- Financial Management

Содержание

- 2. INTRODUCTION TO FINANCIAL MANAGEMENT Nature of Financial Management 1 Objectives of Financial Management 2 Functions of

- 3. DEFINITION OF FINANCIAL MANAGEMENT The ways and means of managing money. Planning, acquisition, allocation, and utilization

- 4. NATURE OF FINANCIAL MANAGEMENT Financial Management is mainly concerned with the proper management of funds. The

- 5. SCOPE OF FINANCIAL MANAGEMENT Traditional approach It is concerned with raising of funds and administration of

- 6. SCOPE OF FINANCIAL MANAGEMENT Modern approach To decide how much amount is required from where and

- 7. OBJECTIVES OF FINANCIAL MANAGEMENT Financial objectives Non-financial objectives

- 8. FINANCIAL OBJECTIVES Profit maximization Wealth maximization

- 9. FINANCIAL OBJECTIVES Profit: Profit earning. Profitability is a barometer for measuring efficiency and economic prosperity of

- 10. PROFIT vs WEALTH The term profit is vague. Ignores the time value of money. Ignores Risk

- 11. NON-FINANCIAL OBJECTIVES General welfare of employees General welfare of society Fulfillment of responsibilities toward customers, suppliers

- 12. FUNCTIONS Of A FINANCE MANAGER Forecasting Financial Requirements Acquiring Necessary Capital Investment Decision Cash Management Interrelation

- 13. RESPONSIBILITIES OF FINANCE MANAGER The basic responsibility of the treasurer is to provide, manage and protect

- 14. FUNCTIONS OF FM

- 15. FINANCIAL MANAGEMENT PROCESS FM is a dynamic decision-making process include a series of interrelated activities involving:

- 16. FINANCIAL MANAGEMENT INSTRUMENTS Time value analysis 1 Cost of Capital 2 Investment Decisions 3

- 17. CONCEPT OF TIME VALUE OF MONEY Value of the money received today is more than the

- 18. REASONS FOR TIME PREFERENCE OF MONEY The future is always uncertain and involves risk. People generally

- 19. TIMELINE AND TIME TRAVEL An important tool used in time value of money analysis; it is

- 20. TECHNIQUES OF TIME VALUE OF MONEY Compounding Technique The process of going from today’s values, or

- 21. COMPOUNDING TECHNIQUE PV - present value, or beginning amount. (Here PV = $100). i - interest

- 22. FUTURE VALUE Future Value (FV)- The amount to which a cash flow or series of cash

- 23. FUTURE VALUE FORMULA Methods of calculating Numerical Solution Interest Tables (Tabular Solution) Financial Calculator Solution Spreadsheet

- 24. SOLVING METHODS OF TIME VALUE PROBLEM First, we state the problem in words. Next, we diagram

- 25. SOLVING METHODS OF TIME VALUE PROBLEM Numerical Solution: One can use a regular calculator and either

- 26. SOLVING METHODS OF TIME VALUE PROBLEM Interest Tables (Tabular Solution) The Future Value Interest Factor for

- 27. SOLVING METHODS OF TIME VALUE PROBLEM Financial Calculator Solution: Equation and a number of other equations

- 28. SOLVING METHODS OF TIME VALUE PROBLEM Spreadsheet Solution

- 29. MULTI PERIOD COMPOUNDING The actual rate of interest realized called effective rate in case of multi

- 30. COMPOUNDED (FUTURE) VALUE OF ANNUITY Annuity - a series of payments of an equal amount at

- 31. COMPOUNDED (FUTURE) VALUE OF ANNUITY Annuity Due - an annuity whose payments occur at the beginning

- 32. PROBLEMS What will be the value of Rs.100 after two years at 10% p.a. Rate of

- 33. PROBLEMS Mr. Adams deposits Rs.1000 at the end of every year for four years and the

- 34. TECHNIQUES OF TIME VALUE OF MONEY (cont) Discounting or Present Value Technique Present value shows what

- 35. PRESENT VALUE OF AN ANNUITY Ordinary annuities - If the payments come at the end of

- 36. PRESENT VALUE OF AN ANNUITY Annuities due - payments been made at the beginning of each

- 37. PRESENT VALUE OF AN ANNUITY Perpetuity - a stream of equal payments expected to continue forever.

- 38. PROBLEMS Calculate the present value of Rs.1000 to be received after one year @ 10% time

- 39. PROBLEMS Mr. X has to receive Rs.2000 per year for five years. Calculate the present value

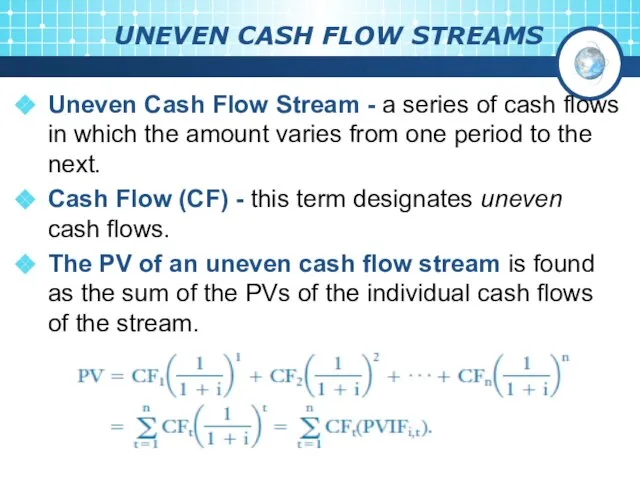

- 40. UNEVEN CASH FLOW STREAMS Uneven Cash Flow Stream - a series of cash flows in which

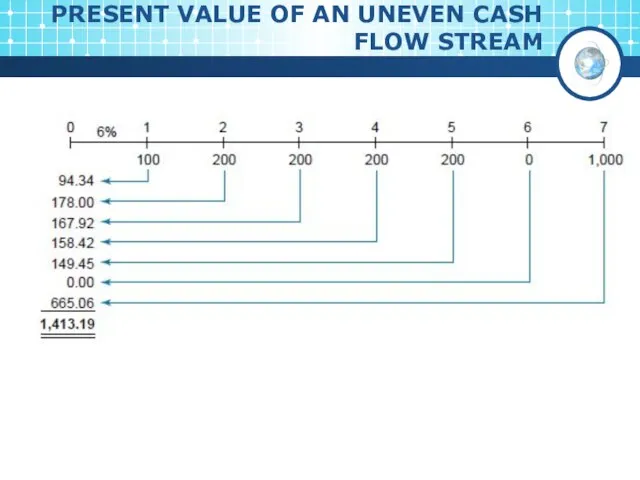

- 41. PRESENT VALUE OF AN UNEVEN CASH FLOW STREAM

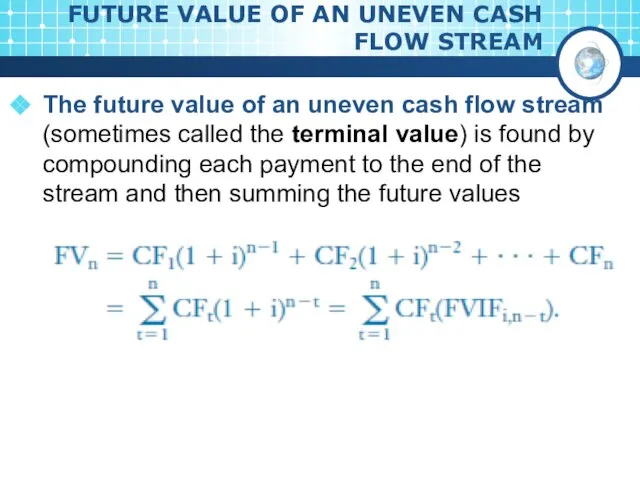

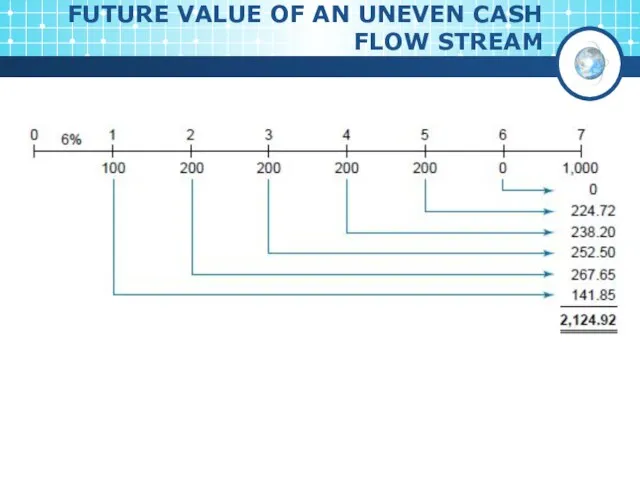

- 42. FUTURE VALUE OF AN UNEVEN CASH FLOW STREAM The future value of an uneven cash flow

- 43. FUTURE VALUE OF AN UNEVEN CASH FLOW STREAM

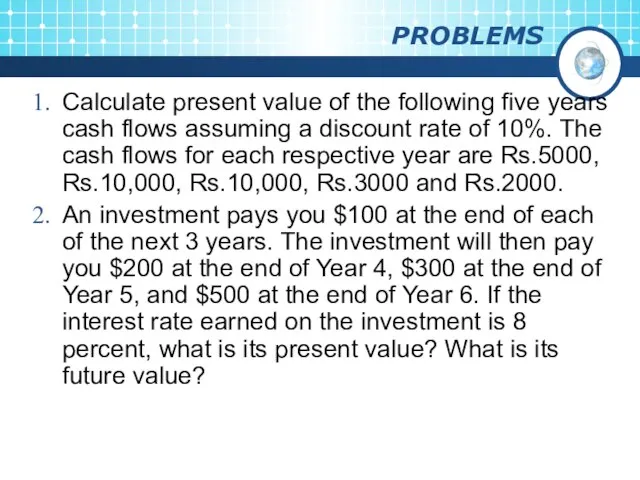

- 44. PROBLEMS Calculate present value of the following five years cash flows assuming a discount rate of

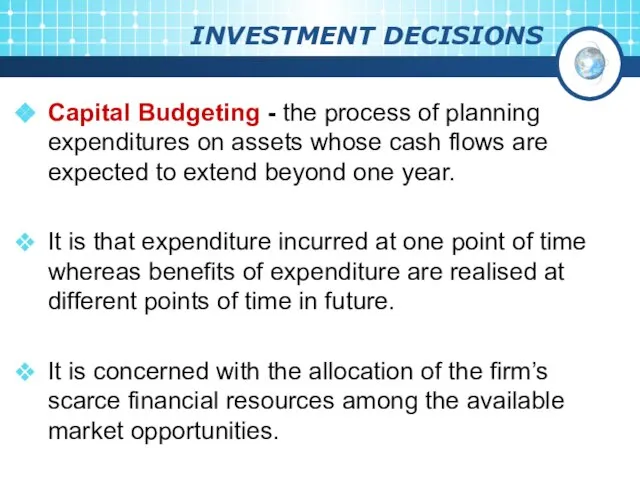

- 45. INVESTMENT DECISIONS Capital Budgeting - the process of planning expenditures on assets whose cash flows are

- 46. DISTINCTION OF CAPITAL BUDGETING DECISIONS Involves the exchange of current funds for the benefits to be

- 47. NATURE OF INVESTMENT DECISIONS Large investments. Long-term commitment of funds. Irreversible in nature. Long-term effect on

- 48. CAPITAL BUDGETING PROCESS Identification on Investment proposals. Screening the proposals. Evaluation of various proposals. Fixing priorities.

- 49. CAPITAL BUDGETING DECISION RULES payback, discounted payback, net present value (NPV), internal rate of return (IRR),

- 50. NET CASH FLOWS FOR PROJECTS S AND L

- 51. PAYBACK PERIOD (PP) Payback Period - the length of time required for an investment’s net revenues

- 52. ADVANTAGES OF PP Simple to understand and easy to calculate. A project with a shorter pay-back

- 53. DISADVANTAGES OF PP It does not take into account the cash inflows earned after the pay-back

- 54. DISCOUNTED PAYBACK PERIOD The length of time required for an investment’s cash flows, discounted at the

- 55. PROBLEMS There are two projects X and Y. Each project requires an investment of Rs. 20,000.

- 56. NET PRESENT VALUE (NPV) METHOD A method of ranking investment proposals using the NPV, which is

- 57. MERITS AND DEMERITS OF NPV Merits: It recognizes the time value of money It takes into

- 58. NPV FORMULA

- 59. RATIONALE FOR THE NPV METHOD An NPV of zero signifies that the project’s cash flows are

- 60. PROBLEMS From the following information, calculate the net present value of the two project and suggest

- 61. INTERNAL RATE OF RETURN (IRR) METHOD A method of ranking investment proposals using the rate of

- 62. IRR FORMULA

- 63. MERITS AND DEMERITS Merits It consider the time value of money. It takes into account the

- 64. ACCEPT/REJECT CRITERIA If the present value of the sum total of the compounded reinvested cash flows

- 65. DIFFERENCES BETWEEN NPV & IRR Size disparity Time disparity Projects with unequal lives Re-investment rate assumption

- 66. PROBLEMS A company has to select one of the following two projects using the Internal Rate

- 67. MODIFIED IRR (MIRR) The discount rate at which the present value of a project’s cost is

- 68. EXAMPLE

- 69. MIRR vs. IRR MIRR assumes that cash flows from all projects are reinvested at the cost

- 70. PROFITABILITY INDEX OR BENEFIT-COST RATIO It is the relationship between present value of cash inflows and

- 71. FINANCING DECISIONS Capital structure refers to the relationship between the various long-term source financing such as

- 72. FACTORS INFLUENCING CAPITAL STRUCTURE Business risk, or the riskiness inherent in the firm’s operations if it

- 73. OPTIMUM CAPITAL STRUCTURE Optimum capital structure is the capital structure at which the weighted average cost

- 74. OBJECTIVES OF CAPITAL STRUCTURE Maximize the value of the firm. Minimize the overall cost of capital.

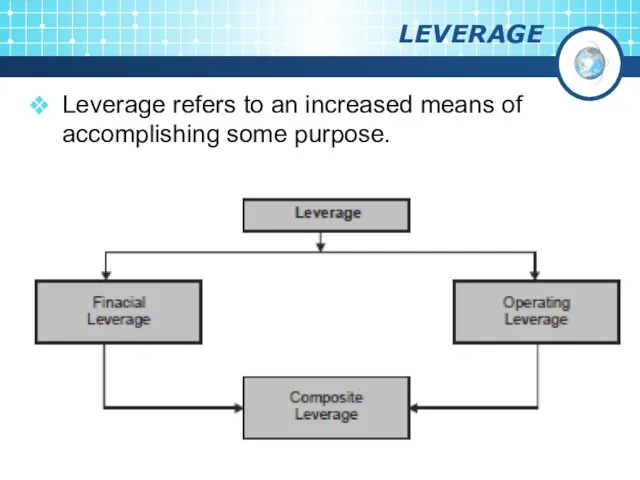

- 75. LEVERAGE Leverage refers to an increased means of accomplishing some purpose.

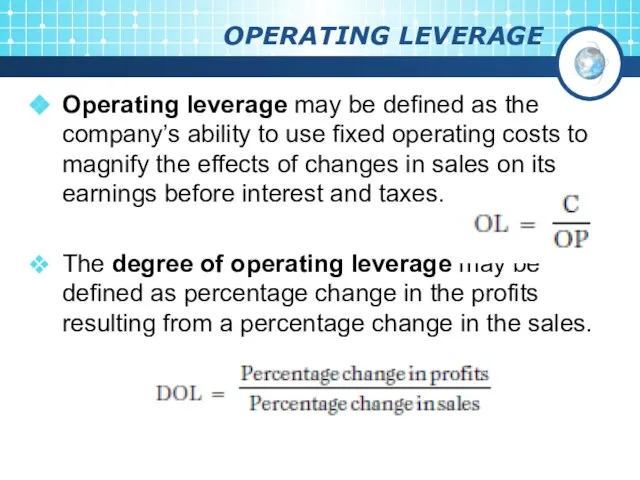

- 76. OPERATING LEVERAGE Operating leverage may be defined as the company’s ability to use fixed operating costs

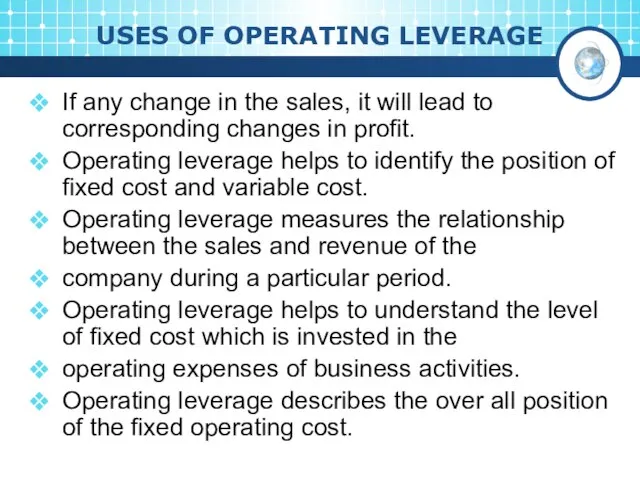

- 77. USES OF OPERATING LEVERAGE If any change in the sales, it will lead to corresponding changes

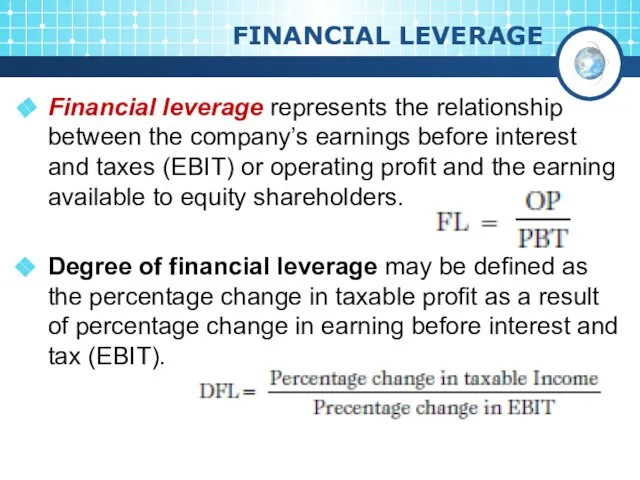

- 78. FINANCIAL LEVERAGE Financial leverage represents the relationship between the company’s earnings before interest and taxes (EBIT)

- 79. USES OF FINANCIAL LEVERAGE Financial leverage helps to examine the relationship between EBIT and EPS. Financial

- 80. DISTINGUISH BETWEEN OPERATING LEVERAGE AND FINANCIAL LEVERAGE

- 81. COMBINED LEVERAGE Combined leverage express the relationship between the revenue in the account of sales and

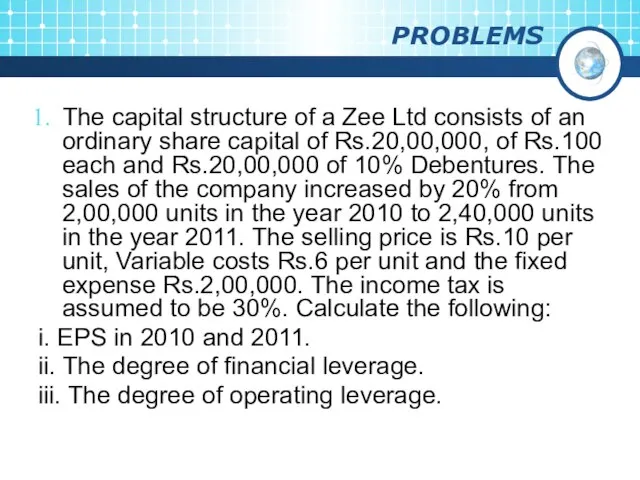

- 82. PROBLEMS The capital structure of a Zee Ltd consists of an ordinary share capital of Rs.20,00,000,

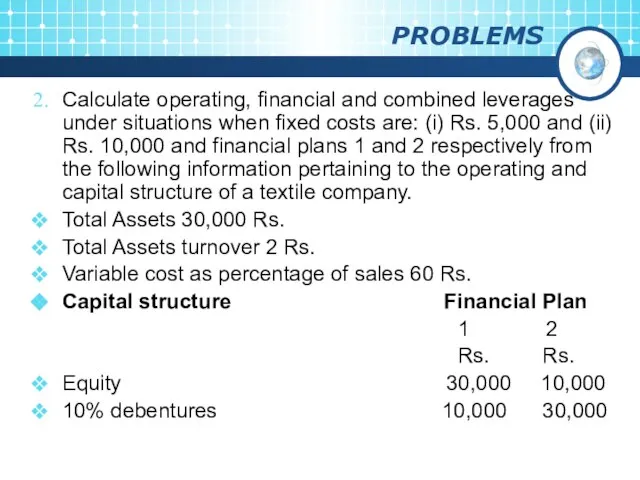

- 83. PROBLEMS Calculate operating, financial and combined leverages under situations when fixed costs are: (i) Rs. 5,000

- 85. Скачать презентацию

Слайд 2INTRODUCTION TO FINANCIAL MANAGEMENT

Nature of Financial Management

1

Objectives of Financial Management

2

Functions of Finance

INTRODUCTION TO FINANCIAL MANAGEMENT

Nature of Financial Management

1

Objectives of Financial Management

2

Functions of Finance

Слайд 3DEFINITION OF FINANCIAL MANAGEMENT

The ways and means of managing money.

Planning, acquisition, allocation,

DEFINITION OF FINANCIAL MANAGEMENT

The ways and means of managing money.

Planning, acquisition, allocation,

Слайд 4NATURE OF FINANCIAL MANAGEMENT

Financial Management is mainly concerned with the proper management

NATURE OF FINANCIAL MANAGEMENT

Financial Management is mainly concerned with the proper management

Слайд 5SCOPE OF FINANCIAL MANAGEMENT

Traditional approach

It is concerned with raising of funds and

SCOPE OF FINANCIAL MANAGEMENT

Traditional approach

It is concerned with raising of funds and

Слайд 6SCOPE OF FINANCIAL MANAGEMENT

Modern approach

To decide how much amount is required from

SCOPE OF FINANCIAL MANAGEMENT

Modern approach

To decide how much amount is required from

Слайд 7OBJECTIVES OF FINANCIAL MANAGEMENT

Financial objectives

Non-financial objectives

OBJECTIVES OF FINANCIAL MANAGEMENT

Financial objectives

Non-financial objectives

Слайд 8FINANCIAL OBJECTIVES

Profit maximization

Wealth maximization

FINANCIAL OBJECTIVES

Profit maximization

Wealth maximization

Слайд 9FINANCIAL OBJECTIVES

Profit:

Profit earning.

Profitability is a barometer for measuring efficiency and economic prosperity

FINANCIAL OBJECTIVES

Profit:

Profit earning.

Profitability is a barometer for measuring efficiency and economic prosperity

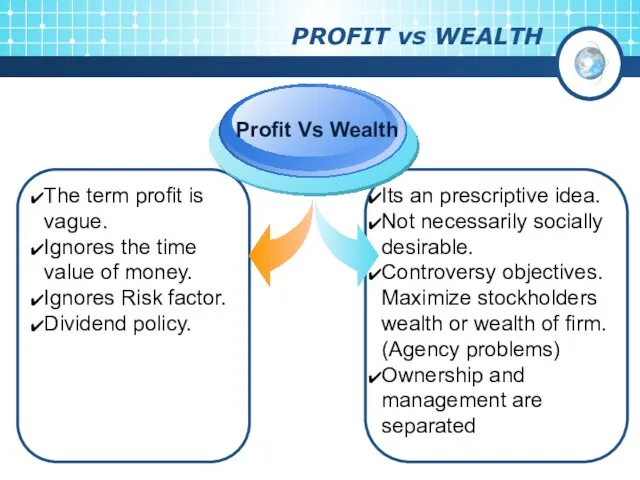

Слайд 10PROFIT vs WEALTH

The term profit is vague.

Ignores the time value of money.

Ignores

PROFIT vs WEALTH

The term profit is vague.

Ignores the time value of money.

Ignores

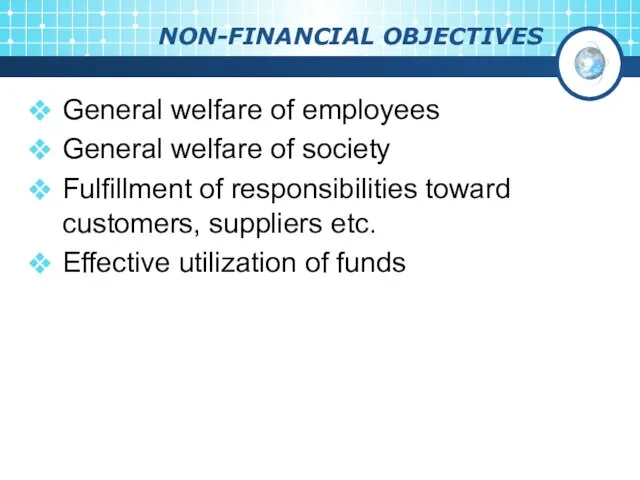

Слайд 11NON-FINANCIAL OBJECTIVES

General welfare of employees

General welfare of society

Fulfillment of responsibilities toward customers,

NON-FINANCIAL OBJECTIVES

General welfare of employees

General welfare of society

Fulfillment of responsibilities toward customers,

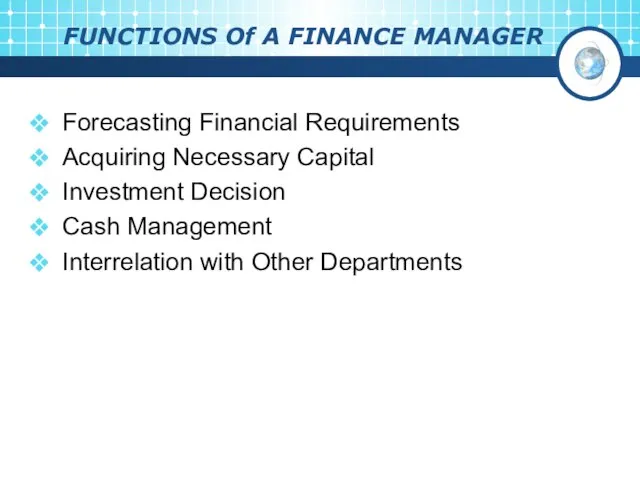

Слайд 12FUNCTIONS Of A FINANCE MANAGER

Forecasting Financial Requirements

Acquiring Necessary Capital

Investment Decision

Cash Management

Interrelation with

FUNCTIONS Of A FINANCE MANAGER

Forecasting Financial Requirements

Acquiring Necessary Capital

Investment Decision

Cash Management

Interrelation with

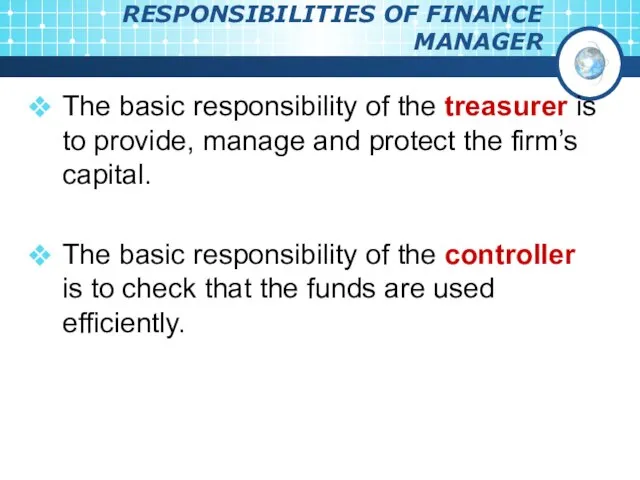

Слайд 13RESPONSIBILITIES OF FINANCE MANAGER

The basic responsibility of the treasurer is to provide,

RESPONSIBILITIES OF FINANCE MANAGER

The basic responsibility of the treasurer is to provide,

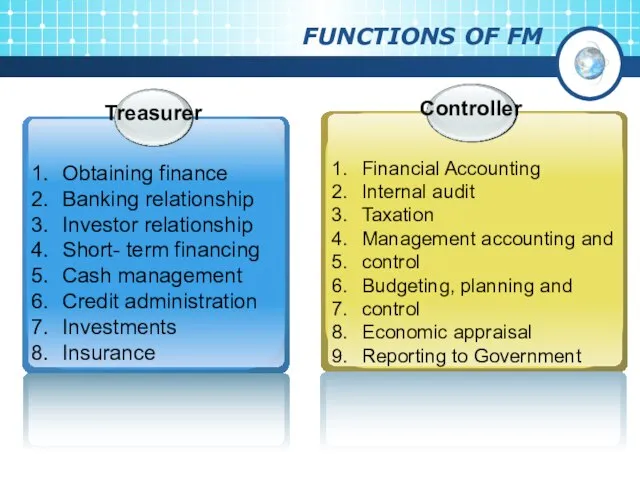

Слайд 14FUNCTIONS OF FM

FUNCTIONS OF FM

Слайд 15FINANCIAL MANAGEMENT PROCESS

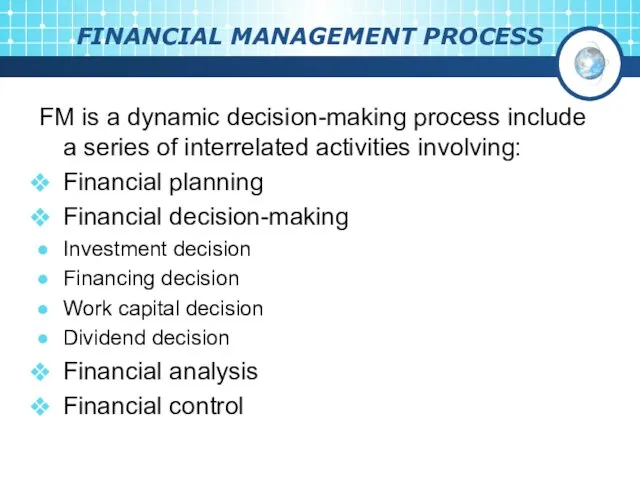

FM is a dynamic decision-making process include a series of

FINANCIAL MANAGEMENT PROCESS

FM is a dynamic decision-making process include a series of

Слайд 16FINANCIAL MANAGEMENT INSTRUMENTS

Time value analysis

1

Cost of Capital

2

Investment Decisions

3

FINANCIAL MANAGEMENT INSTRUMENTS

Time value analysis

1

Cost of Capital

2

Investment Decisions

3

Слайд 17CONCEPT OF TIME VALUE OF

MONEY

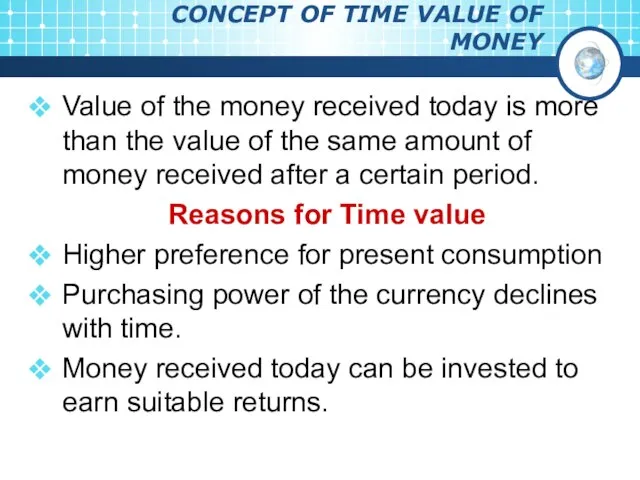

Value of the money received today is

CONCEPT OF TIME VALUE OF

MONEY

Value of the money received today is

Слайд 18REASONS FOR TIME PREFERENCE OF MONEY

The future is always uncertain and

REASONS FOR TIME PREFERENCE OF MONEY

The future is always uncertain and

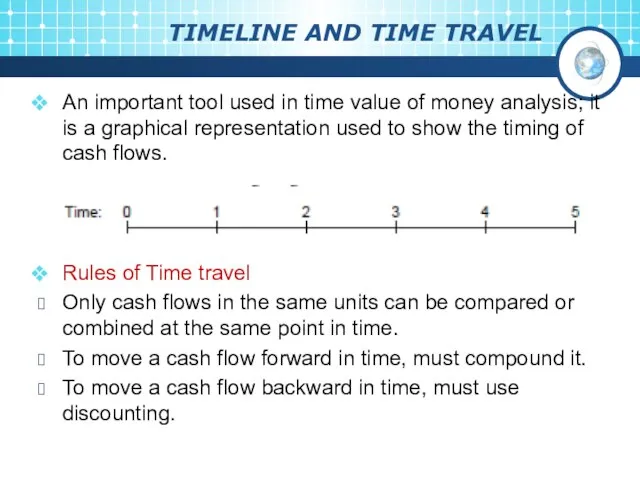

Слайд 19TIMELINE AND TIME TRAVEL

An important tool used in time value of money

TIMELINE AND TIME TRAVEL

An important tool used in time value of money

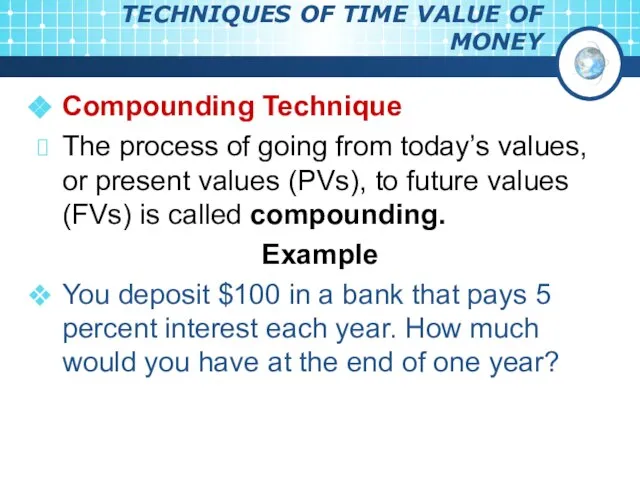

Слайд 20TECHNIQUES OF TIME VALUE OF MONEY

Compounding Technique

The process of going from today’s

TECHNIQUES OF TIME VALUE OF MONEY

Compounding Technique

The process of going from today’s

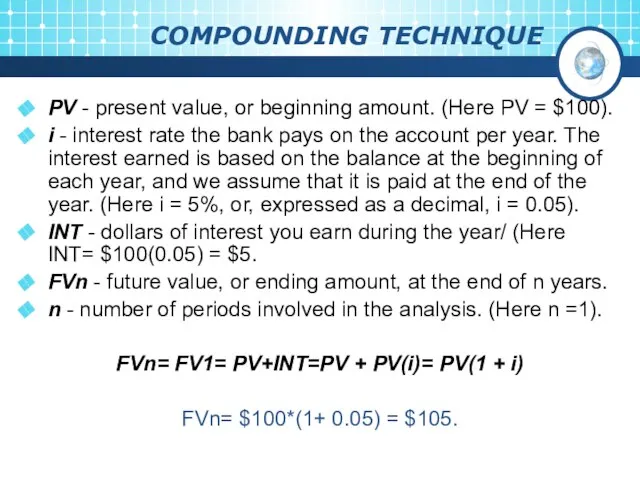

Слайд 21COMPOUNDING TECHNIQUE

PV - present value, or beginning amount. (Here PV = $100).

i

COMPOUNDING TECHNIQUE

PV - present value, or beginning amount. (Here PV = $100).

i

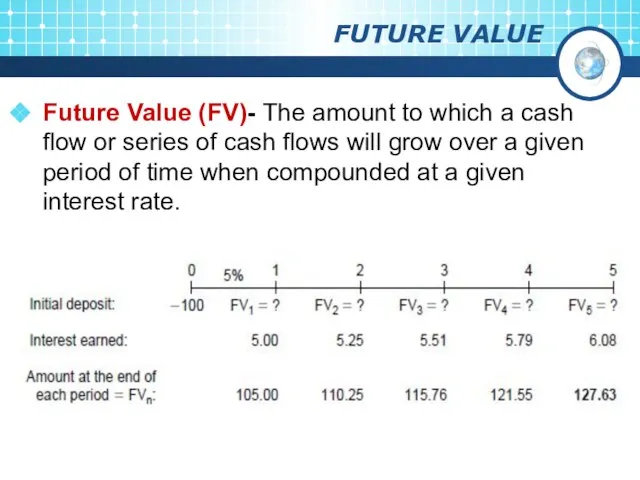

Слайд 22FUTURE VALUE

Future Value (FV)- The amount to which a cash flow or

FUTURE VALUE

Future Value (FV)- The amount to which a cash flow or

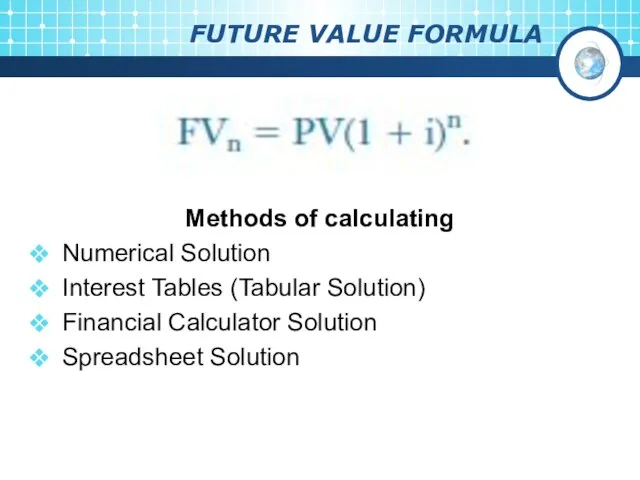

Слайд 23FUTURE VALUE FORMULA

Methods of calculating

Numerical Solution

Interest Tables (Tabular Solution)

Financial Calculator Solution

Spreadsheet Solution

FUTURE VALUE FORMULA

Methods of calculating

Numerical Solution

Interest Tables (Tabular Solution)

Financial Calculator Solution

Spreadsheet Solution

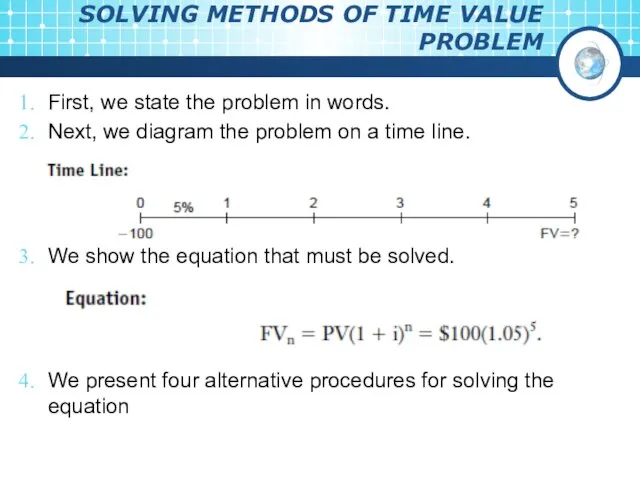

Слайд 24SOLVING METHODS OF TIME VALUE PROBLEM

First, we state the problem in words.

SOLVING METHODS OF TIME VALUE PROBLEM

First, we state the problem in words.

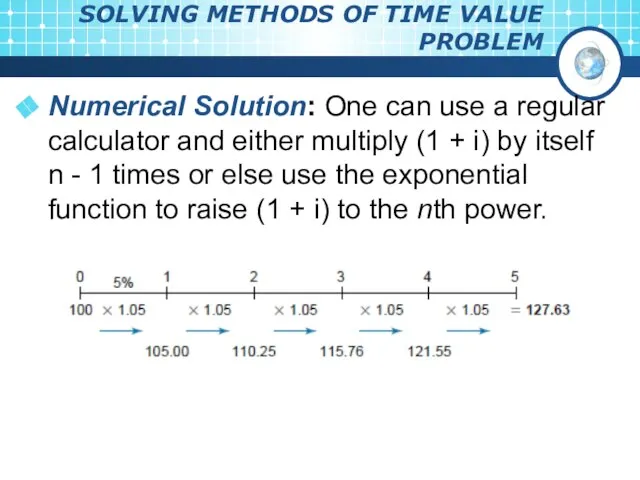

Слайд 25SOLVING METHODS OF TIME VALUE PROBLEM

Numerical Solution: One can use a regular

SOLVING METHODS OF TIME VALUE PROBLEM

Numerical Solution: One can use a regular

Слайд 26SOLVING METHODS OF TIME VALUE PROBLEM

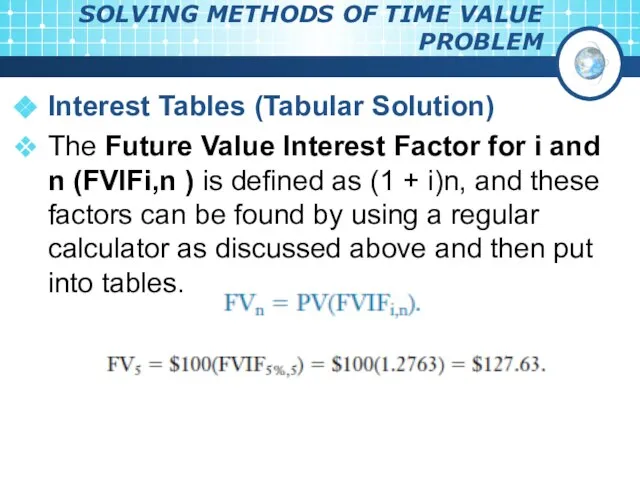

Interest Tables (Tabular Solution)

The Future Value Interest

SOLVING METHODS OF TIME VALUE PROBLEM

Interest Tables (Tabular Solution)

The Future Value Interest

Слайд 27SOLVING METHODS OF TIME VALUE PROBLEM

Financial Calculator Solution: Equation and a number

SOLVING METHODS OF TIME VALUE PROBLEM

Financial Calculator Solution: Equation and a number

Слайд 28SOLVING METHODS OF TIME VALUE PROBLEM

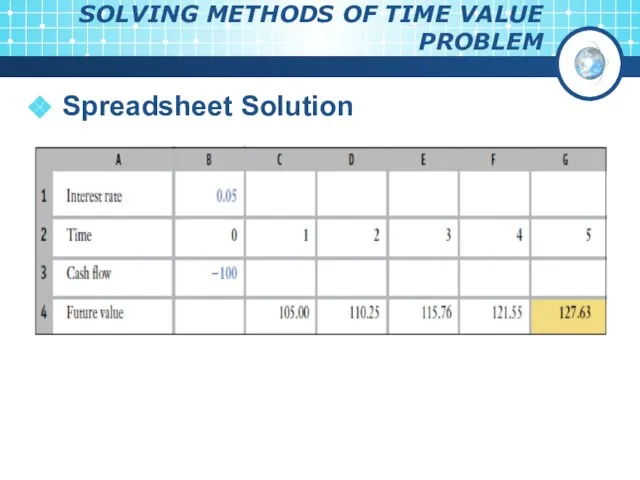

Spreadsheet Solution

SOLVING METHODS OF TIME VALUE PROBLEM

Spreadsheet Solution

Слайд 29MULTI PERIOD COMPOUNDING

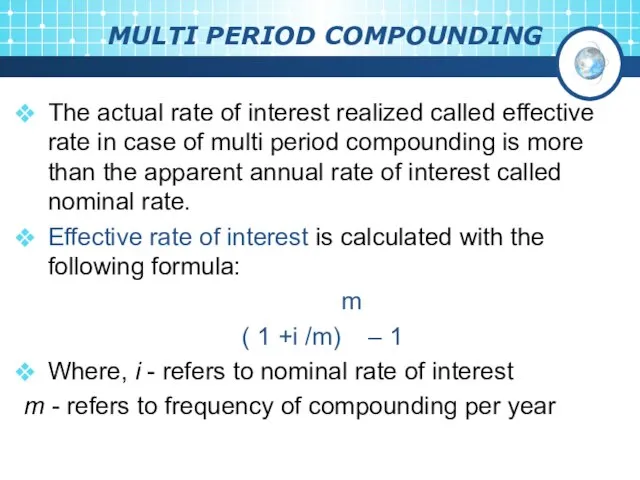

The actual rate of interest realized called effective rate in

MULTI PERIOD COMPOUNDING

The actual rate of interest realized called effective rate in

Слайд 30COMPOUNDED (FUTURE) VALUE OF ANNUITY

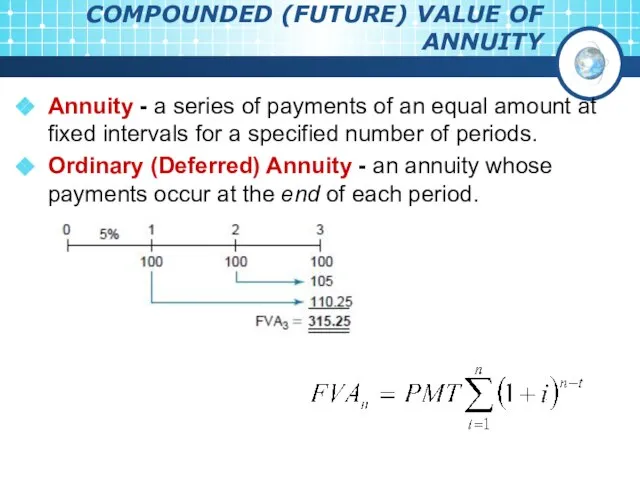

Annuity - a series of payments of an

COMPOUNDED (FUTURE) VALUE OF ANNUITY

Annuity - a series of payments of an

Слайд 31COMPOUNDED (FUTURE) VALUE OF ANNUITY

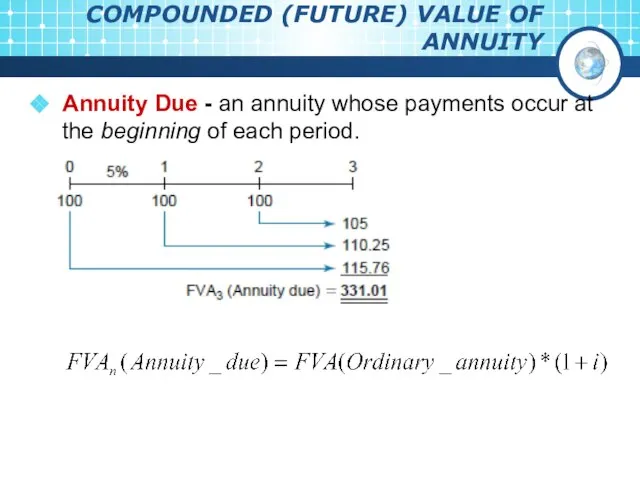

Annuity Due - an annuity whose payments occur

COMPOUNDED (FUTURE) VALUE OF ANNUITY

Annuity Due - an annuity whose payments occur

Слайд 32PROBLEMS

What will be the value of Rs.100 after two years at 10%

PROBLEMS

What will be the value of Rs.100 after two years at 10%

Слайд 33PROBLEMS

Mr. Adams deposits Rs.1000 at the end of every year for four

PROBLEMS

Mr. Adams deposits Rs.1000 at the end of every year for four

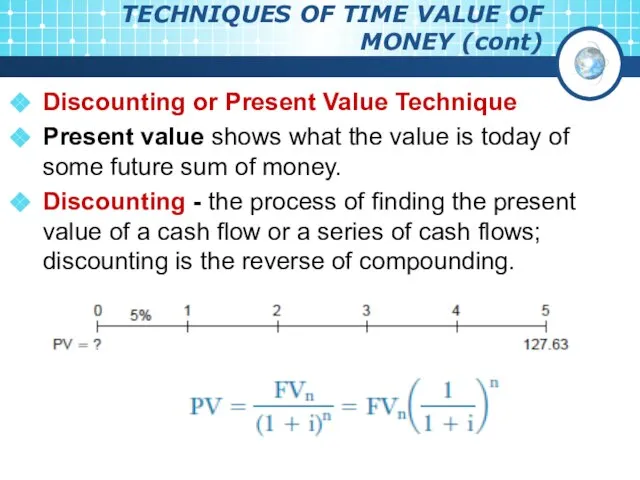

Слайд 34TECHNIQUES OF TIME VALUE OF MONEY (cont)

Discounting or Present Value Technique

Present value

TECHNIQUES OF TIME VALUE OF MONEY (cont)

Discounting or Present Value Technique

Present value

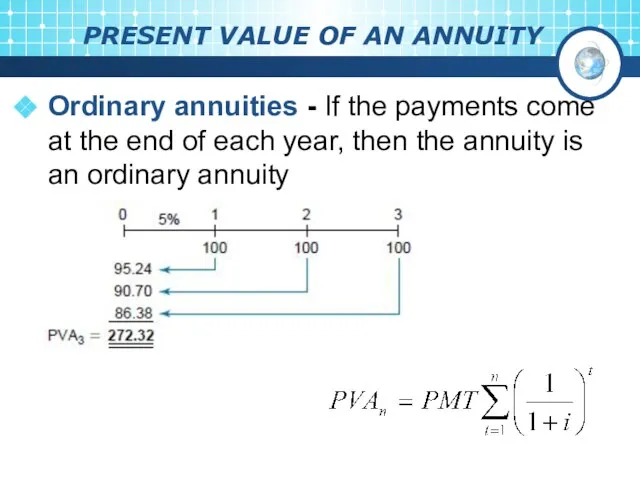

Слайд 35PRESENT VALUE OF AN ANNUITY

Ordinary annuities - If the payments come at

PRESENT VALUE OF AN ANNUITY

Ordinary annuities - If the payments come at

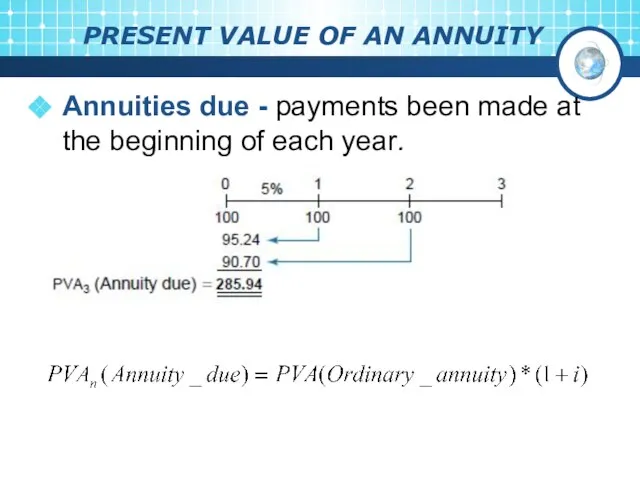

Слайд 36PRESENT VALUE OF AN ANNUITY

Annuities due - payments been made at the

PRESENT VALUE OF AN ANNUITY

Annuities due - payments been made at the

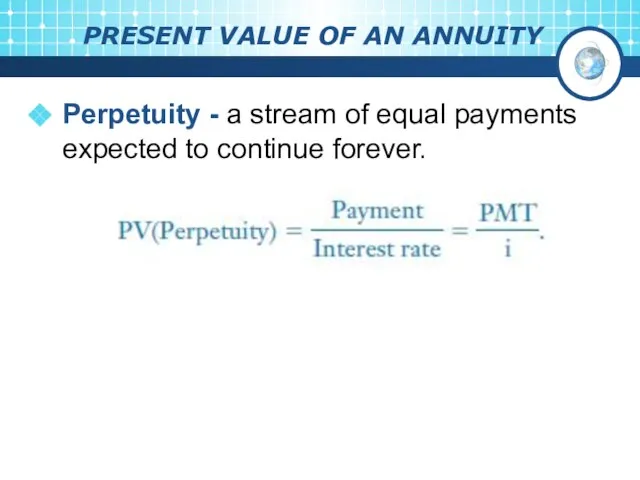

Слайд 37PRESENT VALUE OF AN ANNUITY

Perpetuity - a stream of equal payments expected

PRESENT VALUE OF AN ANNUITY

Perpetuity - a stream of equal payments expected

Слайд 38PROBLEMS

Calculate the present value of Rs.1000 to be received after one year

PROBLEMS

Calculate the present value of Rs.1000 to be received after one year

Слайд 39PROBLEMS

Mr. X has to receive Rs.2000 per year for five years. Calculate

PROBLEMS

Mr. X has to receive Rs.2000 per year for five years. Calculate

Слайд 40UNEVEN CASH FLOW STREAMS

Uneven Cash Flow Stream - a series of cash

UNEVEN CASH FLOW STREAMS

Uneven Cash Flow Stream - a series of cash

Слайд 41PRESENT VALUE OF AN UNEVEN CASH FLOW STREAM

PRESENT VALUE OF AN UNEVEN CASH FLOW STREAM

Слайд 42FUTURE VALUE OF AN UNEVEN CASH FLOW STREAM

The future value of an

FUTURE VALUE OF AN UNEVEN CASH FLOW STREAM

The future value of an

Слайд 43FUTURE VALUE OF AN UNEVEN CASH FLOW STREAM

FUTURE VALUE OF AN UNEVEN CASH FLOW STREAM

Слайд 44PROBLEMS

Calculate present value of the following five years cash flows assuming a

PROBLEMS

Calculate present value of the following five years cash flows assuming a

Слайд 45INVESTMENT DECISIONS

Capital Budgeting - the process of planning expenditures on assets whose

INVESTMENT DECISIONS

Capital Budgeting - the process of planning expenditures on assets whose

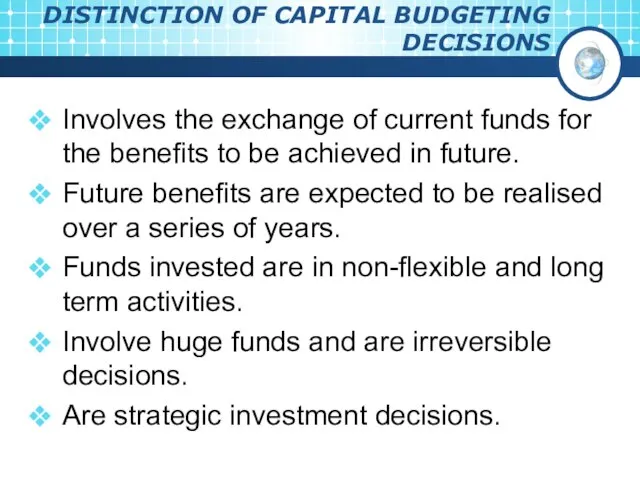

Слайд 46DISTINCTION OF CAPITAL BUDGETING DECISIONS

Involves the exchange of current funds for the

DISTINCTION OF CAPITAL BUDGETING DECISIONS

Involves the exchange of current funds for the

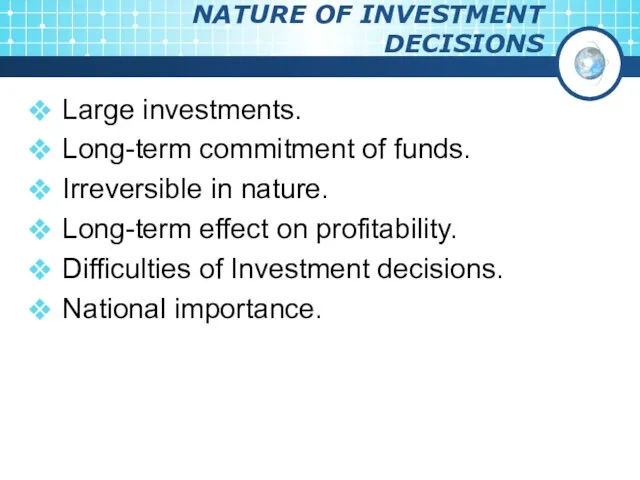

Слайд 47NATURE OF INVESTMENT DECISIONS

Large investments.

Long-term commitment of funds.

Irreversible in nature.

Long-term effect on

NATURE OF INVESTMENT DECISIONS

Large investments.

Long-term commitment of funds.

Irreversible in nature.

Long-term effect on

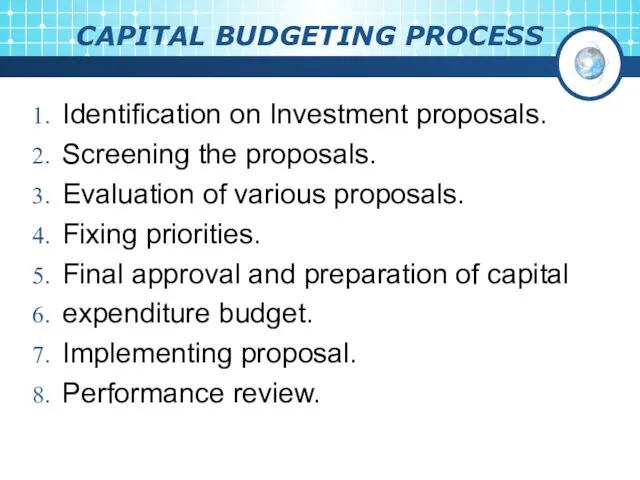

Слайд 48CAPITAL BUDGETING PROCESS

Identification on Investment proposals.

Screening the proposals.

Evaluation of various proposals.

Fixing priorities.

Final

CAPITAL BUDGETING PROCESS

Identification on Investment proposals.

Screening the proposals.

Evaluation of various proposals.

Fixing priorities.

Final

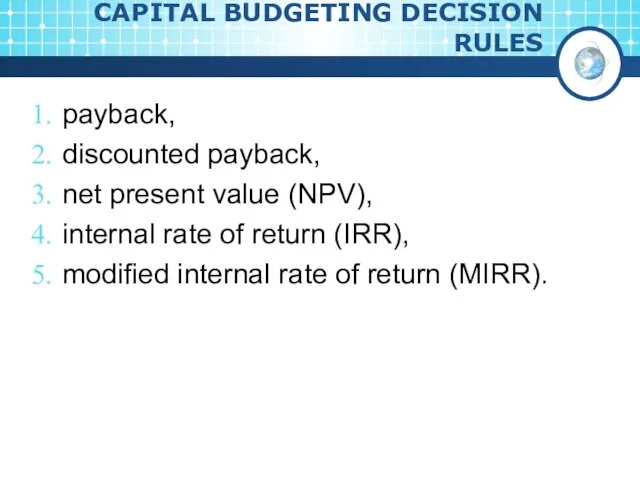

Слайд 49CAPITAL BUDGETING DECISION RULES

payback,

discounted payback,

net present value (NPV),

internal rate

CAPITAL BUDGETING DECISION RULES

payback,

discounted payback,

net present value (NPV),

internal rate

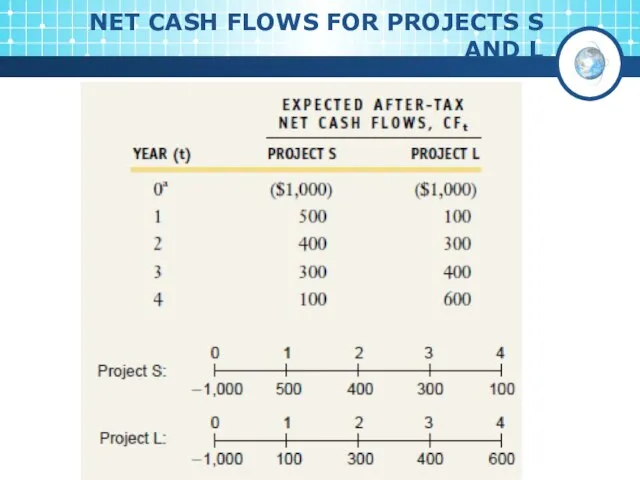

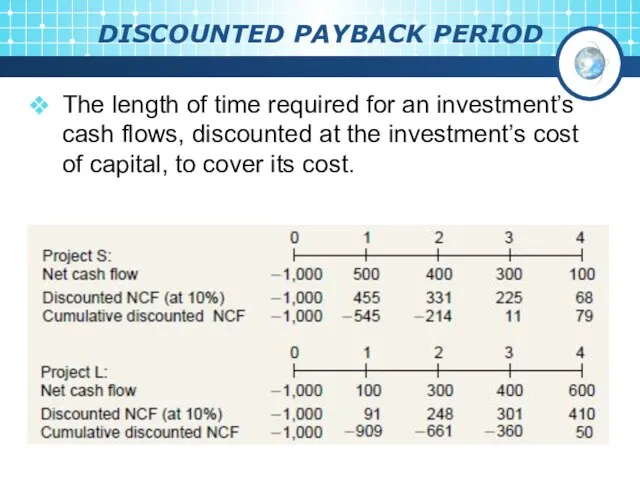

Слайд 50NET CASH FLOWS FOR PROJECTS S AND L

NET CASH FLOWS FOR PROJECTS S AND L

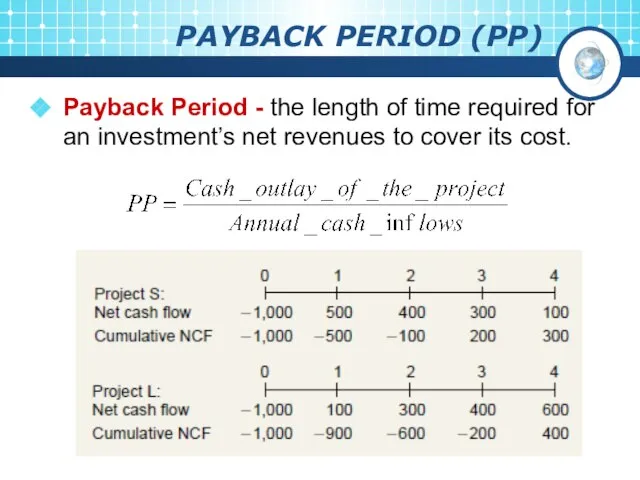

Слайд 51PAYBACK PERIOD (PP)

Payback Period - the length of time required for an

PAYBACK PERIOD (PP)

Payback Period - the length of time required for an

Слайд 52ADVANTAGES OF PP

Simple to understand and easy to calculate.

A project with a

ADVANTAGES OF PP

Simple to understand and easy to calculate.

A project with a

Слайд 53DISADVANTAGES OF PP

It does not take into account the cash inflows earned

DISADVANTAGES OF PP

It does not take into account the cash inflows earned

Слайд 54DISCOUNTED PAYBACK PERIOD

The length of time required for an investment’s cash flows,

DISCOUNTED PAYBACK PERIOD

The length of time required for an investment’s cash flows,

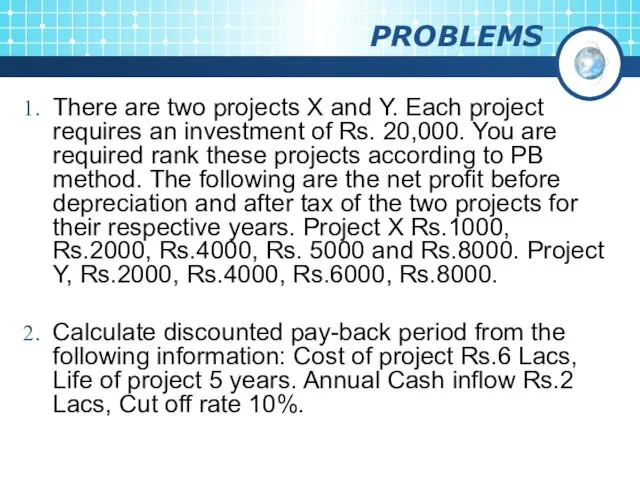

Слайд 55PROBLEMS

There are two projects X and Y. Each project requires an investment

PROBLEMS

There are two projects X and Y. Each project requires an investment

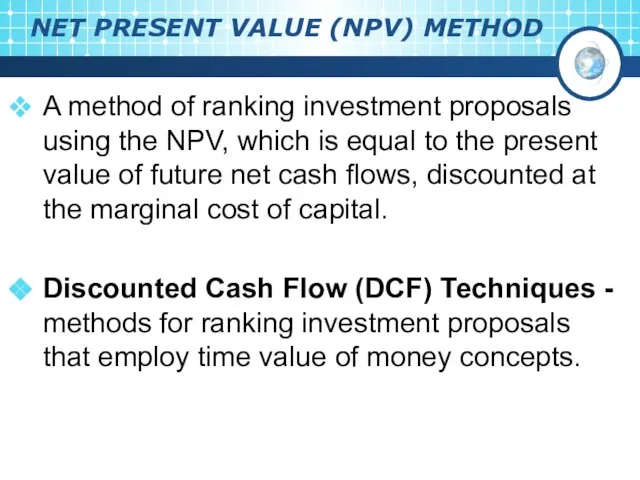

Слайд 56NET PRESENT VALUE (NPV) METHOD

A method of ranking investment proposals using the

NET PRESENT VALUE (NPV) METHOD

A method of ranking investment proposals using the

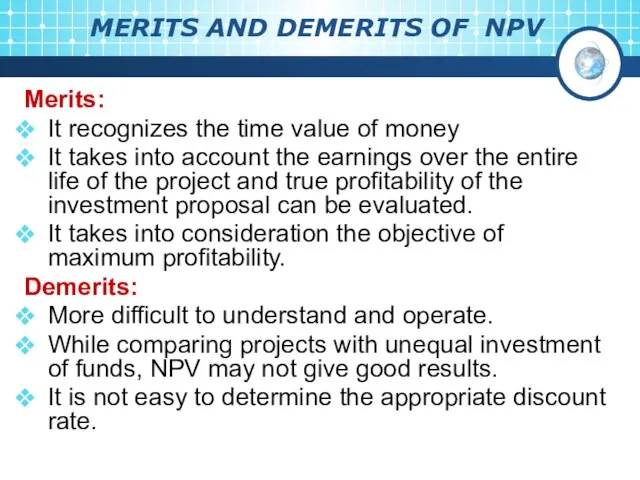

Слайд 57MERITS AND DEMERITS OF NPV

Merits:

It recognizes the time value of money

It takes

MERITS AND DEMERITS OF NPV

Merits:

It recognizes the time value of money

It takes

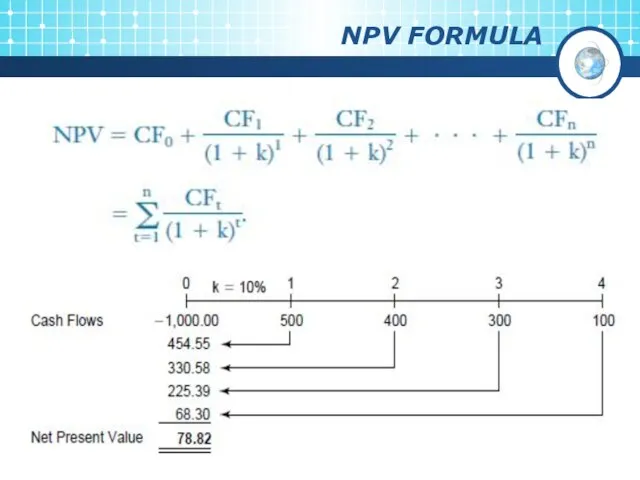

Слайд 58NPV FORMULA

NPV FORMULA

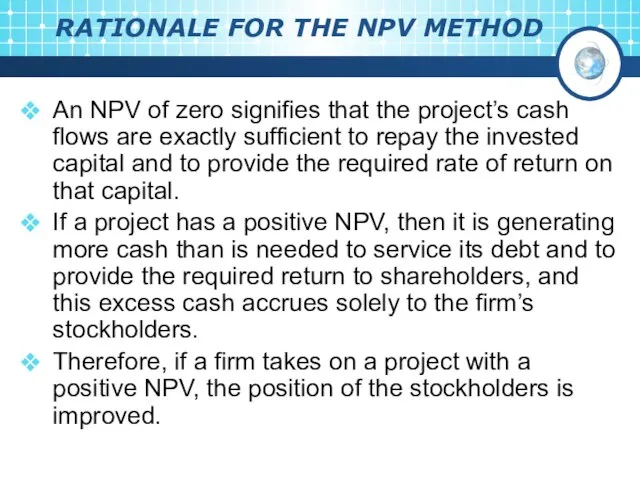

Слайд 59RATIONALE FOR THE NPV METHOD

An NPV of zero signifies that the project’s

RATIONALE FOR THE NPV METHOD

An NPV of zero signifies that the project’s

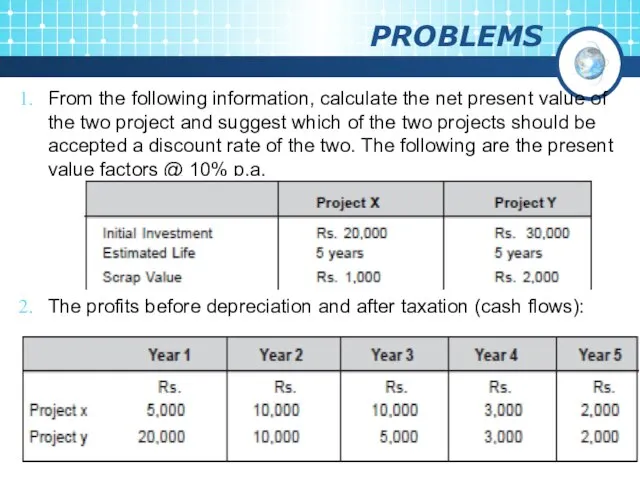

Слайд 60PROBLEMS

From the following information, calculate the net present value of the two

PROBLEMS

From the following information, calculate the net present value of the two

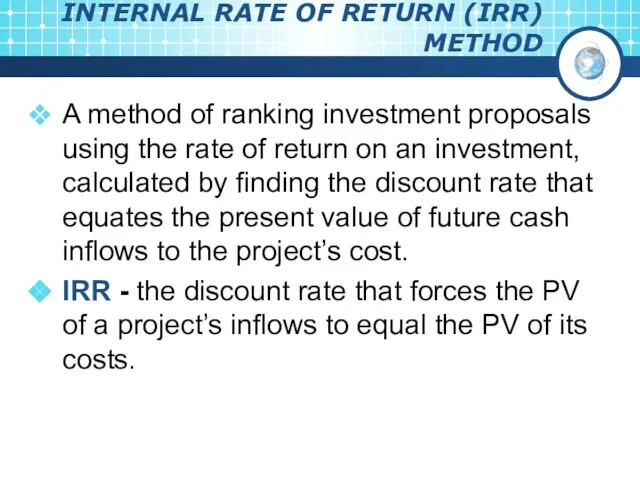

Слайд 61INTERNAL RATE OF RETURN (IRR) METHOD

A method of ranking investment proposals using

INTERNAL RATE OF RETURN (IRR) METHOD

A method of ranking investment proposals using

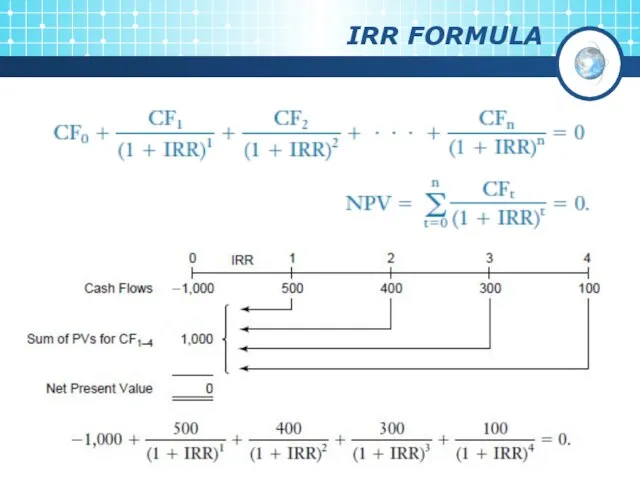

Слайд 62IRR FORMULA

IRR FORMULA

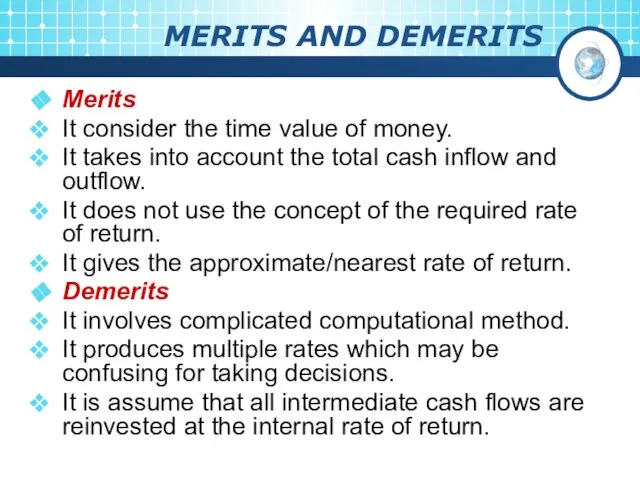

Слайд 63MERITS AND DEMERITS

Merits

It consider the time value of money.

It takes into account

MERITS AND DEMERITS

Merits

It consider the time value of money.

It takes into account

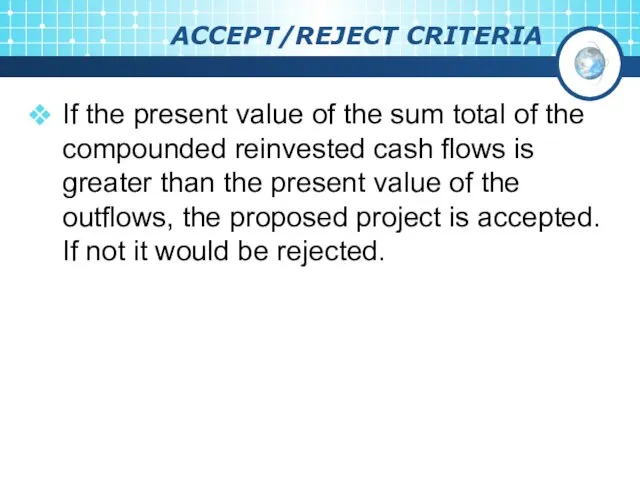

Слайд 64ACCEPT/REJECT CRITERIA

If the present value of the sum total of the compounded

ACCEPT/REJECT CRITERIA

If the present value of the sum total of the compounded

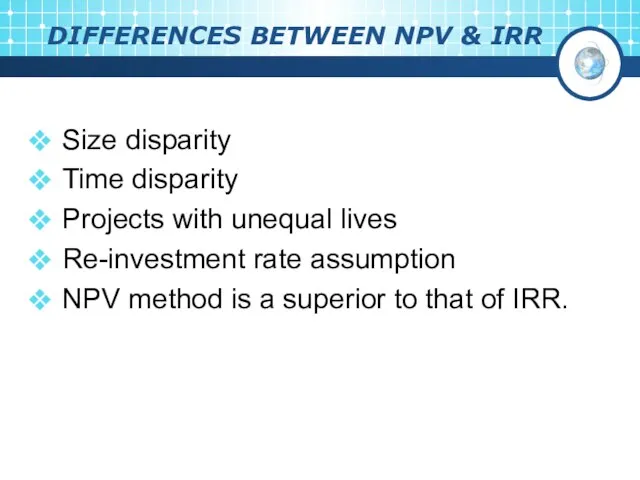

Слайд 65DIFFERENCES BETWEEN NPV & IRR

Size disparity

Time disparity

Projects with unequal lives

Re-investment rate assumption

NPV

DIFFERENCES BETWEEN NPV & IRR

Size disparity

Time disparity

Projects with unequal lives

Re-investment rate assumption

NPV

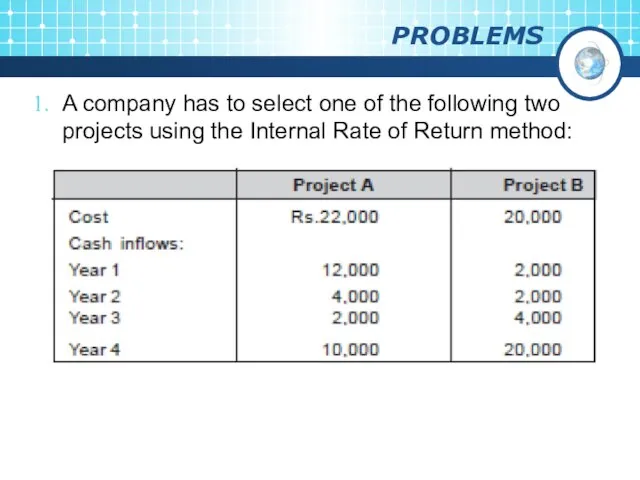

Слайд 66PROBLEMS

A company has to select one of the following two projects using

PROBLEMS

A company has to select one of the following two projects using

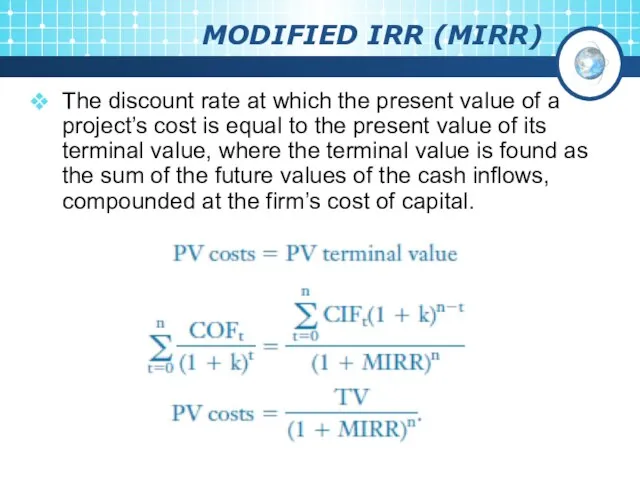

Слайд 67MODIFIED IRR (MIRR)

The discount rate at which the present value of a

MODIFIED IRR (MIRR)

The discount rate at which the present value of a

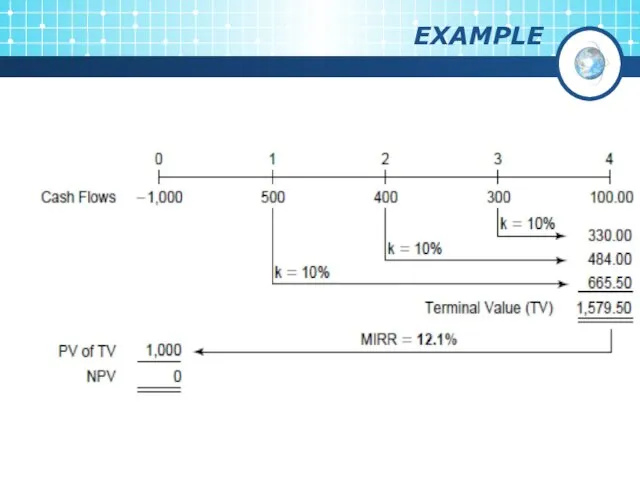

Слайд 68EXAMPLE

EXAMPLE

Слайд 69MIRR vs. IRR

MIRR assumes that cash flows from all projects are reinvested

MIRR vs. IRR

MIRR assumes that cash flows from all projects are reinvested

Слайд 70PROFITABILITY INDEX OR BENEFIT-COST RATIO

It is the relationship between present value of

PROFITABILITY INDEX OR BENEFIT-COST RATIO

It is the relationship between present value of

Слайд 71FINANCING DECISIONS

Capital structure refers to the relationship between the various long-term source

FINANCING DECISIONS

Capital structure refers to the relationship between the various long-term source

Слайд 72FACTORS INFLUENCING CAPITAL STRUCTURE

Business risk, or the riskiness inherent in the firm’s

FACTORS INFLUENCING CAPITAL STRUCTURE

Business risk, or the riskiness inherent in the firm’s

Слайд 73OPTIMUM CAPITAL STRUCTURE

Optimum capital structure is the capital structure at which the

OPTIMUM CAPITAL STRUCTURE

Optimum capital structure is the capital structure at which the

Слайд 74OBJECTIVES OF CAPITAL STRUCTURE

Maximize the value of the firm.

Minimize the overall cost

OBJECTIVES OF CAPITAL STRUCTURE

Maximize the value of the firm.

Minimize the overall cost

Слайд 75LEVERAGE

Leverage refers to an increased means of accomplishing some purpose.

LEVERAGE

Leverage refers to an increased means of accomplishing some purpose.

Слайд 76OPERATING LEVERAGE

Operating leverage may be defined as the company’s ability to use

OPERATING LEVERAGE

Operating leverage may be defined as the company’s ability to use

Слайд 77USES OF OPERATING LEVERAGE

If any change in the sales, it will lead

USES OF OPERATING LEVERAGE

If any change in the sales, it will lead

Слайд 78FINANCIAL LEVERAGE

Financial leverage represents the relationship between the company’s earnings before interest

FINANCIAL LEVERAGE

Financial leverage represents the relationship between the company’s earnings before interest

Слайд 79USES OF FINANCIAL LEVERAGE

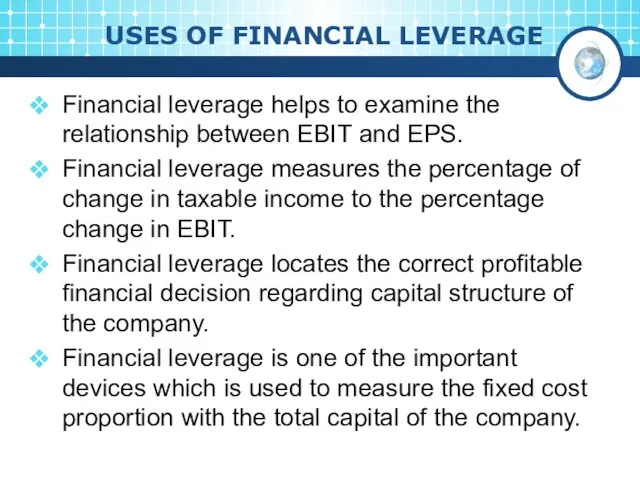

Financial leverage helps to examine the relationship between EBIT

USES OF FINANCIAL LEVERAGE

Financial leverage helps to examine the relationship between EBIT

Слайд 80DISTINGUISH BETWEEN OPERATING LEVERAGE AND FINANCIAL LEVERAGE

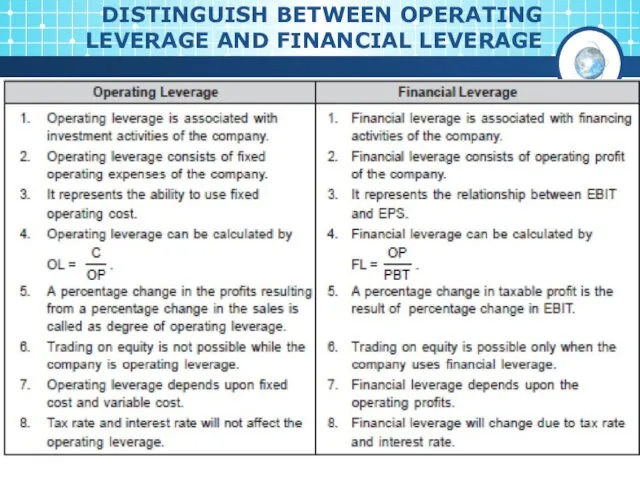

DISTINGUISH BETWEEN OPERATING LEVERAGE AND FINANCIAL LEVERAGE

Слайд 81COMBINED LEVERAGE

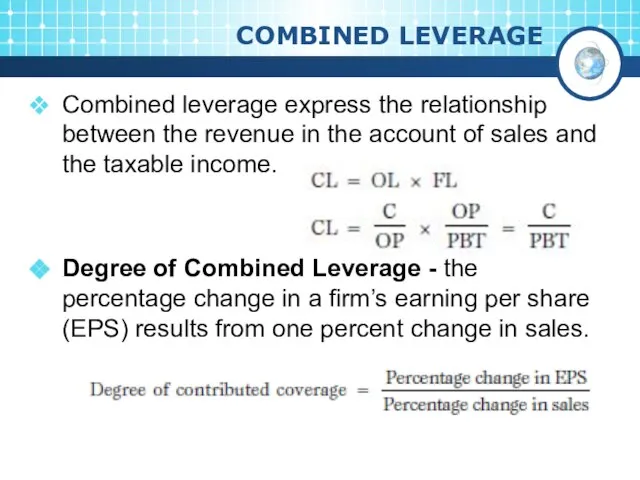

Combined leverage express the relationship between the revenue in the account

COMBINED LEVERAGE

Combined leverage express the relationship between the revenue in the account

Слайд 82PROBLEMS

The capital structure of a Zee Ltd consists of an ordinary share

PROBLEMS

The capital structure of a Zee Ltd consists of an ordinary share

Слайд 83PROBLEMS

Calculate operating, financial and combined leverages under situations when fixed costs are:

PROBLEMS

Calculate operating, financial and combined leverages under situations when fixed costs are:

Clever

Clever Праздничные народные гулянья. Урок изобразительного искусства. 5 класс

Праздничные народные гулянья. Урок изобразительного искусства. 5 класс Тöс ле эчеҥи члендер

Тöс ле эчеҥи члендер ЕГЭ 2010 задачи С1-С6

ЕГЭ 2010 задачи С1-С6 Справка о МТО

Справка о МТО Учебно-методическое обеспечение современного образования подростков

Учебно-методическое обеспечение современного образования подростков Размещение бытового газоборудования в квартирах

Размещение бытового газоборудования в квартирах Нормы, закрепленные в статьях 163,165,166 УК РФ

Нормы, закрепленные в статьях 163,165,166 УК РФ Геометрическая оптика

Геометрическая оптика CashFlow

CashFlow ВРЕМЕННОЕ ПЛОМБИРОВАНИЕ КОРНЕВЫХ КАНАЛОВ

ВРЕМЕННОЕ ПЛОМБИРОВАНИЕ КОРНЕВЫХ КАНАЛОВ Экваториальные леса Южной Америки

Экваториальные леса Южной Америки Презентация на тему Формула здоровья

Презентация на тему Формула здоровья  Неомодерн в архитектуре Ростова

Неомодерн в архитектуре Ростова Производительность МП и ее тестирование

Производительность МП и ее тестирование Внешность человека

Внешность человека Золотое содержание в национальной валюте. Финансы и кредит

Золотое содержание в национальной валюте. Финансы и кредит Сервис Взаимозачет

Сервис Взаимозачет Логарифмическая функция

Логарифмическая функция  Оценка и анализ финансовых рисков

Оценка и анализ финансовых рисков Договор транспортной экспедиции

Договор транспортной экспедиции Бюджетное учреждение здравоохранения Омской Области «Таврическая центральная районная больница»

Бюджетное учреждение здравоохранения Омской Области «Таврическая центральная районная больница» Развитие образа Снегурочки в искусстве

Развитие образа Снегурочки в искусстве Архитектура Серебряного века России

Архитектура Серебряного века России Презентация на тему Рождество в Великобритании

Презентация на тему Рождество в Великобритании  Решение уравнения в 1 классе

Решение уравнения в 1 классе Презентация на тему Русский язык среди других славянских языков

Презентация на тему Русский язык среди других славянских языков Умей бороться честно. Что такое допинг

Умей бороться честно. Что такое допинг