- Financial Law of Kazakhstan

Содержание

- 2. Home assignment Civil Code, Chapter 3, articles 128-1 – 139-1. Statute “On Securities Market”. (Закон РК

- 3. Plan Financial Instruments Derivatives Shares Bonds

- 4. Financial Instruments Financial Instruments: Money Securities Derivatives

- 5. Derivatives Derivative financial Instrument: Swap Option Futures Forward

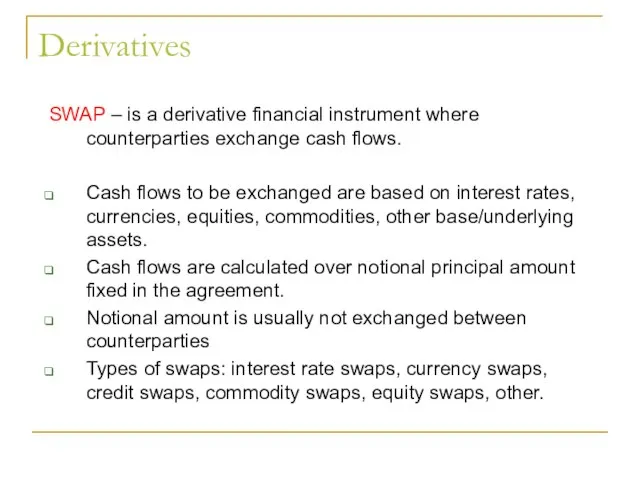

- 6. Derivatives SWAP – is a derivative financial instrument where counterparties exchange cash flows. Cash flows to

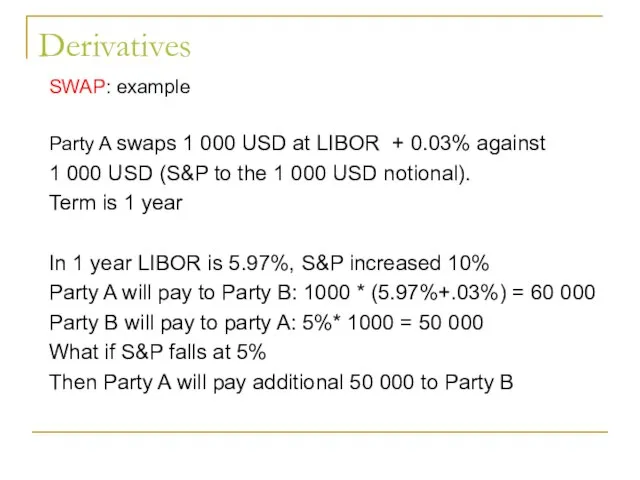

- 7. Derivatives SWAP: example Party A swaps 1 000 USD at LIBOR + 0.03% against 1 000

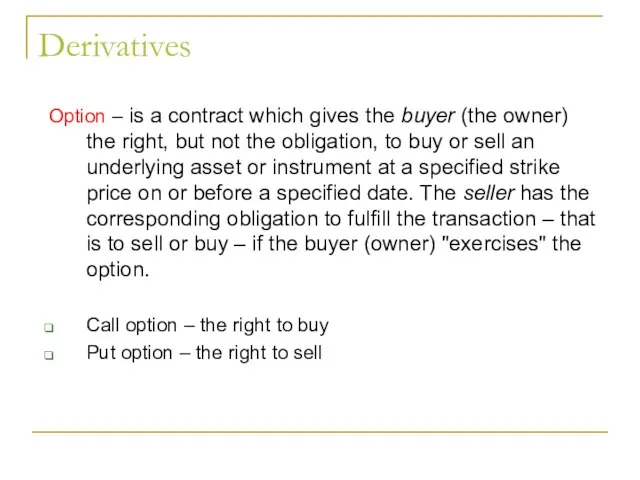

- 8. Derivatives Option – is a contract which gives the buyer (the owner) the right, but not

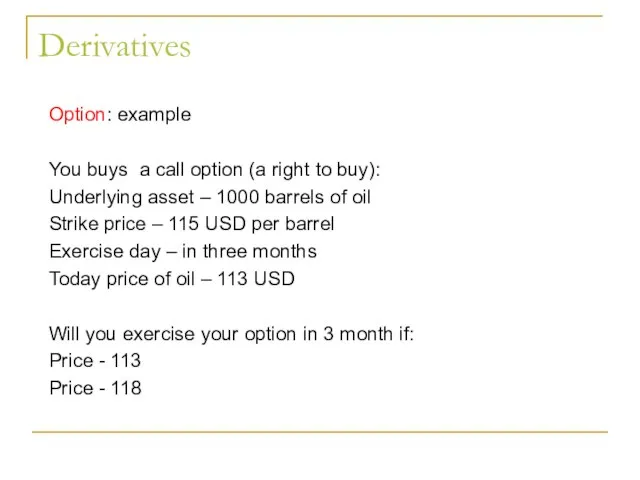

- 9. Derivatives Option: example You buys a call option (a right to buy): Underlying asset – 1000

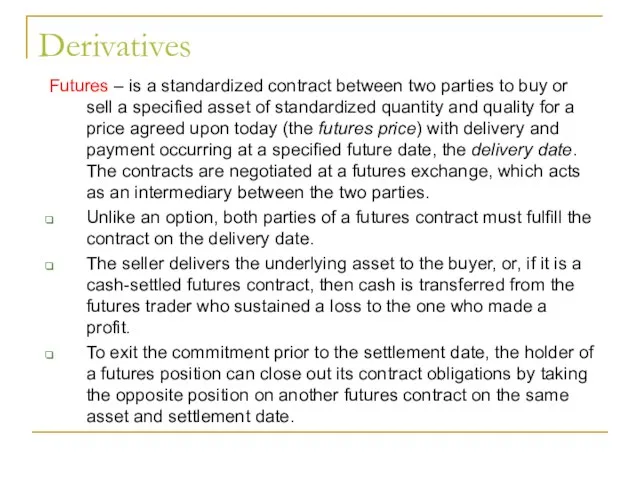

- 10. Derivatives Futures – is a standardized contract between two parties to buy or sell a specified

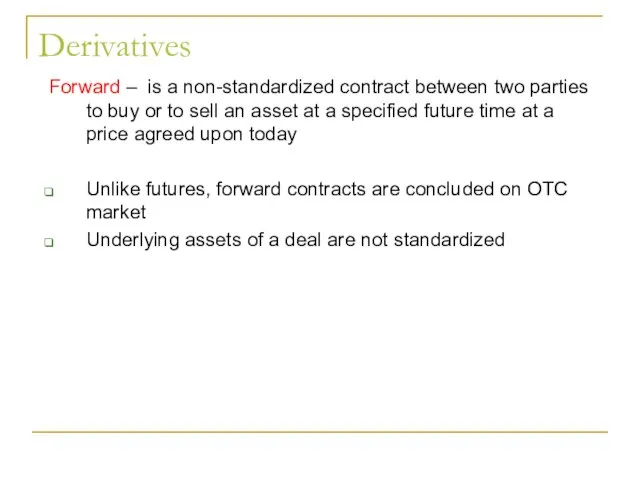

- 11. Derivatives Forward – is a non-standardized contract between two parties to buy or to sell an

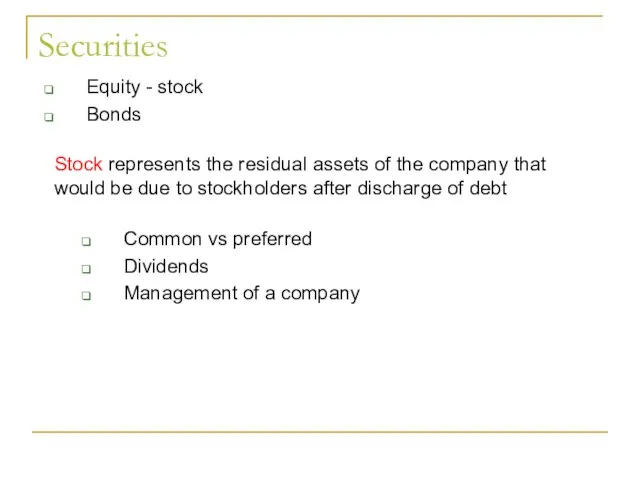

- 12. Securities Equity - stock Bonds Stock represents the residual assets of the company that would be

- 14. Скачать презентацию

Слайд 3Plan

Financial Instruments

Derivatives

Shares

Bonds

Plan

Financial Instruments

Derivatives

Shares

Bonds

Слайд 4Financial Instruments

Financial Instruments:

Money

Securities

Derivatives

Financial Instruments

Financial Instruments:

Money

Securities

Derivatives

Слайд 5Derivatives

Derivative financial Instrument:

Swap

Option

Futures

Forward

Derivatives

Derivative financial Instrument:

Swap

Option

Futures

Forward

Слайд 6Derivatives

SWAP – is a derivative financial instrument where counterparties exchange cash

Derivatives

SWAP – is a derivative financial instrument where counterparties exchange cash

Слайд 7Derivatives

SWAP: example

Party A swaps 1 000 USD at LIBOR +

Derivatives

SWAP: example

Party A swaps 1 000 USD at LIBOR +

Слайд 8Derivatives

Option – is a contract which gives the buyer (the owner) the right, but

Derivatives

Option – is a contract which gives the buyer (the owner) the right, but

Слайд 9Derivatives

Option: example

You buys a call option (a right to buy):

Underlying asset

Derivatives

Option: example

You buys a call option (a right to buy):

Underlying asset

Слайд 10Derivatives

Futures – is a standardized contract between two parties to buy or

Derivatives

Futures – is a standardized contract between two parties to buy or

Слайд 11Derivatives

Forward – is a non-standardized contract between two parties to buy

Derivatives

Forward – is a non-standardized contract between two parties to buy

Слайд 12Securities

Equity - stock

Bonds

Stock represents the residual assets of the

Securities

Equity - stock

Bonds

Stock represents the residual assets of the

Учебный проект как средство активизации познавательной деятельности обучающихся

Учебный проект как средство активизации познавательной деятельности обучающихся Информационная страничка для детей в картинках

Информационная страничка для детей в картинках дельтаплан. Тематический блок

дельтаплан. Тематический блок Подготовка к сочинению-рассуждению на лингвистическую тему(С 2. 1)

Подготовка к сочинению-рассуждению на лингвистическую тему(С 2. 1) Паучок из фольги

Паучок из фольги На примере Реабилитационного Центра «Новая Жизнь» (Ленинградская область, Россия) Докладчик: Алексей Фомичев

На примере Реабилитационного Центра «Новая Жизнь» (Ленинградская область, Россия) Докладчик: Алексей Фомичев СПЕЦИФИКА УПРАВЛЕНИЯ ПЕРСОНАЛОМ В ХОЛДИНГЕ

СПЕЦИФИКА УПРАВЛЕНИЯ ПЕРСОНАЛОМ В ХОЛДИНГЕ Геральдика стран Европы

Геральдика стран Европы Чернышов Вадим Геннадьевич. Сертификат участника

Чернышов Вадим Геннадьевич. Сертификат участника 20161221_rossiya_v_mire1

20161221_rossiya_v_mire1 Историческая тема в живописи. Василий Иванович Суриков

Историческая тема в живописи. Василий Иванович Суриков Религии

Религии PR-кампания Института транспорта. Осенняя премьера 2016 г

PR-кампания Института транспорта. Осенняя премьера 2016 г Общее учение о субъектах административно-правовых отношений

Общее учение о субъектах административно-правовых отношений  Славные люди России

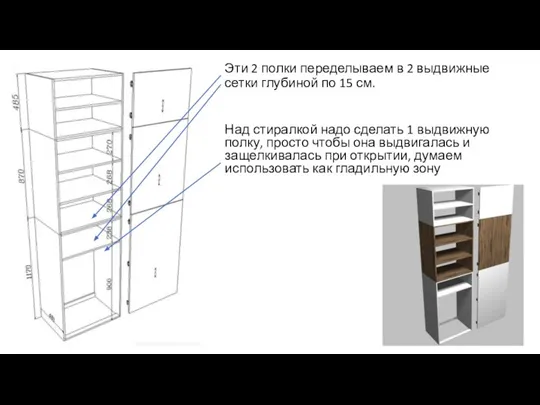

Славные люди России Ванная и спальня

Ванная и спальня ДРОНД 2010

ДРОНД 2010 Сравнительный анализ качества и обученности учащихся за 1 полугодие 2011-2012 уч.года

Сравнительный анализ качества и обученности учащихся за 1 полугодие 2011-2012 уч.года ЗАРЕЧЬЕ

ЗАРЕЧЬЕ Единая государственная система предупреждения и ликвидации чрезвычайных ситуаций (РСЧС)

Единая государственная система предупреждения и ликвидации чрезвычайных ситуаций (РСЧС) Гай Плиний старший и Клавдий Гален их вклад в биологию

Гай Плиний старший и Клавдий Гален их вклад в биологию Дистанционное открывание откидных створок

Дистанционное открывание откидных створок По страницам пройденных тем

По страницам пройденных тем Лекция_1 Магистры

Лекция_1 Магистры Презентация на тему Англия

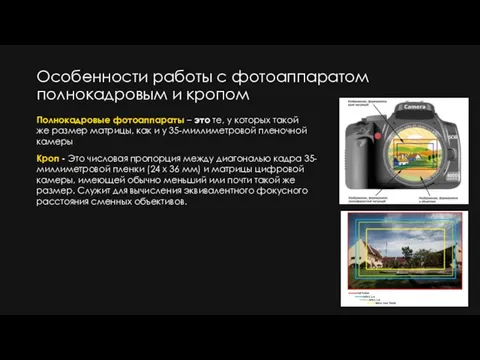

Презентация на тему Англия  Особенности работы с фотоаппаратом полнокадровым и кропом

Особенности работы с фотоаппаратом полнокадровым и кропом Middle enlgish

Middle enlgish Personal letter

Personal letter