- Session 2_Annuities, Perpetuities and Other Special Cases

Содержание

- 2. The formulas we have developed so far allow us to compute the present or future value

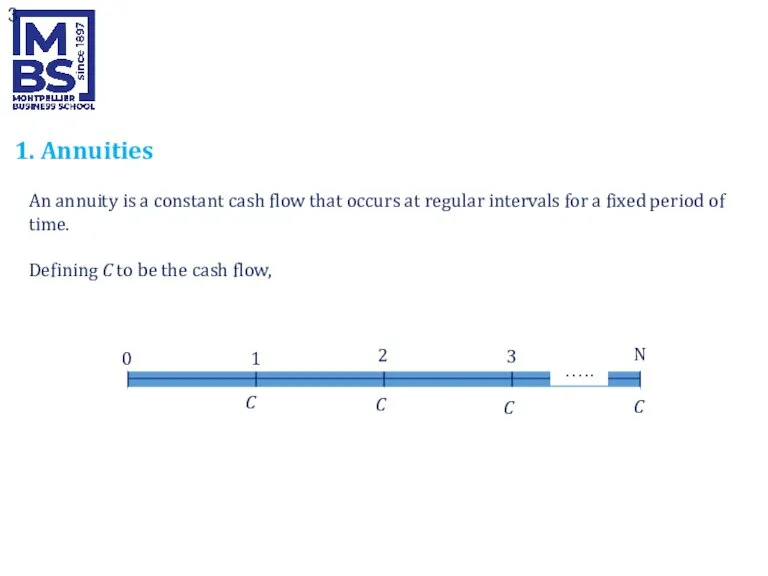

- 3. 1. Annuities An annuity is a constant cash flow that occurs at regular intervals for a

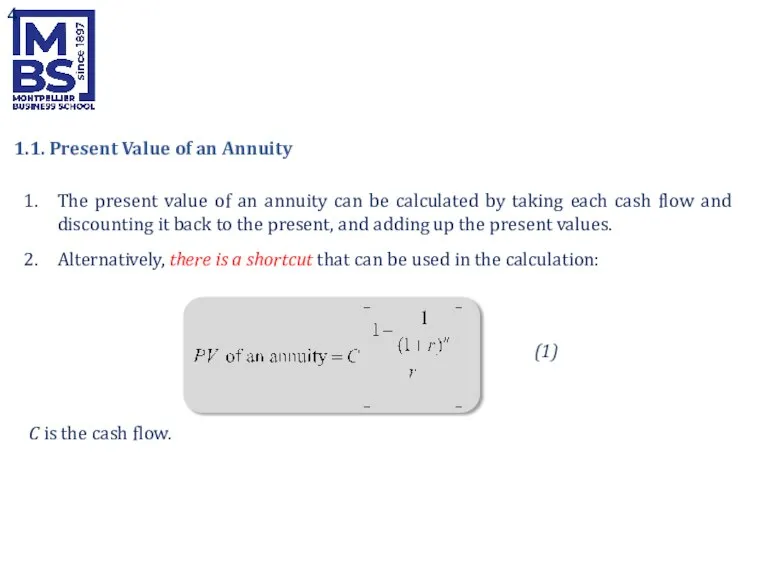

- 4. 1.1. Present Value of an Annuity The present value of an annuity can be calculated by

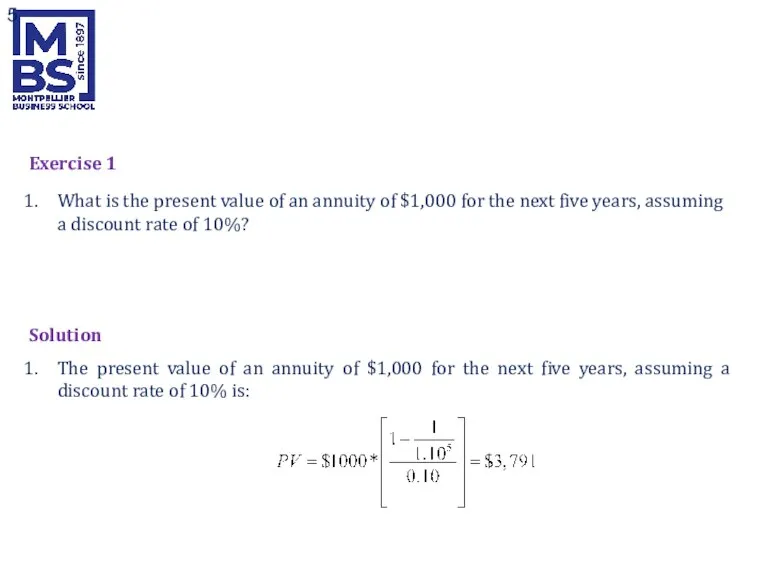

- 5. Exercise 1 What is the present value of an annuity of $1,000 for the next five

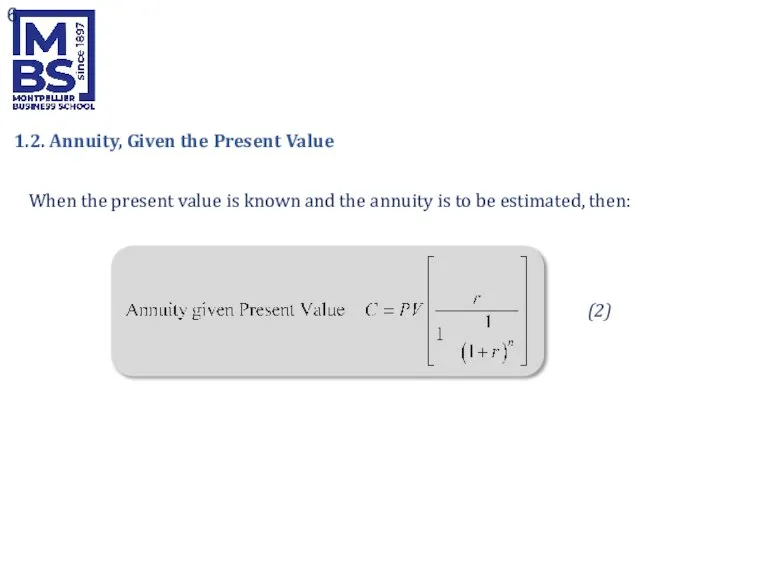

- 6. When the present value is known and the annuity is to be estimated, then: 1.2. Annuity,

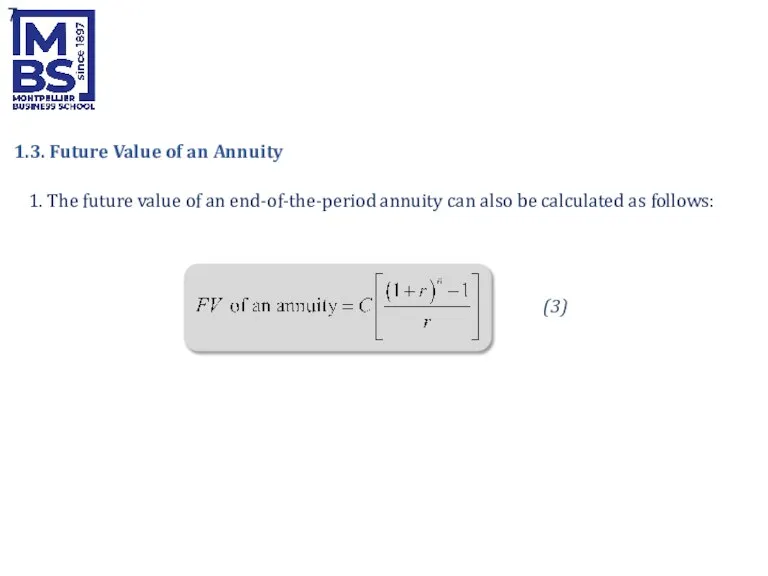

- 7. 1. The future value of an end-of-the-period annuity can also be calculated as follows: 1.3. Future

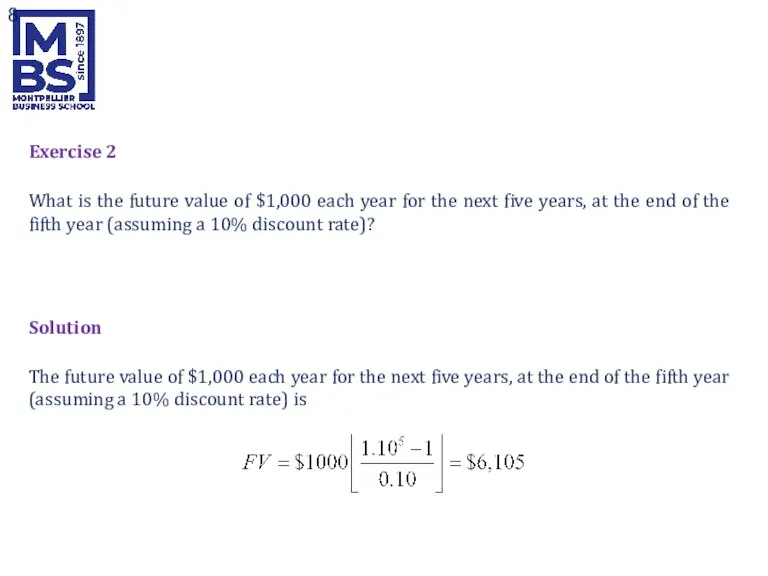

- 8. Exercise 2 What is the future value of $1,000 each year for the next five years,

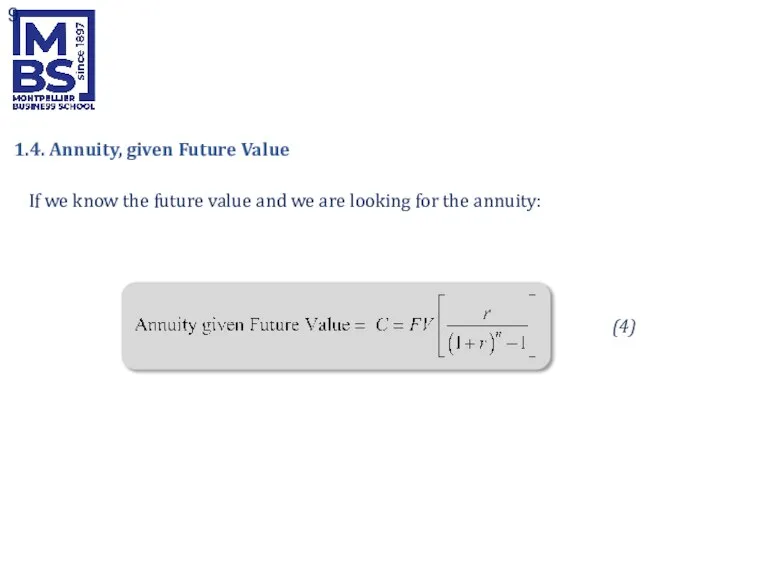

- 9. If we know the future value and we are looking for the annuity: 1.4. Annuity, given

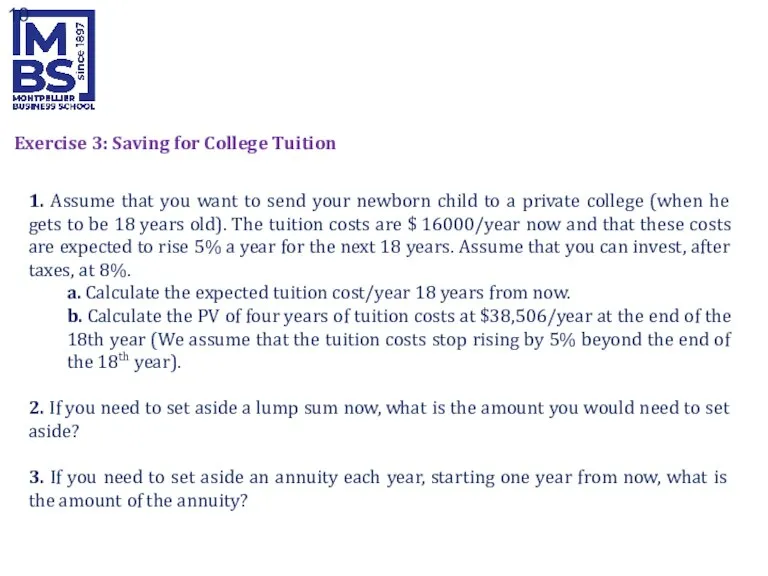

- 10. Exercise 3: Saving for College Tuition 1. Assume that you want to send your newborn child

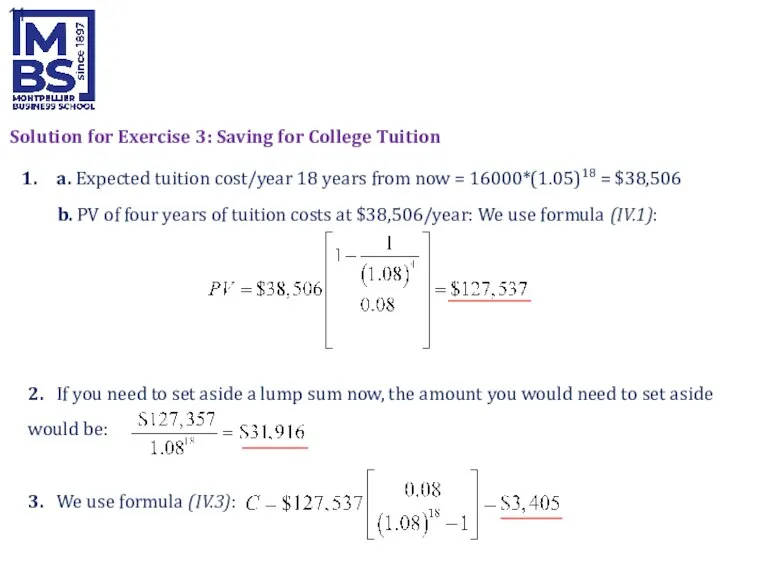

- 11. Solution for Exercise 3: Saving for College Tuition a. Expected tuition cost/year 18 years from now

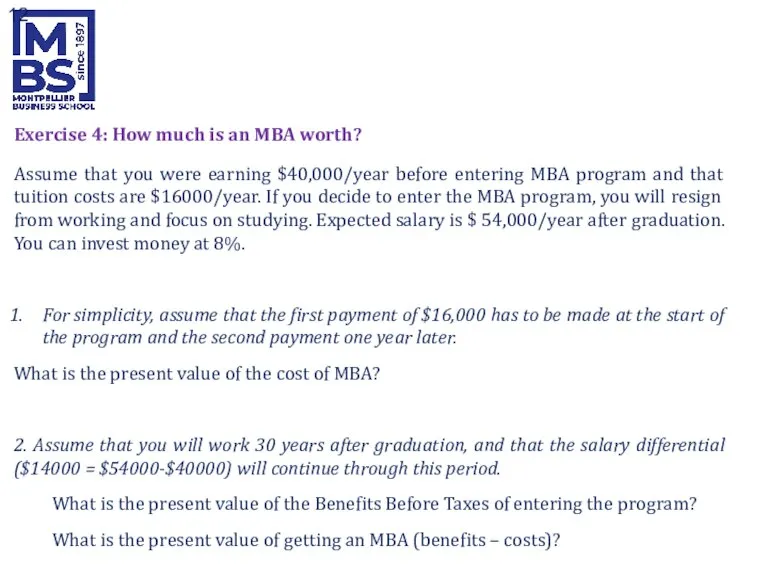

- 12. Exercise 4: How much is an MBA worth? Assume that you were earning $40,000/year before entering

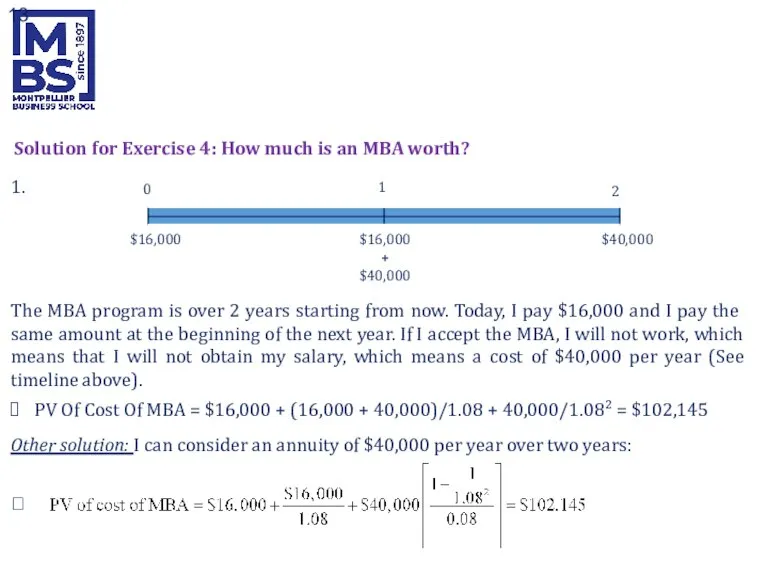

- 13. Solution for Exercise 4: How much is an MBA worth? 1. The MBA program is over

- 14. Solution for Exercise 4: How much is an MBA worth? 2. This has to be discounted

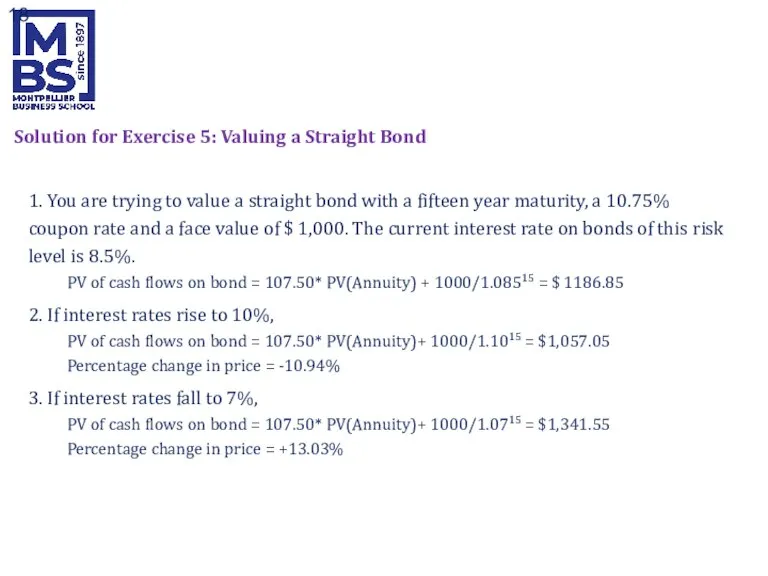

- 15. Exercise 5: Valuing a Straight Bond 1. You are trying to value a straight bond with

- 16. Solution for Exercise 5: Valuing a Straight Bond 1. You are trying to value a straight

- 17. 1. You are trying to value a straight bond with a fifteen year maturity, a 10.75%

- 18. 1. You are trying to value a straight bond with a fifteen year maturity, a 10.75%

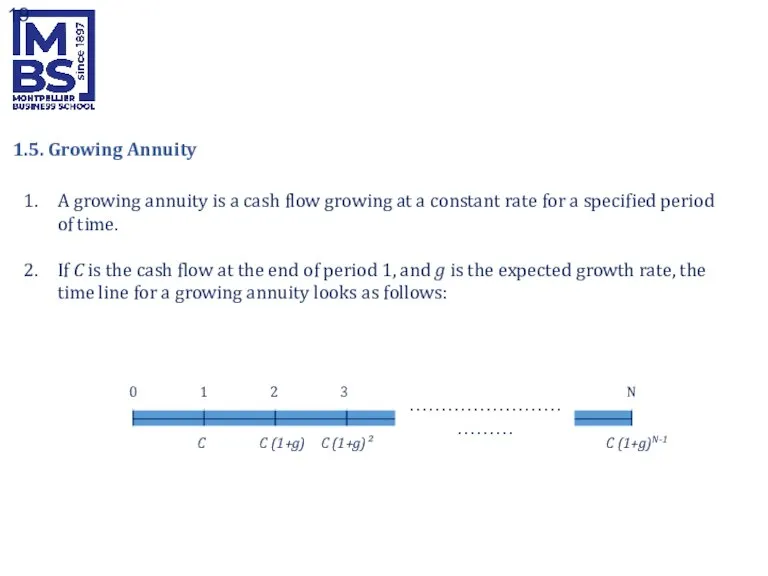

- 19. A growing annuity is a cash flow growing at a constant rate for a specified period

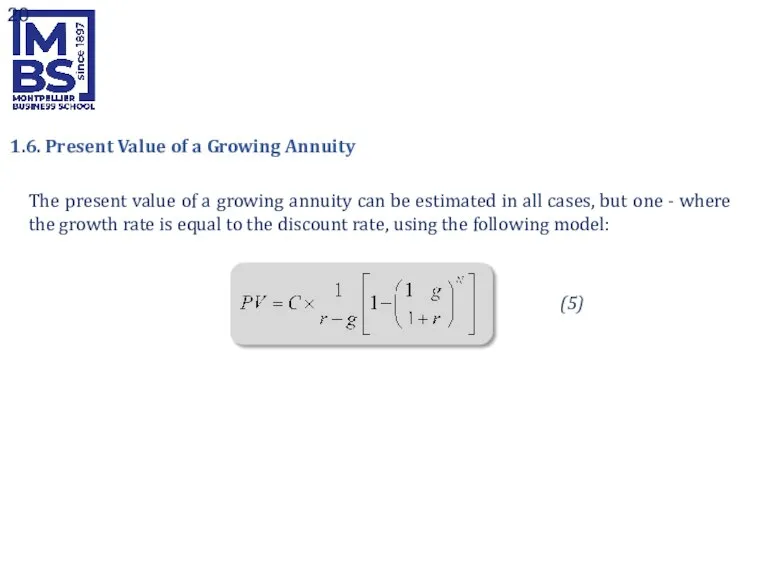

- 20. The present value of a growing annuity can be estimated in all cases, but one -

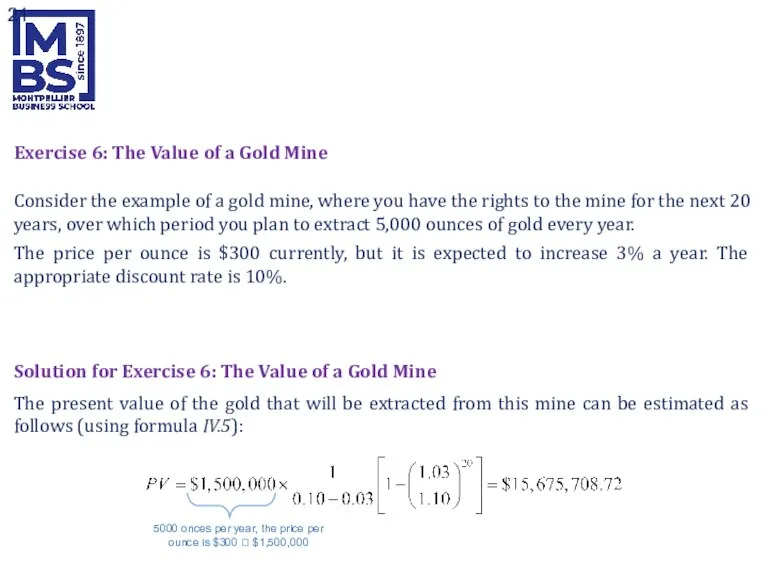

- 21. Exercise 6: The Value of a Gold Mine Consider the example of a gold mine, where

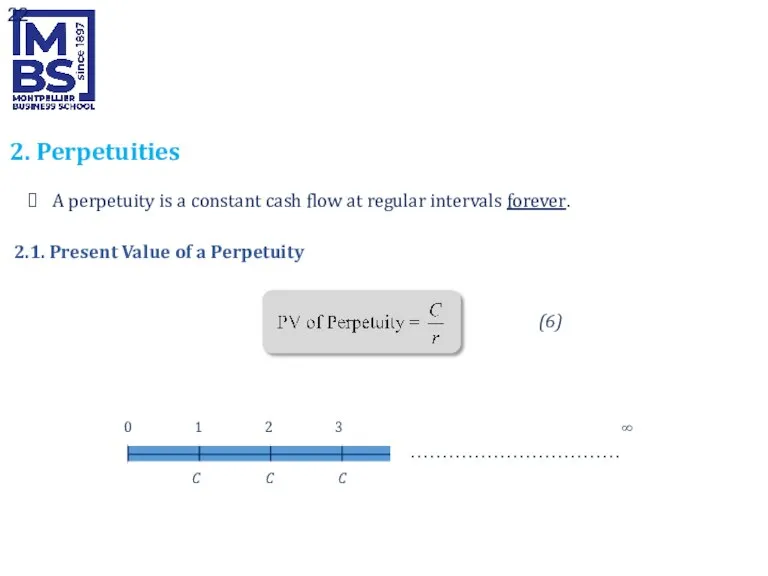

- 22. A perpetuity is a constant cash flow at regular intervals forever. 2. Perpetuities …………………………… 0 2

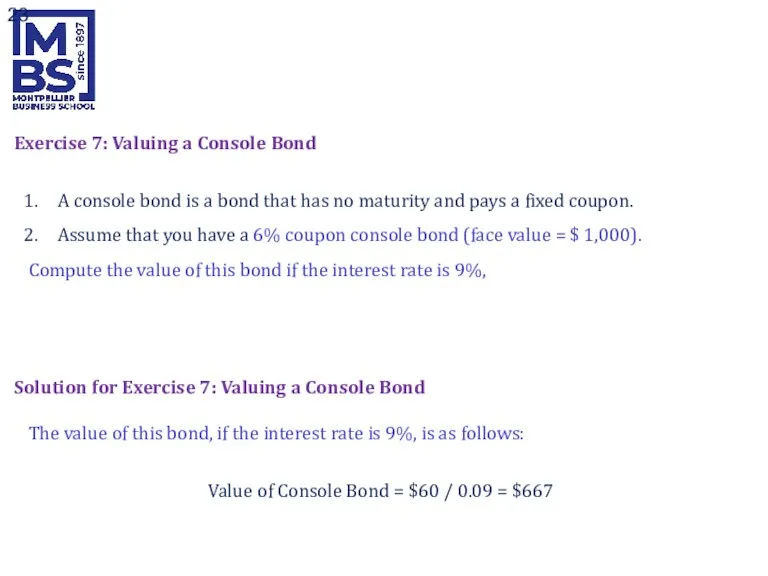

- 23. Exercise 7: Valuing a Console Bond A console bond is a bond that has no maturity

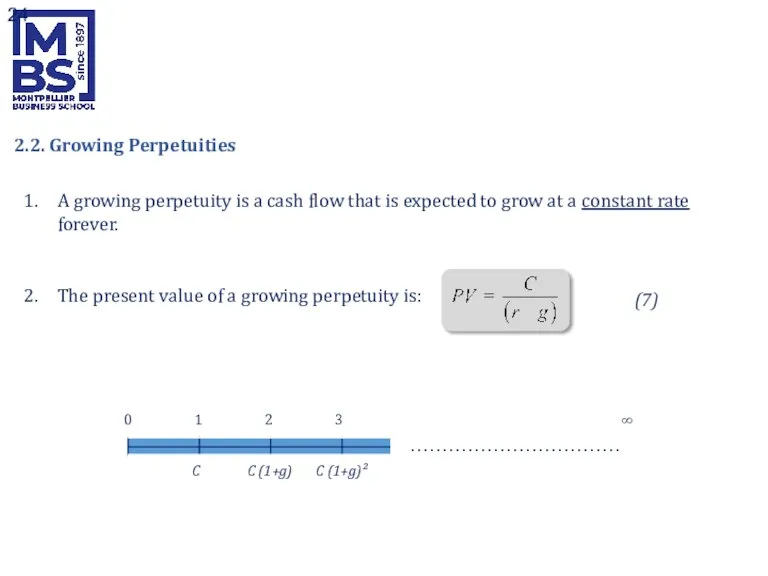

- 24. A growing perpetuity is a cash flow that is expected to grow at a constant rate

- 26. Скачать презентацию

Слайд 31. Annuities

An annuity is a constant cash flow that occurs at regular

1. Annuities

An annuity is a constant cash flow that occurs at regular

Слайд 41.1. Present Value of an Annuity

The present value of an annuity can

1.1. Present Value of an Annuity

The present value of an annuity can

Слайд 5Exercise 1

What is the present value of an annuity of $1,000 for

Exercise 1

What is the present value of an annuity of $1,000 for

Слайд 6When the present value is known and the annuity is to be

When the present value is known and the annuity is to be

Слайд 71. The future value of an end-of-the-period annuity can also be calculated

1. The future value of an end-of-the-period annuity can also be calculated

Слайд 8Exercise 2

What is the future value of $1,000 each year for the

Exercise 2

What is the future value of $1,000 each year for the

Слайд 9If we know the future value and we are looking for the

If we know the future value and we are looking for the

Слайд 10Exercise 3: Saving for College Tuition

1. Assume that you want to send

Exercise 3: Saving for College Tuition

1. Assume that you want to send

Слайд 11Solution for Exercise 3: Saving for College Tuition

a. Expected tuition cost/year 18

Solution for Exercise 3: Saving for College Tuition

a. Expected tuition cost/year 18

Слайд 12Exercise 4: How much is an MBA worth?

Assume that you were earning

Exercise 4: How much is an MBA worth?

Assume that you were earning

Слайд 13Solution for Exercise 4: How much is an MBA worth?

1.

The MBA

Solution for Exercise 4: How much is an MBA worth?

1.

The MBA

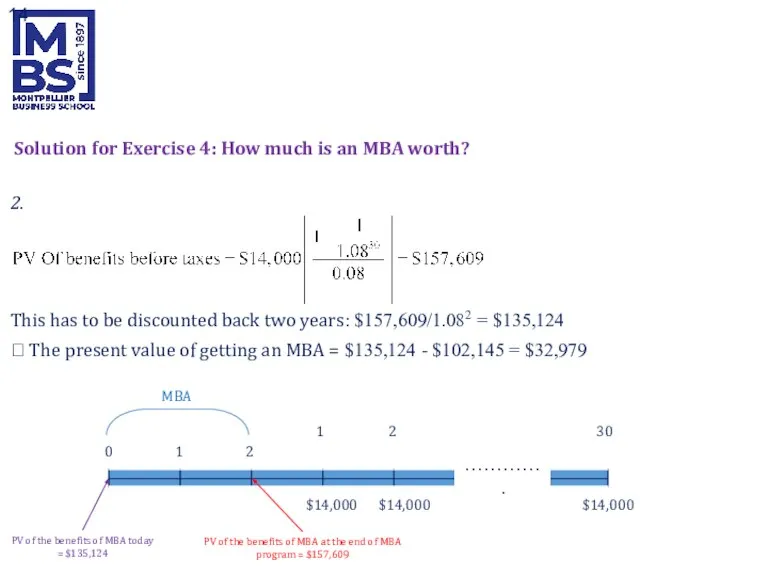

Слайд 14Solution for Exercise 4: How much is an MBA worth?

2.

This has

Solution for Exercise 4: How much is an MBA worth?

2.

This has

Слайд 15Exercise 5: Valuing a Straight Bond

1. You are trying to value a

Exercise 5: Valuing a Straight Bond

1. You are trying to value a

Слайд 16Solution for Exercise 5: Valuing a Straight Bond

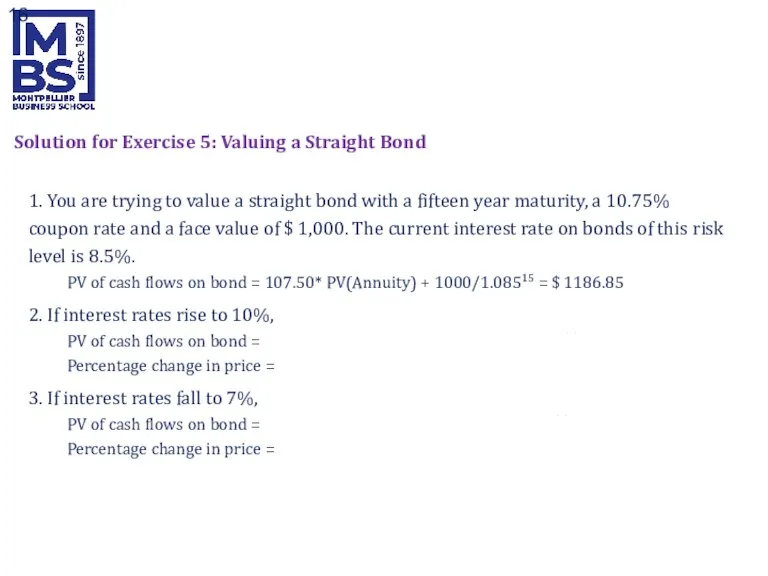

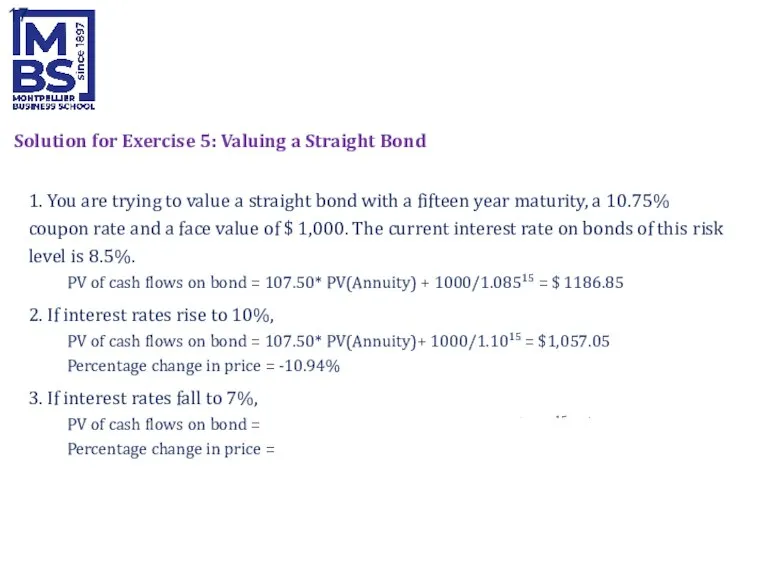

1. You are trying to

Solution for Exercise 5: Valuing a Straight Bond

1. You are trying to

Слайд 171. You are trying to value a straight bond with a fifteen

1. You are trying to value a straight bond with a fifteen

Слайд 181. You are trying to value a straight bond with a fifteen

1. You are trying to value a straight bond with a fifteen

Слайд 19A growing annuity is a cash flow growing at a constant rate

A growing annuity is a cash flow growing at a constant rate

Слайд 20The present value of a growing annuity can be estimated in all

The present value of a growing annuity can be estimated in all

Слайд 21Exercise 6: The Value of a Gold Mine

Consider the example of a

Exercise 6: The Value of a Gold Mine

Consider the example of a

Слайд 22A perpetuity is a constant cash flow at regular intervals forever.

2.

A perpetuity is a constant cash flow at regular intervals forever.

2.

Слайд 23Exercise 7: Valuing a Console Bond

A console bond is a bond that

Exercise 7: Valuing a Console Bond

A console bond is a bond that

Слайд 24A growing perpetuity is a cash flow that is expected to grow

A growing perpetuity is a cash flow that is expected to grow

КАДРОВАЯ ПОЛИТИКАв области найма, адаптации и мотивации персонала

КАДРОВАЯ ПОЛИТИКАв области найма, адаптации и мотивации персонала Відділ зовнішніх зв'язків університету ім. О.О. Богомольця

Відділ зовнішніх зв'язків університету ім. О.О. Богомольця Предпринимательское мышление

Предпринимательское мышление Повелитель молний Никола Тесла

Повелитель молний Никола Тесла Свойства логарифмов

Свойства логарифмов  Линейные индикаторные диаграммы

Линейные индикаторные диаграммы Презентация на тему "Воспитание культуры поведения ребёнка" - скачать презентации по Педагогике

Презентация на тему "Воспитание культуры поведения ребёнка" - скачать презентации по Педагогике Работающие примеры Как вести торговлю в социальных сетях? - презентация

Работающие примеры Как вести торговлю в социальных сетях? - презентация Чеченцы XIX ― XX вв

Чеченцы XIX ― XX вв Лекция 1 (1)

Лекция 1 (1) Война в судьбе моей семьи

Война в судьбе моей семьи Об итогах летней оздоровительной кампании 2011 года в Ленинградской области и задачах по подготовке загородных летних оздоровитель

Об итогах летней оздоровительной кампании 2011 года в Ленинградской области и задачах по подготовке загородных летних оздоровитель Первая женщина- космонавт

Первая женщина- космонавт 28 мая - День пограничника!

28 мая - День пограничника! Волшебный праздник Рождество

Волшебный праздник Рождество ТАРИФНОЕ РЕГУЛИРОВАНИЕ КОМПЛЕКСА ТЕПЛОСНАБЖЕНИЯ КЕМЕРОВСКОЙ ОБЛАСТИ

ТАРИФНОЕ РЕГУЛИРОВАНИЕ КОМПЛЕКСА ТЕПЛОСНАБЖЕНИЯ КЕМЕРОВСКОЙ ОБЛАСТИ День Матери

День Матери Экспозиция Музея чувашской вышивки

Экспозиция Музея чувашской вышивки Religious and ethnic diversity in the USA

Religious and ethnic diversity in the USA 못 VS 을 수 없다

못 VS 을 수 없다 «Энергоэффективная технологическая система пеллетизации органических отходов ООО «Экологические системы»»

«Энергоэффективная технологическая система пеллетизации органических отходов ООО «Экологические системы»» Качество муниципальных услуг: основные подходы к оценке и разработка стандарта 2009 г.

Качество муниципальных услуг: основные подходы к оценке и разработка стандарта 2009 г. Электролиз

Электролиз XII традиционный легкоатлетический пробег памяти В.И. Мусихина

XII традиционный легкоатлетический пробег памяти В.И. Мусихина Организация и законодательная основа таможенного дела в РФ

Организация и законодательная основа таможенного дела в РФ Гимназия № 18 г. Краснодара

Гимназия № 18 г. Краснодара Стратегия продвижения компаний и проектов в социальных сетях. INTOURFEST 2012

Стратегия продвижения компаний и проектов в социальных сетях. INTOURFEST 2012 Мы хотим поступить ВУЗ

Мы хотим поступить ВУЗ