- lecture 2 cornett_finance_5e_chapter_02_ppt_accessible

Содержание

- 2. Introduction 1 A financial statement provides an accounting-based picture of a firm’s financial position. An annual

- 3. Introduction 2 Reports are used by accountants as a picture of past financial performance. Finance professionals

- 4. Balance Sheet The balance sheet reports firm’s assets, liabilities and equity at a point in time.

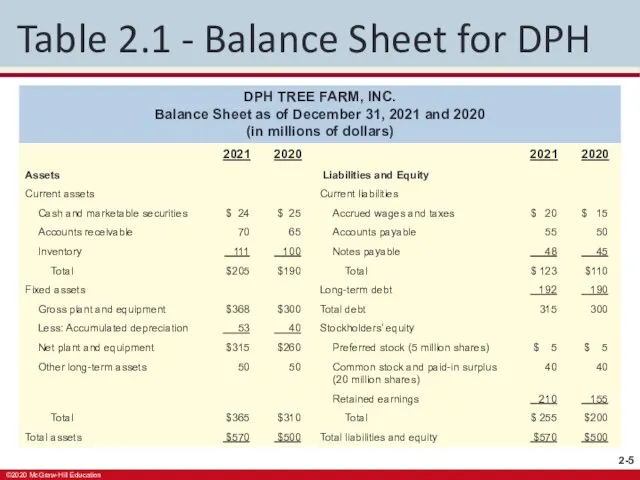

- 5. Table 2.1 - Balance Sheet for DPH DPH TREE FARM, INC. Balance Sheet as of December

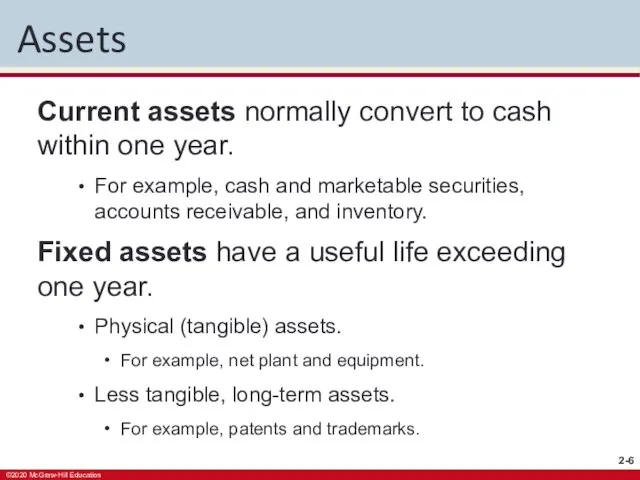

- 6. Assets Current assets normally convert to cash within one year. For example, cash and marketable securities,

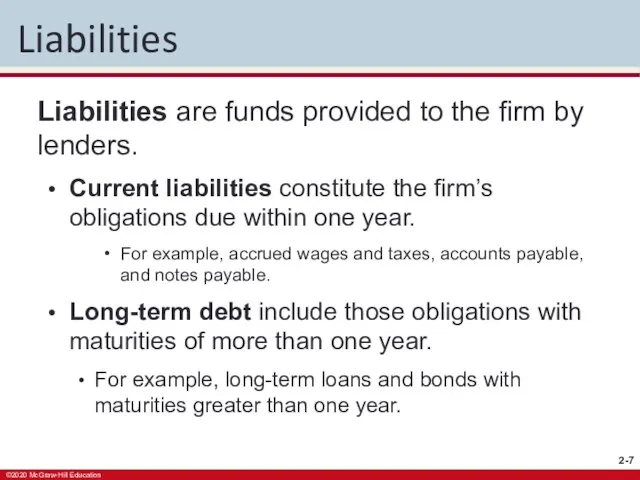

- 7. Liabilities Liabilities are funds provided to the firm by lenders. Current liabilities constitute the firm’s obligations

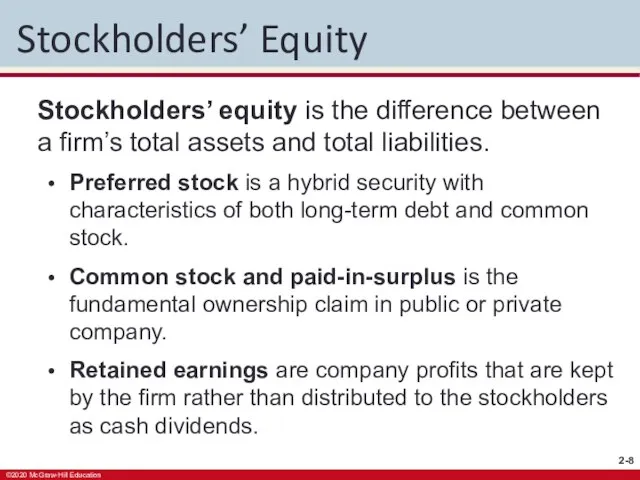

- 8. Stockholders’ Equity Stockholders’ equity is the difference between a firm’s total assets and total liabilities. Preferred

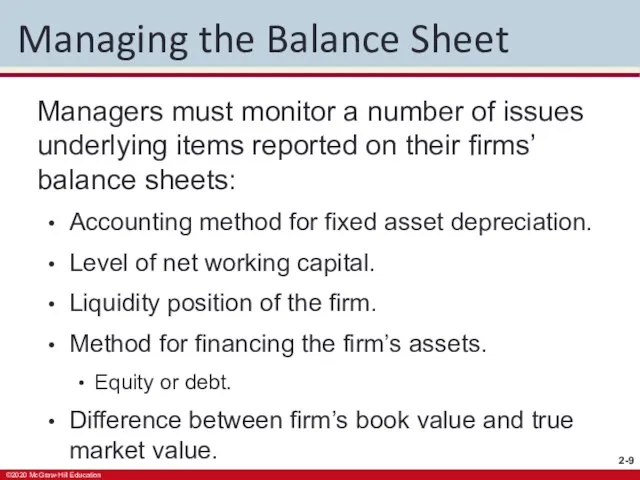

- 9. Managing the Balance Sheet Managers must monitor a number of issues underlying items reported on their

- 10. Accounting Method for Fixed Asset Depreciation Managers can choose the accounting method they use to record

- 11. Net Working Capital Net Working Capital = Current assets − Current liabilities Net working capital is

- 12. Liquidity 1 Liquidity refers to two dimensions. Ease with which the firm can convert an asset

- 13. Liquidity 2 Liquidity is double-edged sword. The good? The more liquid assets a firm holds, the

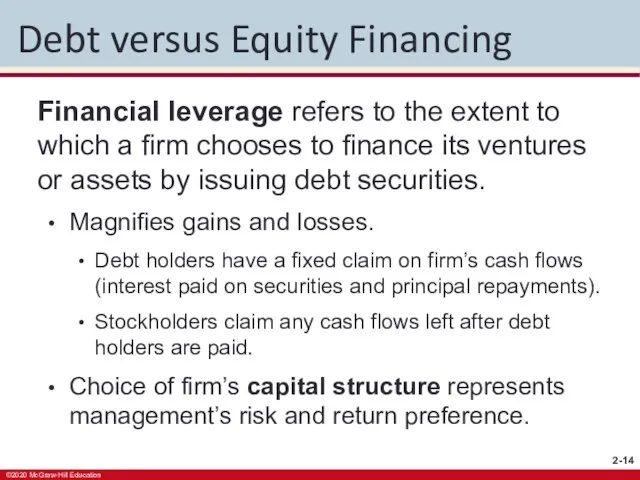

- 14. Debt versus Equity Financing Financial leverage refers to the extent to which a firm chooses to

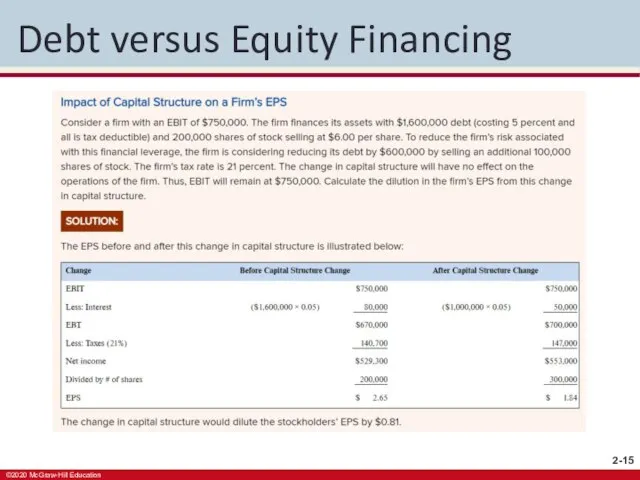

- 15. Debt versus Equity Financing

- 16. Book Value versus Market Value In many cases, book values differ widely from market values. The

- 17. Income Statement The income statement shows the total revenues that a firm earns and the total

- 18. Income Statement Structure FIGURE 2.2 The Basic Income Statement Net sales Less: Cost of goods sold

- 19. DPH Tree Farm Income Statement TABLE 2.2 Income Statement for DPH Tree Farm, Inc. DPH TREE

- 20. Income/Firm Value Summary Below the Bottom Line

- 21. Corporate Income Taxes 1 Firms taxed on earnings. U.S. tax code determines corporate tax obligations –

- 22. Corporate Income Taxes 2 Average tax rate. Percentage of each dollar of taxable income that the

- 23. Corporate Income Taxes

- 24. Corporate Income Taxes

- 25. Interest and Dividends Received Interest is taxable with two exceptions. Interest on state and local government

- 26. Interest and Dividends Paid Interest payments appear on the income statement as an expense item. They

- 27. Statement of Cash Flows The statement of cash flows is a financial statement that shows firm’s

- 28. GAAP Accounting Principles Company accountants use GAAP principles to prepare firm income statements. Revenue recognition and

- 29. Sources and Uses of Cash 1 An activity that increases cash is a cash source. Increasing

- 30. Sources and Uses of Cash 2 Four categories are used to separate cash flows on the

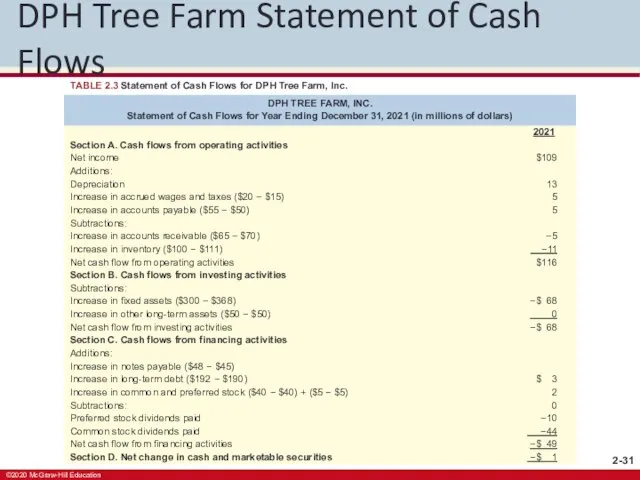

- 31. DPH Tree Farm Statement of Cash Flows TABLE 2.3 Statement of Cash Flows for DPH Tree

- 32. Cash Flows from Operations Cash flows that are the direct result of the production and sale

- 33. Cash Flows from Investing Activities Cash flows associated with the purchase or sale of fixed or

- 34. Cash Flows from Financing Activities Cash flows from financing activities result from debt and equity financing

- 35. Net Change in Cash and Marketable Securities The sum of the cash flows from operations, investing

- 36. Free Cash Flow 1 Free cash flows is the cash actually available for distribution to the

- 37. Free Cash Flow 2 Firms generate operating cash flow (OCF) after they have paid necessary operating

- 38. Free Cash Flow 3 Firms with positive free cash flow (FCF) have funds available for distribution

- 39. Free Cash Flow Equation

- 40. Free Cash Flow

- 41. Statement of Retained Earnings The statement of retained earnings reconciles net income earned during a given

- 42. Cautions in Interpreting Financial Statements GAAP standards required for financial statements. Firms can use earnings management

- 44. Скачать презентацию

Слайд 2Introduction 1

A financial statement provides an accounting-based picture of a firm’s financial

Introduction 1

A financial statement provides an accounting-based picture of a firm’s financial

Слайд 3Introduction 2

Reports are used by accountants as a picture of past financial

Introduction 2

Reports are used by accountants as a picture of past financial

Слайд 4Balance Sheet

The balance sheet reports firm’s assets, liabilities and equity at a

Balance Sheet

The balance sheet reports firm’s assets, liabilities and equity at a

Слайд 5Table 2.1 - Balance Sheet for DPH

DPH TREE FARM, INC.

Balance Sheet

Table 2.1 - Balance Sheet for DPH

DPH TREE FARM, INC. Balance Sheet

Слайд 6Assets

Current assets normally convert to cash within one year.

For example, cash and

Assets

Current assets normally convert to cash within one year.

For example, cash and

Слайд 7Liabilities

Liabilities are funds provided to the firm by lenders.

Current liabilities constitute the

Liabilities

Liabilities are funds provided to the firm by lenders.

Current liabilities constitute the

Слайд 8Stockholders’ Equity

Stockholders’ equity is the difference between a firm’s total assets and

Stockholders’ Equity

Stockholders’ equity is the difference between a firm’s total assets and

Слайд 9Managing the Balance Sheet

Managers must monitor a number of issues underlying items

Managing the Balance Sheet

Managers must monitor a number of issues underlying items

Слайд 10Accounting Method for Fixed Asset Depreciation

Managers can choose the accounting method they

Accounting Method for Fixed Asset Depreciation

Managers can choose the accounting method they

Слайд 11Net Working Capital

Net Working Capital =

Current assets − Current liabilities

Net working

Net Working Capital

Net Working Capital =

Current assets − Current liabilities

Net working

Слайд 12Liquidity 1

Liquidity refers to two dimensions.

Ease with which the firm can convert

Liquidity 1

Liquidity refers to two dimensions.

Ease with which the firm can convert

Слайд 13Liquidity 2

Liquidity is double-edged sword.

The good?

The more liquid assets a firm holds,

Liquidity 2

Liquidity is double-edged sword.

The good?

The more liquid assets a firm holds,

Слайд 14Debt versus Equity Financing

Financial leverage refers to the extent to which a

Debt versus Equity Financing

Financial leverage refers to the extent to which a

Слайд 15Debt versus Equity Financing

Debt versus Equity Financing

Слайд 16Book Value versus Market Value

In many cases, book values differ widely from

Book Value versus Market Value

In many cases, book values differ widely from

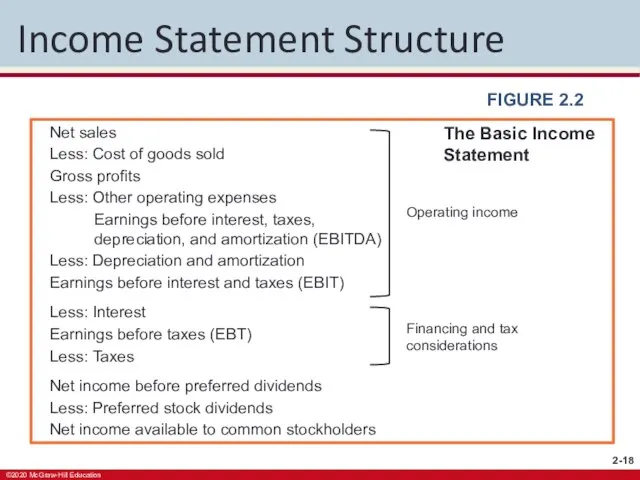

Слайд 17Income Statement

The income statement shows the total revenues that a firm earns

Income Statement

The income statement shows the total revenues that a firm earns

Слайд 18Income Statement Structure

FIGURE 2.2

The Basic Income

Statement

Net sales

Less: Cost of goods sold

Gross profits

Less:

Income Statement Structure

FIGURE 2.2

The Basic Income

Statement

Net sales

Less: Cost of goods sold

Gross profits

Less:

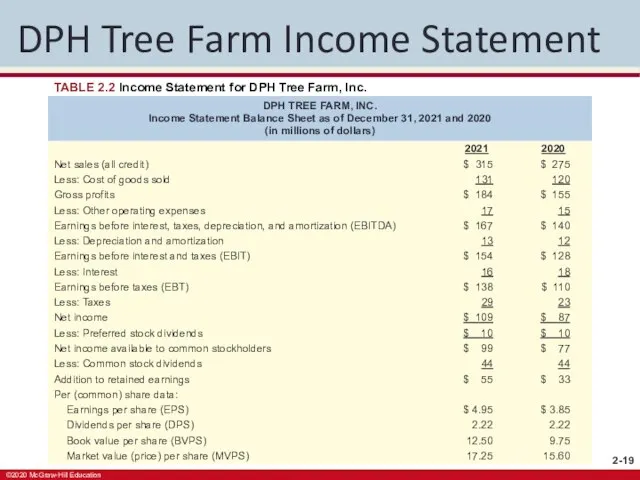

Слайд 19DPH Tree Farm Income Statement

TABLE 2.2 Income Statement for DPH Tree Farm,

DPH Tree Farm Income Statement

TABLE 2.2 Income Statement for DPH Tree Farm,

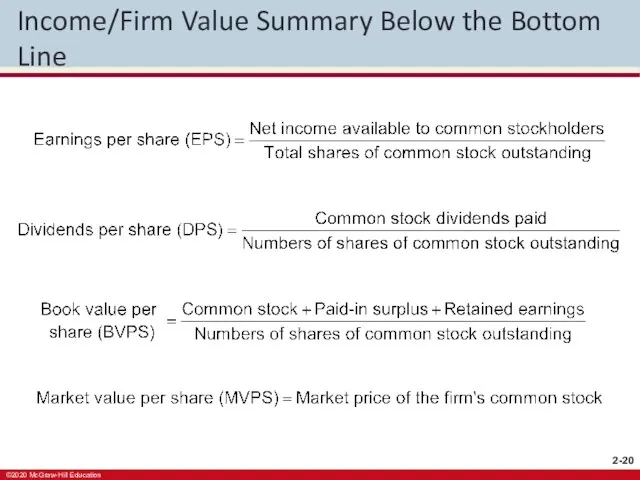

Слайд 20Income/Firm Value Summary Below the Bottom Line

Income/Firm Value Summary Below the Bottom Line

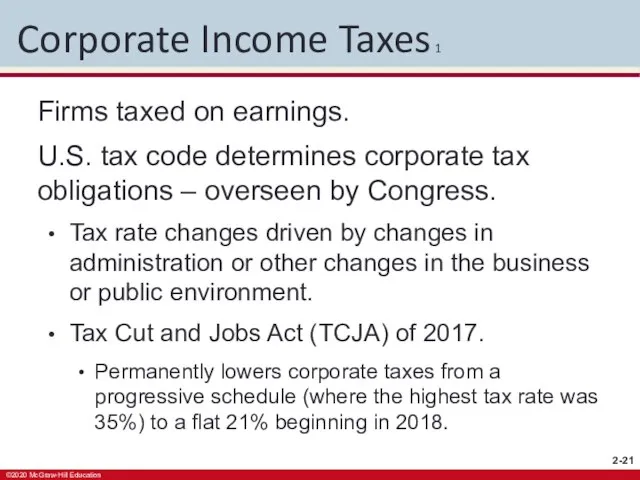

Слайд 21Corporate Income Taxes 1

Firms taxed on earnings.

U.S. tax code determines corporate tax

Corporate Income Taxes 1

Firms taxed on earnings.

U.S. tax code determines corporate tax

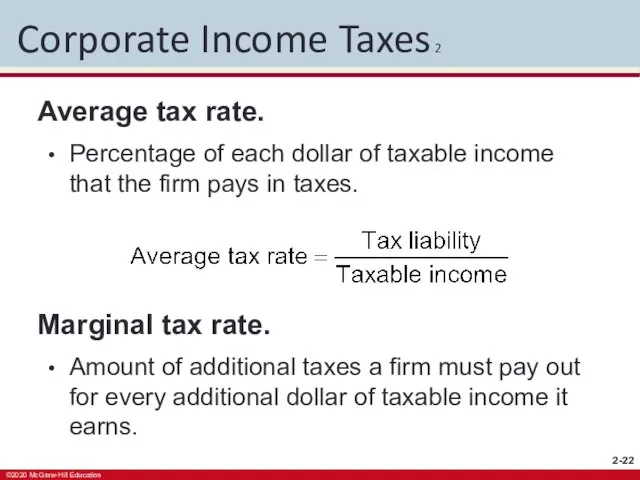

Слайд 22Corporate Income Taxes 2

Average tax rate.

Percentage of each dollar of taxable income

Corporate Income Taxes 2

Average tax rate.

Percentage of each dollar of taxable income

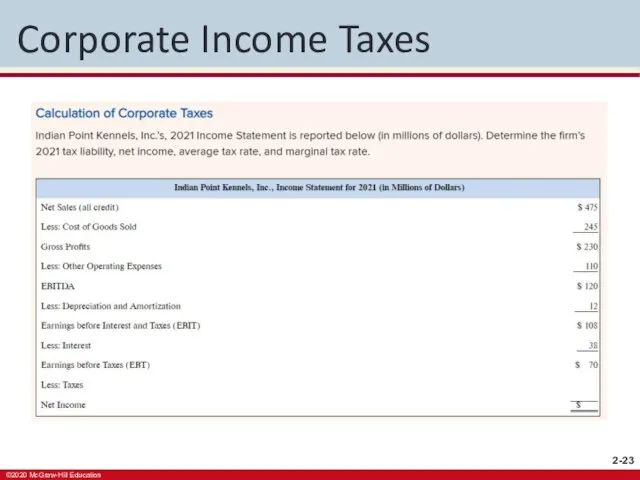

Слайд 23Corporate Income Taxes

Corporate Income Taxes

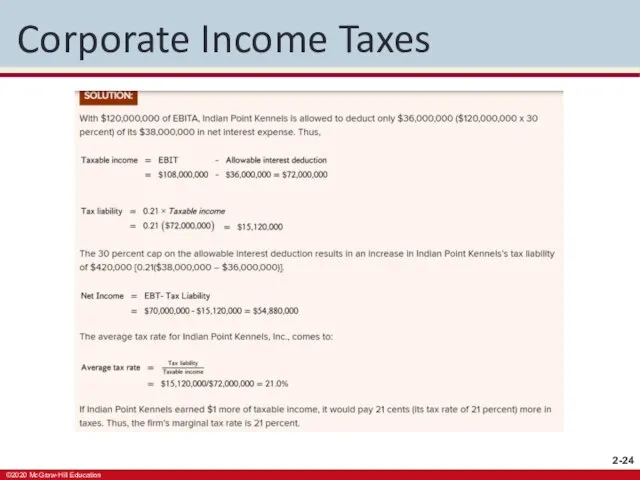

Слайд 24Corporate Income Taxes

Corporate Income Taxes

Слайд 25Interest and Dividends Received

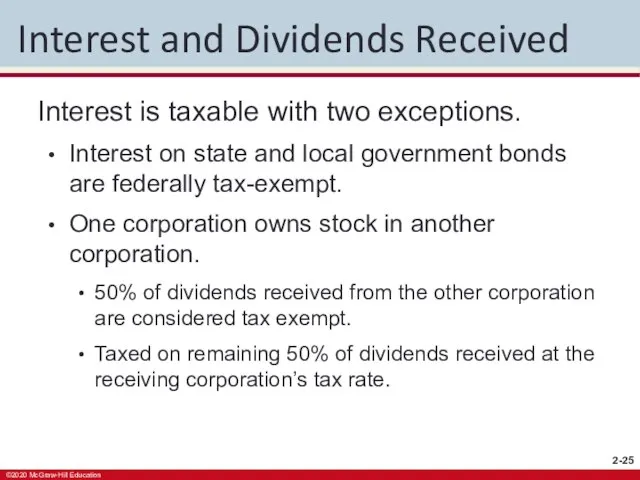

Interest is taxable with two exceptions.

Interest on state and

Interest and Dividends Received

Interest is taxable with two exceptions.

Interest on state and

Слайд 26Interest and Dividends Paid

Interest payments appear on the income statement as an

Interest and Dividends Paid

Interest payments appear on the income statement as an

Слайд 27Statement of Cash Flows

The statement of cash flows is a financial statement

Statement of Cash Flows

The statement of cash flows is a financial statement

Слайд 28GAAP Accounting Principles

Company accountants use GAAP principles to prepare firm income statements.

Revenue

GAAP Accounting Principles

Company accountants use GAAP principles to prepare firm income statements.

Revenue

Слайд 29Sources and Uses of Cash 1

An activity that increases cash is a

Sources and Uses of Cash 1

An activity that increases cash is a

Слайд 30Sources and Uses of Cash 2

Four categories are used to separate cash

Sources and Uses of Cash 2

Four categories are used to separate cash

Слайд 31DPH Tree Farm Statement of Cash Flows

TABLE 2.3 Statement of Cash Flows

DPH Tree Farm Statement of Cash Flows

TABLE 2.3 Statement of Cash Flows

Слайд 32Cash Flows from Operations

Cash flows that are the direct result of the

Cash Flows from Operations

Cash flows that are the direct result of the

Слайд 33Cash Flows from Investing Activities

Cash flows associated with the purchase or sale

Cash Flows from Investing Activities

Cash flows associated with the purchase or sale

Слайд 34Cash Flows from Financing Activities

Cash flows from financing activities result from debt

Cash Flows from Financing Activities

Cash flows from financing activities result from debt

Слайд 35Net Change in Cash and Marketable Securities

The sum of the cash flows

Net Change in Cash and Marketable Securities

The sum of the cash flows

Слайд 36Free Cash Flow 1

Free cash flows is the cash actually available for

Free Cash Flow 1

Free cash flows is the cash actually available for

Слайд 37Free Cash Flow 2

Firms generate operating cash flow (OCF) after they have

Free Cash Flow 2

Firms generate operating cash flow (OCF) after they have

Слайд 38Free Cash Flow 3

Firms with positive free cash flow (FCF) have funds

Free Cash Flow 3

Firms with positive free cash flow (FCF) have funds

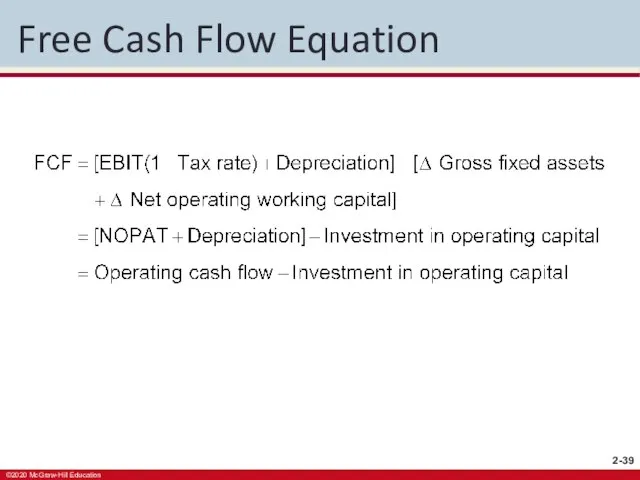

Слайд 39Free Cash Flow Equation

Free Cash Flow Equation

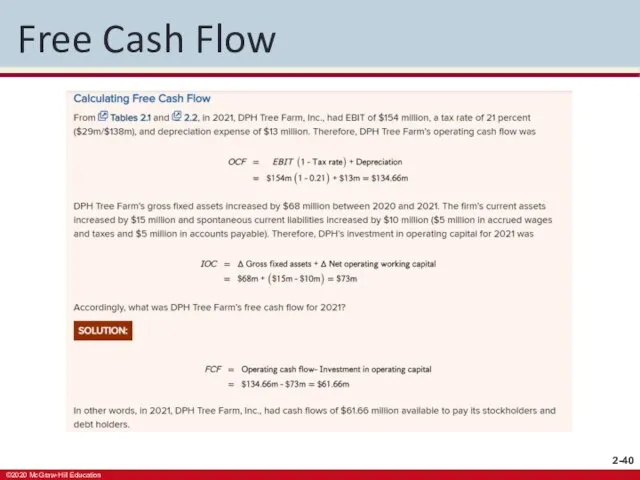

Слайд 40Free Cash Flow

Free Cash Flow

Слайд 41Statement of Retained Earnings

The statement of retained earnings reconciles net income earned

Statement of Retained Earnings

The statement of retained earnings reconciles net income earned

Слайд 42Cautions in Interpreting Financial Statements

GAAP standards required for financial statements.

Firms can use

Cautions in Interpreting Financial Statements

GAAP standards required for financial statements.

Firms can use

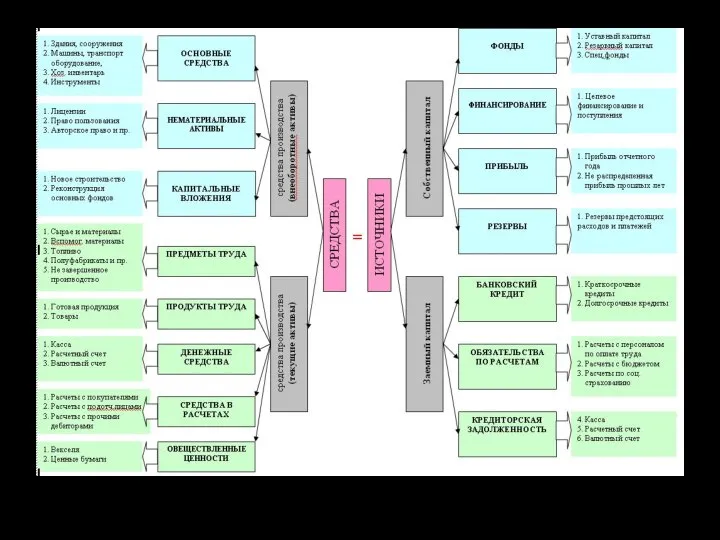

Владимиро- Суздальская земля

Владимиро- Суздальская земля Лабораторная работа № 5. Приготовление блюд

Лабораторная работа № 5. Приготовление блюд Подснежники - нежный и гордый вестник весны

Подснежники - нежный и гордый вестник весны Где зимуют птицы?

Где зимуют птицы? Пищеварительная система

Пищеварительная система  Обзор жилищного законодательстваРоссийской Федерации

Обзор жилищного законодательстваРоссийской Федерации Теории происхождения и сущность религии

Теории происхождения и сущность религии Немцы ворвались в город со стороны станицы Пашковской. В обороне переправы, прикрывая отступление советских войск, участвовали 1

Немцы ворвались в город со стороны станицы Пашковской. В обороне переправы, прикрывая отступление советских войск, участвовали 1 Свіфт Джонатан

Свіфт Джонатан Структура литературного произведения

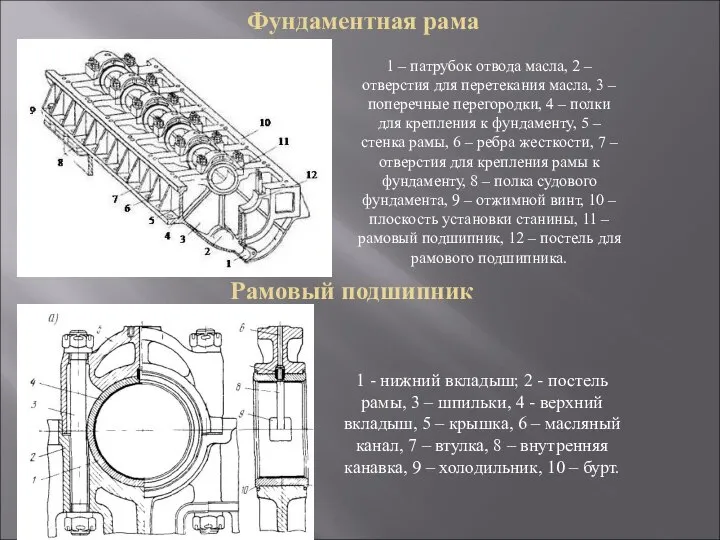

Структура литературного произведения Фундаментная рама. Шестеренный насос. Указатель длины якорной цепи на судне

Фундаментная рама. Шестеренный насос. Указатель длины якорной цепи на судне БУ торгово-материальные ценности

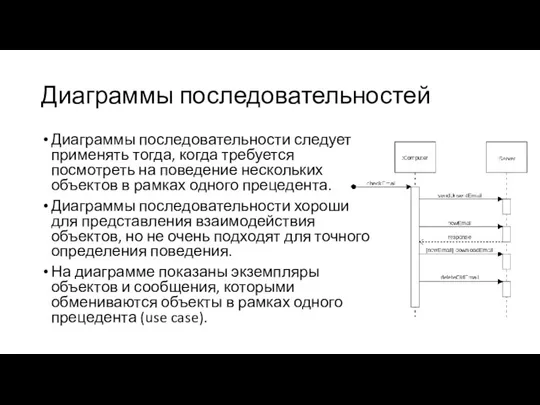

БУ торгово-материальные ценности UML_osnovy (1)

UML_osnovy (1) «Чем люди живы?»

«Чем люди живы?» Системы вентиляции

Системы вентиляции Технические средства компьютерной графики

Технические средства компьютерной графики Портрет в музыке и живописи

Портрет в музыке и живописи Трудовая функция

Трудовая функция Фармакоэкономический анализ лечения больных ХОБЛ

Фармакоэкономический анализ лечения больных ХОБЛ Ураганы ,бури ,смерчи 5 класс

Ураганы ,бури ,смерчи 5 класс 1 Русское искусство XVIII века Архитектура Архитектура Санкт - Петербурга. - презентация

1 Русское искусство XVIII века Архитектура Архитектура Санкт - Петербурга. - презентация Международное право. Международно-правовые средства разрешения споров

Международное право. Международно-правовые средства разрешения споров Тест жи - ши

Тест жи - ши Рекомендации к выполнению заданий части С по обществознанию

Рекомендации к выполнению заданий части С по обществознанию Общероссийской общественной организации«научно-педагогический союз историков России»

Общероссийской общественной организации«научно-педагогический союз историков России» Словарь в картинках

Словарь в картинках "Профилактика вредных привычек у подростков"

"Профилактика вредных привычек у подростков" Палитра

Палитра