- FIRM BEHAVIOR AND THE ORGANIZATION OF Industry

Содержание

- 2. 13 The Costs of Production

- 3. The Market Forces of Supply and Demand Supply and demand are the two words that economists

- 4. WHAT ARE COSTS? According to the Law of Supply: Firms are willing to produce and sell

- 5. WHAT ARE COSTS? The Firm’s Objective The economic goal of the firm is to maximize profits.

- 6. Total Revenue, Total Cost, and Profit Total Revenue The amount a firm receives for the sale

- 7. Total Revenue, Total Cost, and Profit Profit is the firm’s total revenue minus its total cost.

- 8. Costs as Opportunity Costs A firm’s cost of production includes all the opportunity costs of making

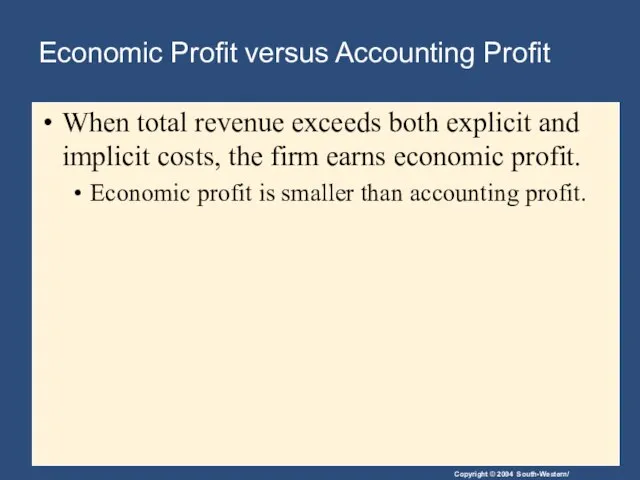

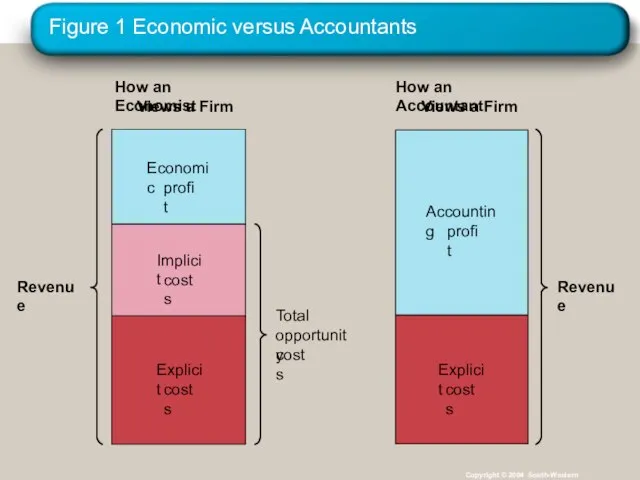

- 9. Economic Profit versus Accounting Profit Economists measure a firm’s economic profit as total revenue minus total

- 10. Economic Profit versus Accounting Profit When total revenue exceeds both explicit and implicit costs, the firm

- 11. Figure 1 Economic versus Accountants Copyright © 2004 South-Western How an Economist Views a Firm How

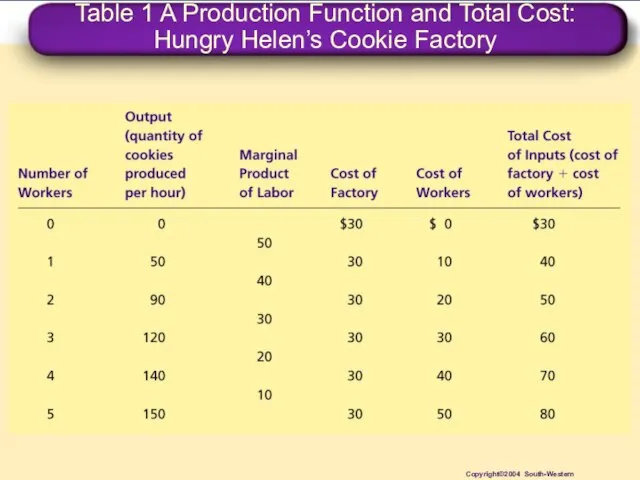

- 12. Table 1 A Production Function and Total Cost: Hungry Helen’s Cookie Factory Copyright©2004 South-Western

- 13. PRODUCTION AND COSTS The Production Function The production function shows the relationship between quantity of inputs

- 14. The Production Function Marginal Product The marginal product of any input in the production process is

- 15. The Production Function Diminishing Marginal Product Diminishing marginal product is the property whereby the marginal product

- 16. Figure 2 Hungry Helen’s Production Function Copyright © 2004 South-Western Quantity of Output (cookies per hour)

- 17. The Production Function Diminishing Marginal Product The slope of the production function measures the marginal product

- 18. From the Production Function to the Total-Cost Curve The relationship between the quantity a firm can

- 19. Table 1 A Production Function and Total Cost: Hungry Helen’s Cookie Factory Copyright©2004 South-Western

- 20. Figure 3 Hungry Helen’s Total-Cost Curve Copyright © 2004 South-Western Total Cost $80 70 60 50

- 21. THE VARIOUS MEASURES OF COST Costs of production may be divided into fixed costs and variable

- 22. Fixed and Variable Costs Fixed costs are those costs that do not vary with the quantity

- 23. Fixed and Variable Costs Total Costs Total Fixed Costs (TFC) Total Variable Costs (TVC) Total Costs

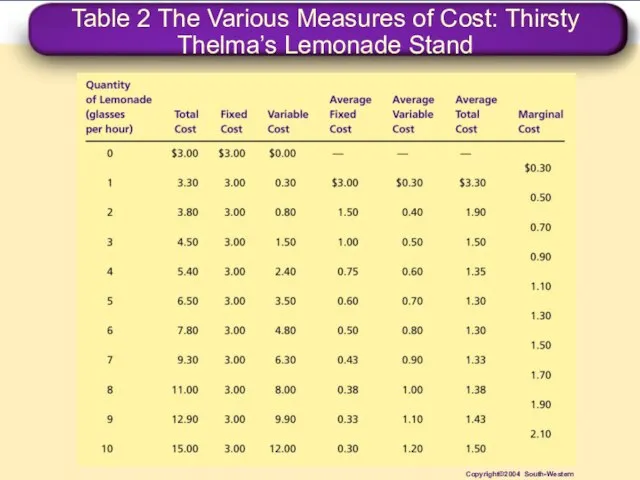

- 24. Table 2 The Various Measures of Cost: Thirsty Thelma’s Lemonade Stand Copyright©2004 South-Western

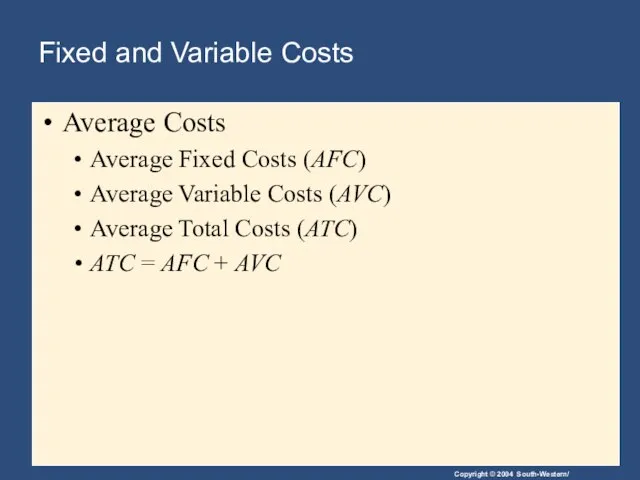

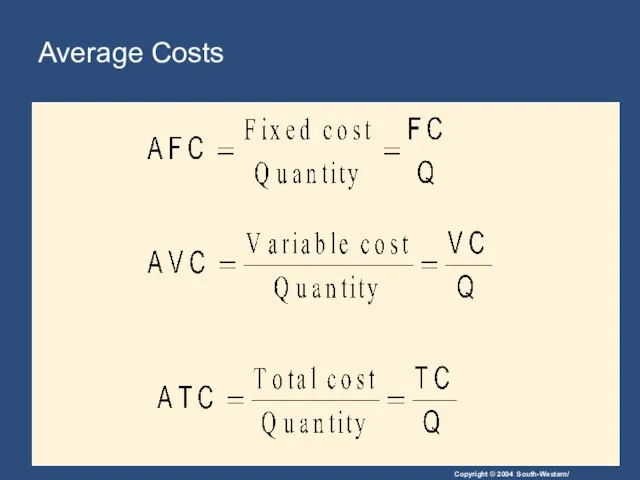

- 25. Fixed and Variable Costs Average Costs Average costs can be determined by dividing the firm’s costs

- 26. Fixed and Variable Costs Average Costs Average Fixed Costs (AFC) Average Variable Costs (AVC) Average Total

- 27. Average Costs

- 28. Table 2 The Various Measures of Cost: Thirsty Thelma’s Lemonade Stand Copyright©2004 South-Western

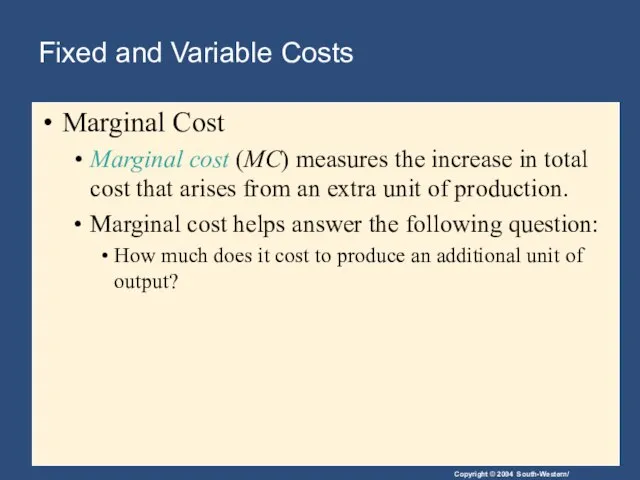

- 29. Fixed and Variable Costs Marginal Cost Marginal cost (MC) measures the increase in total cost that

- 30. Marginal Cost

- 31. Marginal Cost Thirsty Thelma’s Lemonade Stand

- 32. Figure 4 Thirsty Thelma’s Total-Cost Curves Copyright © 2004 South-Western Total Cost $15.00 14.00 13.00 12.00

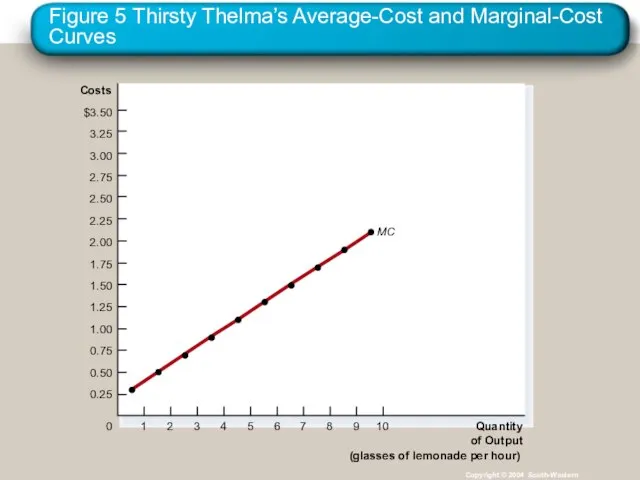

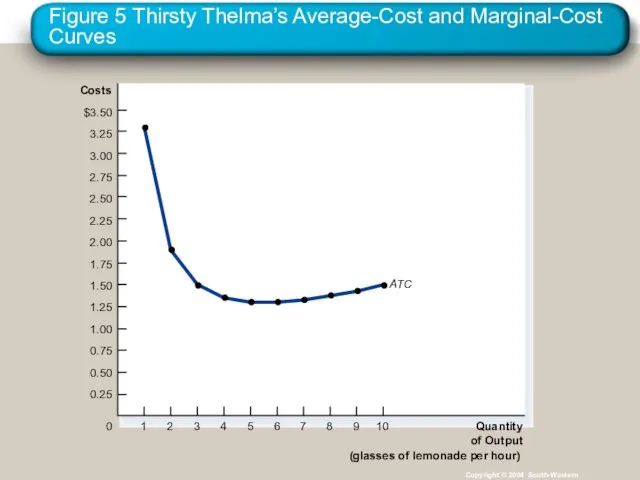

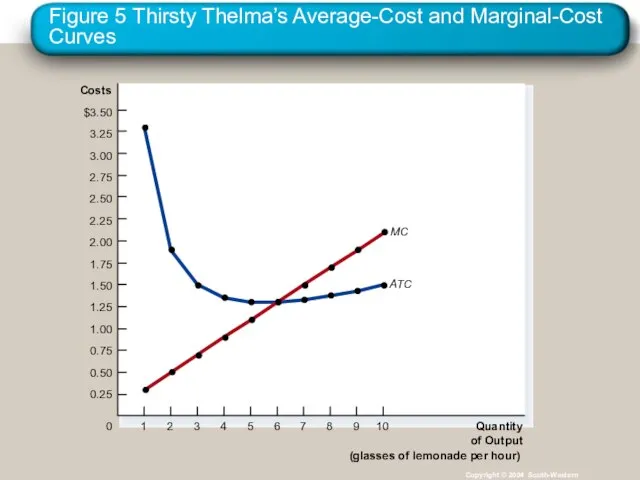

- 33. Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves Copyright © 2004 South-Western Costs $3.50 3.25 3.00

- 34. Cost Curves and Their Shapes Marginal cost rises with the amount of output produced. This reflects

- 35. Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves Copyright © 2004 South-Western Costs $3.50 3.25 3.00

- 36. Cost Curves and Their Shapes The average total-cost curve is U-shaped. At very low levels of

- 37. Cost Curves and Their Shapes The bottom of the U-shaped ATC curve occurs at the quantity

- 38. Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves Copyright © 2004 South-Western Costs $3.50 3.25 3.00

- 39. Cost Curves and Their Shapes Relationship between Marginal Cost and Average Total Cost Whenever marginal cost

- 40. Cost Curves and Their Shapes Relationship Between Marginal Cost and Average Total Cost The marginal-cost curve

- 41. Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves Copyright © 2004 South-Western Costs $3.50 3.25 3.00

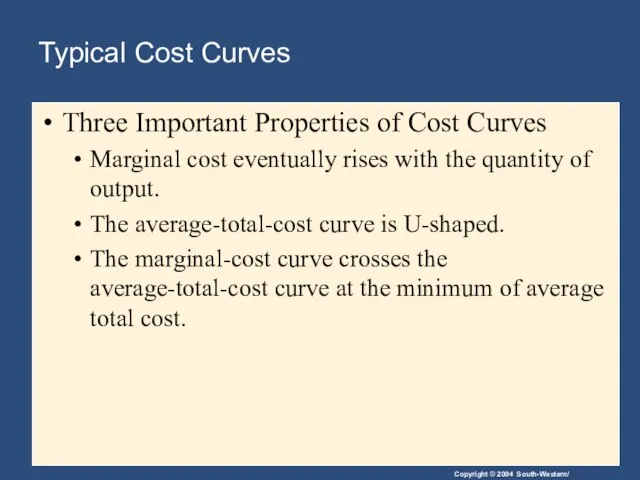

- 42. Typical Cost Curves It is now time to examine the relationships that exist between the different

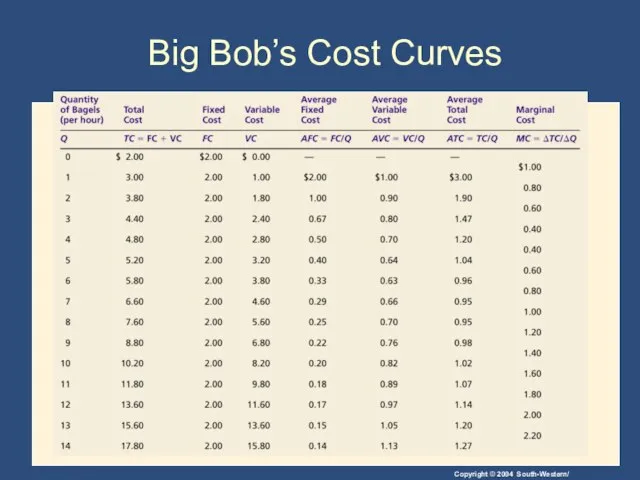

- 43. Big Bob’s Cost Curves

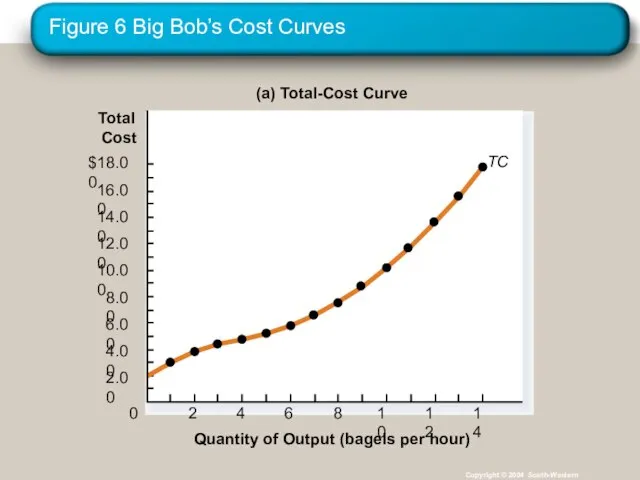

- 44. Figure 6 Big Bob’s Cost Curves Copyright © 2004 South-Western (a) Total-Cost Curve $18.00 16.00 14.00

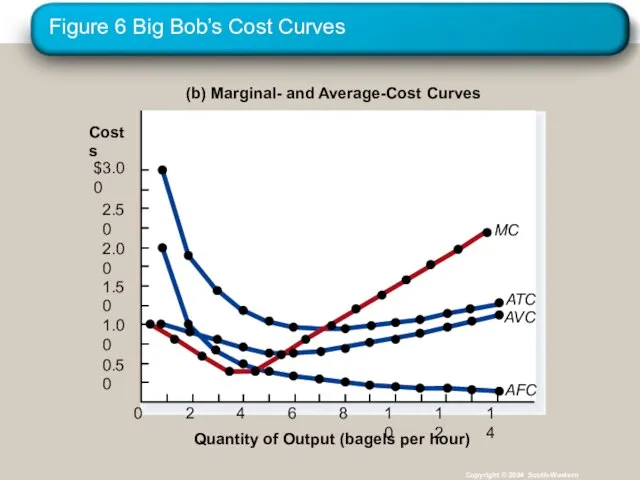

- 45. Figure 6 Big Bob’s Cost Curves Copyright © 2004 South-Western (b) Marginal- and Average-Cost Curves Quantity

- 46. Typical Cost Curves Three Important Properties of Cost Curves Marginal cost eventually rises with the quantity

- 47. COSTS IN THE SHORT RUN AND IN THE LONG RUN For many firms, the division of

- 48. COSTS IN THE SHORT RUN AND IN THE LONG RUN Because many costs are fixed in

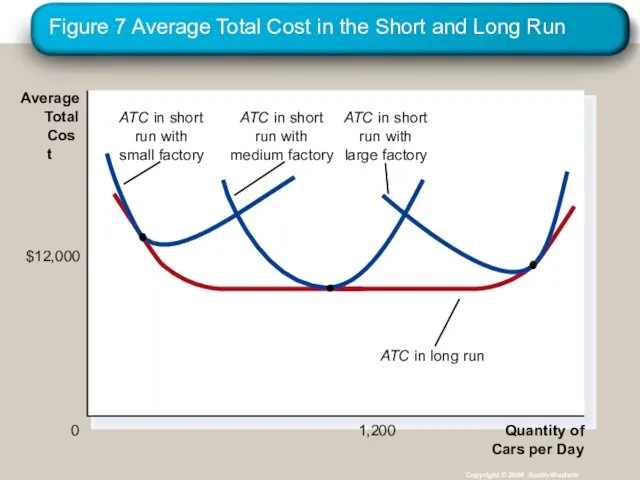

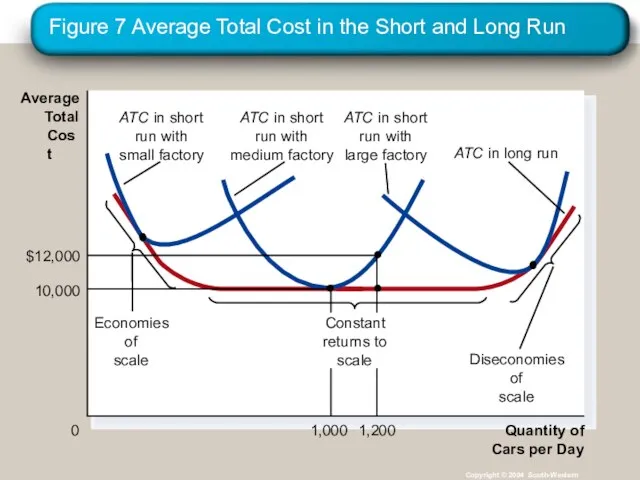

- 49. Figure 7 Average Total Cost in the Short and Long Run Copyright © 2004 South-Western Quantity

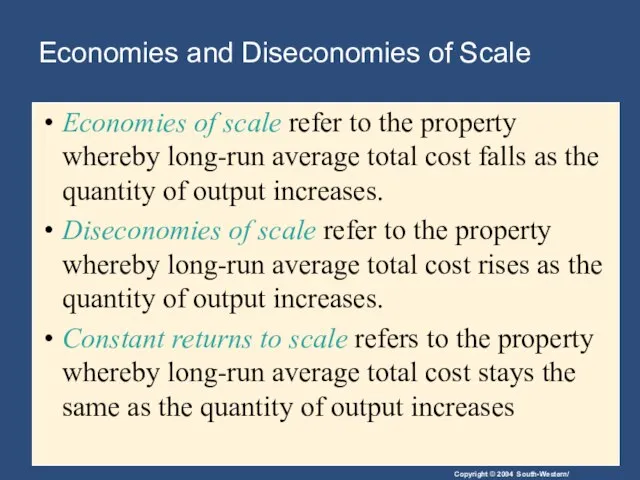

- 50. Economies and Diseconomies of Scale Economies of scale refer to the property whereby long-run average total

- 51. Figure 7 Average Total Cost in the Short and Long Run Copyright © 2004 South-Western Quantity

- 52. Summary The goal of firms is to maximize profit, which equals total revenue minus total cost.

- 53. Summary A firm’s costs reflect its production process. A typical firm’s production function gets flatter as

- 54. Summary Average total cost is total cost divided by the quantity of output. Marginal cost is

- 56. Скачать презентацию

Слайд 3The Market Forces of Supply and Demand

Supply and demand are the two

The Market Forces of Supply and Demand

Supply and demand are the two

Слайд 4WHAT ARE COSTS?

According to the Law of Supply:

Firms are willing to produce

WHAT ARE COSTS?

According to the Law of Supply:

Firms are willing to produce

Слайд 5WHAT ARE COSTS?

The Firm’s Objective

The economic goal of the firm is to

WHAT ARE COSTS?

The Firm’s Objective

The economic goal of the firm is to

Слайд 6Total Revenue, Total Cost, and Profit

Total Revenue

The amount a firm receives for

Total Revenue, Total Cost, and Profit

Total Revenue

The amount a firm receives for

Слайд 7Total Revenue, Total Cost, and Profit

Profit is the firm’s total revenue minus

Total Revenue, Total Cost, and Profit

Profit is the firm’s total revenue minus

Слайд 8Costs as Opportunity Costs

A firm’s cost of production includes all the opportunity

Costs as Opportunity Costs

A firm’s cost of production includes all the opportunity

Слайд 9Economic Profit versus Accounting Profit

Economists measure a firm’s economic profit as total

Economic Profit versus Accounting Profit

Economists measure a firm’s economic profit as total

Слайд 10Economic Profit versus Accounting Profit

When total revenue exceeds both explicit and implicit

Economic Profit versus Accounting Profit

When total revenue exceeds both explicit and implicit

Слайд 11Figure 1 Economic versus Accountants

Copyright © 2004 South-Western

How an Economist

Views a Firm

How

Figure 1 Economic versus Accountants

Copyright © 2004 South-Western

How an Economist

Views a Firm

How

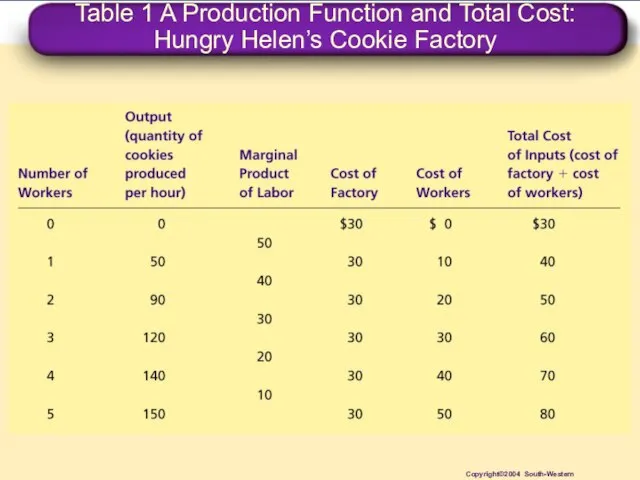

Слайд 12Table 1 A Production Function and Total Cost: Hungry Helen’s Cookie Factory

Copyright©2004

Table 1 A Production Function and Total Cost: Hungry Helen’s Cookie Factory

Copyright©2004

Слайд 13PRODUCTION AND COSTS

The Production Function

The production function shows the relationship between quantity

PRODUCTION AND COSTS

The Production Function

The production function shows the relationship between quantity

Слайд 14The Production Function

Marginal Product

The marginal product of any input in the

The Production Function

Marginal Product

The marginal product of any input in the

Слайд 15The Production Function

Diminishing Marginal Product

Diminishing marginal product is the property whereby

The Production Function

Diminishing Marginal Product

Diminishing marginal product is the property whereby

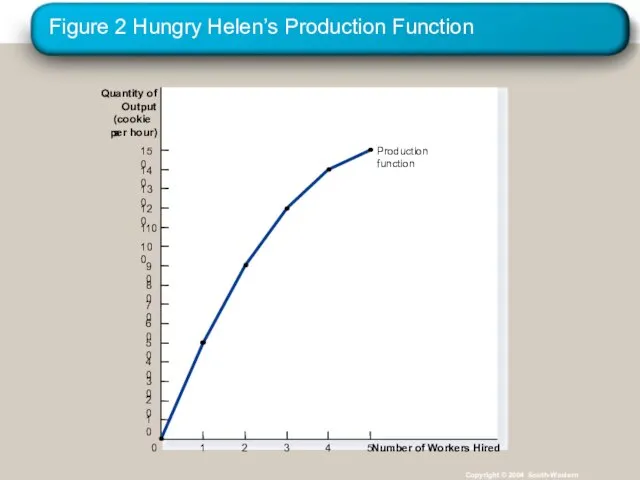

Слайд 16Figure 2 Hungry Helen’s Production Function

Copyright © 2004 South-Western

Quantity of

Output

(cookies

per hour)

150

140

130

120

110

100

90

80

70

60

50

40

30

20

10

Number of

Figure 2 Hungry Helen’s Production Function

Copyright © 2004 South-Western

Quantity of

Output

(cookies

per hour)

150

140

130

120

110

100

90

80

70

60

50

40

30

20

10

Number of

Слайд 17The Production Function

Diminishing Marginal Product

The slope of the production function

The Production Function

Diminishing Marginal Product

The slope of the production function

Слайд 18From the Production Function to the Total-Cost Curve

The relationship between the quantity

From the Production Function to the Total-Cost Curve

The relationship between the quantity

Слайд 19Table 1 A Production Function and Total Cost: Hungry Helen’s Cookie Factory

Copyright©2004

Table 1 A Production Function and Total Cost: Hungry Helen’s Cookie Factory

Copyright©2004

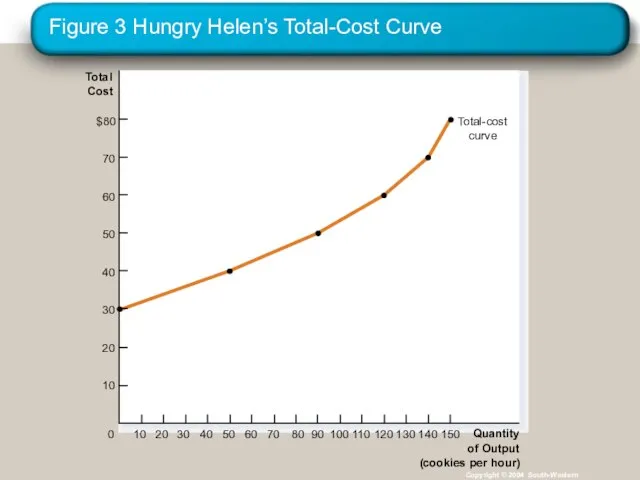

Слайд 20Figure 3 Hungry Helen’s Total-Cost Curve

Copyright © 2004 South-Western

Total

Cost

$80

70

60

50

40

30

20

10

Quantity

of Output

(cookies per hour)

0

10

20

30

150

130

110

90

70

50

40

140

120

100

80

60

Figure 3 Hungry Helen’s Total-Cost Curve

Copyright © 2004 South-Western

Total

Cost

$80

70

60

50

40

30

20

10

Quantity

of Output

(cookies per hour)

0

10

20

30

150

130

110

90

70

50

40

140

120

100

80

60

Слайд 21THE VARIOUS MEASURES OF COST

Costs of production may be divided into fixed

THE VARIOUS MEASURES OF COST

Costs of production may be divided into fixed

Слайд 22Fixed and Variable Costs

Fixed costs are those costs that do not vary

Fixed and Variable Costs

Fixed costs are those costs that do not vary

Слайд 23Fixed and Variable Costs

Total Costs

Total Fixed Costs (TFC)

Total Variable Costs (TVC)

Total Costs

Fixed and Variable Costs

Total Costs

Total Fixed Costs (TFC)

Total Variable Costs (TVC)

Total Costs

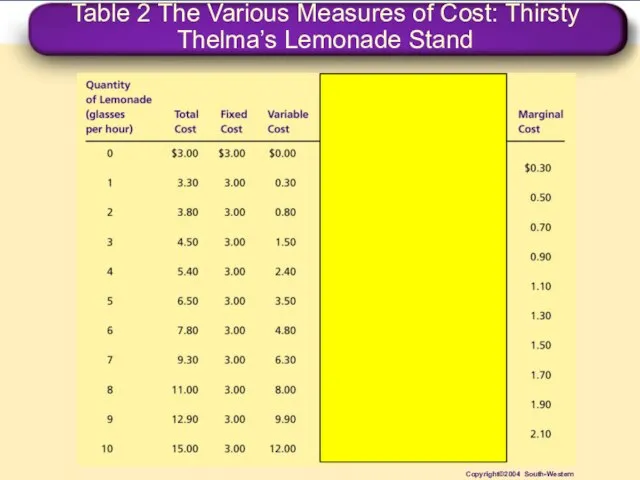

Слайд 24Table 2 The Various Measures of Cost: Thirsty Thelma’s Lemonade Stand

Copyright©2004 South-Western

Table 2 The Various Measures of Cost: Thirsty Thelma’s Lemonade Stand

Copyright©2004 South-Western

Слайд 25Fixed and Variable Costs

Average Costs

Average costs can be determined by dividing the

Fixed and Variable Costs

Average Costs

Average costs can be determined by dividing the

Слайд 26Fixed and Variable Costs

Average Costs

Average Fixed Costs (AFC)

Average Variable Costs (AVC)

Average Total

Fixed and Variable Costs

Average Costs

Average Fixed Costs (AFC)

Average Variable Costs (AVC)

Average Total

Слайд 27Average Costs

Average Costs

Слайд 28Table 2 The Various Measures of Cost: Thirsty Thelma’s Lemonade Stand

Copyright©2004 South-Western

Table 2 The Various Measures of Cost: Thirsty Thelma’s Lemonade Stand

Copyright©2004 South-Western

Слайд 29Fixed and Variable Costs

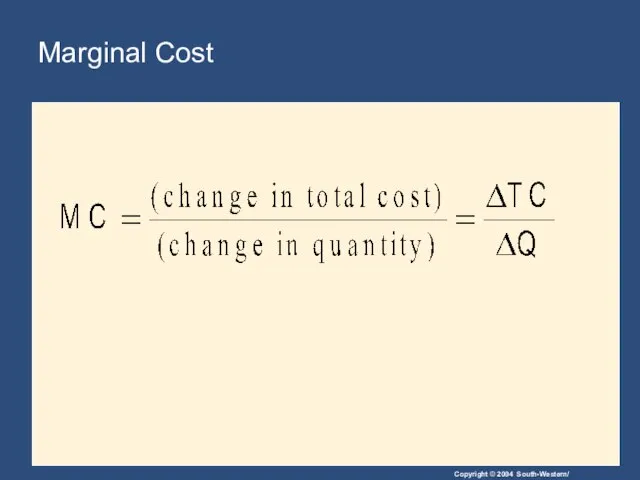

Marginal Cost

Marginal cost (MC) measures the increase in total

Fixed and Variable Costs

Marginal Cost

Marginal cost (MC) measures the increase in total

Слайд 30Marginal Cost

Marginal Cost

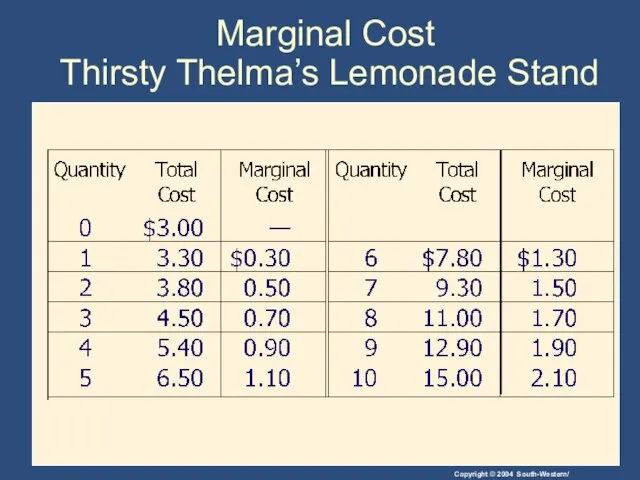

Слайд 31Marginal Cost

Thirsty Thelma’s Lemonade Stand

Marginal Cost

Thirsty Thelma’s Lemonade Stand

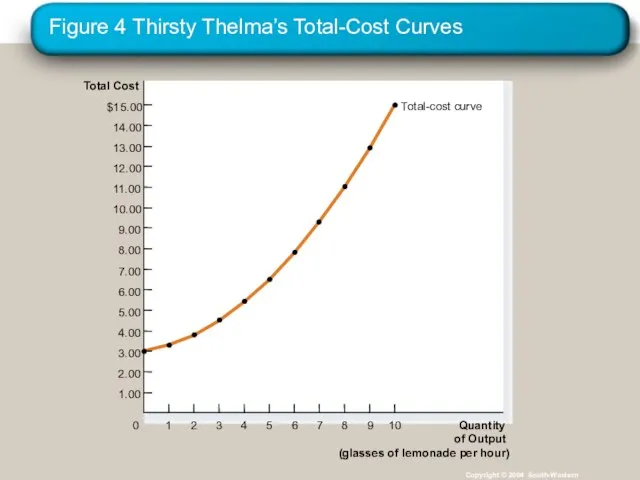

Слайд 32Figure 4 Thirsty Thelma’s Total-Cost Curves

Copyright © 2004 South-Western

Total Cost

$15.00

14.00

13.00

12.00

11.00

10.00

9.00

8.00

7.00

6.00

5.00

4.00

3.00

2.00

1.00

Quantity

of Output

(glasses of

Figure 4 Thirsty Thelma’s Total-Cost Curves

Copyright © 2004 South-Western

Total Cost

$15.00

14.00

13.00

12.00

11.00

10.00

9.00

8.00

7.00

6.00

5.00

4.00

3.00

2.00

1.00

Quantity

of Output

(glasses of

Слайд 33Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of Output

(glasses

Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of Output

(glasses

Слайд 34Cost Curves and Their Shapes

Marginal cost rises with the amount of output

Cost Curves and Their Shapes

Marginal cost rises with the amount of output

Слайд 35Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of Output

(glasses

Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of Output

(glasses

Слайд 36Cost Curves and Their Shapes

The average total-cost curve is U-shaped.

At very low

Cost Curves and Their Shapes

The average total-cost curve is U-shaped.

At very low

Слайд 37Cost Curves and Their Shapes

The bottom of the U-shaped ATC curve occurs

Cost Curves and Their Shapes

The bottom of the U-shaped ATC curve occurs

Слайд 38Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of Output

(glasses

Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of Output

(glasses

Слайд 39Cost Curves and Their Shapes

Relationship between Marginal Cost and Average Total

Cost Curves and Their Shapes

Relationship between Marginal Cost and Average Total

Слайд 40Cost Curves and Their Shapes

Relationship Between Marginal Cost and Average Total

Cost Curves and Their Shapes

Relationship Between Marginal Cost and Average Total

Слайд 41Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of Output

(glasses

Figure 5 Thirsty Thelma’s Average-Cost and Marginal-Cost Curves

Copyright © 2004 South-Western

Costs

$3.50

3.25

3.00

2.75

2.50

2.25

2.00

1.75

1.50

1.25

1.00

0.75

0.50

0.25

Quantity

of Output

(glasses

Слайд 42Typical Cost Curves

It is now time to examine the relationships that exist

Typical Cost Curves

It is now time to examine the relationships that exist

Слайд 43Big Bob’s Cost Curves

Big Bob’s Cost Curves

Слайд 44Figure 6 Big Bob’s Cost Curves

Copyright © 2004 South-Western

(a) Total-Cost Curve

$18.00

16.00

14.00

12.00

10.00

8.00

6.00

4.00

Quantity of

Figure 6 Big Bob’s Cost Curves

Copyright © 2004 South-Western

(a) Total-Cost Curve

$18.00

16.00

14.00

12.00

10.00

8.00

6.00

4.00

Quantity of

Слайд 45Figure 6 Big Bob’s Cost Curves

Copyright © 2004 South-Western

(b) Marginal- and Average-Cost

Figure 6 Big Bob’s Cost Curves

Copyright © 2004 South-Western

(b) Marginal- and Average-Cost

Слайд 46Typical Cost Curves

Three Important Properties of Cost Curves

Marginal cost eventually rises

Typical Cost Curves

Three Important Properties of Cost Curves

Marginal cost eventually rises

Слайд 47COSTS IN THE SHORT RUN AND IN THE LONG RUN

For many firms,

COSTS IN THE SHORT RUN AND IN THE LONG RUN

For many firms,

Слайд 48COSTS IN THE SHORT RUN AND IN THE LONG RUN

Because many costs

COSTS IN THE SHORT RUN AND IN THE LONG RUN

Because many costs

Слайд 49Figure 7 Average Total Cost in the Short and Long Run

Copyright ©

Figure 7 Average Total Cost in the Short and Long Run

Copyright ©

Слайд 50Economies and Diseconomies of Scale

Economies of scale refer to the property whereby

Economies and Diseconomies of Scale

Economies of scale refer to the property whereby

Слайд 51Figure 7 Average Total Cost in the Short and Long Run

Copyright ©

Figure 7 Average Total Cost in the Short and Long Run

Copyright ©

Слайд 52Summary

The goal of firms is to maximize profit, which equals total revenue

Summary

The goal of firms is to maximize profit, which equals total revenue

Слайд 53Summary

A firm’s costs reflect its production process.

A typical firm’s production function gets

Summary

A firm’s costs reflect its production process.

A typical firm’s production function gets

Слайд 54Summary

Average total cost is total cost divided by the quantity of output.

Marginal

Summary

Average total cost is total cost divided by the quantity of output.

Marginal

Khan Al-Khalili, Egypt (фотографии)

Khan Al-Khalili, Egypt (фотографии) Металлургический комплекс

Металлургический комплекс Жанры фольклора

Жанры фольклора Машиностроение. Значение отрасли

Машиностроение. Значение отрасли Планировка 0 этажа ТЦ Прага

Планировка 0 этажа ТЦ Прага основные примеры типологии общества

основные примеры типологии общества «Информатизация учебно – воспитательного процесса»

«Информатизация учебно – воспитательного процесса» Учет оплаты труда

Учет оплаты труда Презентация этикеток

Презентация этикеток Текст. Смысловая и композиционная целостность текста. Последовательность предложений в тексте.

Текст. Смысловая и композиционная целостность текста. Последовательность предложений в тексте. Vidy_soderzhanie_i_forma_konstruktorskih_dokumentov_7

Vidy_soderzhanie_i_forma_konstruktorskih_dokumentov_7 Что за чудо домовой?

Что за чудо домовой? Объект и пространство. От плоскостного изображения к объемному макету. Взаимосвязь объектов в архитектурном макете

Объект и пространство. От плоскостного изображения к объемному макету. Взаимосвязь объектов в архитектурном макете Проект Путь к цифре

Проект Путь к цифре Итоги 2011-2012 учебного года

Итоги 2011-2012 учебного года ПРИЗНАНИЕ И ПРИВЕДЕНИЕ В ИСПОЛНЕНИЕ ИНОСТРАННЫХ АРБИТРАЖНЫХ РЕШЕНИЙ НА ТЕРРИТОРИИ РОССИЙСКОЙ ФЕДЕРАЦИИ

ПРИЗНАНИЕ И ПРИВЕДЕНИЕ В ИСПОЛНЕНИЕ ИНОСТРАННЫХ АРБИТРАЖНЫХ РЕШЕНИЙ НА ТЕРРИТОРИИ РОССИЙСКОЙ ФЕДЕРАЦИИ Урачыстая лінейка. Дзень ведаў 2017

Урачыстая лінейка. Дзень ведаў 2017 От Таможенного союза к Единому экономическому пространству

От Таможенного союза к Единому экономическому пространству Расшифруй название сказки

Расшифруй название сказки Каталог №6 Beauty Awards

Каталог №6 Beauty Awards Российский народ (4 класс)

Российский народ (4 класс) The International Structure of Words

The International Structure of Words Новая форма МЧС России

Новая форма МЧС России Шаблон для проведения дня матери

Шаблон для проведения дня матери ВЛИЯНИЕ ИЗМЕНЕНИЯ КРИВОЙ ФИЗИЧЕСКОГО БИОРИТМА НА АКТИВНОСТЬ СТУДЕНТОВ ПЕРВОГО КУРСА УЧЕБНО-ИССЛЕДОВАТЕЛЬСКАЯ РАБОТА

ВЛИЯНИЕ ИЗМЕНЕНИЯ КРИВОЙ ФИЗИЧЕСКОГО БИОРИТМА НА АКТИВНОСТЬ СТУДЕНТОВ ПЕРВОГО КУРСА УЧЕБНО-ИССЛЕДОВАТЕЛЬСКАЯ РАБОТА Маленький принц

Маленький принц RENTAL COMPANY EFFECTIVE MANAGEMENT Эффективное управление арендной компанией

RENTAL COMPANY EFFECTIVE MANAGEMENT Эффективное управление арендной компанией Интернет-портал «Мобильные новости»Mnovosti.ru

Интернет-портал «Мобильные новости»Mnovosti.ru