- International taxation Introduction

Содержание

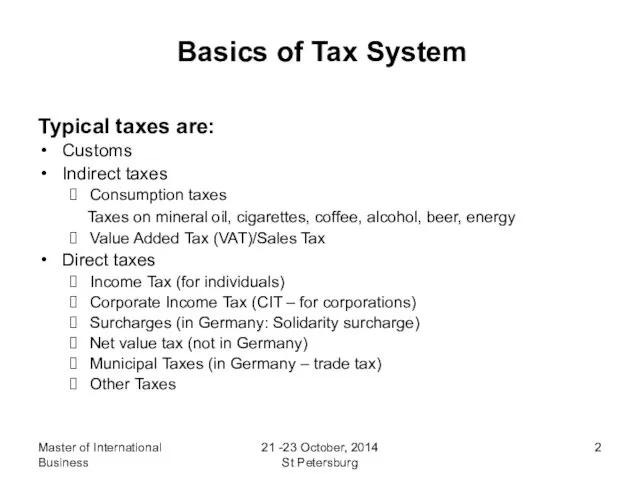

- 2. Master of International Business 21 -23 October, 2014 St Petersburg Basics of Tax System Typical taxes

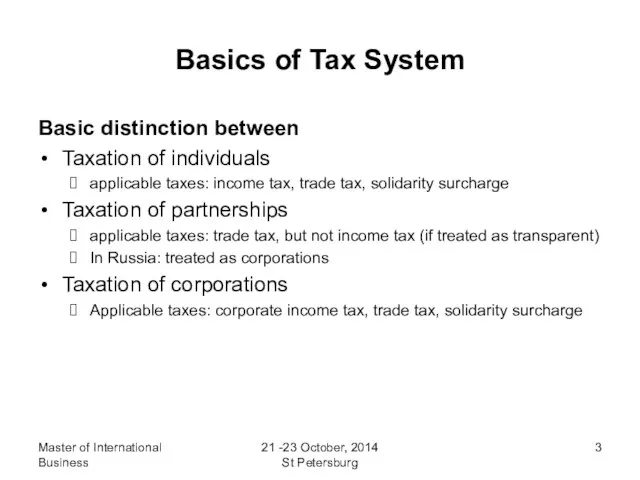

- 3. Master of International Business 21 -23 October, 2014 St Petersburg Basics of Tax System Basic distinction

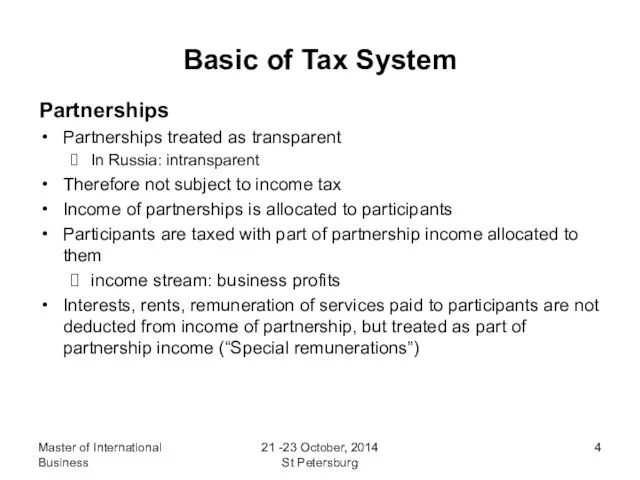

- 4. Master of International Business 21 -23 October, 2014 St Petersburg Basic of Tax System Partnerships Partnerships

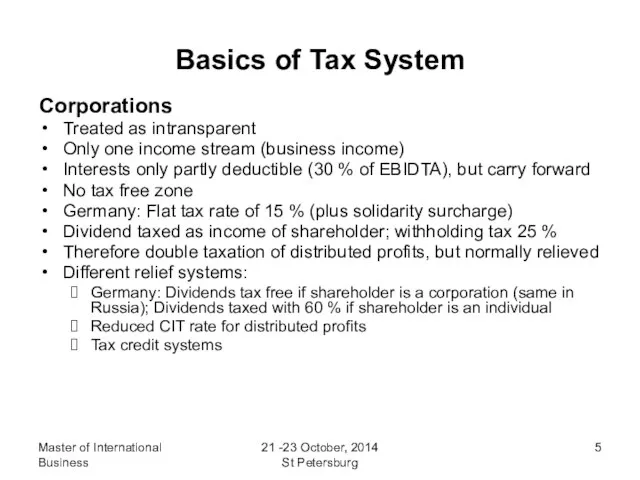

- 5. Master of International Business 21 -23 October, 2014 St Petersburg Basics of Tax System Corporations Treated

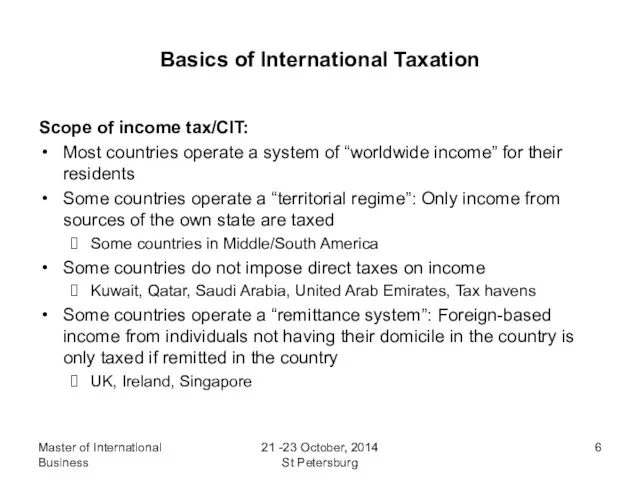

- 6. Master of International Business 21 -23 October, 2014 St Petersburg Basics of International Taxation Scope of

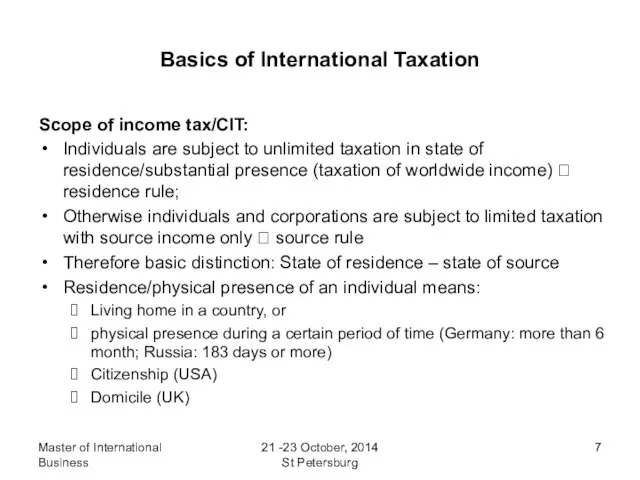

- 7. Master of International Business 21 -23 October, 2014 St Petersburg Basics of International Taxation Scope of

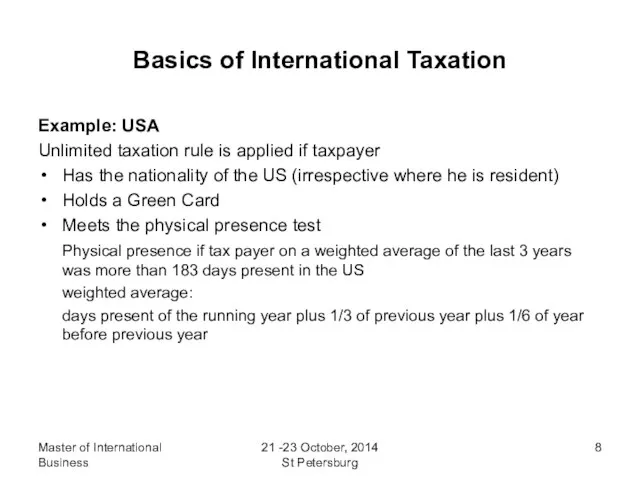

- 8. Master of International Business 21 -23 October, 2014 St Petersburg Basics of International Taxation Example: USA

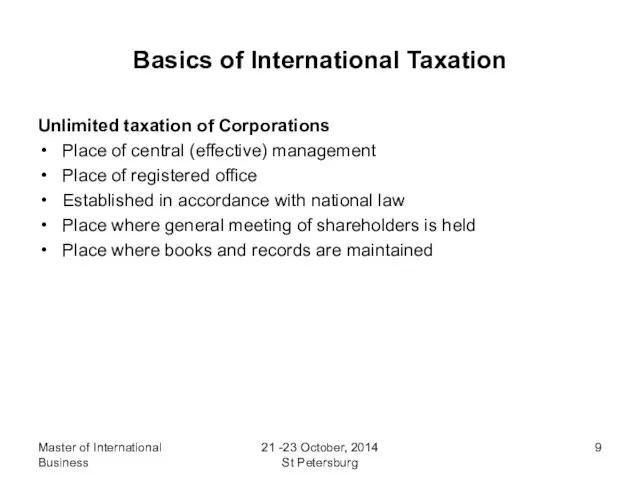

- 9. Master of International Business 21 -23 October, 2014 St Petersburg Basics of International Taxation Unlimited taxation

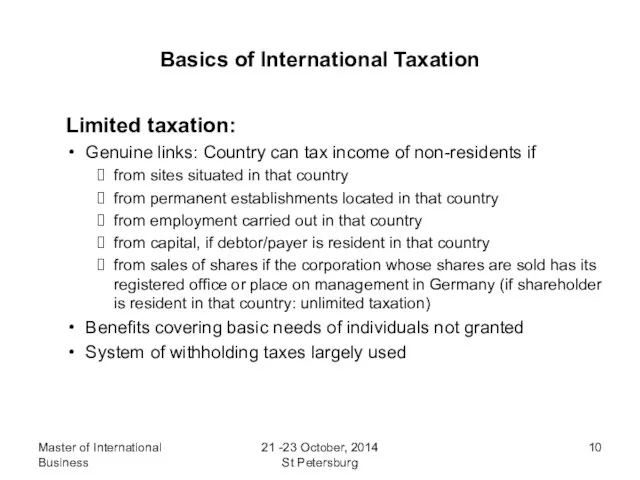

- 10. Master of International Business 21 -23 October, 2014 St Petersburg Basics of International Taxation Limited taxation:

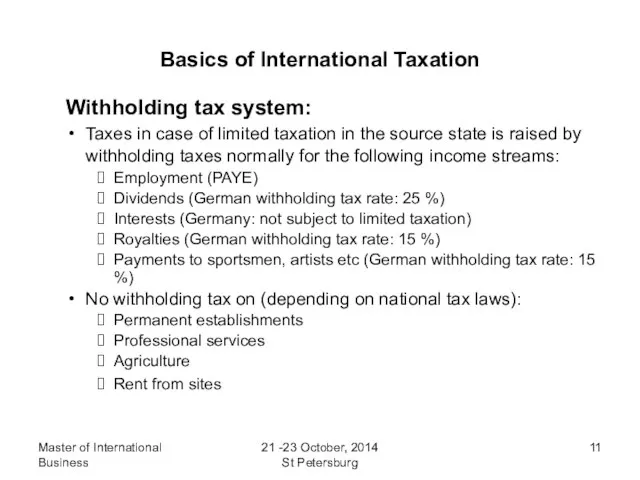

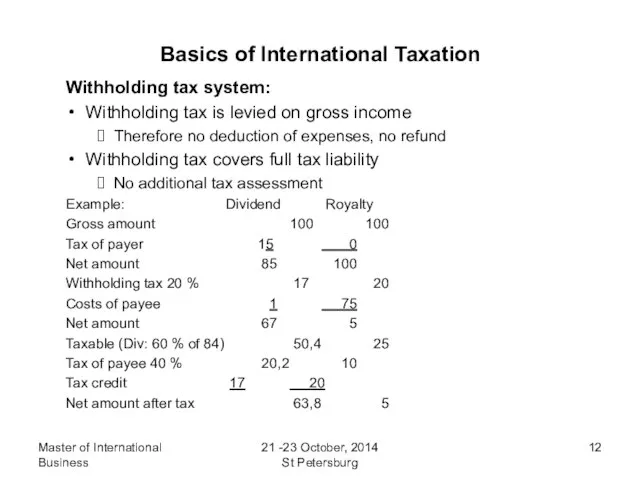

- 11. Master of International Business 21 -23 October, 2014 St Petersburg Basics of International Taxation Withholding tax

- 12. Master of International Business 21 -23 October, 2014 St Petersburg Basics of International Taxation Withholding tax

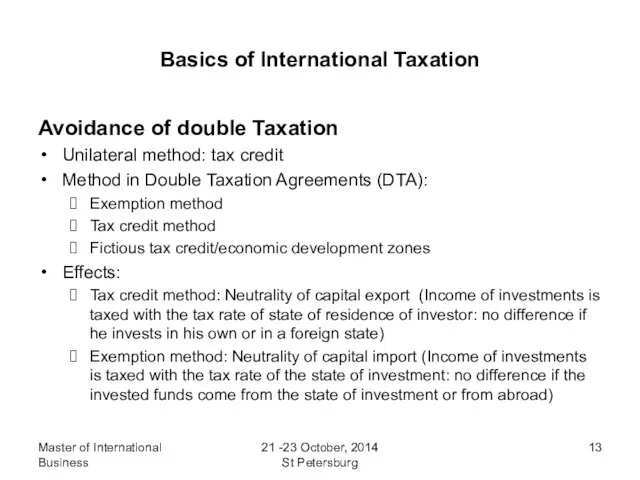

- 13. Master of International Business 21 -23 October, 2014 St Petersburg Basics of International Taxation Avoidance of

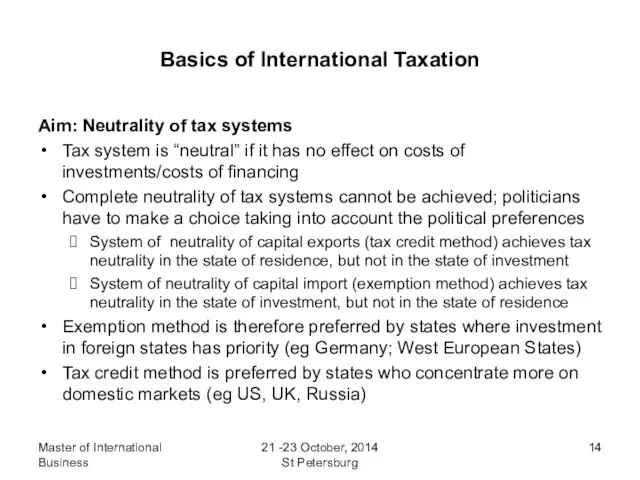

- 14. Master of International Business 21 -23 October, 2014 St Petersburg Basics of International Taxation Aim: Neutrality

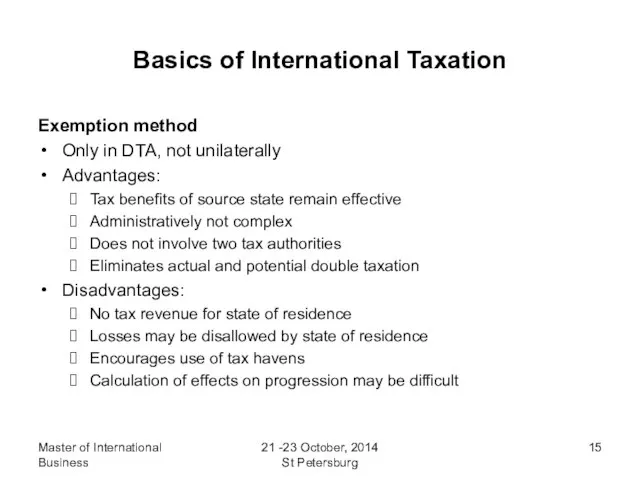

- 15. Master of International Business 21 -23 October, 2014 St Petersburg Basics of International Taxation Exemption method

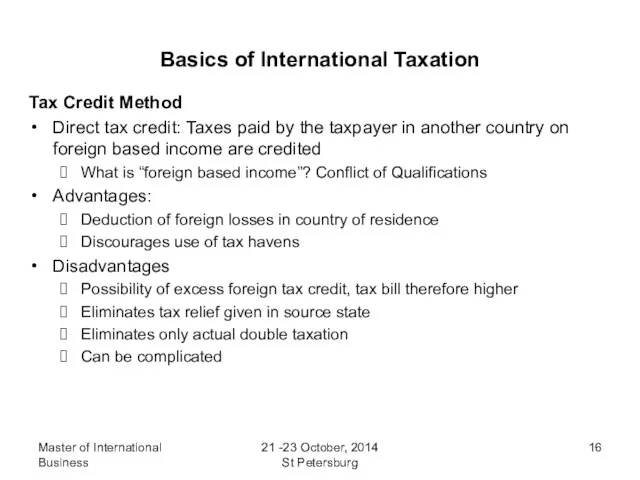

- 16. Master of International Business 21 -23 October, 2014 St Petersburg Basics of International Taxation Tax Credit

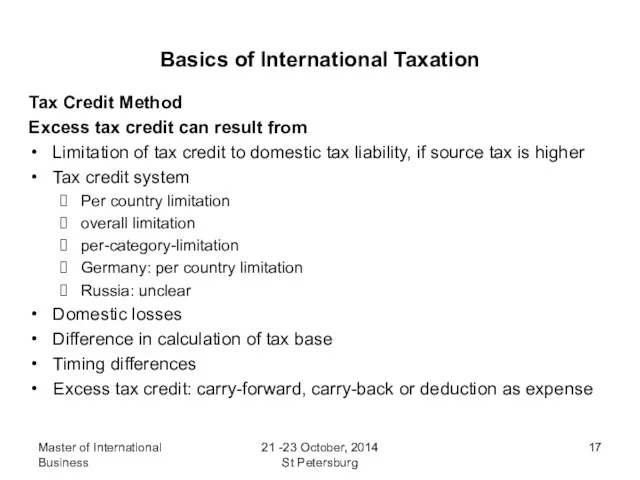

- 17. Master of International Business 21 -23 October, 2014 St Petersburg Basics of International Taxation Tax Credit

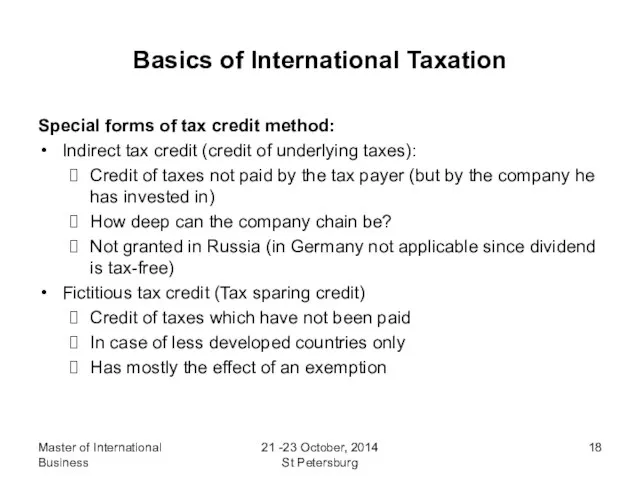

- 18. Master of International Business 21 -23 October, 2014 St Petersburg Basics of International Taxation Special forms

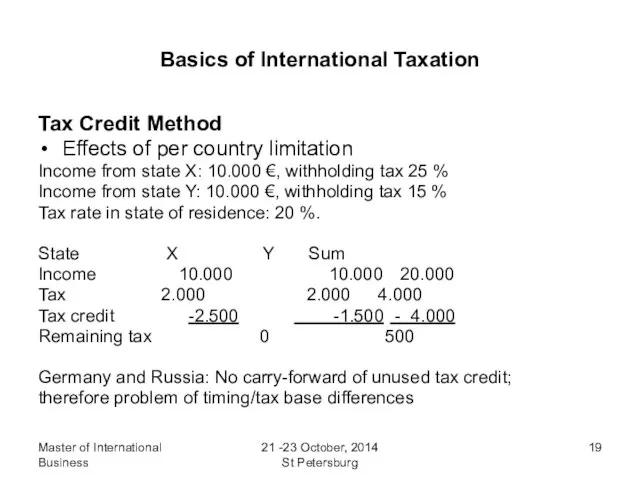

- 19. Master of International Business 21 -23 October, 2014 St Petersburg Basics of International Taxation Tax Credit

- 21. Скачать презентацию

Слайд 2Master of International Business

21 -23 October, 2014 St Petersburg

Basics of Tax System

Typical

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of Tax System

Typical

Слайд 3Master of International Business

21 -23 October, 2014 St Petersburg

Basics of Tax System

Basic

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of Tax System

Basic

Слайд 4Master of International Business

21 -23 October, 2014 St Petersburg

Basic of Tax System

Partnerships

Partnerships

Master of International Business

21 -23 October, 2014 St Petersburg

Basic of Tax System

Partnerships

Partnerships

Слайд 5Master of International Business

21 -23 October, 2014 St Petersburg

Basics of Tax System

Corporations

Treated

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of Tax System

Corporations

Treated

Слайд 6Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Scope

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Scope

Слайд 7Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Scope

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Scope

Слайд 8Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Example:

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Example:

Слайд 9Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Unlimited

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Unlimited

Слайд 10Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Limited

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Limited

Слайд 11Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Withholding

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Withholding

Слайд 12Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Withholding

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Withholding

Слайд 13Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Avoidance

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Avoidance

Слайд 14Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Aim:

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Aim:

Слайд 15Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Exemption

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Exemption

Слайд 16Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Tax

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Tax

Слайд 17Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Tax

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Tax

Слайд 18Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Special

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Special

Слайд 19Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Tax

Master of International Business

21 -23 October, 2014 St Petersburg

Basics of International Taxation

Tax

Новогоднее украшение «Серебряный шар»

Новогоднее украшение «Серебряный шар» Урок математики

Урок математики Чтение как путь формированиячеловеческого капитала

Чтение как путь формированиячеловеческого капитала Федеральное государственное унитарное предприятие Научно-исследовательский институт радио Главный научный сотрудник ФГУП НИИР,

Федеральное государственное унитарное предприятие Научно-исследовательский институт радио Главный научный сотрудник ФГУП НИИР,  Портфолио педагога

Портфолио педагога Букингемский дворец

Букингемский дворец Золотой век

Золотой век Контроль как один из методов диагностики учебных достижений учащихся в школьном курсе химии

Контроль как один из методов диагностики учебных достижений учащихся в школьном курсе химии Психология развития и личности

Психология развития и личности а,с,m,b

а,с,m,b Заявление руководителю

Заявление руководителю 11

11 Презентация на тему Агропромышленный комплекс России. Состав и значение.

Презентация на тему Агропромышленный комплекс России. Состав и значение.  Оптимизация процесса работы приемочной комиссии МБДОУ детский сад № 24 г. Ельца по приему продуктов питания от поставщиков

Оптимизация процесса работы приемочной комиссии МБДОУ детский сад № 24 г. Ельца по приему продуктов питания от поставщиков Команда Туристы-следопыты

Команда Туристы-следопыты Презентация на тему Материки

Презентация на тему Материки Product Placement Правила съема: метод Хитча

Product Placement Правила съема: метод Хитча Презентация на тему:“Кровеносная система ”

Презентация на тему:“Кровеносная система ” Презентация на тему Презентация о хлебе

Презентация на тему Презентация о хлебе Немного о программе: В 2010 году в Беларуси вышел первый сезон программ «Брэйн-ринг». После успешных эфиров и многочисленных заявок н

Немного о программе: В 2010 году в Беларуси вышел первый сезон программ «Брэйн-ринг». После успешных эфиров и многочисленных заявок н Открытый аукцион по продаже права на заключение договора аренды земельного участка для строительства объекта размещения организ

Открытый аукцион по продаже права на заключение договора аренды земельного участка для строительства объекта размещения организ РЕШЕНИЕ СОЦИАЛЬНО-ЭКОНОМИЧЕСКИХ ПРОБЛЕМ МОСКОВСКОЙ ОБЛАСТИ

РЕШЕНИЕ СОЦИАЛЬНО-ЭКОНОМИЧЕСКИХ ПРОБЛЕМ МОСКОВСКОЙ ОБЛАСТИ Презентация на тему Опционы: понятие, виды, стратегии покупки / продажи

Презентация на тему Опционы: понятие, виды, стратегии покупки / продажи  Читаем человека с первого взгляда. Введение. Модуль 1

Читаем человека с первого взгляда. Введение. Модуль 1 Проект трансформации МФИ Центральная Азия Май 2011

Проект трансформации МФИ Центральная Азия Май 2011 Dizenteria_amebiaz

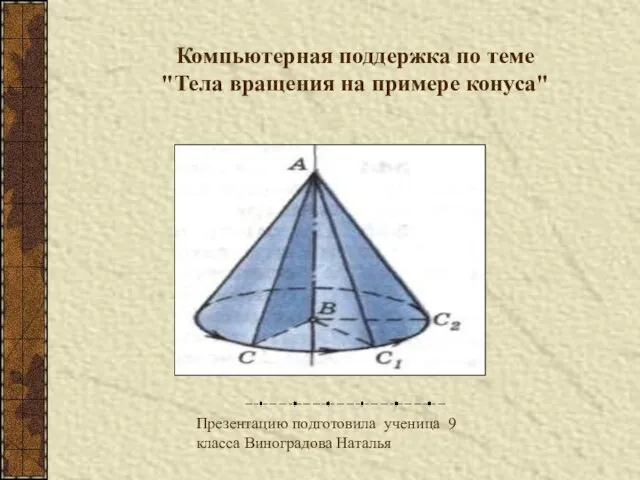

Dizenteria_amebiaz Тела вращения на примере конуса

Тела вращения на примере конуса Онлайн-конкурс по робототехнике RoboHack

Онлайн-конкурс по робототехнике RoboHack