- Financial Markets

Содержание

- 2. Financial Markets On the evening news you have heard that the bond market or stock market

- 3. Financial markets Channels funds from savers to investors, thereby promoting economic efficiency. Affects personal wealth and

- 4. Financial markets The stock market is the market where stock, representing ownership in a company, are

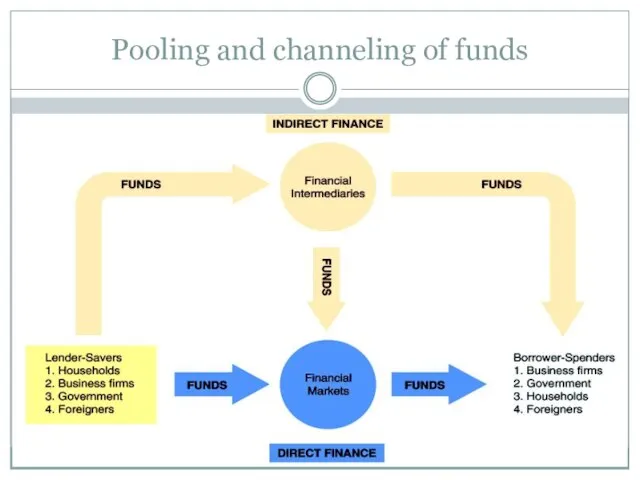

- 5. Pooling and channeling of funds Copyright © 2003 Pearson Education, Inc.

- 6. Structure of Financial Markets Even though firms don’t get any money, per se, from the secondary

- 7. Structure of Financial Markets We can further classify secondary markets as follows: Exchanges Trades conducted in

- 8. Interest rates We develop a better understanding of interest rates. We examine the terminology and calculation

- 9. Maturity and the Volatility of Bond Returns Only bond whose return is equals the yield to

- 10. Reinvestment Risk Occurs if an investor’s holding period is longer than the term to maturity of

- 11. Calculating Duration i = 20%, 10-Year 10% Coupon Bond

- 12. Formula for Duration Key facts about duration All else equal, when the maturity of a bond

- 13. Why interest rates change? Determinants of asset demand Wealth – total resources owned Expected returns –

- 14. Expected returns Is the return expected over the next period on one asset relative to alternative

- 15. Risk The degree of uncertainty associated with the return on one asset relative to alternative assets

- 16. Changes in Equilibrium Interest Rates Shifts in the Supply of Bonds Expected profitability of investment opportunities:

- 17. How do risk and term structure affect interest rates? Risk structure of interest rates Interest rates

- 18. Default Risk A bond with default risk will always have a positive risk premium, and an

- 19. Term structure of interest rates Bonds with identical risk, liquidity, and tax characteristics may have different

- 20. Expectations theory Proposition: the interest rate on long-term bond will equal an average of short-term interest

- 22. Efficient Market Hypothesis The Efficient Market Hypothesis Stronger Version of Efficient Market Hypothesis Evidence on the

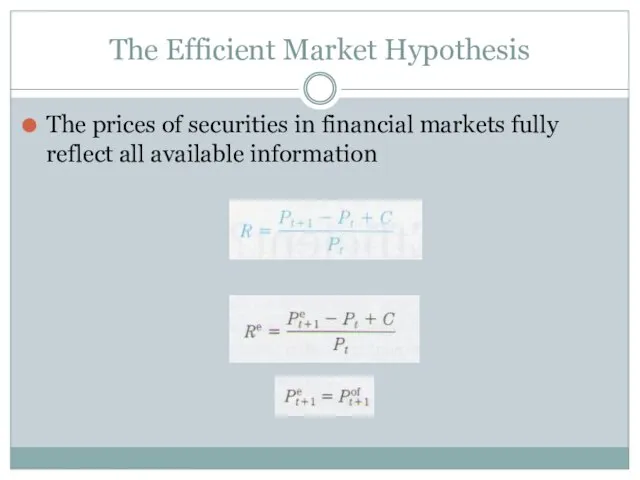

- 23. The Efficient Market Hypothesis The prices of securities in financial markets fully reflect all available information

- 24. Current prices in a financial market will be set so that the optimal forecast of a

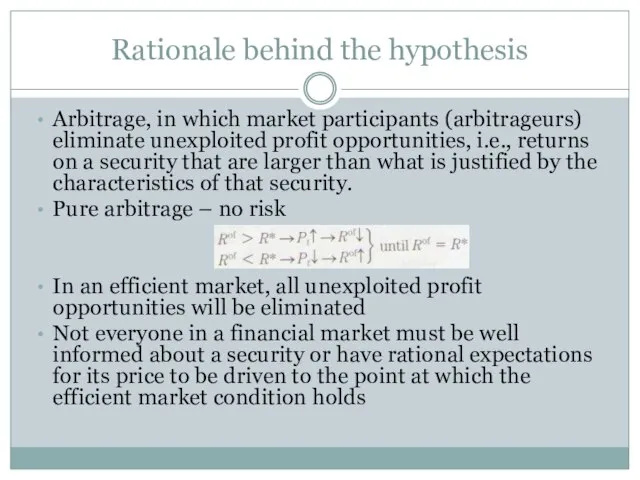

- 25. Rationale behind the hypothesis Arbitrage, in which market participants (arbitrageurs) eliminate unexploited profit opportunities, i.e., returns

- 26. Dynamics of crises Stage one (initiation) Financial liberalization (credit boom) Asset price boom and bust Spikes

- 27. Top 10 causes of crisis Credit bubble (developing countries building up large capital surpluses (post-Asia crisis)

- 28. Causes contd. Leverage and liquidity risk – too little capital to offset higher risk – reliance

- 29. Post-crisis regulation Oversight and supervision of financial institutions (Special Council to monitor systemic risks (leverage, liquidity

- 30. Why do we need Central Banks? Prevent banking crisis Stability of financial sector Ensuring deposits Providing

- 31. Goals of Monetary Policy 6 Goals Inflation targeting High employment Economic growth Stability of financial markets

- 32. Taylor Rule It is a monetary-policy rule that stipulates how much the central bank should change

- 33. Ch. 11 The Money Markets

- 34. Today’s Lecture Overview The Money Market: definition, purpose and participants Money Market’s instruments: The Treasury Bills

- 35. Page 296 Copyright © 2003 Pearson Education, Inc. Slide 8–

- 36. The Money Markets Money Market’s securities: Maturity is less than 1 year and liquid Money market

- 37. Purpose of Money Markets Investors: the money markets provide a place for warehousing surplus funds for

- 38. Participants in Money Markets Government’s Treasury (e.g. US Treasury Department) Central Bank (e.g. Federal Reserve System)

- 39. Money Market Instruments Treasury Bills Federal Funds Repurchase Agreements Negotiable Certificates of Deposit Commercial Papers Banker’s

- 40. Treasury Bills Short-term borrowings of the federal government (31 days, 182 days, 12 months maturity) Sold

- 41. Discounting Example You pay $9850 for a 91-day T-bill. It is worth $10,000 at maturity. What

- 42. Treasury Bill Auctions Every Thursday, the Treasury announces how many 91-days and 182-days Treasury bills are

- 43. Treasury Bill Auction Competitive bids are satisfied starting from the lowest yield to highest or alternatively

- 44. Example: Treasury Bill Auctions The Treasury auctioned $2.5 billion par value 91-day T-bills, the following bids

- 45. Treasury Bill Auctions Example You have $1.750 BN left for competitive bids because all non-competitive will

- 46. Federal Funds Short-term funds transferred (loaned or borrowed) between financial institutions, usually for a period of

- 47. Repurchase agreements (Repos) Repo is a securities sale contract with an agreement to repurchase them back

- 48. KAZAKHSTAN REPOs: Government securities and the private A-rated (at KASE) securities can be transacted and serve

- 49. Repo formula Pc = (i/365) x n x (P0/100) + P0 , were Pc = closing

- 50. Example of the Repo transaction BTA needs a one day funds of $10 MM and enters

- 51. Negotiable Certificates of Deposit A bank-issued security that documents a deposit and specifies the interest rate

- 52. Commercial Paper Unsecured promissory notes, issued by corporations, that mature in no more than 270 days.

- 53. Banker’s Acceptances A banker’s acceptance is an order to pay a specified amount to the bearer

- 54. Exporter (Seller) Exporter‘s Bank Importer’s Bank Importer (Buyer) (2) Equipment (6) Payment at maturity Letter of

- 55. Advantages of Banker’s Acceptances Essentially, without the banker’s acceptances many international trade transactions would not occur

- 56. Eurodollars Dollar denominated deposits held in foreign banks Time deposits with fixed maturities Largest short term

- 57. Money Market Mutual Funds Money market mutual funds (MMMF) are open-edned investment funds that invest only

- 58. Page 316 Copyright © 2003 Pearson Education, Inc. Slide 8–

- 59. Next week read chapters 12 Bond Market 13 Stock Market

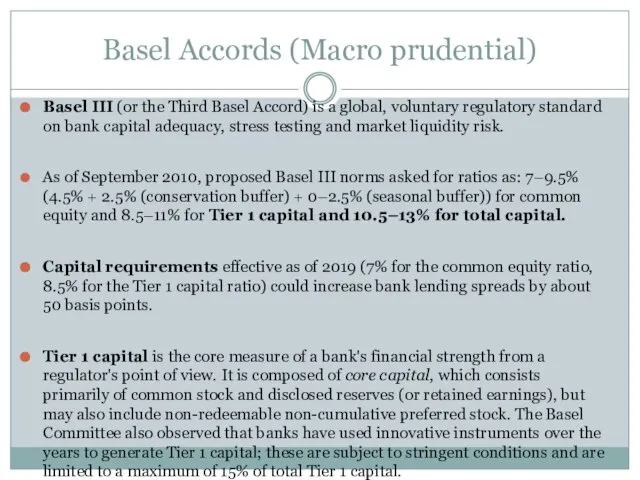

- 60. Basel Accords (Macro prudential) Basel III (or the Third Basel Accord) is a global, voluntary regulatory

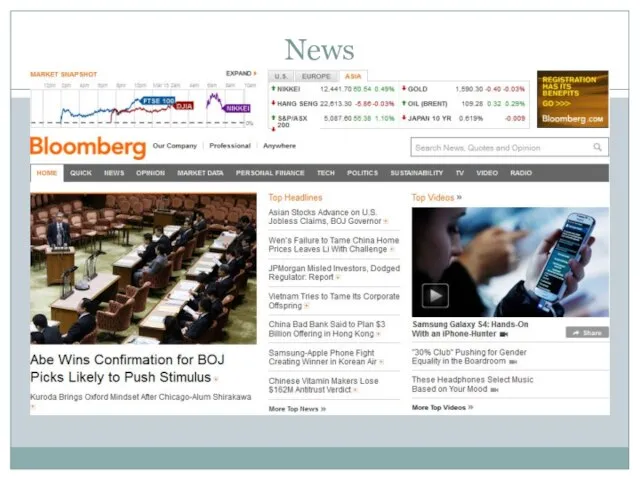

- 61. News Slide 8–

- 63. Скачать презентацию

Слайд 3Financial markets

Channels funds from savers to investors, thereby promoting economic efficiency.

Affects personal

Financial markets

Channels funds from savers to investors, thereby promoting economic efficiency.

Affects personal

Слайд 4Financial markets

The stock market is the market where stock, representing ownership in

Financial markets

The stock market is the market where stock, representing ownership in

Слайд 5Pooling and channeling of funds

Copyright © 2003 Pearson Education, Inc.

Pooling and channeling of funds

Copyright © 2003 Pearson Education, Inc.

Слайд 6Structure of Financial Markets

Even though firms don’t get any money, per se,

Structure of Financial Markets

Even though firms don’t get any money, per se,

Слайд 7Structure of Financial Markets

We can further classify secondary markets as follows:

Exchanges

Trades conducted

Structure of Financial Markets

We can further classify secondary markets as follows:

Exchanges

Trades conducted

Слайд 8Interest rates

We develop a better understanding of interest rates. We examine the

Interest rates

We develop a better understanding of interest rates. We examine the

Слайд 9Maturity and the Volatility

of Bond Returns

Only bond whose return is equals

Maturity and the Volatility

of Bond Returns

Only bond whose return is equals

Слайд 10Reinvestment Risk

Occurs if an investor’s holding period is longer than the

Reinvestment Risk

Occurs if an investor’s holding period is longer than the

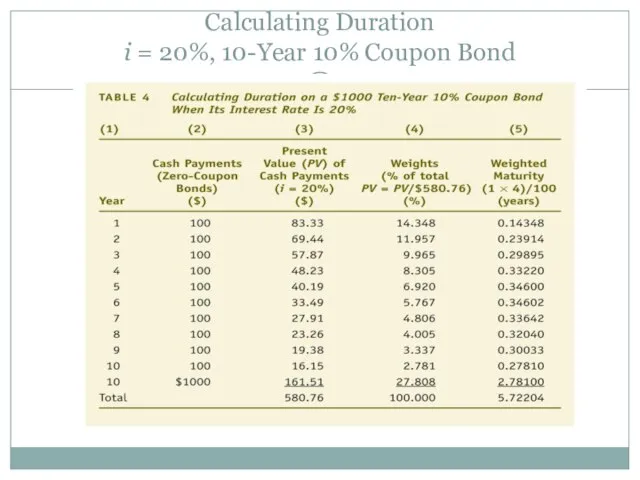

Слайд 11Calculating Duration

i = 20%, 10-Year 10% Coupon Bond

Calculating Duration

i = 20%, 10-Year 10% Coupon Bond

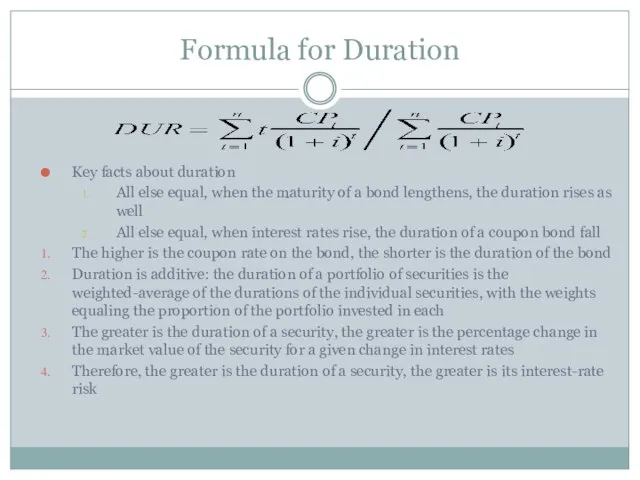

Слайд 12Formula for Duration

Key facts about duration

All else equal, when the maturity of

Formula for Duration

Key facts about duration

All else equal, when the maturity of

Слайд 13Why interest rates change?

Determinants of asset demand

Wealth – total resources owned

Expected returns

Why interest rates change?

Determinants of asset demand

Wealth – total resources owned

Expected returns

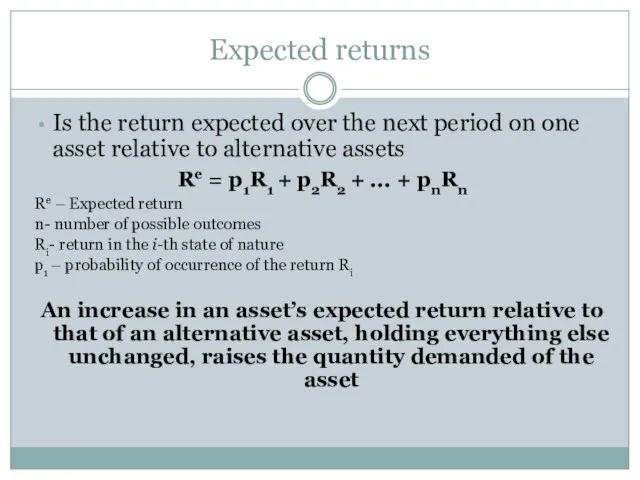

Слайд 14Expected returns

Is the return expected over the next period on one asset

Expected returns

Is the return expected over the next period on one asset

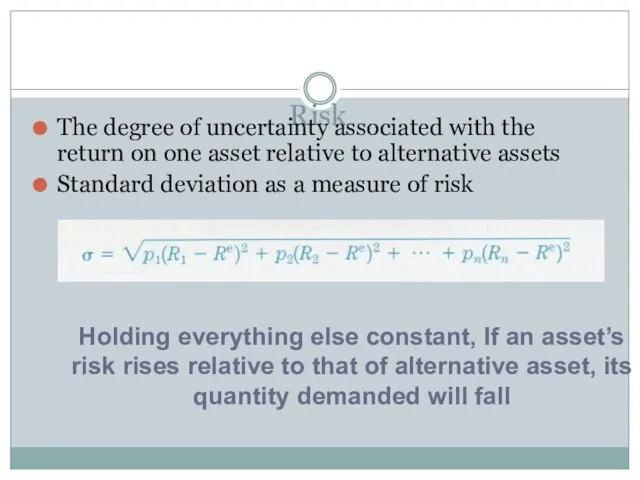

Слайд 15Risk

The degree of uncertainty associated with the return on one asset relative

Risk

The degree of uncertainty associated with the return on one asset relative

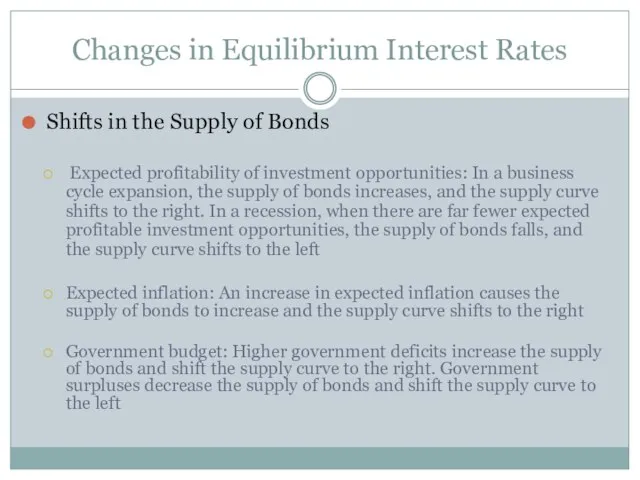

Слайд 16Changes in Equilibrium Interest Rates

Shifts in the Supply of Bonds

Expected profitability

Changes in Equilibrium Interest Rates

Shifts in the Supply of Bonds

Expected profitability

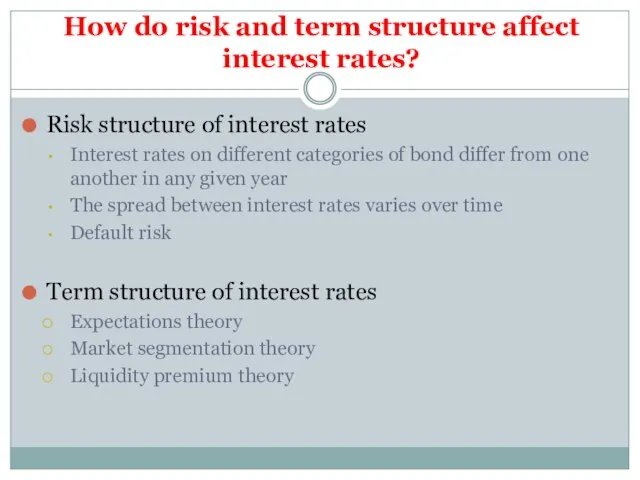

Слайд 17How do risk and term structure affect interest rates?

Risk structure of interest

How do risk and term structure affect interest rates?

Risk structure of interest

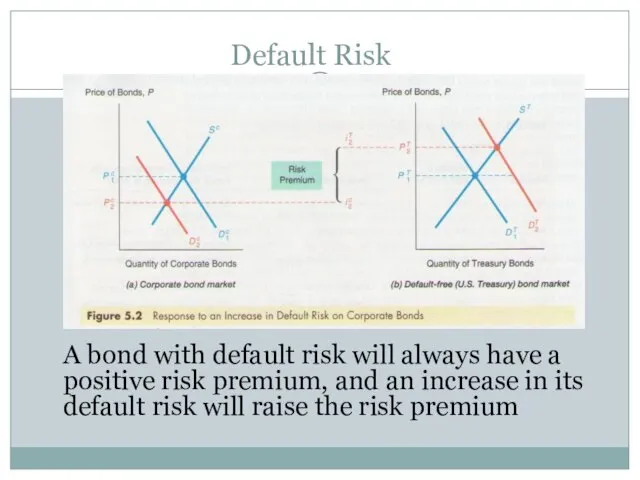

Слайд 18Default Risk

A bond with default risk will always have a positive risk

Default Risk

A bond with default risk will always have a positive risk

Слайд 19Term structure of interest rates

Bonds with identical risk, liquidity, and tax characteristics

Term structure of interest rates

Bonds with identical risk, liquidity, and tax characteristics

Слайд 20Expectations theory

Proposition: the interest rate on long-term bond will equal an average

Expectations theory

Proposition: the interest rate on long-term bond will equal an average

Слайд 22Efficient Market Hypothesis

The Efficient Market Hypothesis

Stronger Version of Efficient Market Hypothesis

Evidence on

Efficient Market Hypothesis

The Efficient Market Hypothesis

Stronger Version of Efficient Market Hypothesis

Evidence on

Слайд 23The Efficient Market Hypothesis

The prices of securities in financial markets fully reflect

The Efficient Market Hypothesis

The prices of securities in financial markets fully reflect

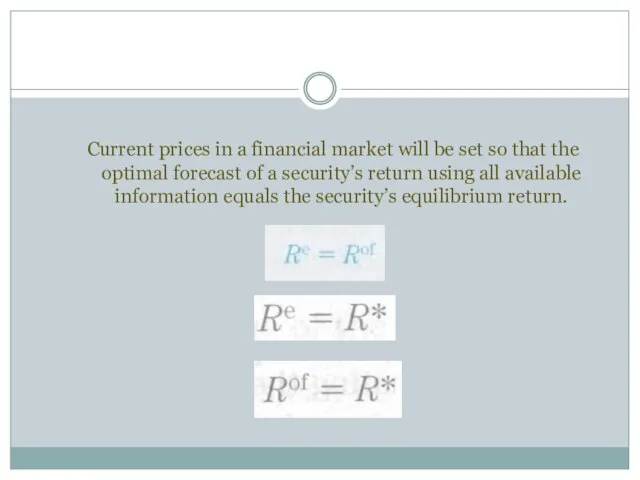

Слайд 24Current prices in a financial market will be set so that the

Слайд 25Rationale behind the hypothesis

Arbitrage, in which market participants (arbitrageurs) eliminate unexploited profit

Rationale behind the hypothesis

Arbitrage, in which market participants (arbitrageurs) eliminate unexploited profit

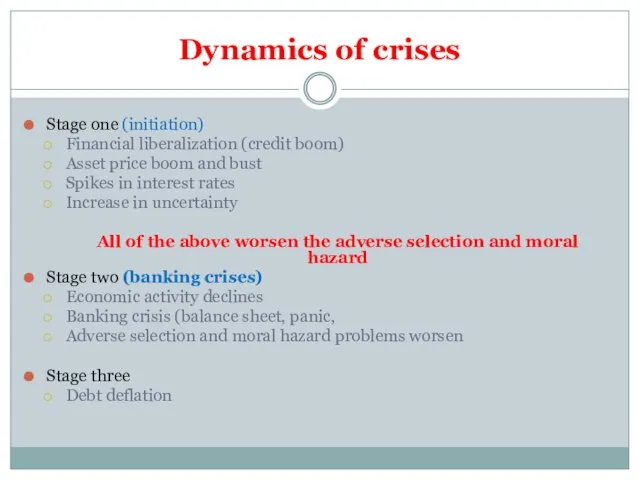

Слайд 26Dynamics of crises

Stage one (initiation)

Financial liberalization (credit boom)

Asset price boom and bust

Spikes

Dynamics of crises

Stage one (initiation)

Financial liberalization (credit boom)

Asset price boom and bust

Spikes

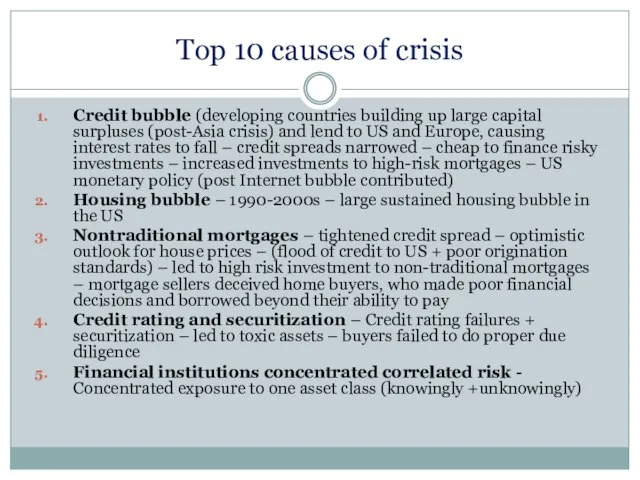

Слайд 27Top 10 causes of crisis

Credit bubble (developing countries building up large capital

Top 10 causes of crisis

Credit bubble (developing countries building up large capital

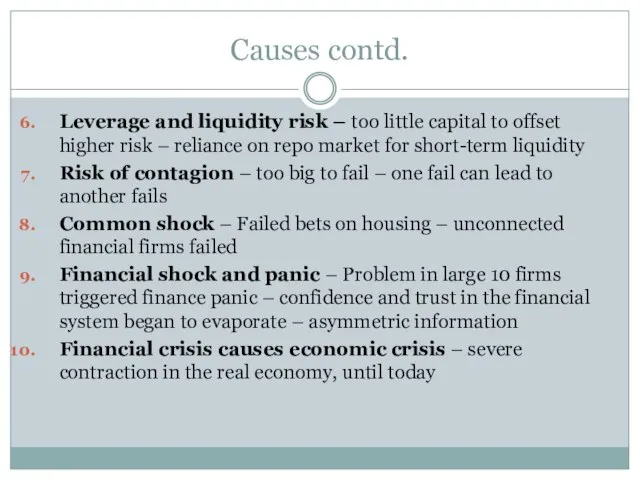

Слайд 28Causes contd.

Leverage and liquidity risk – too little capital to offset higher

Causes contd.

Leverage and liquidity risk – too little capital to offset higher

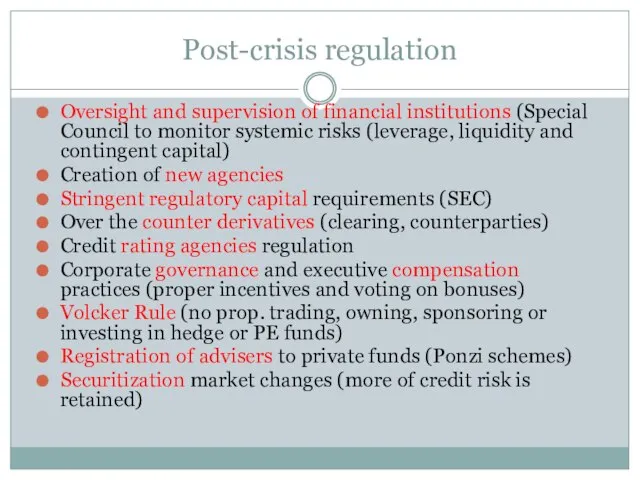

Слайд 29Post-crisis regulation

Oversight and supervision of financial institutions (Special Council to monitor systemic

Post-crisis regulation

Oversight and supervision of financial institutions (Special Council to monitor systemic

Слайд 30Why do we need Central Banks?

Prevent banking crisis

Stability of financial sector

Ensuring deposits

Providing

Why do we need Central Banks?

Prevent banking crisis

Stability of financial sector

Ensuring deposits

Providing

Слайд 31Goals of Monetary Policy

6 Goals

Inflation targeting

High employment

Economic growth

Stability of financial markets

Interest-rate stability

Foreign

Goals of Monetary Policy

6 Goals

Inflation targeting

High employment

Economic growth

Stability of financial markets

Interest-rate stability

Foreign

Слайд 32Taylor Rule

It is a monetary-policy rule that stipulates how much the central

Taylor Rule

It is a monetary-policy rule that stipulates how much the central

Слайд 33Ch. 11

The Money Markets

Ch. 11

The Money Markets

Слайд 34Today’s Lecture Overview

The Money Market: definition, purpose and participants

Money Market’s instruments:

The Treasury

Today’s Lecture Overview

The Money Market: definition, purpose and participants

Money Market’s instruments:

The Treasury

Слайд 35Page 296

Copyright © 2003 Pearson Education, Inc.

Slide 8–

Page 296

Copyright © 2003 Pearson Education, Inc.

Slide 8–

Слайд 36 The Money Markets

Money Market’s securities:

Maturity is less than 1 year and

The Money Markets

Money Market’s securities:

Maturity is less than 1 year and

Слайд 37Purpose of Money Markets

Investors: the money markets provide a place for warehousing

Purpose of Money Markets

Investors: the money markets provide a place for warehousing

Слайд 38Participants in Money Markets

Government’s Treasury (e.g. US Treasury Department)

Central Bank (e.g. Federal

Participants in Money Markets

Government’s Treasury (e.g. US Treasury Department)

Central Bank (e.g. Federal

Слайд 39Money Market Instruments

Treasury Bills

Federal Funds

Repurchase Agreements

Negotiable Certificates of Deposit

Commercial Papers

Banker’s Acceptances

Eurodollars

Money

Money Market Instruments

Treasury Bills

Federal Funds

Repurchase Agreements

Negotiable Certificates of Deposit

Commercial Papers

Banker’s Acceptances

Eurodollars

Money

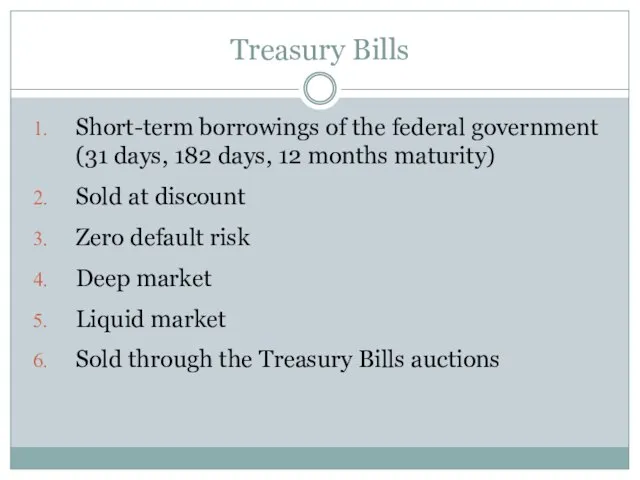

Слайд 40Treasury Bills

Short-term borrowings of the federal government (31 days, 182 days, 12

Treasury Bills

Short-term borrowings of the federal government (31 days, 182 days, 12

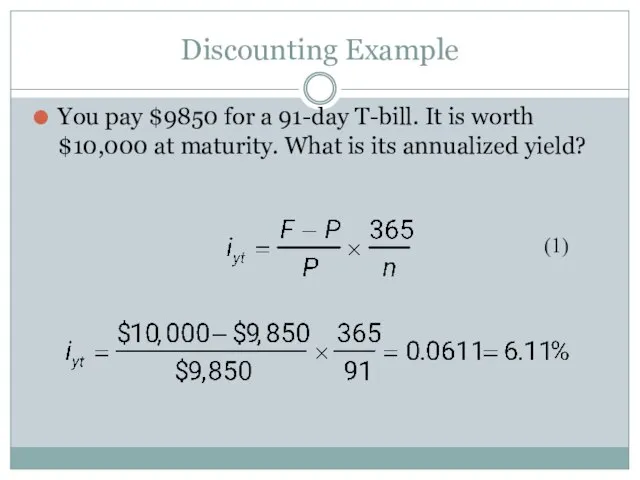

Слайд 41Discounting Example

You pay $9850 for a 91-day T-bill. It is worth $10,000

Discounting Example

You pay $9850 for a 91-day T-bill. It is worth $10,000

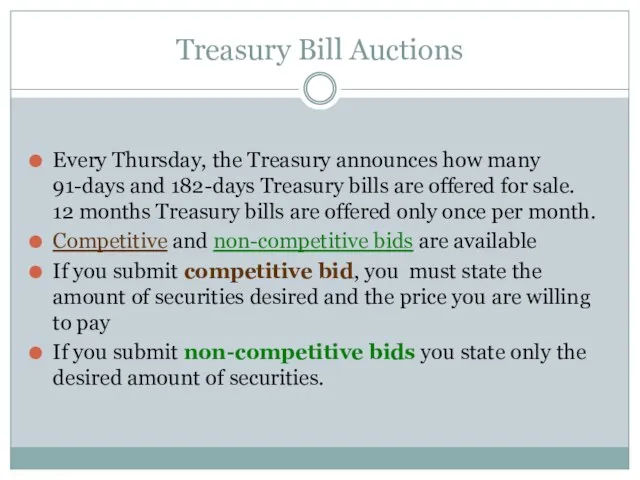

Слайд 42Treasury Bill Auctions

Every Thursday, the Treasury announces how many 91-days and 182-days

Treasury Bill Auctions

Every Thursday, the Treasury announces how many 91-days and 182-days

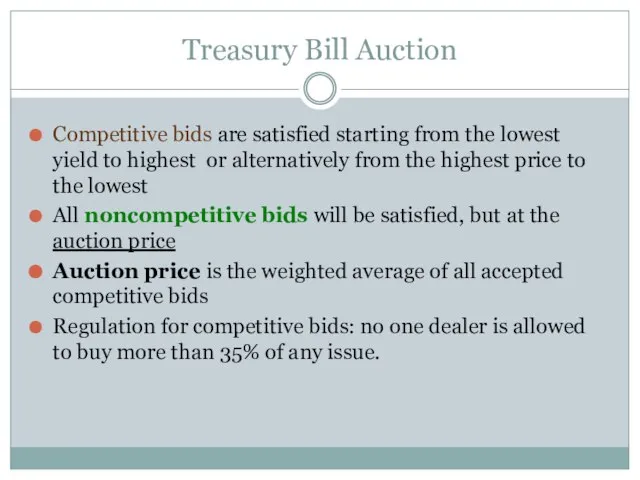

Слайд 43Treasury Bill Auction

Competitive bids are satisfied starting from the lowest yield to

Treasury Bill Auction

Competitive bids are satisfied starting from the lowest yield to

Слайд 44

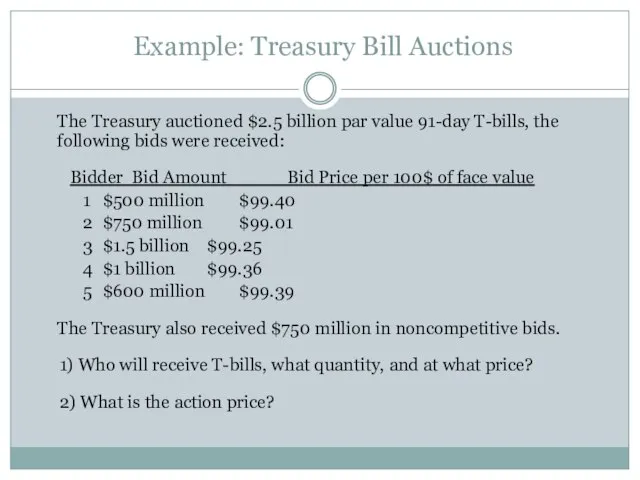

Example: Treasury Bill Auctions

The Treasury auctioned $2.5 billion par value 91-day

Example: Treasury Bill Auctions

The Treasury auctioned $2.5 billion par value 91-day

Слайд 45Treasury Bill Auctions Example

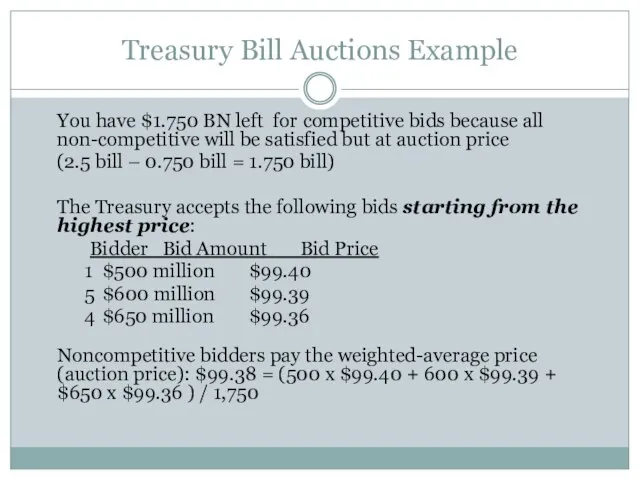

You have $1.750 BN left for competitive bids because

Treasury Bill Auctions Example

You have $1.750 BN left for competitive bids because

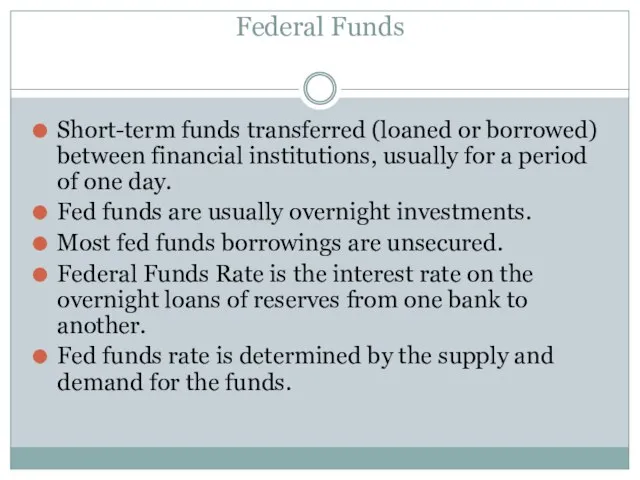

Слайд 46Federal Funds

Short-term funds transferred (loaned or borrowed) between financial institutions, usually

Federal Funds

Short-term funds transferred (loaned or borrowed) between financial institutions, usually

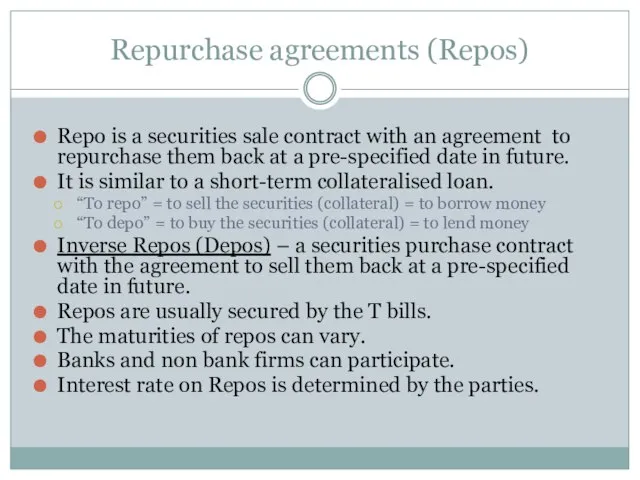

Слайд 47Repurchase agreements (Repos)

Repo is a securities sale contract with an agreement to

Repurchase agreements (Repos)

Repo is a securities sale contract with an agreement to

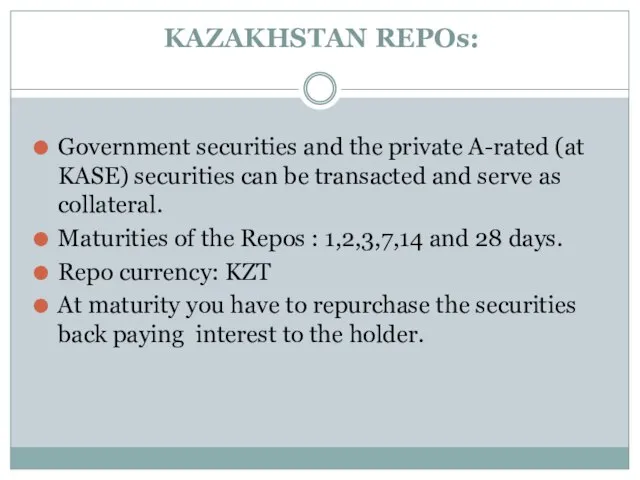

Слайд 48KAZAKHSTAN REPOs:

Government securities and the private A-rated (at KASE) securities can be

KAZAKHSTAN REPOs:

Government securities and the private A-rated (at KASE) securities can be

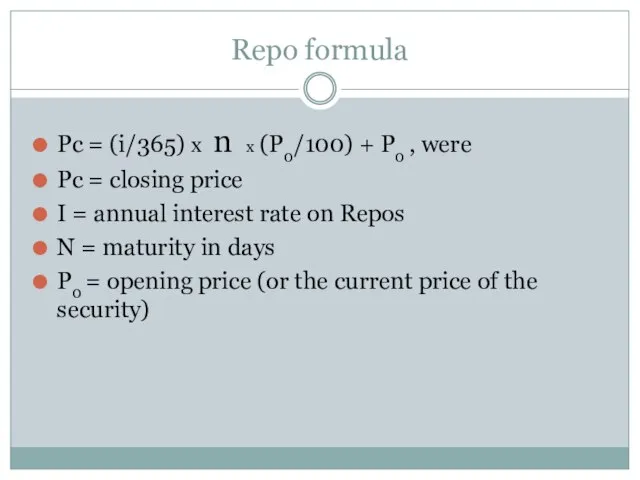

Слайд 49Repo formula

Pc = (i/365) x n x (P0/100) + P0 , were

Pc

Repo formula

Pc = (i/365) x n x (P0/100) + P0 , were

Pc

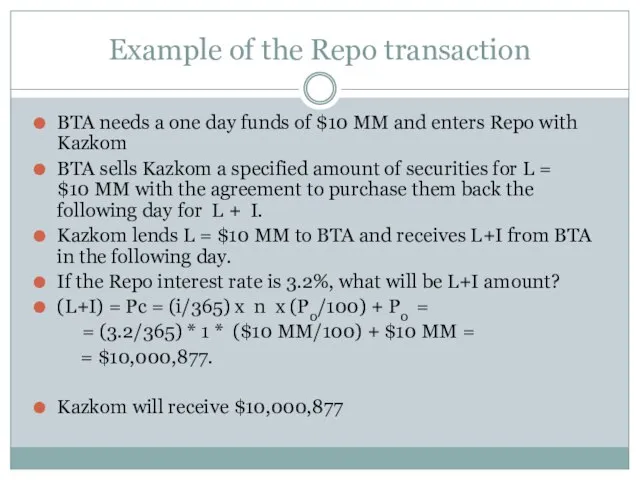

Слайд 50Example of the Repo transaction

BTA needs a one day funds of

Example of the Repo transaction

BTA needs a one day funds of

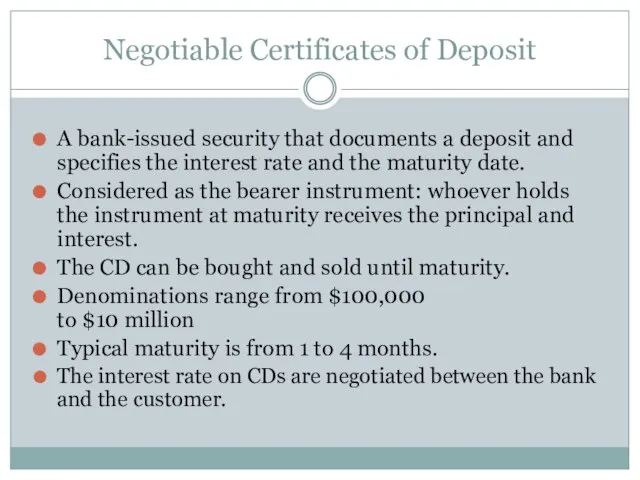

Слайд 51Negotiable Certificates of Deposit

A bank-issued security that documents a deposit and specifies

Negotiable Certificates of Deposit

A bank-issued security that documents a deposit and specifies

Слайд 52Commercial Paper

Unsecured promissory notes, issued by corporations, that mature in no more

Commercial Paper

Unsecured promissory notes, issued by corporations, that mature in no more

Слайд 53Banker’s Acceptances

A banker’s acceptance is an order to pay a specified amount

Banker’s Acceptances

A banker’s acceptance is an order to pay a specified amount

Слайд 54

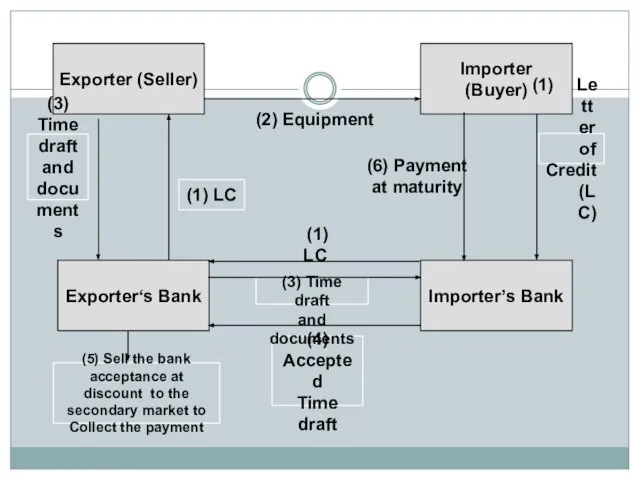

Exporter (Seller)

Exporter‘s Bank

Importer’s Bank

Importer (Buyer)

(2) Equipment

(6) Payment

at maturity

Letter of

Credit (LC)

Exporter (Seller)

Exporter‘s Bank

Importer’s Bank

Importer (Buyer)

(2) Equipment

(6) Payment

at maturity

Letter of

Credit (LC)

Слайд 55Advantages of Banker’s Acceptances

Essentially, without the banker’s acceptances many international trade transactions

Advantages of Banker’s Acceptances

Essentially, without the banker’s acceptances many international trade transactions

Слайд 56Eurodollars

Dollar denominated deposits held

in foreign banks

Time deposits with fixed maturities

Largest

Eurodollars

Dollar denominated deposits held

in foreign banks

Time deposits with fixed maturities

Largest

Слайд 57Money Market Mutual Funds

Money market mutual funds (MMMF) are open-edned investment funds

Money Market Mutual Funds

Money market mutual funds (MMMF) are open-edned investment funds

Слайд 58Page 316

Copyright © 2003 Pearson Education, Inc.

Slide 8–

Page 316

Copyright © 2003 Pearson Education, Inc.

Slide 8–

Слайд 59Next week read chapters

12 Bond Market

13 Stock Market

Next week read chapters

12 Bond Market

13 Stock Market

Слайд 60Basel Accords (Macro prudential)

Basel III (or the Third Basel Accord) is a

Basel Accords (Macro prudential)

Basel III (or the Third Basel Accord) is a

Слайд 61News

Slide 8–

News

Slide 8–

Интерактивное взаимодействие со зрителями Танец с огнем, веселая клоунада и немного мистики объединяются в сюжетную историю Наше

Интерактивное взаимодействие со зрителями Танец с огнем, веселая клоунада и немного мистики объединяются в сюжетную историю Наше  Презентация аватария

Презентация аватария Функционирование организации. (Тема 6)

Функционирование организации. (Тема 6) 12.10.2022, 10_38 Microsoft Lens

12.10.2022, 10_38 Microsoft Lens КОЛЛЕКЦИЯ НОВОГОДНИХ ПОДАРКОВ ОТ КОМПАНИИ «КОНТИ» 2011-2012

КОЛЛЕКЦИЯ НОВОГОДНИХ ПОДАРКОВ ОТ КОМПАНИИ «КОНТИ» 2011-2012 Культуры Древнего мира

Культуры Древнего мира Les jours fériés

Les jours fériés ЖОСТОВО

ЖОСТОВО врт презентация

врт презентация Обеды

Обеды Cведения о нейронах и искусственных нейросетях

Cведения о нейронах и искусственных нейросетях Амины. Анилин

Амины. Анилин Принципы технического регулирования

Принципы технического регулирования Овощатка

Овощатка Аудит бренда работодателя

Аудит бренда работодателя Поздравление для бабушки

Поздравление для бабушки Информационно- компьютерная культура

Информационно- компьютерная культура Реклама

Реклама Приготовление воздушного теста

Приготовление воздушного теста RUS-01 Compensation plan Wantage One 2.4 Euro

RUS-01 Compensation plan Wantage One 2.4 Euro Гармония инноваций и традиций в учебном процессе

Гармония инноваций и традиций в учебном процессе Технічне завдання 3

Технічне завдання 3 Автор: Сыркина Н.Ф. учитель технологии МОУ СОШ № 1 г. Катав- Ивановска

Автор: Сыркина Н.Ф. учитель технологии МОУ СОШ № 1 г. Катав- Ивановска Портфолио педагога

Портфолио педагога Личность тренера в командообразовании

Личность тренера в командообразовании ГОУ ВПО СГТУКафедра ИФСКонтрольная по Excel

ГОУ ВПО СГТУКафедра ИФСКонтрольная по Excel Медиастудия Фристайл МБУДО ДШИ №2

Медиастудия Фристайл МБУДО ДШИ №2 Автоматизация деятельности архивной службы предприятия Система “АРХИВНОЕ ДЕЛО” (версия 4.0)

Автоматизация деятельности архивной службы предприятия Система “АРХИВНОЕ ДЕЛО” (версия 4.0)