- Double Taxation Agreements

Содержание

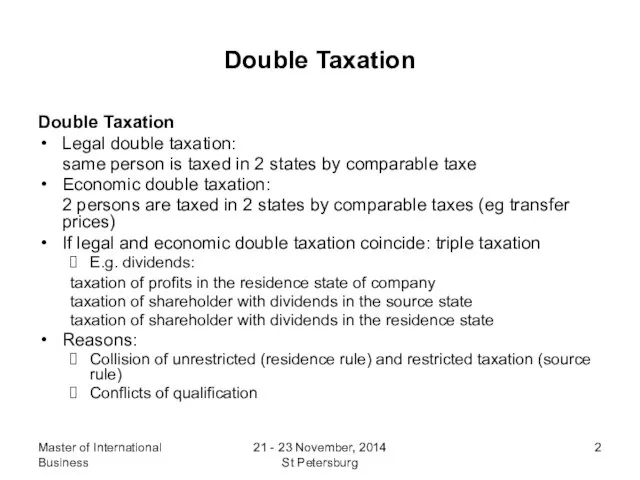

- 2. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Double Taxation Legal

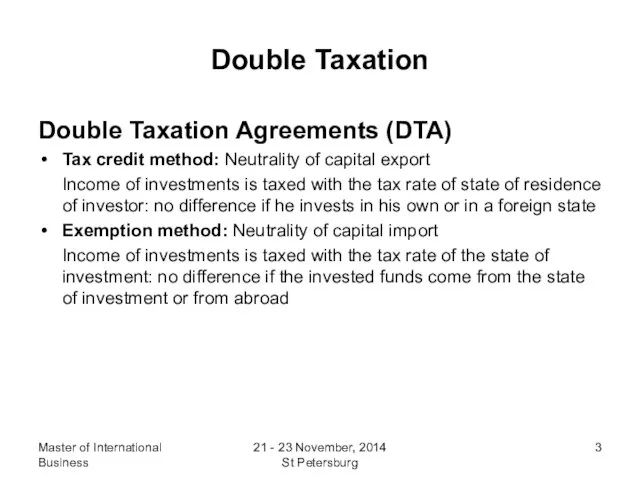

- 3. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Double Taxation Agreements

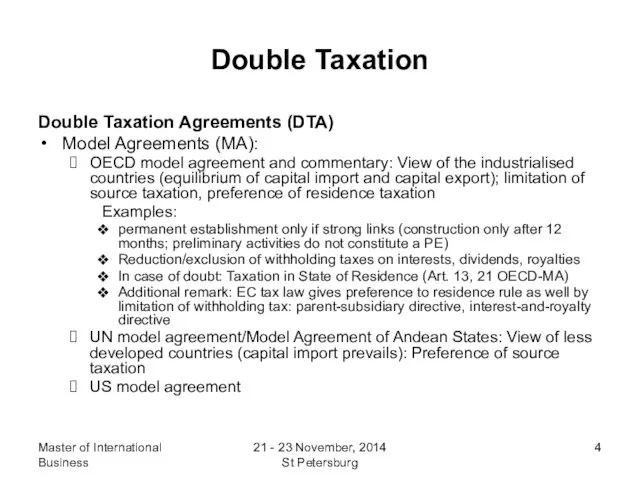

- 4. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Double Taxation Agreements

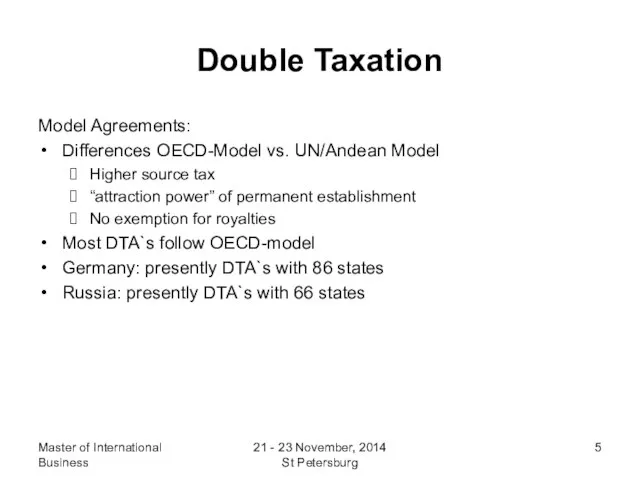

- 5. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Model Agreements: Differences

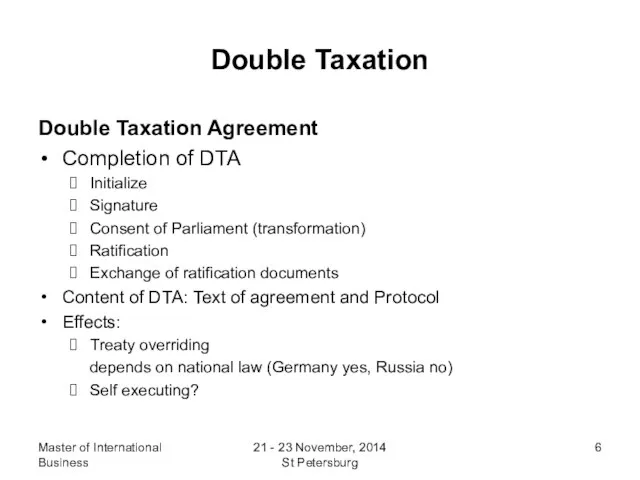

- 6. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Double Taxation Agreement

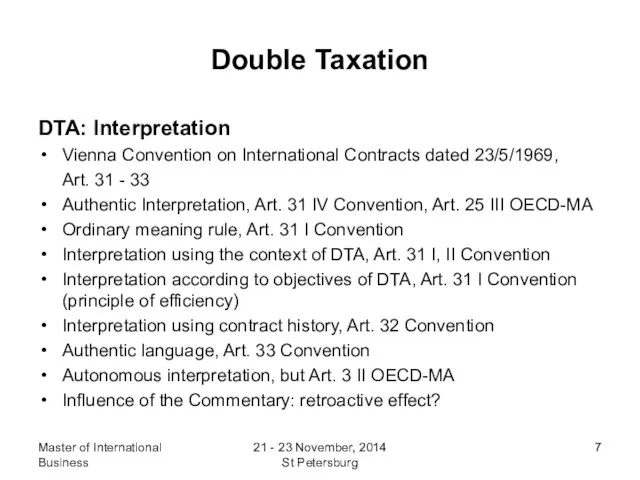

- 7. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation DTA: Interpretation Vienna

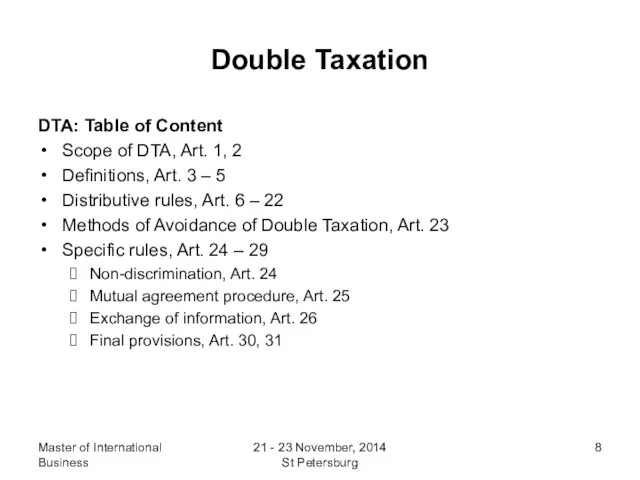

- 8. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation DTA: Table of

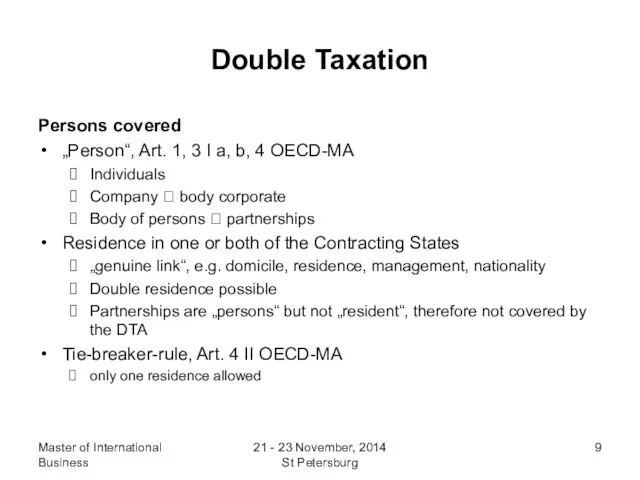

- 9. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Persons covered „Person“,

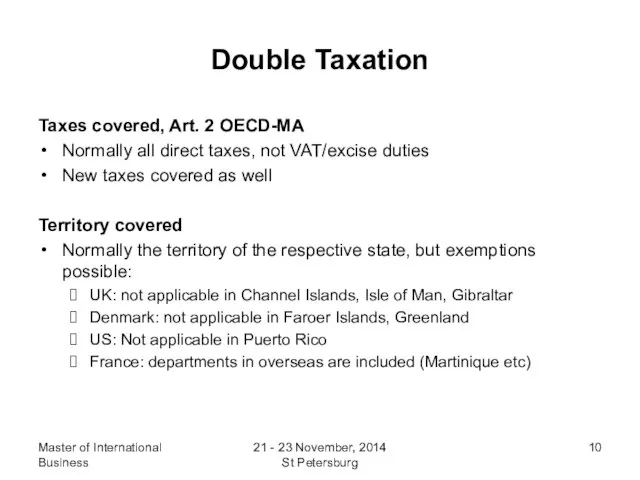

- 10. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Taxes covered, Art.

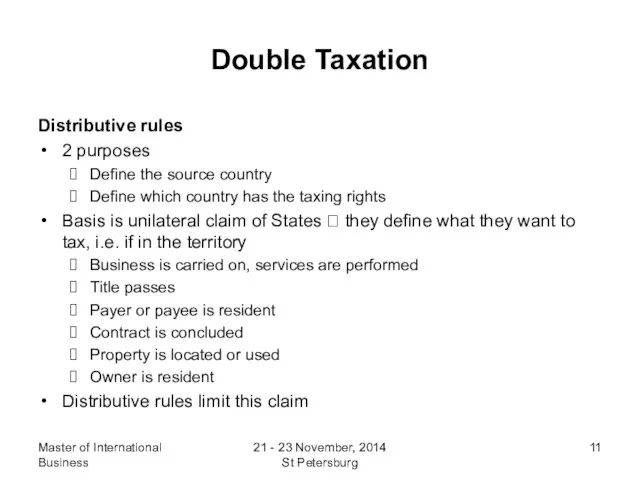

- 11. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Distributive rules 2

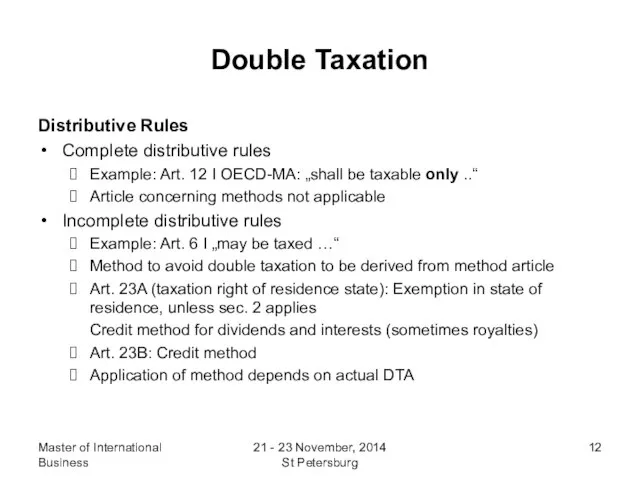

- 12. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Distributive Rules Complete

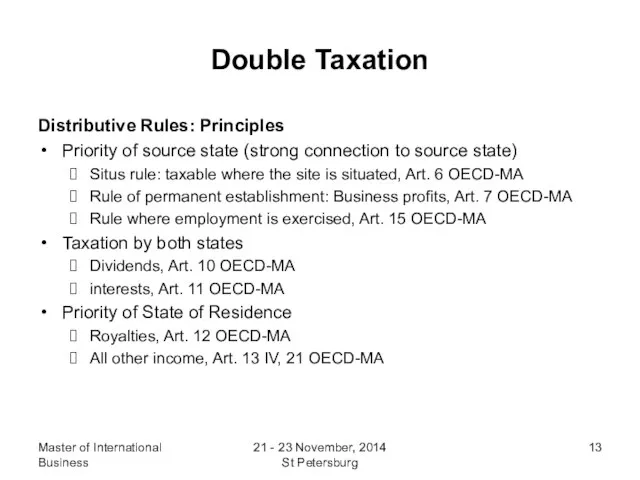

- 13. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Distributive Rules: Principles

- 14. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Type of Income

- 15. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Immovable Property (agriculture/

- 16. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Business profits, Art.

- 17. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Permanent establishment, Art.

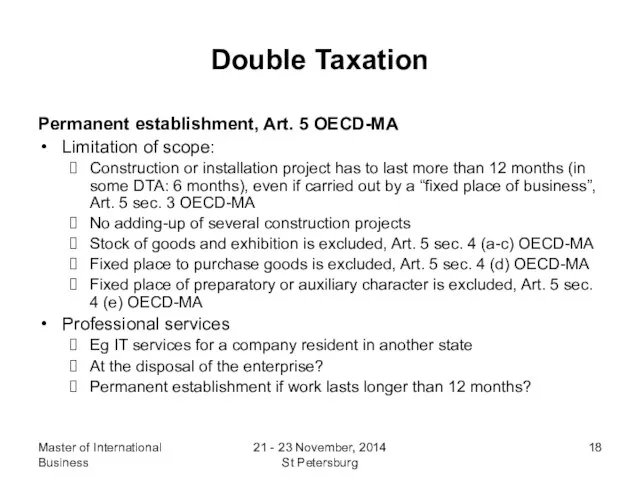

- 18. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Permanent establishment, Art.

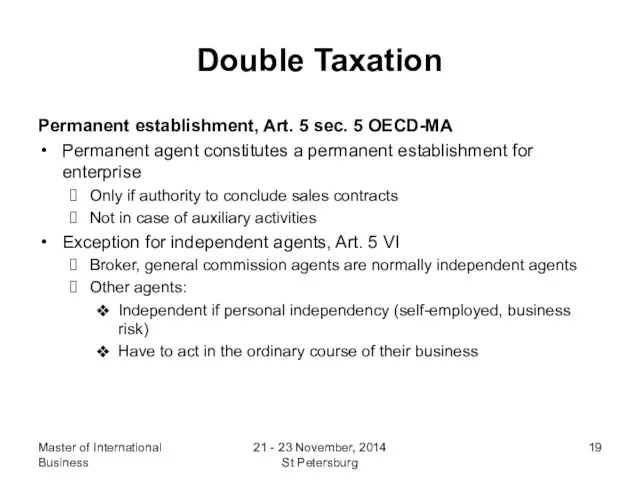

- 19. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Permanent establishment, Art.

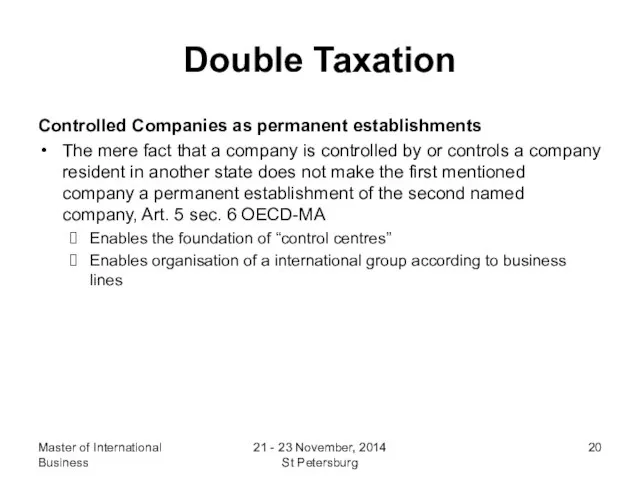

- 20. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Controlled Companies as

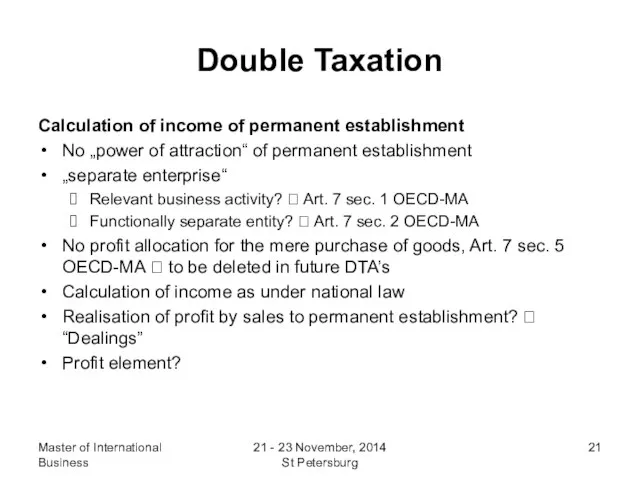

- 21. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Calculation of income

- 22. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Calculation of income

- 23. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Calculation of Income

- 24. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Calculation of Income

- 25. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Taxation of perm.

- 26. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Partnerships If transparent,

- 27. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Dividends, Interests, Royalties

- 28. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Dividends, Interests, Royalties

- 29. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Capital gains, Art.

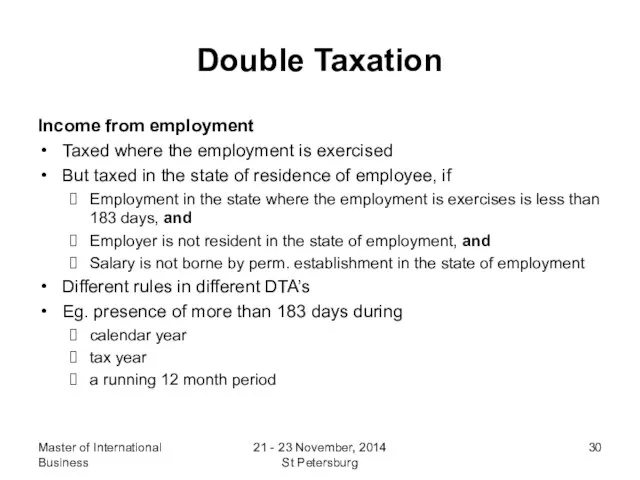

- 30. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Income from employment

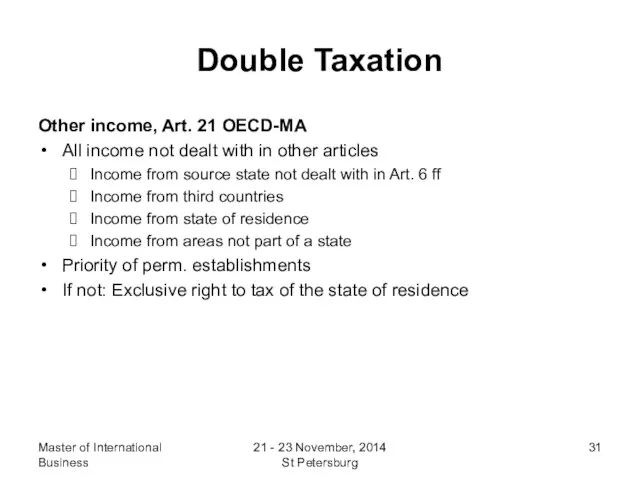

- 31. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Other income, Art.

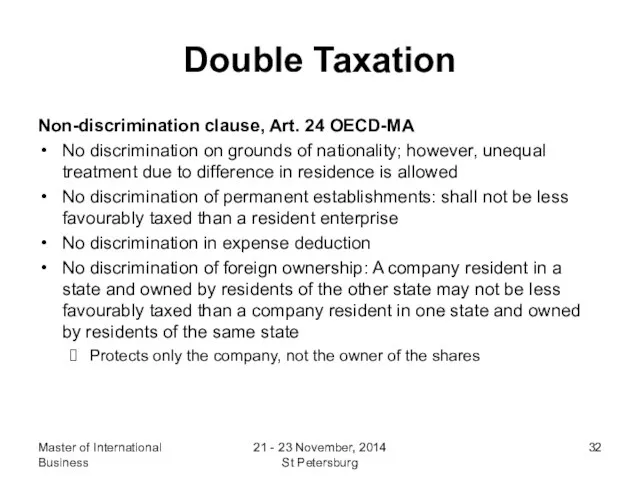

- 32. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Non-discrimination clause, Art.

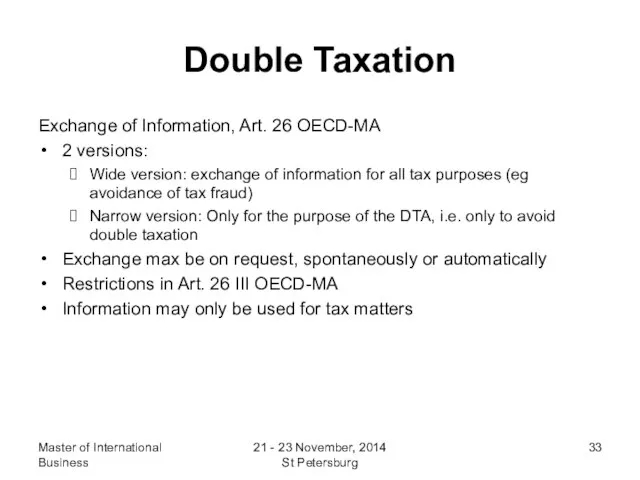

- 33. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Exchange of Information,

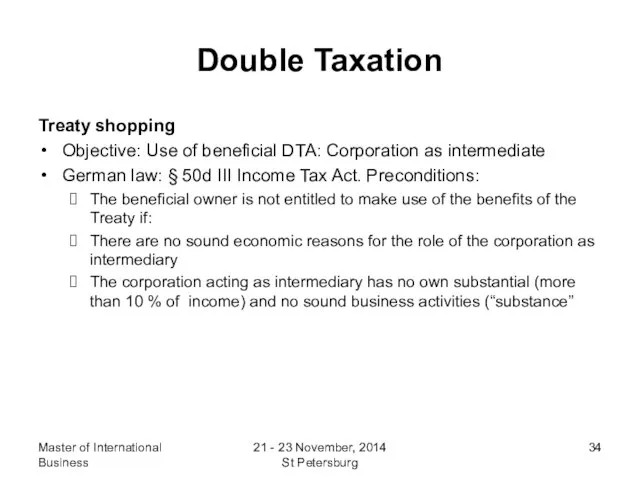

- 34. Master of International Business 21 - 23 November, 2014 St Petersburg Double Taxation Treaty shopping Objective:

- 36. Скачать презентацию

Слайд 2Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Double Taxation

Legal

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Double Taxation

Legal

Слайд 3Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Double Taxation

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Double Taxation

Слайд 4Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Double Taxation

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Double Taxation

Слайд 5Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Model Agreements:

Differences

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Model Agreements:

Differences

Слайд 6Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Double Taxation

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Double Taxation

Слайд 7Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

DTA: Interpretation

Vienna

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

DTA: Interpretation

Vienna

Слайд 8Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

DTA: Table

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

DTA: Table

Слайд 9Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Persons covered

„Person“,

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Persons covered

„Person“,

Слайд 10Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Taxes covered,

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Taxes covered,

Слайд 11Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Distributive rules

2

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Distributive rules

2

Слайд 12Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Distributive Rules

Complete

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Distributive Rules

Complete

Слайд 13Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Distributive Rules:

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Distributive Rules:

Слайд 14Master of International Business

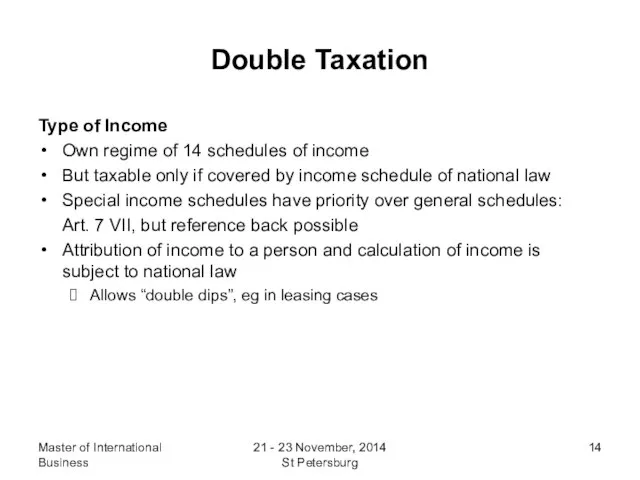

21 - 23 November, 2014 St Petersburg

Double Taxation

Type of

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Type of

Слайд 15Master of International Business

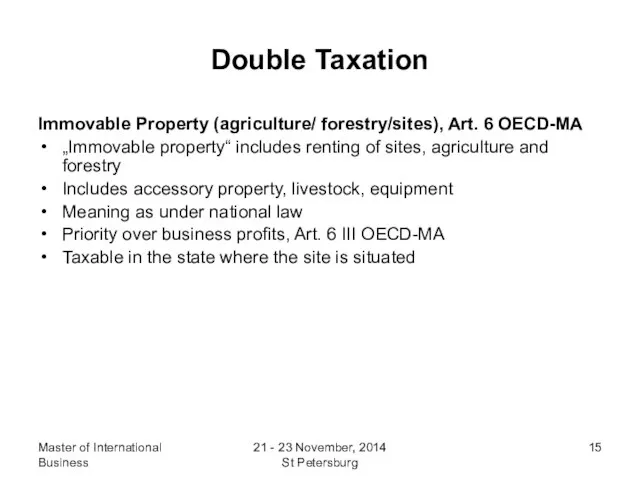

21 - 23 November, 2014 St Petersburg

Double Taxation

Immovable Property

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Immovable Property

Слайд 16Master of International Business

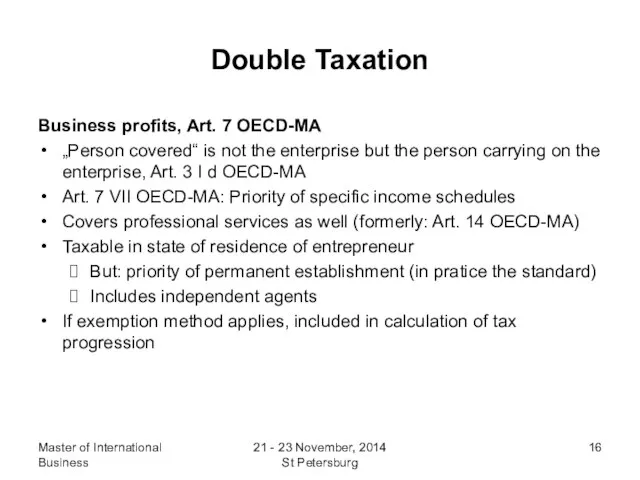

21 - 23 November, 2014 St Petersburg

Double Taxation

Business profits,

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Business profits,

Слайд 17Master of International Business

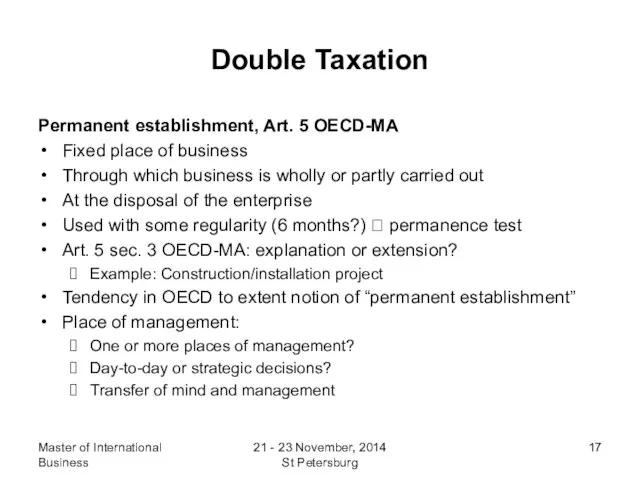

21 - 23 November, 2014 St Petersburg

Double Taxation

Permanent establishment,

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Permanent establishment,

Слайд 18Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Permanent establishment,

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Permanent establishment,

Слайд 19Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Permanent establishment,

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Permanent establishment,

Слайд 20Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Controlled Companies

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Controlled Companies

Слайд 21Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Calculation of

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Calculation of

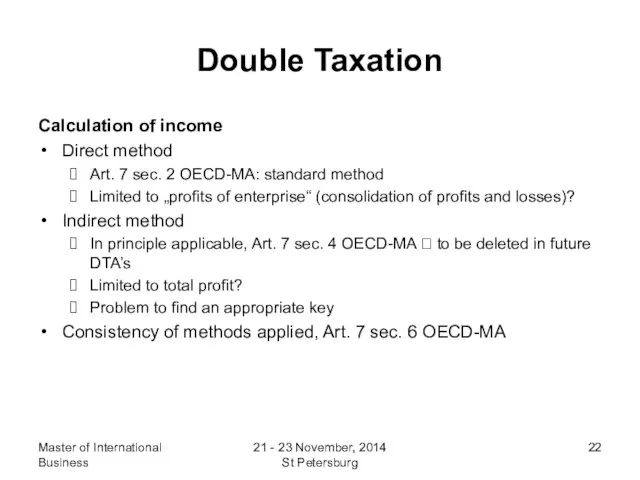

Слайд 22Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Calculation of

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Calculation of

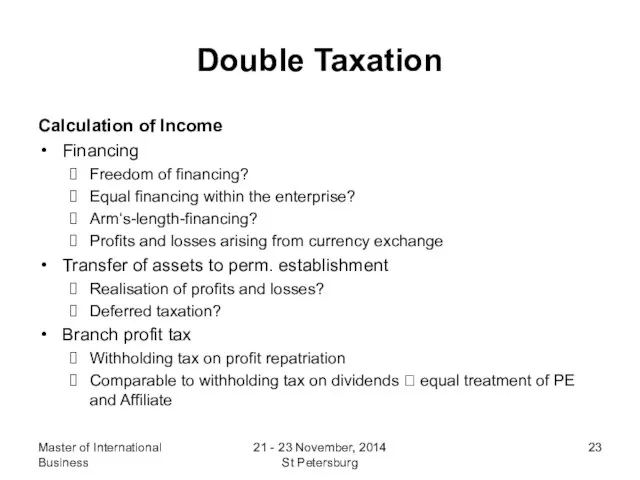

Слайд 23Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Calculation of

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Calculation of

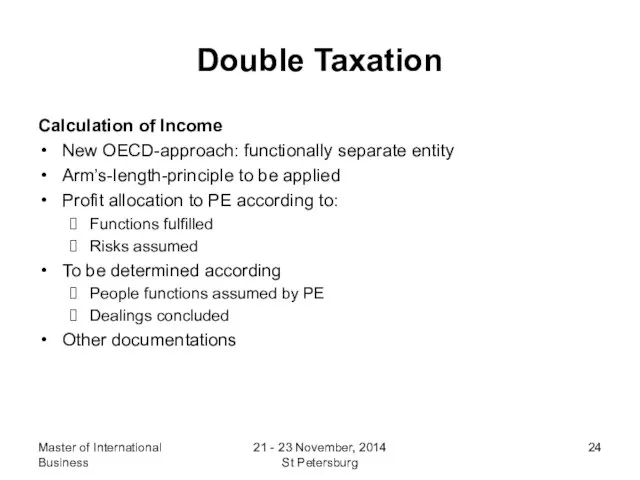

Слайд 24Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Calculation of

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Calculation of

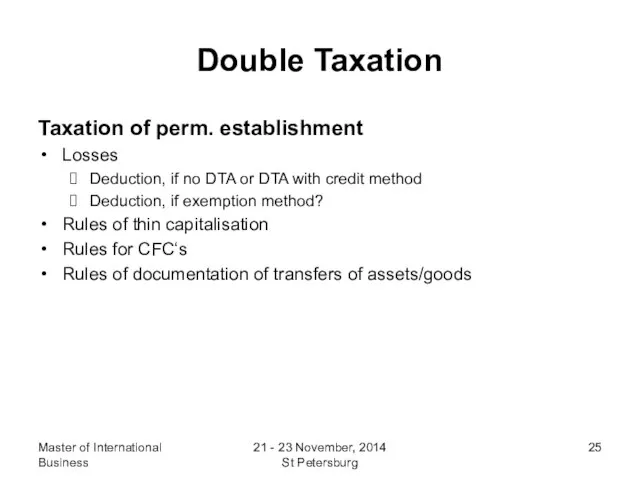

Слайд 25Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Taxation of

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Taxation of

Слайд 26Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

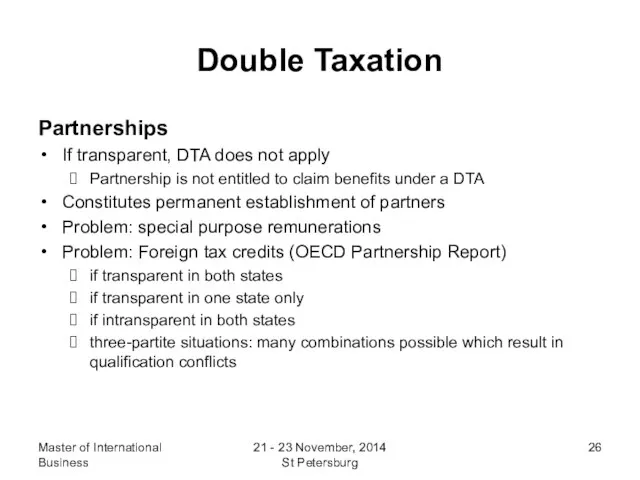

Partnerships

If transparent,

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Partnerships

If transparent,

Слайд 27Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

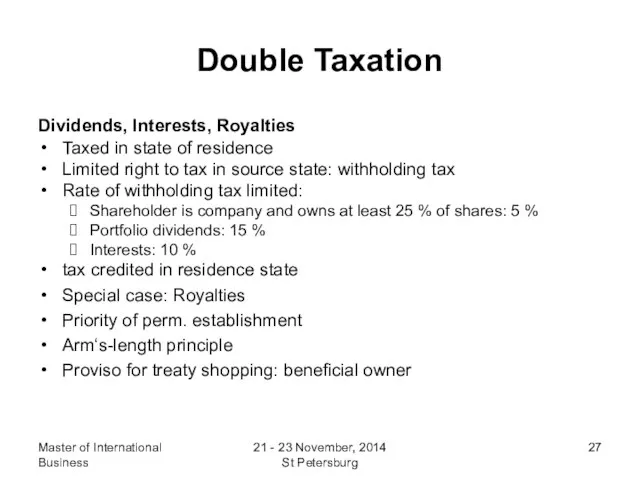

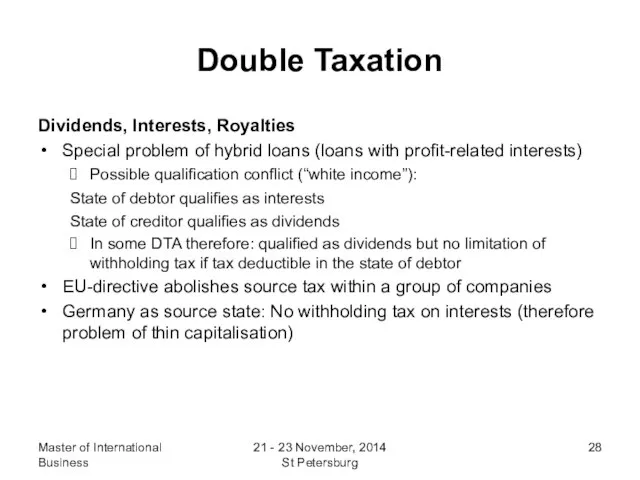

Dividends, Interests,

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Dividends, Interests,

Слайд 28Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Dividends, Interests,

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Dividends, Interests,

Слайд 29Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

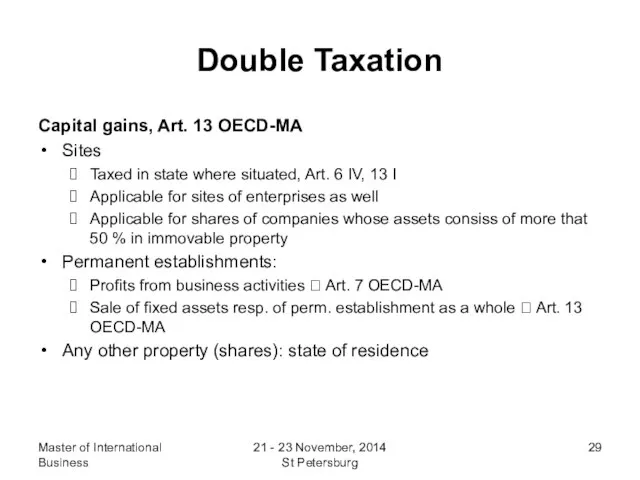

Capital gains,

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Capital gains,

Слайд 30Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Income from

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Income from

Слайд 31Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Other income,

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Other income,

Слайд 32Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Non-discrimination clause,

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Non-discrimination clause,

Слайд 33Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Exchange of

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Exchange of

Слайд 34Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Treaty shopping

Objective:

Master of International Business

21 - 23 November, 2014 St Petersburg

Double Taxation

Treaty shopping

Objective:

Основные виды организационных структур

Основные виды организационных структур ПРОГРАММА профилактики детского электротравматизма ОАО «Кубаньэнерго» Тематический урок «Основы электробезопасности» (для у

ПРОГРАММА профилактики детского электротравматизма ОАО «Кубаньэнерго» Тематический урок «Основы электробезопасности» (для у Брендинг в индустрии моды

Брендинг в индустрии моды Профориентация: новые форматы, ГАУ ДПО СОИРО

Профориентация: новые форматы, ГАУ ДПО СОИРО Традиционный бурятский мужской костюм

Традиционный бурятский мужской костюм Добор опоздавших на регистрацию пассажиров

Добор опоздавших на регистрацию пассажиров ФСКН Молодёжи

ФСКН Молодёжи Рамы переменного сечения

Рамы переменного сечения 568120

568120 Добро пожаловать в ВГПУ!

Добро пожаловать в ВГПУ! Управление коллективом исполнителей

Управление коллективом исполнителей Интерьер, который мы создаем. Дизайн. Моделирование

Интерьер, который мы создаем. Дизайн. Моделирование В гостях у Барбариков

В гостях у Барбариков Функции и структура ЛЭС. Оформление трассы

Функции и структура ЛЭС. Оформление трассы Сборы с носителей информации и оборудования

Сборы с носителей информации и оборудования «1С:Документооборот 8»

«1С:Документооборот 8» Вопросы проверки и перепроверки экзаменационных работ в условиях формирования независимой оценки качества образования

Вопросы проверки и перепроверки экзаменационных работ в условиях формирования независимой оценки качества образования Творчество Евгения Рачёва

Творчество Евгения Рачёва Презентация_Касимов

Презентация_Касимов Бесстрашный рыцарь неба

Бесстрашный рыцарь неба энн

энн Инновационные приоритеты в высокотехнологичной области Дмитрий Конаш, Региональный Директор Intel в странах СНГ

Инновационные приоритеты в высокотехнологичной области Дмитрий Конаш, Региональный Директор Intel в странах СНГ Символы России. Государственный флаг

Символы России. Государственный флаг Презентация на тему ЛАТВИЯ

Презентация на тему ЛАТВИЯ Новые люди

Новые люди Горы мира

Горы мира Photoshop. Конкурс. Supermen - GGG

Photoshop. Конкурс. Supermen - GGG Презентация

Презентация