- EU Financial Markets

Содержание

- 2. Introduction Public offer of Securities Prospectus requirements Post-listing Disclosure Liability for breaches

- 3. Introduction Private vs Public enforcement – clearly evident in pre- and post-listing disclosure requirement rules Information

- 4. Prospectus Directive Rules on pre- and post-listing disclosure in VPTS and also Nasdaq OMX Tallinn rules

- 5. Prospectus Directive Prospectus directive: Single passport regime (passporting) Definition of notion of public offer of securities

- 6. Prospectus Directive Following principles ought to be respected (preamble, recital 43): Need to provide investors with

- 7. Prospectus Directive Following principles ought to be respected (preamble, recital 43): Need to foster the international

- 8. Prospectus Directive Prospectus Directive (2003/6/EC) Regulation (EC) No 809/2004 of 29 April 2004 implementing Directive 2003/71/EC

- 9. Public offer Participants to the securities markets (VPTS § 4-7): Issuer Offeror Investor

- 10. Public offer Offer of securities (VPTS § 11): Communication to persons in any form and by

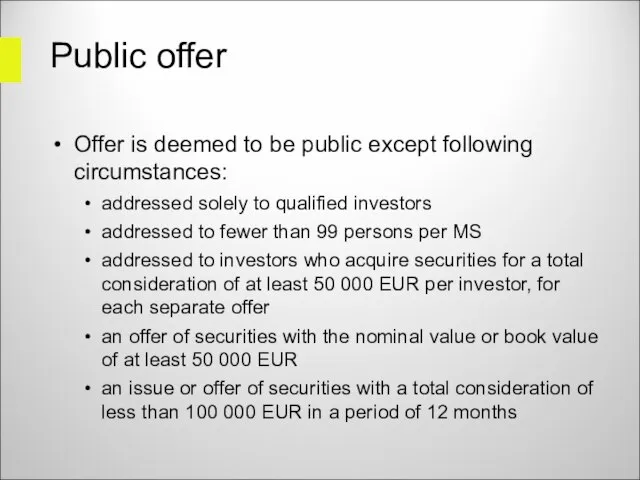

- 11. Public offer Offer is deemed to be public except following circumstances: addressed solely to qualified investors

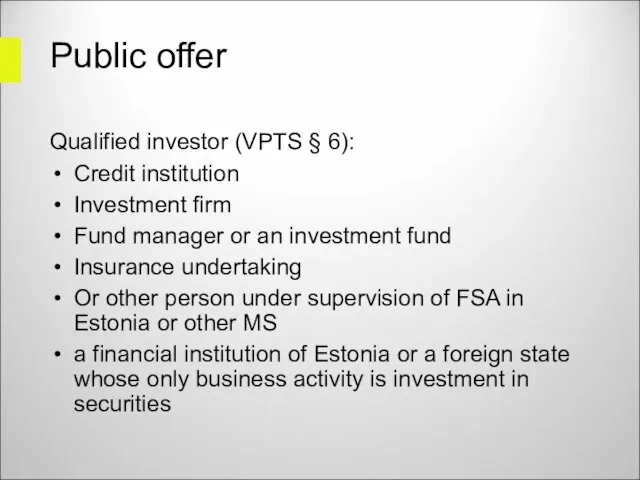

- 12. Public offer Qualified investor (VPTS § 6): Credit institution Investment firm Fund manager or an investment

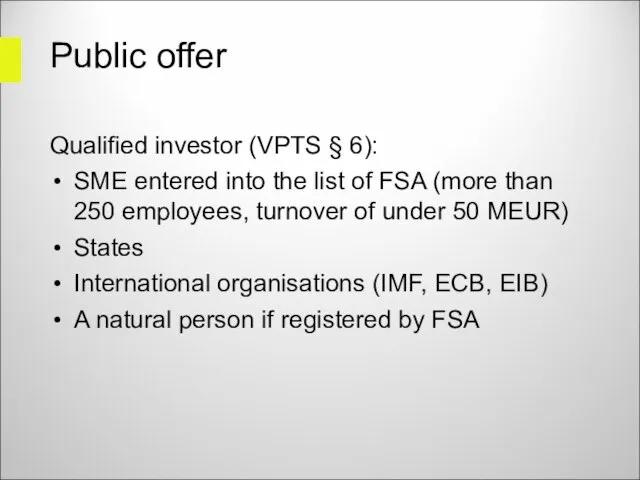

- 13. Public offer Qualified investor (VPTS § 6): SME entered into the list of FSA (more than

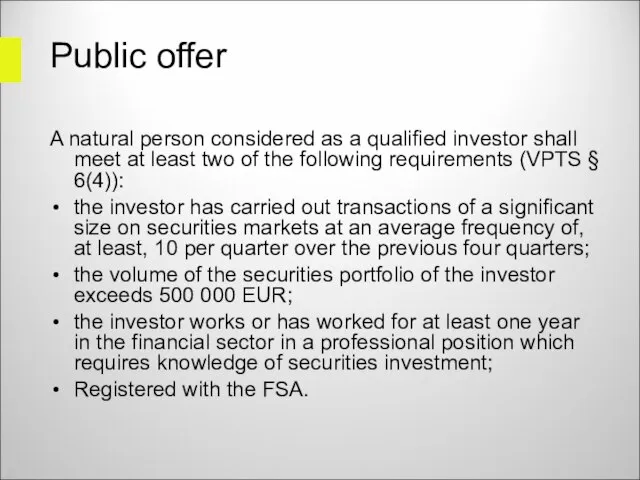

- 14. Public offer A natural person considered as a qualified investor shall meet at least two of

- 15. Public offer Following offers are also considered as public offers: Any subsequent resale of securities considered

- 16. Public offer Issue of securities (VPTS § 13): a pool of securities of the same type

- 17. Public offer Issue structure: Shares: existing shares offered vs issue of new shares Bonds: bonds issued

- 18. Prospectus In the case of public offer a prospectus must be drafted subject to VPTS and

- 19. Prospectus Prospectus Directive underline only principal requirements to the prospectus The exact requirements on parts and

- 20. Prospectus Schedule – a list of minimum information requirements adapted to the particular nature of the

- 21. Prospectus General requirements (VPTS § 141 and Prospectus Regulation preamble): Must contain all information Information must

- 22. Prospectus General requirements (VPTS § 141 and Prospectus Regulation preamble): Voluntary disclosure of profit forecasts should

- 23. Prospectus The ultimate underlying principle is that the information should be sufficient for an investor to

- 24. Prospectus Taking account the specific nature of the requirements already mentioned before such decision is rather

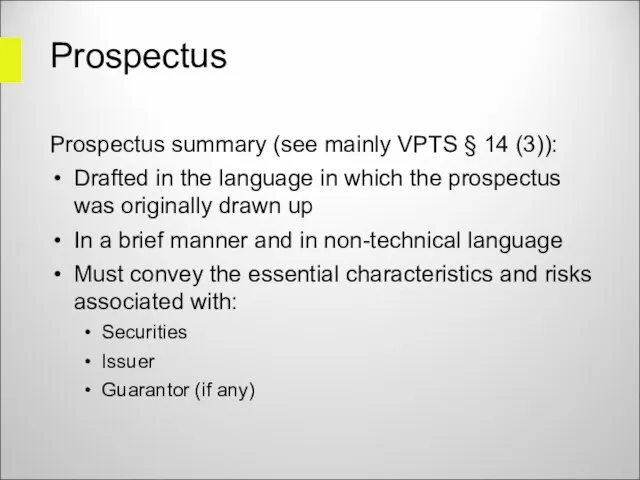

- 25. Prospectus Prospectus summary (see mainly VPTS § 14 (3)): Drafted in the language in which the

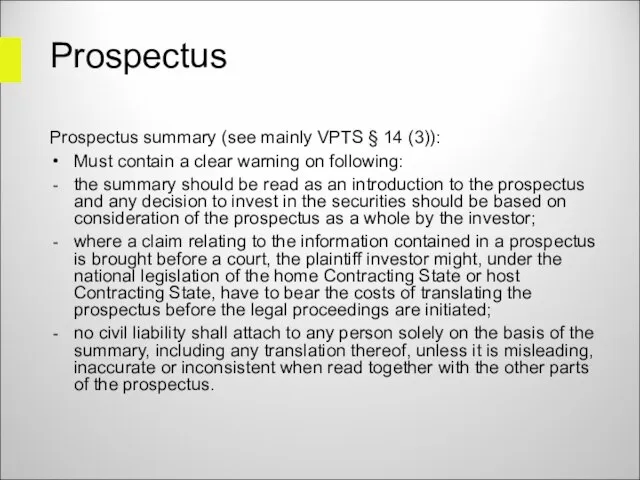

- 26. Prospectus Prospectus summary (see mainly VPTS § 14 (3)): Must contain a clear warning on following:

- 27. Prospectus Parts of prospectus (VTPS § 141): Consisting of one document Consisting of separate documents Registration

- 28. Making prospectus public Rules on advertisements: A notice in a daily newspaper must be published (see

- 29. Prospectus Registration Prospectus must be registered with the (local) FSA Additional rules on listing apply –

- 30. Prospectus Registration Application to FSA Application Prospectus Copy of Articles of Association of the issuer (if

- 31. Prospectus Registration FSA resolution within 10 days FSA can refuse to register the conditions of the

- 32. Passporting One single approval of the prospectus (namely the approval by the home MS) is “valid

- 33. Prospectus liability Requirements for civil liability: Information proves different from actual circumstances or omission of facts

- 34. Prospectus liability Requirements for civil liability: Owner of the security can claim damages Limitation period of

- 35. Post-listing disclosure Rules stipulated in: VPTS, largely based on the Directive 2004/109/EC on the harmonization of

- 36. Post-listing disclosure Existing Directive 2004/109/EC will be substituted by new directive 2013/50/eu (22.10.2013).

- 37. Post-listing disclosure Annual reports Within 4 months after the end of financial year Annual financial report

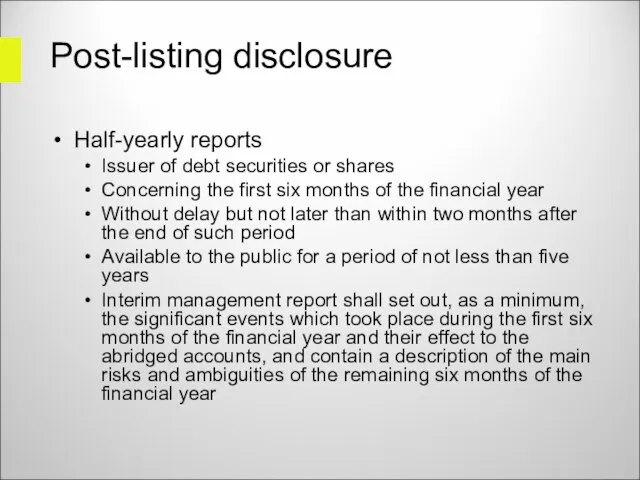

- 38. Post-listing disclosure Half-yearly reports Issuer of debt securities or shares Concerning the first six months of

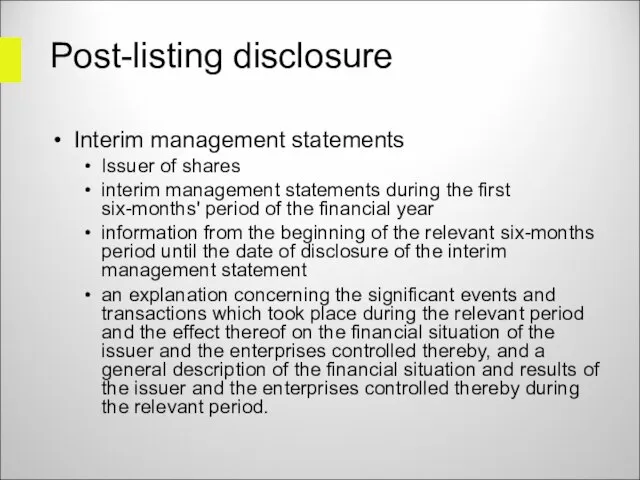

- 39. Post-listing disclosure Interim management statements Issuer of shares interim management statements during the first six-months' period

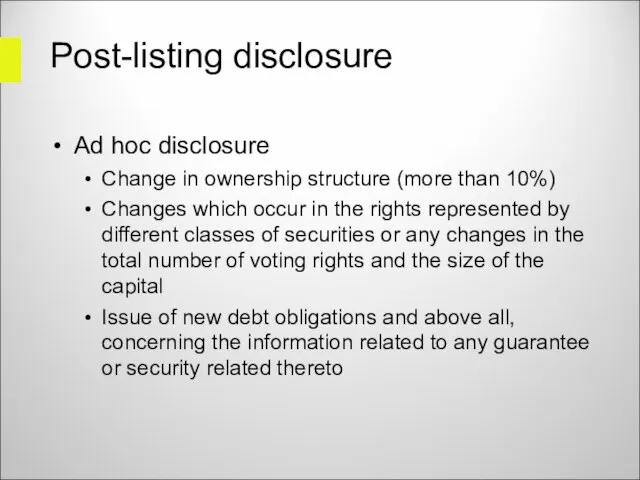

- 40. Post-listing disclosure Ad hoc disclosure Change in ownership structure (more than 10%) Changes which occur in

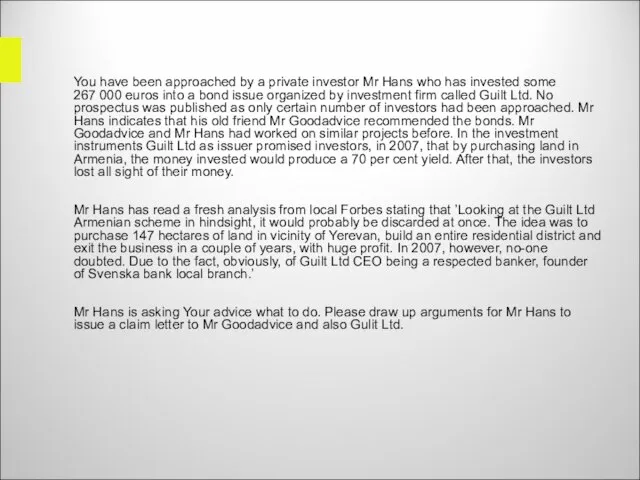

- 41. You have been approached by a private investor Mr Hans who has invested some 267 000

- 43. Скачать презентацию

Слайд 2Introduction

Public offer of Securities

Prospectus requirements

Post-listing Disclosure

Liability for breaches

Introduction

Public offer of Securities

Prospectus requirements

Post-listing Disclosure

Liability for breaches

Слайд 3Introduction

Private vs Public enforcement – clearly evident in pre- and post-listing

Introduction

Private vs Public enforcement – clearly evident in pre- and post-listing

Слайд 4Prospectus Directive

Rules on pre- and post-listing disclosure in VPTS and also Nasdaq

Prospectus Directive

Rules on pre- and post-listing disclosure in VPTS and also Nasdaq

Слайд 5Prospectus Directive

Prospectus directive:

Single passport regime (passporting)

Definition of notion of public offer

Prospectus Directive

Prospectus directive:

Single passport regime (passporting)

Definition of notion of public offer

Слайд 6Prospectus Directive

Following principles ought to be respected (preamble, recital 43):

Need to provide

Prospectus Directive

Following principles ought to be respected (preamble, recital 43):

Need to provide

Слайд 7Prospectus Directive

Following principles ought to be respected (preamble, recital 43):

Need to foster

Prospectus Directive

Following principles ought to be respected (preamble, recital 43):

Need to foster

Слайд 8Prospectus Directive

Prospectus Directive (2003/6/EC)

Regulation (EC) No 809/2004 of 29 April 2004 implementing

Prospectus Directive

Prospectus Directive (2003/6/EC)

Regulation (EC) No 809/2004 of 29 April 2004 implementing

Слайд 9Public offer

Participants to the securities markets (VPTS § 4-7):

Issuer

Offeror

Investor

Public offer

Participants to the securities markets (VPTS § 4-7):

Issuer

Offeror

Investor

Слайд 10Public offer

Offer of securities (VPTS § 11):

Communication to persons in any form

Public offer

Offer of securities (VPTS § 11):

Communication to persons in any form

Слайд 11Public offer

Offer is deemed to be public except following circumstances:

addressed solely

Public offer

Offer is deemed to be public except following circumstances:

addressed solely

Слайд 12Public offer

Qualified investor (VPTS § 6):

Credit institution

Investment firm

Fund manager or an

Public offer

Qualified investor (VPTS § 6):

Credit institution

Investment firm

Fund manager or an

Слайд 13Public offer

Qualified investor (VPTS § 6):

SME entered into the list of

Public offer

Qualified investor (VPTS § 6):

SME entered into the list of

Слайд 14Public offer

A natural person considered as a qualified investor shall meet at

Public offer

A natural person considered as a qualified investor shall meet at

Слайд 15Public offer

Following offers are also considered as public offers:

Any subsequent resale

Public offer

Following offers are also considered as public offers:

Any subsequent resale

Слайд 16Public offer

Issue of securities (VPTS § 13):

a pool of securities

Public offer

Issue of securities (VPTS § 13):

a pool of securities

Слайд 17Public offer

Issue structure:

Shares: existing shares offered vs issue of new

Public offer

Issue structure:

Shares: existing shares offered vs issue of new

Слайд 18Prospectus

In the case of public offer a prospectus must be drafted subject

Prospectus

In the case of public offer a prospectus must be drafted subject

Слайд 19Prospectus

Prospectus Directive underline only principal requirements to the prospectus

The exact requirements on

Prospectus

Prospectus Directive underline only principal requirements to the prospectus

The exact requirements on

Слайд 20Prospectus

Schedule – a list of minimum information requirements adapted to the particular

Prospectus

Schedule – a list of minimum information requirements adapted to the particular

Слайд 21Prospectus

General requirements (VPTS § 141 and Prospectus Regulation preamble):

Must contain

Prospectus

General requirements (VPTS § 141 and Prospectus Regulation preamble):

Must contain

Слайд 22Prospectus

General requirements (VPTS § 141 and Prospectus Regulation preamble):

Voluntary disclosure

Prospectus

General requirements (VPTS § 141 and Prospectus Regulation preamble):

Voluntary disclosure

Слайд 23Prospectus

The ultimate underlying principle is that the information should be sufficient

Prospectus

The ultimate underlying principle is that the information should be sufficient

Слайд 24Prospectus

Taking account the specific nature of the requirements already mentioned before

Prospectus

Taking account the specific nature of the requirements already mentioned before

Слайд 25Prospectus

Prospectus summary (see mainly VPTS § 14 (3)):

Drafted in the language

Prospectus

Prospectus summary (see mainly VPTS § 14 (3)):

Drafted in the language

Слайд 26Prospectus

Prospectus summary (see mainly VPTS § 14 (3)):

Must contain a clear

Prospectus

Prospectus summary (see mainly VPTS § 14 (3)):

Must contain a clear

Слайд 27Prospectus

Parts of prospectus (VTPS § 141):

Consisting of one document

Consisting

Prospectus

Parts of prospectus (VTPS § 141):

Consisting of one document

Consisting

Слайд 28Making prospectus public

Rules on advertisements:

A notice in a daily newspaper must

Making prospectus public

Rules on advertisements:

A notice in a daily newspaper must

Слайд 29Prospectus Registration

Prospectus must be registered with the (local) FSA

Additional rules on

Prospectus Registration

Prospectus must be registered with the (local) FSA

Additional rules on

Слайд 30Prospectus Registration

Application to FSA

Application

Prospectus

Copy of Articles of Association of the issuer

Prospectus Registration

Application to FSA

Application

Prospectus

Copy of Articles of Association of the issuer

Слайд 31Prospectus Registration

FSA resolution within 10 days

FSA can refuse to register

the

Prospectus Registration

FSA resolution within 10 days

FSA can refuse to register

the

Слайд 32Passporting

One single approval of the prospectus (namely the approval by the

Passporting

One single approval of the prospectus (namely the approval by the

Слайд 33Prospectus liability

Requirements for civil liability:

Information proves different from actual circumstances or

Prospectus liability

Requirements for civil liability:

Information proves different from actual circumstances or

Слайд 34Prospectus liability

Requirements for civil liability:

Owner of the security can claim damages

Prospectus liability

Requirements for civil liability:

Owner of the security can claim damages

Слайд 35Post-listing disclosure

Rules stipulated in:

VPTS, largely based on the Directive 2004/109/EC on

Post-listing disclosure

Rules stipulated in:

VPTS, largely based on the Directive 2004/109/EC on

Слайд 36Post-listing disclosure

Existing Directive 2004/109/EC will be substituted by new directive 2013/50/eu (22.10.2013).

Post-listing disclosure

Existing Directive 2004/109/EC will be substituted by new directive 2013/50/eu (22.10.2013).

Слайд 37Post-listing disclosure

Annual reports

Within 4 months after the end of financial year

Annual

Post-listing disclosure

Annual reports

Within 4 months after the end of financial year

Annual

Слайд 38Post-listing disclosure

Half-yearly reports

Issuer of debt securities or shares

Concerning the first six months

Post-listing disclosure

Half-yearly reports

Issuer of debt securities or shares

Concerning the first six months

Слайд 39Post-listing disclosure

Interim management statements

Issuer of shares

interim management statements during the first six-months'

Post-listing disclosure

Interim management statements

Issuer of shares

interim management statements during the first six-months'

Слайд 40Post-listing disclosure

Ad hoc disclosure

Change in ownership structure (more than 10%)

Changes which occur

Post-listing disclosure

Ad hoc disclosure

Change in ownership structure (more than 10%)

Changes which occur

Слайд 41 You have been approached by a private investor Mr Hans who has

You have been approached by a private investor Mr Hans who has

Собор Парижской Богоматери. Франция - родина готической архитектуры

Собор Парижской Богоматери. Франция - родина готической архитектуры Паркет Europa

Паркет Europa О подготовке образовательных учреждений города Лангепаса к началу 2012-2013 учебного года

О подготовке образовательных учреждений города Лангепаса к началу 2012-2013 учебного года Тайна Шекспира

Тайна Шекспира Торнадо любви. Направление Личные Цели

Торнадо любви. Направление Личные Цели Who took the cookie from the cookie jar

Who took the cookie from the cookie jar Сказка «Волшебное число»

Сказка «Волшебное число» My giant nerd boyfriend

My giant nerd boyfriend Роль системы развития персонала организации

Роль системы развития персонала организации Цифровая подстанция - важный элемент интеллектуальной энергосистемы

Цифровая подстанция - важный элемент интеллектуальной энергосистемы Как работают экономисты

Как работают экономисты «Вода – капля жизни» Участники: Дети и родители Воспитатели: Андреева Янина Евгеньевна

«Вода – капля жизни» Участники: Дети и родители Воспитатели: Андреева Янина Евгеньевна Жемчужины Республики Марий Эл

Жемчужины Республики Марий Эл Социальная напряжённость

Социальная напряжённость Метрологическое обеспечение технологического процесса изготовления продукции

Метрологическое обеспечение технологического процесса изготовления продукции Технологии разработки проектов, программ и требования к их реализации

Технологии разработки проектов, программ и требования к их реализации Построение чертежа фартука

Построение чертежа фартука Финансовая отчетностьв реальном времени.

Финансовая отчетностьв реальном времени. Кислоты 11 класс

Кислоты 11 класс Внутреннее строение рыб

Внутреннее строение рыб Автоматизация АОСЧ

Автоматизация АОСЧ М.А.Шолохов

М.А.Шолохов Гармония образа

Гармония образа Словарик горнорудных профессий

Словарик горнорудных профессий План «Барбаросса» предполагал «блицкриг» - т.е. рассчитан на молниеносную войну в течение нескольких месяцевБарбароссаблицкриг.

План «Барбаросса» предполагал «блицкриг» - т.е. рассчитан на молниеносную войну в течение нескольких месяцевБарбароссаблицкриг. Гражданское общество и правовое государство. 9 класс

Гражданское общество и правовое государство. 9 класс Конкурс чтецов, посвящённый творчеству Э. Асадова

Конкурс чтецов, посвящённый творчеству Э. Асадова СГУ им. Чернышевского

СГУ им. Чернышевского