- CORPORATE FINANCE

Содержание

- 2. FINANCIAL MARKETS AND INTEREST RATES

- 3. Market Players An investor / lender is an individual, company, government, or any entity that owns

- 4. Securities Debt security or bond – promises periodic payments of interest and/or principal from a claim

- 5. Types of Financial Markets Money markets trade short-term, marketable, liquid, low-risk debt securities - "cash equivalents“

- 6. INTEREST RATES The stated or offered rate of interest (r) reflects three factors: Pure rate of

- 7. Pure Interest Rate the rate for a risk-free security when no inflation is expected constantly changes

- 8. Inflation Investors build in an inflation premium to compensate for this loss of value the inflation

- 9. Risk Counterparty (default) risk is the chance that the borrower will not be able to pay

- 10. Risk Liquidity risk – possible losses if there is no opportunity to buy or to sell

- 11. Risk Interest rate risk - possible changes of asset value due to changes of the interest

- 12. Risk Currency risk – possible changes of the assets value due to changes of the currency

- 13. Normal Yield Curve Theories upward sloping yield curve is considered normal: expectations theory, the market segmentation

- 14. Expectations Theory The yield curve reflects lenders' and borrowers' expectations of inflation Changes in these expectations

- 15. Market Segmentation Theory The slope of the yield curve depends on supply / demand conditions in

- 16. Liquidity Preference Theory long-term securities often yield more than short-term securities Investors generally prefer short-term securities,

- 17. Liquidity Preference Theory Borrowers dislike short-term debt because it exposes them to the risk of having

- 19. Скачать презентацию

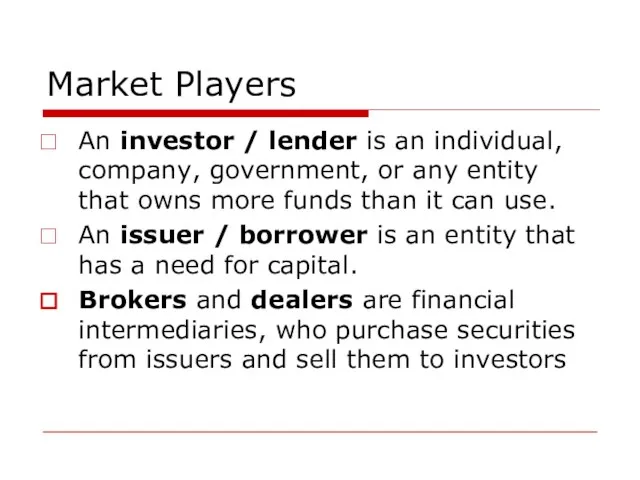

Слайд 3Market Players

An investor / lender is an individual, company, government, or any

Market Players

An investor / lender is an individual, company, government, or any

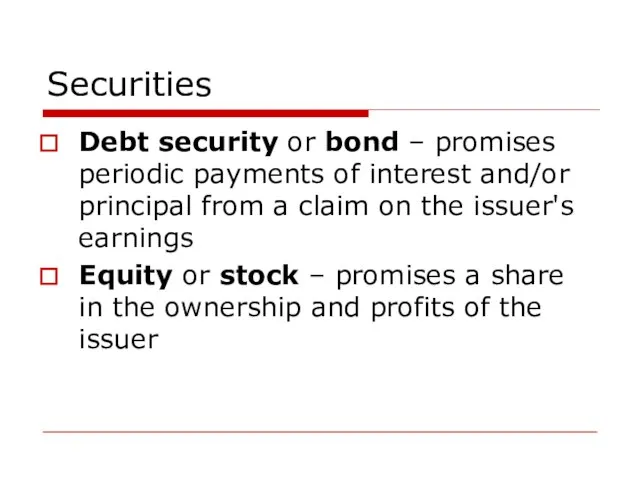

Слайд 4Securities

Debt security or bond – promises periodic payments of interest and/or principal

Securities

Debt security or bond – promises periodic payments of interest and/or principal

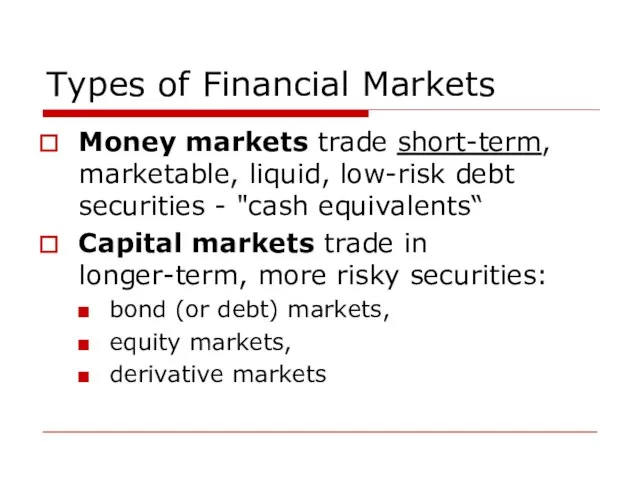

Слайд 5Types of Financial Markets

Money markets trade short-term, marketable, liquid, low-risk debt securities

Types of Financial Markets

Money markets trade short-term, marketable, liquid, low-risk debt securities

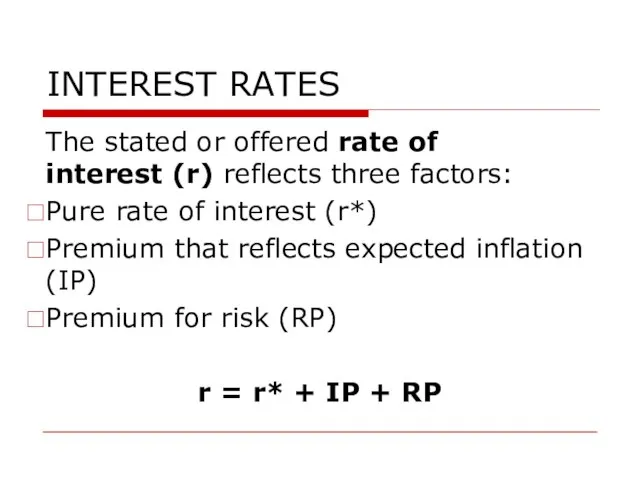

Слайд 6INTEREST RATES

The stated or offered rate of

interest (r) reflects three factors:

Pure

INTEREST RATES

The stated or offered rate of

interest (r) reflects three factors:

Pure

Слайд 7Pure Interest Rate

the rate for a risk-free security when no inflation is

Pure Interest Rate

the rate for a risk-free security when no inflation is

Слайд 8Inflation

Investors build in an inflation premium to compensate for this loss of

Inflation

Investors build in an inflation premium to compensate for this loss of

Слайд 9Risk

Counterparty (default) risk is the chance that the borrower will not be

Risk

Counterparty (default) risk is the chance that the borrower will not be

Слайд 10Risk

Liquidity risk – possible losses if there is no opportunity to buy

Risk

Liquidity risk – possible losses if there is no opportunity to buy

Слайд 11Risk

Interest rate risk - possible changes of asset value due to changes

Risk

Interest rate risk - possible changes of asset value due to changes

Слайд 12Risk

Currency risk – possible changes of the assets value due to changes

Risk

Currency risk – possible changes of the assets value due to changes

Слайд 13Normal Yield Curve Theories

upward sloping yield curve is considered normal:

expectations theory,

the

Normal Yield Curve Theories

upward sloping yield curve is considered normal:

expectations theory,

the

Слайд 14Expectations Theory

The yield curve reflects lenders' and borrowers' expectations of inflation

Changes in

Expectations Theory

The yield curve reflects lenders' and borrowers' expectations of inflation

Changes in

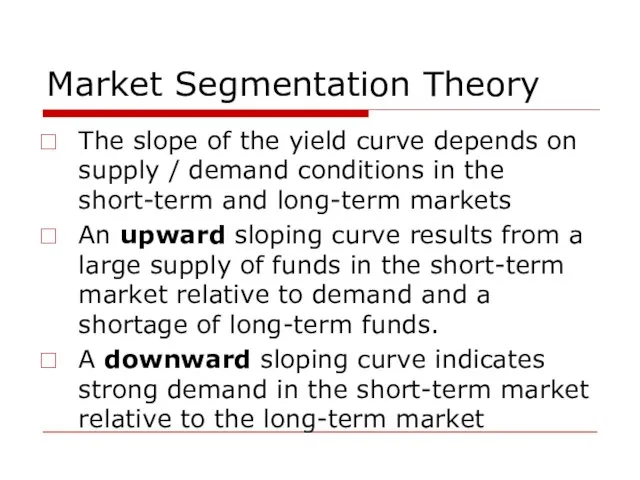

Слайд 15Market Segmentation Theory

The slope of the yield curve depends on supply /

Market Segmentation Theory

The slope of the yield curve depends on supply /

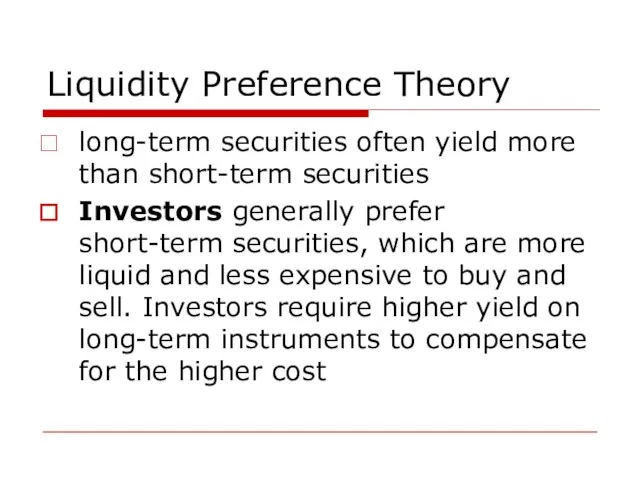

Слайд 16Liquidity Preference Theory

long-term securities often yield more than short-term securities

Investors generally prefer

Liquidity Preference Theory

long-term securities often yield more than short-term securities

Investors generally prefer

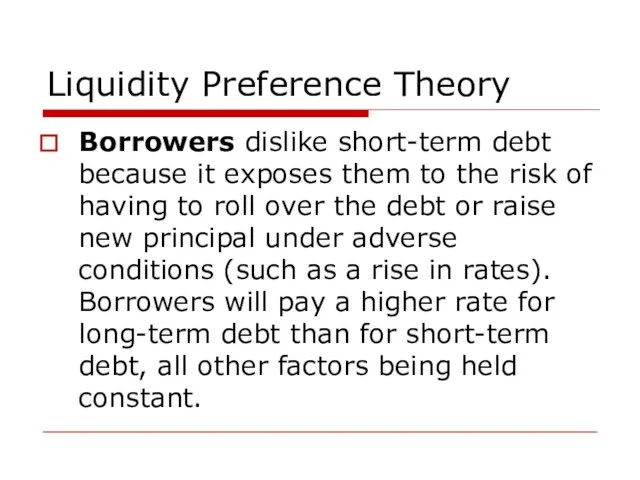

Слайд 17Liquidity Preference Theory

Borrowers dislike short-term debt because it exposes them to the

Liquidity Preference Theory

Borrowers dislike short-term debt because it exposes them to the

ПОРТФОЛИО ВОСПИТАТЕЛЯ

ПОРТФОЛИО ВОСПИТАТЕЛЯ Презентация на тему Минойская цивилизация

Презентация на тему Минойская цивилизация  PHIL 1- Lecture 3 - Week 3 moodle

PHIL 1- Lecture 3 - Week 3 moodle Железнодорожный тоннель

Железнодорожный тоннель FINANCIAL ANALYSIS AND

FINANCIAL ANALYSIS AND Использование проектной методики в обучении иностранному языку

Использование проектной методики в обучении иностранному языку Система права

Система права Гигиена питания

Гигиена питания Гигиена коз и овец

Гигиена коз и овец Использование ФЦИОР на уроках физики

Использование ФЦИОР на уроках физики Налоговый вычет по ценным бумагам

Налоговый вычет по ценным бумагам Доли федеральных телеканалов при национальном и региональном размещении рекламы

Доли федеральных телеканалов при национальном и региональном размещении рекламы Презентация WasteVEM процесса

Презентация WasteVEM процесса Фея Флора. Богиня цветов и весны. С приходом весны властвовала над всеми живыми существами. Имя образовано от flos ("цветок"). По леген

Фея Флора. Богиня цветов и весны. С приходом весны властвовала над всеми живыми существами. Имя образовано от flos ("цветок"). По леген Старшов Петр Павлович

Старшов Петр Павлович Классицизм в литературе

Классицизм в литературе Методическая тема

Методическая тема He’s. She

He’s. She Программа коррекции синдрова эмоционального выгорания и повышения стрессоустойчивости личности

Программа коррекции синдрова эмоционального выгорания и повышения стрессоустойчивости личности Пирог Ленивец

Пирог Ленивец Учебный семинар «Формирование универсальных учебных действий на уроках в начальной школе»

Учебный семинар «Формирование универсальных учебных действий на уроках в начальной школе» Диалог о вредной привычке.

Диалог о вредной привычке. Права та обовязки споживачів

Права та обовязки споживачів Mother teresa

Mother teresa Удаление третьих моляров верхней и нижней челюсти. Ретенция и дистопия зубов мудрости

Удаление третьих моляров верхней и нижней челюсти. Ретенция и дистопия зубов мудрости Мыс өндіріс қалдықтарынан түсті металл тұздарын алуды жобалау

Мыс өндіріс қалдықтарынан түсті металл тұздарын алуды жобалау Персональное предложение по регистрации товарного знака Баранкино для ИП (ООО) Под ключ

Персональное предложение по регистрации товарного знака Баранкино для ИП (ООО) Под ключ Семь дней недели

Семь дней недели