- Capital badgeting

Содержание

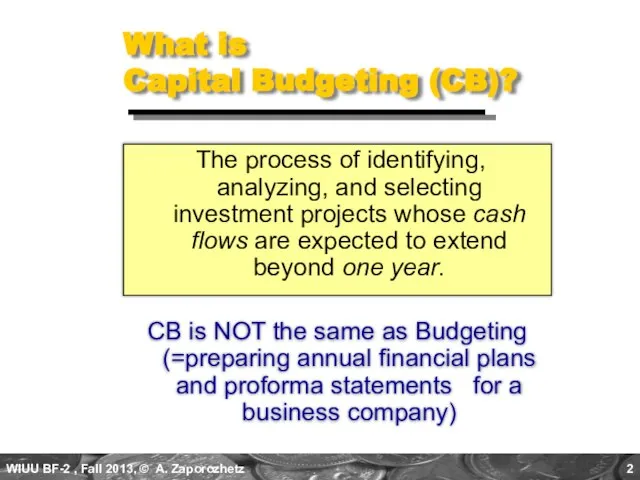

- 2. What is Capital Budgeting (CB)? The process of identifying, analyzing, and selecting investment projects whose cash

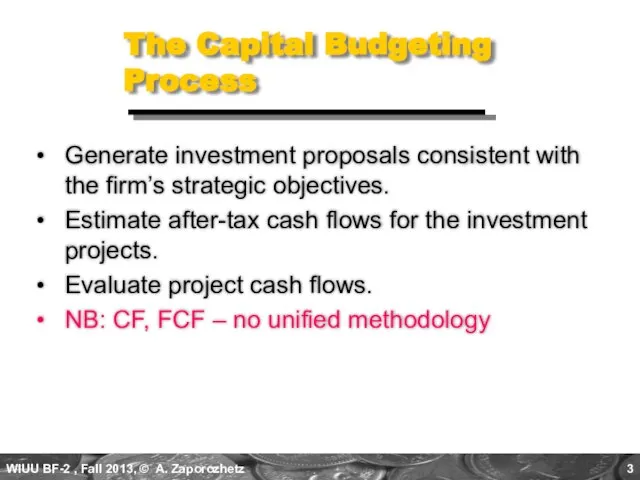

- 3. The Capital Budgeting Process Generate investment proposals consistent with the firm’s strategic objectives. Estimate after-tax cash

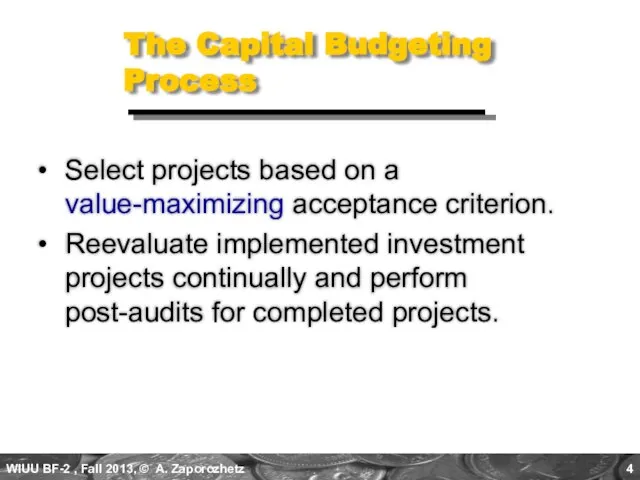

- 4. The Capital Budgeting Process Select projects based on a value-maximizing acceptance criterion. Reevaluate implemented investment projects

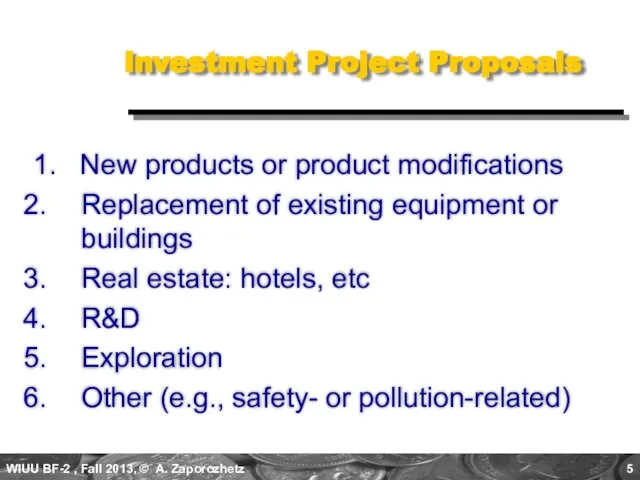

- 5. Investment Project Proposals 1. New products or product modifications Replacement of existing equipment or buildings Real

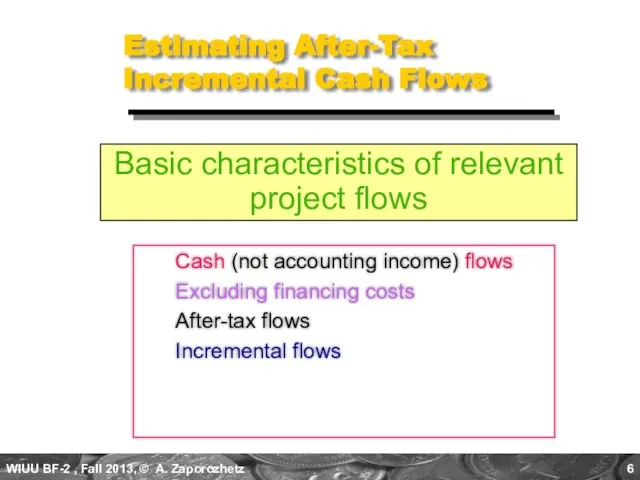

- 6. Estimating After-Tax Incremental Cash Flows Cash (not accounting income) flows Excluding financing costs After-tax flows Incremental

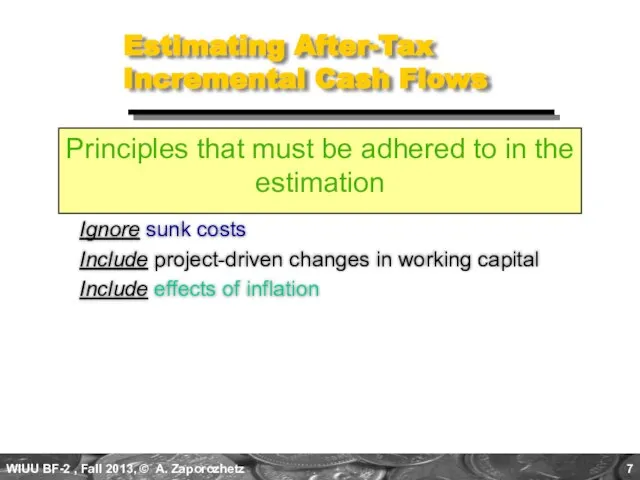

- 7. Estimating After-Tax Incremental Cash Flows Ignore sunk costs Include project-driven changes in working capital Include effects

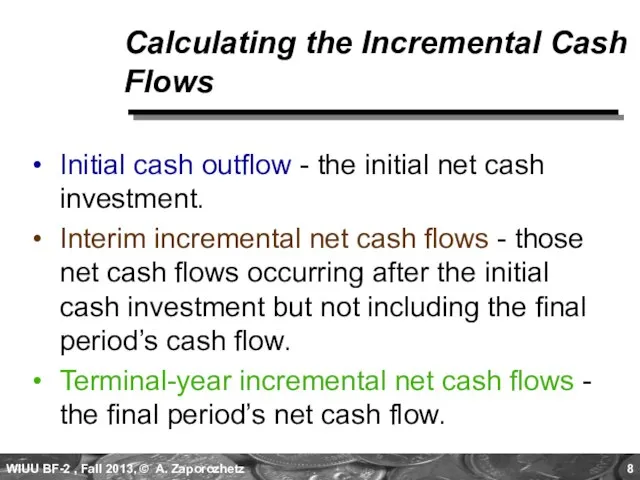

- 8. Calculating the Incremental Cash Flows Initial cash outflow - the initial net cash investment. Interim incremental

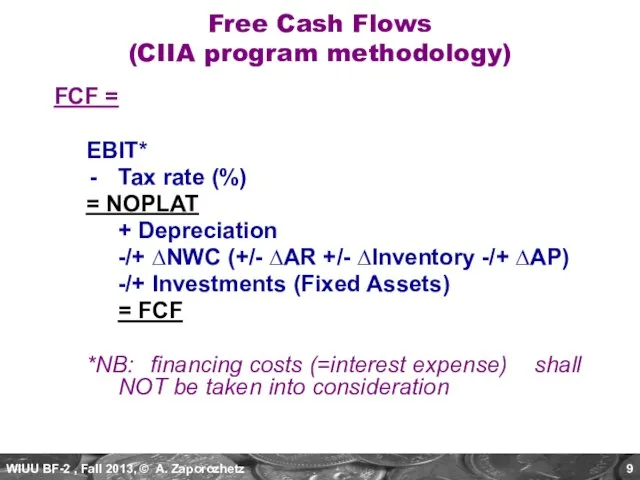

- 9. FCF = EBIT* Tax rate (%) = NOPLAT + Depreciation -/+ ∆NWC (+/- ∆AR +/- ∆Inventory

- 10. Initial Cash Outflow, ICO a) Cost of “new” assets b) + Capitalized expenditures c) + (-)

- 11. Terminal-Year Incremental Cash Flows a) Calculate the incremental net cash flow for the terminal period b)

- 12. Project Evaluation: Alternative Methods Payback Period (PBP) Discounted PBP (DPBP) Internal Rate of Return (IRR) Net

- 13. Proposed Project Data Julie is evaluating a new project for her firm, Basket Wonders (BW). She

- 14. Payback Period (PBP) PBP is the period of time required for the cumulative expected cash flows

- 15. (c) 10 K 22 K 37 K 47 K 54 K Payback Solution (#1) PBP =

- 16. Payback Solution (#2) PBP = 3 + ( 3K ) / 10K = 3.30 Years Note:

- 17. PBP Acceptance Criterion Yes! The firm will receive back the initial cash outlay in less than

- 18. The PBP Method Strengths and Weaknesses Strengths: Easy to use and understand Can be used as

- 19. Internal Rate of Return (IRR) IRR is the discount rate that equates the PV of the

- 20. $15,000 $10,000 $7,000 IRR Solution $10,000 $12,000 (1+IRR)1 (1+IRR)2 Need to find the interest rate (=IRR)

- 21. IRR Solution (Try 10%) $40,000 = $10,000(PVIF10%,1) + $12,000(PVIF10%,2) + $15,000(PVIF10%,3) + $10,000(PVIF10%,4) + $ 7,000(PVIF10%,5)

- 22. IRR Solution (Try 15%) $40,000 = $10,000(PVIF15%,1) + $12,000(PVIF15%,2) + $15,000(PVIF15%,3) + $10,000(PVIF15%,4) + $ 7,000(PVIF15%,5)

- 23. 0.10 $41,444 0.05 IRR $40,000 $4,603 0.15 $36,841 X $1,444 0.05 $4,603 IRR Solution (Interpolate) $1,444

- 24. .10 $41,444 .05 IRR $40,000 $4,603 .15 $36,841 X $1,444 .05 $4,603 IRR Solution (Interpolate) $1,444

- 25. 0.10 $41,444 0.05 IRR $40,000 $4,603 0.15 $36,841 ($1,444)(0.05) $4,603 IRR Solution (Interpolate) $1,444 X X

- 26. IRR Acceptance Criterion No! The firm will “receive” 11.57% for each dollar “required” for this project

- 27. IRR Strengths and Weaknesses Strengths: Accounts for TVM Considers all the cash flows Less subjectivity Weaknesses:

- 28. Net Present Value (NPV) NPV is the present value of an investment project’s net DCFs minus

- 29. Basket Wonders has determined that the appropriate discount rate (k) for this project is 13%. $10,000

- 30. NPV Solution NPV = $10,000(PVIF13%,1) + $12,000(PVIF13%,2) + $15,000(PVIF13%,3) + $10,000(PVIF13%,4) + $ 7,000(PVIF13%,5) - $40,000

- 31. NPV Acceptance Criterion No! The NPV is negative. This means that the project is reducing shareholder

- 32. NPV Strengths and Weaknesses Strengths: (Cash flows assumed to be reinvested at the hurdle rate.) Accounts

- 33. Net Present Value Profile Discount Rate (%) 0 3 6 9 12 15 IRR NPV@13% Sum

- 34. Profitability Index (PI) PI is the ratio of the present value of a project’s future net

- 35. PI Acceptance Criterion No! The PI is less than 1.00. This means that the project is

- 36. PI Strengths and Weaknesses Strengths: Same as NPV Allows for comparison of different scale and lifetime

- 37. Evaluation Summary Basket Wonders Independent Project

- 38. Other Project Relationships Mutually Exclusive - A project whose acceptance precludes the acceptance of one or

- 39. Potential Problems Under Mutual Exclusivity A. Scale of Investment B. Cash-flow Pattern C. Project Life Ranking

- 40. A. Scale Differences Compare a small (S) and a large (L) project. NET CASH FLOWS Project

- 41. A. Scale Differences Calculate the PBP, IRR, NPV@10%, and PI@10%. Which project is preferred? Why? Project

- 42. B. Cash Flow Pattern Let us compare a decreasing cash-flow (D) project and an increasing cash-flow

- 43. D 23% $197 1.16 I 17% $198 1.17 Cash Flow Pattern Calculate the IRR, NPV@10%, and

- 44. Examine NPV Profiles Discount Rate (%) 0 5 10 15 20 25 -200 0 200 400

- 45. Fisher’s Rate of Intersection Discount Rate ($) 0 5 10 15 20 25 -200 0 200

- 46. C. Project Life Differences Let us compare a long life (X) project and a short life

- 47. X 50% $1,536 2.54 Y 100% $ 818 1.82 Project Life Differences Calculate the PBP, IRR,

- 48. Another Way to Look at Things 1. Adjust cash flows to a common terminal year if

- 49. Replacing Projects with Identical Projects 2. Use Replacement Chain Approach (Appendix B) when project “Y” will

- 50. Capital Rationing Capital Rationing occurs when a constraint (or budget ceiling) is placed on the total

- 51. Available Projects for BW Project ICO,$ IRR,% NPV,$ PI A $ 500 18 50 1.10 B

- 52. Choosing by IRRs for BW Project ICO IRR NPV PI C $5,000 37% $5,500 2.10 F

- 53. Choosing by NPVs for BW Project ICO IRR NPV PI F $15,000 28% $21,000 2.40 G

- 54. Choosing by PIs for BW Project ICO IRR NPV PI F $15,000 28% $21,000 2.40 B

- 55. Summary of Comparison Method Projects Accepted Value Added PI F, B, C, and D $38,000 NPV

- 56. Post-Completion Audit: Usus Magister Est Optimus Post-completion Audit A formal comparison of the actual costs and

- 57. Multiple IRR Problem Two!! There are as many potential IRRs as there are sign changes. Let

- 58. NPV Profile -- Multiple IRRs Discount Rate (%) 0 40 80 120 160 200 Net Present

- 60. Скачать презентацию

Слайд 3The Capital Budgeting Process

Generate investment proposals consistent with the firm’s strategic objectives.

Estimate

The Capital Budgeting Process

Generate investment proposals consistent with the firm’s strategic objectives.

Estimate

Слайд 4The Capital Budgeting Process

Select projects based on a value-maximizing acceptance criterion.

Reevaluate implemented

The Capital Budgeting Process

Select projects based on a value-maximizing acceptance criterion.

Reevaluate implemented

Слайд 5Investment Project Proposals

1. New products or product modifications

Replacement of existing equipment or

Investment Project Proposals

1. New products or product modifications

Replacement of existing equipment or

Слайд 6Estimating After-Tax Incremental Cash Flows

Cash (not accounting income) flows

Excluding financing costs

After-tax flows

Incremental

Estimating After-Tax Incremental Cash Flows

Cash (not accounting income) flows

Excluding financing costs

After-tax flows

Incremental

Слайд 7Estimating After-Tax Incremental Cash Flows

Ignore sunk costs

Include project-driven changes in working capital

Estimating After-Tax Incremental Cash Flows

Ignore sunk costs

Include project-driven changes in working capital

Слайд 8Calculating the Incremental Cash Flows

Initial cash outflow - the initial net cash

Calculating the Incremental Cash Flows

Initial cash outflow - the initial net cash

Слайд 9FCF =

EBIT*

Tax rate (%)

= NOPLAT

+ Depreciation

-/+ ∆NWC (+/- ∆AR +/-

FCF =

EBIT*

Tax rate (%)

= NOPLAT

+ Depreciation

-/+ ∆NWC (+/- ∆AR +/-

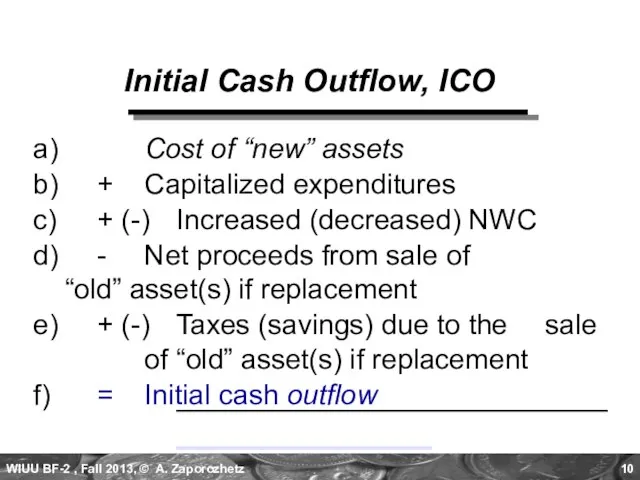

Слайд 10Initial Cash Outflow, ICO

a) Cost of “new” assets

b) + Capitalized expenditures

c) + (-) Increased

Initial Cash Outflow, ICO

a) Cost of “new” assets

b) + Capitalized expenditures

c) + (-) Increased

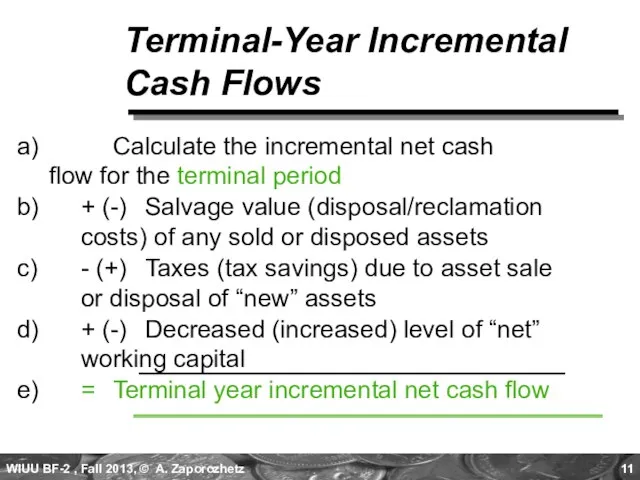

Слайд 11Terminal-Year Incremental Cash Flows

a) Calculate the incremental net cash flow for the

Terminal-Year Incremental Cash Flows

a) Calculate the incremental net cash flow for the

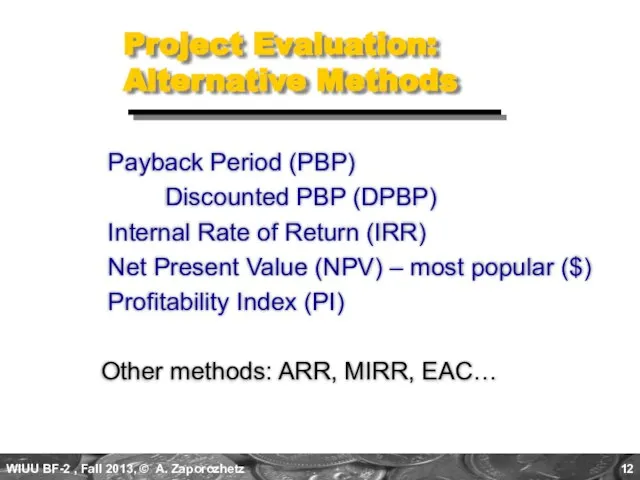

Слайд 12Project Evaluation: Alternative Methods

Payback Period (PBP)

Discounted PBP (DPBP)

Internal Rate

Project Evaluation: Alternative Methods

Payback Period (PBP)

Discounted PBP (DPBP)

Internal Rate

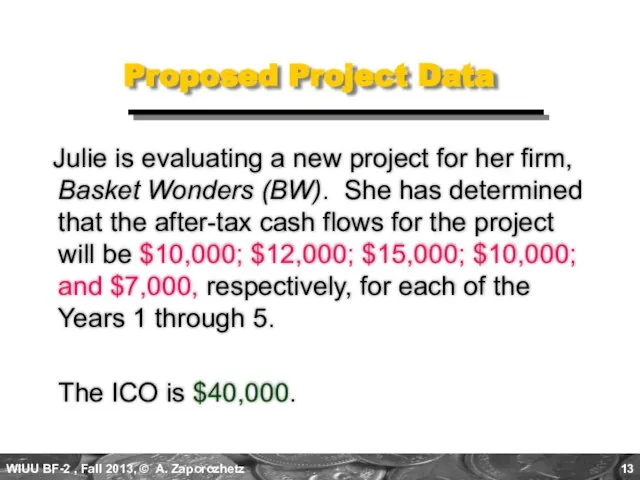

Слайд 13Proposed Project Data

Julie is evaluating a new project for her firm,

Proposed Project Data

Julie is evaluating a new project for her firm,

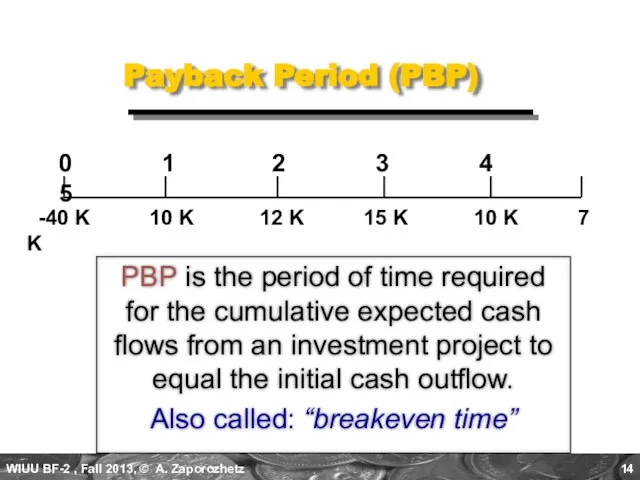

Слайд 14Payback Period (PBP)

PBP is the period of time required for the cumulative

Payback Period (PBP)

PBP is the period of time required for the cumulative

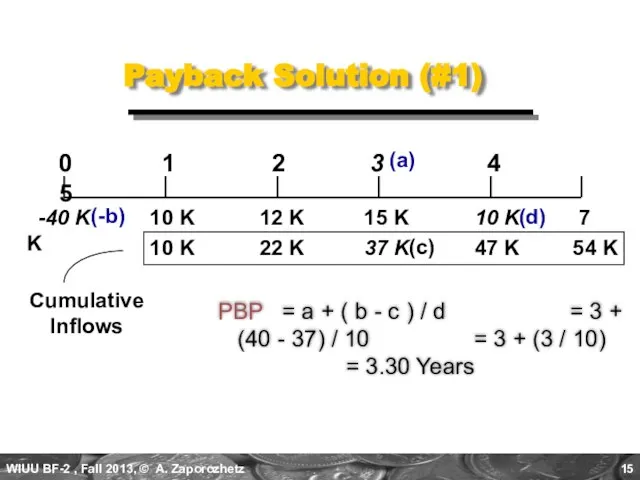

Слайд 15(c)

10 K 22 K 37 K 47 K 54 K

Payback Solution (#1)

PBP

(c)

10 K 22 K 37 K 47 K 54 K

Payback Solution (#1)

PBP

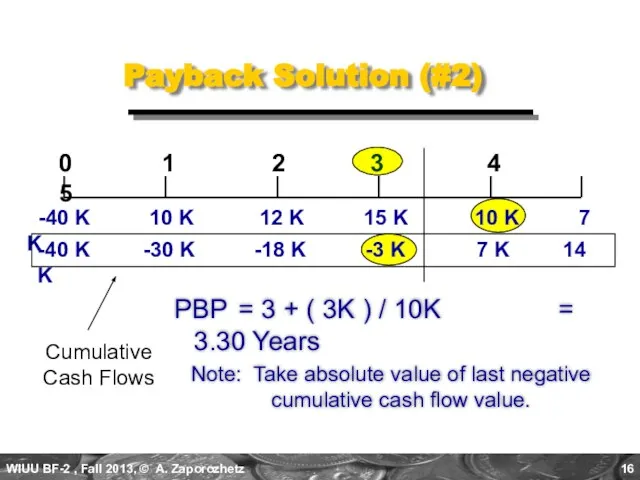

Слайд 16Payback Solution (#2)

PBP = 3 + ( 3K ) / 10K = 3.30

Payback Solution (#2)

PBP = 3 + ( 3K ) / 10K = 3.30

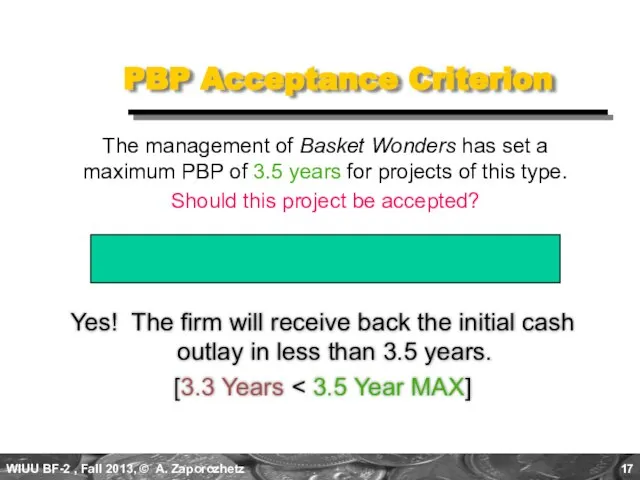

Слайд 17PBP Acceptance Criterion

Yes! The firm will receive back the initial cash outlay

PBP Acceptance Criterion

Yes! The firm will receive back the initial cash outlay

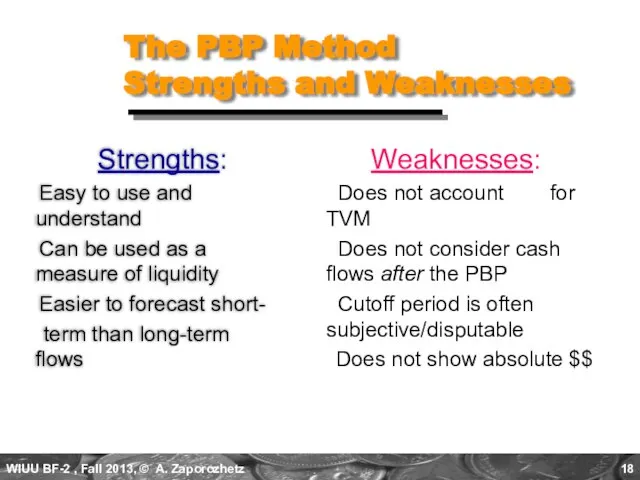

Слайд 18The PBP Method

Strengths and Weaknesses

Strengths:

Easy to use and understand

Can

The PBP Method

Strengths and Weaknesses

Strengths:

Easy to use and understand

Can

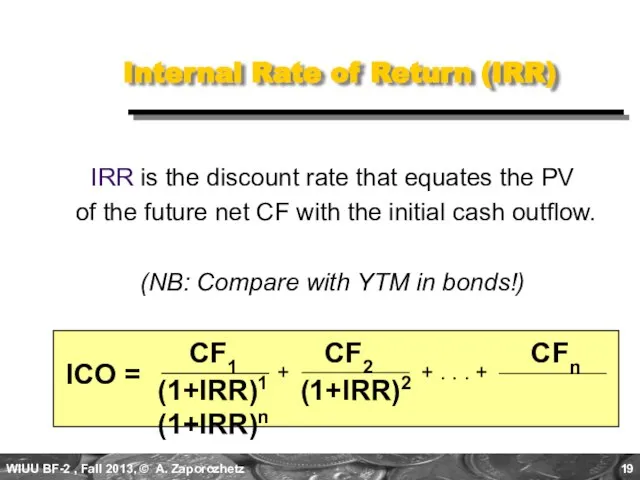

Слайд 19Internal Rate of Return (IRR)

IRR is the discount rate that equates the

Internal Rate of Return (IRR)

IRR is the discount rate that equates the

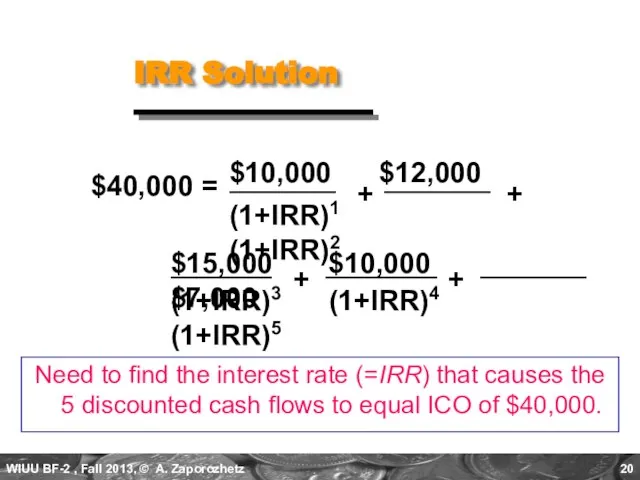

Слайд 20$15,000 $10,000 $7,000

IRR Solution

$10,000 $12,000

(1+IRR)1 (1+IRR)2

Need to find the interest rate

$15,000 $10,000 $7,000

IRR Solution

$10,000 $12,000

(1+IRR)1 (1+IRR)2

Need to find the interest rate

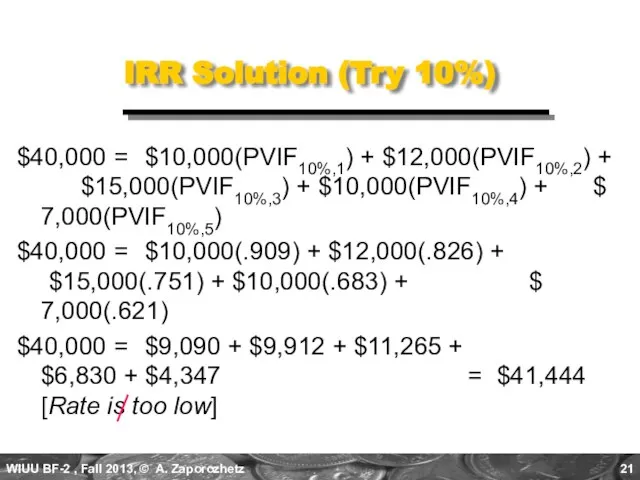

Слайд 21IRR Solution (Try 10%)

$40,000 = $10,000(PVIF10%,1) + $12,000(PVIF10%,2) + $15,000(PVIF10%,3) + $10,000(PVIF10%,4) +

IRR Solution (Try 10%)

$40,000 = $10,000(PVIF10%,1) + $12,000(PVIF10%,2) + $15,000(PVIF10%,3) + $10,000(PVIF10%,4) +

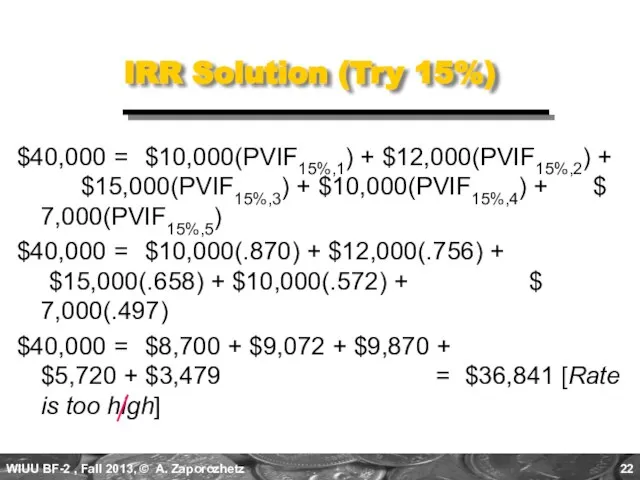

Слайд 22IRR Solution (Try 15%)

$40,000 = $10,000(PVIF15%,1) + $12,000(PVIF15%,2) + $15,000(PVIF15%,3) + $10,000(PVIF15%,4)

IRR Solution (Try 15%)

$40,000 = $10,000(PVIF15%,1) + $12,000(PVIF15%,2) + $15,000(PVIF15%,3) + $10,000(PVIF15%,4)

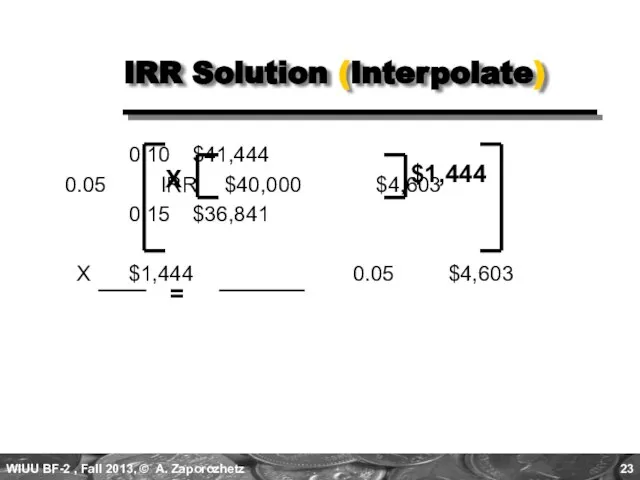

Слайд 23 0.10 $41,444

0.05 IRR $40,000 $4,603

0.15 $36,841

X $1,444 0.05 $4,603

IRR Solution (Interpolate)

$1,444

X

=

0.10 $41,444

0.05 IRR $40,000 $4,603

0.15 $36,841

X $1,444 0.05 $4,603

IRR Solution (Interpolate)

$1,444

X

=

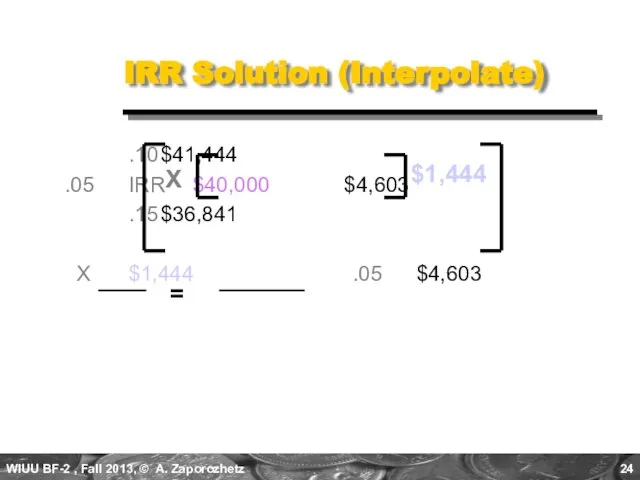

Слайд 24 .10 $41,444

.05 IRR $40,000 $4,603

.15 $36,841

X $1,444 .05 $4,603

IRR Solution (Interpolate)

$1,444

X

=

.10 $41,444

.05 IRR $40,000 $4,603

.15 $36,841

X $1,444 .05 $4,603

IRR Solution (Interpolate)

$1,444

X

=

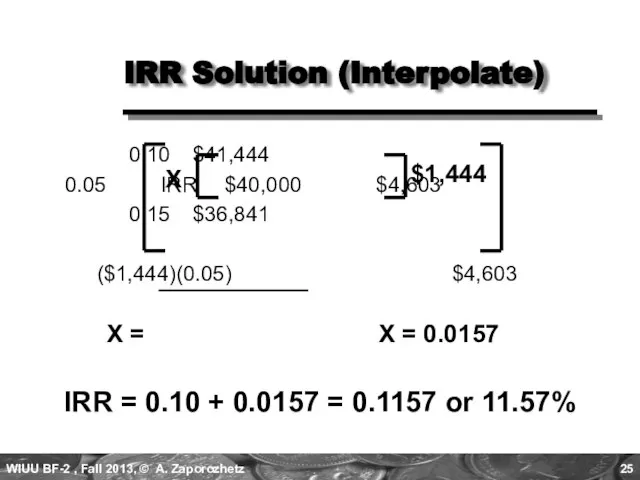

Слайд 25 0.10 $41,444

0.05 IRR $40,000 $4,603

0.15 $36,841

($1,444)(0.05) $4,603

IRR Solution (Interpolate)

$1,444

X

X =

X = 0.0157

IRR = 0.10 + 0.0157

0.10 $41,444

0.05 IRR $40,000 $4,603

0.15 $36,841

($1,444)(0.05) $4,603

IRR Solution (Interpolate)

$1,444

X

X =

X = 0.0157

IRR = 0.10 + 0.0157

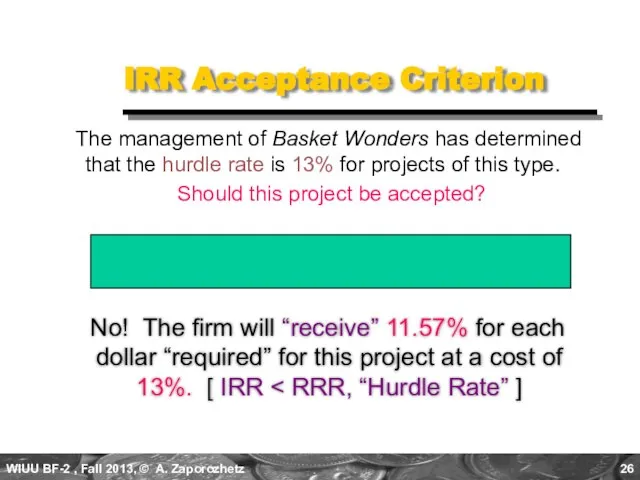

Слайд 26IRR Acceptance Criterion

No! The firm will “receive” 11.57% for each dollar

IRR Acceptance Criterion

No! The firm will “receive” 11.57% for each dollar

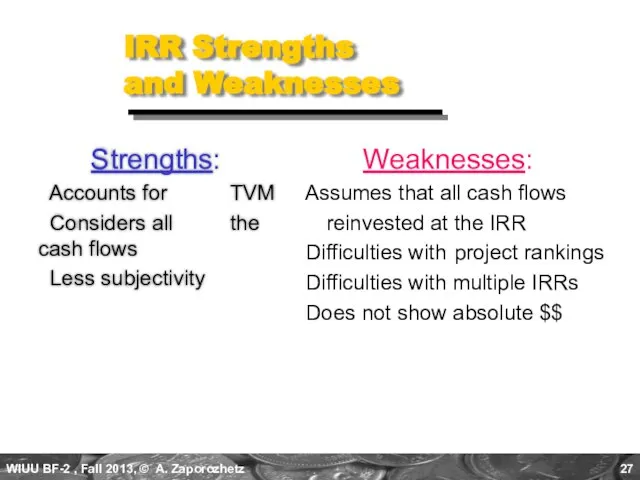

Слайд 27IRR Strengths

and Weaknesses

Strengths:

Accounts for TVM

Considers all the

IRR Strengths

and Weaknesses

Strengths:

Accounts for TVM

Considers all the

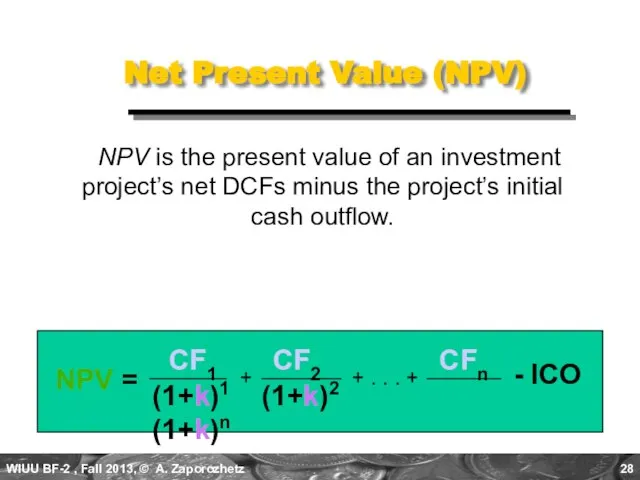

Слайд 28Net Present Value (NPV)

NPV is the present value of an investment

Net Present Value (NPV)

NPV is the present value of an investment

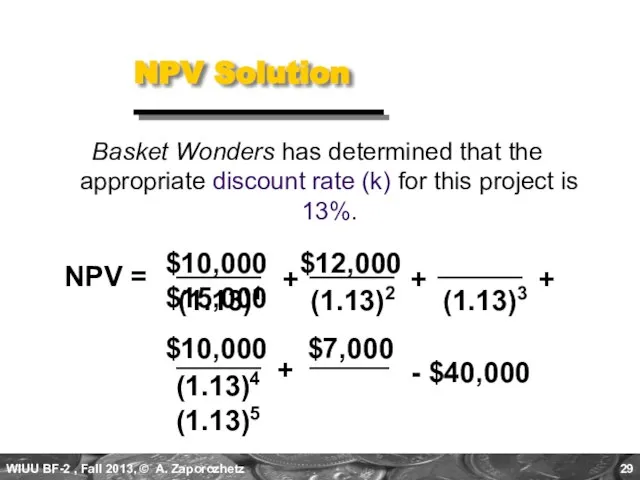

Слайд 29Basket Wonders has determined that the appropriate discount rate (k) for this

Basket Wonders has determined that the appropriate discount rate (k) for this

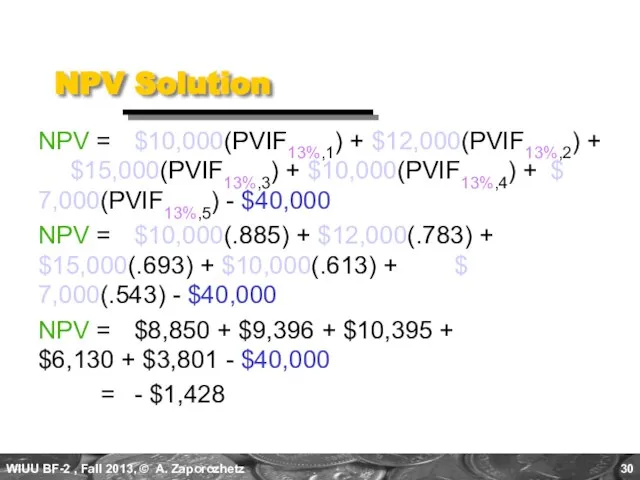

Слайд 30NPV Solution

NPV = $10,000(PVIF13%,1) + $12,000(PVIF13%,2) + $15,000(PVIF13%,3) + $10,000(PVIF13%,4) + $

NPV Solution

NPV = $10,000(PVIF13%,1) + $12,000(PVIF13%,2) + $15,000(PVIF13%,3) + $10,000(PVIF13%,4) + $

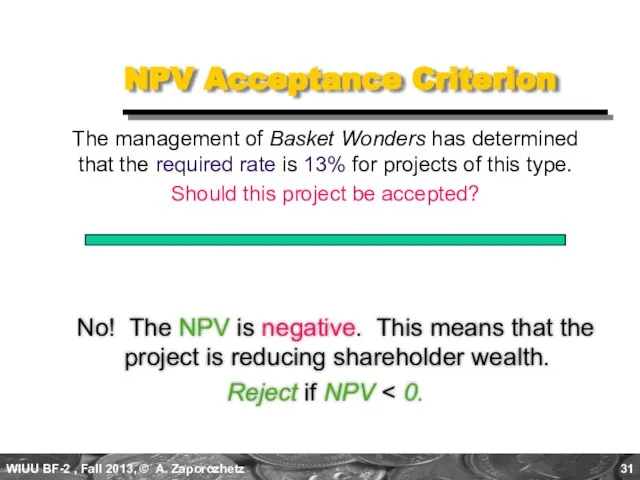

Слайд 31NPV Acceptance Criterion

No! The NPV is negative. This means that the

NPV Acceptance Criterion

No! The NPV is negative. This means that the

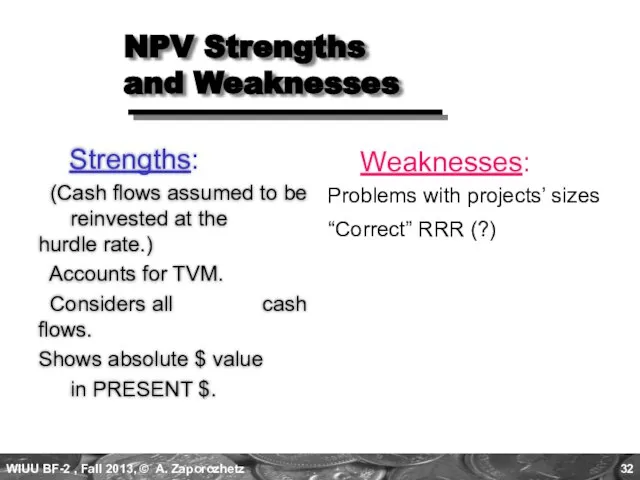

Слайд 32NPV Strengths

and Weaknesses

Strengths:

(Cash flows assumed to be reinvested at

NPV Strengths

and Weaknesses

Strengths:

(Cash flows assumed to be reinvested at

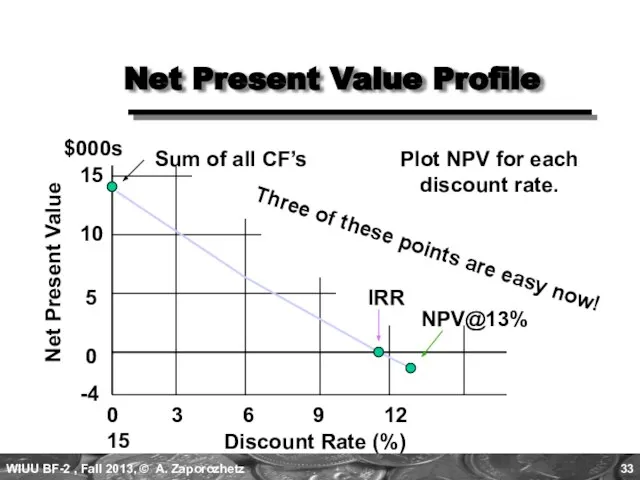

Слайд 33Net Present Value Profile

Discount Rate (%)

0 3 6 9 12 15

IRR

NPV@13%

Sum of

Net Present Value Profile

Discount Rate (%)

0 3 6 9 12 15

IRR

NPV@13%

Sum of

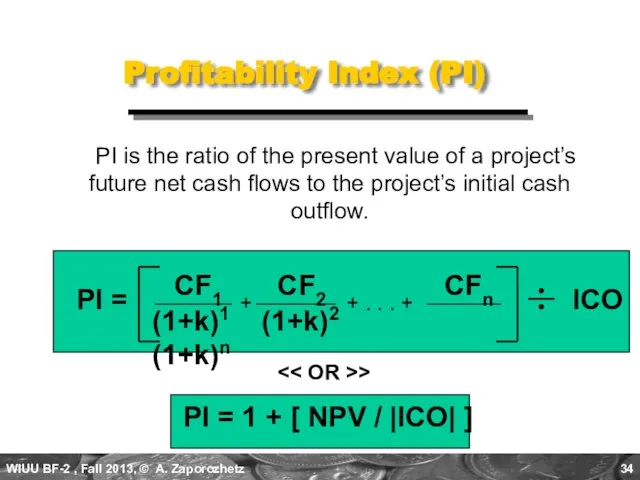

Слайд 34Profitability Index (PI)

PI is the ratio of the present value of

Profitability Index (PI)

PI is the ratio of the present value of

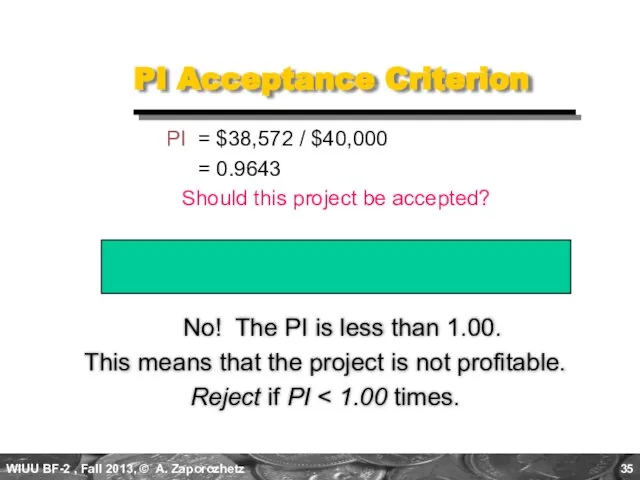

Слайд 35 PI Acceptance Criterion

No! The PI is less than 1.00.

This

PI Acceptance Criterion

No! The PI is less than 1.00.

This

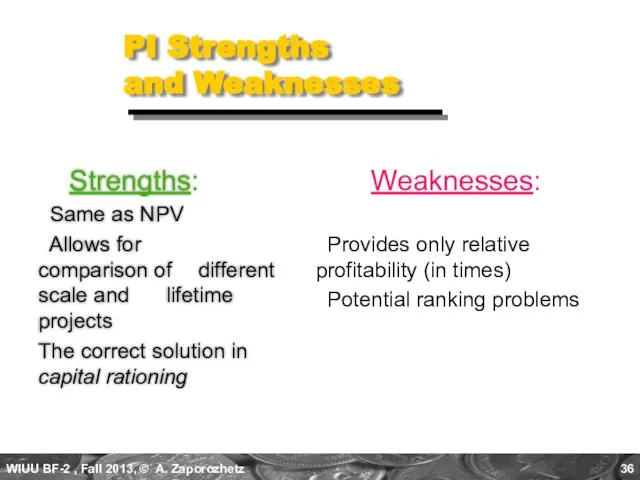

Слайд 36PI Strengths

and Weaknesses

Strengths:

Same as NPV

Allows for comparison of

PI Strengths

and Weaknesses

Strengths:

Same as NPV

Allows for comparison of

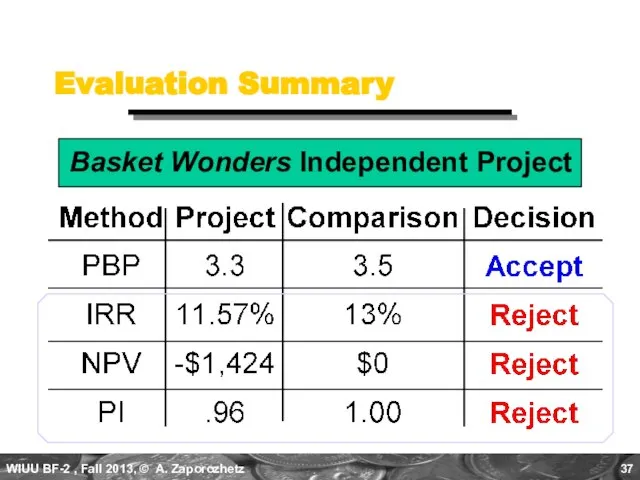

Слайд 37Evaluation Summary

Basket Wonders Independent Project

Evaluation Summary

Basket Wonders Independent Project

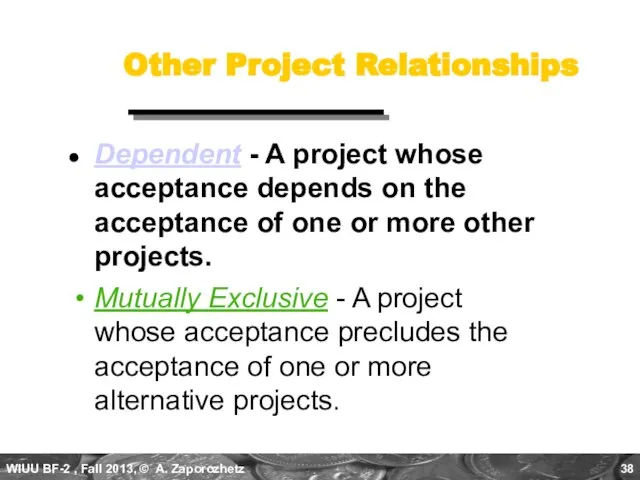

Слайд 38Other Project Relationships

Mutually Exclusive - A project whose acceptance precludes the acceptance

Other Project Relationships

Mutually Exclusive - A project whose acceptance precludes the acceptance

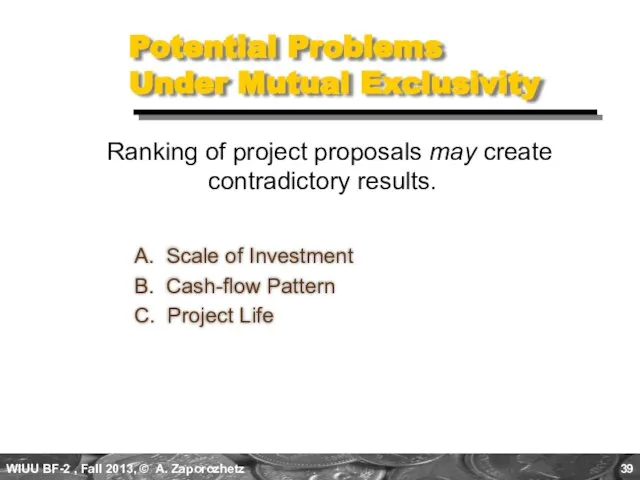

Слайд 39Potential Problems

Under Mutual Exclusivity

A. Scale of Investment

B. Cash-flow Pattern

C. Project Life

Potential Problems

Under Mutual Exclusivity

A. Scale of Investment

B. Cash-flow Pattern

C. Project Life

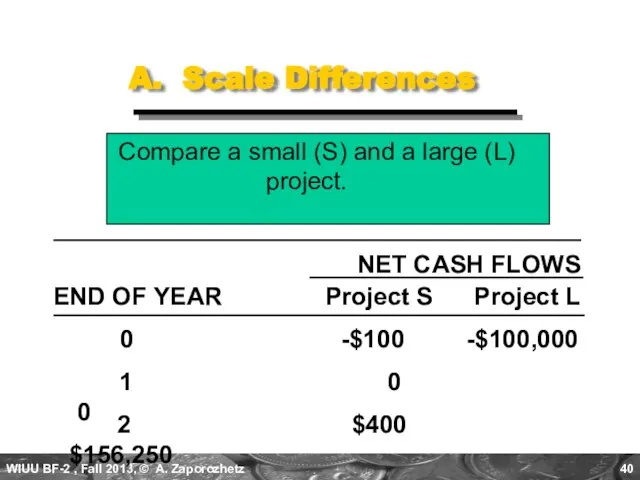

Слайд 40A. Scale Differences

Compare a small (S) and a large (L) project.

NET

A. Scale Differences

Compare a small (S) and a large (L) project.

NET

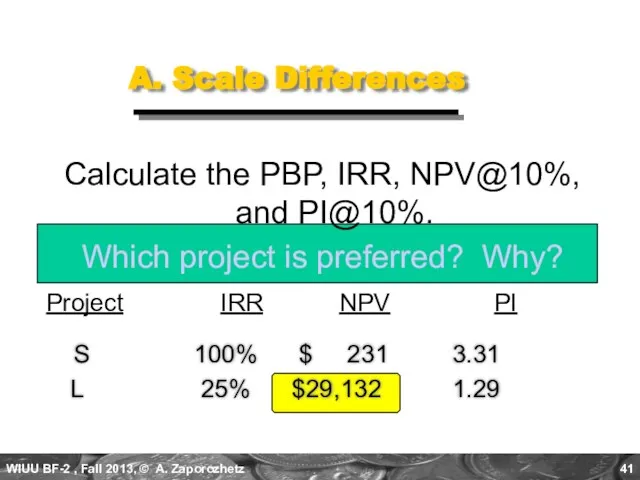

Слайд 41A. Scale Differences

Calculate the PBP, IRR, NPV@10%, and PI@10%.

Which project is preferred?

A. Scale Differences

Calculate the PBP, IRR, NPV@10%, and PI@10%.

Which project is preferred?

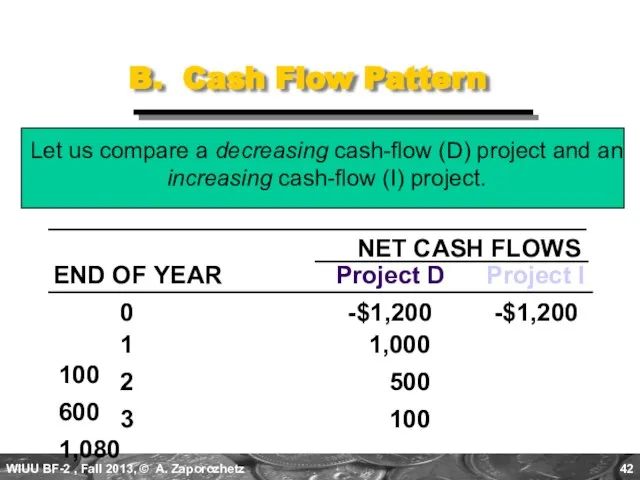

Слайд 42B. Cash Flow Pattern

Let us compare a decreasing cash-flow (D) project and

B. Cash Flow Pattern

Let us compare a decreasing cash-flow (D) project and

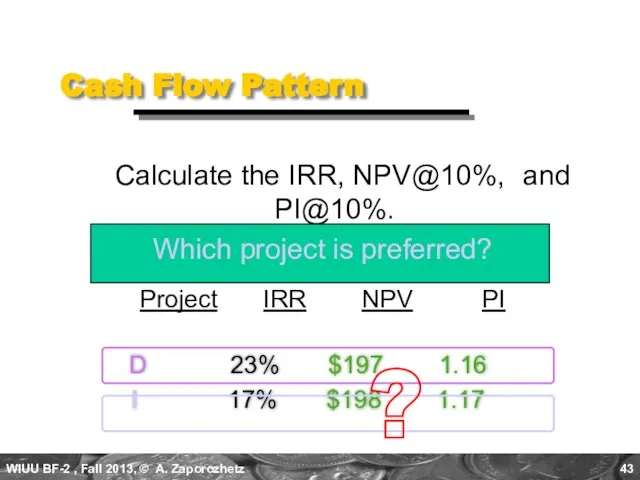

Слайд 43 D 23% $197 1.16

I 17% $198 1.17

Cash Flow Pattern

Calculate

D 23% $197 1.16

I 17% $198 1.17

Cash Flow Pattern

Calculate

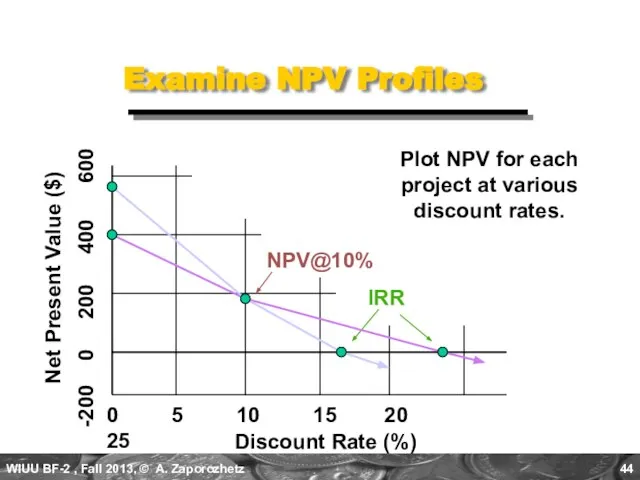

Слайд 44Examine NPV Profiles

Discount Rate (%)

0 5 10 15 20 25

-200 0 200

Examine NPV Profiles

Discount Rate (%)

0 5 10 15 20 25

-200 0 200

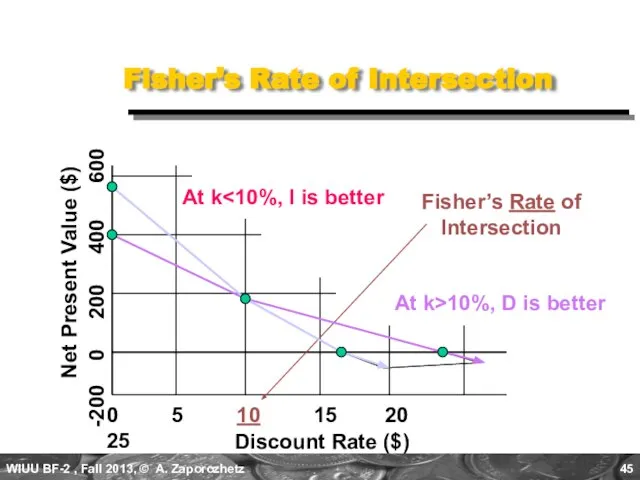

Слайд 45Fisher’s Rate of Intersection

Discount Rate ($)

0 5 10 15 20 25

-200 0

Fisher’s Rate of Intersection

Discount Rate ($)

0 5 10 15 20 25

-200 0

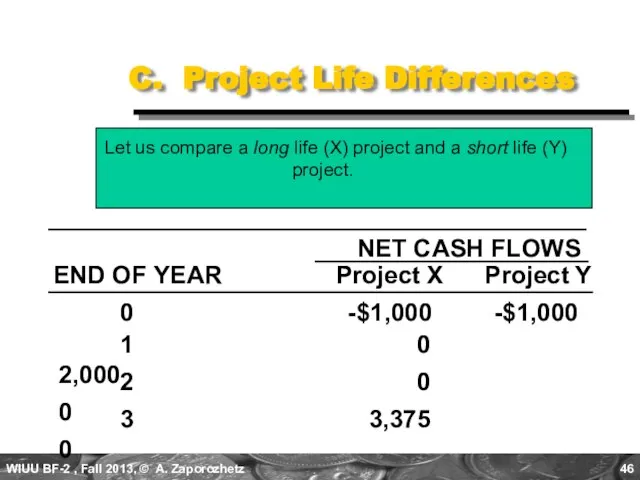

Слайд 46C. Project Life Differences

Let us compare a long life (X) project

C. Project Life Differences

Let us compare a long life (X) project

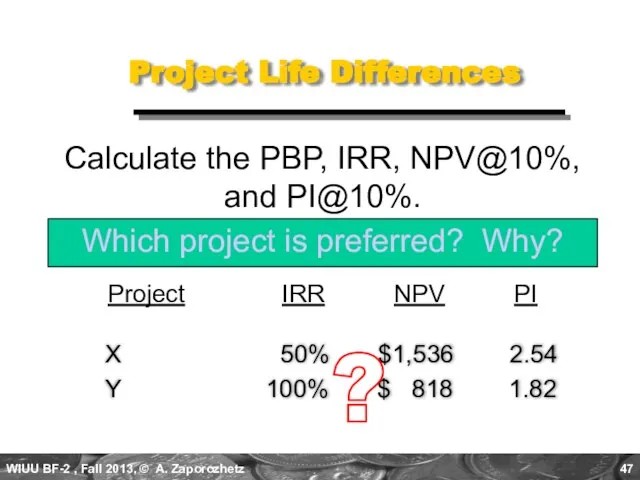

Слайд 47 X 50% $1,536 2.54

Y 100% $ 818 1.82

Project Life Differences

Calculate

X 50% $1,536 2.54

Y 100% $ 818 1.82

Project Life Differences

Calculate

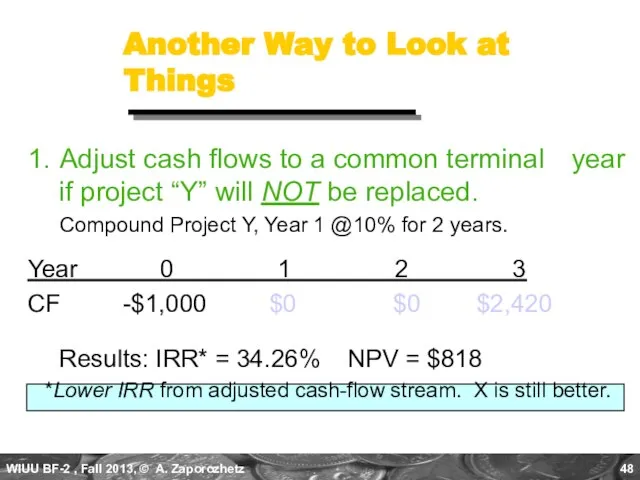

Слайд 48Another Way to Look at Things

1. Adjust cash flows to a common terminal

Another Way to Look at Things

1. Adjust cash flows to a common terminal

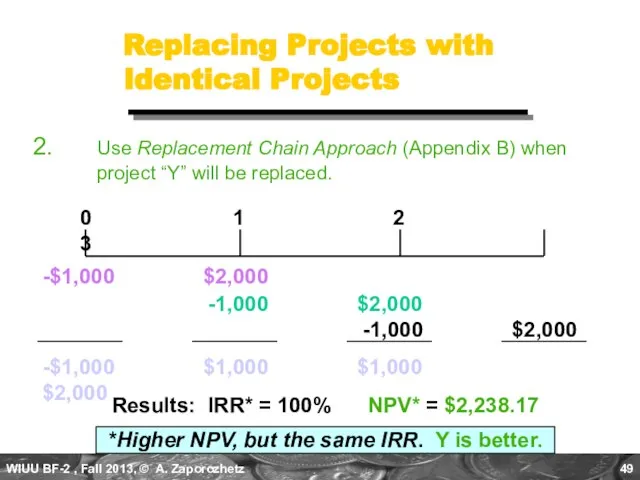

Слайд 49Replacing Projects with Identical Projects

2. Use Replacement Chain Approach (Appendix B) when project

Replacing Projects with Identical Projects

2. Use Replacement Chain Approach (Appendix B) when project

Слайд 50Capital Rationing

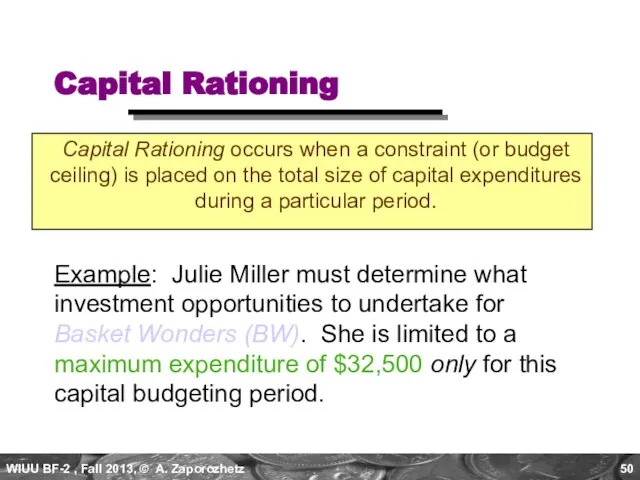

Capital Rationing occurs when a constraint (or budget ceiling) is placed

Capital Rationing

Capital Rationing occurs when a constraint (or budget ceiling) is placed

Слайд 51Available Projects for BW

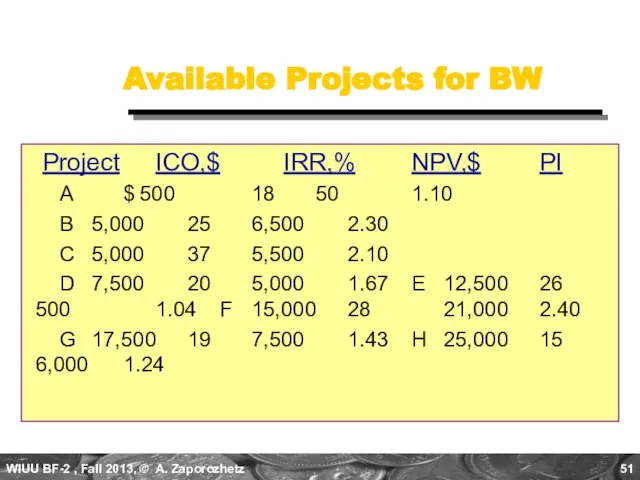

Project ICO,$ IRR,% NPV,$ PI

A $ 500 18

Available Projects for BW

Project ICO,$ IRR,% NPV,$ PI

A $ 500 18

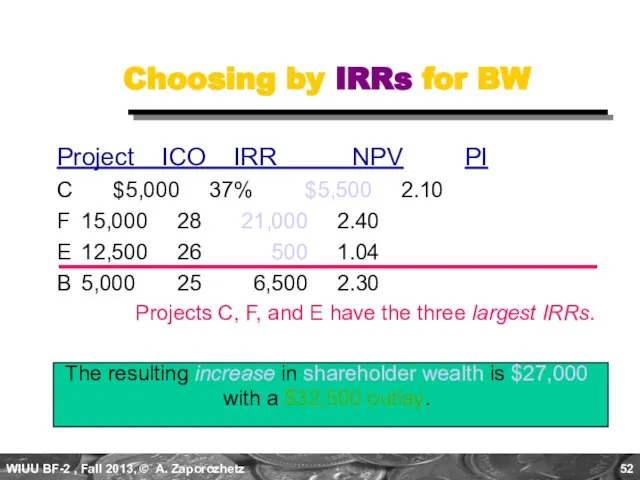

Слайд 52Choosing by IRRs for BW

Project ICO IRR NPV PI

C $5,000 37% $5,500 2.10

Choosing by IRRs for BW

Project ICO IRR NPV PI

C $5,000 37% $5,500 2.10

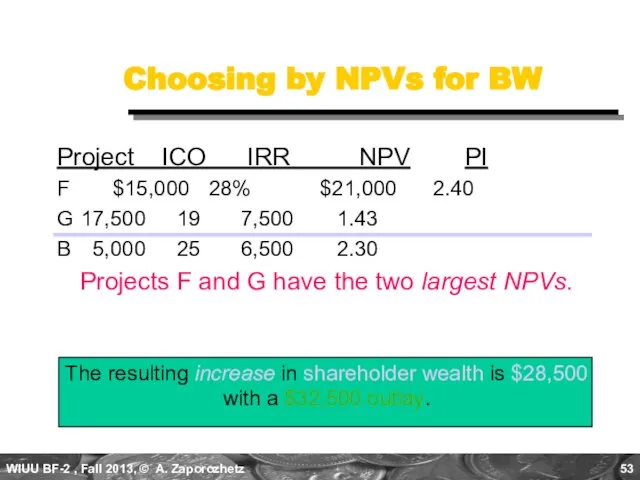

Слайд 53Choosing by NPVs for BW

Project ICO IRR NPV PI

F $15,000 28% $21,000

Choosing by NPVs for BW

Project ICO IRR NPV PI

F $15,000 28% $21,000

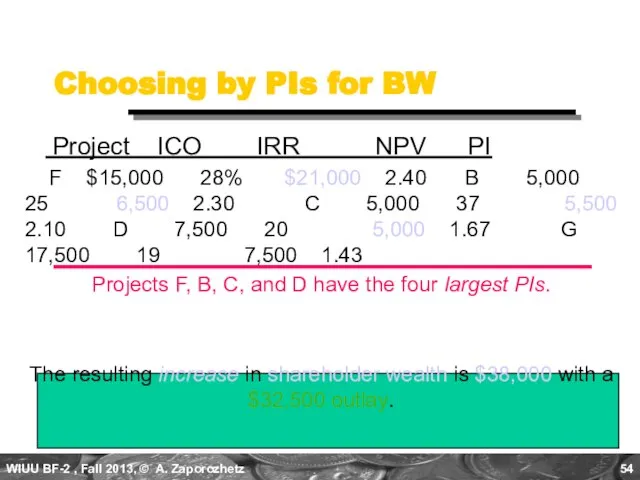

Слайд 54Choosing by PIs for BW

Project ICO IRR NPV PI

F $15,000

Choosing by PIs for BW

Project ICO IRR NPV PI

F $15,000

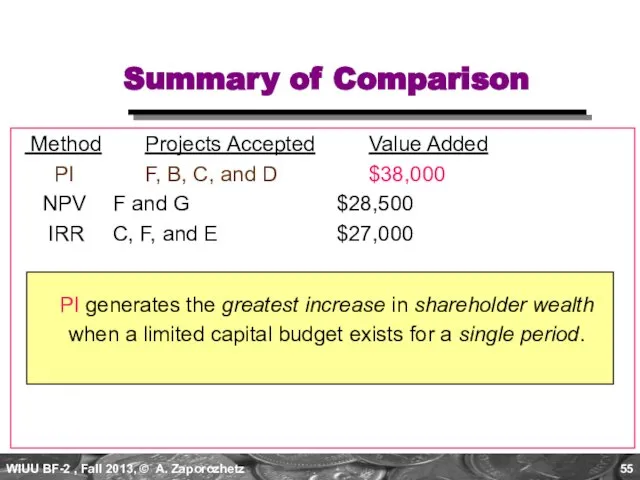

Слайд 55Summary of Comparison

Method Projects Accepted Value Added

PI F, B, C,

Summary of Comparison

Method Projects Accepted Value Added

PI F, B, C,

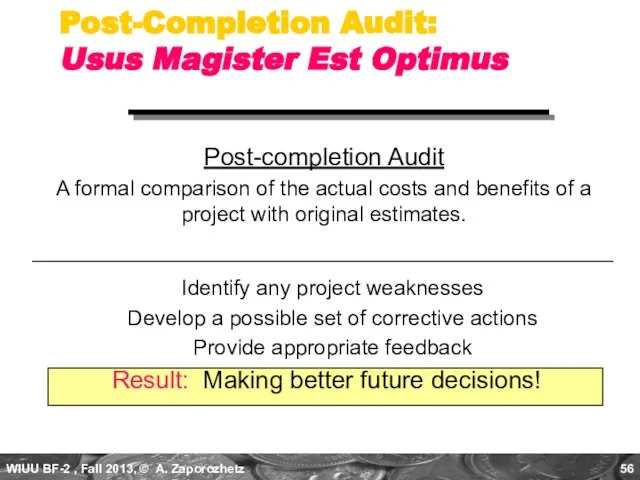

Слайд 56Post-Completion Audit:

Usus Magister Est Optimus

Post-completion Audit

A formal comparison of the actual

Post-Completion Audit:

Usus Magister Est Optimus

Post-completion Audit

A formal comparison of the actual

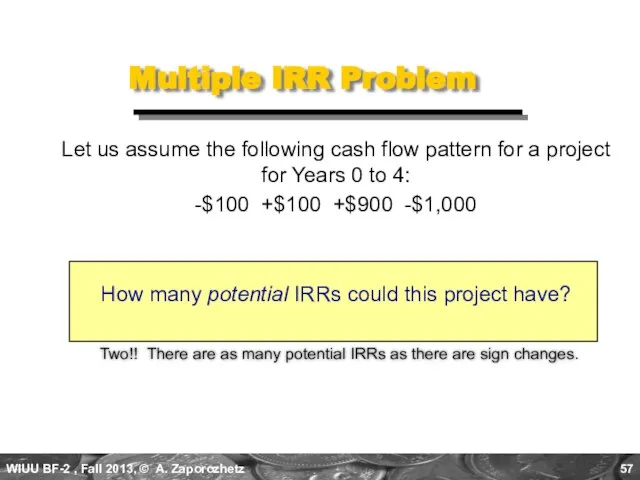

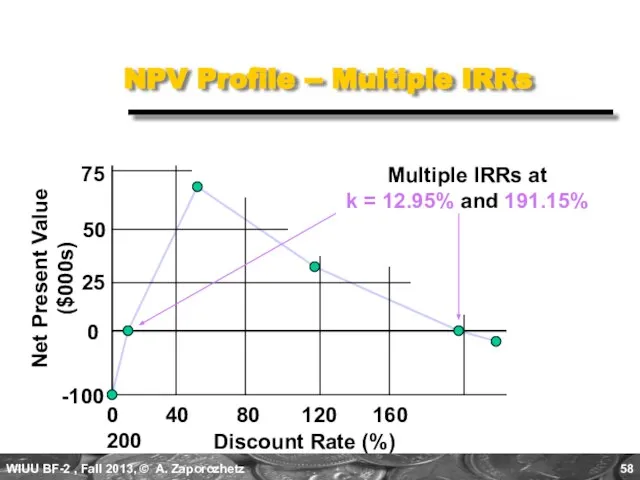

Слайд 57Multiple IRR Problem

Two!! There are as many potential IRRs as there

Multiple IRR Problem

Two!! There are as many potential IRRs as there

Слайд 58NPV Profile -- Multiple IRRs

Discount Rate (%)

0 40 80 120 160 200

Net

NPV Profile -- Multiple IRRs

Discount Rate (%)

0 40 80 120 160 200

Net

Папка проведение ВВ

Папка проведение ВВ Загадка карты

Загадка карты Разработка модифицированной (авторизованной) учебной программы

Разработка модифицированной (авторизованной) учебной программы Можно ли верить рекламе?

Можно ли верить рекламе? Многослойное стекло в технике Галле, Императорского стеклянного завода

Многослойное стекло в технике Галле, Императорского стеклянного завода Теория обучения (Дидактика)

Теория обучения (Дидактика)  ХУДОЖЕСТВЕННОЕ ОФОРМЛЕНИЕ МАГИЧЕСКИХ РИТУАЛОВ И ОБРЯДОВ

ХУДОЖЕСТВЕННОЕ ОФОРМЛЕНИЕ МАГИЧЕСКИХ РИТУАЛОВ И ОБРЯДОВ 10

10 Будущее доменных имен

Будущее доменных имен Иллюстрации к стихам Агнии Львовны Барто

Иллюстрации к стихам Агнии Львовны Барто По морю, по океану

По морю, по океану Ярмарка инноваций в образовании Секция: Инновации в дошкольном образовании

Ярмарка инноваций в образовании Секция: Инновации в дошкольном образовании شرحةأسماء الإشارة بالصوت 2

شرحةأسماء الإشارة بالصوت 2 Образовательный процесс в условиях инновационного развития вуза

Образовательный процесс в условиях инновационного развития вуза в 20 школе

в 20 школе Деньги–оплатники. Фальшивые деньги – ложники

Деньги–оплатники. Фальшивые деньги – ложники Презентация к уроку русского языка в 3 классе на тему: «Текст. Закрепление»

Презентация к уроку русского языка в 3 классе на тему: «Текст. Закрепление» Дәріс №9

Дәріс №9 Жилетки. Турнир на кубок микрорайона

Жилетки. Турнир на кубок микрорайона Имидж сотрудников. Стиль, карьера и красота

Имидж сотрудников. Стиль, карьера и красота Формы (источники) права. Основы права. Тема 5

Формы (источники) права. Основы права. Тема 5 Отношения в обществе

Отношения в обществе Муниципальное образовательное учреждение средняя общеобразовательная школа № 36 г. Владимира

Муниципальное образовательное учреждение средняя общеобразовательная школа № 36 г. Владимира Региональные и федеральные службы помощи

Региональные и федеральные службы помощи Тема

Тема Принципы защиты интеллектуальной собственности при создании инновационных проектов

Принципы защиты интеллектуальной собственности при создании инновационных проектов Презентация на тему Обстоятельство (4 класс)

Презентация на тему Обстоятельство (4 класс) Знаки препинания в простом осложнённом предложении (однородные члены предложения)

Знаки препинания в простом осложнённом предложении (однородные члены предложения)