- National Payment System of Kazakhstan

Содержание

- 3. Kazakhstan's modern national payment system is compatible with all international payment systems. Now in the Republic

- 4. The first chapter reveals the theoretical aspects of the payment system, its functions, roles and the

- 5. Theoretical aspects Payment system – is a set of procedures and associated with these procedures computer

- 6. History Republic of Kazakhstan, has a rich development history of the existing national payment system. The

- 7. The second step was the creation in 1995 of the first in the Republic of Kazakhstan

- 8. Oversight of payment system The concept of oversight of payment systems is defined in the Law

- 9. The National Bank of Kazakhstan considers appeals of individuals and entities with respect to violations of

- 10. KISC and national payment system of RK "Kazakhstan interbank settlement center of the National Bank of

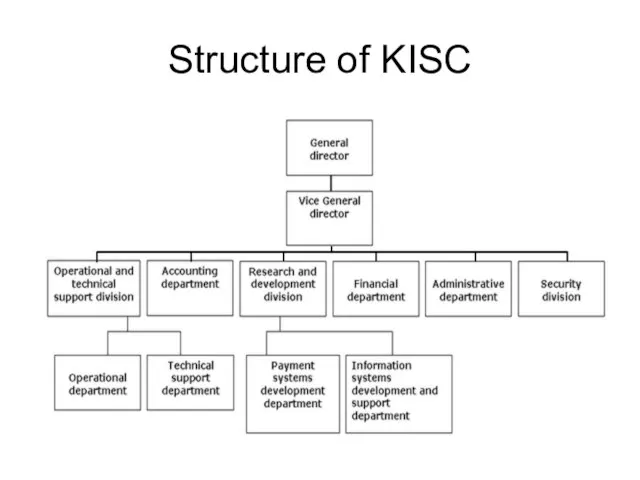

- 11. Structure of KISC

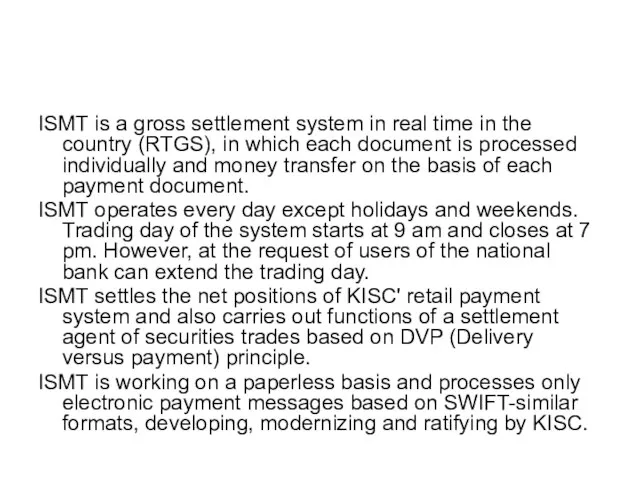

- 12. ISMT is a gross settlement system in real time in the country (RTGS), in which each

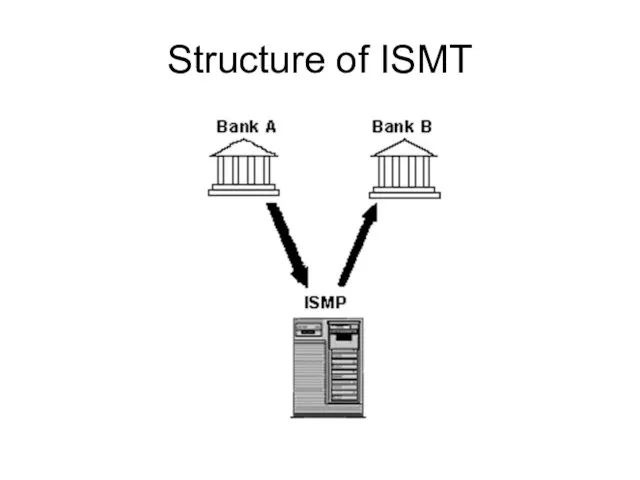

- 13. Structure of ISMT

- 14. System of Interbank Clearing Interbank Clearing System (offset of mutual claims and liabilities) settles on a

- 15. Banking Messages Exchange System All incoming messages passed checking procedures of BMES are forwarded either to

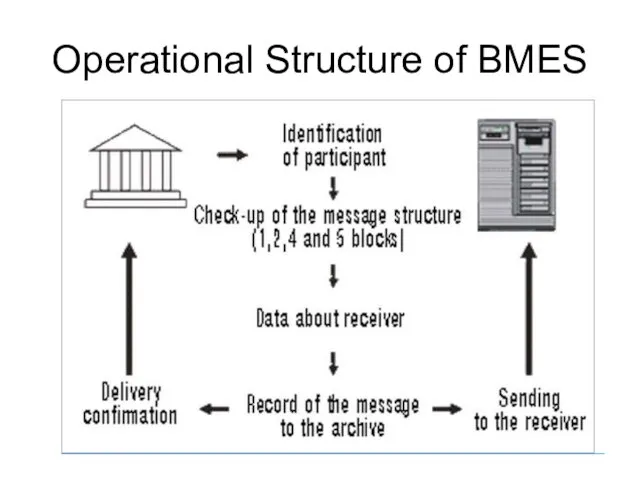

- 16. Operational Structure of BMES

- 17. Analysis of the payment system of the RK In order to manage risks when making payments

- 18. PROSPECTS FOR THE INTRODUCTION OF NEW PAYMENT SYSTEM IN THE REPUBLIC OF KAZAKHSTAN Electronic money legalized

- 19. E-money issuers may be any bank. The bank itself, in accordance with its domestic business strategy

- 21. Скачать презентацию

Слайд 3Kazakhstan's modern national payment system is compatible with all international payment systems.

Kazakhstan's modern national payment system is compatible with all international payment systems.

Слайд 4The first chapter reveals the theoretical aspects of the payment system, its

The first chapter reveals the theoretical aspects of the payment system, its

Слайд 5Theoretical aspects

Payment system – is a set of procedures and associated with

Theoretical aspects

Payment system – is a set of procedures and associated with

Слайд 6History

Republic of Kazakhstan, has a rich development history of the existing national

History

Republic of Kazakhstan, has a rich development history of the existing national

Слайд 7The second step was the creation in 1995 of the first in

The second step was the creation in 1995 of the first in

Слайд 8Oversight of payment system

The concept of oversight of payment systems is defined

Oversight of payment system

The concept of oversight of payment systems is defined

Слайд 9The National Bank of Kazakhstan considers appeals of individuals and entities with

The National Bank of Kazakhstan considers appeals of individuals and entities with

Слайд 10KISC and national payment system of RK

"Kazakhstan interbank settlement center of the

KISC and national payment system of RK

"Kazakhstan interbank settlement center of the

Слайд 11Structure of KISC

Structure of KISC

Слайд 12ISMT is a gross settlement system in real time in the country

ISMT is a gross settlement system in real time in the country

Слайд 13Structure of ISMT

Structure of ISMT

Слайд 14System of Interbank Clearing

Interbank Clearing System (offset of mutual claims and liabilities)

System of Interbank Clearing

Interbank Clearing System (offset of mutual claims and liabilities)

Слайд 15Banking Messages Exchange System

All incoming messages passed checking procedures of BMES

Banking Messages Exchange System

All incoming messages passed checking procedures of BMES

Слайд 16Operational Structure of BMES

Operational Structure of BMES

Слайд 17Analysis of the payment system of the RK

In order to manage risks

Analysis of the payment system of the RK

In order to manage risks

Слайд 18PROSPECTS FOR THE INTRODUCTION OF NEW PAYMENT SYSTEM IN THE REPUBLIC OF

PROSPECTS FOR THE INTRODUCTION OF NEW PAYMENT SYSTEM IN THE REPUBLIC OF

Слайд 19E-money issuers may be any bank. The bank itself, in accordance with

E-money issuers may be any bank. The bank itself, in accordance with

Партнерская программа Станкин - Siemens

Партнерская программа Станкин - Siemens История часов

История часов Мое хобби - иностранные языки. Практическая работа

Мое хобби - иностранные языки. Практическая работа Объемная резьба по дереву

Объемная резьба по дереву Неологизмы 6 класс

Неологизмы 6 класс Контрольная работа по дисциплине менеджмент качества

Контрольная работа по дисциплине менеджмент качества Сочинение по картине Грабаря «Февральская лазурь».

Сочинение по картине Грабаря «Февральская лазурь». схема компьютера

схема компьютера Каникулы в международном детском лагере

Каникулы в международном детском лагере Художник - моренист

Художник - моренист Внеклассное мероприятие «Звёздный час»

Внеклассное мероприятие «Звёздный час» Apģērbs. Apģērba materiāli

Apģērbs. Apģērba materiāli 7_

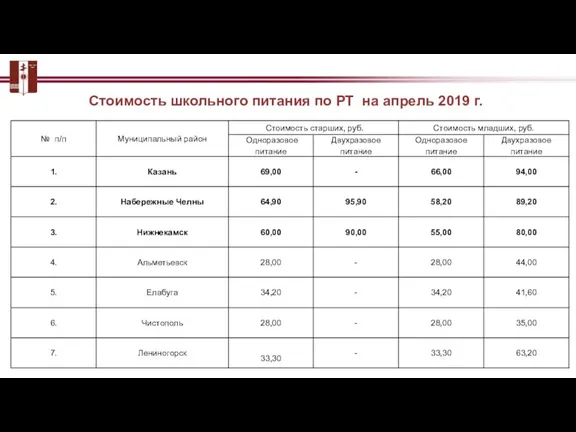

7_ Стоимость школьного питания

Стоимость школьного питания Жюль Ардуэн – Мансар (1646-1708)

Жюль Ардуэн – Мансар (1646-1708) Automotive Industry. Массовое производство

Automotive Industry. Массовое производство Парад Профессий - ХХI век. Автор: Тихонов Данил

Парад Профессий - ХХI век. Автор: Тихонов Данил Подготовила: студентка 401 группы Подготовила: студентка 401 группы заочного отделения факультета «Психология и педагогика» Бул

Подготовила: студентка 401 группы Подготовила: студентка 401 группы заочного отделения факультета «Психология и педагогика» Бул Виды и классификация моделей

Виды и классификация моделей Картины на квест

Картины на квест ФГУП «Комбинат Питания «Кремлевский» Предлагает организацию банкетных мероприятий в г. Сочина территории « санатория «Русь»З

ФГУП «Комбинат Питания «Кремлевский» Предлагает организацию банкетных мероприятий в г. Сочина территории « санатория «Русь»З Садимся за уроки Цели: выявить представления родителей об организации учебной работы детей дома; познакомить родителей с гиг

Садимся за уроки Цели: выявить представления родителей об организации учебной работы детей дома; познакомить родителей с гиг 8Г2_2022-10-12_урок 11_devoir (1)

8Г2_2022-10-12_урок 11_devoir (1) Стиль Людовика XV

Стиль Людовика XV программа проведения фестиваля военно-исторической реконструкции 4 августа 2012 года

программа проведения фестиваля военно-исторической реконструкции 4 августа 2012 года Читаем с удовольствием

Читаем с удовольствием ТЕОРИЯ ВЕРОЯТНОСТЕЙ НА ЕГЭ ПО МАТЕМАТИКЕ

ТЕОРИЯ ВЕРОЯТНОСТЕЙ НА ЕГЭ ПО МАТЕМАТИКЕ МОУ "ЛИЦЕЙ №3" 2010 - 2011 год

МОУ "ЛИЦЕЙ №3" 2010 - 2011 год