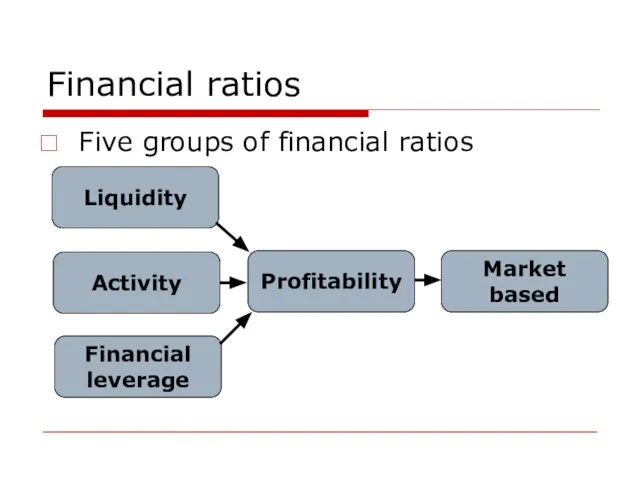

Слайд 70Financial ratios

Five groups of financial ratios

Profitability

Liquidity

Activity

Financial

leverage

Market

based

Financial ratios

Five groups of financial ratios

Profitability

Liquidity

Activity

Financial

leverage

Market

based

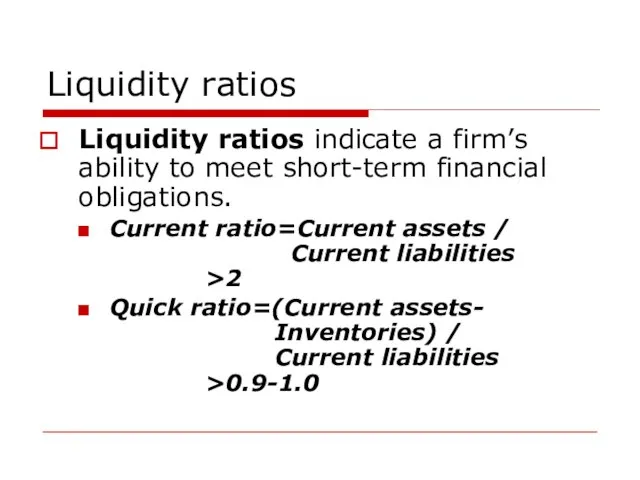

Слайд 71Liquidity ratios

Liquidity ratios indicate a firm’s ability to meet short-term financial obligations.

Current

Liquidity ratios

Liquidity ratios indicate a firm’s ability to meet short-term financial obligations.

Current

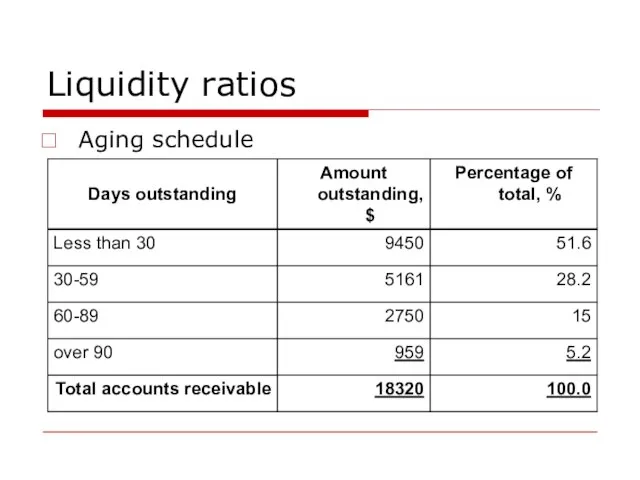

Слайд 72Liquidity ratios

Aging schedule

Liquidity ratios

Aging schedule

Слайд 73Activity ratios

Activity ratios indicate how efficiently a firm is utilizing its assets

Activity ratios

Activity ratios indicate how efficiently a firm is utilizing its assets

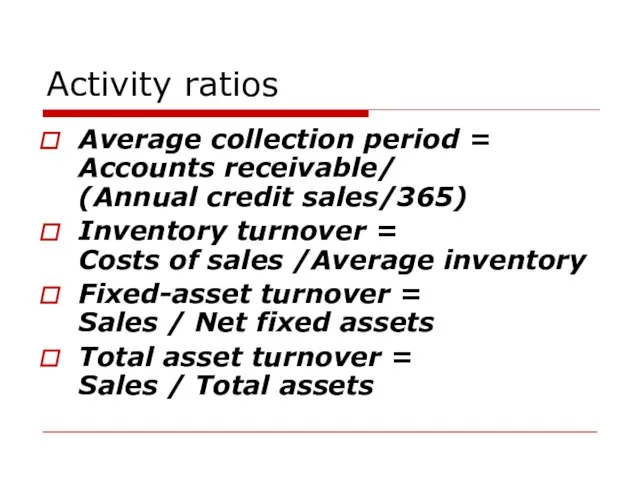

Слайд 74Activity ratios

Average collection period = Accounts receivable/

(Annual credit sales/365)

Inventory turnover =

Costs

Activity ratios

Average collection period = Accounts receivable/

(Annual credit sales/365)

Inventory turnover =

Costs

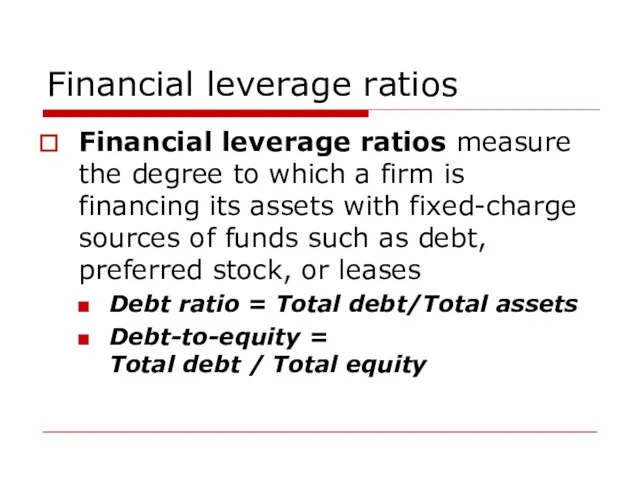

Слайд 75Financial leverage ratios

Financial leverage ratios measure the degree to which a firm

Financial leverage ratios

Financial leverage ratios measure the degree to which a firm

Слайд 76Financial leverage ratios

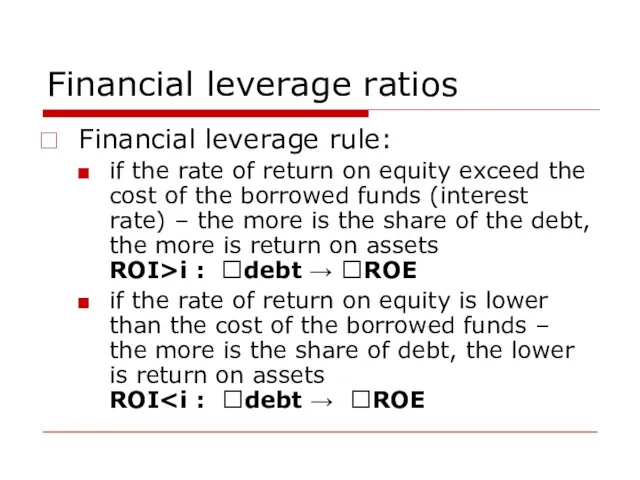

Financial leverage rule:

if the rate of return on equity exceed

Financial leverage ratios

Financial leverage rule:

if the rate of return on equity exceed

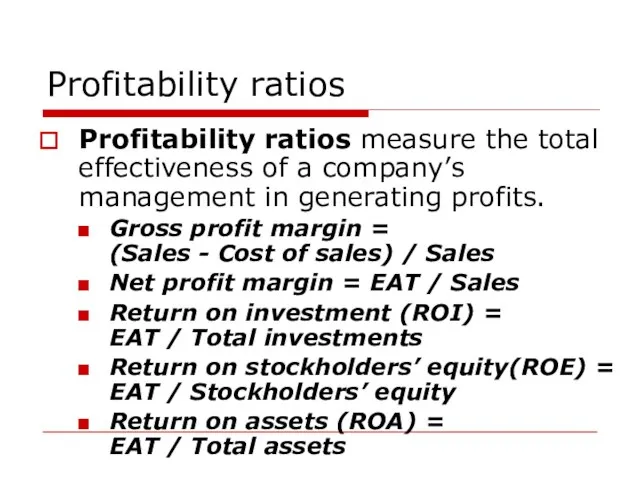

Слайд 77Profitability ratios

Profitability ratios measure the total effectiveness of a company’s management in

Profitability ratios

Profitability ratios measure the total effectiveness of a company’s management in

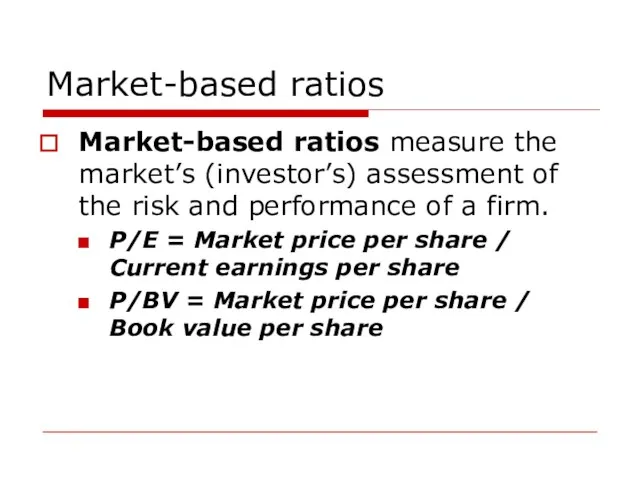

Слайд 78Market-based ratios

Market-based ratios measure the market’s (investor’s) assessment of the risk and

Market-based ratios

Market-based ratios measure the market’s (investor’s) assessment of the risk and

Слайд 79SOME METHODS OF FINANCIAL ANALYSIS

SOME METHODS OF FINANCIAL ANALYSIS

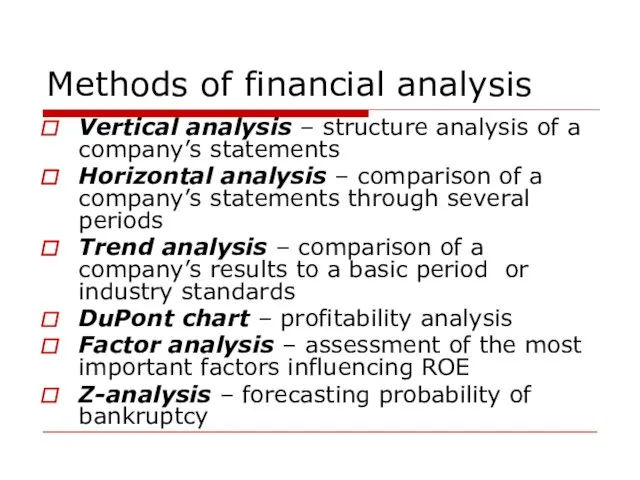

Слайд 80Methods of financial analysis

Vertical analysis – structure analysis of a company’s statements

Horizontal

Methods of financial analysis

Vertical analysis – structure analysis of a company’s statements

Horizontal

Слайд 81Trend analysis

Steps of the trend analysis:

Choose a ratio

Choose a basic period /

Trend analysis

Steps of the trend analysis:

Choose a ratio

Choose a basic period /

Слайд 82Trend analysis

Ratio value

Industry standard

Trend analysis

Ratio value

Industry standard

Слайд 83DuPont Chart analysis

ROI = NPM * TAT

ROE = NPM * TAT *

DuPont Chart analysis

ROI = NPM * TAT

ROE = NPM * TAT *

Слайд 84DuPont Chart analysis

Net profit margin

4,45%

Total Asset Turnover

1,377

Earnings after taxes

$5,016

Sales

$112,760

Sales

$112,760

Total assets

$81,890

Sales

$112,760

Total Expenses

Cost of

DuPont Chart analysis

Net profit margin

4,45%

Total Asset Turnover

1,377

Earnings after taxes

$5,016

Sales

$112,760

Sales

$112,760

Total assets

$81,890

Sales

$112,760

Total Expenses

Cost of

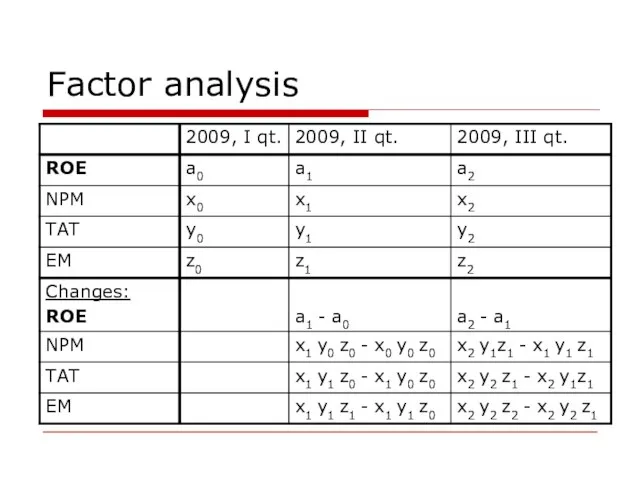

Слайд 85Factor analysis

Factor analysis

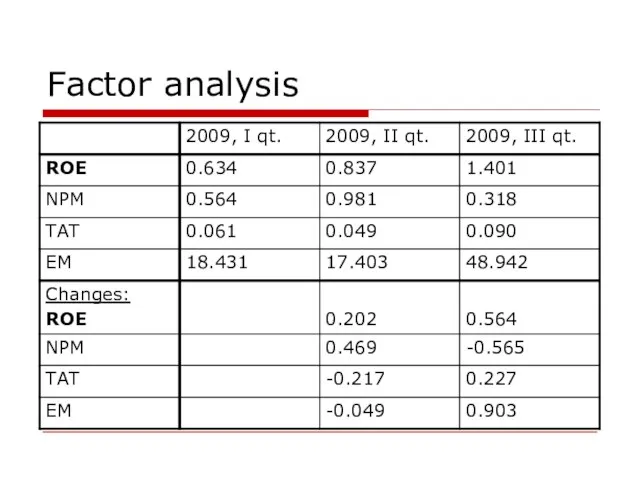

Слайд 86Factor analysis

Factor analysis

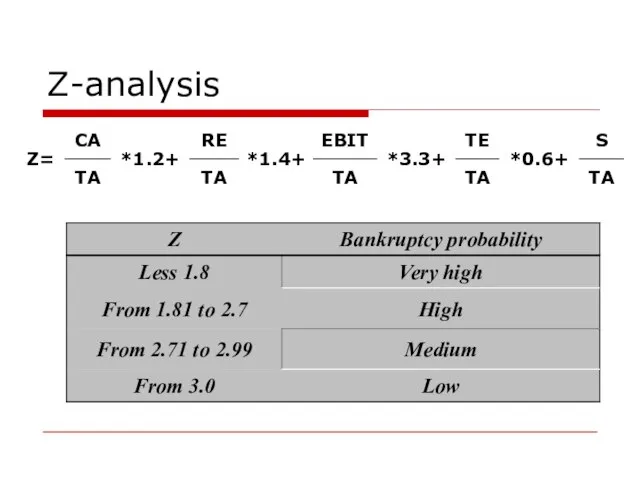

Слайд 87Z-analysis

Z-analysis

Слайд 88CASH FLOW MANAGEMENT

CASH FLOW MANAGEMENT

Слайд 89NET CASH FLOW

NET CASH FLOW

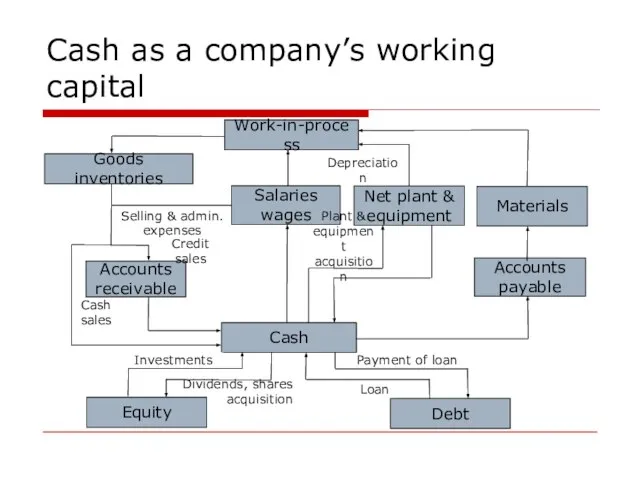

Слайд 90Cash as a company’s working capital

Cash as a company’s working capital

Слайд 91Cash as a company’s working capital

Cash volume depends on:

Production phase

Sales

Collection of accounts

Cash as a company’s working capital

Cash volume depends on:

Production phase

Sales

Collection of accounts

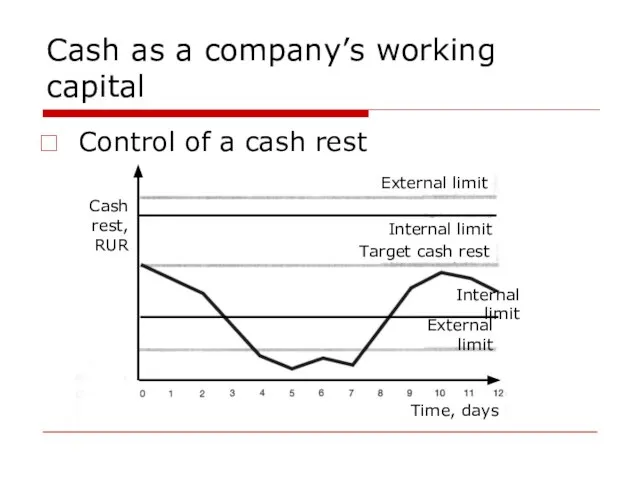

Слайд 92Cash as a company’s working capital

Control of a cash rest

Cash

rest,

RUR

External

Cash as a company’s working capital

Control of a cash rest

Cash

rest,

RUR

External

Слайд 93Cash as a company’s working capital

Cash turnover cycle

Cash as a company’s working capital

Cash turnover cycle

Слайд 94Accounts

payable

payment

period

Accounts

receivable

collection

period

Cash as a company’s working capital

Cash turnover cycle

Inventories

lifetime

Cash

turnover

cycle

Accounts

payable

payment

period

Accounts

receivable

collection

period

Cash as a company’s working capital

Cash turnover cycle

Inventories

lifetime

Cash

turnover

cycle

Слайд 95Statement of cash sources & disbursements

Cash sources

Current assets reduction (excl. cash)

Fixed assets

Statement of cash sources & disbursements

Cash sources

Current assets reduction (excl. cash)

Fixed assets

Слайд 96Depreciation

Depreciation norm depends on:

Initial

Lifetime:

Technical

Effective

Rest cost

Method of depreciation:

Straight line

Accelerated

Depreciation

Depreciation norm depends on:

Initial

Lifetime:

Technical

Effective

Rest cost

Method of depreciation:

Straight line

Accelerated

Слайд 97Depreciation

Straight-line

Accelerated

Depreciation

Straight-line

Accelerated

Слайд 98Deferred taxes

Straight-line

Accelerated

Deferred taxes

Straight-line

Accelerated

Слайд 99Deferred taxes

Deferred taxes

Слайд 100CASH FLOW FORECASTING

CASH FLOW FORECASTING

Слайд 101Forecasting of financial statements

5 steps:

Define basic data for forecasting:

external

income tax rate

interest rate

inflation

technological

Forecasting of financial statements

5 steps:

Define basic data for forecasting:

external

income tax rate

interest rate

inflation

technological

Слайд 102Forecasting of financial statements

internal:

investments policy

external financing policy

accounting policy

dividend policy

planned profitability level

cost structure

asset

Forecasting of financial statements

internal:

investments policy

external financing policy

accounting policy

dividend policy

planned profitability level

cost structure

asset

Слайд 103Forecasting of financial statements

Forecast the volume of sales

bottom-up forecasting

statistics analysis

marketing analysis

Forecast other

Forecasting of financial statements

Forecast the volume of sales

bottom-up forecasting

statistics analysis

marketing analysis

Forecast other

Слайд 104Forecasting of financial statements

Analysis of pro forma financial statements

Cash flows

Additional financing &

Forecasting of financial statements

Analysis of pro forma financial statements

Cash flows

Additional financing &

Слайд 105Percentage of sales forecasting method

The percentage of sales forecasting method:

permits a

Percentage of sales forecasting method

The percentage of sales forecasting method:

permits a

Слайд 106Percentage of sales forecasting method

Internal net cash provided = Forecasted CF -

Percentage of sales forecasting method

Internal net cash provided = Forecasted CF -

Слайд 107Percentage of sales forecasting method

To support the sales increase the management of

Percentage of sales forecasting method

To support the sales increase the management of

Слайд 108Budgeting

Five steps in preparing a budget

Budgeting

Five steps in preparing a budget

Слайд 109COSTS PLANNING

COSTS PLANNING

Слайд 110Types of costs

Variable costs are expenses that change in proportion to the

Types of costs

Variable costs are expenses that change in proportion to the

Слайд 111Types of costs

Dependence of per unit cost on the volume of production

Per

Types of costs

Dependence of per unit cost on the volume of production

Per

Слайд 112Types of costs

Total costs / quantity

TC =

FC + (VC*Q)

Total costs, RUR

Quantity, units

Fixed

Types of costs

Total costs / quantity

TC =

FC + (VC*Q)

Total costs, RUR

Quantity, units

Fixed

Слайд 113Cost structure

A cost is the value of money that has been used

Cost structure

A cost is the value of money that has been used

Слайд 114Cost structure

Costs usually charged directly

Project staff

Consultants

Project supplies

Publications

Travel

Training

Cost structure

Costs usually charged directly

Project staff

Consultants

Project supplies

Publications

Travel

Training

ПОРТФОЛИО ВОСПИТАТЕЛЯ

ПОРТФОЛИО ВОСПИТАТЕЛЯ Презентация на тему Минойская цивилизация

Презентация на тему Минойская цивилизация  PHIL 1- Lecture 3 - Week 3 moodle

PHIL 1- Lecture 3 - Week 3 moodle Железнодорожный тоннель

Железнодорожный тоннель Использование проектной методики в обучении иностранному языку

Использование проектной методики в обучении иностранному языку Система права

Система права Гигиена питания

Гигиена питания Гигиена коз и овец

Гигиена коз и овец Использование ФЦИОР на уроках физики

Использование ФЦИОР на уроках физики Налоговый вычет по ценным бумагам

Налоговый вычет по ценным бумагам Доли федеральных телеканалов при национальном и региональном размещении рекламы

Доли федеральных телеканалов при национальном и региональном размещении рекламы Презентация WasteVEM процесса

Презентация WasteVEM процесса Фея Флора. Богиня цветов и весны. С приходом весны властвовала над всеми живыми существами. Имя образовано от flos ("цветок"). По леген

Фея Флора. Богиня цветов и весны. С приходом весны властвовала над всеми живыми существами. Имя образовано от flos ("цветок"). По леген Старшов Петр Павлович

Старшов Петр Павлович Классицизм в литературе

Классицизм в литературе Методическая тема

Методическая тема He’s. She

He’s. She Программа коррекции синдрова эмоционального выгорания и повышения стрессоустойчивости личности

Программа коррекции синдрова эмоционального выгорания и повышения стрессоустойчивости личности Пирог Ленивец

Пирог Ленивец Учебный семинар «Формирование универсальных учебных действий на уроках в начальной школе»

Учебный семинар «Формирование универсальных учебных действий на уроках в начальной школе» Диалог о вредной привычке.

Диалог о вредной привычке. Права та обовязки споживачів

Права та обовязки споживачів Mother teresa

Mother teresa Удаление третьих моляров верхней и нижней челюсти. Ретенция и дистопия зубов мудрости

Удаление третьих моляров верхней и нижней челюсти. Ретенция и дистопия зубов мудрости Мыс өндіріс қалдықтарынан түсті металл тұздарын алуды жобалау

Мыс өндіріс қалдықтарынан түсті металл тұздарын алуды жобалау Персональное предложение по регистрации товарного знака Баранкино для ИП (ООО) Под ключ

Персональное предложение по регистрации товарного знака Баранкино для ИП (ООО) Под ключ Семь дней недели

Семь дней недели