- Bond valuation (lecture 3)

Содержание

- 2. Lecture 3. Bond Valuation

- 3. Definition of Bond Terminology & Characteristics of Bonds Bond Valuation Premium Bonds vs Discount Bonds Yield

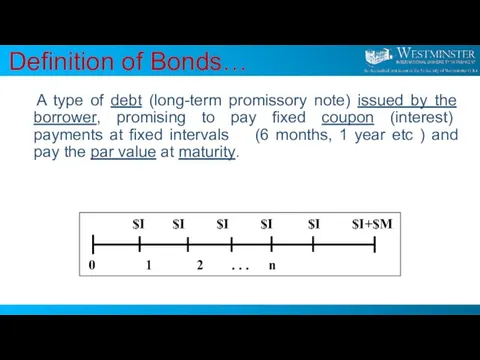

- 4. A type of debt (long-term promissory note) issued by the borrower, promising to pay fixed coupon

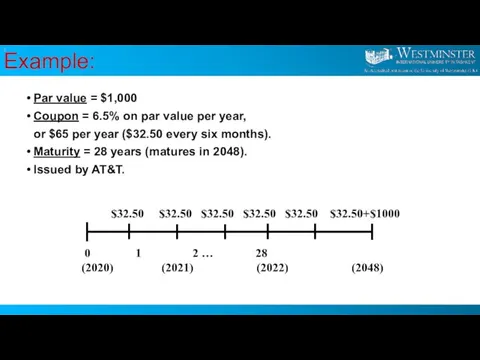

- 5. Par value = $1,000 Coupon = 6.5% on par value per year, or $65 per year

- 6. Bonds

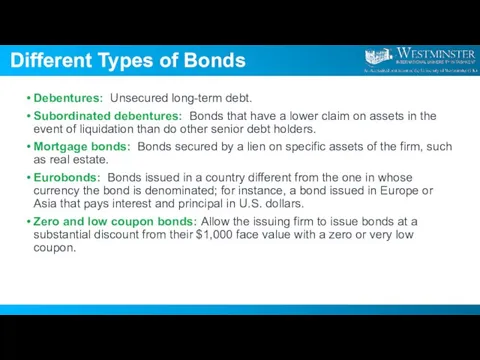

- 7. Different Types of Bonds Debentures: Unsecured long-term debt. Subordinated debentures: Bonds that have a lower claim

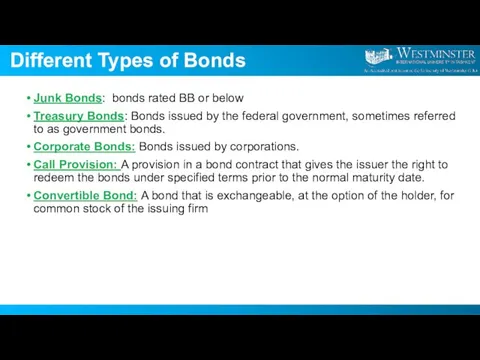

- 8. Different Types of Bonds Junk Bonds: bonds rated BB or below Treasury Bonds: Bonds issued by

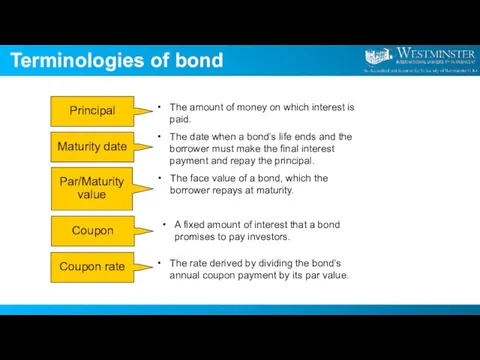

- 9. Terminologies of bond

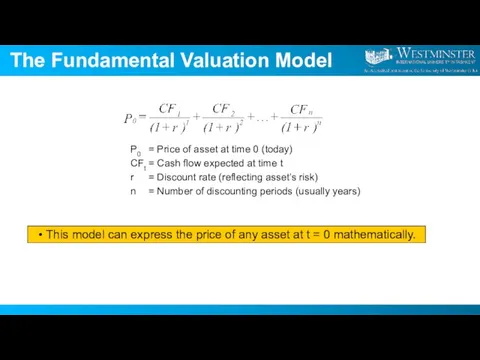

- 10. The Fundamental Valuation Model This model can express the price of any asset at t =

- 11. Valuing Coupon Bonds A non-zero coupon-paying bond is a coupon paying bond with a finite life.

- 12. Valuing Zero Coupon Bonds A zero coupon bond is a bond that pays no interest but

- 13. Valuing Perpetual Bonds A perpetual bond is a bond that never matures. It has an infinite

- 14. Non-annual Compounding Semiannually m=2 Quarterly m=4 Monthly m=12 Weekly m=52 Daily m=365

- 15. Semiannual Compounding A non-zero coupon bond adjusted for semiannual compounding. An example.... Value a T-Bond Par

- 16. Bond Premiums and Discounts What happens to bond values if the required return is not equal

- 17. Yield to Maturity (YTM)/Expected Rate of Return Also called Expected Rate of Return Estimate of return

- 18. Determining the YTM: Interpolation Julie Miller want to determine the YTM for an issue of outstanding

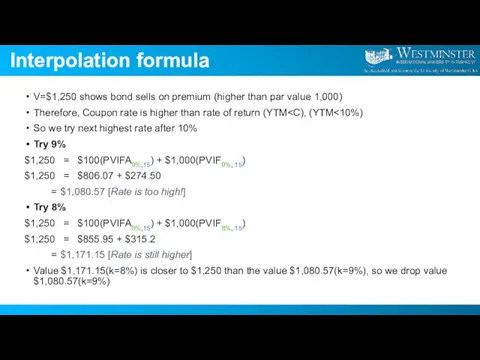

- 19. Interpolation formula V=$1,250 shows bond sells on premium (higher than par value 1,000) Therefore, Coupon rate

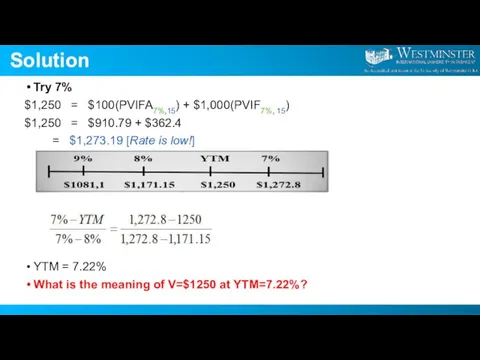

- 20. Solution Try 7% $1,250 = $100(PVIFA7%,15) + $1,000(PVIF7%, 15) $1,250 = $910.79 + $362.4 = $1,273.19

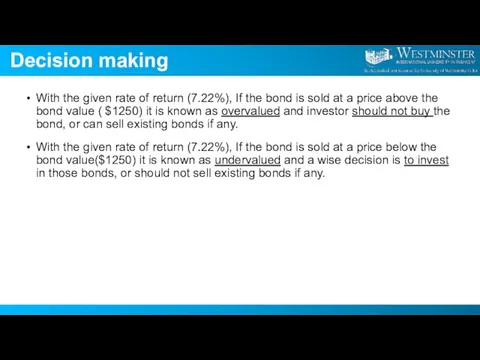

- 21. Decision making With the given rate of return (7.22%), If the bond is sold at a

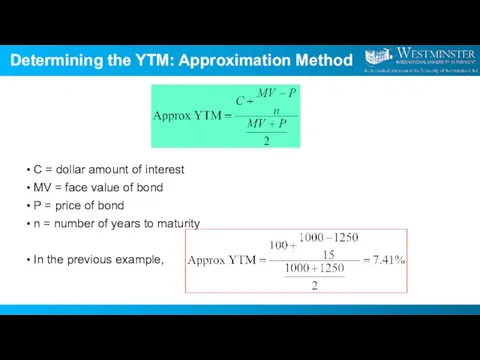

- 22. Determining the YTM: Approximation Method C = dollar amount of interest MV = face value of

- 23. FIRST RELATIONSHIP The value of the bond is inversely related to changes in the investor’s required

- 24. FIVE IMPORTANT RELATIONSHIPS SECOND RELATIONSHIP The market value (Po) will be less than the par value

- 25. FIVE IMPORTANT RELATIONSHIPS THIRD RELATIONSHIP As the maturity approaches, the market value of the bond approaches

- 26. Relationship between bond value & interest rate

- 27. FIVE IMPORTANT RELATIONSHIPS FIFTH RELATIONSHIP The sensitivity of a bond’s value to changing - depends on:

- 28. Exercise: YTM with semiannual coupon Suppose a bond with a 10% coupon rate and semiannual coupons,

- 29. Solution

- 31. Скачать презентацию

Слайд 3Definition of Bond

Terminology & Characteristics of Bonds

Bond Valuation

Premium Bonds vs Discount Bonds

Yield

Definition of Bond

Terminology & Characteristics of Bonds

Bond Valuation

Premium Bonds vs Discount Bonds

Yield

Слайд 4 A type of debt (long-term promissory note) issued by the borrower,

A type of debt (long-term promissory note) issued by the borrower,

Слайд 5Par value = $1,000

Coupon = 6.5% on par value per year,

or $65

Par value = $1,000

Coupon = 6.5% on par value per year,

or $65

Слайд 6Bonds

Bonds

Слайд 7Different Types of Bonds

Debentures: Unsecured long-term debt.

Subordinated debentures: Bonds that have a

Different Types of Bonds

Debentures: Unsecured long-term debt.

Subordinated debentures: Bonds that have a

Слайд 8Different Types of Bonds

Junk Bonds: bonds rated BB or below

Treasury Bonds: Bonds

Junk Bonds: bonds rated BB or below

Treasury Bonds: Bonds

Слайд 9Terminologies of bond

Слайд 10The Fundamental Valuation Model

This model can express the price of any asset

The Fundamental Valuation Model

This model can express the price of any asset

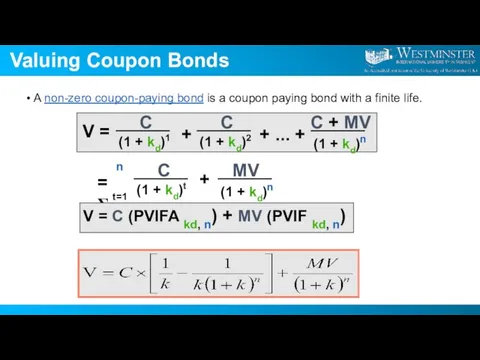

Слайд 11Valuing Coupon Bonds

A non-zero coupon-paying bond is a coupon paying bond with

Valuing Coupon Bonds

A non-zero coupon-paying bond is a coupon paying bond with

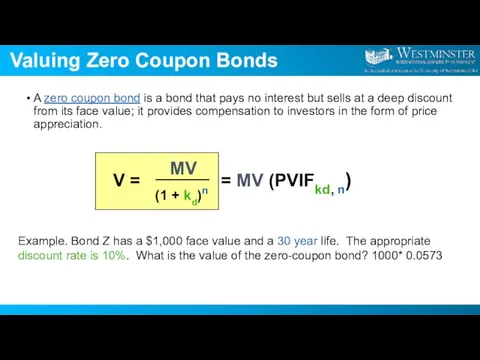

Слайд 12Valuing Zero Coupon Bonds

A zero coupon bond is a bond that pays

Valuing Zero Coupon Bonds

A zero coupon bond is a bond that pays

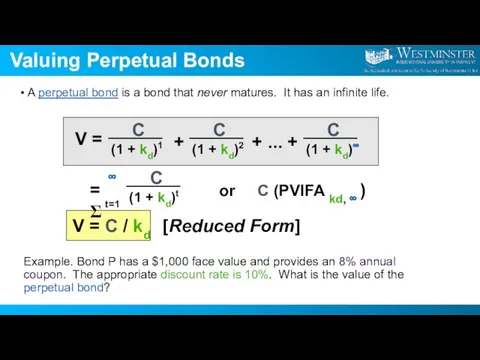

Слайд 13Valuing Perpetual Bonds

A perpetual bond is a bond that never matures. It

Valuing Perpetual Bonds

A perpetual bond is a bond that never matures. It

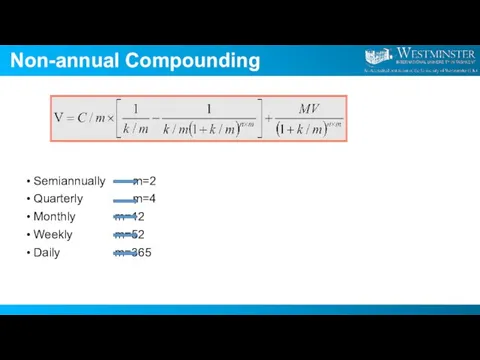

Слайд 14Non-annual Compounding

Semiannually m=2

Quarterly m=4

Monthly m=12

Weekly m=52

Daily m=365

Non-annual Compounding

Semiannually m=2

Quarterly m=4

Monthly m=12

Weekly m=52

Daily m=365

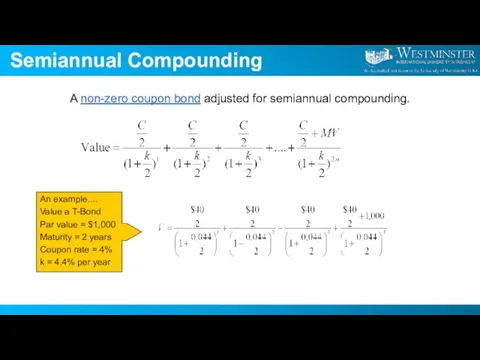

Слайд 15Semiannual Compounding

A non-zero coupon bond adjusted for semiannual compounding.

An example....

Value a T-Bond

Semiannual Compounding

A non-zero coupon bond adjusted for semiannual compounding.

An example....

Value a T-Bond

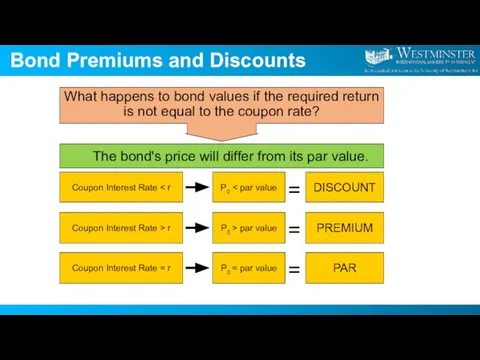

Слайд 16Bond Premiums and Discounts

What happens to bond values if the required return

Bond Premiums and Discounts

What happens to bond values if the required return

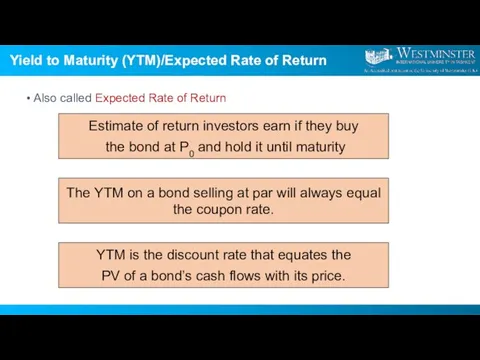

Слайд 17Yield to Maturity (YTM)/Expected Rate of Return

Also called Expected Rate of Return

Estimate

Yield to Maturity (YTM)/Expected Rate of Return

Also called Expected Rate of Return

Estimate

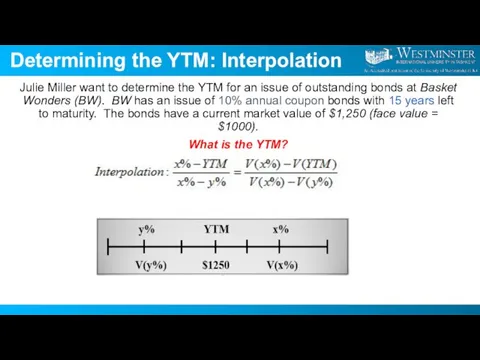

Слайд 18Determining the YTM: Interpolation

Julie Miller want to determine the YTM for an

Determining the YTM: Interpolation

Julie Miller want to determine the YTM for an

Слайд 19Interpolation formula

V=$1,250 shows bond sells on premium (higher than par value 1,000)

Therefore,

Interpolation formula

V=$1,250 shows bond sells on premium (higher than par value 1,000)

Therefore,

Слайд 20Solution

Try 7%

$1,250 = $100(PVIFA7%,15) + $1,000(PVIF7%, 15)

$1,250 = $910.79 + $362.4

=

Solution

Try 7%

$1,250 = $100(PVIFA7%,15) + $1,000(PVIF7%, 15)

$1,250 = $910.79 + $362.4

=

Слайд 21Decision making

With the given rate of return (7.22%), If the bond is

Decision making

With the given rate of return (7.22%), If the bond is

Слайд 22Determining the YTM: Approximation Method

C = dollar amount of interest

MV = face

Determining the YTM: Approximation Method

C = dollar amount of interest

MV = face

Слайд 23FIRST RELATIONSHIP

The value of the bond is inversely related to changes in

FIRST RELATIONSHIP

The value of the bond is inversely related to changes in

Слайд 24FIVE IMPORTANT RELATIONSHIPS

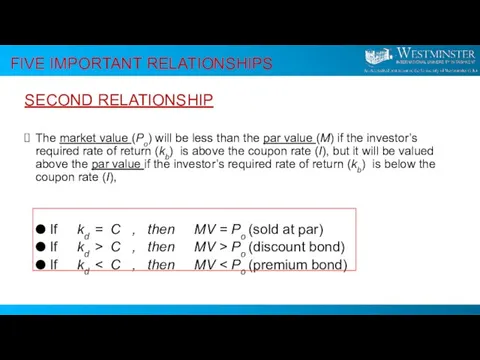

SECOND RELATIONSHIP

The market value (Po) will be less than the

FIVE IMPORTANT RELATIONSHIPS

SECOND RELATIONSHIP

The market value (Po) will be less than the

Слайд 25FIVE IMPORTANT RELATIONSHIPS

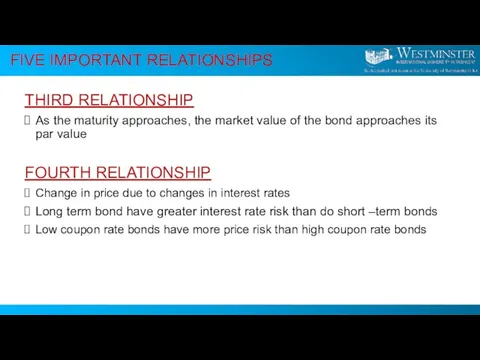

THIRD RELATIONSHIP

As the maturity approaches, the market value of the

FIVE IMPORTANT RELATIONSHIPS

THIRD RELATIONSHIP

As the maturity approaches, the market value of the

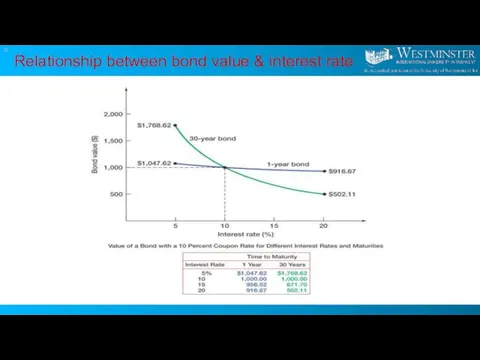

Слайд 26Relationship between bond value & interest rate

Relationship between bond value & interest rate

Слайд 27FIVE IMPORTANT RELATIONSHIPS

FIFTH RELATIONSHIP

The sensitivity of a bond’s value to changing -

FIVE IMPORTANT RELATIONSHIPS

FIFTH RELATIONSHIP

The sensitivity of a bond’s value to changing -

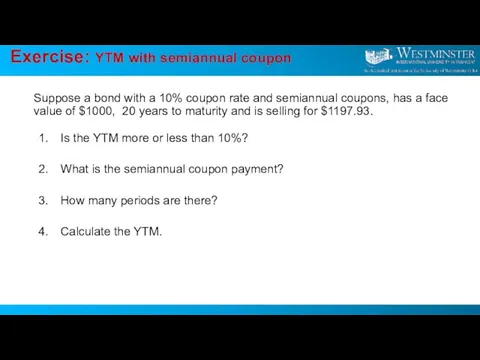

Слайд 28Exercise: YTM with semiannual coupon

Suppose a bond with a 10% coupon rate

Exercise: YTM with semiannual coupon

Suppose a bond with a 10% coupon rate

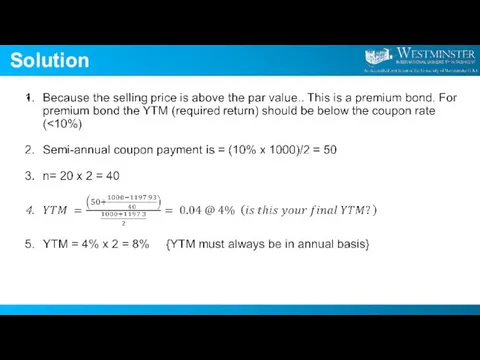

Слайд 29Solution

Solution

PowerPoint Show by Andrew

PowerPoint Show by Andrew Появление трамвая

Появление трамвая Скалярное произведение векторов 9 класс

Скалярное произведение векторов 9 класс Всегда великая Россия

Всегда великая Россия Фараон Тутанхамон (1334 – 1325 гг. до н.э.). Сокровища из его гробницы

Фараон Тутанхамон (1334 – 1325 гг. до н.э.). Сокровища из его гробницы Права человека. Международная защита прав человека в условиях военного времени

Права человека. Международная защита прав человека в условиях военного времени Группа компаний АТМ Альянс

Группа компаний АТМ Альянс Презентация на тему Молдавия

Презентация на тему Молдавия  Работа выполнена в рамках проекта: «Повышение квалификации различных категорий работников образования и формирование у них базов

Работа выполнена в рамках проекта: «Повышение квалификации различных категорий работников образования и формирование у них базов ФИНЛЯНДИЯ

ФИНЛЯНДИЯ Презентация на тему Зона степей (4 класс)

Презентация на тему Зона степей (4 класс) Хаос – высшая степень порядка

Хаос – высшая степень порядка Организационная психология Проблемы мотивации в организации

Организационная психология Проблемы мотивации в организации Единственный магистральный оператор, предоставляющий услуги дальней связи на всей территории России Оператор операторов, обеспе

Единственный магистральный оператор, предоставляющий услуги дальней связи на всей территории России Оператор операторов, обеспе Оружие кировской области

Оружие кировской области Развитие учения об отдельных видах следов. Тема №4

Развитие учения об отдельных видах следов. Тема №4 Издержки и результаты хозяйственной деятельности, ее экономическая эффективность

Издержки и результаты хозяйственной деятельности, ее экономическая эффективность  Проблема и позиция автора

Проблема и позиция автора Формула качественного контента: как быть востребованным везде? Наталья Прачук seven-keys.com.ua

Формула качественного контента: как быть востребованным везде? Наталья Прачук seven-keys.com.ua Кижский погост

Кижский погост British and Russian food and drinks

British and Russian food and drinks Стиль шинуазри в живописи

Стиль шинуазри в живописи Специальное предложение для работников ООО Велфарм и их близких родственников*

Специальное предложение для работников ООО Велфарм и их близких родственников* Мировые финансовые рынки

Мировые финансовые рынки Противоглистные средства

Противоглистные средства 2.2. Целью деятельности Центра является развитие активной жизненной позиции, стимулирование процессов личностного саморазвития де

2.2. Целью деятельности Центра является развитие активной жизненной позиции, стимулирование процессов личностного саморазвития де Степи Кубани

Степи Кубани Матренин двор

Матренин двор