- Financial Statesment

Содержание

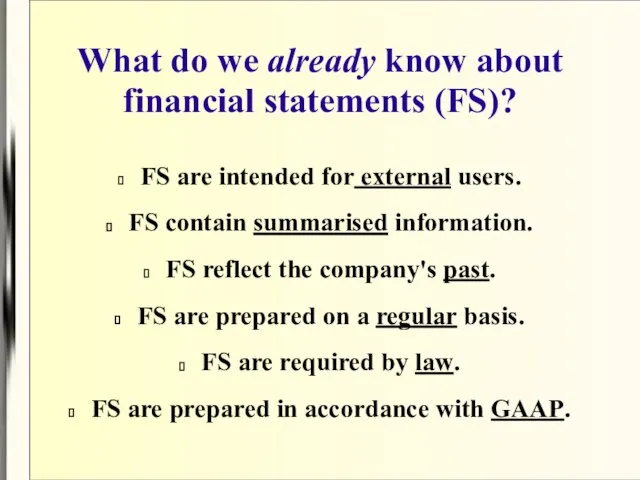

- 2. What do we already know about financial statements (FS)? FS are intended for external users. FS

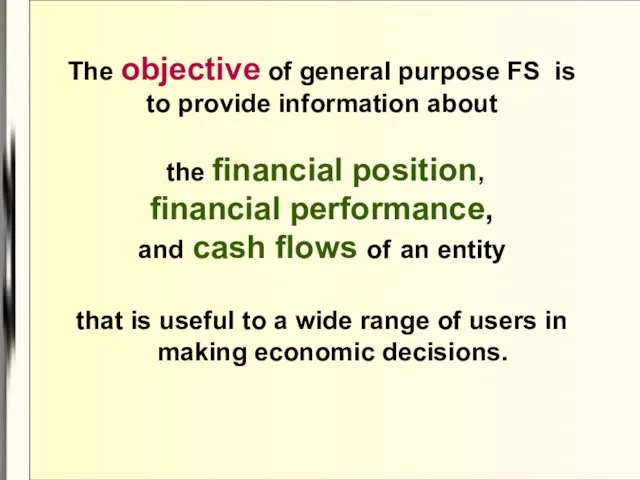

- 3. The objective of general purpose FS is to provide information about the financial position, financial performance,

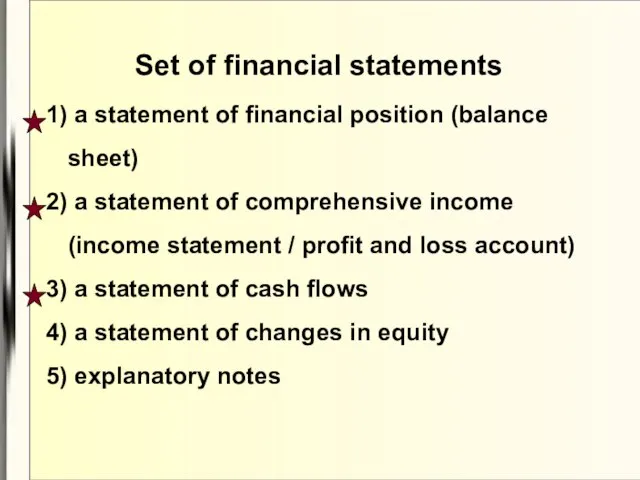

- 4. Set of financial statements 1) a statement of financial position (balance sheet) 2) a statement of

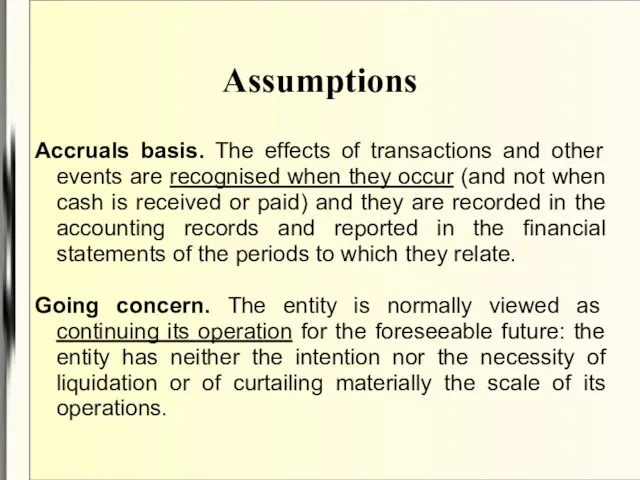

- 5. Assumptions Accruals basis. The effects of transactions and other events are recognised when they occur (and

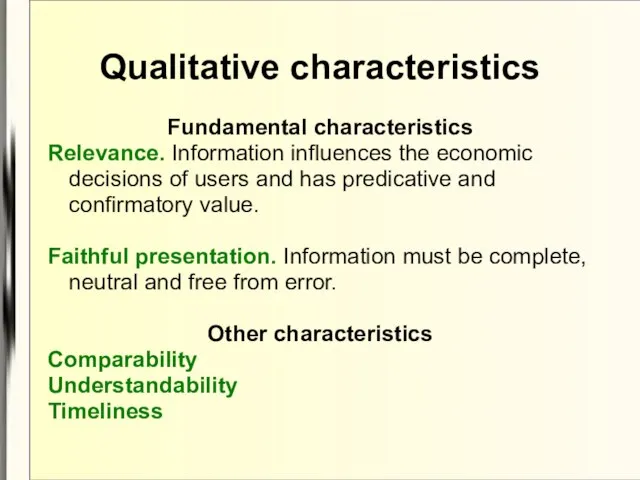

- 6. Qualitative characteristics Fundamental characteristics Relevance. Information influences the economic decisions of users and has predicative and

- 7. The Balance Sheet The Statement of Financial Position (SOFP)

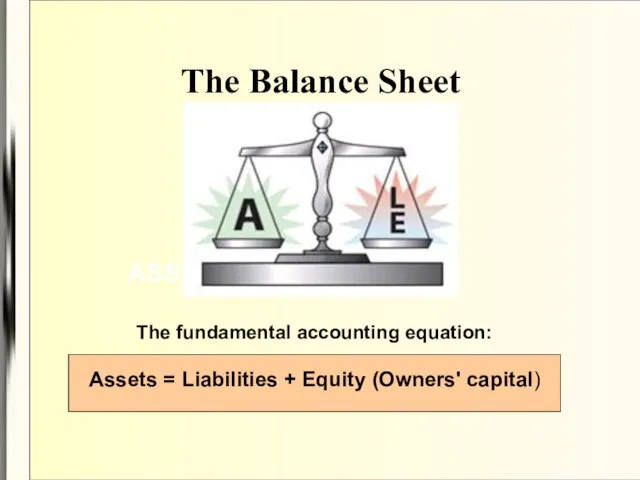

- 8. The Balance Sheet ASSETS The fundamental accounting equation: Assets = Liabilities + Equity (Owners' capital)

- 9. What is an asset? something that we own cash furniture vehicles inventory equipment land

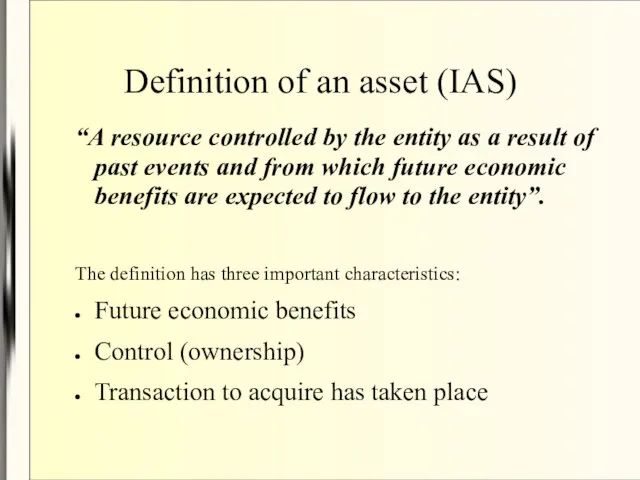

- 10. Definition of an asset (IAS) “A resource controlled by the entity as a result of past

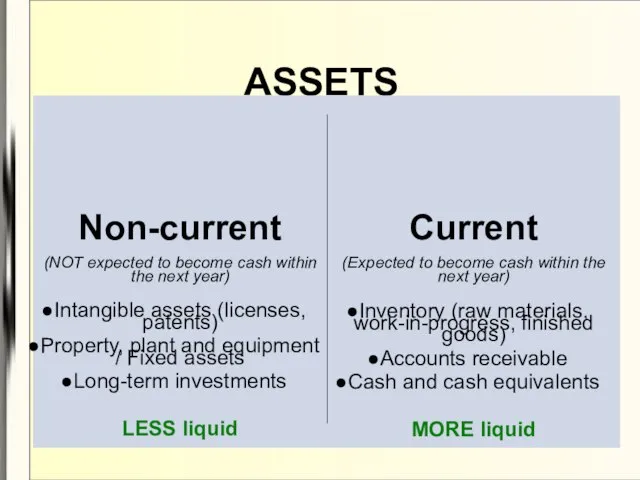

- 11. ASSETS

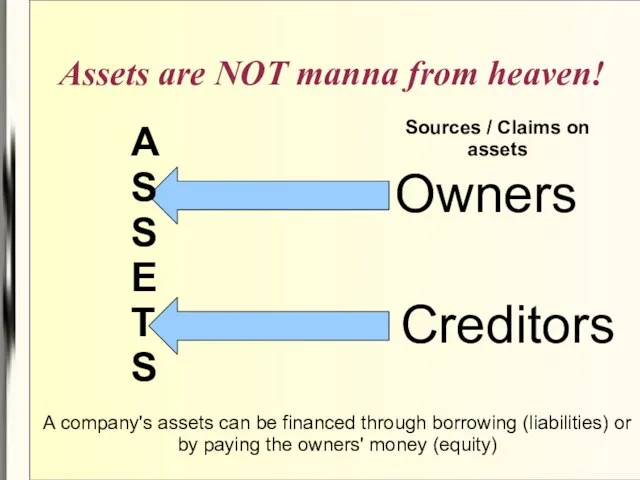

- 12. Assets are NOT manna from heaven! Sources / Claims on assets Owners Creditors A company's assets

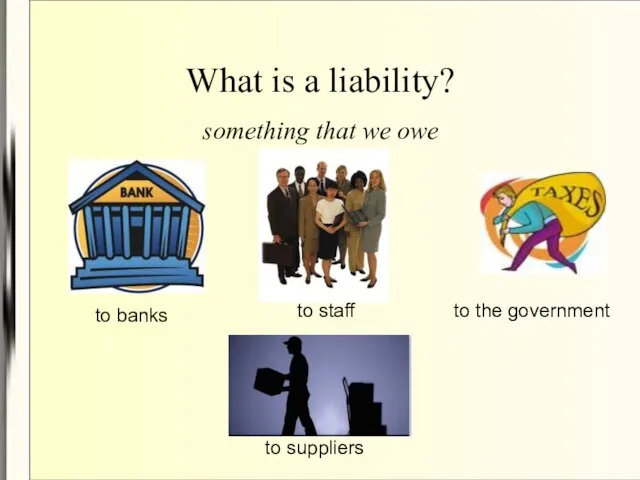

- 13. What is a liability? something that we owe to banks to staff to the government to

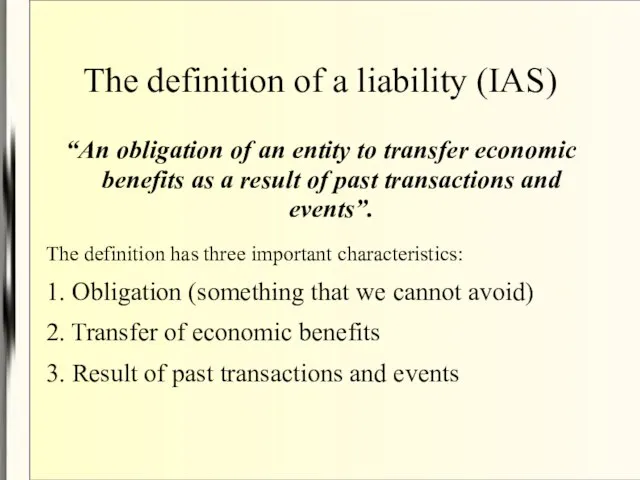

- 14. The definition of a liability (IAS) “An obligation of an entity to transfer economic benefits as

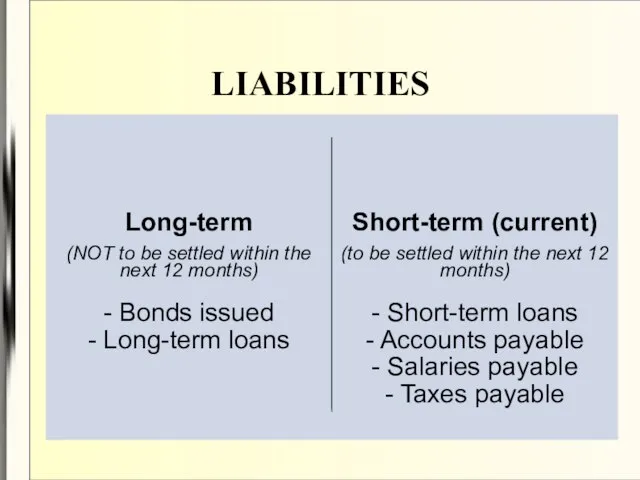

- 15. LIABILITIES

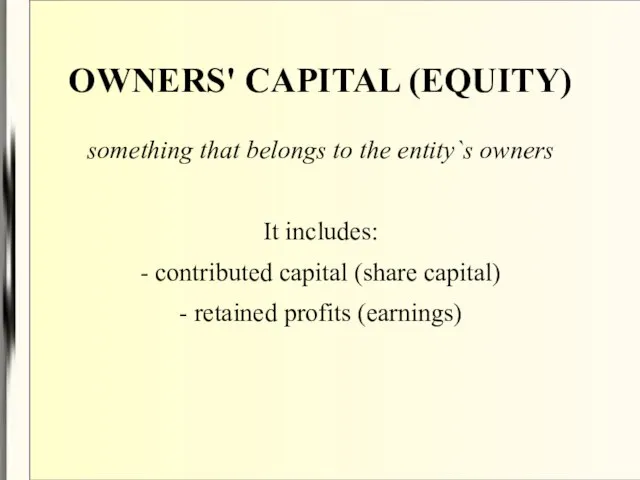

- 16. OWNERS' CAPITAL (EQUITY) something that belongs to the entity`s owners It includes: - contributed capital (share

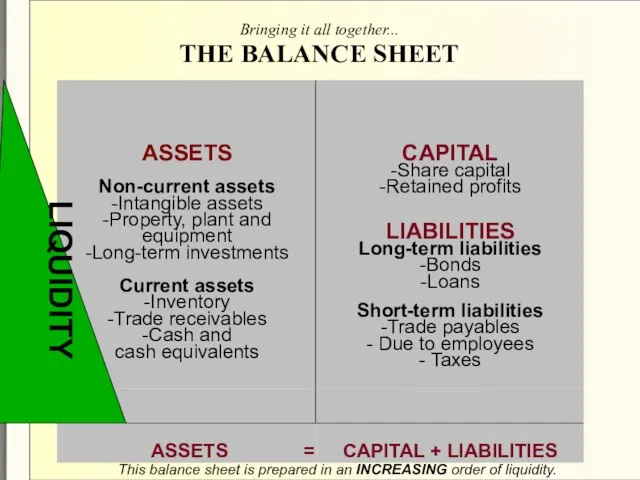

- 17. Bringing it all together... THE BALANCE SHEET This balance sheet is prepared in an INCREASING order

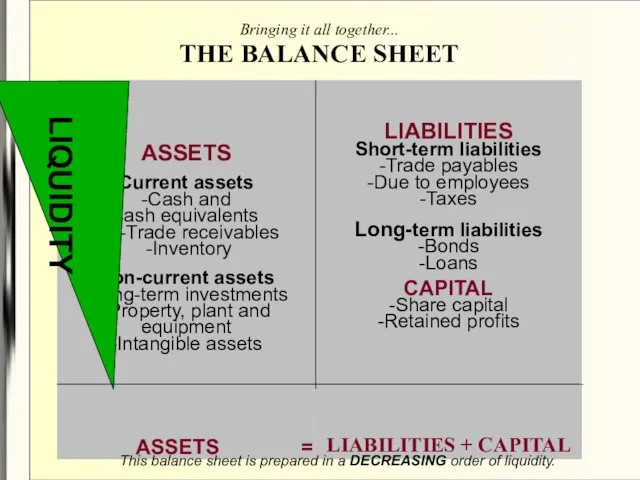

- 18. Bringing it all together... THE BALANCE SHEET This balance sheet is prepared in a DECREASING order

- 19. A balance sheet is a snapshot of a company at a moment in time . It

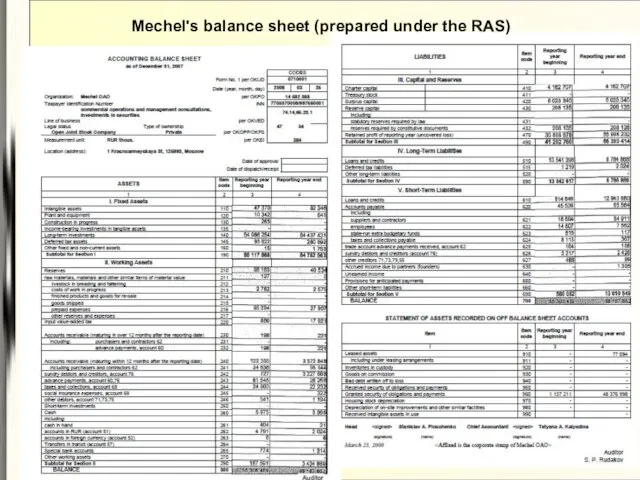

- 20. Mechel's balance sheet (prepared under the RAS))

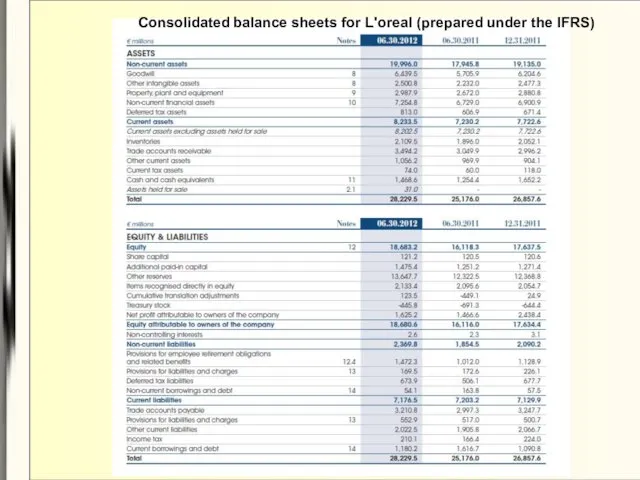

- 21. Consolidated balance sheets for L'oreal (prepared under the IFRS)

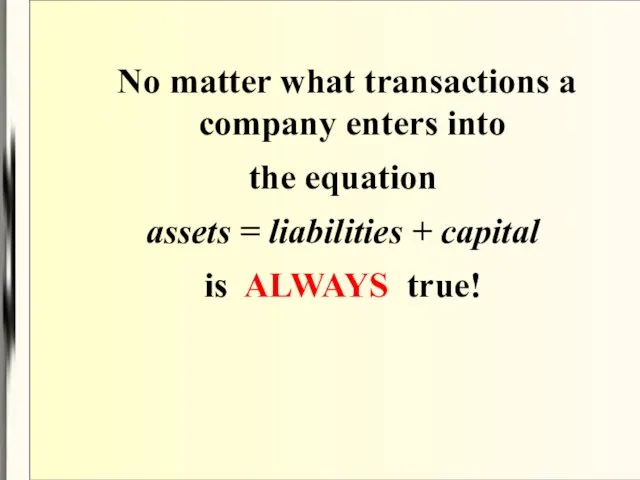

- 22. No matter what transactions a company enters into the equation assets = liabilities + capital is

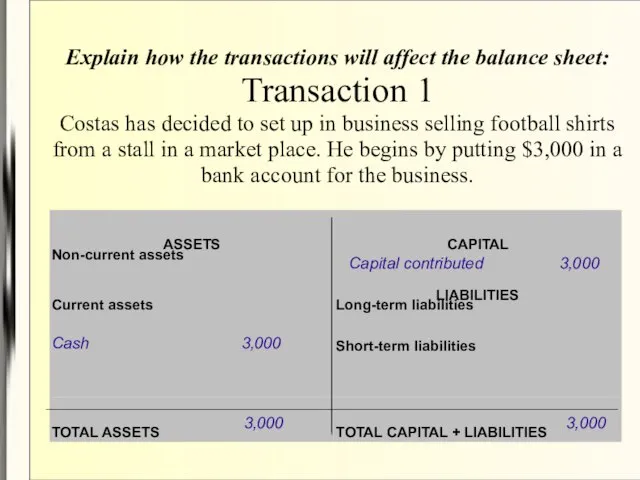

- 23. Explain how the transactions will affect the balance sheet: Transaction 1 Costas has decided to set

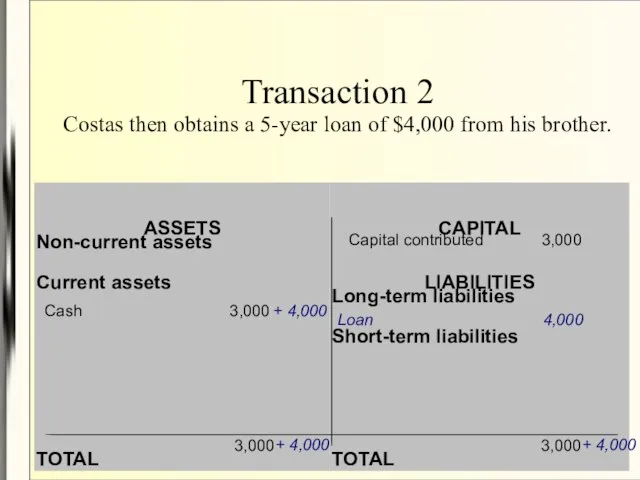

- 24. Transaction 2 Costas then obtains a 5-year loan of $4,000 from his brother. Cash 3,000 Capital

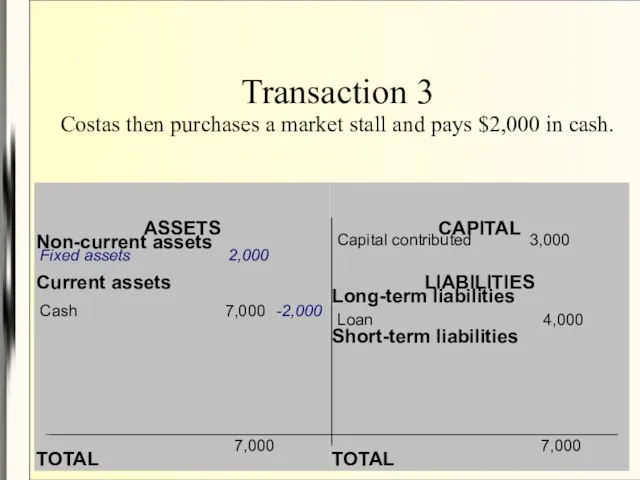

- 25. Transaction 3 Costas then purchases a market stall and pays $2,000 in cash. Cash 7,000 Capital

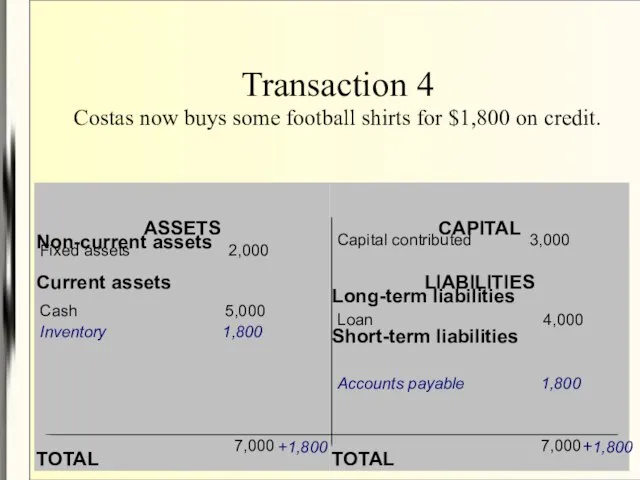

- 26. Transaction 4 Costas now buys some football shirts for $1,800 on credit. Cash 5,000 Capital contributed

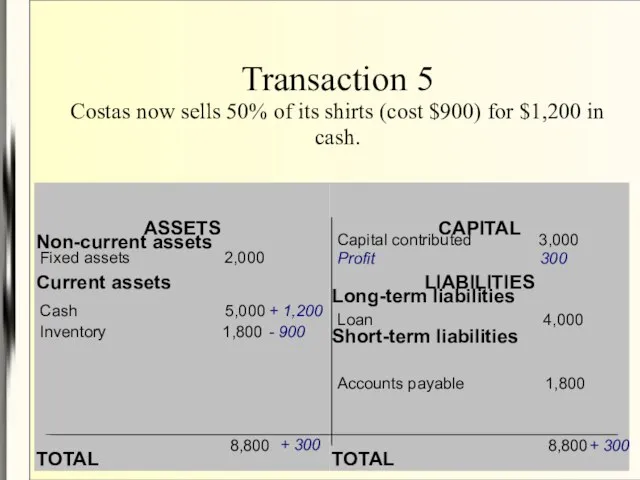

- 27. Transaction 5 Costas now sells 50% of its shirts (cost $900) for $1,200 in cash. Cash

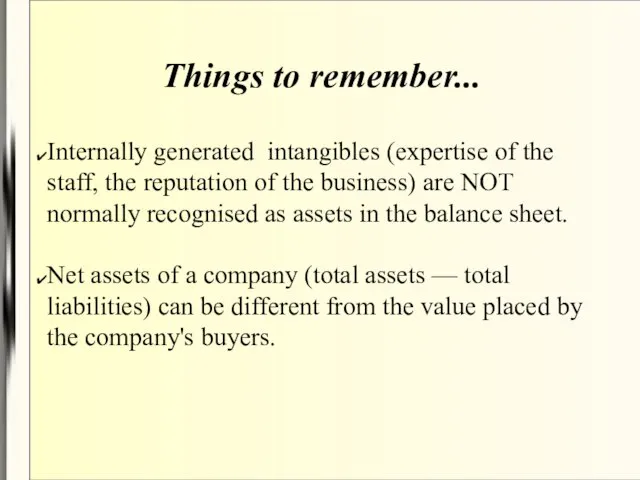

- 28. Things to remember... Internally generated intangibles (expertise of the staff, the reputation of the business) are

- 30. Скачать презентацию

Слайд 3The objective of general purpose FS is

to provide information about

the financial

The objective of general purpose FS is

to provide information about

the financial

Слайд 4Set of financial statements

1) a statement of financial position (balance sheet)

2)

Set of financial statements

1) a statement of financial position (balance sheet)

2)

Слайд 5Assumptions

Accruals basis. The effects of transactions and other events are recognised when

Assumptions

Accruals basis. The effects of transactions and other events are recognised when

Слайд 6Qualitative characteristics

Fundamental characteristics

Relevance. Information influences the economic decisions of users and has

Qualitative characteristics

Fundamental characteristics

Relevance. Information influences the economic decisions of users and has

Слайд 7The Balance Sheet

The Statement of Financial Position (SOFP)

The Balance Sheet

The Statement of Financial Position (SOFP)

Слайд 8The Balance Sheet

ASSETS

The fundamental accounting equation:

Assets = Liabilities + Equity (Owners'

The Balance Sheet

ASSETS

The fundamental accounting equation:

Assets = Liabilities + Equity (Owners'

Слайд 9What is an asset?

something that we own

cash

furniture

vehicles

inventory

equipment

land

What is an asset?

something that we own

cash

furniture

vehicles

inventory

equipment

land

Слайд 10Definition of an asset (IAS)

“A resource controlled by the entity as a

Definition of an asset (IAS)

“A resource controlled by the entity as a

Слайд 11

ASSETS

ASSETS

Слайд 12Assets are NOT manna from heaven!

Sources / Claims on assets

Owners

Creditors

A company's

Assets are NOT manna from heaven!

Sources / Claims on assets

Owners

Creditors

A company's

Слайд 13What is a liability?

something that we owe

to banks

to staff

to the government

to suppliers

What is a liability?

something that we owe

to banks

to staff

to the government

to suppliers

Слайд 14The definition of a liability (IAS)

“An obligation of an entity to transfer

The definition of a liability (IAS)

“An obligation of an entity to transfer

Слайд 15LIABILITIES

LIABILITIES

Слайд 16OWNERS' CAPITAL (EQUITY)

something that belongs to the entity`s owners

It includes:

- contributed capital

OWNERS' CAPITAL (EQUITY)

something that belongs to the entity`s owners

It includes:

- contributed capital

Слайд 17Bringing it all together...

THE BALANCE SHEET

This balance sheet is prepared in an

Bringing it all together...

THE BALANCE SHEET

This balance sheet is prepared in an

Слайд 18Bringing it all together...

THE BALANCE SHEET

This balance sheet is prepared in a

Bringing it all together...

THE BALANCE SHEET

This balance sheet is prepared in a

Слайд 19A balance sheet is a snapshot of a company at a moment

A balance sheet is a snapshot of a company at a moment

Слайд 20Mechel's balance sheet (prepared under the RAS))

Mechel's balance sheet (prepared under the RAS))

Слайд 21Consolidated balance sheets for L'oreal (prepared under the IFRS)

Consolidated balance sheets for L'oreal (prepared under the IFRS)

Слайд 22 No matter what transactions a company enters into

the equation

assets

No matter what transactions a company enters into

the equation

assets

Слайд 23Explain how the transactions will affect the balance sheet:

Transaction 1

Costas has decided

Explain how the transactions will affect the balance sheet: Transaction 1 Costas has decided

Слайд 24Transaction 2

Costas then obtains a 5-year loan of $4,000 from his brother.

Cash

Transaction 2

Costas then obtains a 5-year loan of $4,000 from his brother.

Cash

Слайд 25Transaction 3

Costas then purchases a market stall and pays $2,000 in cash.

Cash

Transaction 3

Costas then purchases a market stall and pays $2,000 in cash.

Cash

Слайд 26Transaction 4

Costas now buys some football shirts for $1,800 on credit.

Cash

Transaction 4

Costas now buys some football shirts for $1,800 on credit.

Cash

Слайд 27Transaction 5

Costas now sells 50% of its shirts (cost $900) for $1,200

Transaction 5 Costas now sells 50% of its shirts (cost $900) for $1,200

Слайд 28Things to remember...

Internally generated intangibles (expertise of the staff, the reputation of

Things to remember...

Internally generated intangibles (expertise of the staff, the reputation of

Моу лицей №34

Моу лицей №34 ко дню матери

ко дню матери Урок презентация на тему Мировое хозяйство (4 класс)

Урок презентация на тему Мировое хозяйство (4 класс) Образование будущего в СГЭУ

Образование будущего в СГЭУ Презентация на тему Почему табак называют ядом

Презентация на тему Почему табак называют ядом Оновлені дизайни масла Селянське

Оновлені дизайни масла Селянське Презентация на тему Художник

Презентация на тему Художник workflow

workflow Коммерческое предложение по установке КМС-400/1

Коммерческое предложение по установке КМС-400/1 Презентация на тему Новейшая история

Презентация на тему Новейшая история  Xxiv сессия комитета Бетон, железобетон, преднапряжнный железобетон международной организации по стандартизации ИСО

Xxiv сессия комитета Бетон, железобетон, преднапряжнный железобетон международной организации по стандартизации ИСО Новая Боровая, 1 квартал. Классы жилья

Новая Боровая, 1 квартал. Классы жилья ПРИМЕНЕНИЕ ИТОГОВ С.ПЕТЕРБУРГСКОЙ КОНФЕРЕНЦИИ МЕЖДУНАРОДНЫМ ОБЩЕСТВОМ

ПРИМЕНЕНИЕ ИТОГОВ С.ПЕТЕРБУРГСКОЙ КОНФЕРЕНЦИИ МЕЖДУНАРОДНЫМ ОБЩЕСТВОМ Древняя Спарта

Древняя Спарта We are the world. We are the children

We are the world. We are the children ПЕРСПЕКТИВЫ РАЗВИТИЯ ПЕРЕСТРАХОВОЧНОГО РЫНКА РОССИИ КАК ОДНОГО ИЗ МЕЖДУНАРОДНЫХ ПЕРЕСТРАХОВОЧНЫХ ЦЕНТРОВ

ПЕРСПЕКТИВЫ РАЗВИТИЯ ПЕРЕСТРАХОВОЧНОГО РЫНКА РОССИИ КАК ОДНОГО ИЗ МЕЖДУНАРОДНЫХ ПЕРЕСТРАХОВОЧНЫХ ЦЕНТРОВ Основы построения процесса спортивной тренировки

Основы построения процесса спортивной тренировки Солнечные батареи

Солнечные батареи Сущность и принципы построения организационной структуры управления. Горизонтальное и вертикальное разделение труда

Сущность и принципы построения организационной структуры управления. Горизонтальное и вертикальное разделение труда Корней Чуковский.

Корней Чуковский. Что изучает курс «География материков и океанов»

Что изучает курс «География материков и океанов» Изображение одного и того же предмета в различных цветовых гаммах. Холодная гамма

Изображение одного и того же предмета в различных цветовых гаммах. Холодная гамма Мхи

Мхи Презентация на тему Сатира в начале XX века

Презентация на тему Сатира в начале XX века  Право на труд

Право на труд Технологии Flexus Balasystem для мусорных полигонов современного города

Технологии Flexus Balasystem для мусорных полигонов современного города Вопросы местного значения поселений в сфере жилищных отношений Закон № 131-ФЗ, ст. 14 (поселения), 16 (гор. округа): 1. К вопросам местно

Вопросы местного значения поселений в сфере жилищных отношений Закон № 131-ФЗ, ст. 14 (поселения), 16 (гор. округа): 1. К вопросам местно Итоги работы отрасли и основные направления инновационного развития легкой промышленности

Итоги работы отрасли и основные направления инновационного развития легкой промышленности