- Fixed capital

Содержание

- 2. Content: Fixed Assets: general description, structure and classification Evaluation of Fixed Assets Deterioration and Amortization of

- 3. Legislative Acts: Clauses of The Accounting Standard #7 “Fixed Assets” (The Ministry`s of Finance of Ukraine

- 4. Fixed Capital Business Capital – The money, property, and other valuables which collectively represent the wealth

- 5. Fixed Capital Fixed Capital – Amount of business Capital, invested in all its Fixed Assets. Non-current

- 6. According to The Accounting Standard №7 Fixed assets – tangible assets, which are used in business

- 7. The Group of Fixed Assets Group of Fixed Assets – is a sum-total of single-type technical

- 8. Fixed Assets can be classified by the following signs - 1: Participation in Business Activity: Production

- 9. Fixed Assets can be classified by the following signs - 2: By purposes: Land, Capital costs

- 10. Fixed Assets can be classified by the following signs - 3: By Property: Private, Involved (f.e.,

- 11. Fixed Assets can be classified by the following signs - 4: By Amortization charge rate for

- 12. Fixed Assets are evaluated by: Original cost; Revaluation cost; Fair value; Book value; Residual value; Net

- 13. Original cost The total costs, associated with the purchase of an asset, for accounting purposes.

- 14. Original cost includes: The money business pays to suppliers or contractors for obtaining of the fixed

- 15. Revaluation cost: The cost of fixed assets after the process of reappraisal.

- 16. Indexing of Fixed Assets: Business has a right to apply annual indexing of the fixed assets

- 17. Fair Value: Rational and unbiased estimate of the potential market price of asset, taking into account

- 18. Book value: Can also be defined as deterioration adjustment, using formula Vb = Vo – Det.,

- 19. Net liquidation value: Responds to the fair value of assets excluding prospective sale costs.

- 20. Salvage value: the remaining value of an asset after it has been fully depreciated. It is

- 21. Average annual Production Fixed Assets Value FApVaa = Vbeg. + (Vpo. * k/12) – (Vp out

- 22. Deterioration and Obsolescence Deterioration – gradual loss of consumer value by non-tangible assets during operation. Obsolescence

- 23. According to the Accounting Standard №7: Depreciation – systematic amortized value of non-tangible assets carry-forward during

- 24. Object of Depreciation Object of Depreciation includes the value of fixed assets (except value of lands

- 25. Useful life of Assets Useful life of Assets – is an expected period of time, during

- 26. When defining the term of Assets` Useful life consideration must be given to: Expected using of

- 27. Useful life`s Term (Exploitation) of an Object Useful life`s Term (Exploitation) of the Fixed Assets is

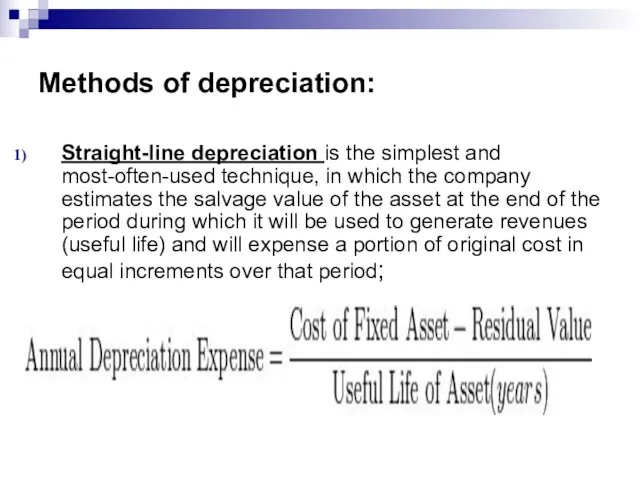

- 28. Methods of depreciation: Straight-line depreciation is the simplest and most-often-used technique, in which the company estimates

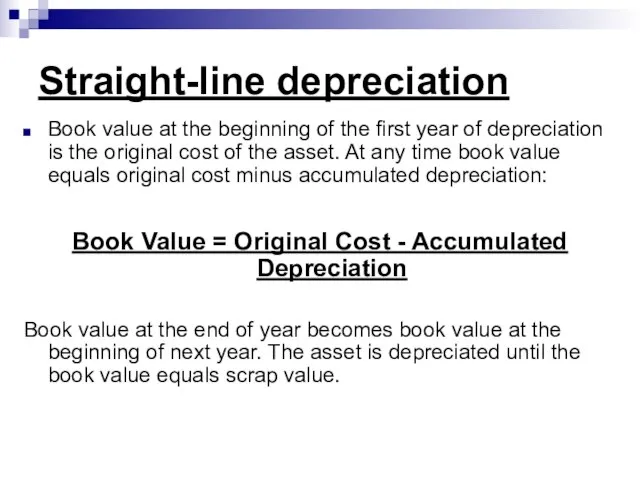

- 29. Straight-line depreciation Book value at the beginning of the first year of depreciation is the original

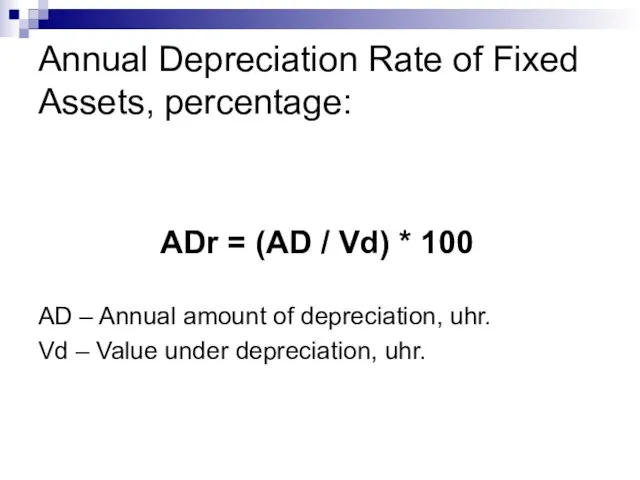

- 30. Annual Depreciation Rate of Fixed Assets, percentage: ADr = (AD / Vd) * 100 AD –

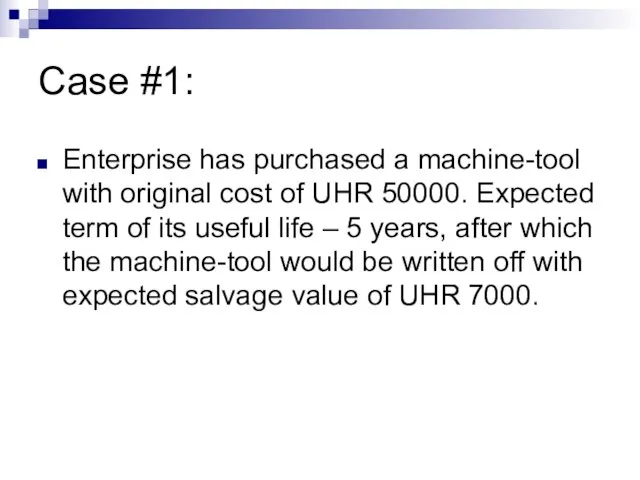

- 31. Case #1: Enterprise has purchased a machine-tool with original cost of UHR 50000. Expected term of

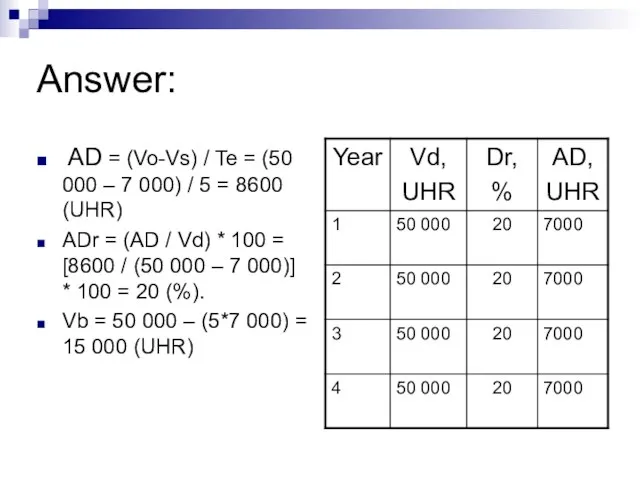

- 32. Answer: AD = (Vo-Vs) / Te = (50 000 – 7 000) / 5 = 8600

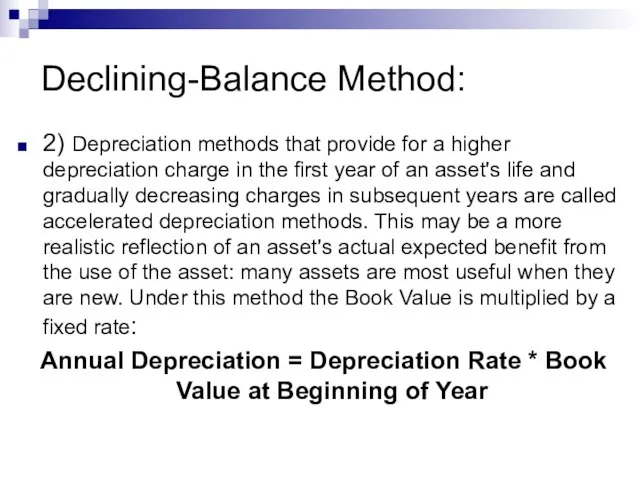

- 33. Declining-Balance Method: 2) Depreciation methods that provide for a higher depreciation charge in the first year

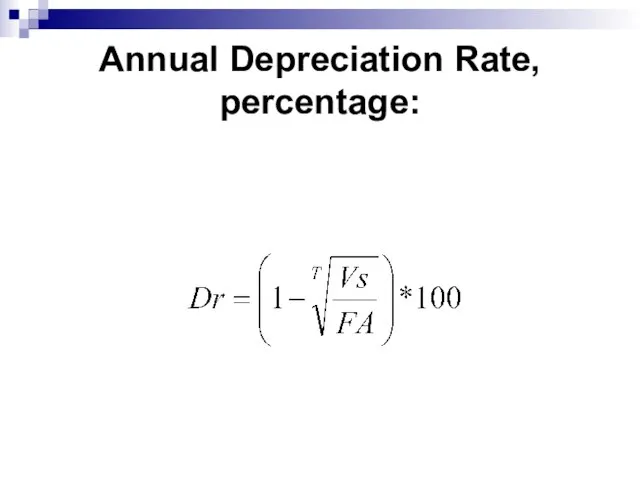

- 34. Annual Depreciation Rate, percentage:

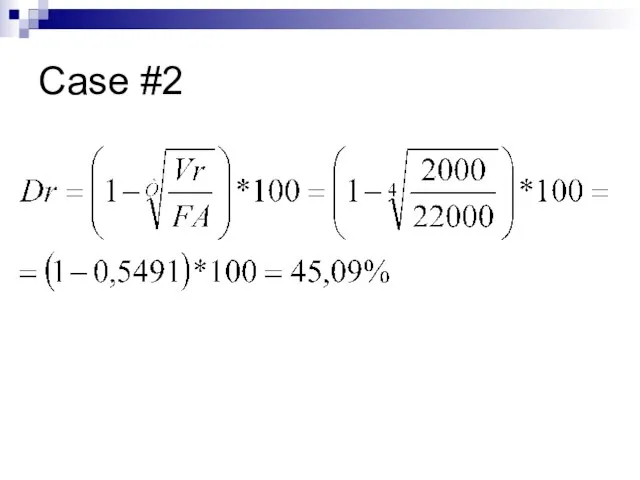

- 35. Case #2

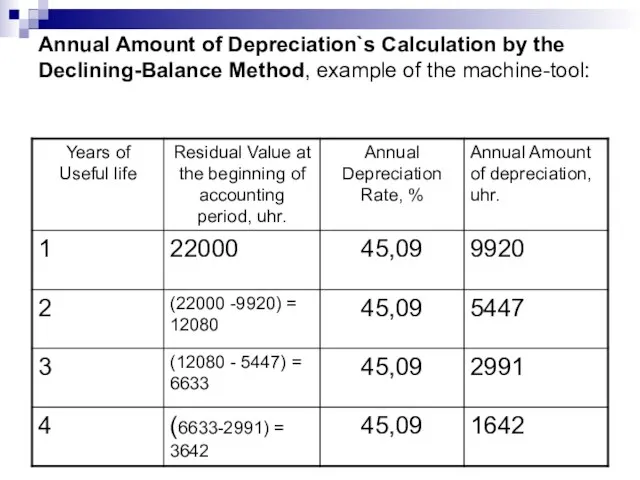

- 36. Annual Amount of Depreciation`s Calculation by the Declining-Balance Method, example of the machine-tool:

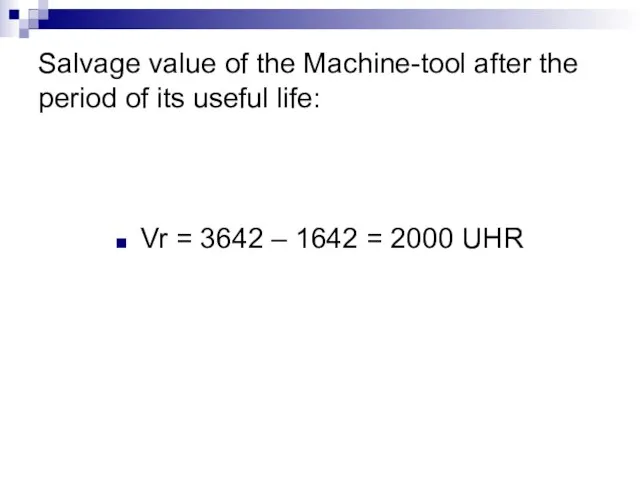

- 37. Salvage value of the Machine-tool after the period of its useful life: Vr = 3642 –

- 38. Method of the Book Value Accelerated decrease: 3) Method of the Book Value Accelerated decrease, which

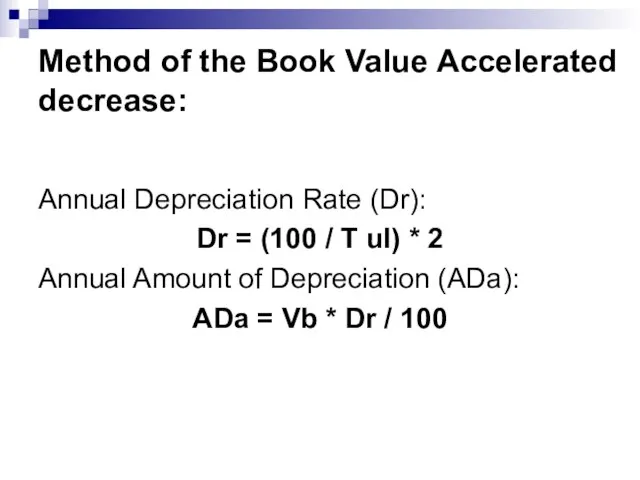

- 39. Method of the Book Value Accelerated decrease: Annual Depreciation Rate (Dr): Dr = (100 / T

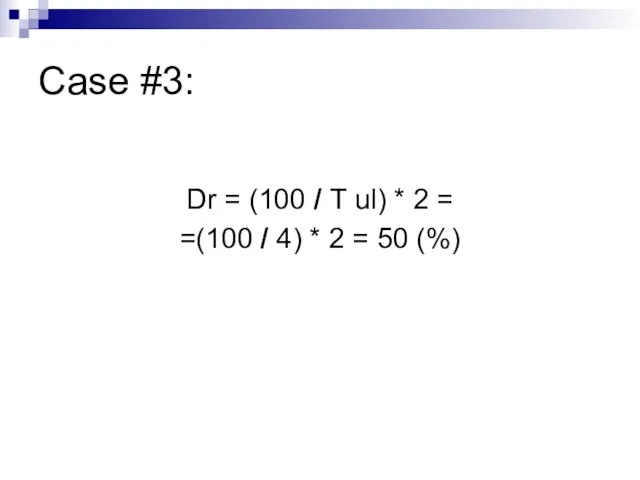

- 40. Case #3: Dr = (100 / Т ul) * 2 = =(100 / 4) * 2

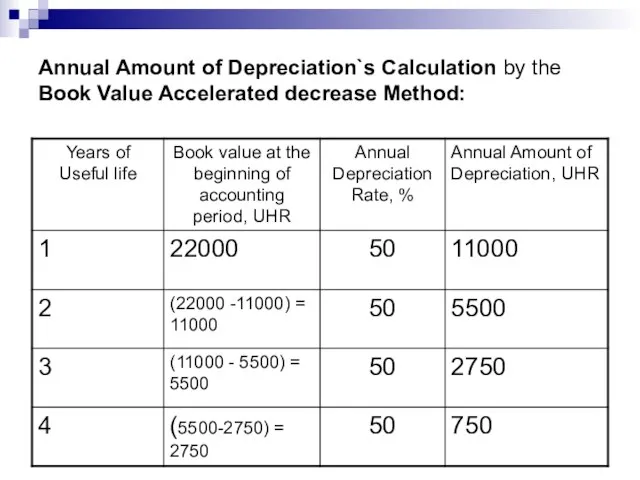

- 41. Annual Amount of Depreciation`s Calculation by the Book Value Accelerated decrease Method:

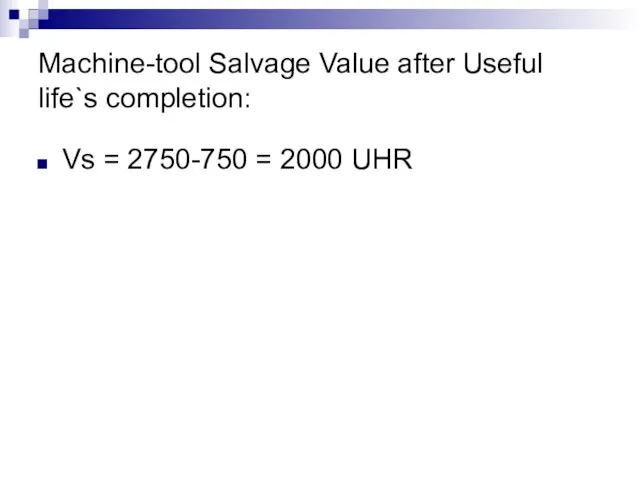

- 42. Machine-tool Salvage Value after Useful life`s completion: Vs = 2750-750 = 2000 UHR

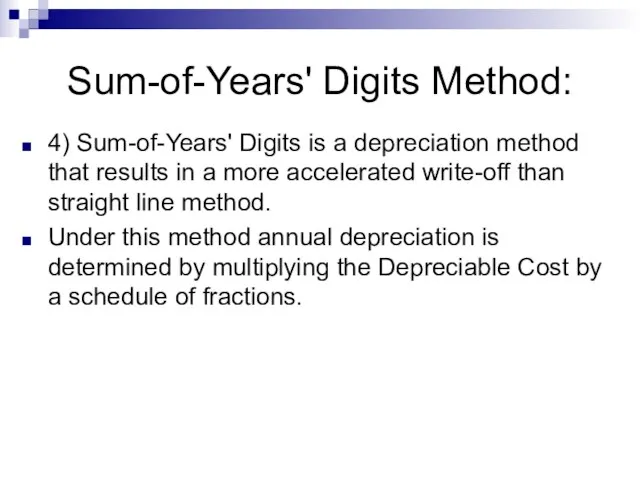

- 43. Sum-of-Years' Digits Method: 4) Sum-of-Years' Digits is a depreciation method that results in a more accelerated

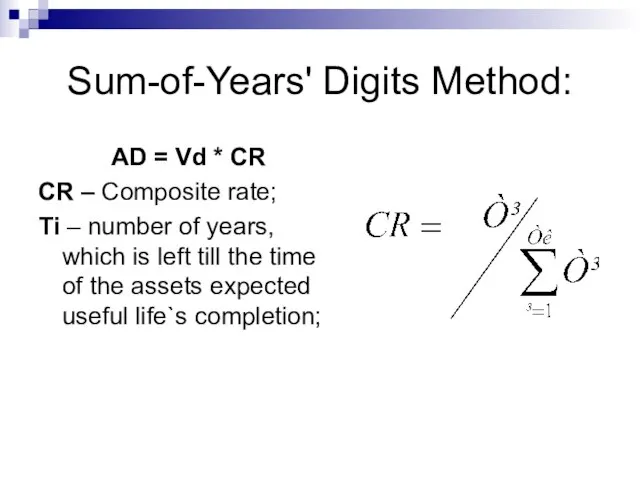

- 44. Sum-of-Years' Digits Method: AD = Vd * CR CR – Composite rate; Ті – number of

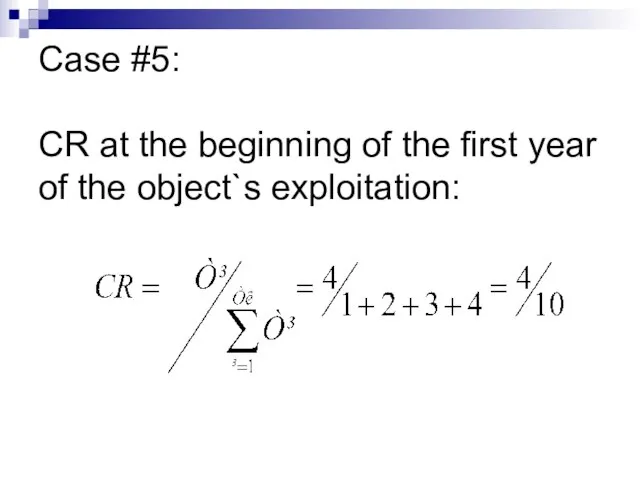

- 45. Case #5: CR at the beginning of the first year of the object`s exploitation:

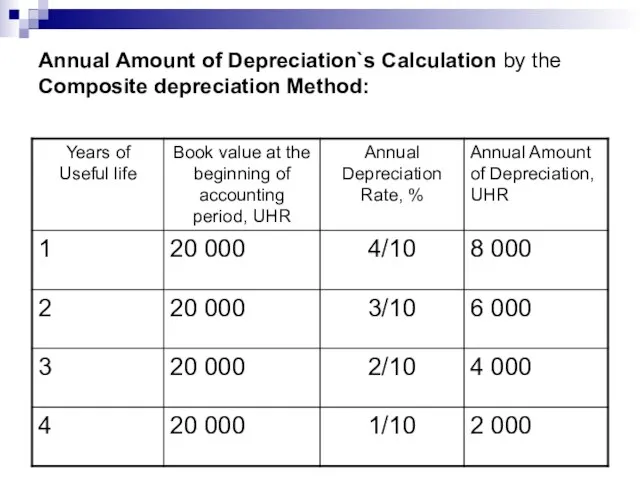

- 46. Annual Amount of Depreciation`s Calculation by the Composite depreciation Method:

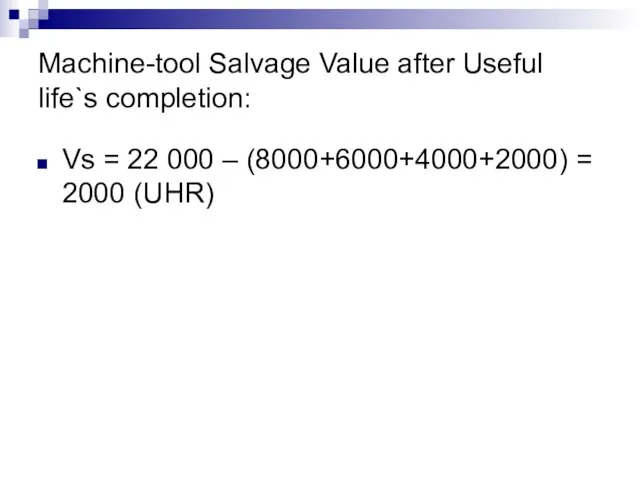

- 47. Machine-tool Salvage Value after Useful life`s completion: Vs = 22 000 – (8000+6000+4000+2000) = 2000 (UHR)

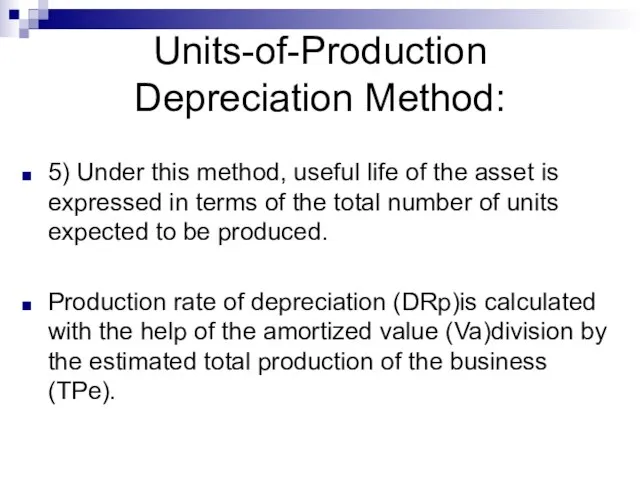

- 48. Units-of-Production Depreciation Method: 5) Under this method, useful life of the asset is expressed in terms

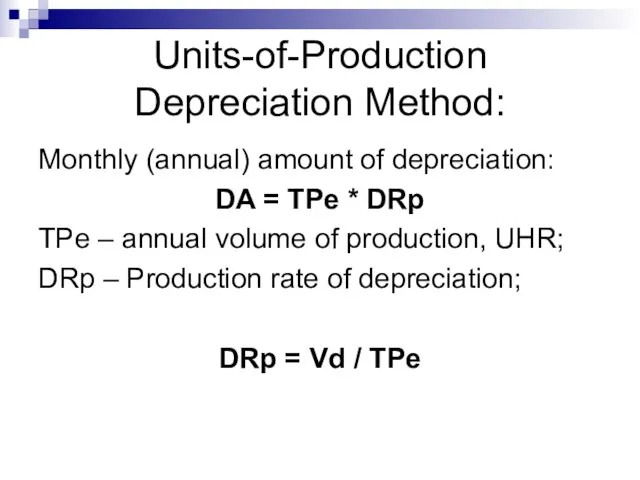

- 49. Units-of-Production Depreciation Method: Monthly (annual) amount of depreciation: DA = TPe * DRp TPe – annual

- 50. Case #6: Let`s apply Units-of-Production Depreciation Method in order to calculate depreciation charges by the years

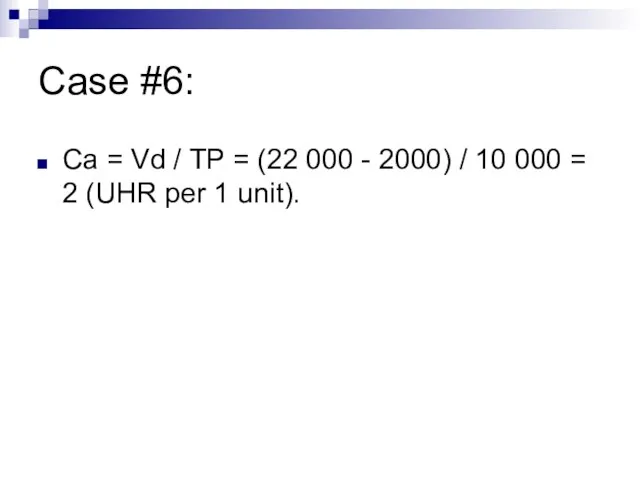

- 51. Case #6: Са = Vd / TP = (22 000 - 2000) / 10 000 =

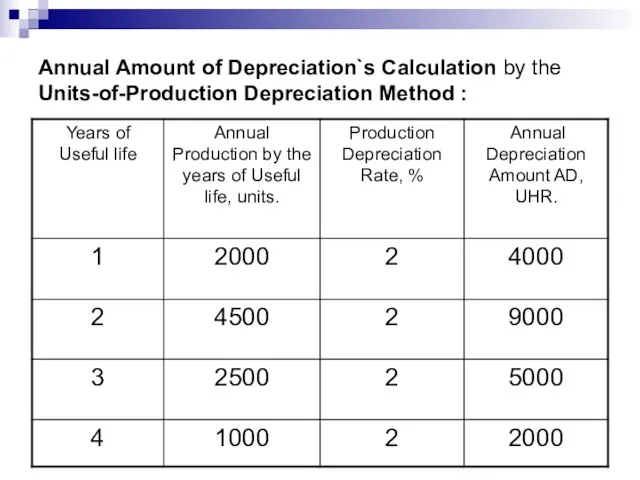

- 52. Annual Amount of Depreciation`s Calculation by the Units-of-Production Depreciation Method :

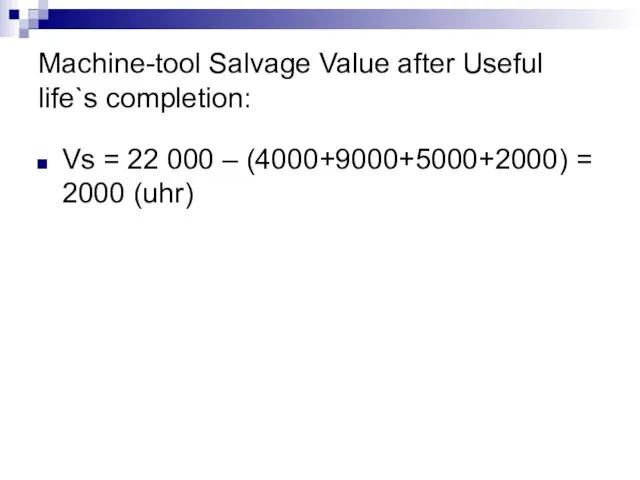

- 53. Machine-tool Salvage Value after Useful life`s completion: Vs = 22 000 – (4000+9000+5000+2000) = 2000 (uhr)

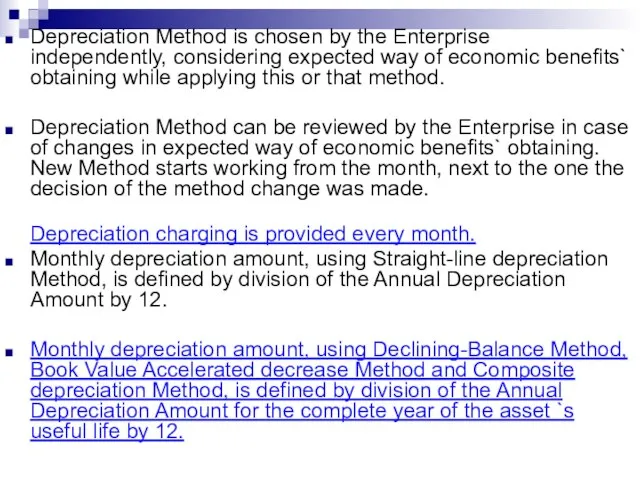

- 54. Depreciation Method is chosen by the Enterprise independently, considering expected way of economic benefits` obtaining while

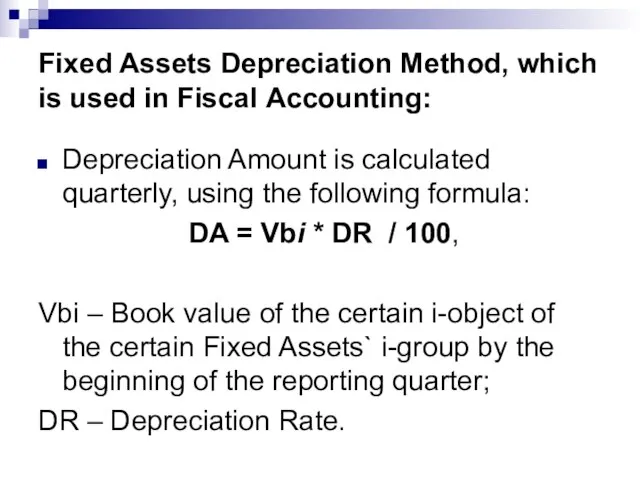

- 55. Fixed Assets Depreciation Method, which is used in Fiscal Accounting: Depreciation Amount is calculated quarterly, using

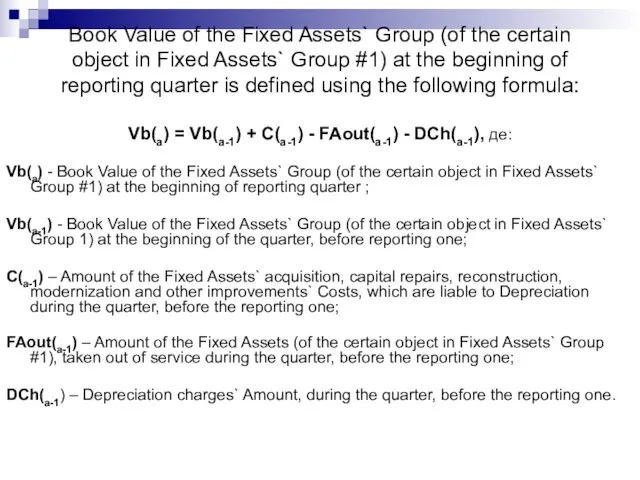

- 56. Book Value of the Fixed Assets` Group (of the certain object in Fixed Assets` Group #1)

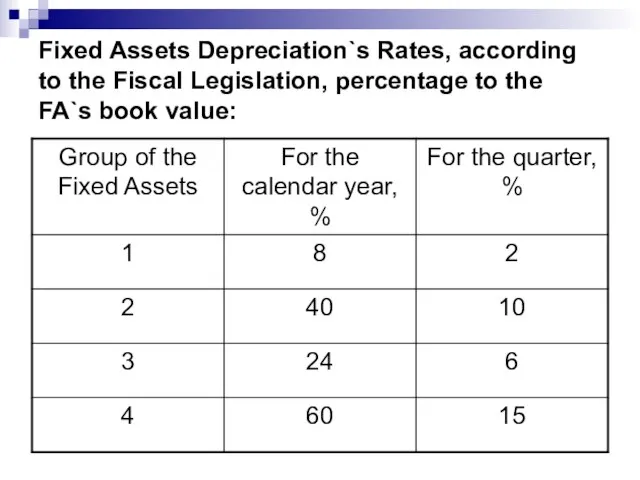

- 57. Fixed Assets Depreciation`s Rates, according to the Fiscal Legislation, percentage to the FA`s book value:

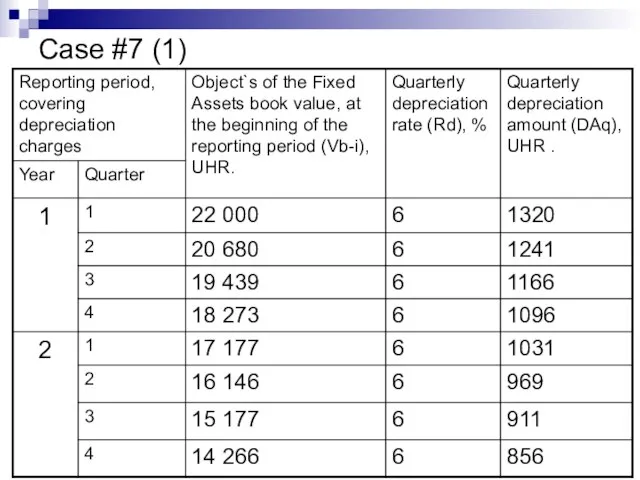

- 58. Case #7 (1)

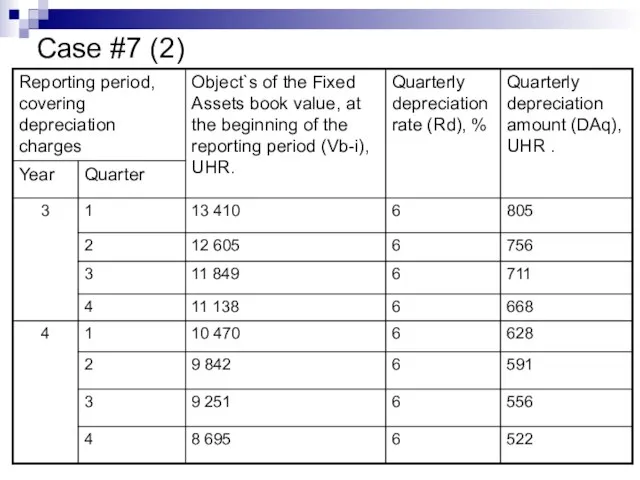

- 59. Case #7 (2)

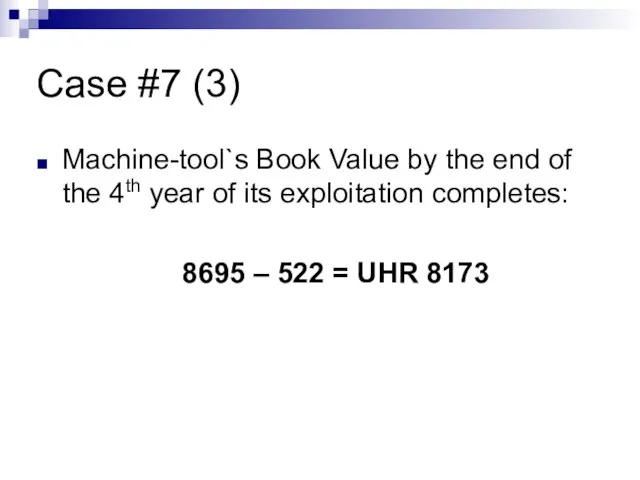

- 60. Case #7 (3) Machine-tool`s Book Value by the end of the 4th year of its exploitation

- 61. 4. Indicators of Fixed Assets` provision, condition and efficiency

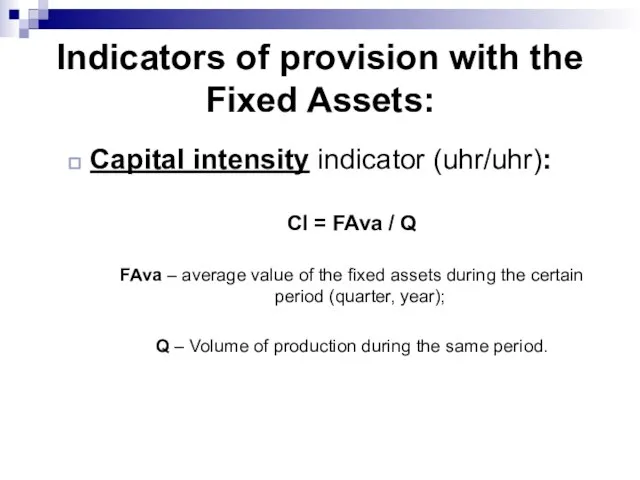

- 62. Indicators of provision with the Fixed Assets: Capital intensity indicator (uhr/uhr): CI = FAva / Q

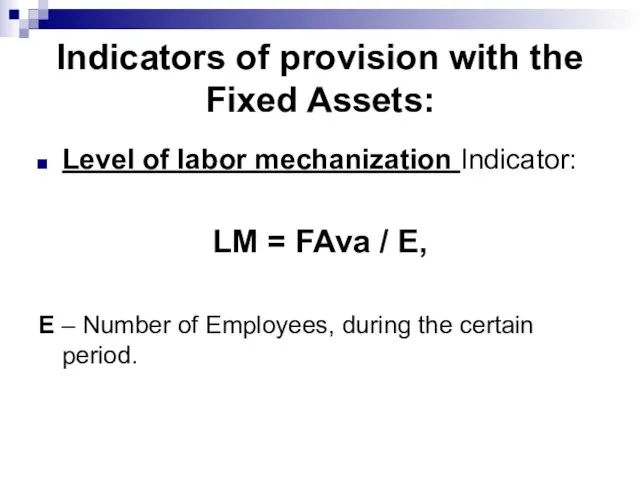

- 63. Indicators of provision with the Fixed Assets: Level of labor mechanization Indicator: LM = FAva /

- 64. Indicators of provision with the Fixed Assets: Real value of the fixed productive assets is reflected

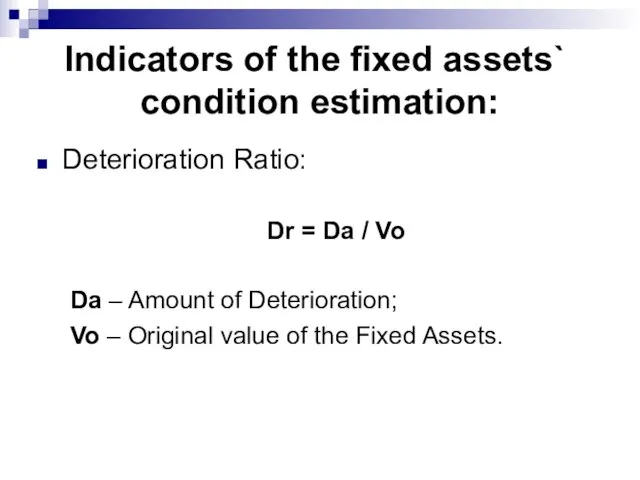

- 65. Indicators of the fixed assets` condition estimation: Deterioration Ratio: Dr = Da / Vo Da –

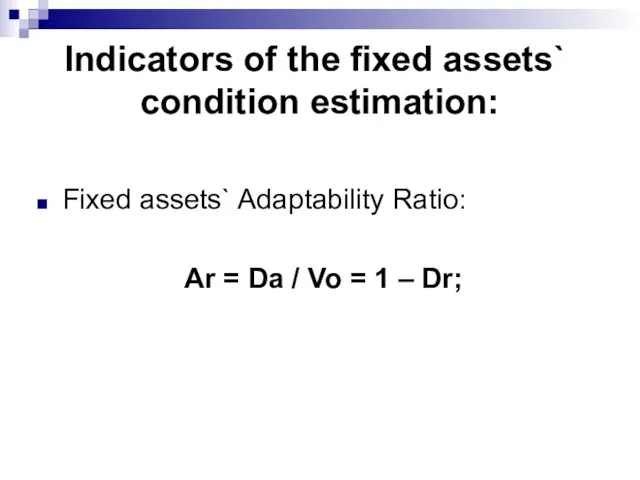

- 66. Indicators of the fixed assets` condition estimation: Fixed assets` Adaptability Ratio: Ar = Da / Vo

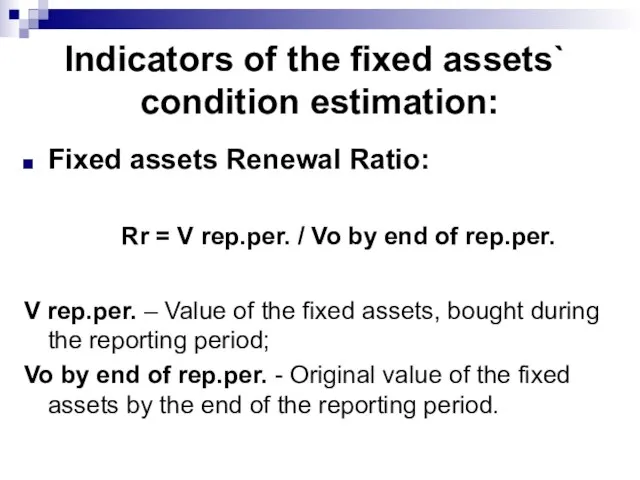

- 67. Indicators of the fixed assets` condition estimation: Fixed assets Renewal Ratio: Rr = V rep.per. /

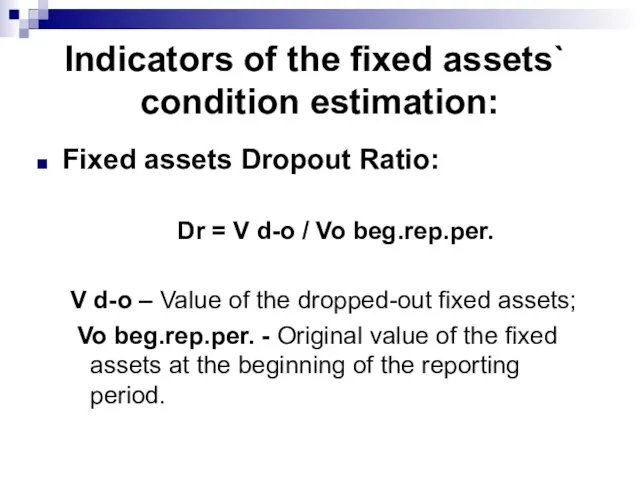

- 68. Indicators of the fixed assets` condition estimation: Fixed assets Dropout Ratio: Dr = V d-o /

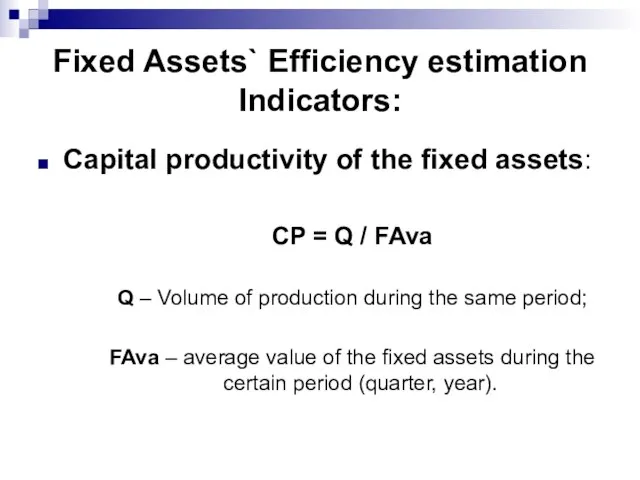

- 69. Fixed Assets` Efficiency estimation Indicators: Capital productivity of the fixed assets: CP = Q / FAva

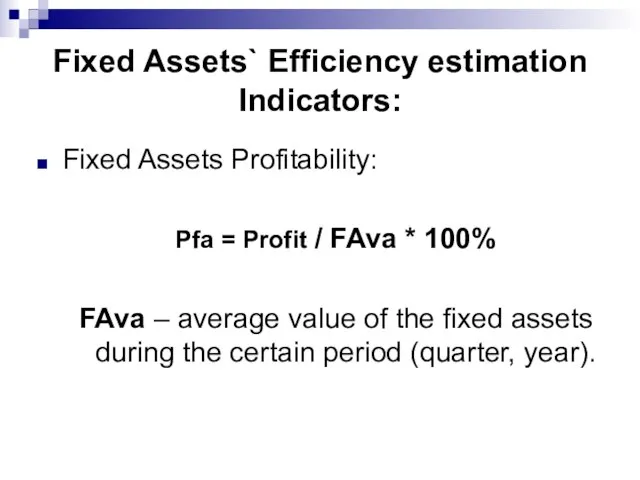

- 70. Fixed Assets` Efficiency estimation Indicators: Fixed Assets Profitability: Pfa = Profit / FAva * 100% FAva

- 72. Скачать презентацию

Слайд 2Content:

Fixed Assets: general description, structure and classification

Evaluation of Fixed Assets

Deterioration and Amortization

Content:

Fixed Assets: general description, structure and classification

Evaluation of Fixed Assets

Deterioration and Amortization

Слайд 3Legislative Acts:

Clauses of The Accounting Standard #7 “Fixed Assets” (The Ministry`s of

Legislative Acts:

Clauses of The Accounting Standard #7 “Fixed Assets” (The Ministry`s of

Слайд 4Fixed Capital

Business Capital – The money, property, and other valuables which collectively

Fixed Capital

Business Capital – The money, property, and other valuables which collectively

Слайд 5Fixed Capital

Fixed Capital – Amount of business Capital, invested in all its

Fixed Capital

Fixed Capital – Amount of business Capital, invested in all its

Слайд 6According to The Accounting Standard №7

Fixed assets – tangible assets, which are

According to The Accounting Standard №7

Fixed assets – tangible assets, which are

Слайд 7The Group of Fixed Assets

Group of Fixed Assets – is a sum-total

The Group of Fixed Assets

Group of Fixed Assets – is a sum-total

Слайд 8

Fixed Assets can be classified by the following signs - 1:

Participation in

Fixed Assets can be classified by the following signs - 1:

Participation in

Слайд 9Fixed Assets can be classified by the following signs - 2:

By

Fixed Assets can be classified by the following signs - 2:

By

Слайд 10Fixed Assets can be classified by the following signs - 3:

By Property:

Fixed Assets can be classified by the following signs - 3:

By Property:

Слайд 11Fixed Assets can be classified by the following signs - 4:

By Amortization

Fixed Assets can be classified by the following signs - 4:

By Amortization

Слайд 12Fixed Assets are evaluated by:

Original cost;

Revaluation cost;

Fair value;

Book value;

Residual value;

Net liquidation value;

Salvage

Fixed Assets are evaluated by:

Original cost;

Revaluation cost;

Fair value;

Book value;

Residual value;

Net liquidation value;

Salvage

Слайд 13

Original cost

The total costs, associated with the purchase of an asset, for

Original cost

The total costs, associated with the purchase of an asset, for

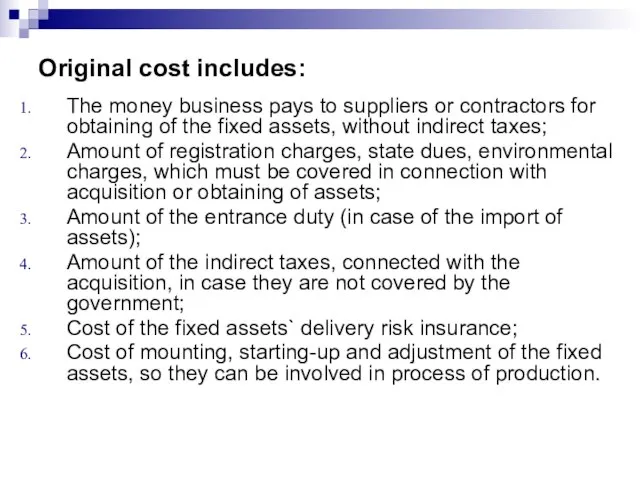

Слайд 14Original cost includes:

The money business pays to suppliers or contractors for obtaining

Original cost includes:

The money business pays to suppliers or contractors for obtaining

Слайд 15Revaluation cost:

The cost of fixed assets after the process of reappraisal.

Revaluation cost:

The cost of fixed assets after the process of reappraisal.

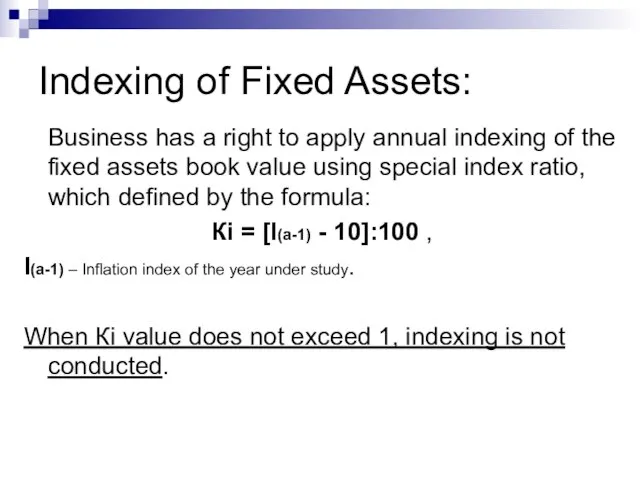

Слайд 16Indexing of Fixed Assets:

Business has a right to apply annual indexing of

Indexing of Fixed Assets:

Business has a right to apply annual indexing of

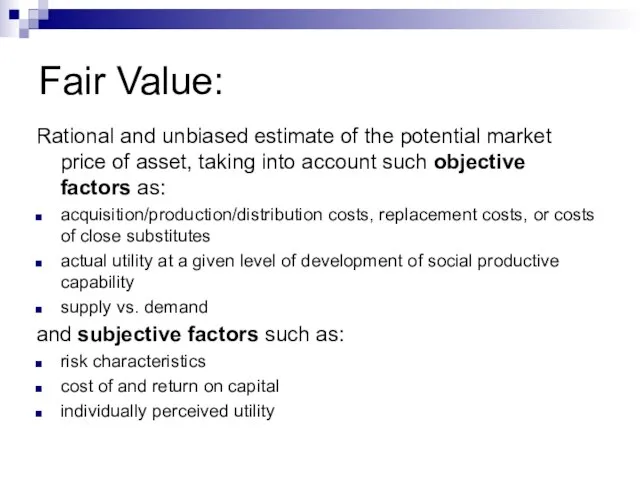

Слайд 17Fair Value:

Rational and unbiased estimate of the potential market price of asset,

Fair Value:

Rational and unbiased estimate of the potential market price of asset,

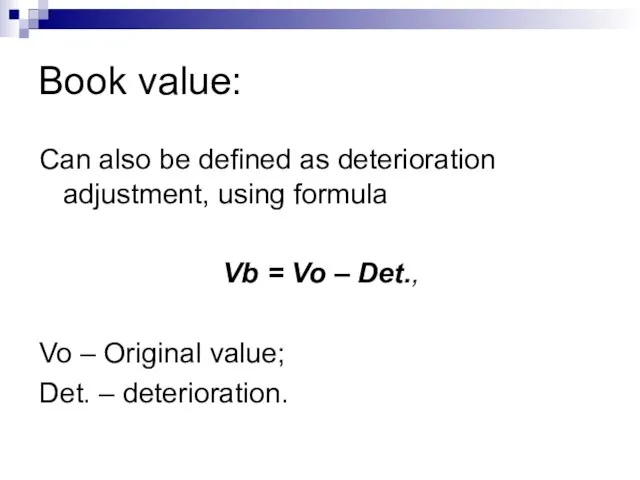

Слайд 18Book value:

Can also be defined as deterioration adjustment, using formula

Vb = Vo

Book value:

Can also be defined as deterioration adjustment, using formula

Vb = Vo

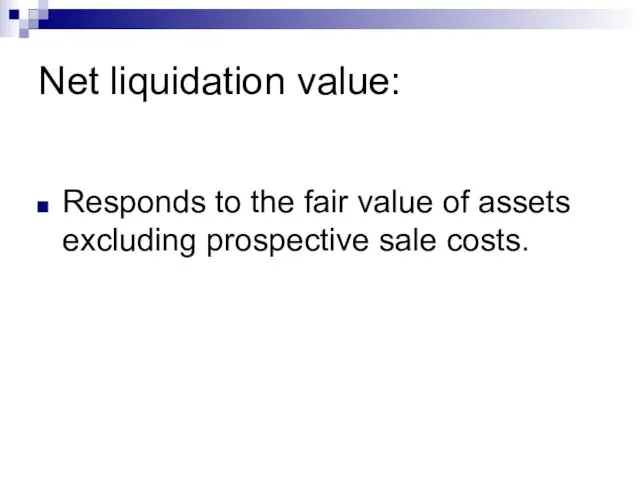

Слайд 19Net liquidation value:

Responds to the fair value of assets excluding prospective sale

Net liquidation value:

Responds to the fair value of assets excluding prospective sale

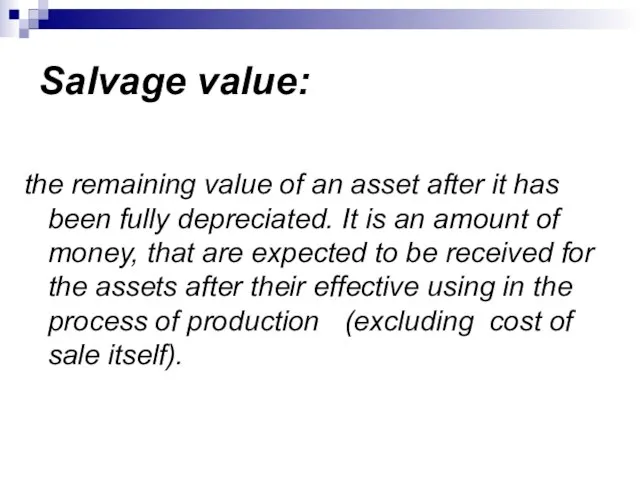

Слайд 20Salvage value:

the remaining value of an asset after it has been fully

Salvage value:

the remaining value of an asset after it has been fully

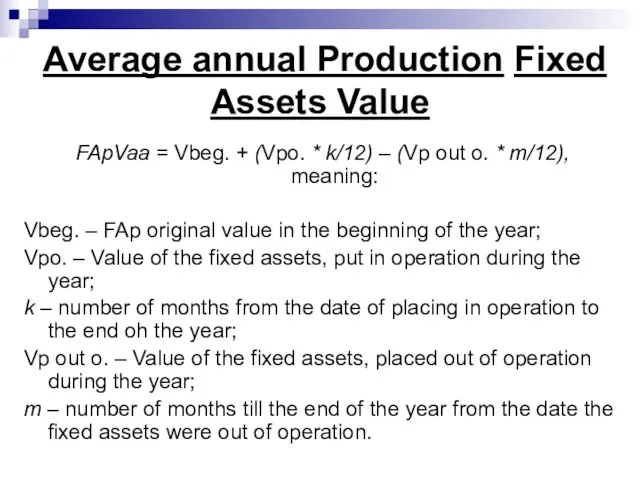

Слайд 21Average annual Production Fixed Assets Value

FApVaa = Vbeg. + (Vpo. * k/12)

Average annual Production Fixed Assets Value

FApVaa = Vbeg. + (Vpo. * k/12)

Слайд 22Deterioration and Obsolescence

Deterioration – gradual loss of consumer value by non-tangible assets

Deterioration and Obsolescence

Deterioration – gradual loss of consumer value by non-tangible assets

Слайд 23

According to the Accounting Standard №7:

Depreciation – systematic amortized value of non-tangible

According to the Accounting Standard №7:

Depreciation – systematic amortized value of non-tangible

Слайд 24Object of Depreciation

Object of Depreciation includes the value of fixed assets (except

Object of Depreciation

Object of Depreciation includes the value of fixed assets (except

Слайд 25Useful life of Assets

Useful life of Assets – is an expected period

Useful life of Assets

Useful life of Assets – is an expected period

Слайд 26When defining the term of Assets` Useful life consideration must be given

When defining the term of Assets` Useful life consideration must be given

Слайд 27Useful life`s Term (Exploitation) of an Object

Useful life`s Term (Exploitation) of the

Useful life`s Term (Exploitation) of an Object

Useful life`s Term (Exploitation) of the

Слайд 28Methods of depreciation:

Straight-line depreciation is the simplest and most-often-used technique, in

Methods of depreciation:

Straight-line depreciation is the simplest and most-often-used technique, in

Слайд 29Straight-line depreciation

Book value at the beginning of the first year of depreciation

Straight-line depreciation

Book value at the beginning of the first year of depreciation

Слайд 30Annual Depreciation Rate of Fixed Assets, percentage:

ADr = (AD / Vd) *

Annual Depreciation Rate of Fixed Assets, percentage:

ADr = (AD / Vd) *

Слайд 31Case #1:

Enterprise has purchased a machine-tool with original cost of UHR 50000.

Case #1:

Enterprise has purchased a machine-tool with original cost of UHR 50000.

Слайд 32Answer:

AD = (Vo-Vs) / Te = (50 000 – 7 000)

Answer:

AD = (Vo-Vs) / Te = (50 000 – 7 000)

Слайд 33Declining-Balance Method:

2) Depreciation methods that provide for a higher depreciation charge in

Declining-Balance Method:

2) Depreciation methods that provide for a higher depreciation charge in

Слайд 34Annual Depreciation Rate, percentage:

Annual Depreciation Rate, percentage:

Слайд 35Case #2

Case #2

Слайд 36Annual Amount of Depreciation`s Calculation by the Declining-Balance Method, example of the

Annual Amount of Depreciation`s Calculation by the Declining-Balance Method, example of the

Слайд 37Salvage value of the Machine-tool after the period of its useful life:

Vr

Salvage value of the Machine-tool after the period of its useful life:

Vr

Слайд 38Method of the Book Value Accelerated decrease:

3) Method of the Book Value

Method of the Book Value Accelerated decrease:

3) Method of the Book Value

Слайд 39Method of the Book Value Accelerated decrease:

Annual Depreciation Rate (Dr):

Dr = (100

Method of the Book Value Accelerated decrease:

Annual Depreciation Rate (Dr):

Dr = (100

Слайд 40Case #3:

Dr = (100 / Т ul) * 2 =

=(100 /

Case #3:

Dr = (100 / Т ul) * 2 =

=(100 /

Слайд 41Annual Amount of Depreciation`s Calculation by the Book Value Accelerated decrease Method:

Annual Amount of Depreciation`s Calculation by the Book Value Accelerated decrease Method:

Слайд 42Machine-tool Salvage Value after Useful life`s completion:

Vs = 2750-750 = 2000 UHR

Machine-tool Salvage Value after Useful life`s completion:

Vs = 2750-750 = 2000 UHR

Слайд 43Sum-of-Years' Digits Method:

4) Sum-of-Years' Digits is a depreciation method that results in

Sum-of-Years' Digits Method:

4) Sum-of-Years' Digits is a depreciation method that results in

Слайд 44Sum-of-Years' Digits Method:

AD = Vd * CR

CR – Composite rate;

Ті – number

Sum-of-Years' Digits Method:

AD = Vd * CR

CR – Composite rate;

Ті – number

Слайд 45

Case #5:

CR at the beginning of the first year of the

Case #5: CR at the beginning of the first year of the

Слайд 46Annual Amount of Depreciation`s Calculation by the Composite depreciation Method:

Annual Amount of Depreciation`s Calculation by the Composite depreciation Method:

Слайд 47Machine-tool Salvage Value after Useful life`s completion:

Vs = 22 000 – (8000+6000+4000+2000)

Machine-tool Salvage Value after Useful life`s completion:

Vs = 22 000 – (8000+6000+4000+2000)

Слайд 48

Units-of-Production Depreciation Method:

5) Under this method, useful life of the asset is

Units-of-Production Depreciation Method:

5) Under this method, useful life of the asset is

Слайд 49

Units-of-Production Depreciation Method:

Monthly (annual) amount of depreciation:

DA = TPe * DRp

TPe –

Units-of-Production Depreciation Method:

Monthly (annual) amount of depreciation:

DA = TPe * DRp

TPe –

Слайд 50Case #6:

Let`s apply Units-of-Production Depreciation Method in order to calculate depreciation charges

Case #6:

Let`s apply Units-of-Production Depreciation Method in order to calculate depreciation charges

Слайд 51Case #6:

Са = Vd / TP = (22 000 - 2000) /

Case #6:

Са = Vd / TP = (22 000 - 2000) /

Слайд 52Annual Amount of Depreciation`s Calculation by the Units-of-Production Depreciation Method :

Annual Amount of Depreciation`s Calculation by the Units-of-Production Depreciation Method :

Слайд 53Machine-tool Salvage Value after Useful life`s completion:

Vs = 22 000 – (4000+9000+5000+2000)

Machine-tool Salvage Value after Useful life`s completion:

Vs = 22 000 – (4000+9000+5000+2000)

Слайд 54Depreciation Method is chosen by the Enterprise independently, considering expected way of

Слайд 55Fixed Assets Depreciation Method, which is used in Fiscal Accounting:

Depreciation Amount is

Fixed Assets Depreciation Method, which is used in Fiscal Accounting:

Depreciation Amount is

Слайд 56

Book Value of the Fixed Assets` Group (of the certain object in

Book Value of the Fixed Assets` Group (of the certain object in

Слайд 57Fixed Assets Depreciation`s Rates, according to the Fiscal Legislation, percentage to the

Fixed Assets Depreciation`s Rates, according to the Fiscal Legislation, percentage to the

Слайд 58Case #7 (1)

Case #7 (1)

Слайд 59Case #7 (2)

Case #7 (2)

Слайд 60Case #7 (3)

Machine-tool`s Book Value by the end of the 4th year

Case #7 (3)

Machine-tool`s Book Value by the end of the 4th year

Слайд 61

4. Indicators of Fixed Assets` provision, condition and efficiency

4. Indicators of Fixed Assets` provision, condition and efficiency

Слайд 62

Indicators of provision with the Fixed Assets:

Capital intensity indicator (uhr/uhr):

CI = FAva

Indicators of provision with the Fixed Assets:

Capital intensity indicator (uhr/uhr):

CI = FAva

Слайд 63

Indicators of provision with the Fixed Assets:

Level of labor mechanization Indicator:

LM =

Indicators of provision with the Fixed Assets:

Level of labor mechanization Indicator:

LM =

Слайд 64

Indicators of provision with the Fixed Assets:

Real value of the fixed

Indicators of provision with the Fixed Assets:

Real value of the fixed

Слайд 65Indicators of the fixed assets` condition estimation:

Deterioration Ratio:

Dr = Da / Vo

Da

Indicators of the fixed assets` condition estimation:

Deterioration Ratio:

Dr = Da / Vo

Da

Слайд 66Indicators of the fixed assets` condition estimation:

Fixed assets` Adaptability Ratio:

Ar =

Indicators of the fixed assets` condition estimation:

Fixed assets` Adaptability Ratio:

Ar =

Слайд 67Indicators of the fixed assets` condition estimation:

Fixed assets Renewal Ratio:

Rr = V

Indicators of the fixed assets` condition estimation:

Fixed assets Renewal Ratio:

Rr = V

Слайд 68Indicators of the fixed assets` condition estimation:

Fixed assets Dropout Ratio:

Dr = V

Indicators of the fixed assets` condition estimation:

Fixed assets Dropout Ratio:

Dr = V

Слайд 69Fixed Assets` Efficiency estimation Indicators:

Capital productivity of the fixed assets:

CP = Q

Fixed Assets` Efficiency estimation Indicators:

Capital productivity of the fixed assets:

CP = Q

Слайд 70Fixed Assets` Efficiency estimation Indicators:

Fixed Assets Profitability:

Pfa = Profit / FAva *

Fixed Assets` Efficiency estimation Indicators:

Fixed Assets Profitability:

Pfa = Profit / FAva *

Строевая стойка с оружием

Строевая стойка с оружием Правление Петра I

Правление Петра I Отечественная_война_1812_года

Отечественная_война_1812_года Региональный бюджет, финансовая и налоговая политика

Региональный бюджет, финансовая и налоговая политика HR Мотивация персонала

HR Мотивация персонала Подпотолочная роспись, Государственный Эрмитаж, Зал 121. К письменной экзаменационной работе

Подпотолочная роспись, Государственный Эрмитаж, Зал 121. К письменной экзаменационной работе Социальная работа с разными группами населения

Социальная работа с разными группами населения Оборотные средства организации

Оборотные средства организации Машины

Машины МОУ-Клинская средняя школа № 17Эссе по обществознанию:ТЕОРИЯ И ПРАКТИКААвтор: Романова Валентина Александровна

МОУ-Клинская средняя школа № 17Эссе по обществознанию:ТЕОРИЯ И ПРАКТИКААвтор: Романова Валентина Александровна Prilozhenie_1_k_individualnomu_zadaniyu_po_PM_01_shablon_dlya_zapolneniya

Prilozhenie_1_k_individualnomu_zadaniyu_po_PM_01_shablon_dlya_zapolneniya Сергей Есенин

Сергей Есенин Говорю «СПАСИБО»

Говорю «СПАСИБО» Деньги Сомали

Деньги Сомали Патент

Патент Презентация на тему Действия с векторами

Презентация на тему Действия с векторами Производственная структура предприятия

Производственная структура предприятия Романское искусство и его примеры

Романское искусство и его примеры Арктика

Арктика Гражданские правоотношения

Гражданские правоотношения Фруктовые деревья

Фруктовые деревья Невесомость предсказаная и неожиданная

Невесомость предсказаная и неожиданная Звук. Звуковые явления

Звук. Звуковые явления Логические основы компьютера

Логические основы компьютера Решение уравнений третьей степени

Решение уравнений третьей степени Реализация региональной программы профориентационной работы в Костромской области

Реализация региональной программы профориентационной работы в Костромской области Синтаксис коррелятивных конструкций русского языка с позиции генеративной грамматики

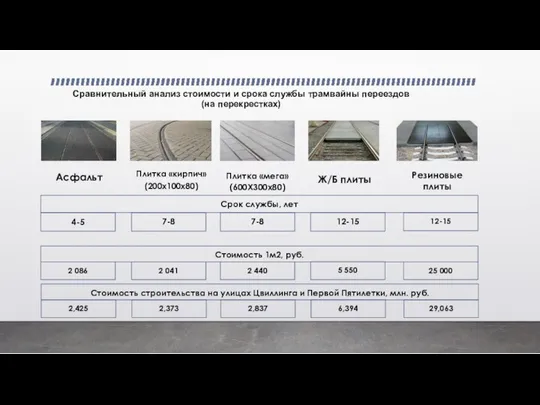

Синтаксис коррелятивных конструкций русского языка с позиции генеративной грамматики Сравнительный анализ стоимости и срока службы трамвайных переездов (на перекрестках)

Сравнительный анализ стоимости и срока службы трамвайных переездов (на перекрестках)