- International Bond Market

Содержание

- 2. Plan: Structure of the Market Types of Instruments Bonds credit ratings Eurobond market practice http://www.eurobonds.info/

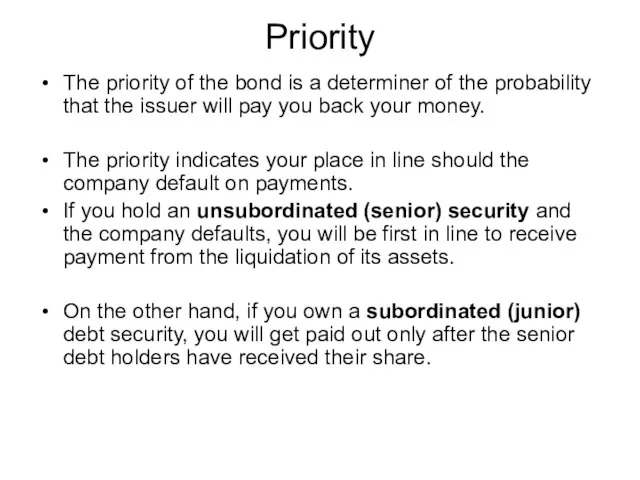

- 4. Priority The priority of the bond is a determiner of the probability that the issuer will

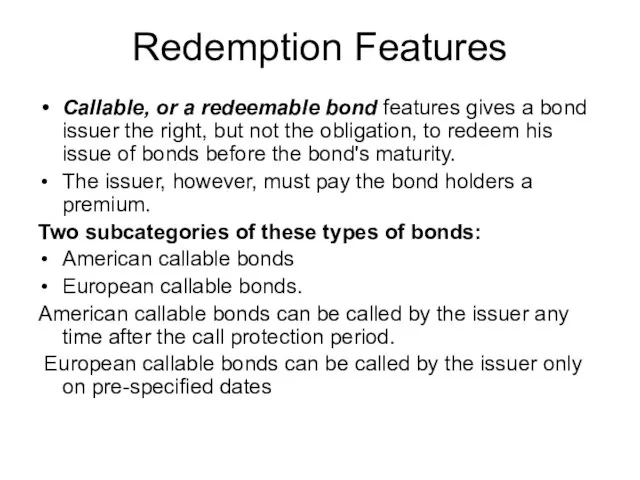

- 5. Redemption Features Callable, or a redeemable bond features gives a bond issuer the right, but not

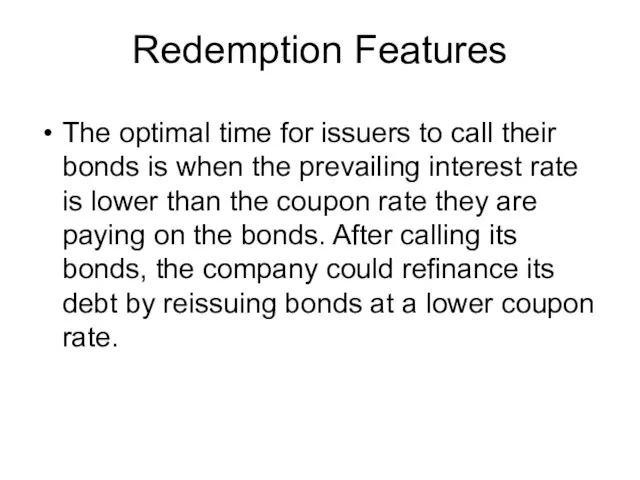

- 6. Redemption Features The optimal time for issuers to call their bonds is when the prevailing interest

- 7. Redemption Features Convertible bonds give bondholders the right but not the obligation to convert their bonds

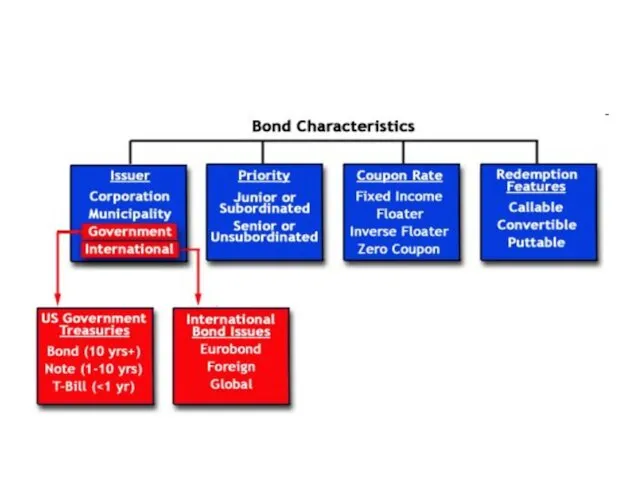

- 8. Structure of the Market

- 9. Foreign bond A foreign bond - a bond that is issued in a domestic market by

- 10. Foreign bonds Foreign bonds are regulated by the domestic market authorities and are usually given nicknames

- 11. Foreign bonds Yankee Bond - A bond denominated in U.S. dollars that is publicly issued in

- 12. Foreign bonds Kangaroo Bond (Matilda bond) - a type of foreign bond that is issued in

- 13. Foreign bonds Matador Bond – a term used to identify a foreign bond issued in Spain

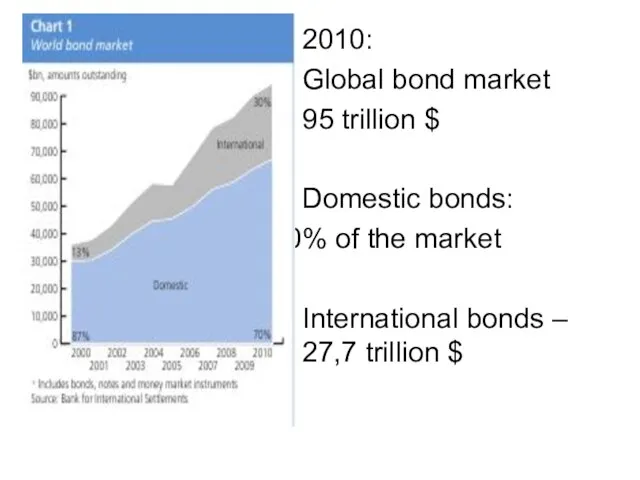

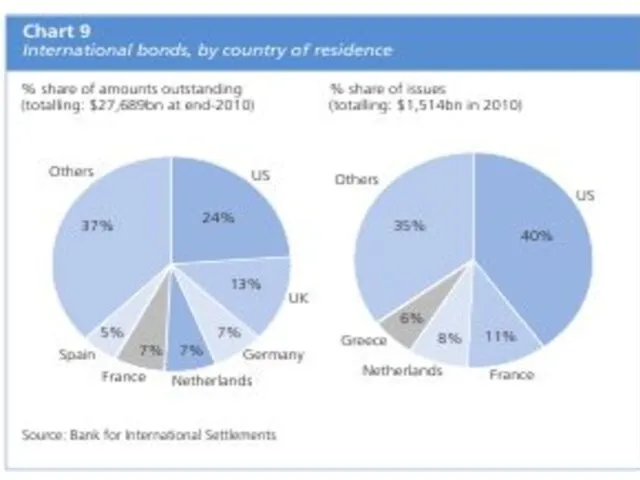

- 14. 2010: Global bond market 95 trillion $ Domestic bonds: % of the market International bonds –

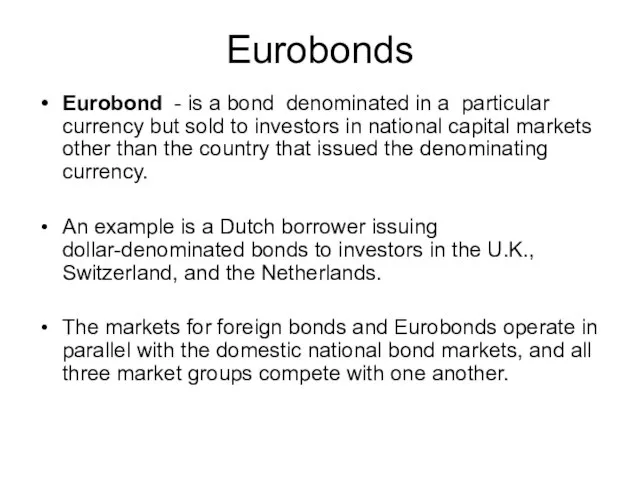

- 16. Eurobonds Eurobond - is a bond denominated in a particular currency but sold to investors in

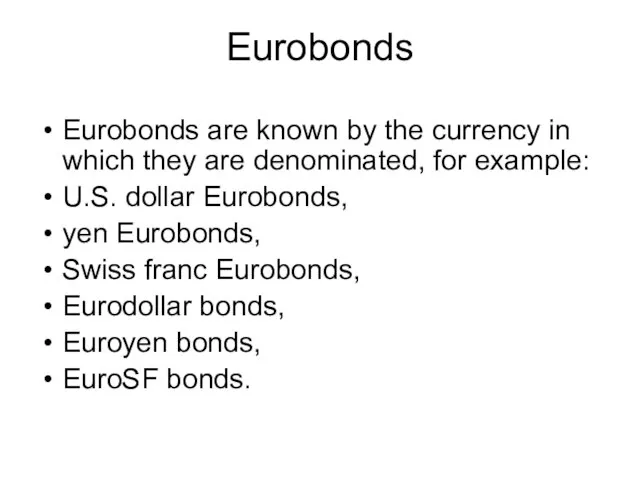

- 17. Eurobonds Eurobonds are known by the currency in which they are denominated, for example: U.S. dollar

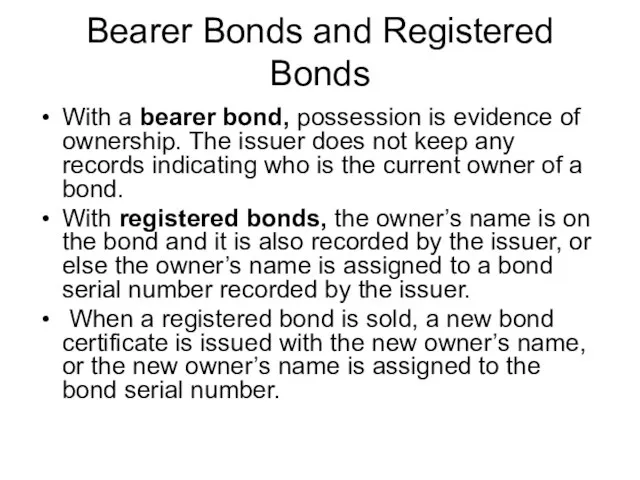

- 18. Bearer Bonds and Registered Bonds With a bearer bond, possession is evidence of ownership. The issuer

- 19. Eurobonds are usually bearer bonds. U.S. security regulations require Yankee bonds and U.S. corporate bonds sold

- 20. Recent changes in U.S. security regulations Rule 415, which the SEC instituted in 1982 to allow

- 21. Global Bonds A global bond issue is a very large international bond offering by a single

- 22. Largest corporate global bond issue $14.6 billion Deutsche Telekom multicurrency offering. The issue includes three U.S.dollar

- 23. 2. Types of Instruments

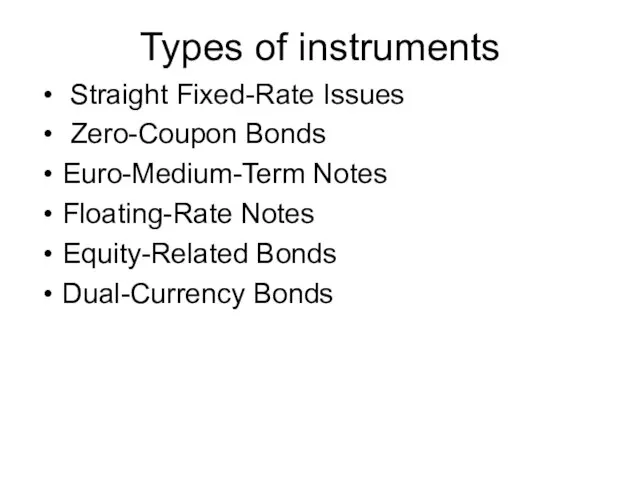

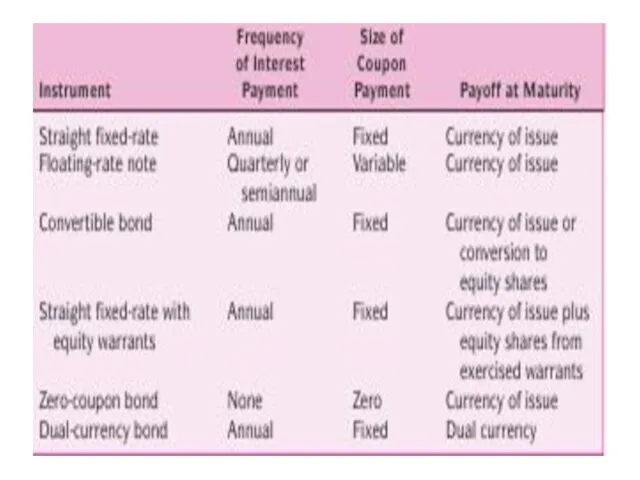

- 24. Types of instruments Straight Fixed-Rate Issues Zero-Coupon Bonds Euro-Medium-Term Notes Floating-Rate Notes Equity-Related Bonds Dual-Currency Bonds

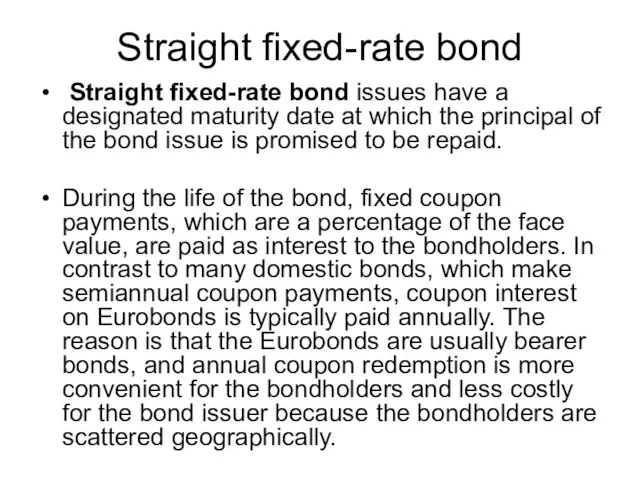

- 25. Straight fixed-rate bond Straight fixed-rate bond issues have a designated maturity date at which the principal

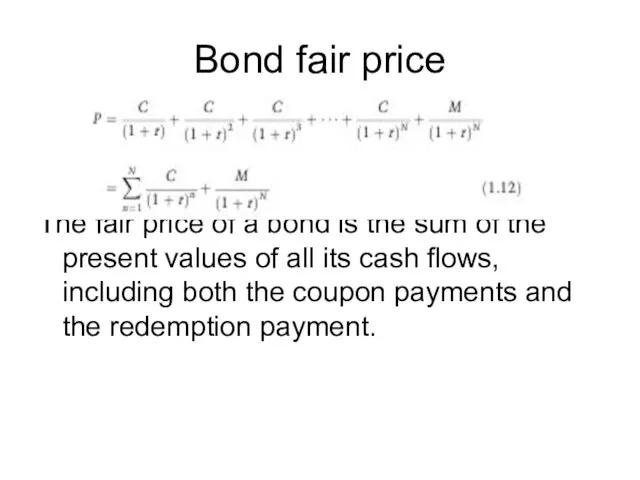

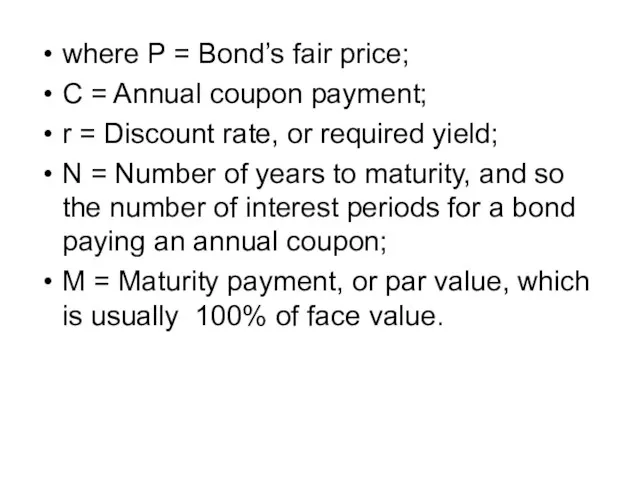

- 26. Bond fair price The fair price of a bond is the sum of the present values

- 27. where P = Bond’s fair price; C = Annual coupon payment; r = Discount rate, or

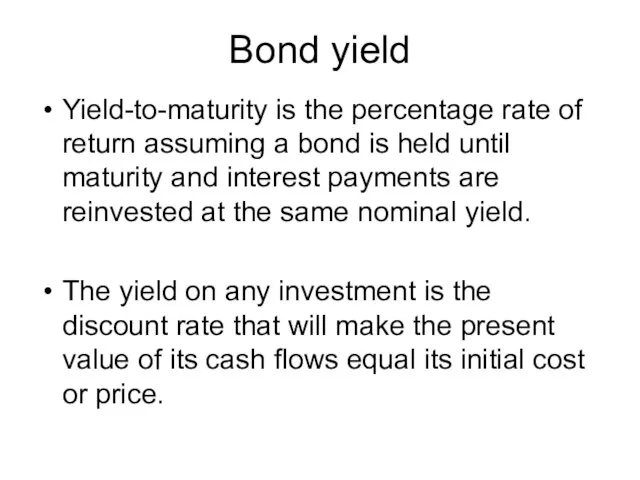

- 28. Bond yield Yield-to-maturity is the percentage rate of return assuming a bond is held until maturity

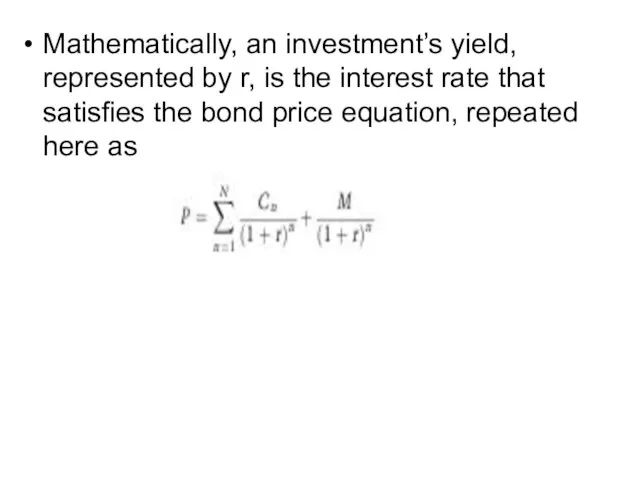

- 29. Mathematically, an investment’s yield, represented by r, is the interest rate that satisfies the bond price

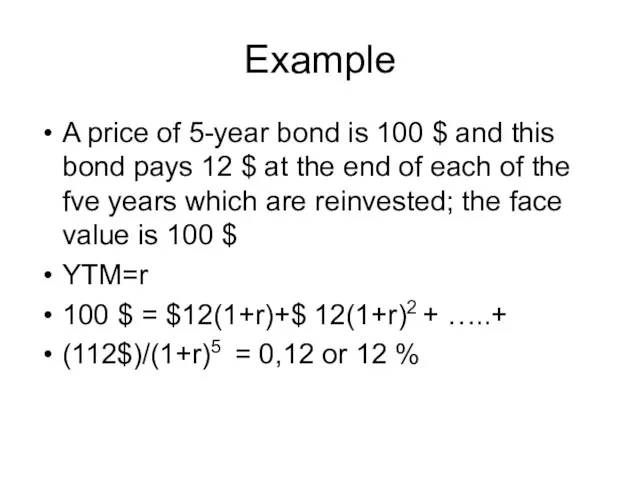

- 30. Example A price of 5-year bond is 100 $ and this bond pays 12 $ at

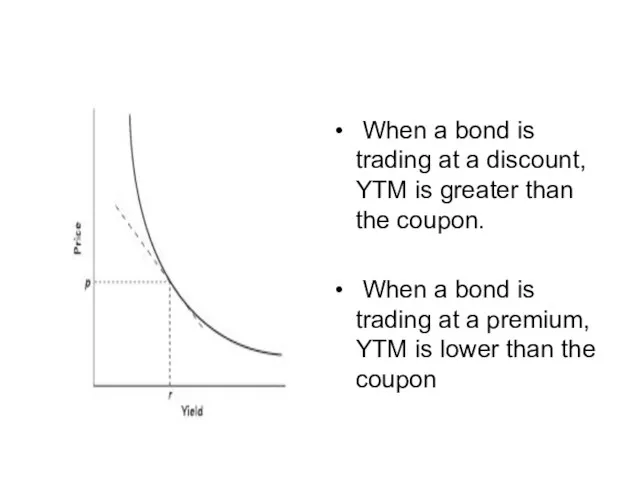

- 31. When a bond is trading at a discount, YTM is greater than the coupon. When a

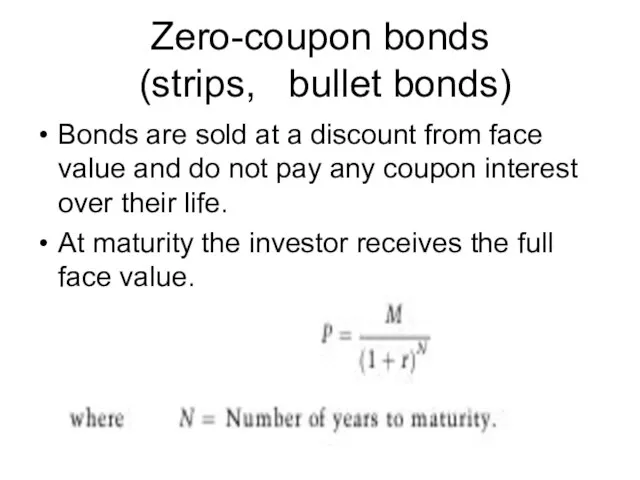

- 32. Zero-coupon bonds (strips, bullet bonds) Bonds are sold at a discount from face value and do

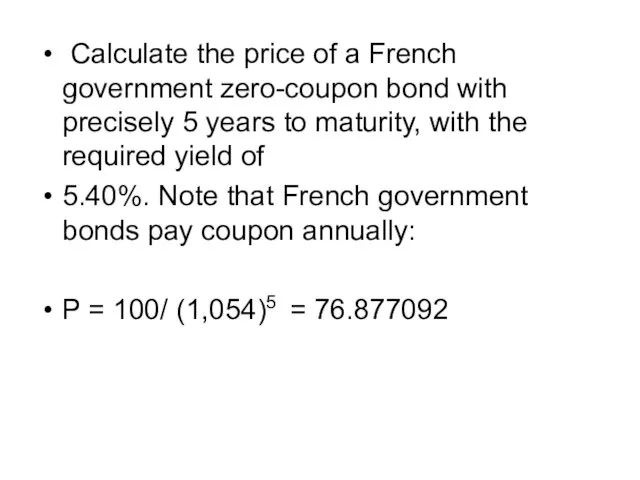

- 33. Calculate the price of a French government zero-coupon bond with precisely 5 years to maturity, with

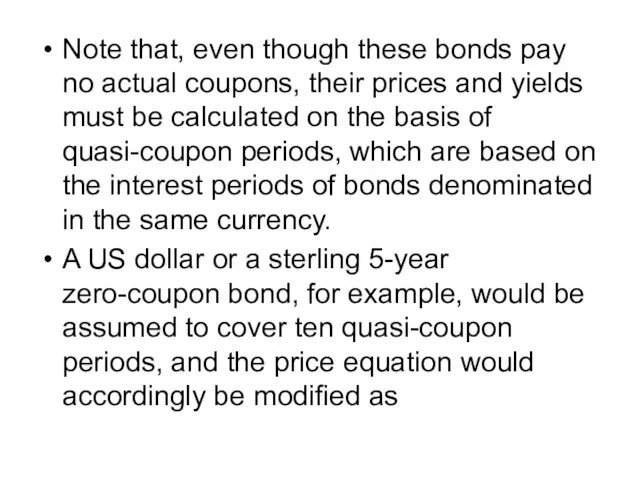

- 34. Note that, even though these bonds pay no actual coupons, their prices and yields must be

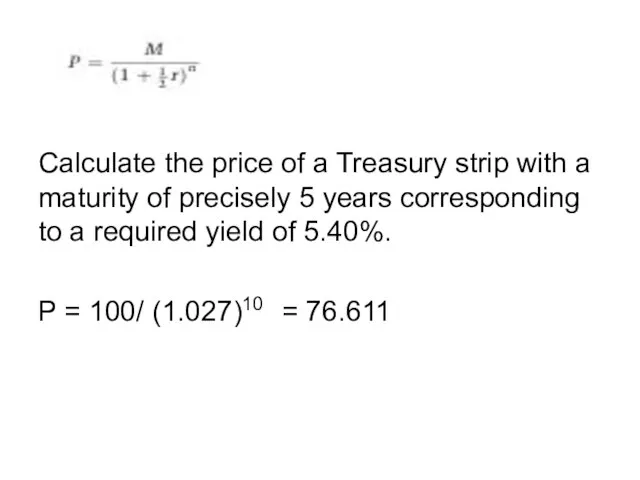

- 35. Calculate the price of a Treasury strip with a maturity of precisely 5 years corresponding to

- 36. Calculate the price of a Treasury strip with a maturity of precisely 5 years corresponding to

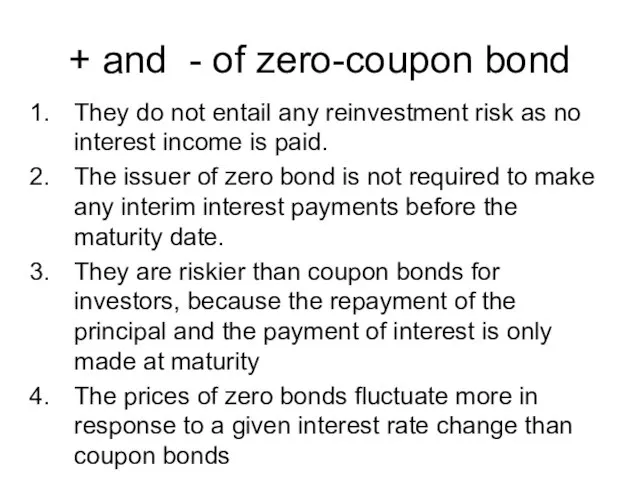

- 37. + and - of zero-coupon bond They do not entail any reinvestment risk as no interest

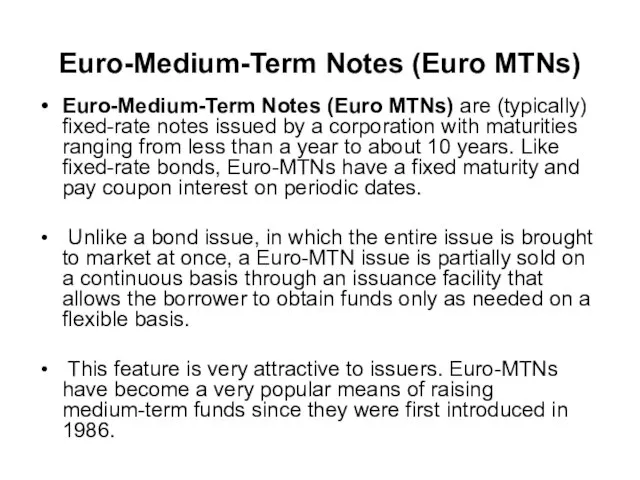

- 38. Euro-Medium-Term Notes (Euro MTNs) Euro-Medium-Term Notes (Euro MTNs) are (typically) fixed-rate notes issued by a corporation

- 39. Euro-Medium-Term Notes (Euro MTNs) EMTNs make it easier for issuers to enter into foreign markets for

- 40. Floating-Rate Notes (FRNs) A note with a variable interest rate. The adjustments to the interest rate

- 41. FRNs Additional features have been added to FRNs, including floors (the coupon cannot fall below a

- 42. Equity-related Bonds There are two types of equity-related bonds: convertible bonds bonds with equity Bonds warrants.

- 43. Equity-related Bonds Bonds with equity warrants can be viewed as straight fixed-rate bonds with the addition

- 44. Dual-currency bonds A dual-currency bond is a straight fixed-rate bond issued in one currency, say, Swiss

- 47. International Bond Market Credit Ratings Fitch IBCA, Moody’s Investors Service, Standard & Poor’s (S&P) www.fitchibca.com www.moodys.com

- 48. These three credit-rating organizations classify bond issues into categories based upon the creditworthiness of the borrower.

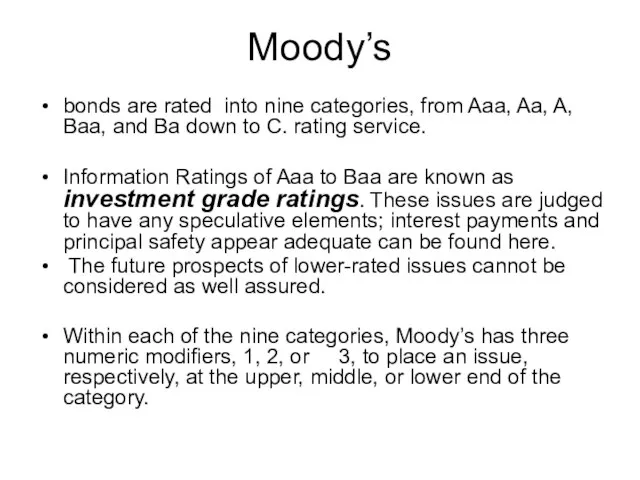

- 49. Moody’s bonds are rated into nine categories, from Aaa, Aa, A, Baa, and Ba down to

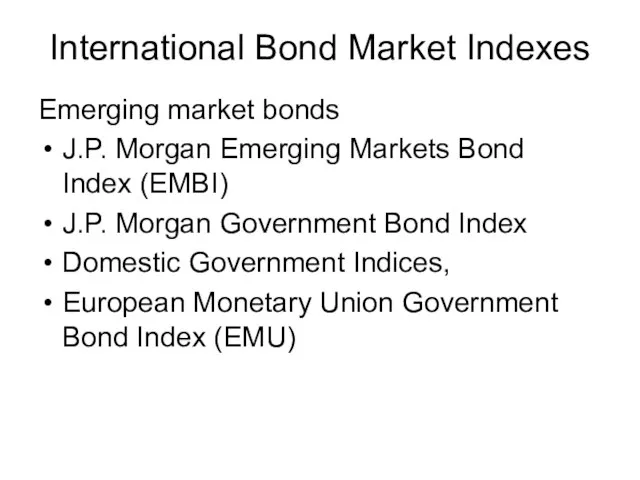

- 50. International Bond Market Indexes Emerging market bonds J.P. Morgan Emerging Markets Bond Index (EMBI) J.P. Morgan

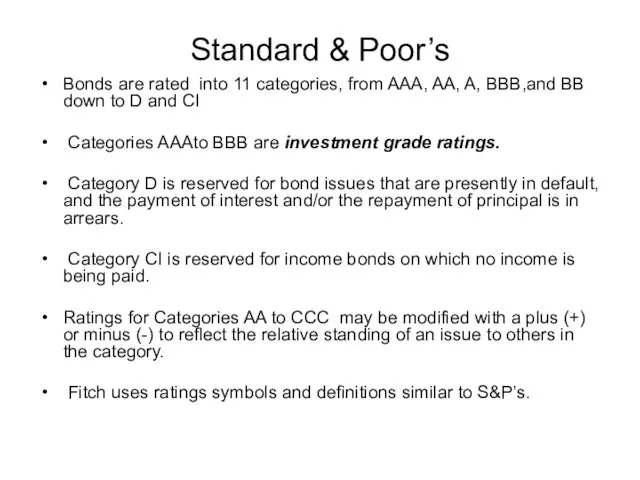

- 51. Standard & Poor’s Bonds are rated into 11 categories, from AAA, AA, A, BBB,and BB down

- 52. 4. Eurobond market practice

- 53. Eurobond market makers and dealers are members of the International Securities Market Association (ISMA), a self-regulatory

- 54. Euroclear Euroclear settles domestic and international securities transactions, covering bonds, equities, derivatives and investment funds. Euroclear

- 55. Supervision Incorporated in Belgium, Euroclear SA/NV is subject to the supervision of the Belgium Banking, Finance

- 56. Each clearing system has a group of depository banks that physically store bond certificates. Members of

- 57. (1) The clearing systems will finance up to 90 percent of the inventory that a Eurobond

- 58. Issuers of eurobond Domotechnika Donbass Resources Donbassenergo Donetsk City Donetsktelekom Dongorbank Donsnab-service

- 59. International portfolio strategies 1. Benchmark selection 2. Bond market selection 3.Sector selection/credit selection 4.Currency management

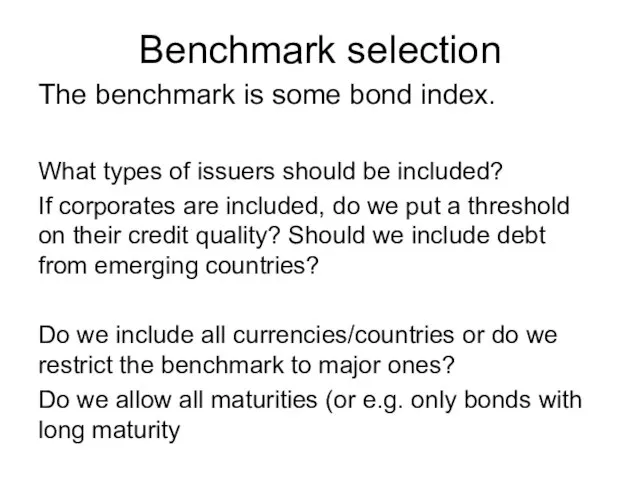

- 60. Benchmark selection The benchmark is some bond index. What types of issuers should be included? If

- 61. Bond market selection Take into account currency and interest rate forecast and volatility. Economic fundamentals: monetary

- 63. Скачать презентацию

Слайд 2Plan:

Structure of the Market

Types of Instruments

Bonds credit ratings

Eurobond market practice

http://www.eurobonds.info/

Plan:

Structure of the Market

Types of Instruments

Bonds credit ratings

Eurobond market practice

http://www.eurobonds.info/

Слайд 4Priority

The priority of the bond is a determiner of the probability

Priority

The priority of the bond is a determiner of the probability

Слайд 5Redemption Features

Callable, or a redeemable bond features gives a bond issuer the

Redemption Features

Callable, or a redeemable bond features gives a bond issuer the

Слайд 6Redemption Features

The optimal time for issuers to call their bonds is when

Redemption Features

The optimal time for issuers to call their bonds is when

Слайд 7Redemption Features

Convertible bonds give bondholders the right but not the obligation to

Redemption Features

Convertible bonds give bondholders the right but not the obligation to

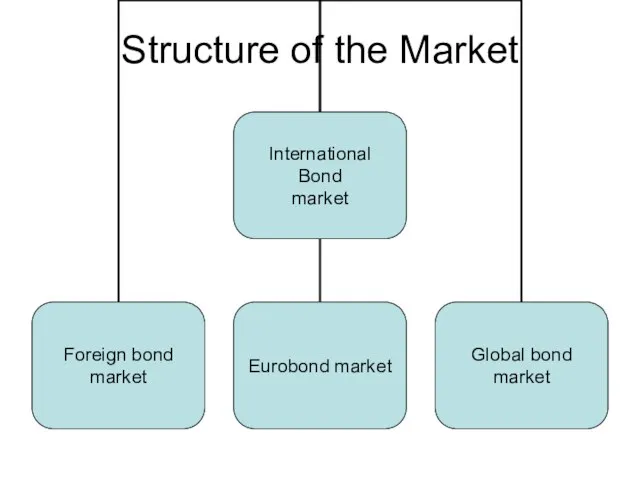

Слайд 8Structure of the Market

Structure of the Market

Слайд 9Foreign bond

A foreign bond - a bond that is issued in a

Foreign bond

A foreign bond - a bond that is issued in a

Слайд 10Foreign bonds

Foreign bonds are regulated by the domestic market authorities and are

Foreign bonds

Foreign bonds are regulated by the domestic market authorities and are

Слайд 11Foreign bonds

Yankee Bond - A bond denominated in U.S. dollars that is

Foreign bonds

Yankee Bond - A bond denominated in U.S. dollars that is

Слайд 12Foreign bonds

Kangaroo Bond (Matilda bond) - a type of foreign bond that

Foreign bonds

Kangaroo Bond (Matilda bond) - a type of foreign bond that

Слайд 13Foreign bonds

Matador Bond – a term used to identify a foreign bond

Foreign bonds

Matador Bond – a term used to identify a foreign bond

Слайд 142010:

Global bond market

95 trillion $

Domestic bonds:

% of the market

International bonds –

2010:

Global bond market

95 trillion $

Domestic bonds:

% of the market

International bonds –

Слайд 16Eurobonds

Eurobond - is a bond denominated in a particular currency but sold

Eurobonds

Eurobond - is a bond denominated in a particular currency but sold

Слайд 17Eurobonds

Eurobonds are known by the currency in which they are denominated, for

Eurobonds

Eurobonds are known by the currency in which they are denominated, for

Слайд 18Bearer Bonds and Registered Bonds

With a bearer bond, possession is evidence

Bearer Bonds and Registered Bonds

With a bearer bond, possession is evidence

Слайд 19 Eurobonds are usually bearer bonds.

U.S. security regulations require Yankee bonds and

Eurobonds are usually bearer bonds.

U.S. security regulations require Yankee bonds and

Слайд 20Recent changes in U.S. security regulations

Rule 415, which the SEC instituted in

Recent changes in U.S. security regulations

Rule 415, which the SEC instituted in

Слайд 21Global Bonds

A global bond issue is a very large international bond

Global Bonds

A global bond issue is a very large international bond

Слайд 22Largest corporate global bond issue

$14.6 billion Deutsche Telekom multicurrency offering.

The

Largest corporate global bond issue

$14.6 billion Deutsche Telekom multicurrency offering.

The

Слайд 232. Types of Instruments

2. Types of Instruments

Слайд 24Types of instruments

Straight Fixed-Rate Issues

Zero-Coupon Bonds

Euro-Medium-Term Notes

Floating-Rate

Types of instruments

Straight Fixed-Rate Issues

Zero-Coupon Bonds

Euro-Medium-Term Notes

Floating-Rate

Слайд 25Straight fixed-rate bond

Straight fixed-rate bond issues have a designated maturity date

Straight fixed-rate bond

Straight fixed-rate bond issues have a designated maturity date

Слайд 26Bond fair price

The fair price of a bond is the sum of

Bond fair price

The fair price of a bond is the sum of

Слайд 27where P = Bond’s fair price;

C = Annual coupon payment;

r = Discount

where P = Bond’s fair price;

C = Annual coupon payment;

r = Discount

Слайд 28

Bond yield

Yield-to-maturity is the percentage rate of return assuming a bond is

Bond yield

Yield-to-maturity is the percentage rate of return assuming a bond is

Слайд 29Mathematically, an investment’s yield, represented by r, is the interest rate that

Mathematically, an investment’s yield, represented by r, is the interest rate that

Слайд 30Example

A price of 5-year bond is 100 $ and this bond pays

Example

A price of 5-year bond is 100 $ and this bond pays

Слайд 31 When a bond is trading at a discount, YTM is greater

When a bond is trading at a discount, YTM is greater

Слайд 32Zero-coupon bonds

(strips, bullet bonds)

Bonds are sold at a discount from face

Zero-coupon bonds

(strips, bullet bonds)

Bonds are sold at a discount from face

Слайд 33 Calculate the price of a French government zero-coupon bond with precisely

Calculate the price of a French government zero-coupon bond with precisely

Слайд 34Note that, even though these bonds pay no actual coupons, their prices

Note that, even though these bonds pay no actual coupons, their prices

Слайд 35

Calculate the price of a Treasury strip with a maturity of precisely

Calculate the price of a Treasury strip with a maturity of precisely

Слайд 36 Calculate the price of a Treasury strip with a maturity of

Calculate the price of a Treasury strip with a maturity of

Слайд 37+ and - of zero-coupon bond

They do not entail any reinvestment risk

+ and - of zero-coupon bond

They do not entail any reinvestment risk

Слайд 38

Euro-Medium-Term Notes (Euro MTNs)

Euro-Medium-Term Notes (Euro MTNs) are (typically) fixed-rate notes issued

Euro-Medium-Term Notes (Euro MTNs)

Euro-Medium-Term Notes (Euro MTNs) are (typically) fixed-rate notes issued

Слайд 39Euro-Medium-Term Notes (Euro MTNs)

EMTNs make it easier for issuers to enter into

Euro-Medium-Term Notes (Euro MTNs)

EMTNs make it easier for issuers to enter into

Слайд 40Floating-Rate Notes (FRNs)

A note with a variable interest rate. The adjustments to

Floating-Rate Notes (FRNs)

A note with a variable interest rate. The adjustments to

Слайд 41FRNs

Additional features have been added to FRNs, including floors (the coupon

FRNs

Additional features have been added to FRNs, including floors (the coupon

Слайд 42Equity-related Bonds

There are two types of equity-related bonds:

convertible bonds

bonds

Equity-related Bonds

There are two types of equity-related bonds:

convertible bonds

bonds

Слайд 43Equity-related Bonds

Bonds with equity warrants can be viewed as straight fixed-rate bonds

Equity-related Bonds

Bonds with equity warrants can be viewed as straight fixed-rate bonds

Слайд 44Dual-currency bonds

A dual-currency bond is a straight fixed-rate bond issued in one

Dual-currency bonds

A dual-currency bond is a straight fixed-rate bond issued in one

Слайд 47International Bond Market Credit Ratings

Fitch IBCA,

Moody’s Investors Service,

Standard &

International Bond Market Credit Ratings

Fitch IBCA,

Moody’s Investors Service,

Standard &

Слайд 48These three credit-rating organizations classify bond issues into categories based upon the

These three credit-rating organizations classify bond issues into categories based upon the

Слайд 49Moody’s

bonds are rated into nine categories, from Aaa, Aa, A, Baa, and

Moody’s

bonds are rated into nine categories, from Aaa, Aa, A, Baa, and

Слайд 50International Bond Market Indexes

Emerging market bonds

J.P. Morgan Emerging Markets Bond Index (EMBI)

International Bond Market Indexes

Emerging market bonds

J.P. Morgan Emerging Markets Bond Index (EMBI)

Слайд 51Standard & Poor’s

Bonds are rated into 11 categories, from AAA, AA, A,

Standard & Poor’s

Bonds are rated into 11 categories, from AAA, AA, A,

Слайд 52 4. Eurobond market practice

4. Eurobond market practice

Слайд 53Eurobond market makers and dealers are members of the International Securities Market

Eurobond market makers and dealers are members of the International Securities Market

Слайд 54Euroclear

Euroclear settles domestic and international securities transactions, covering bonds, equities, derivatives and

Euroclear

Euroclear settles domestic and international securities transactions, covering bonds, equities, derivatives and

Слайд 55Supervision

Incorporated in Belgium, Euroclear SA/NV is subject to the supervision of the

Supervision

Incorporated in Belgium, Euroclear SA/NV is subject to the supervision of the

Слайд 56Each clearing system has a group of depository banks that physically store

Each clearing system has a group of depository banks that physically store

Слайд 57 (1) The clearing systems will finance up to 90 percent of

(1) The clearing systems will finance up to 90 percent of

Слайд 58Issuers of eurobond

Domotechnika

Donbass Resources

Donbassenergo

Donetsk City

Donetsktelekom

Dongorbank

Donsnab-service

Issuers of eurobond

Domotechnika

Donbass Resources

Donbassenergo

Donetsk City

Donetsktelekom

Dongorbank

Donsnab-service

Слайд 59International portfolio strategies

1. Benchmark selection

2. Bond market selection

3.Sector selection/credit selection

4.Currency management

International portfolio strategies

1. Benchmark selection

2. Bond market selection

3.Sector selection/credit selection

4.Currency management

Слайд 60Benchmark selection

The benchmark is some bond index.

What types of issuers should be

Benchmark selection

The benchmark is some bond index.

What types of issuers should be

Слайд 61Bond market selection

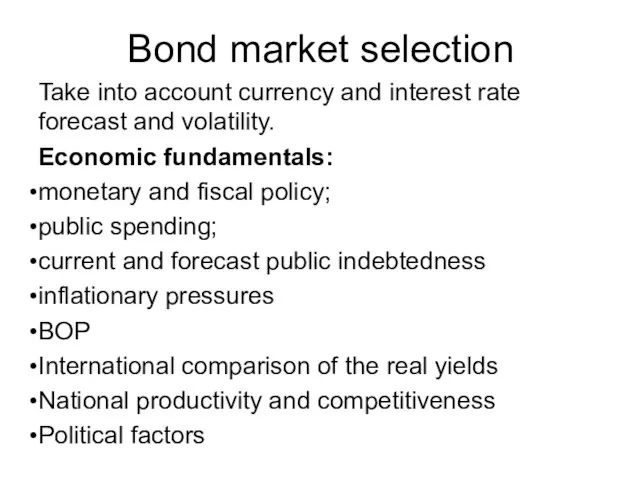

Take into account currency and interest rate forecast and volatility.

Economic

Bond market selection

Take into account currency and interest rate forecast and volatility.

Economic

Черкаський національний університет імені Богдана Хмельницького

Черкаський національний університет імені Богдана Хмельницького «Законодательные изменения в ЕСН: переход на обязательное социальное страхование»

«Законодательные изменения в ЕСН: переход на обязательное социальное страхование» Знамя Победы

Знамя Победы Весеннее печенье тетёрки

Весеннее печенье тетёрки Предпринимательство— самостоятельная, осуществляемая на свой риск деятельность

Предпринимательство— самостоятельная, осуществляемая на свой риск деятельность Продвижение фотостудии The Museum. Проект

Продвижение фотостудии The Museum. Проект Презентация на тему Файлы и файловая система

Презентация на тему Файлы и файловая система Сроки в гражданском праве

Сроки в гражданском праве Подсудность гражданских дел

Подсудность гражданских дел Шаблонизация на стороне клиента

Шаблонизация на стороне клиента Презентация на тему Презентация Солнце

Презентация на тему Презентация Солнце  Образовательные ресурсы сети Интернет

Образовательные ресурсы сети Интернет  Автоматическая энергосберегающая система освещения Automatic Energy Saving Lighting System

Автоматическая энергосберегающая система освещения Automatic Energy Saving Lighting System Выполнение фигурок из палочек

Выполнение фигурок из палочек Неоказание помощи больному

Неоказание помощи больному Презентация на тему Заимствованные слова

Презентация на тему Заимствованные слова Определение значения логического выражения

Определение значения логического выражения Тема: «В поисках смысла» Гасанова Н. М.

Тема: «В поисках смысла» Гасанова Н. М. Zabezpieczenie techniczne wspomagające ochronę osób i mienia cz.1. Systemy dozoru wizyjnego z funkcją nadzoru

Zabezpieczenie techniczne wspomagające ochronę osób i mienia cz.1. Systemy dozoru wizyjnego z funkcją nadzoru Технология проведения стартовой диагностики

Технология проведения стартовой диагностики ПРОГРАММА ПОДДЕРЖКИ ГРАЖДАНСКОГО ОБЩЕСТВА «ДИАЛОГ»

ПРОГРАММА ПОДДЕРЖКИ ГРАЖДАНСКОГО ОБЩЕСТВА «ДИАЛОГ» CLASSIC WARPLANES

CLASSIC WARPLANES Расчет параметров доставки пород в камере

Расчет параметров доставки пород в камере Преза_ВБ_Девятов

Преза_ВБ_Девятов ГОУ СПО ПОЛИТЕХНИЧЕСКИЙКОЛЛЕДЖ № 50Презентация по Экономикена тему: ПРЕДПРИНИМАТЕЛЬСТВО

ГОУ СПО ПОЛИТЕХНИЧЕСКИЙКОЛЛЕДЖ № 50Презентация по Экономикена тему: ПРЕДПРИНИМАТЕЛЬСТВО Система распространения и технической поддержки сертифицированных продуктов

Система распространения и технической поддержки сертифицированных продуктов Конкурс ДжиИ Мани Банк – SIFE Россия 2009 «Управление кредитными обязательствами в период кризиса. Брать или не брать кредит?»

Конкурс ДжиИ Мани Банк – SIFE Россия 2009 «Управление кредитными обязательствами в период кризиса. Брать или не брать кредит?» Вводная беседа о видах искусств (виды и жанры). Часть вторая

Вводная беседа о видах искусств (виды и жанры). Часть вторая