- Insurance of International Trade Risks

Содержание

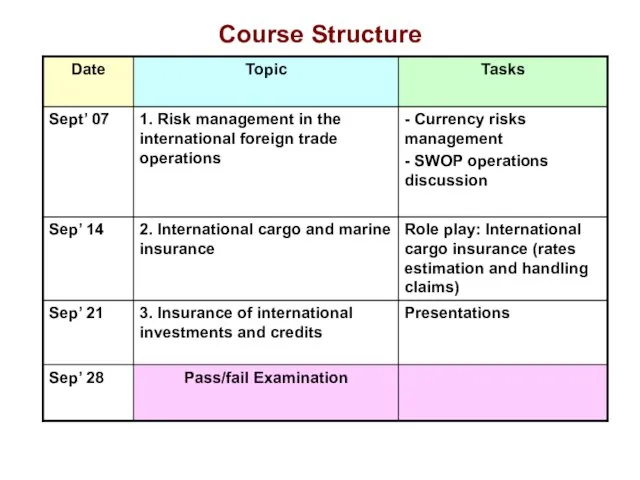

- 2. Course Structure

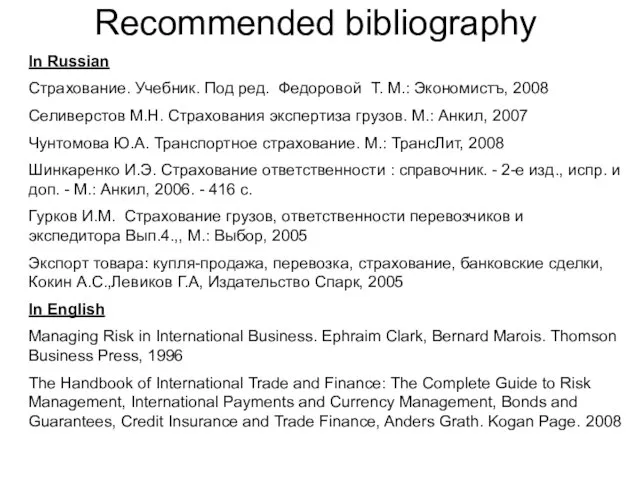

- 3. Recommended bibliography In Russian Страхование. Учебник. Под ред. Федоровой Т. М.: Экономистъ, 2008 Селиверстов М.Н. Страхования

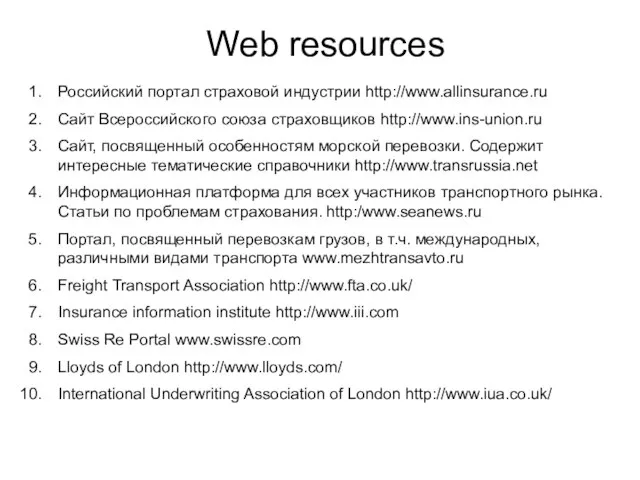

- 4. Web resources Российский портал страховой индустрии http://www.allinsurance.ru Сайт Всероссийского союза страховщиков http://www.ins-union.ru Сайт, посвященный особенностям морской

- 5. 1. Risk management in the international foreign trade operations

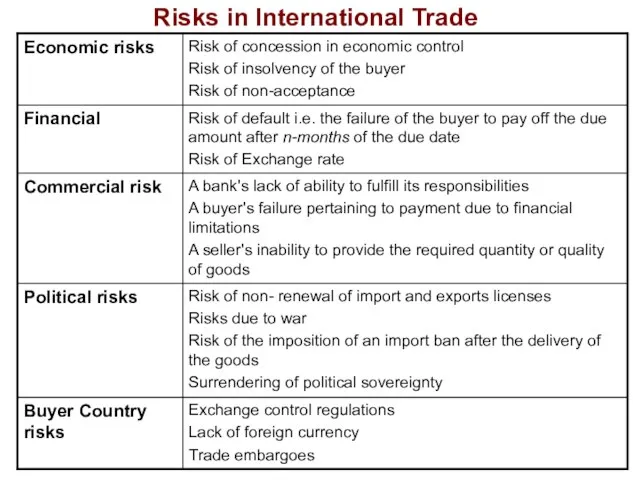

- 6. Risks in International Trade

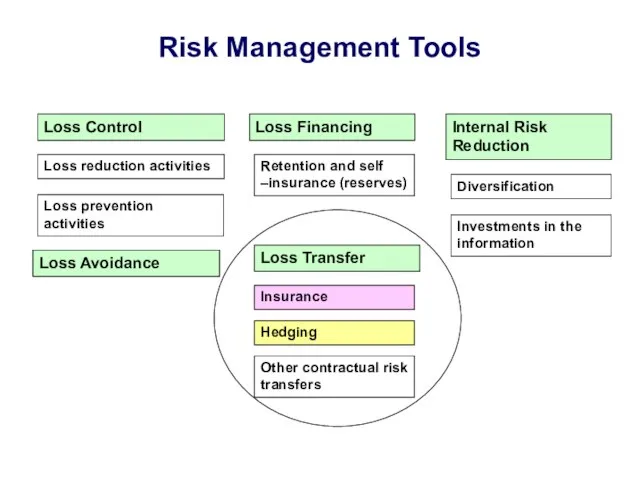

- 7. Risk Management Tools Loss Control Loss Financing Internal Risk Reduction Loss reduction activities Loss prevention activities

- 8. Most popular risk management instruments A documentary letter of credit offers the best protection for overseas

- 9. How a documentary letter of credit works? A documentary letter of credit is opened by the

- 10. 1. After a contract is concluded between buyer and seller, buyer's bank supplies a letter of

- 11. 2. Seller consigns the goods to a carrier in exchange for a bill of lading Goods

- 12. Seller put bill of lading for payment from buyer's bank. Buyer's bank exchanges bill of lading

- 13. Buyer provides bill of lading to carrier and takes delivery of goods Goods BL

- 14. Exchange rate exposure You make forward purchases of foreign currencies and wish to protect yourself against

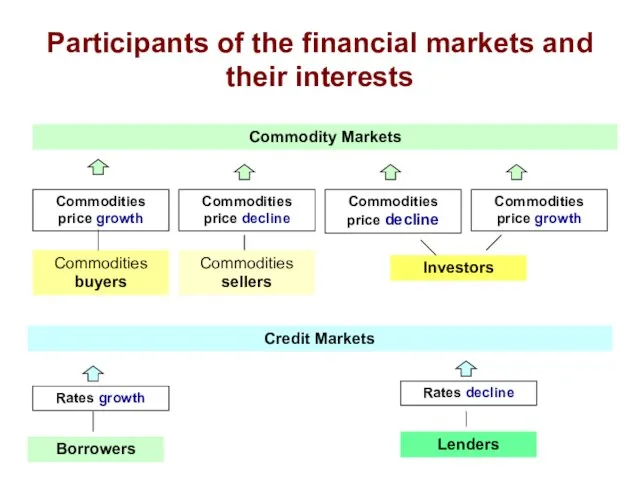

- 15. Participants of the financial markets and their interests

- 16. Participants of the financial markets and their interests Commodity Markets Commodities price growth Commodities price decline

- 17. Currency appreciations and depreciations Previous Exchange Rate (X): Currency A/ Currency B Current Exchange Rate (Y):

- 18. Foreign currency exchange rate risks Translation risks Arising from the ownership of operating companies outside the

- 19. Minimizing contractual risks Example: UK based company buys property in USA for $ 440 mln. Payment

- 20. Minimizing contractual risks Method 2. Buy dollars forward Cost of hedging = Forward rate – Expected

- 21. Currency forward contracts and rates $0,0655

- 22. Forward premium Fair Forward Exchange Rate = Spot rate * (1+ R for) / (1+R home)

- 23. Hedging with currency forward contracts UK company expects to receive SFr 10 mln in 90 days

- 24. SWAPS & Interest rate risks SWAPS – arrangement by two counterparties to exchange one stream of

- 25. Fixed for floating swaps Notional principal = $ 10 mln Semi annual net CF for fixed

- 26. Example of currency swap US based company A is going to invest in Germany in EURO

- 27. Risk Hedging, Risk Management and Value

- 28. 2. International cargo and marine insurance

- 29. Plan of the lecture Structure of insurance programs Forms of insurance agreements International Cargo Clauses Carrier’s

- 30. Insurance programs for foreign trade organizations INSURABLE RISKS Hull Cargo Carrier’s Liability Damage, total destruction or

- 31. Who are interested in transportation of cargo insurance? Importers, buying on FOB & CPT conditions Exporters,

- 32. Forms of insurance agreements

- 33. Single insurance policy / Разовый полис страхования Valid for one shipping Valid for a period from

- 34. Open cover / Генеральный полис (договор) страхования Applicable when: Is issued once by the insurer under

- 35. Open cover Client Insurer 1. Specification of main conditions of insurance agreement 2. Signing the open

- 36. Sum insured (cargo) Max sum insured by open policy on annual basis Max limit by each

- 37. Open cover (frequent deliveries) Client Insurer During the month: Cargo shipments Акцепт (Страховой сертификат) / Issue

- 38. Open cover Advantages: - decreasing the administrative costs all the shipments automatically insured for 1 year

- 39. What factors influence on the amount of the insurance rate and cost of insurance? Insurance Conditions

- 40. International Cargo Clauses (ICC)

- 41. A, B, C Clauses of ICC - Institute Cargo Clauses (Institute of London Undewriters) С =

- 42. Cargo insurance conditions Clauses cover all risks of loss of or damage (All risks) Clauses cover

- 43. Cargo insurance conditions All risks (A) Damage, total destruction or loss of the whole cargo or

- 44. Comparative analysis of ICC coverages

- 45. Carrier’s liability insurance

- 46. Insurance of liability for international transportation organizations Responsibility to cargo damage (including insurance within the limits

- 47. Claim cover limitations (cargo damage) * - The SDR is an international reserve asset, created by

- 48. Special Drawing Rights (SDR) Valuation It is calculated as the sum of specific amounts of the

- 49. Specific of handling claims

- 50. Handling of claims What are the steps if the losses took place ?

- 51. The process of handling the claims Damage Insured info Written Notice of Loss Carrier Survey/ inspection

- 52. Who else involved in claim producing process? Surveyor Adjuster Defines: Fact of damage Amount of loss

- 53. What documents are included in the claim to insurance company? Proof of ownership of cargo Survey

- 54. Survey report is one of the most important documents for insurer A survey should contain the

- 55. Generally the following documents will be required to settle a claim 1. Proof of Insurance: Declaration

- 56. Cases when insurers don’t respond to the clients When claims have to be sent to the

- 57. 3. Insurance of international credits and investments

- 58. Country risks classification Political risks are related either to the country of a foreign buyer or

- 59. Political risks Political risk may materialise as the consequence of a long course of events, or

- 60. Political risks classification

- 61. Risk management for political risks Internal techniques: Decreasing overall risk exposure (choice of country or trade

- 62. Commercial risks Financial risk assumed by a seller when extending credit without any collateral or recourse.

- 63. Guarantees offered to exporter in the export/import operations Credit Risk Guarantee provides the exporter with cover

- 64. Biggest credit insurers/guarantee providers in Europe

- 65. Coface

- 66. Euler Hermes Group

- 67. Guarantee Services Guarantees are issued for clients in respect of their contractual or statutory obligations to

- 68. Guarantee Premiums Short-term (repayment period less than 2 years) Buyer Credit and Credit Risk Guarantees usually

- 69. Example of Guarantee Premiums Table

- 70. Country Ratings Rating classification for credit guarantees’ rates: 0 : Advanced economy - no minimum premium

- 71. Credit rating agencies Business Environmental Risk Intelligence (BERI) Frost and Sullivan (Index WPRF – World Political

- 72. Credit Insurance

- 73. Structure of credit insurance market Private insurers State Insurance of commercial credits inside the countries Insurance

- 74. Capital concentration in the European credit insurance market

- 75. Commercial insurance companies, operating on the export credit insurance market Lloyds of London (Robert and Hiscox

- 76. Export credit scheme Risks considered by insurer: Unpaid maturities notified by one or more insureds Bankruptcy,

- 77. Types of credit insurance policies 1. Extraordinary coverage (specific coverage) Is used when the outstanding balances

- 78. Stages of insurance

- 79. Factors, influencing on the decision about insurance

- 80. Credit limit 2 Credit limit 1 Credit limit 3 Credit limit 4 Buyer B Buyer А

- 81. 3. Financial results became worse 4. Serious declining of financial position Buyer Monitoring of contractors enables

- 82. Risk analysis of credit portfolio and conditions of insurance Buyer Risk class (solvency, financial stability, ratio

- 83. Amount of debt minus Sum that was partially paid Revenue from the sales of returned goods

- 84. Example of coverage table (credit limits)

- 85. Coinsurance and Loss

- 86. Условия: Поставлен товар на сумму 100 000.00 руб. Безусловная франшиза-20% Сумма неоплаченного счета- 50 000.00 руб.

- 87. Dynamics of payments’ delays index by branches of economics (Basis - 100) (chemical industry) (mechanical engineering

- 88. Dynamics of payments’ delays index by branches of economics (Basis - 100) (average on the world

- 89. Branch risks by regions and the world countries (according to ratings of Coface) Source: Sector Analysis,

- 90. International investments’ insurance agencies Multilateral Investments Guaranteeing Agency (MIGA) - a member of the World Bank

- 91. Functions of MIGA Political risks insured: Currency transfer restriction Expropriation War and civil disturbance Breach of

- 92. Who eligible for MIGA’s Guarantee Coverage? New cross-border investments originating in any MIGA member country, destined

- 93. MIGA's Reinsurance Partners (1)

- 94. MIGA's Reinsurance Partners (2)

- 95. Currency transfer restriction Coverage protects against: losses arising from an investor's inability to convert local currency

- 96. Expropriation Coverage offers protection against: loss of the insured investment as a result of acts by

- 97. Breach of contract Coverage protects against: Losses arising from the host government's breach or repudiation of

- 99. Скачать презентацию

Слайд 3Recommended bibliography

In Russian

Страхование. Учебник. Под ред. Федоровой Т. М.: Экономистъ, 2008

Селиверстов М.Н.

Recommended bibliography

In Russian

Страхование. Учебник. Под ред. Федоровой Т. М.: Экономистъ, 2008

Селиверстов М.Н.

Слайд 4Web resources

Российский портал страховой индустрии http://www.allinsurance.ru

Сайт Всероссийского союза страховщиков http://www.ins-union.ru

Сайт, посвященный особенностям

Web resources

Российский портал страховой индустрии http://www.allinsurance.ru

Сайт Всероссийского союза страховщиков http://www.ins-union.ru

Сайт, посвященный особенностям

Слайд 51. Risk management in the international foreign trade operations

1. Risk management in the international foreign trade operations

Слайд 6Risks in International Trade

Risks in International Trade

Слайд 7Risk Management Tools

Loss Control

Loss Financing

Internal Risk Reduction

Loss reduction activities

Loss prevention activities

Retention and

Risk Management Tools

Loss Control

Loss Financing

Internal Risk Reduction

Loss reduction activities

Loss prevention activities

Retention and

Слайд 8Most popular risk management instruments

A documentary letter of credit

offers the best

Most popular risk management instruments

A documentary letter of credit

offers the best

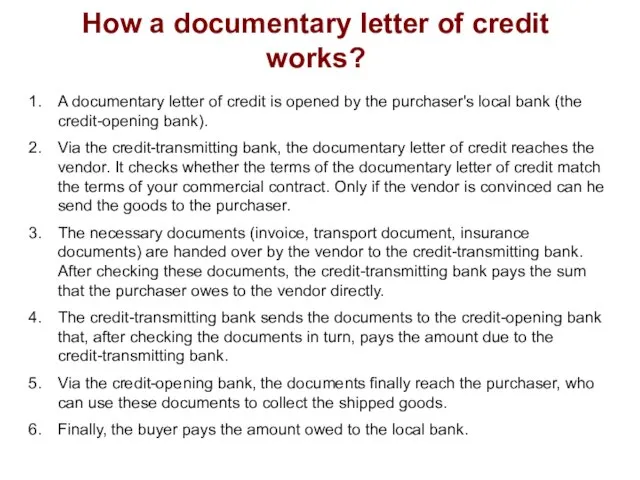

Слайд 9How a documentary letter of credit works?

A documentary letter of credit is

How a documentary letter of credit works?

A documentary letter of credit is

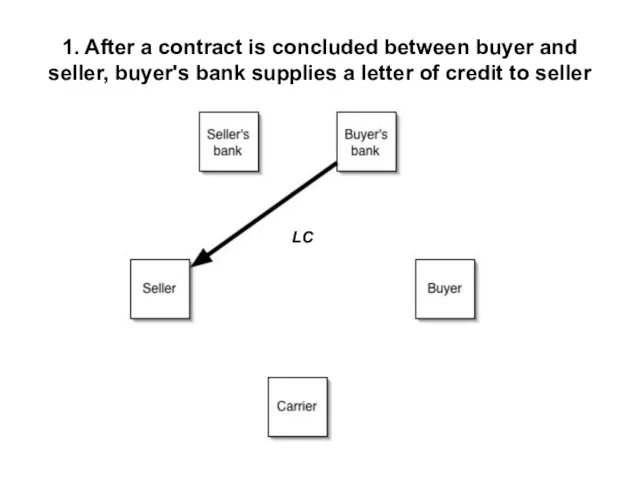

Слайд 101. After a contract is concluded between buyer and seller, buyer's bank

1. After a contract is concluded between buyer and seller, buyer's bank

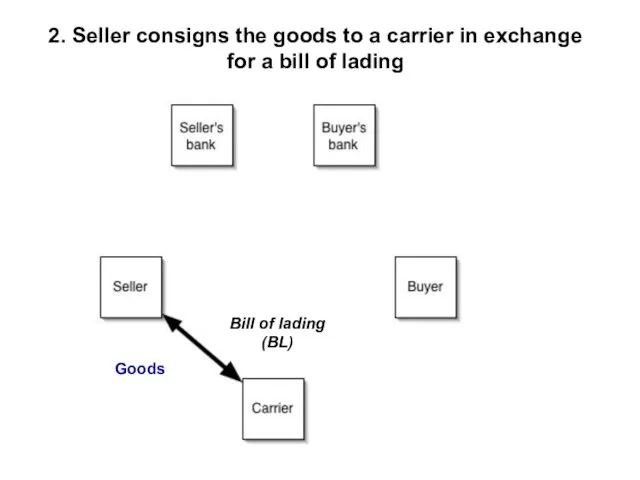

Слайд 112. Seller consigns the goods to a carrier in exchange for a

2. Seller consigns the goods to a carrier in exchange for a

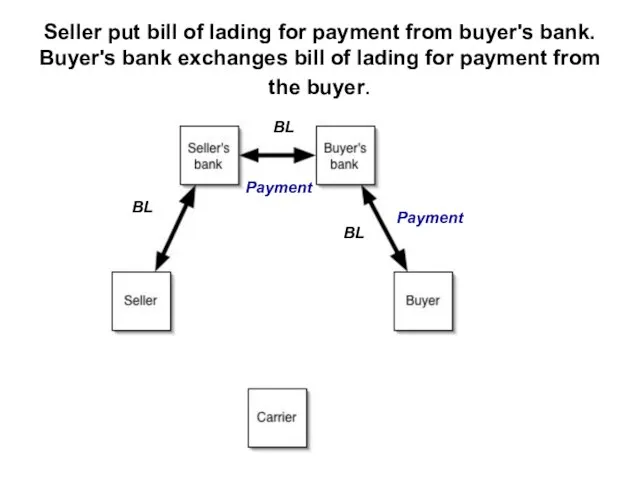

Слайд 12Seller put bill of lading for payment from buyer's bank. Buyer's bank

Seller put bill of lading for payment from buyer's bank. Buyer's bank

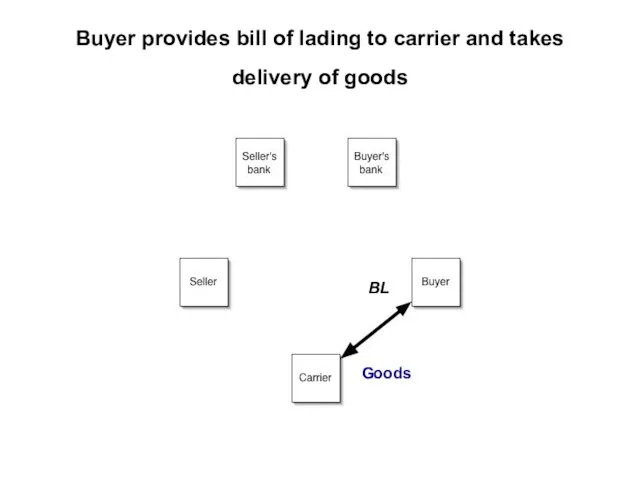

Слайд 13Buyer provides bill of lading to carrier and takes delivery of goods

Buyer provides bill of lading to carrier and takes delivery of goods

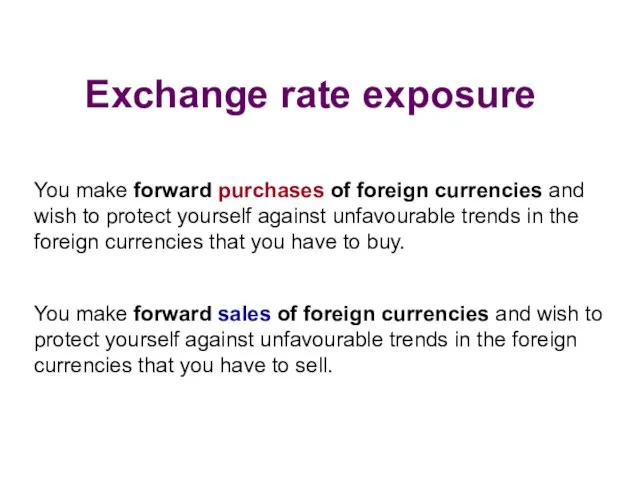

Слайд 14Exchange rate exposure

You make forward purchases of foreign currencies and wish to

Exchange rate exposure

You make forward purchases of foreign currencies and wish to

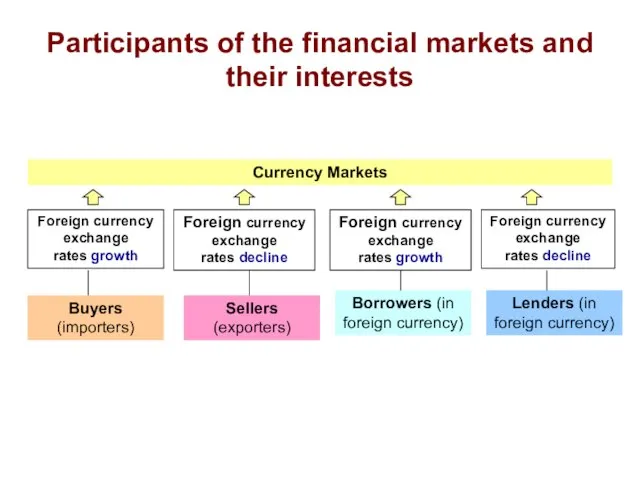

Слайд 15Participants of the financial markets and their interests

Participants of the financial markets and their interests

Слайд 16Participants of the financial markets and their interests

Commodity Markets

Commodities price growth

Commodities price

Participants of the financial markets and their interests

Commodity Markets

Commodities price growth

Commodities price

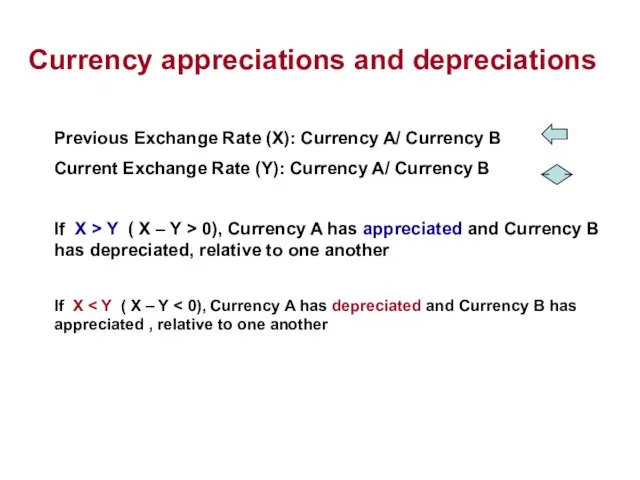

Слайд 17Currency appreciations and depreciations

Previous Exchange Rate (X): Currency A/ Currency B

Current Exchange

Currency appreciations and depreciations

Previous Exchange Rate (X): Currency A/ Currency B

Current Exchange

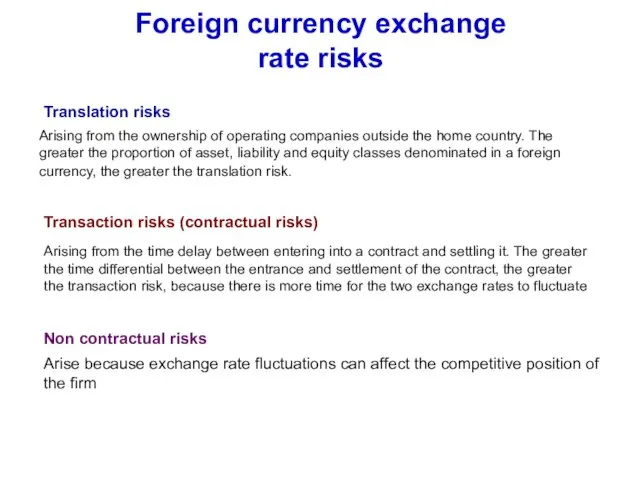

Слайд 18Foreign currency exchange

rate risks

Translation risks

Arising from the ownership of operating companies

Foreign currency exchange

rate risks

Translation risks

Arising from the ownership of operating companies

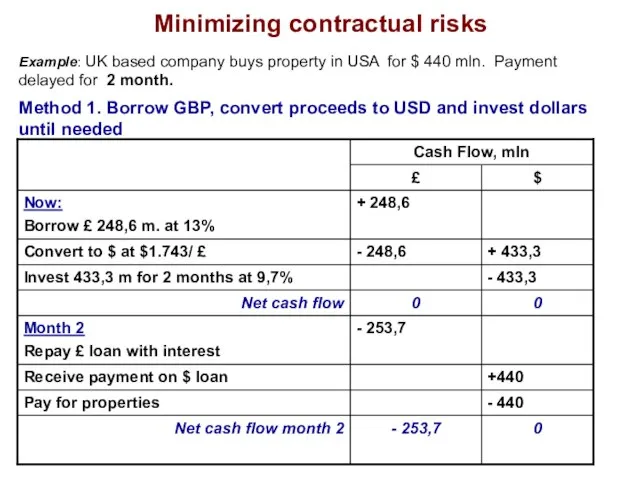

Слайд 19Minimizing contractual risks

Example: UK based company buys property in USA for $

Minimizing contractual risks

Example: UK based company buys property in USA for $

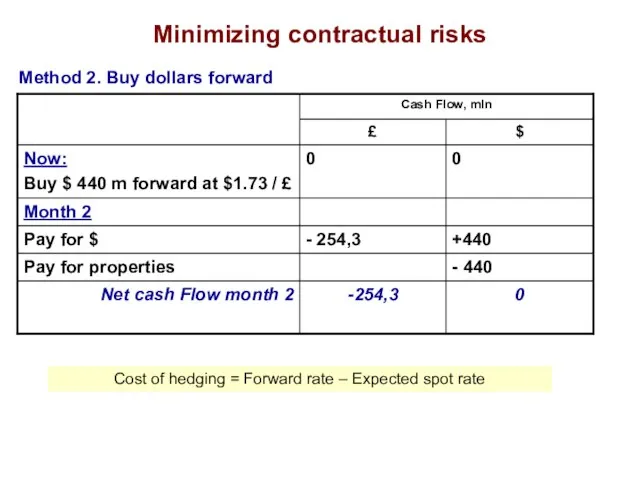

Слайд 20Minimizing contractual risks

Method 2. Buy dollars forward

Cost of hedging = Forward rate

Minimizing contractual risks

Method 2. Buy dollars forward

Cost of hedging = Forward rate

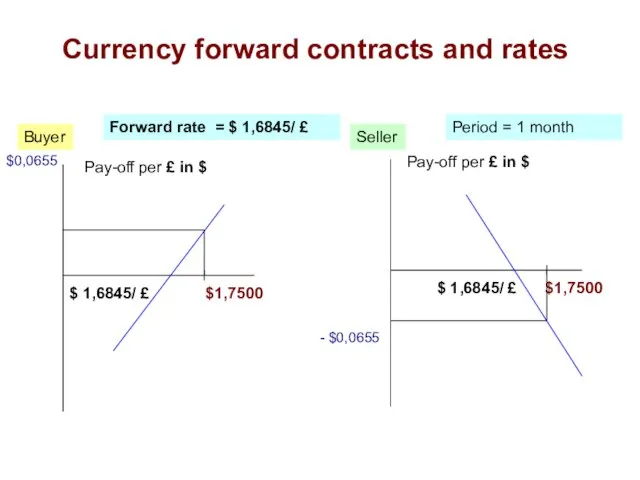

Слайд 21Currency forward contracts and rates

$0,0655

Currency forward contracts and rates

$0,0655

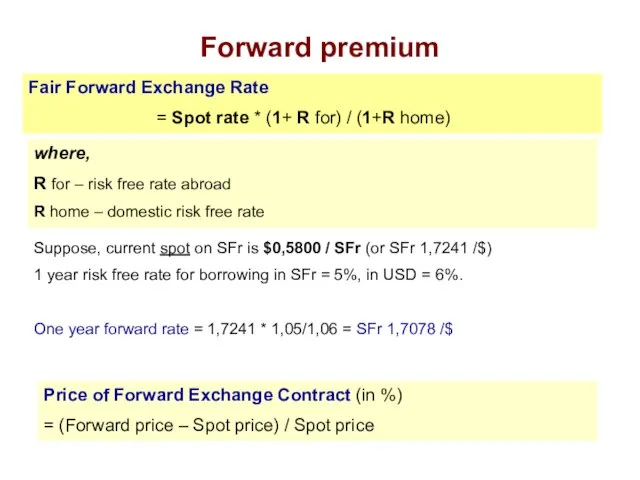

Слайд 22Forward premium

Fair Forward Exchange Rate

= Spot rate * (1+ R for)

Forward premium

Fair Forward Exchange Rate

= Spot rate * (1+ R for)

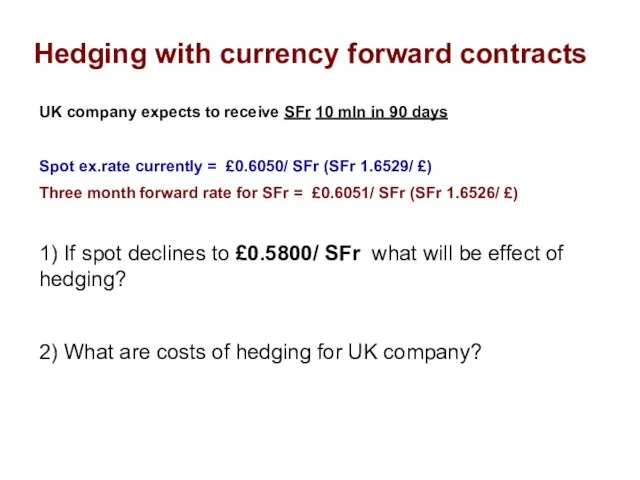

Слайд 23Hedging with currency forward contracts

UK company expects to receive SFr 10 mln

Hedging with currency forward contracts

UK company expects to receive SFr 10 mln

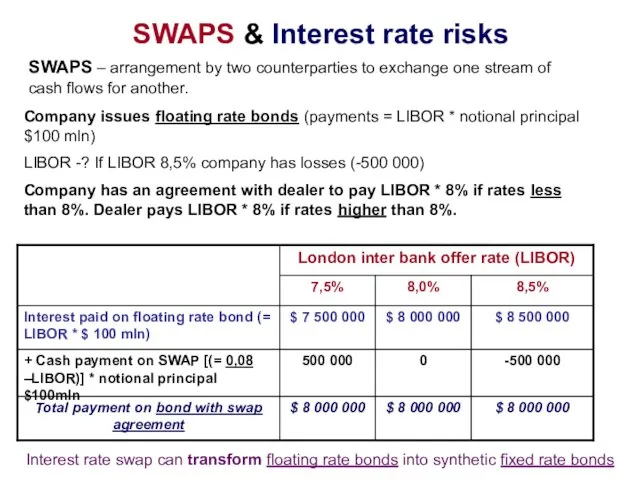

Слайд 24SWAPS & Interest rate risks

SWAPS – arrangement by two counterparties to exchange

SWAPS & Interest rate risks

SWAPS – arrangement by two counterparties to exchange

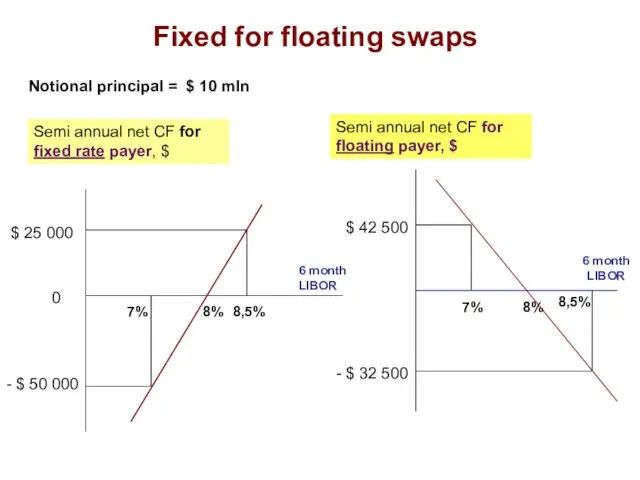

Слайд 25Fixed for floating swaps

Notional principal = $ 10 mln

Semi annual net

Fixed for floating swaps

Notional principal = $ 10 mln

Semi annual net

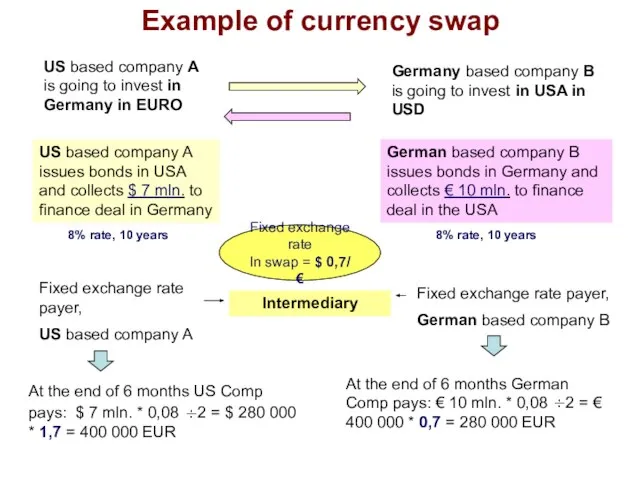

Слайд 26Example of currency swap

US based company A is going to invest in

Example of currency swap

US based company A is going to invest in

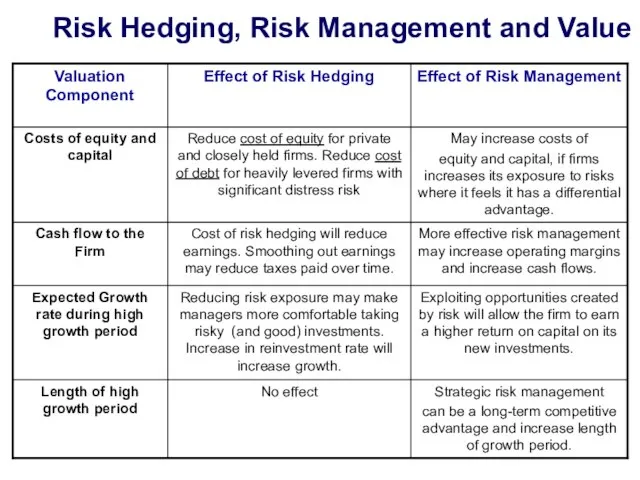

Слайд 27Risk Hedging, Risk Management and Value

Risk Hedging, Risk Management and Value

Слайд 282. International cargo and marine insurance

2. International cargo and marine insurance

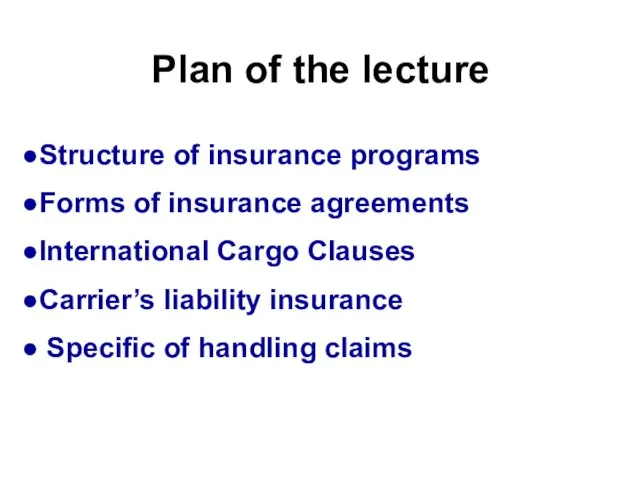

Слайд 29Plan of the lecture

Structure of insurance programs

Forms of insurance agreements

International Cargo Clauses

Carrier’s

Plan of the lecture

Structure of insurance programs

Forms of insurance agreements

International Cargo Clauses

Carrier’s

Слайд 30Insurance programs for foreign trade organizations

INSURABLE RISKS

Hull

Cargo

Carrier’s Liability

Damage, total

destruction

or loss

Insurance programs for foreign trade organizations

INSURABLE RISKS

Hull

Cargo

Carrier’s Liability

Damage, total

destruction

or loss

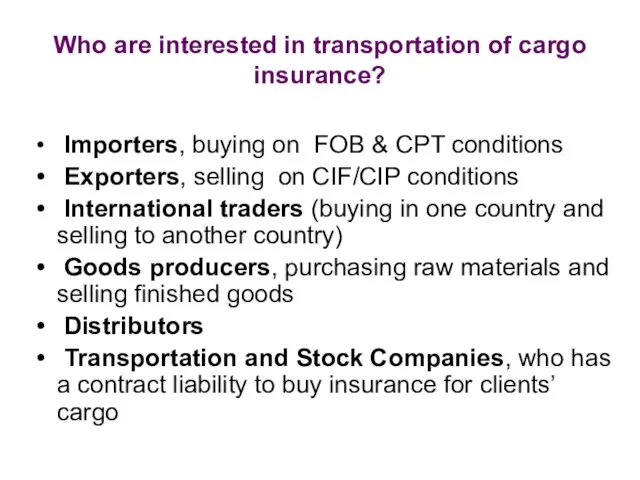

Слайд 31Who are interested in transportation of cargo insurance?

Importers, buying on FOB

Who are interested in transportation of cargo insurance?

Importers, buying on FOB

Слайд 32Forms of insurance agreements

Forms of insurance agreements

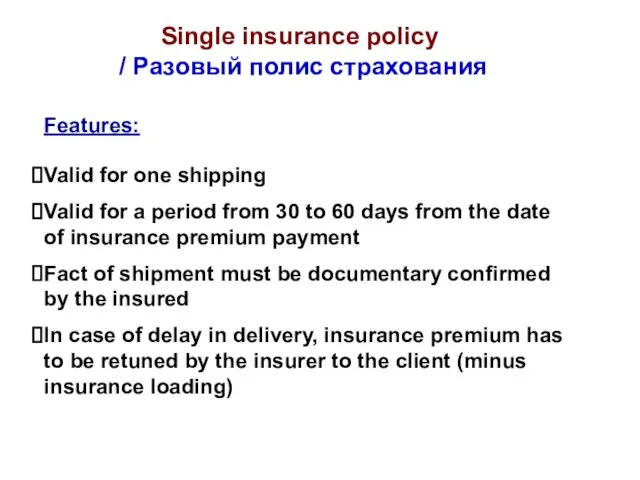

Слайд 33Single insurance policy / Разовый полис страхования

Valid for one shipping

Valid for a

Single insurance policy / Разовый полис страхования

Valid for one shipping

Valid for a

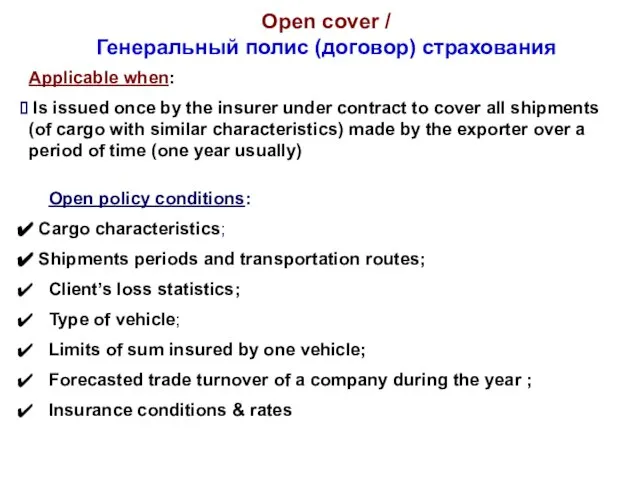

Слайд 34Open cover /

Генеральный полис (договор) страхования

Applicable when:

Is issued once by

Open cover /

Генеральный полис (договор) страхования

Applicable when:

Is issued once by

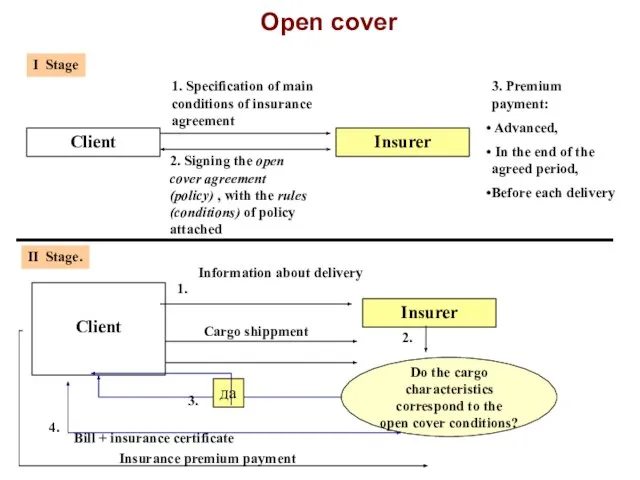

Слайд 35Open cover

Client

Insurer

1. Specification of main conditions of insurance agreement

2. Signing the open

Open cover

Client

Insurer

1. Specification of main conditions of insurance agreement

2. Signing the open

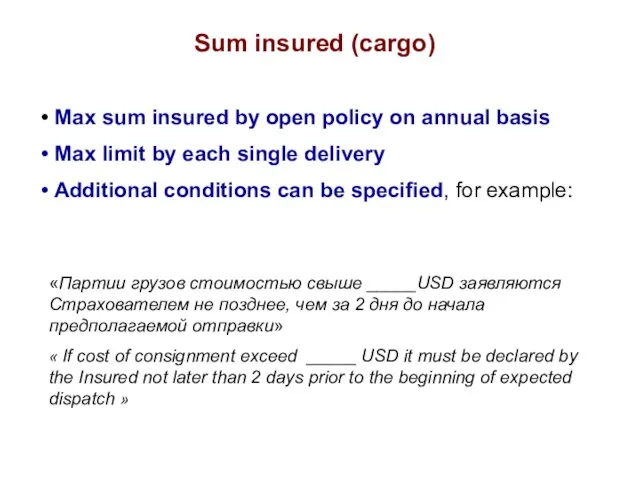

Слайд 36Sum insured (cargo)

Max sum insured by open policy on annual basis

Sum insured (cargo)

Max sum insured by open policy on annual basis

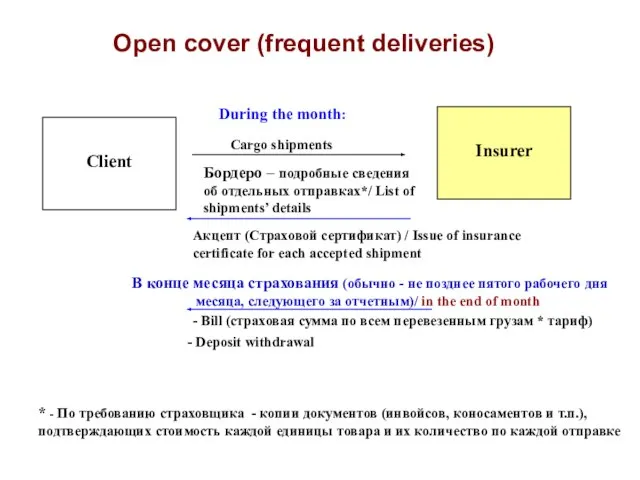

Слайд 37Open cover (frequent deliveries)

Client

Insurer

During the month:

Cargo shipments

Акцепт (Страховой сертификат) / Issue

Open cover (frequent deliveries)

Client

Insurer

During the month:

Cargo shipments

Акцепт (Страховой сертификат) / Issue

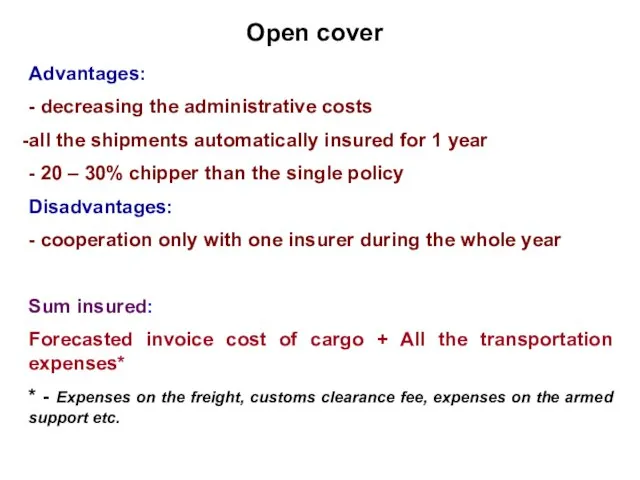

Слайд 38Open cover

Advantages:

- decreasing the administrative costs

all the shipments automatically insured for

Open cover

Advantages:

- decreasing the administrative costs

all the shipments automatically insured for

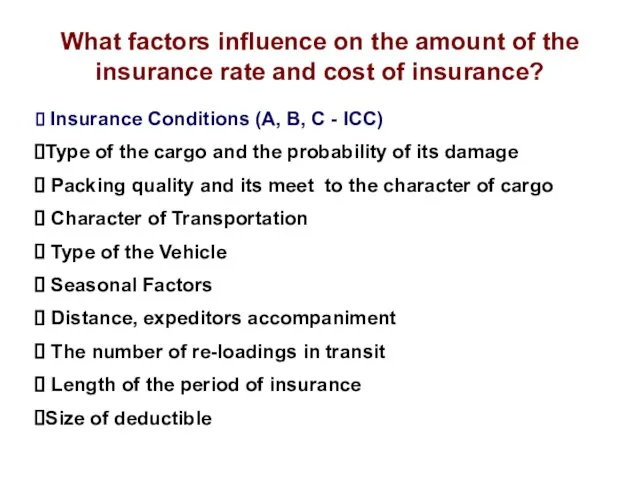

Слайд 39What factors influence on the amount of the insurance rate and cost

What factors influence on the amount of the insurance rate and cost

Слайд 40International Cargo Clauses (ICC)

International Cargo Clauses (ICC)

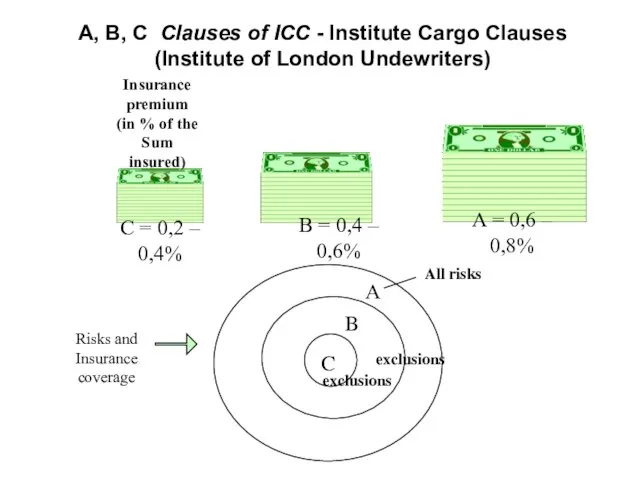

Слайд 41A, B, C Clauses of ICC - Institute Cargo Clauses (Institute of

A, B, C Clauses of ICC - Institute Cargo Clauses (Institute of

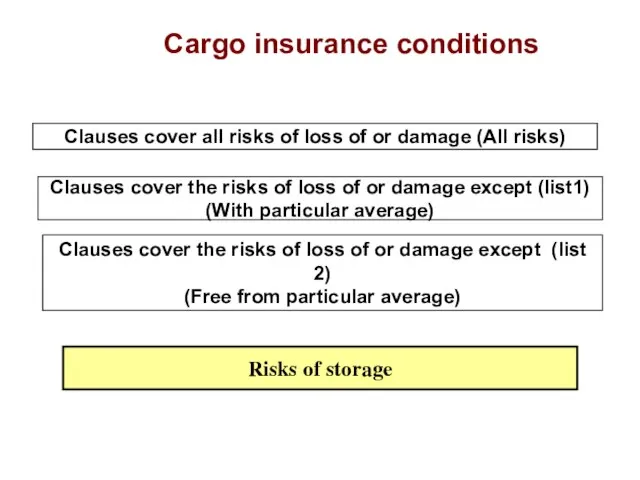

Слайд 42Cargo insurance conditions

Clauses cover all risks of loss of or damage (All

Cargo insurance conditions

Clauses cover all risks of loss of or damage (All

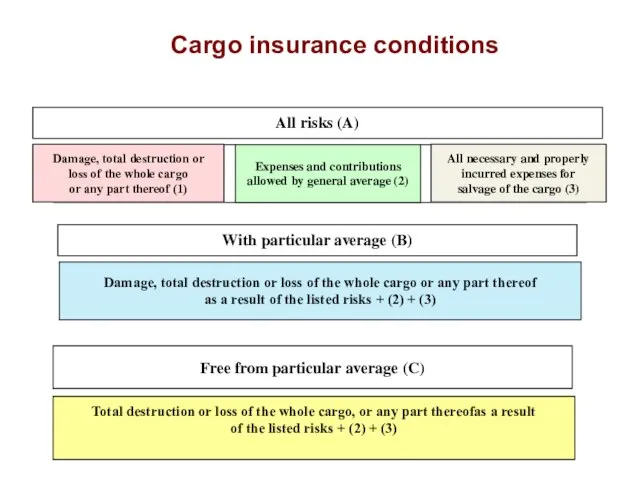

Слайд 43Cargo insurance conditions

All risks (A)

Damage, total destruction or

loss of the whole

Cargo insurance conditions

All risks (A)

Damage, total destruction or

loss of the whole

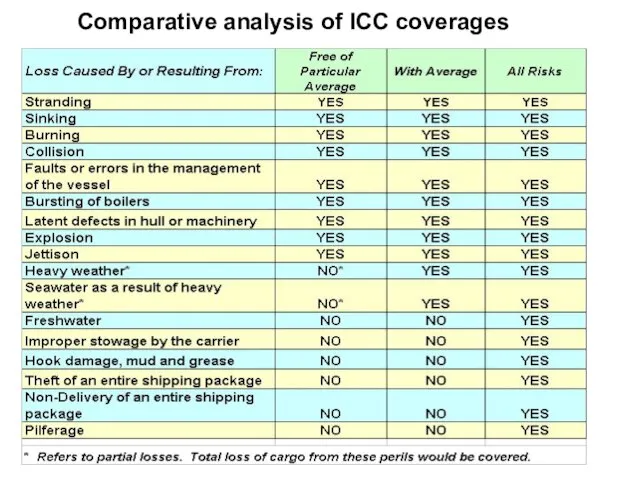

Слайд 44Comparative analysis of ICC coverages

Comparative analysis of ICC coverages

Слайд 45Carrier’s liability insurance

Carrier’s liability insurance

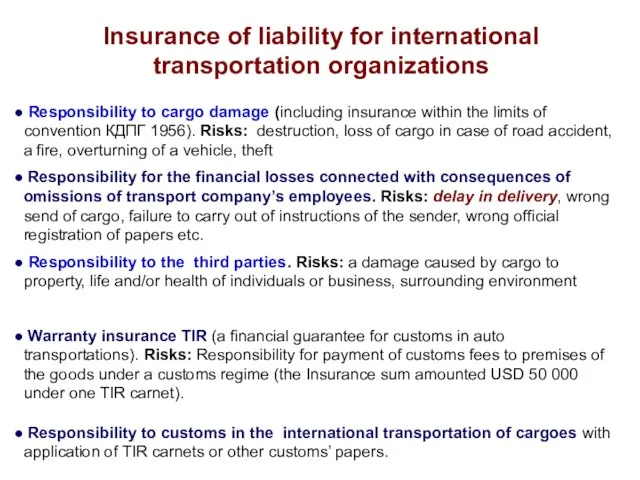

Слайд 46Insurance of liability for international transportation organizations

Responsibility to cargo damage (including

Insurance of liability for international transportation organizations

Responsibility to cargo damage (including

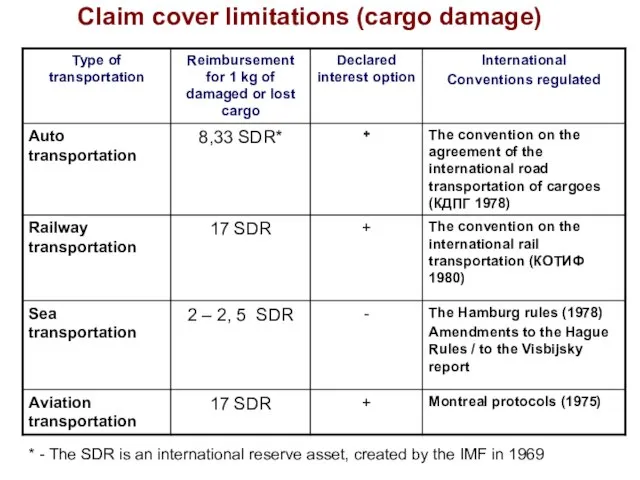

Слайд 47Claim cover limitations (cargo damage)

* - The SDR is an international reserve

Claim cover limitations (cargo damage)

* - The SDR is an international reserve

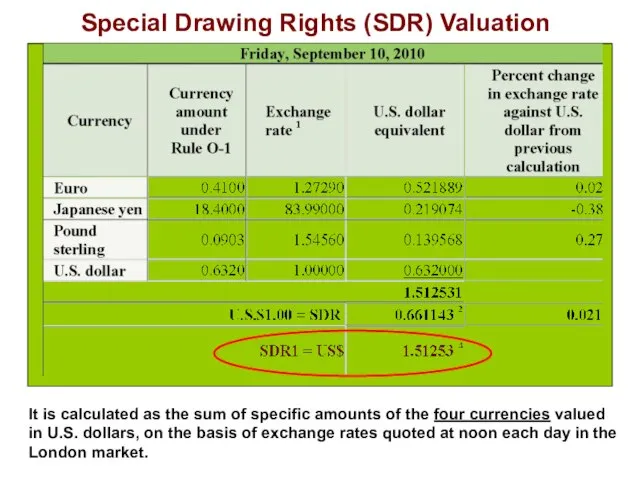

Слайд 48Special Drawing Rights (SDR) Valuation

It is calculated as the sum of specific

Special Drawing Rights (SDR) Valuation

It is calculated as the sum of specific

Слайд 49Specific of handling claims

Specific of handling claims

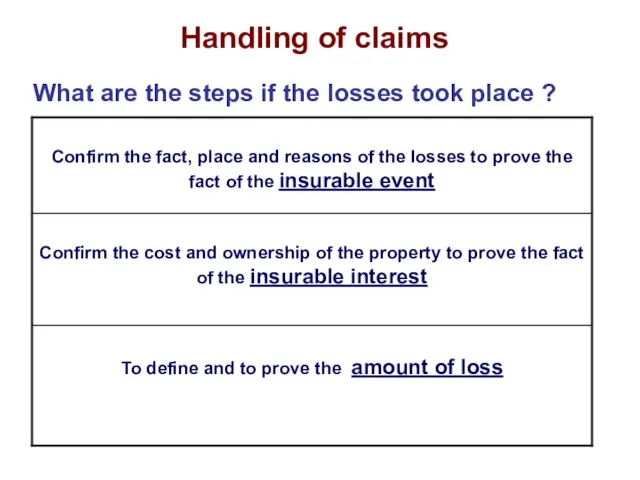

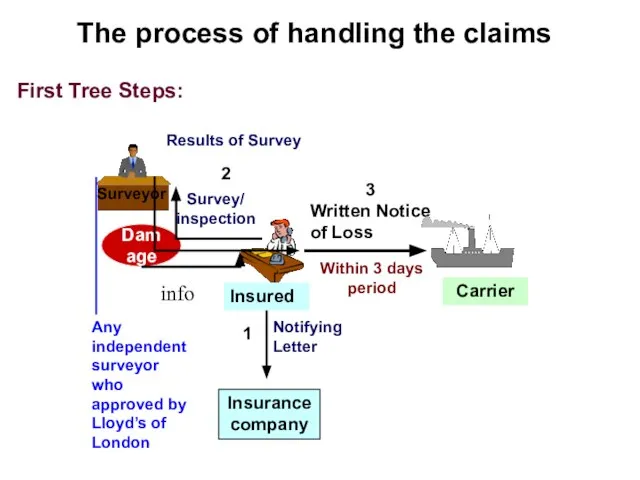

Слайд 50Handling of claims

What are the steps if the losses took place ?

Handling of claims

What are the steps if the losses took place ?

Слайд 51The process of handling the claims

Damage

Insured

info

Written Notice of Loss

Carrier

Survey/ inspection

Results of Survey

Within

The process of handling the claims

Damage

Insured

info

Written Notice of Loss

Carrier

Survey/ inspection

Results of Survey

Within

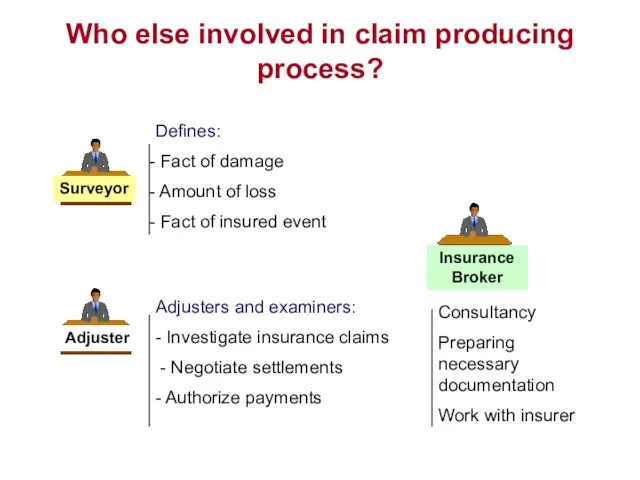

Слайд 52Who else involved in claim producing process?

Surveyor

Adjuster

Defines:

Fact of damage

Amount of

Who else involved in claim producing process?

Surveyor

Adjuster

Defines:

Fact of damage

Amount of

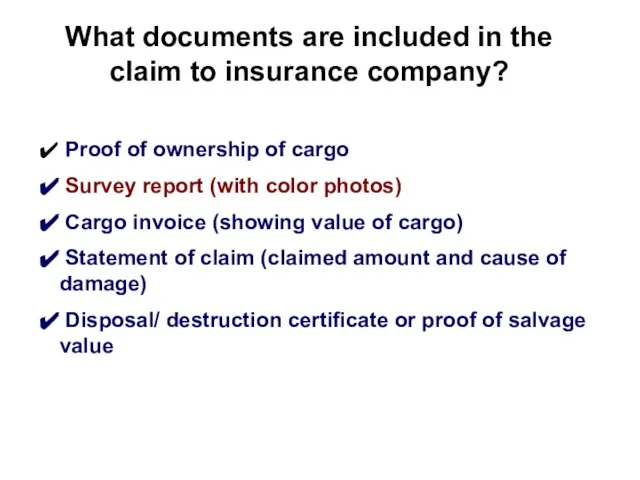

Слайд 53What documents are included in the claim to insurance company?

Proof of

What documents are included in the claim to insurance company?

Proof of

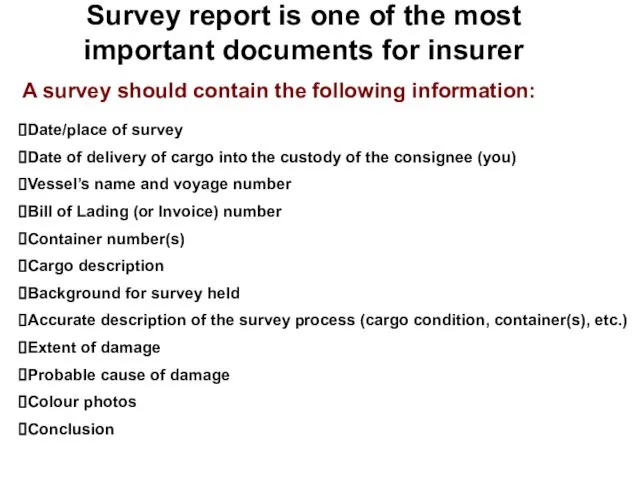

Слайд 54Survey report is one of the most important documents for insurer

A survey

Survey report is one of the most important documents for insurer

A survey

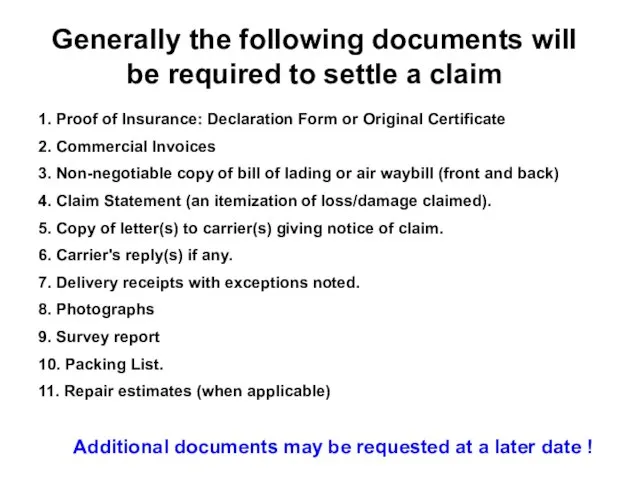

Слайд 55Generally the following documents will be required to settle a claim

1. Proof

Generally the following documents will be required to settle a claim

1. Proof

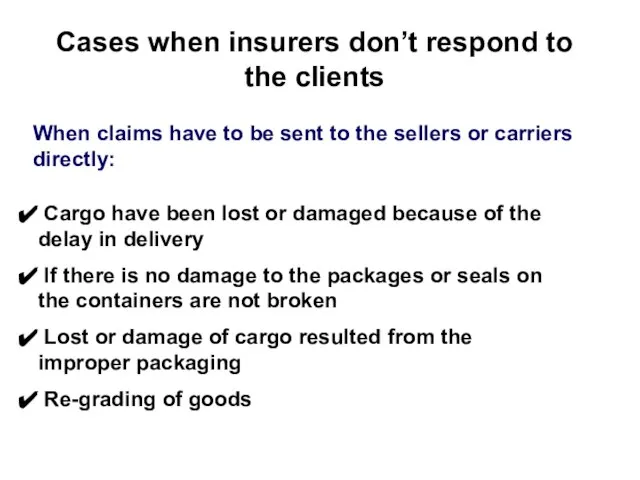

Слайд 56Cases when insurers don’t respond to the clients

When claims have to be

Cases when insurers don’t respond to the clients

When claims have to be

Слайд 573. Insurance

of international credits and investments

3. Insurance

of international credits and investments

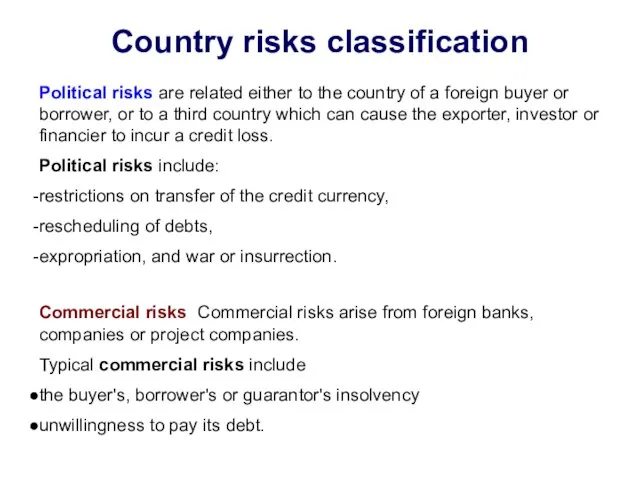

Слайд 58Country risks classification

Political risks are related either to the country of a

Country risks classification

Political risks are related either to the country of a

Слайд 59Political risks

Political risk may materialise as the consequence of a long course

Political risks

Political risk may materialise as the consequence of a long course

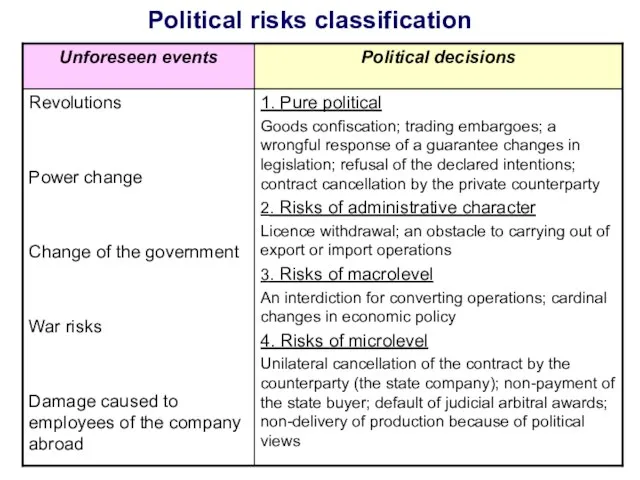

Слайд 60Political risks classification

Political risks classification

Слайд 61Risk management for political risks

Internal techniques:

Decreasing overall risk exposure (choice of country

Risk management for political risks

Internal techniques:

Decreasing overall risk exposure (choice of country

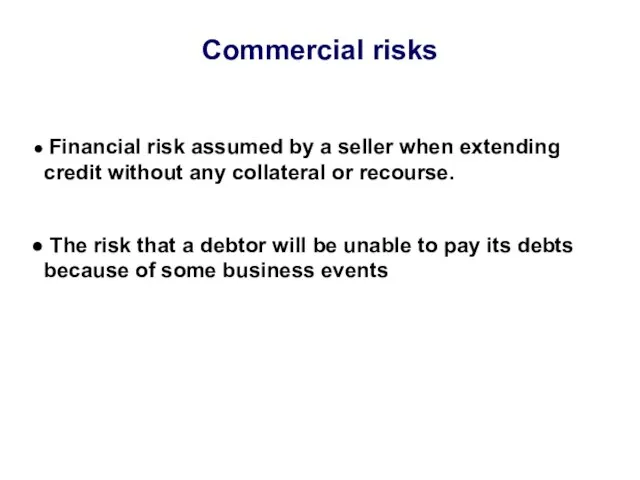

Слайд 62Commercial risks

Financial risk assumed by a seller when extending credit without

Commercial risks

Financial risk assumed by a seller when extending credit without

Слайд 63Guarantees offered to exporter in the export/import operations

Credit Risk Guarantee provides the

Guarantees offered to exporter in the export/import operations

Credit Risk Guarantee provides the

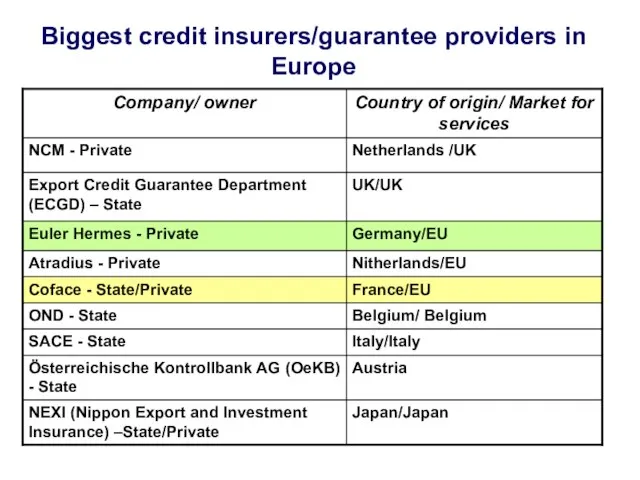

Слайд 64Biggest credit insurers/guarantee providers in Europe

Biggest credit insurers/guarantee providers in Europe

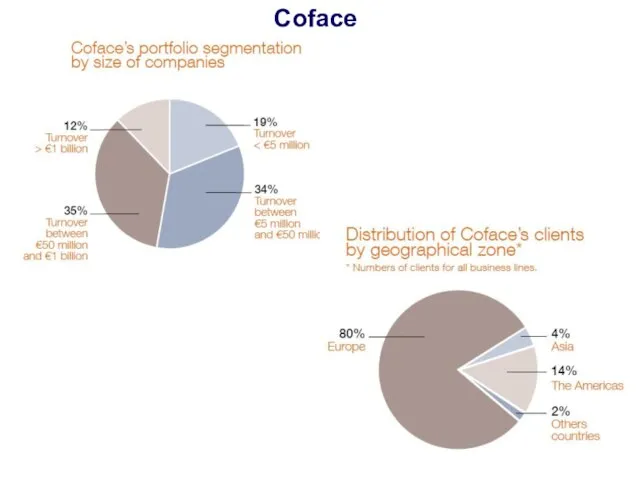

Слайд 65Coface

Coface

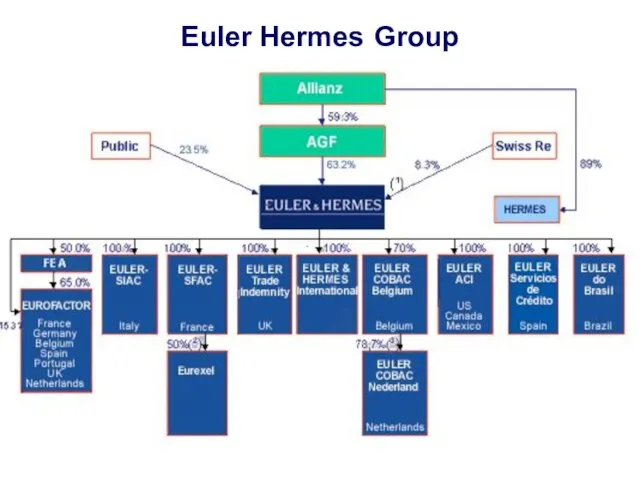

Слайд 66Euler Hermes Group

Euler Hermes Group

Слайд 67Guarantee Services

Guarantees are issued for clients in respect of their contractual or

Guarantee Services

Guarantees are issued for clients in respect of their contractual or

Слайд 68Guarantee Premiums

Short-term (repayment period less than 2 years) Buyer Credit and Credit

Guarantee Premiums

Short-term (repayment period less than 2 years) Buyer Credit and Credit

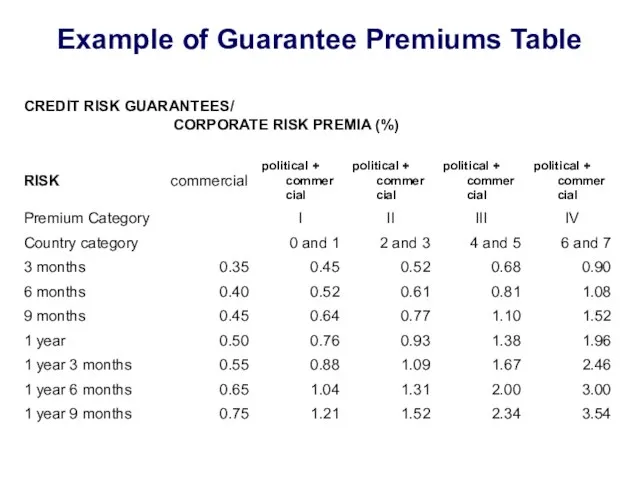

Слайд 69Example of Guarantee Premiums Table

Example of Guarantee Premiums Table

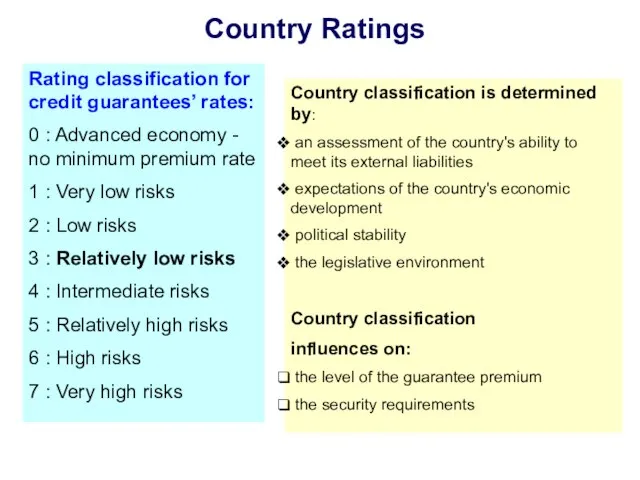

Слайд 70Country Ratings

Rating classification for credit guarantees’ rates:

0 : Advanced economy - no

Country Ratings

Rating classification for credit guarantees’ rates:

0 : Advanced economy - no

Слайд 71Credit rating agencies

Business Environmental Risk Intelligence (BERI)

Frost and Sullivan (Index WPRF –

Credit rating agencies

Business Environmental Risk Intelligence (BERI)

Frost and Sullivan (Index WPRF –

Слайд 72Credit Insurance

Credit Insurance

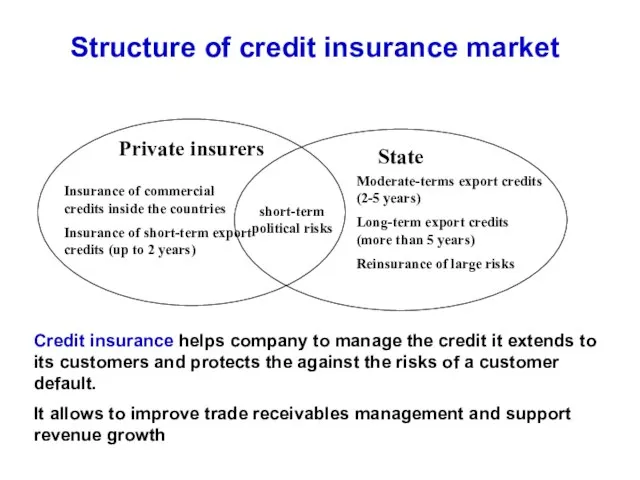

Слайд 73Structure of credit insurance market

Private insurers

State

Insurance of commercial credits inside the countries

Insurance

Structure of credit insurance market

Private insurers

State

Insurance of commercial credits inside the countries

Insurance

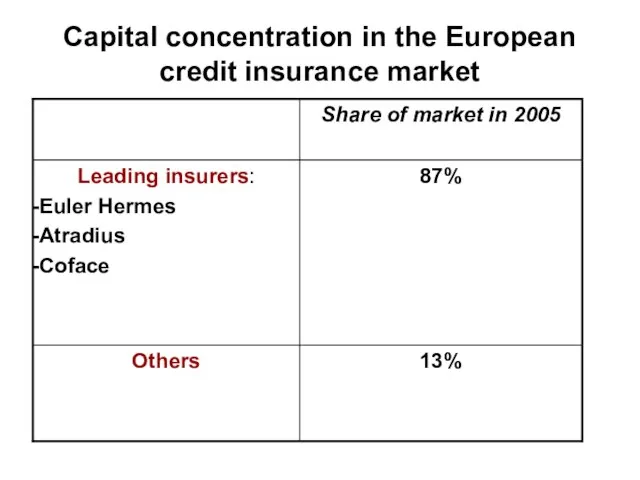

Слайд 74Capital concentration in the European credit insurance market

Capital concentration in the European credit insurance market

Слайд 75Commercial insurance companies, operating on the export credit insurance market

Lloyds of London

Commercial insurance companies, operating on the export credit insurance market

Lloyds of London

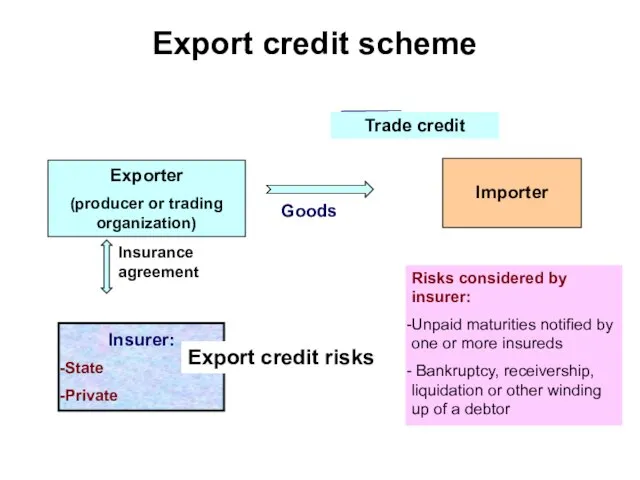

Слайд 76Export credit scheme

Risks considered by insurer:

Unpaid maturities notified by one or more

Export credit scheme

Risks considered by insurer:

Unpaid maturities notified by one or more

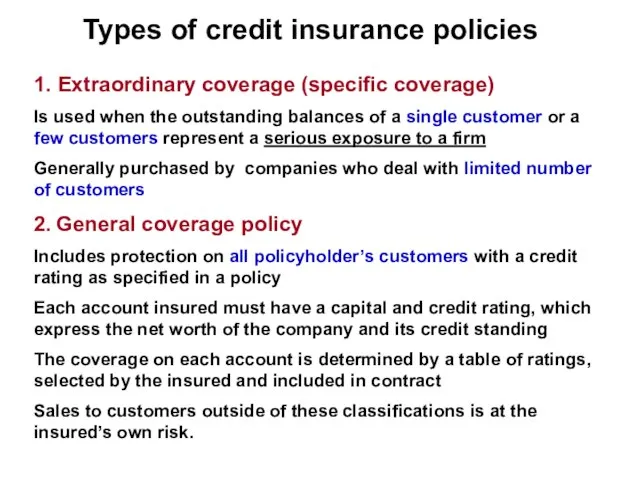

Слайд 77Types of credit insurance policies

1. Extraordinary coverage (specific coverage)

Is used when the

Types of credit insurance policies

1. Extraordinary coverage (specific coverage)

Is used when the

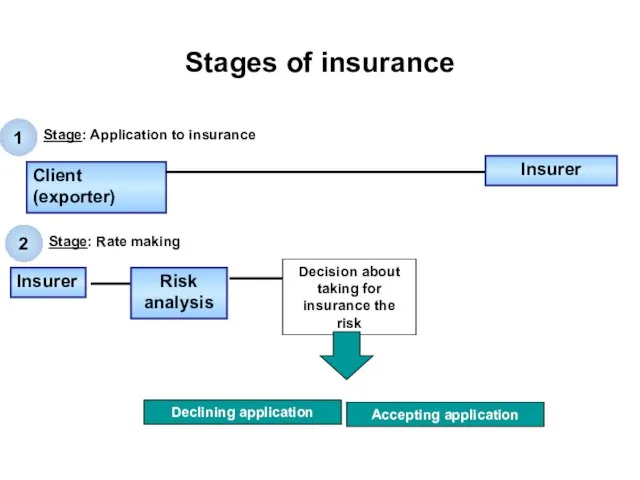

Слайд 78Stages of insurance

Stages of insurance

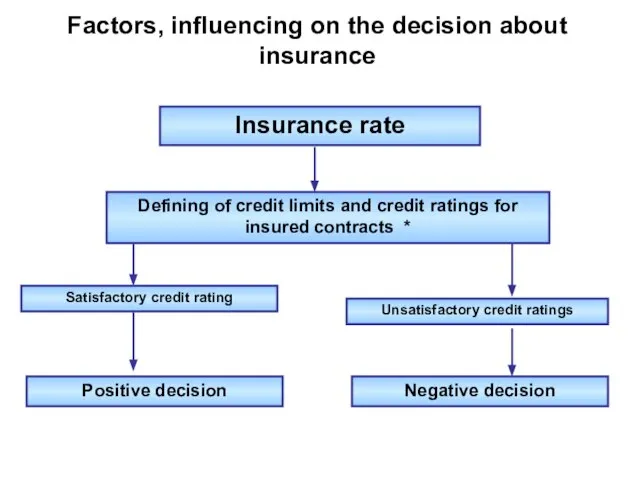

Слайд 79Factors, influencing on the decision about insurance

Factors, influencing on the decision about insurance

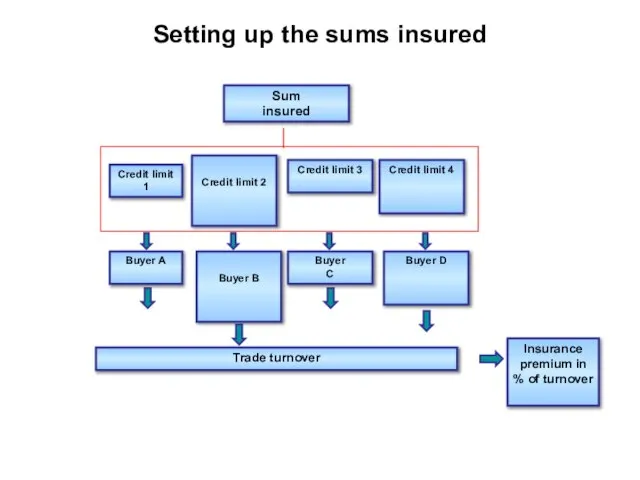

Слайд 80Credit limit 2

Credit limit 1

Credit limit 3

Credit limit 4

Buyer B

Buyer А

Buyer

C

Buyer

Credit limit 1

Credit limit 3

Credit limit 4

Buyer B

Buyer А

Buyer

C

Buyer

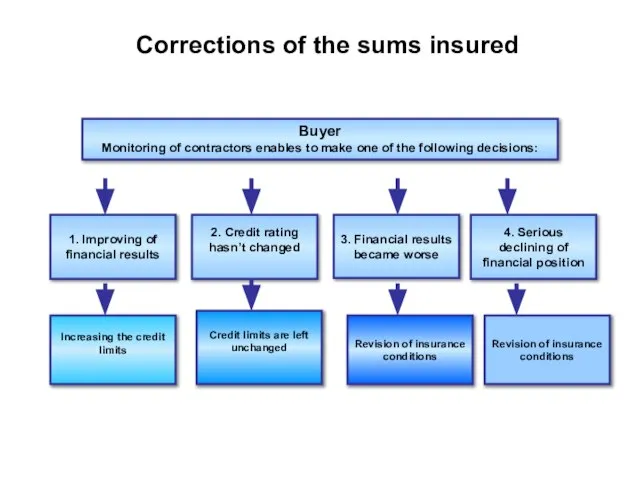

Слайд 813. Financial results became worse

4. Serious declining of financial position

Buyer

Monitoring of contractors

4. Serious declining of financial position

Buyer

Monitoring of contractors

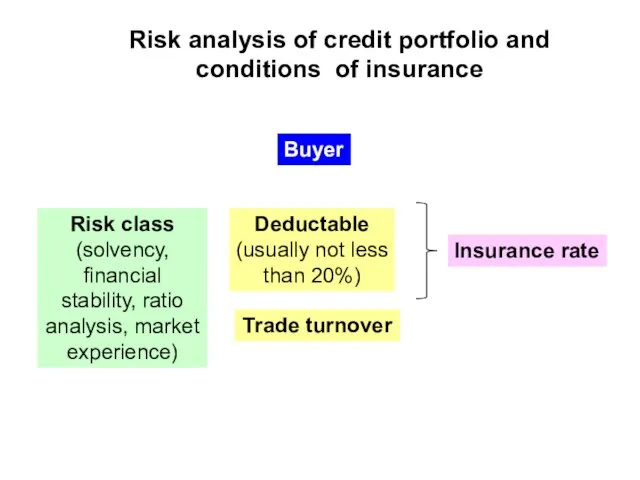

Слайд 82Risk analysis of credit portfolio and conditions of insurance

Buyer

Risk class (solvency,

Risk analysis of credit portfolio and conditions of insurance

Buyer

Risk class (solvency,

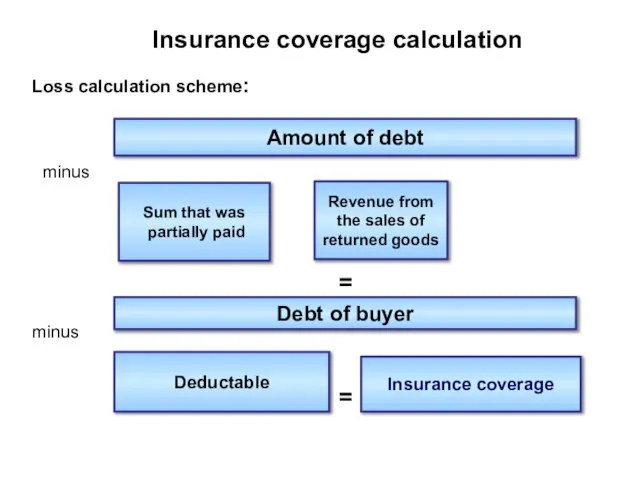

Слайд 83Amount of debt

minus

Sum that was

partially paid

Revenue from

the sales of

returned

Amount of debt

minus

Sum that was

partially paid

Revenue from

the sales of

returned

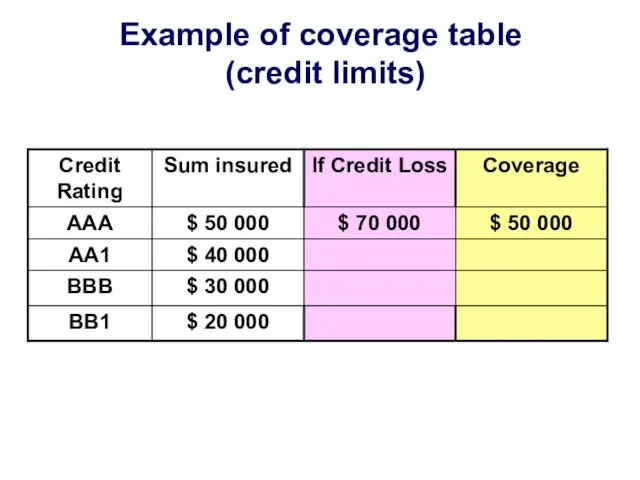

Слайд 84Example of coverage table

(credit limits)

Example of coverage table

(credit limits)

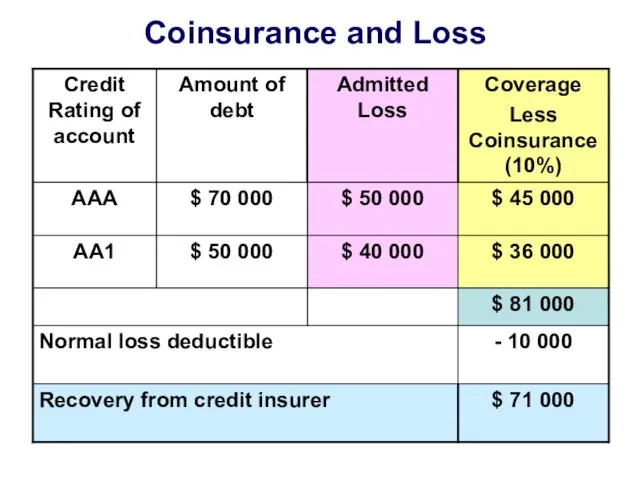

Слайд 85Coinsurance and Loss

Coinsurance and Loss

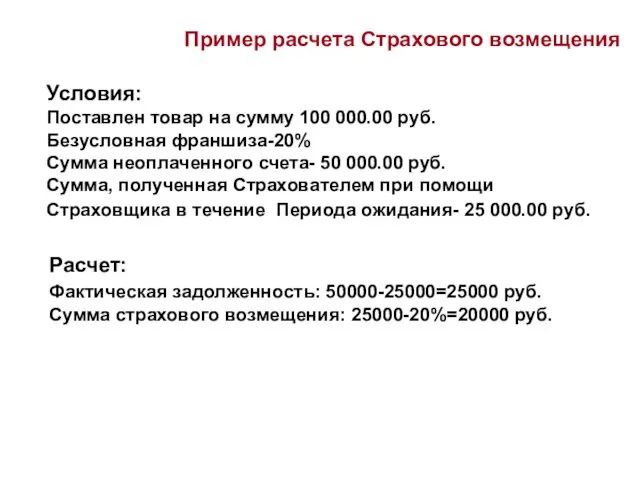

Слайд 86Условия:

Поставлен товар на сумму 100 000.00 руб.

Безусловная франшиза-20%

Сумма неоплаченного счета- 50 000.00

Условия:

Поставлен товар на сумму 100 000.00 руб.

Безусловная франшиза-20%

Сумма неоплаченного счета- 50 000.00

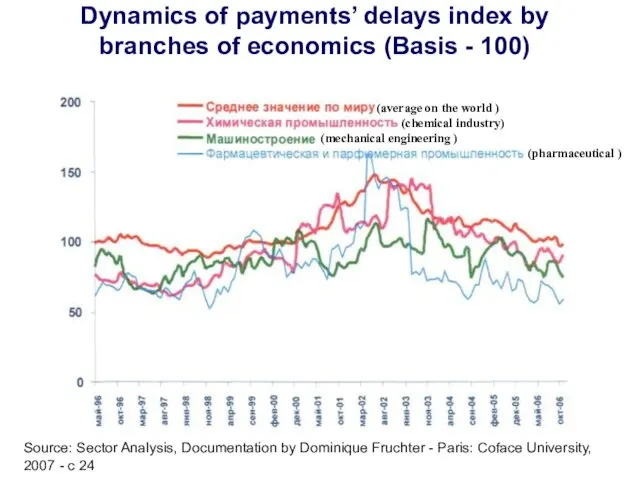

Слайд 87Dynamics of payments’ delays index by branches of economics (Basis - 100)

(chemical

Dynamics of payments’ delays index by branches of economics (Basis - 100)

(chemical

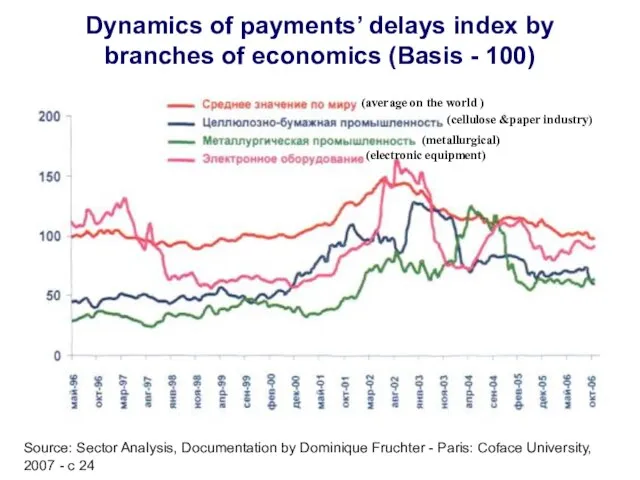

Слайд 88Dynamics of payments’ delays index by branches of economics (Basis - 100)

(average

Dynamics of payments’ delays index by branches of economics (Basis - 100)

(average

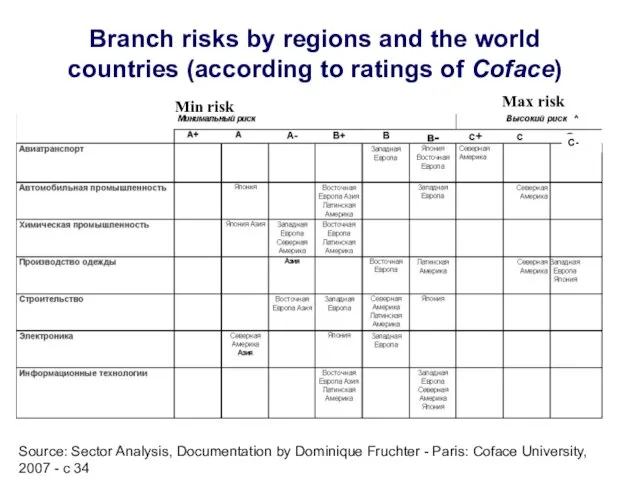

Слайд 89Branch risks by regions and the world countries (according to ratings of

Branch risks by regions and the world countries (according to ratings of

Слайд 90International investments’ insurance agencies

Multilateral Investments Guaranteeing Agency (MIGA) - a member of

International investments’ insurance agencies

Multilateral Investments Guaranteeing Agency (MIGA) - a member of

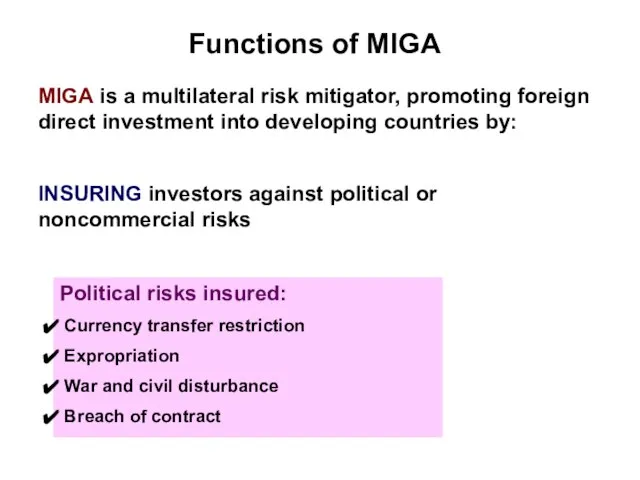

Слайд 91Functions of MIGA

Political risks insured:

Currency transfer restriction

Expropriation

War

Functions of MIGA

Political risks insured:

Currency transfer restriction

Expropriation

War

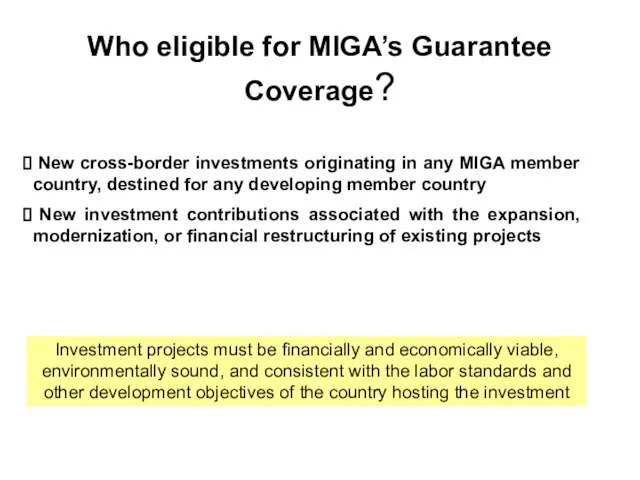

Слайд 92Who eligible for MIGA’s Guarantee Coverage?

New cross-border investments originating in any

Who eligible for MIGA’s Guarantee Coverage?

New cross-border investments originating in any

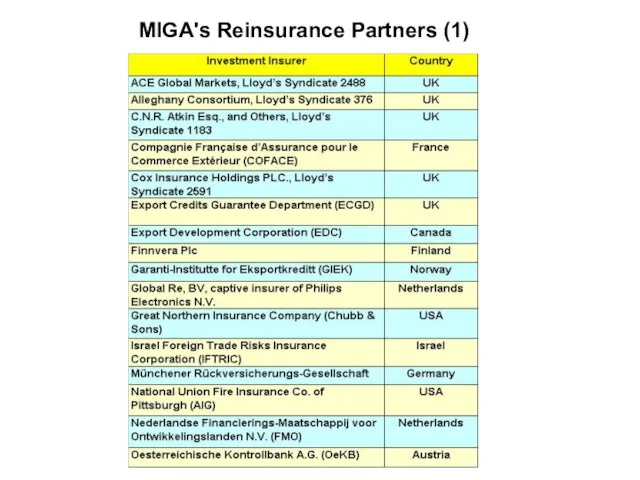

Слайд 93MIGA's Reinsurance Partners (1)

MIGA's Reinsurance Partners (1)

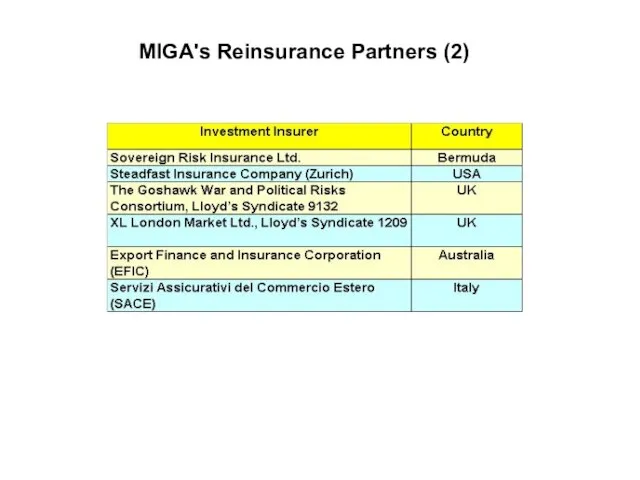

Слайд 94MIGA's Reinsurance Partners (2)

MIGA's Reinsurance Partners (2)

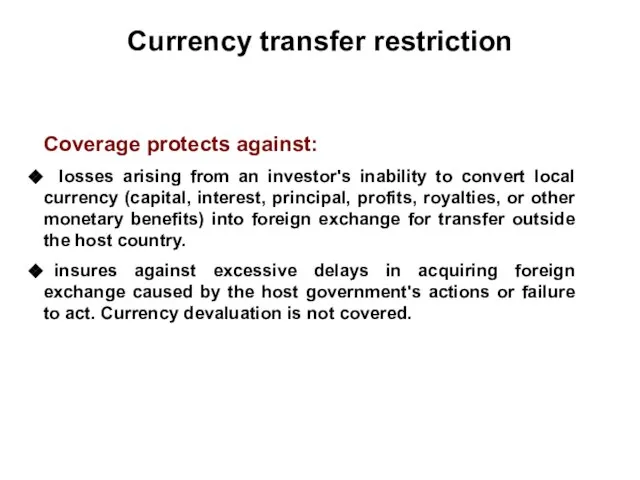

Слайд 95Currency transfer restriction

Coverage protects against:

losses arising from an investor's inability to

Currency transfer restriction

Coverage protects against:

losses arising from an investor's inability to

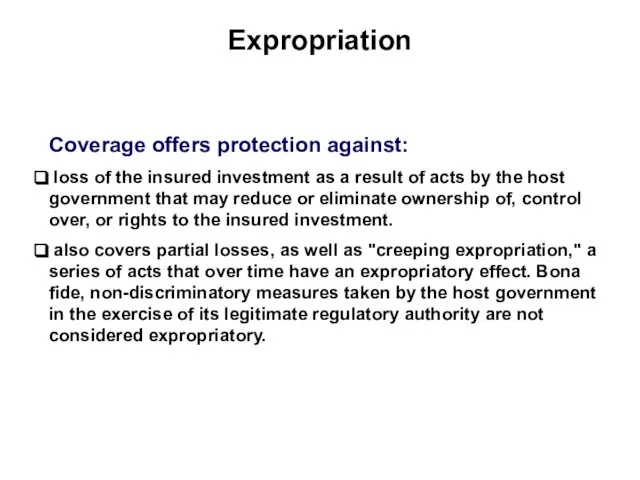

Слайд 96Expropriation

Coverage offers protection against:

loss of the insured investment as a result

Expropriation

Coverage offers protection against:

loss of the insured investment as a result

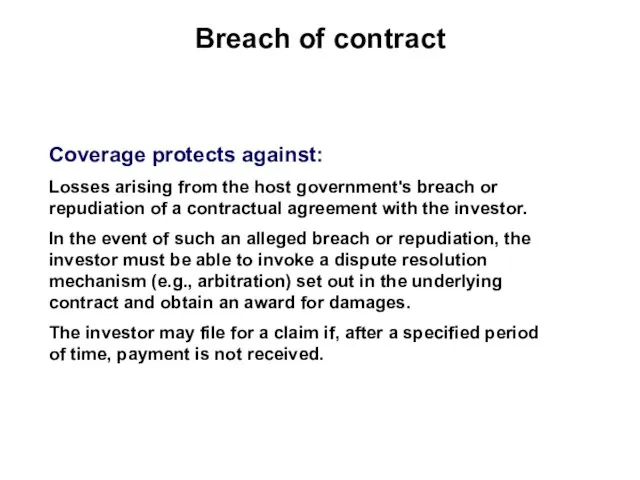

Слайд 97Breach of contract

Coverage protects against:

Losses arising from the host government's breach or

Breach of contract

Coverage protects against:

Losses arising from the host government's breach or

Совесть - голос Бога в сердце человека

Совесть - голос Бога в сердце человека Роскошные образы арабского мира. Образ природы

Роскошные образы арабского мира. Образ природы Західноукраїнські художники

Західноукраїнські художники Методическое Объединение

Методическое Объединение Берегите зрение (Гимнастика для глаз)

Берегите зрение (Гимнастика для глаз) Планетарии – центры популяризации знаний о Вселенной

Планетарии – центры популяризации знаний о Вселенной Дизайн в промышленном производстве

Дизайн в промышленном производстве Абрамович Роман Аркадьевич

Абрамович Роман Аркадьевич Конституция и законы

Конституция и законы Что я знаю об этом ?

Что я знаю об этом ? Кадастровая стоимость как база для расчета арендной платы за землю

Кадастровая стоимость как база для расчета арендной платы за землю Современное состояние и перспективы развития быстроразвертывыаемых комплексов охраны ВС РФ

Современное состояние и перспективы развития быстроразвертывыаемых комплексов охраны ВС РФ Презентация на тему Обучение правилам чтения

Презентация на тему Обучение правилам чтения  Социальный прогресс и развитие общества

Социальный прогресс и развитие общества О внесении изменений в региональный базисный учебный план

О внесении изменений в региональный базисный учебный план Интегрированная распределенная система информационного обмена результатами тестирования

Интегрированная распределенная система информационного обмена результатами тестирования Монополь в квантовой меxанике: армянский след Совместные работы с В. Тер-Антоняном 1994-1997гг и иx развитие Армен Нерсесян

Монополь в квантовой меxанике: армянский след Совместные работы с В. Тер-Антоняном 1994-1997гг и иx развитие Армен Нерсесян Функции DeVita AP

Функции DeVita AP Основные принципы тренировочного процесса

Основные принципы тренировочного процесса Общественное движение в России в 30 - 50 гг. 19 века

Общественное движение в России в 30 - 50 гг. 19 века Человеческий мозг

Человеческий мозг Возрастные особенности памяти у школьников начальных классов Борковской средней общеобразовательной школы

Возрастные особенности памяти у школьников начальных классов Борковской средней общеобразовательной школы Подростковый алкоголизм

Подростковый алкоголизм День Конституции Российской Федерации

День Конституции Российской Федерации Опыт региона Балтийского моря в возрождении и инновационном развитии городов и регионов

Опыт региона Балтийского моря в возрождении и инновационном развитии городов и регионов Вода – уникальное вещество нашей планеты

Вода – уникальное вещество нашей планеты Социально-психологический климат в организации: понятие, факторы формирования

Социально-психологический климат в организации: понятие, факторы формирования Я - ученик 21 века

Я - ученик 21 века