- Overall expenditures and prices of product

Содержание

- 2. Plan of lection 1. Definition of income and cost 2. Classification of costs 3. Price and

- 3. 1 The earning of net income, or profits, is a major goal of almost every business

- 4. Since business managers and economists use the word profits in somewhat different senses, accountants prefer to

- 5. To determine net income, it is necessary to measure for a given time period (1) the

- 6. Revenue is the price of goods sold and services rendered during a given accounting period. Business

- 7. Expenses are the cost of the goods and services used up in the process of earning

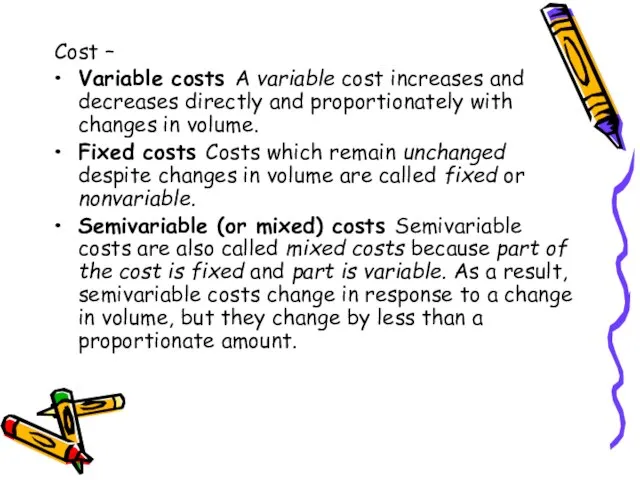

- 8. Cost – Variable costs A variable cost increases and decreases directly and proportionately with changes in

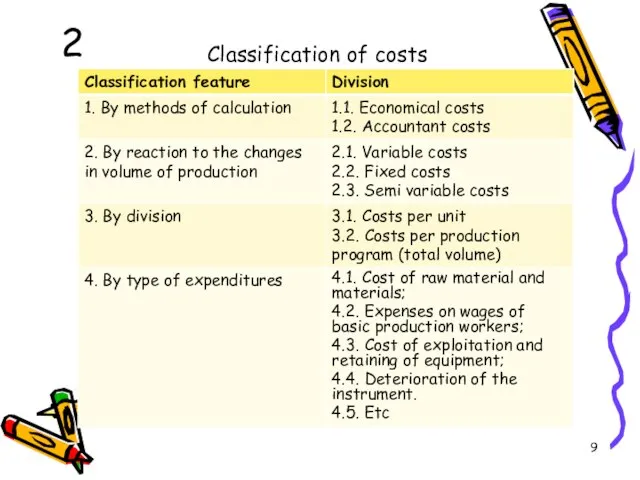

- 9. Classification of costs 2

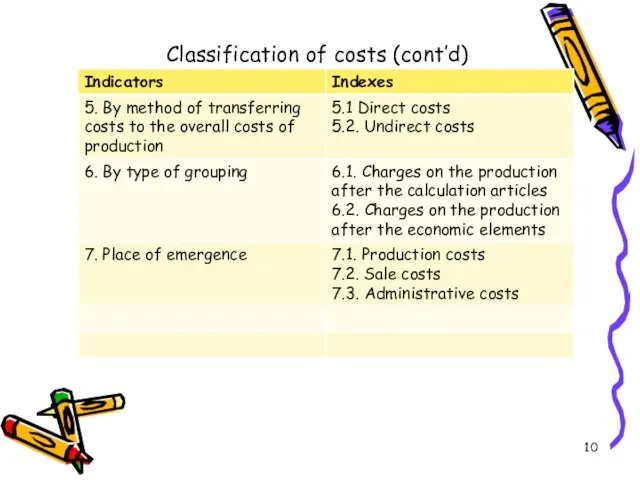

- 10. Classification of costs (cont’d)

- 11. An unit cost shows by itself a money term of charges is on a production and

- 12. The index of marginal charges is used to the analysis of need of changing the production

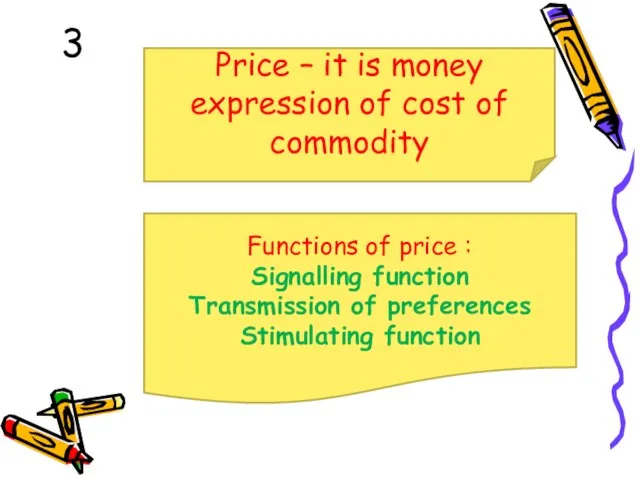

- 13. 3 Price – it is money expression of cost of commodity Functions of price : Signalling

- 14. Signaling function Prices perform a signaling function – they adjust to demonstrate where resources are required,

- 15. Transmission of preferences Through their choices consumers send information to producers about the changing nature of

- 16. Stimulative function of price - rational use of the limited resources., instrumental in scientific and technical

- 17. Pricing – it is the process of establishment and putting of prices and tariffs, later their

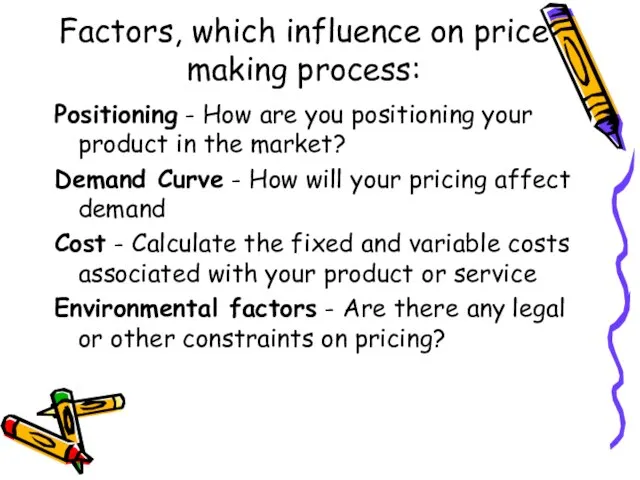

- 18. Factors, which influence on price making process: Positioning - How are you positioning your product in

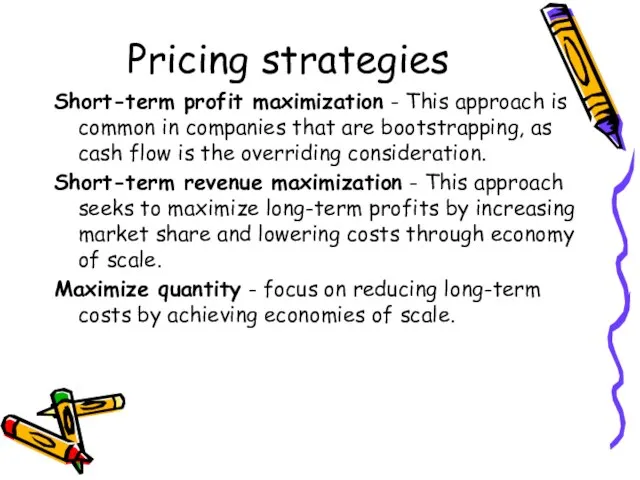

- 19. Pricing strategies Short-term profit maximization - This approach is common in companies that are bootstrapping, as

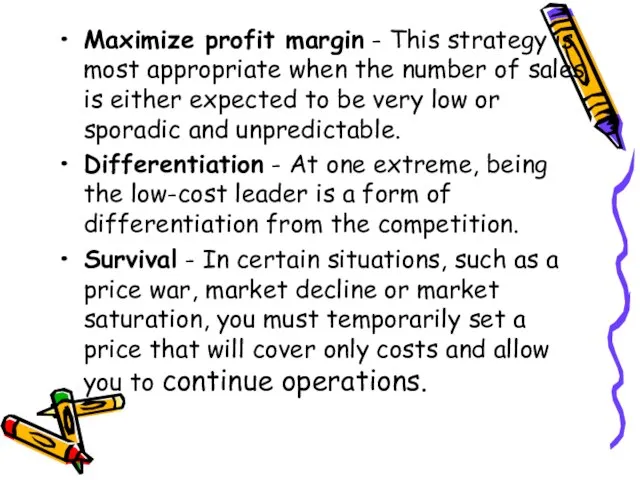

- 20. Maximize profit margin - This strategy is most appropriate when the number of sales is either

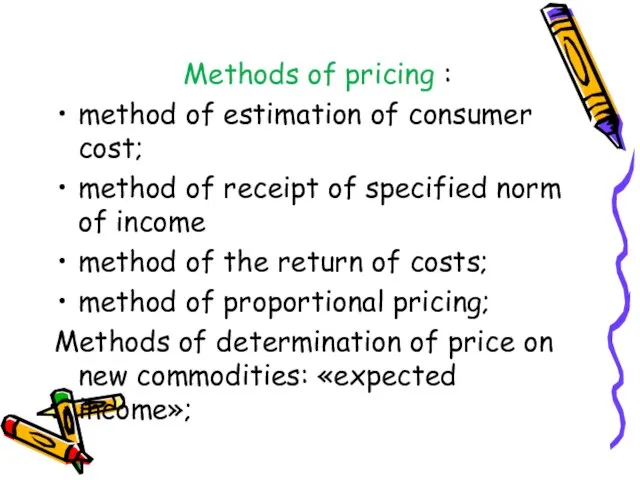

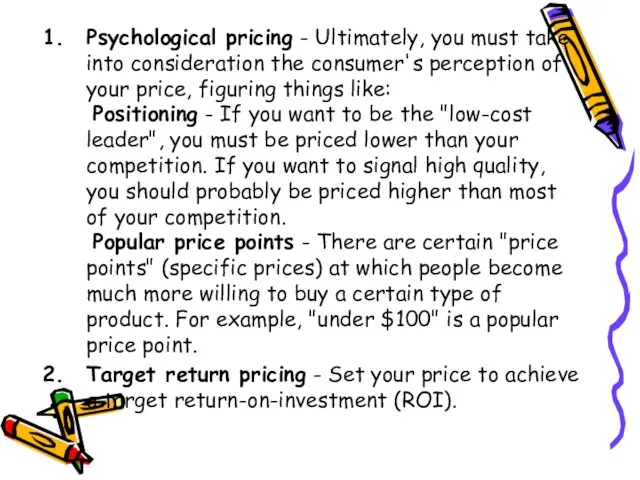

- 21. Methods of pricing : method of estimation of consumer cost; method of receipt of specified norm

- 22. Psychological pricing - Ultimately, you must take into consideration the consumer's perception of your price, figuring

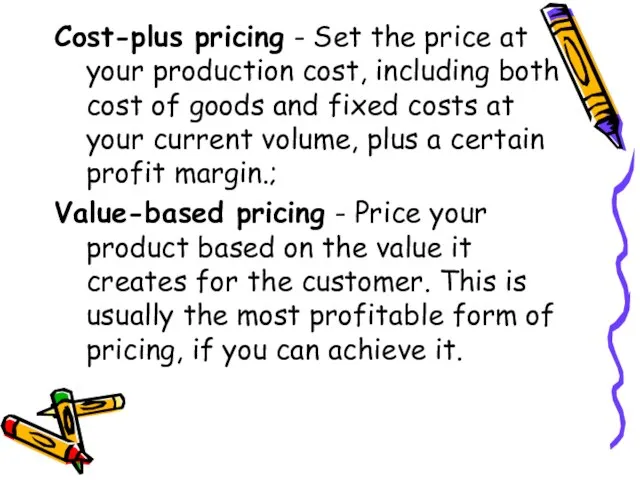

- 23. Cost-plus pricing - Set the price at your production cost, including both cost of goods and

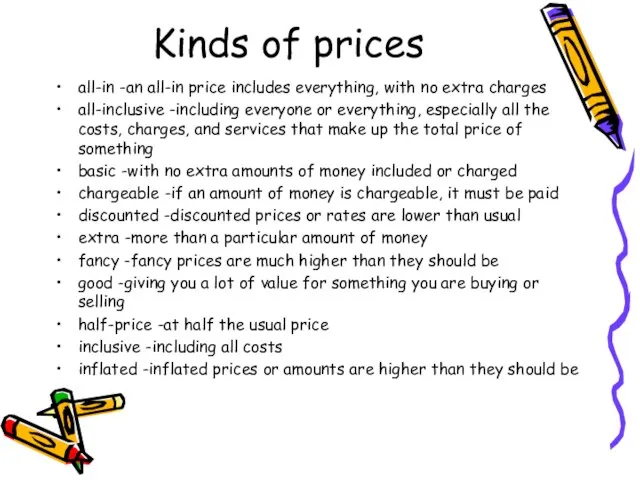

- 24. Kinds of prices all-in -an all-in price includes everything, with no extra charges all-inclusive -including everyone

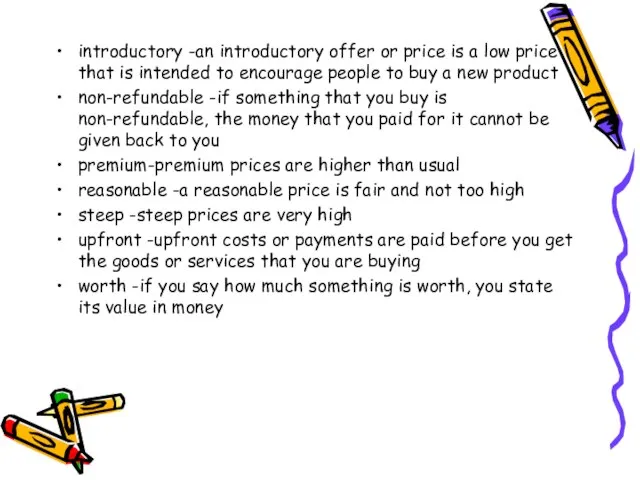

- 25. introductory -an introductory offer or price is a low price that is intended to encourage people

- 26. To the production prices belong: wholesale; of asqusition; estimate; Calculation (self-cost) planned The lower limit of

- 27. Cost-Volume-Profit Analysis Examines the behaviour of total revenues, total costs, and operating income as changes occur

- 28. The resulting break-even formula for composite unit sales is: Break-even point in composite units Fixed costs

- 29. Contribution Margin Contribution margin is equal to the difference between total revenue and total variable costs

- 30. Contribution Margin Income Statement Packages Sold 0 1 2 25 40 Revenue $0 $200 $400 $5,000

- 31. I. Common Cost Behavior Patterns Variable Costs Fixed Costs Discretionary versus Committed Fixed Costs Mixed Costs

- 32. A. Variable Costs Although variable cost per unit remain constant, total variable cost increases and decreases

- 33. B. Fixed Cost in Total Although fixed cost per unit decreases with increases in activity levels,

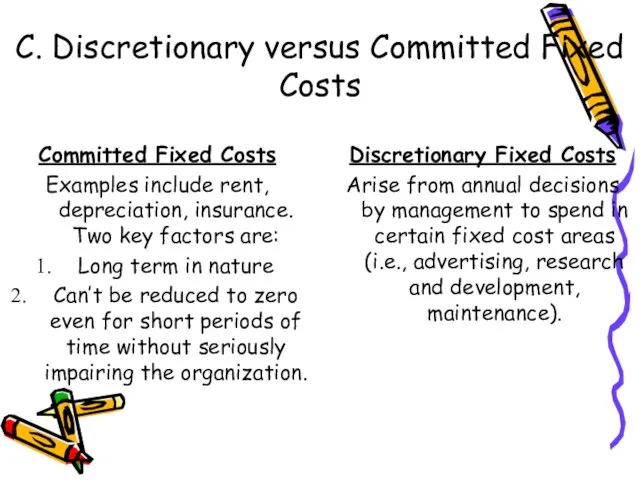

- 34. C. Discretionary versus Committed Fixed Costs Committed Fixed Costs Examples include rent, depreciation, insurance. Two key

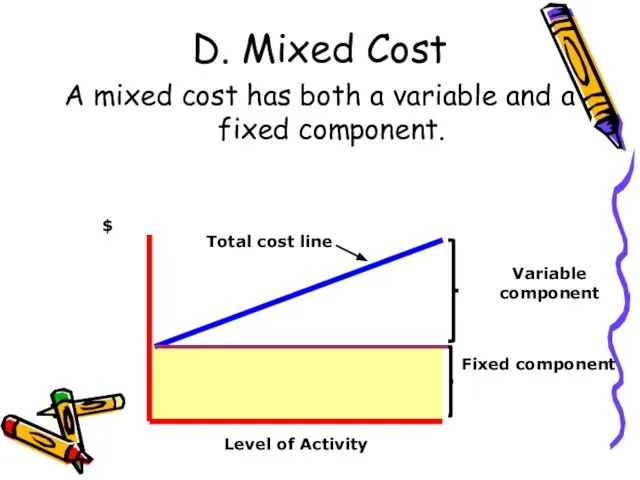

- 35. D. Mixed Cost A mixed cost has both a variable and a fixed component. $ Level

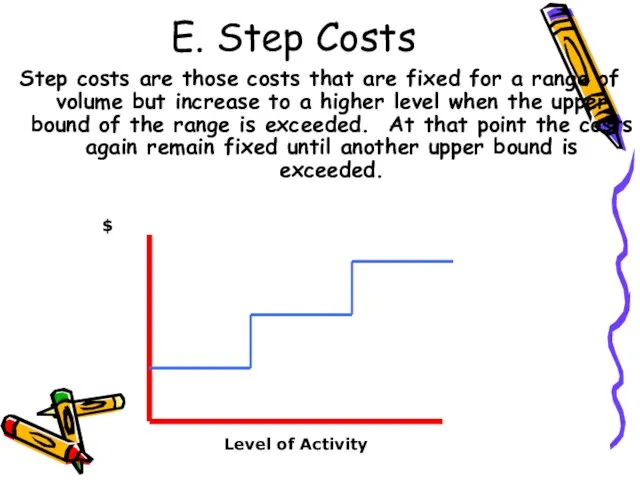

- 36. E. Step Costs Step costs are those costs that are fixed for a range of volume

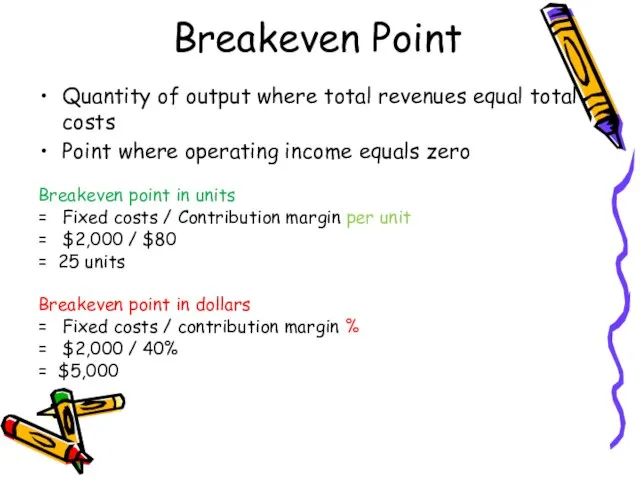

- 37. Breakeven Point Quantity of output where total revenues equal total costs Point where operating income equals

- 38. Cost-Volume-Profit Graph $10,000 $8,000 $6,000 $4,000 $2,000 $0 0 10 20 30 40 50 Units Sold

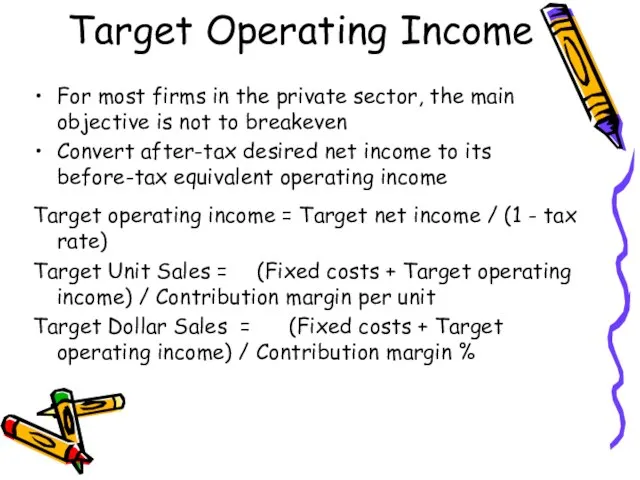

- 39. Target Operating Income For most firms in the private sector, the main objective is not to

- 41. Скачать презентацию

Слайд 31

The earning of net income, or profits, is a major goal of

1

The earning of net income, or profits, is a major goal of

Слайд 4Since business managers and economists use the word profits in somewhat different

Since business managers and economists use the word profits in somewhat different

Слайд 5To determine net income, it is necessary to measure for a given

To determine net income, it is necessary to measure for a given

Слайд 6Revenue is the price of goods sold and services rendered during a

Revenue is the price of goods sold and services rendered during a

Слайд 7Expenses are the cost of the goods and services used up in

Expenses are the cost of the goods and services used up in

Слайд 8Cost –

Variable costs A variable cost increases and decreases directly and

Cost –

Variable costs A variable cost increases and decreases directly and

Слайд 9Classification of costs

2

Classification of costs

2

Слайд 10Classification of costs (cont’d)

Classification of costs (cont’d)

Слайд 11An unit cost shows by itself a money term of charges is

An unit cost shows by itself a money term of charges is

Слайд 12The index of marginal charges is used to the analysis of need

The index of marginal charges is used to the analysis of need

Слайд 133

Price – it is money expression of cost of commodity

Functions of price

3

Price – it is money expression of cost of commodity

Functions of price

Слайд 14Signaling function

Prices perform a signaling function – they adjust to demonstrate where resources are

Signaling function

Prices perform a signaling function – they adjust to demonstrate where resources are

Слайд 15Transmission of preferences

Through their choices consumers send information to producers about the changing nature of needs and

Transmission of preferences

Through their choices consumers send information to producers about the changing nature of needs and

Слайд 16Stimulative function of price - rational use of the limited resources., instrumental

Stimulative function of price - rational use of the limited resources., instrumental

Слайд 17Pricing – it is the process of establishment and putting of prices

Pricing – it is the process of establishment and putting of prices

Слайд 18Factors, which influence on price making process:

Positioning - How are you positioning your

Factors, which influence on price making process:

Positioning - How are you positioning your

Слайд 19Pricing strategies

Short-term profit maximization - This approach is common in companies that are

Pricing strategies

Short-term profit maximization - This approach is common in companies that are

Слайд 20Maximize profit margin - This strategy is most appropriate when the number of

Maximize profit margin - This strategy is most appropriate when the number of

Слайд 21Methods of pricing :

method of estimation of consumer cost;

method of receipt of

Methods of pricing :

method of estimation of consumer cost;

method of receipt of

Слайд 22Psychological pricing - Ultimately, you must take into consideration the consumer's perception of

Psychological pricing - Ultimately, you must take into consideration the consumer's perception of

Слайд 23Cost-plus pricing - Set the price at your production cost, including both cost

Cost-plus pricing - Set the price at your production cost, including both cost

Слайд 24Kinds of prices

all-in -an all-in price includes everything, with no extra charges

all-inclusive

Kinds of prices

all-in -an all-in price includes everything, with no extra charges

all-inclusive

Слайд 25introductory -an introductory offer or price is a low price that is

introductory -an introductory offer or price is a low price that is

Слайд 26To the production prices belong:

wholesale;

of asqusition;

estimate;

Calculation (self-cost)

planned

The lower limit of price is

To the production prices belong:

wholesale;

of asqusition;

estimate;

Calculation (self-cost)

planned

The lower limit of price is

Слайд 27Cost-Volume-Profit Analysis

Examines the behaviour of total revenues, total costs, and operating income

Cost-Volume-Profit Analysis

Examines the behaviour of total revenues, total costs, and operating income

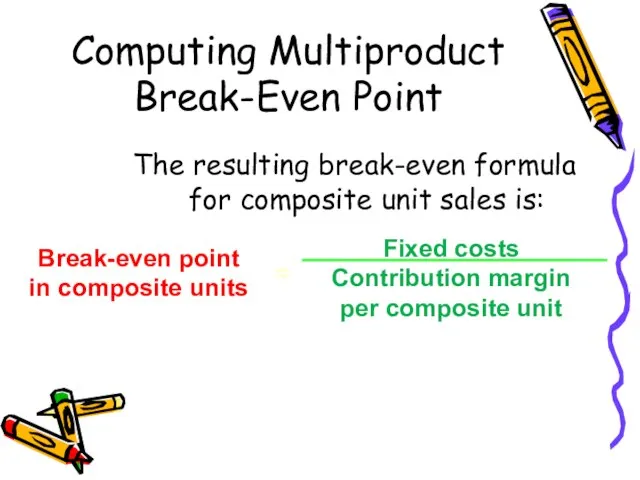

Слайд 28The resulting break-even formula

for composite unit sales is:

Break-even point

in composite units

Fixed costs

Contribution

The resulting break-even formula

for composite unit sales is:

Break-even point

in composite units

Fixed costs Contribution

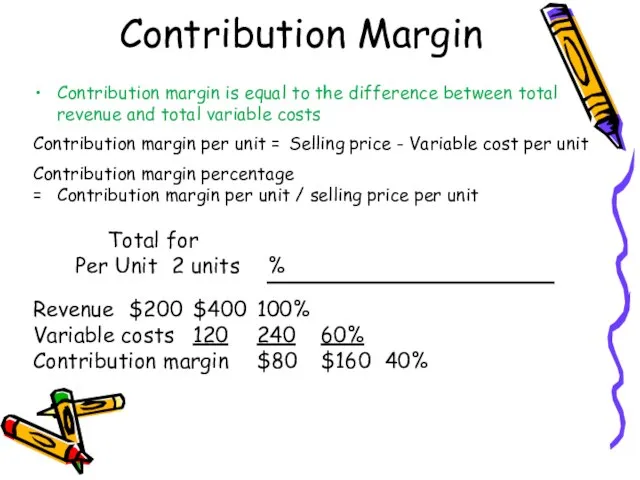

Слайд 29Contribution Margin

Contribution margin is equal to the difference between total revenue and

Contribution Margin

Contribution margin is equal to the difference between total revenue and

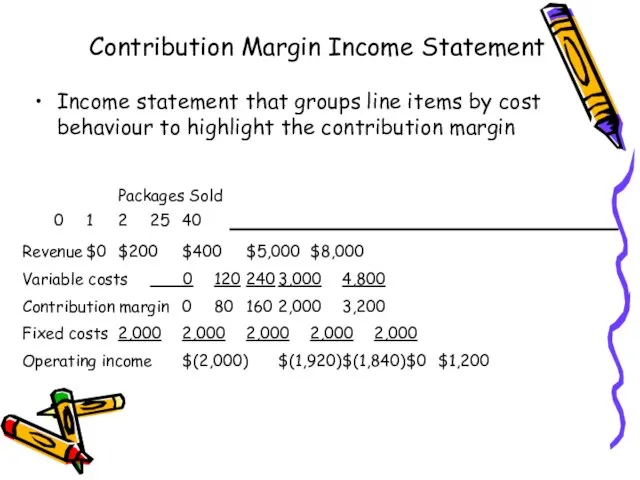

Слайд 30Contribution Margin Income Statement

Packages Sold

0 1 2 25 40

Revenue $0 $200 $400 $5,000 $8,000

Variable costs 0 120 240 3,000 4,800

Contribution margin 0 80 160 2,000 3,200

Fixed costs 2,000 2,000 2,000 2,000 2,000

Operating income $(2,000) $(1,920) $(1,840) $0 $1,200

Income statement that

Contribution Margin Income Statement

Packages Sold

0 1 2 25 40

Revenue $0 $200 $400 $5,000 $8,000

Variable costs 0 120 240 3,000 4,800

Contribution margin 0 80 160 2,000 3,200

Fixed costs 2,000 2,000 2,000 2,000 2,000

Operating income $(2,000) $(1,920) $(1,840) $0 $1,200

Income statement that

Слайд 31I. Common Cost Behavior Patterns

Variable Costs

Fixed Costs

Discretionary versus Committed Fixed Costs

Mixed Costs

Step

I. Common Cost Behavior Patterns

Variable Costs

Fixed Costs

Discretionary versus Committed Fixed Costs

Mixed Costs

Step

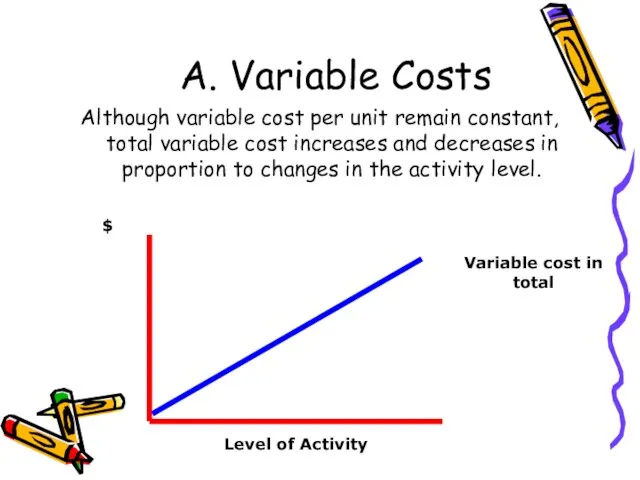

Слайд 32A. Variable Costs

Although variable cost per unit remain constant, total variable cost

A. Variable Costs

Although variable cost per unit remain constant, total variable cost

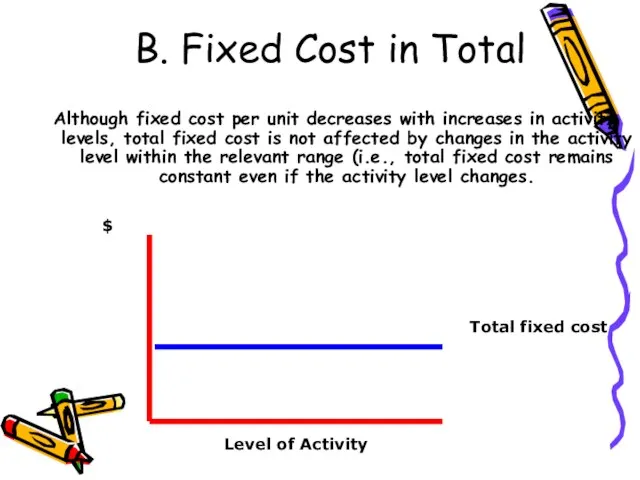

Слайд 33B. Fixed Cost in Total

Although fixed cost per unit decreases with increases

B. Fixed Cost in Total

Although fixed cost per unit decreases with increases

Слайд 34C. Discretionary versus Committed Fixed Costs

Committed Fixed Costs

Examples include rent, depreciation, insurance.

C. Discretionary versus Committed Fixed Costs

Committed Fixed Costs

Examples include rent, depreciation, insurance.

Слайд 35D. Mixed Cost

A mixed cost has both a variable and a fixed

D. Mixed Cost

A mixed cost has both a variable and a fixed

Слайд 36E. Step Costs

Step costs are those costs that are fixed for a

E. Step Costs

Step costs are those costs that are fixed for a

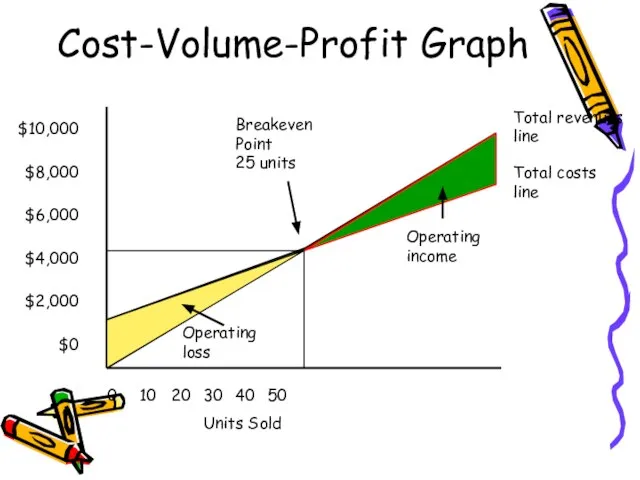

Слайд 37Breakeven Point

Quantity of output where total revenues equal total costs

Point where operating

Breakeven Point

Quantity of output where total revenues equal total costs

Point where operating

Слайд 38Cost-Volume-Profit Graph

$10,000

$8,000

$6,000

$4,000

$2,000

$0

0 10 20 30 40 50

Units Sold

Total revenues

line

Breakeven

Point

25 units

Operating

income

Operating

loss

Total costs

line

Cost-Volume-Profit Graph

$10,000

$8,000

$6,000

$4,000

$2,000

$0

0 10 20 30 40 50

Units Sold

Total revenues

line

Breakeven

Point

25 units

Operating

income

Operating

loss

Total costs

line

Слайд 39Target Operating Income

For most firms in the private sector, the main objective

Target Operating Income

For most firms in the private sector, the main objective

Умирающие и их родственники (72-74)

Умирающие и их родственники (72-74) Рисование ёлочной игрушки

Рисование ёлочной игрушки Зимние забавы группы Солнышко

Зимние забавы группы Солнышко Пищеварение. Желудок

Пищеварение. Желудок Презентация на тему Правила поведения на весенних каникулах

Презентация на тему Правила поведения на весенних каникулах Click to edit Master title style Click to edit Master subtitle style

Click to edit Master title style Click to edit Master subtitle style  Государственные символы Российской Федерации

Государственные символы Российской Федерации Курс лекций по сопротивлению материалов

Курс лекций по сопротивлению материалов Здоровий спосiб життя

Здоровий спосiб життя Семейна псхотерапія,її роль у профілактиці психопатій. Типи неправильного виховання дитини

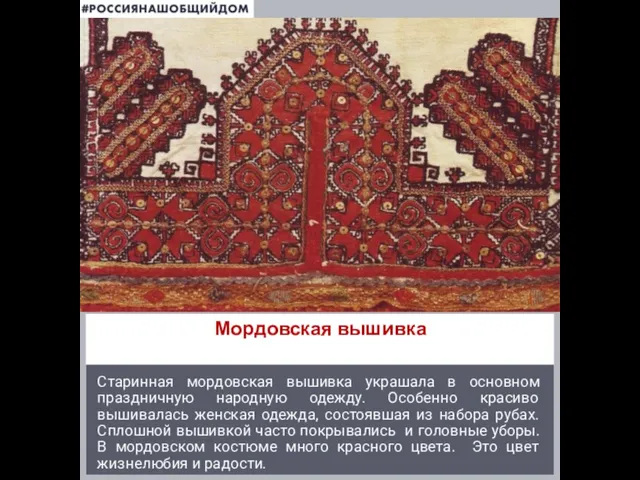

Семейна псхотерапія,її роль у профілактиці психопатій. Типи неправильного виховання дитини Мордовская вышивка

Мордовская вышивка Презентация на тему Модернизм в русской литературе

Презентация на тему Модернизм в русской литературе Гимназия №69 имени Чередова И.М, города Омска

Гимназия №69 имени Чередова И.М, города Омска Описание уровней развития отношения ребенка к той или иной ценности.Это - не точный диагноз, это – тенденция, повод для Вашего пед

Описание уровней развития отношения ребенка к той или иной ценности.Это - не точный диагноз, это – тенденция, повод для Вашего пед RN_block_center_full - презентация

RN_block_center_full - презентация Marketing in China

Marketing in China Презентация на тему Политическая раздробленность Древнерусского государства (XII –XIV века)

Презентация на тему Политическая раздробленность Древнерусского государства (XII –XIV века)  Обобщающий урок по теме «Имя числительное».

Обобщающий урок по теме «Имя числительное». Православный молодежный клуб Восхождение

Православный молодежный клуб Восхождение Я трагедию жизни претворю в грезофарс…Жизнь и творчество И. Северянина

Я трагедию жизни претворю в грезофарс…Жизнь и творчество И. Северянина Презентация на тему Красная книга России

Презентация на тему Красная книга России Свет как экологический фактор

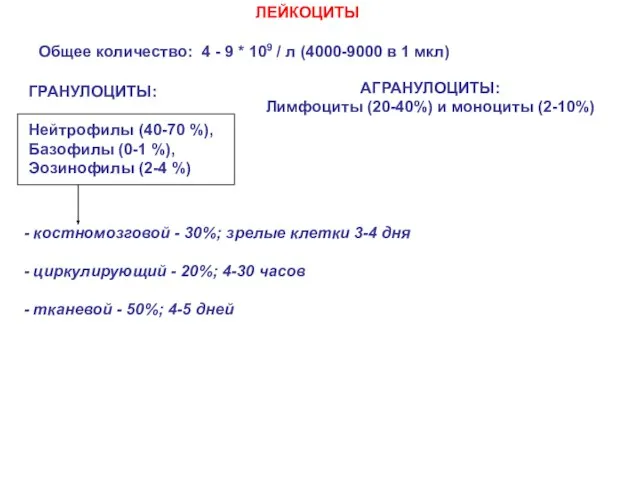

Свет как экологический фактор Лейкоциты

Лейкоциты Travel Notes

Travel Notes Административные механизмы и стимулы в законодательстве об энергосбережении и о повышении энергетической эффективности в Россий

Административные механизмы и стимулы в законодательстве об энергосбережении и о повышении энергетической эффективности в Россий Торт Сникерс по-удмуртски

Торт Сникерс по-удмуртски Интерактивный тест ГИА по математике 9 класс

Интерактивный тест ГИА по математике 9 класс Кошки – домашние животные

Кошки – домашние животные