- The Costs of Production

Содержание

- 2. What are Costs? Total revenue Amount a firm receives for the sale of its output Total

- 3. What are Costs? Costs as opportunity costs The cost of something is what you give up

- 4. What are Costs? Costs as opportunity costs Explicit costs Input costs that require an outlay of

- 5. What are Costs? The cost of capital as an opportunity cost Implicit cost Interest income not

- 6. What are Costs? Economic profit Total revenue minus total cost Including both explicit and implicit costs

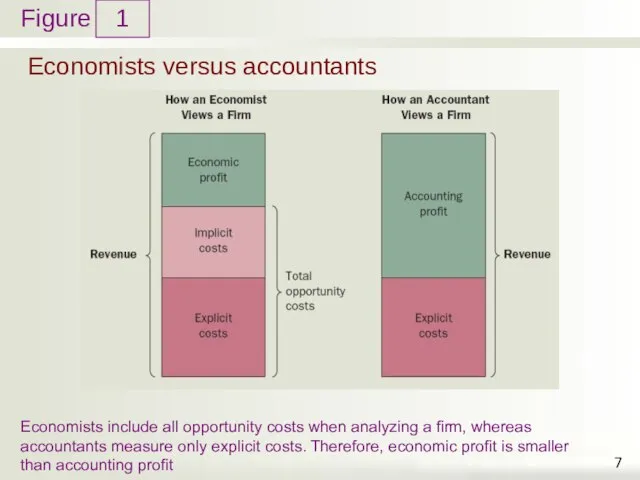

- 7. Economists versus accountants 1 Economists include all opportunity costs when analyzing a firm, whereas accountants measure

- 8. Production and Costs Production function Relationship between Quantity of inputs used to make a good And

- 9. Production and Costs Diminishing marginal product Marginal product of an input declines as the quantity of

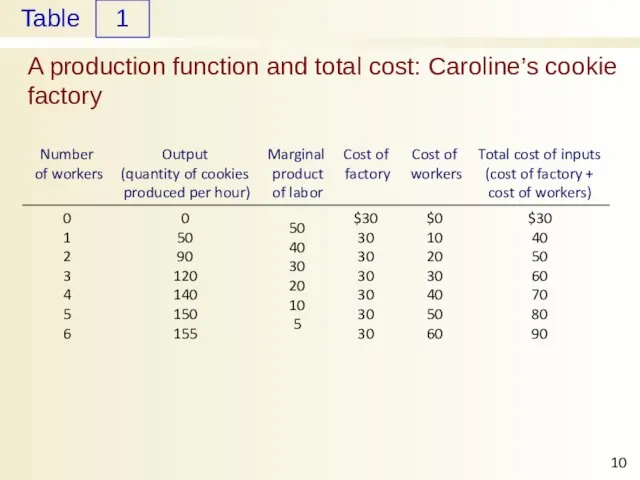

- 10. A production function and total cost: Caroline’s cookie factory 1

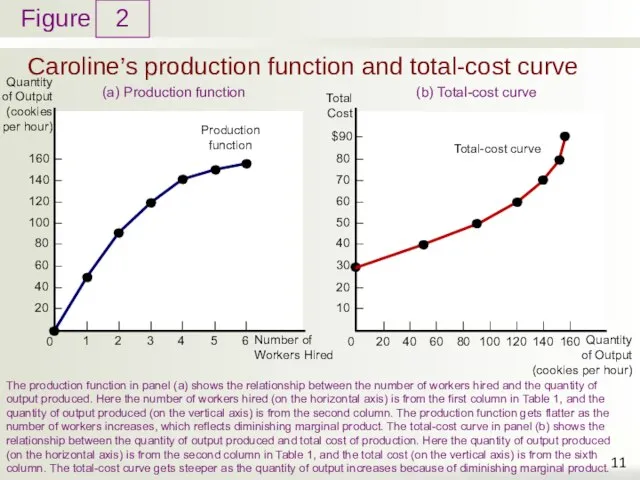

- 11. Caroline’s production function and total-cost curve 2 (a) Production function The production function in panel (a)

- 12. The Various Measures of Cost Fixed costs Do not vary with the quantity of output produced

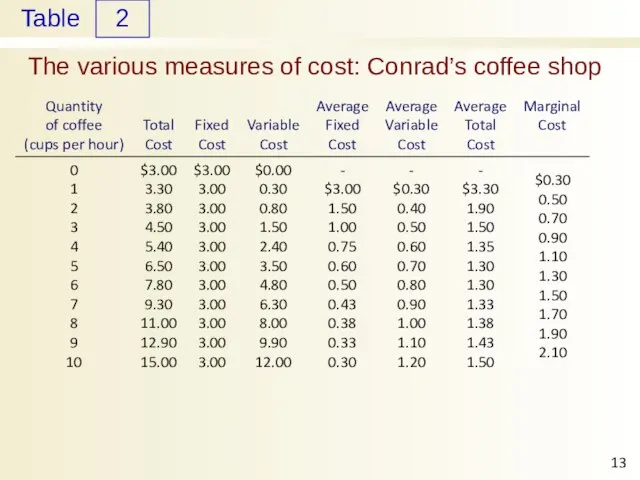

- 13. The various measures of cost: Conrad’s coffee shop 2

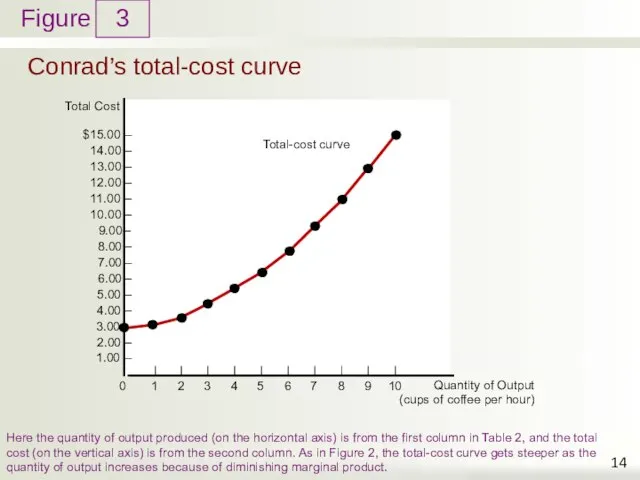

- 14. Conrad’s total-cost curve 3 Here the quantity of output produced (on the horizontal axis) is from

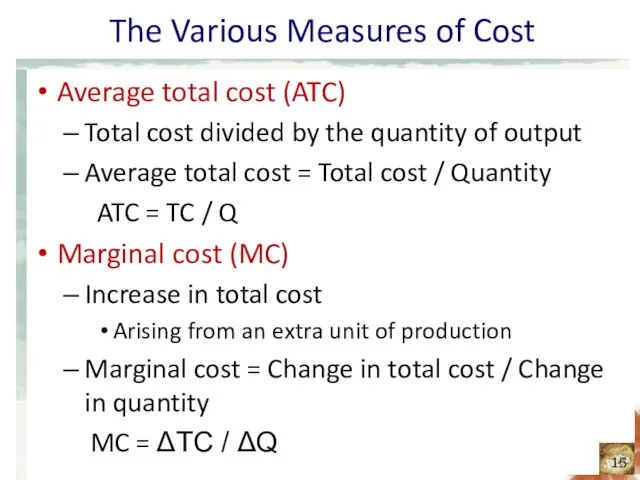

- 15. The Various Measures of Cost Average total cost (ATC) Total cost divided by the quantity of

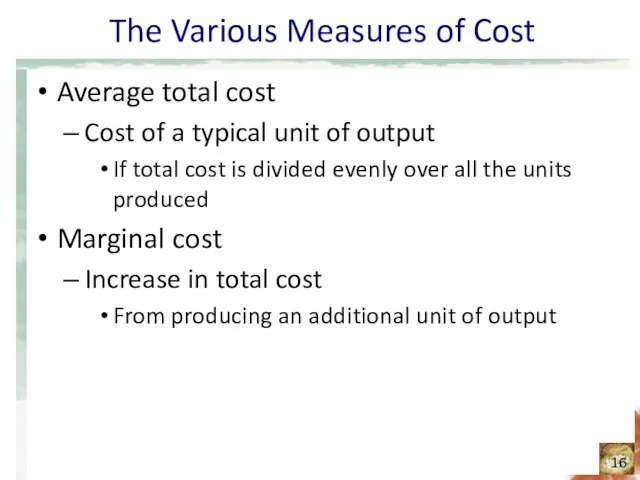

- 16. The Various Measures of Cost Average total cost Cost of a typical unit of output If

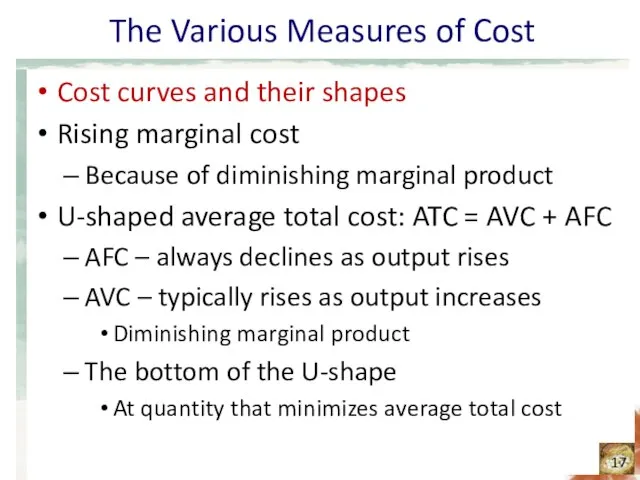

- 17. The Various Measures of Cost Cost curves and their shapes Rising marginal cost Because of diminishing

- 18. The Various Measures of Cost Cost curves and their shapes Efficient scale Quantity of output that

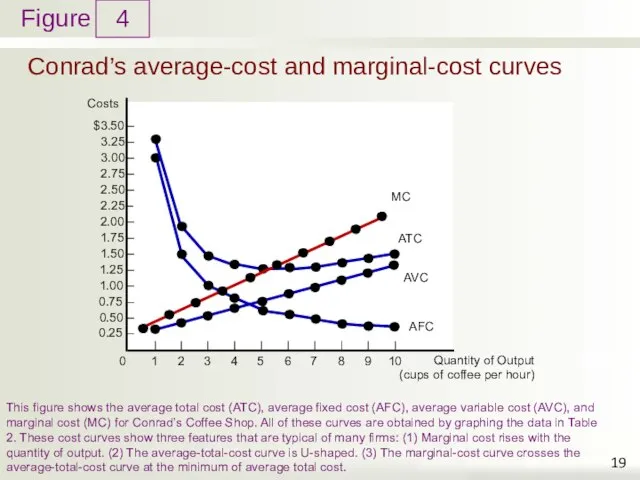

- 19. Conrad’s average-cost and marginal-cost curves 4 This figure shows the average total cost (ATC), average fixed

- 20. The Various Measures of Cost Typical cost curves Marginal cost eventually rises with the quantity of

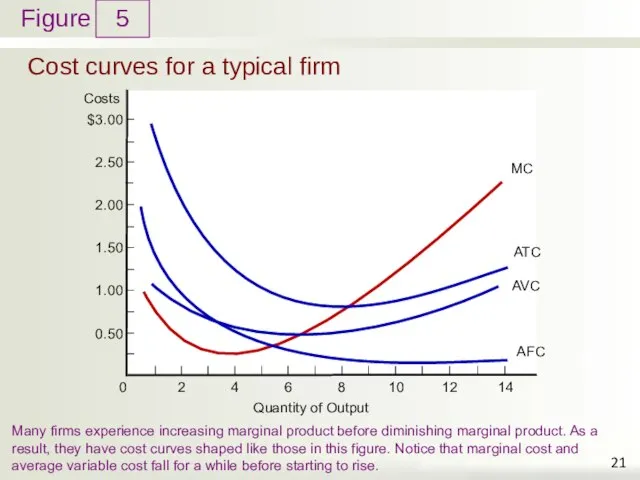

- 21. Cost curves for a typical firm 5 Many firms experience increasing marginal product before diminishing marginal

- 22. Costs in Short Run and in Long Run Many decisions Fixed in the short run Variable

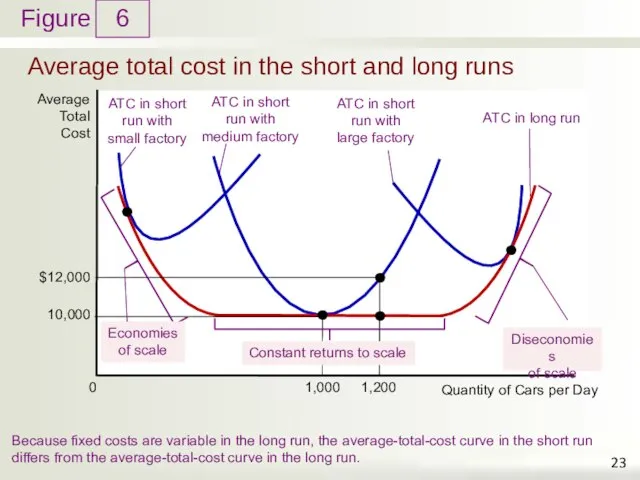

- 23. Average total cost in the short and long runs 6 Because fixed costs are variable in

- 24. Costs in Short Run and in Long Run Economies of scale Long-run average total cost falls

- 25. Costs in Short Run and in Long Run Diseconomies of scale Long-run average total cost rises

- 27. Скачать презентацию

Слайд 3What are Costs?

Costs as opportunity costs

The cost of something is what you

What are Costs?

Costs as opportunity costs

The cost of something is what you

Слайд 4What are Costs?

Costs as opportunity costs

Explicit costs

Input costs that require an outlay

What are Costs?

Costs as opportunity costs

Explicit costs

Input costs that require an outlay

Слайд 5What are Costs?

The cost of capital as an opportunity cost

Implicit cost

Interest income

What are Costs?

The cost of capital as an opportunity cost

Implicit cost

Interest income

Слайд 6What are Costs?

Economic profit

Total revenue minus total cost

Including both explicit and implicit

What are Costs?

Economic profit

Total revenue minus total cost

Including both explicit and implicit

Слайд 7Economists versus accountants

1

Economists include all opportunity costs when analyzing a firm, whereas

Economists versus accountants

1

Economists include all opportunity costs when analyzing a firm, whereas

Слайд 8Production and Costs

Production function

Relationship between

Quantity of inputs used to make a good

And

Production and Costs

Production function

Relationship between

Quantity of inputs used to make a good

And

Слайд 9Production and Costs

Diminishing marginal product

Marginal product of an input declines as the

Production and Costs

Diminishing marginal product

Marginal product of an input declines as the

Слайд 10A production function and total cost: Caroline’s cookie factory

1

A production function and total cost: Caroline’s cookie factory

1

Слайд 11Caroline’s production function and total-cost curve

2

(a) Production function

The production function in panel

Caroline’s production function and total-cost curve

2

(a) Production function

The production function in panel

Слайд 12The Various Measures of Cost

Fixed costs

Do not vary with the quantity of

The Various Measures of Cost

Fixed costs

Do not vary with the quantity of

Слайд 13The various measures of cost: Conrad’s coffee shop

2

The various measures of cost: Conrad’s coffee shop

2

Слайд 14Conrad’s total-cost curve

3

Here the quantity of output produced (on the horizontal axis)

Conrad’s total-cost curve

3

Here the quantity of output produced (on the horizontal axis)

Слайд 15The Various Measures of Cost

Average total cost (ATC)

Total cost divided by the

The Various Measures of Cost

Average total cost (ATC)

Total cost divided by the

Слайд 16The Various Measures of Cost

Average total cost

Cost of a typical unit of

The Various Measures of Cost

Average total cost

Cost of a typical unit of

Слайд 17The Various Measures of Cost

Cost curves and their shapes

Rising marginal cost

Because of

The Various Measures of Cost

Cost curves and their shapes

Rising marginal cost

Because of

Слайд 18The Various Measures of Cost

Cost curves and their shapes

Efficient scale

Quantity of output

The Various Measures of Cost

Cost curves and their shapes

Efficient scale

Quantity of output

Слайд 19Conrad’s average-cost and marginal-cost curves

4

This figure shows the average total cost (ATC),

Conrad’s average-cost and marginal-cost curves

4

This figure shows the average total cost (ATC),

Слайд 20The Various Measures of Cost

Typical cost curves

Marginal cost eventually rises with

The Various Measures of Cost

Typical cost curves

Marginal cost eventually rises with

Слайд 21Cost curves for a typical firm

5

Many firms experience increasing marginal product before

Cost curves for a typical firm

5

Many firms experience increasing marginal product before

Слайд 22Costs in Short Run and in Long Run

Many decisions

Fixed in the short

Costs in Short Run and in Long Run

Many decisions

Fixed in the short

Слайд 23Average total cost in the short and long runs

6

Because fixed costs are

Average total cost in the short and long runs

6

Because fixed costs are

Слайд 24Costs in Short Run and in Long Run

Economies of scale

Long-run average total

Costs in Short Run and in Long Run

Economies of scale

Long-run average total

Слайд 25Costs in Short Run and in Long Run

Diseconomies of scale

Long-run average total

Costs in Short Run and in Long Run

Diseconomies of scale

Long-run average total

Презентация на тему Чем опасно селфи

Презентация на тему Чем опасно селфи Организация и технология торговли в специализированных продовольственных магазинах. Продажа спортивных товаров

Организация и технология торговли в специализированных продовольственных магазинах. Продажа спортивных товаров Мировые финансовые рынки

Мировые финансовые рынки ООО Мелон

ООО Мелон Право природопользования

Право природопользования Презентация на тему Сергей Васильевич Рахманинов

Презентация на тему Сергей Васильевич Рахманинов Косплей. Фарфоровая кожа

Косплей. Фарфоровая кожа Презентация на тему Информация ее хранение и способы передачи

Презентация на тему Информация ее хранение и способы передачи Информацияо результатах деятельности за 2010 годотдела управления предприятиями и организациями

Информацияо результатах деятельности за 2010 годотдела управления предприятиями и организациями Кодирование информации. Двоичное кодирование информации

Кодирование информации. Двоичное кодирование информации Методы обнаружения фальсификации рыбной муки

Методы обнаружения фальсификации рыбной муки Презентация на тему Политическая система и политический режим

Презентация на тему Политическая система и политический режим  Кодекс профессиональной этики проводника пассажирского вагона

Кодекс профессиональной этики проводника пассажирского вагона Традесканция

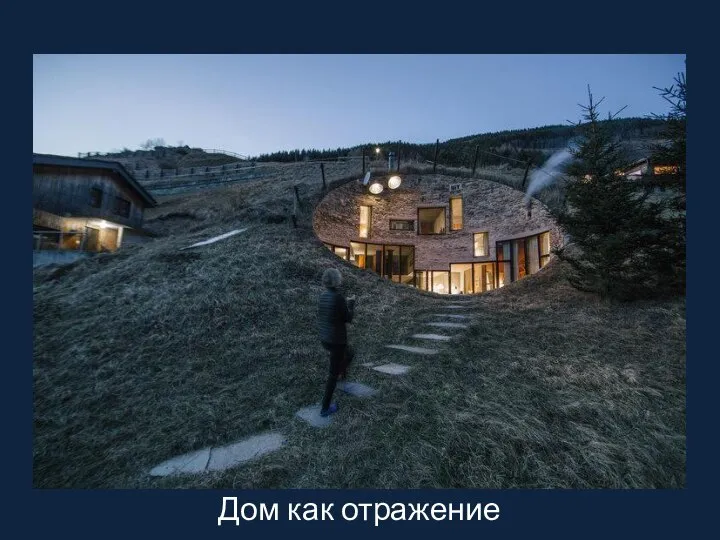

Традесканция Дом как отражение личности

Дом как отражение личности 663980 Красноярский край, г.Бородино, мкрн. Победы, 4. Тел. 8-391-68-3-32-27

663980 Красноярский край, г.Бородино, мкрн. Победы, 4. Тел. 8-391-68-3-32-27 Оптимизация конверсии

Оптимизация конверсии Эпидемиологический надзор за ВИЧ-инфекцией Киев, 1 июня 2010 г.

Эпидемиологический надзор за ВИЧ-инфекцией Киев, 1 июня 2010 г. Это презентационный материал концепции развития Сергиева Посада как столицы Православия был подготовлен в 2007 году. Заказчиками и

Это презентационный материал концепции развития Сергиева Посада как столицы Православия был подготовлен в 2007 году. Заказчиками и  8 шагов на пути успешного решения проблем

8 шагов на пути успешного решения проблем Скифы 11 класс

Скифы 11 класс Преимущества программы «1С:Зарплата и Управление Персоналом 8» при переходе с «1С:Зарплата и Кадры 7.7»

Преимущества программы «1С:Зарплата и Управление Персоналом 8» при переходе с «1С:Зарплата и Кадры 7.7» Устройство освещения пешеходного перехода.

Устройство освещения пешеходного перехода. Отчёт директора МБУ ДО ДШИ №1

Отчёт директора МБУ ДО ДШИ №1 Производительность МП и ее тестирование

Производительность МП и ее тестирование Как продавать продукты Embarcadero

Как продавать продукты Embarcadero Универсальные учебные действия в реализации системно – деятельностного подхода

Универсальные учебные действия в реализации системно – деятельностного подхода Презентация на тему Сергей Павлович Королев

Презентация на тему Сергей Павлович Королев