- Exploration for and Evaluation of Mineral Resources

Содержание

- 2. CONTENT: Objective and Scope Recognition and Measurement of Exploration and Evaluation Assets Impairment Disclosure

- 3. IFRS 6 – Objective and Scope IFRS 6 is limited to the accounting for and reporting

- 4. IFRS 6 – Objective and Scope IFRS 6 is an interim measure pending completion of a

- 5. IFRS 6 – Recognition and Measurement of Exploration and Evaluation Assets Recognition: Companies use a variety

- 6. IFRS 6 – Recognition and Measurement of Exploration and Evaluation Assets Exploration and evaluation assets are

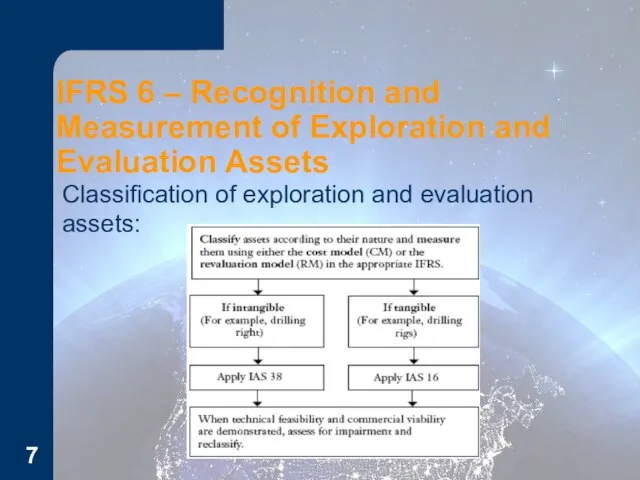

- 7. IFRS 6 – Recognition and Measurement of Exploration and Evaluation Assets Classification of exploration and evaluation

- 8. IFRS 6 - Impairment Impaired? When facts and circumstances suggest that carrying amount > recoverable amount.

- 9. IFRS 6 - Disclosure Disclosure objective: to identify and explain amounts recognized in the financial statements

- 10. IFRS 6 - Disclosure Minimum disclosure: Accounting policies for exploration and evaluation expenditures and their capitalization

- 12. Скачать презентацию

Слайд 2CONTENT:

Objective and Scope

Recognition and Measurement of Exploration and Evaluation Assets

Impairment

Disclosure

CONTENT:

Objective and Scope

Recognition and Measurement of Exploration and Evaluation Assets

Impairment

Disclosure

Слайд 3IFRS 6 – Objective and

Scope

IFRS 6 is limited to the accounting

IFRS 6 – Objective and

Scope

IFRS 6 is limited to the accounting

Слайд 4IFRS 6 – Objective and Scope

IFRS 6 is an interim measure pending

IFRS 6 – Objective and Scope

IFRS 6 is an interim measure pending

Слайд 5IFRS 6 – Recognition and Measurement of Exploration and Evaluation Assets

Recognition:

Companies use

IFRS 6 – Recognition and Measurement of Exploration and Evaluation Assets

Recognition:

Companies use

Слайд 6IFRS 6 – Recognition and Measurement of Exploration and Evaluation Assets

Exploration and

IFRS 6 – Recognition and Measurement of Exploration and Evaluation Assets

Exploration and

Слайд 7IFRS 6 – Recognition and Measurement of Exploration and Evaluation Assets

Classification of

IFRS 6 – Recognition and Measurement of Exploration and Evaluation Assets

Classification of

Слайд 8IFRS 6 - Impairment

Impaired? When facts and circumstances suggest that carrying amount

IFRS 6 - Impairment

Impaired? When facts and circumstances suggest that carrying amount

Слайд 9IFRS 6 - Disclosure

Disclosure objective: to identify and explain amounts recognized in

IFRS 6 - Disclosure

Disclosure objective: to identify and explain amounts recognized in

Слайд 10IFRS 6 - Disclosure

Minimum disclosure:

Accounting policies for exploration and evaluation expenditures and

IFRS 6 - Disclosure

Minimum disclosure:

Accounting policies for exploration and evaluation expenditures and

Основы энергетики

Основы энергетики ЧТО ЛЮБЯТ ДЕЛАТЬ ДЕТИ?

ЧТО ЛЮБЯТ ДЕЛАТЬ ДЕТИ? «Философия жизни...»

«Философия жизни...» Відкриті нічні кіноперегляди у Луцьку

Відкриті нічні кіноперегляди у Луцьку ИБП APC Back-UPS ES 350/500APC CyberFort 350/500BF350-GR, BF500-GRBF350-UK, BF500-UKBF350-IT, BF500-ITBF350-RS, BF500-RSBF350-FR, BF500-FR

ИБП APC Back-UPS ES 350/500APC CyberFort 350/500BF350-GR, BF500-GRBF350-UK, BF500-UKBF350-IT, BF500-ITBF350-RS, BF500-RSBF350-FR, BF500-FR Открытия Христофора Колумба

Открытия Христофора Колумба Краю – 75: помним, гордимся, наследуем!

Краю – 75: помним, гордимся, наследуем! Правописание корня слова

Правописание корня слова Планирование образовательной работы в дошкольном образовательном учреждении в соответствии ФГТ Перспективное и календарное пла

Планирование образовательной работы в дошкольном образовательном учреждении в соответствии ФГТ Перспективное и календарное пла Тетёра

Тетёра А19.Слитное, дефисное, раздельное написание.

А19.Слитное, дефисное, раздельное написание. Приобщение дошкольников к истокам национальной культуры, традиционным культурным ценностям

Приобщение дошкольников к истокам национальной культуры, традиционным культурным ценностям Дымковская игрушка (7 класс)

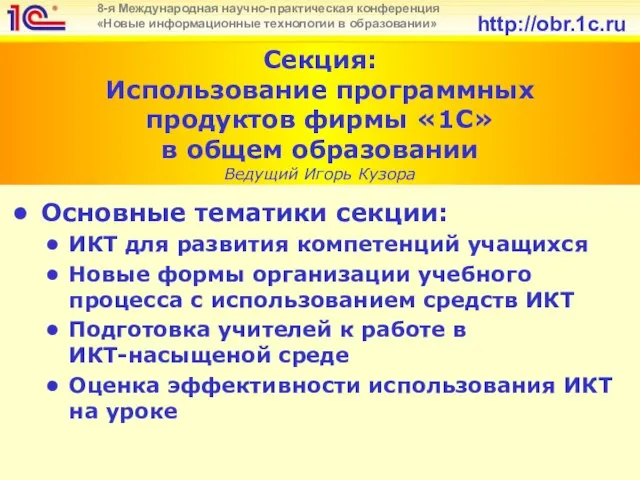

Дымковская игрушка (7 класс) Секция: Использование программных продуктов фирмы «1С» в общем образовании Ведущий Игорь Кузора

Секция: Использование программных продуктов фирмы «1С» в общем образовании Ведущий Игорь Кузора Литература и история

Литература и история Пейзаж, натюрморт, портрет

Пейзаж, натюрморт, портрет Возможности контроля выбросов в странах-нечленах ЕС

Возможности контроля выбросов в странах-нечленах ЕС Презентация на тему Приготовление обеда в походных условиях (7 класс)

Презентация на тему Приготовление обеда в походных условиях (7 класс) Становление Древнерусского государства

Становление Древнерусского государства Вещество номер один!

Вещество номер один! Всероссийская лабораторная

Всероссийская лабораторная История семи великих камней Алмазного фонда России

История семи великих камней Алмазного фонда России Население России. История переписи населения

Население России. История переписи населения Взаимодействие семьи и школы в современных условиях

Взаимодействие семьи и школы в современных условиях Описание внешности

Описание внешности Народный праздник Ивана Купалы

Народный праздник Ивана Купалы МОУ Венгеровская СОШ №2«Опыт работы с одаренными детьми на уроках английского языка.»

МОУ Венгеровская СОШ №2«Опыт работы с одаренными детьми на уроках английского языка.» Оптоволоконный кабель

Оптоволоконный кабель