- MAcc_Lecture 1_2022-2023

Содержание

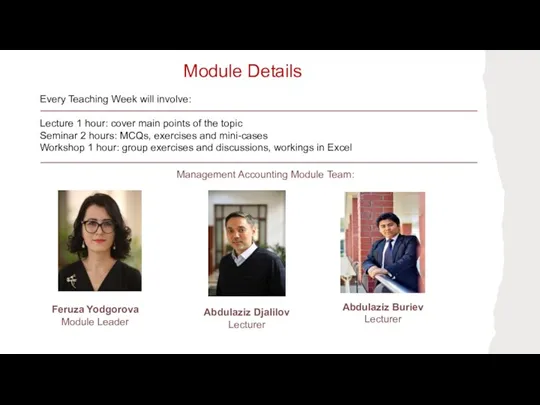

- 2. Module Details Every Teaching Week will involve: Lecture 1 hour: cover main points of the topic

- 3. MODULE DETAILS [email protected] Office hours: Friday, 3pm-5pm MAccWIUT2022-2023 (Telegram channel) Quickly Join!

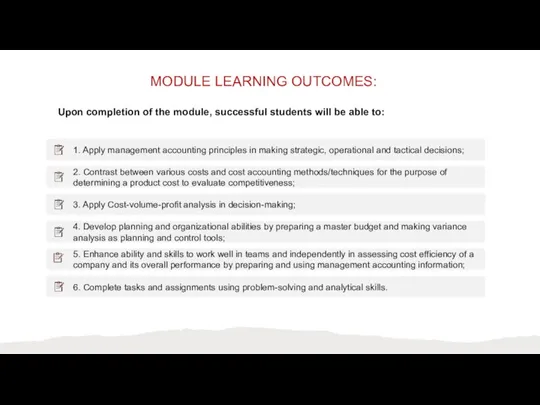

- 4. MODULE LEARNING OUTCOMES: Upon completion of the module, successful students will be able to:

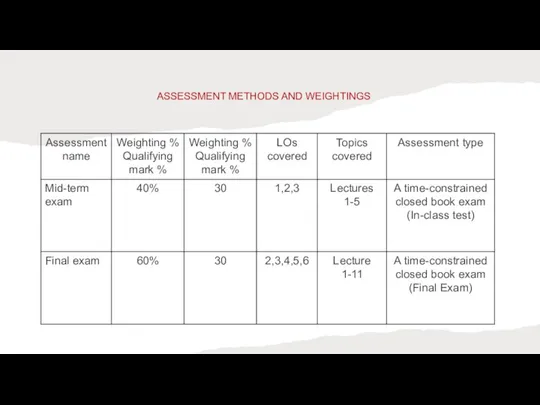

- 5. ASSESSMENT METHODS AND WEIGHTINGS

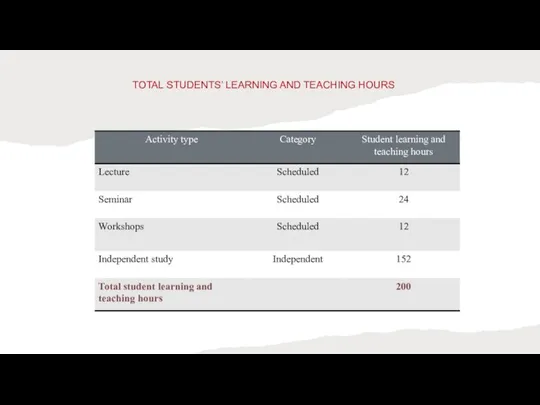

- 6. TOTAL STUDENTS’ LEARNING AND TEACHING HOURS

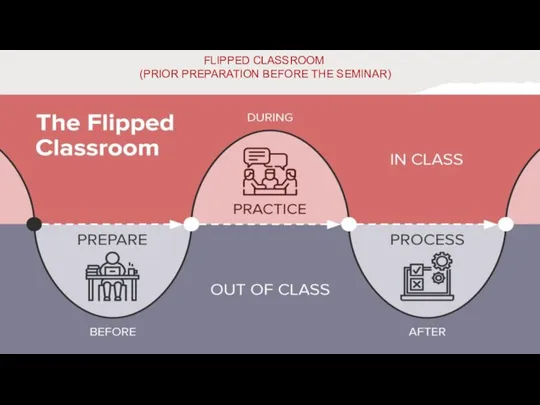

- 7. FLIPPED CLASSROOM (PRIOR PREPARATION BEFORE THE SEMINAR)

- 8. LECTURE 1 INTRODUCTION TO MANAGEMENT ACCOUNTING

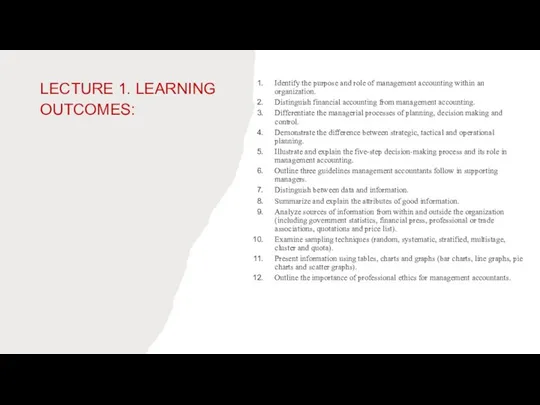

- 9. LECTURE 1. LEARNING OUTCOMES: Identify the purpose and role of management accounting within an organization. Distinguish

- 10. Management accounting is the 'application of the principles of accounting and financial management to create, protect,

- 11. A CASE FROM MANUFACTURING SECTOR

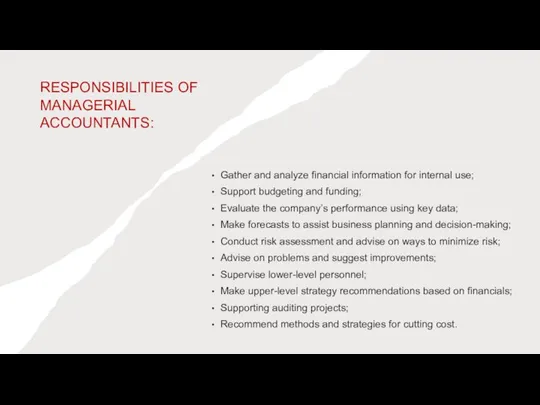

- 12. RESPONSIBILITIES OF MANAGERIAL ACCOUNTANTS: Gather and analyze financial information for internal use; Support budgeting and funding;

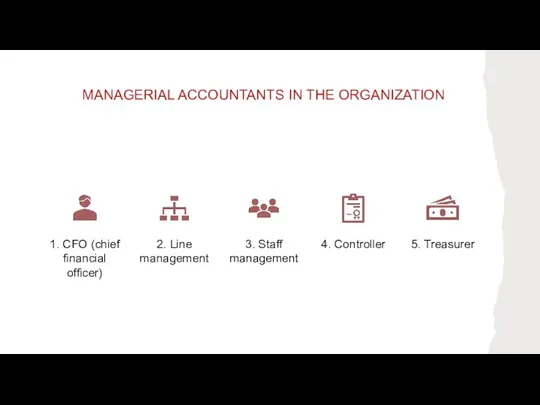

- 13. MANAGERIAL ACCOUNTANTS IN THE ORGANIZATION

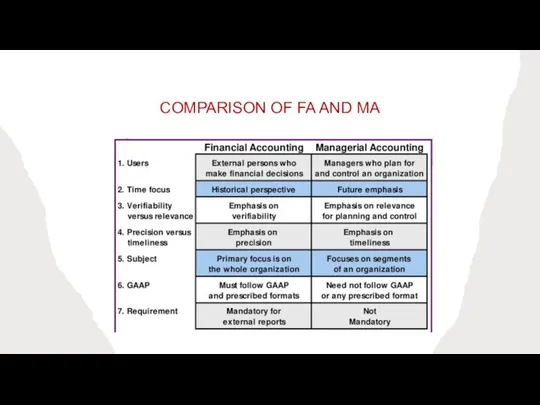

- 14. COMPARISON OF FA AND MA

- 15. THE MAIN FUNCTIONS OF MANAGEMENT ARE:

- 16. EXAMPLE: HOW GEORGE GOES THROUGH THESE 3 STAGES

- 17. DIFFERENCE BETWEEN STRATEGIC, TACTICAL AND OPERATIONAL PLANNING

- 18. STRATEGIC DECISIONS AND THE MANAGEMENT ACCOUNTANT What is strategy?

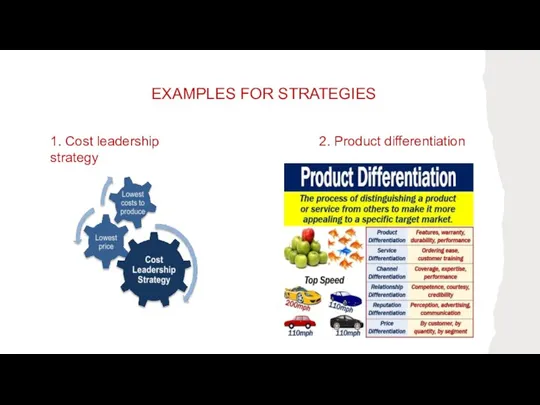

- 19. EXAMPLES FOR STRATEGIES 1. Cost leadership strategy 2. Product differentiation

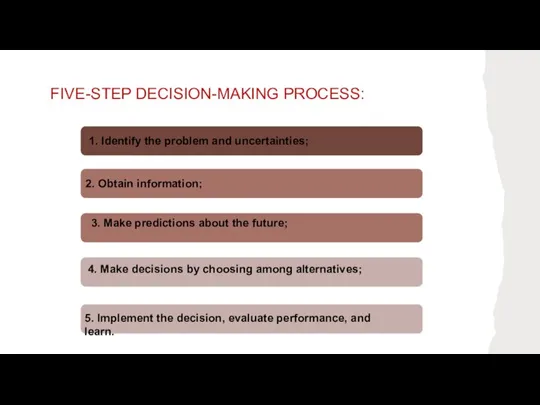

- 20. FIVE-STEP DECISION-MAKING PROCESS: 3. Make predictions about the future; 4. Make decisions by choosing among alternatives;

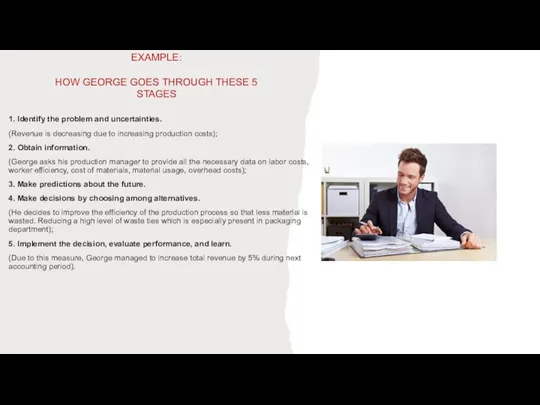

- 21. EXAMPLE: HOW GEORGE GOES THROUGH THESE 5 STAGES 1. Identify the problem and uncertainties. (Revenue is

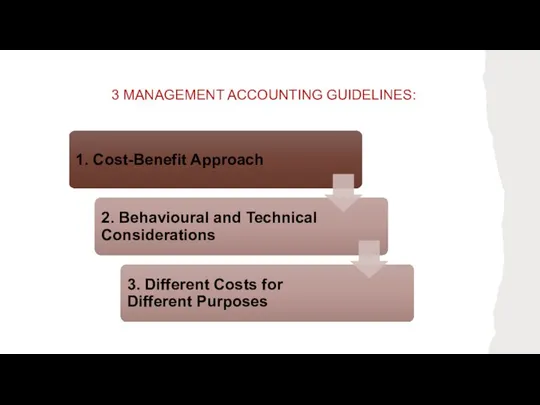

- 22. 3 MANAGEMENT ACCOUNTING GUIDELINES:

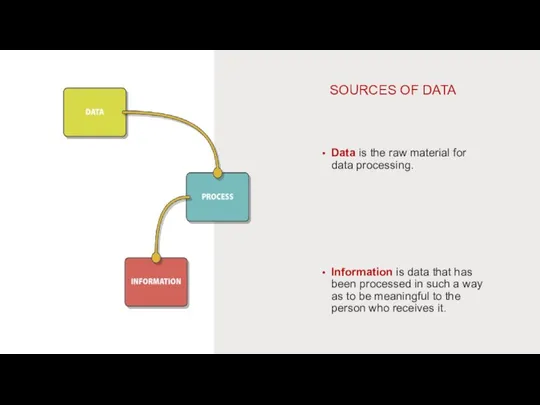

- 23. SOURCES OF DATA Data is the raw material for data processing. Information is data that has

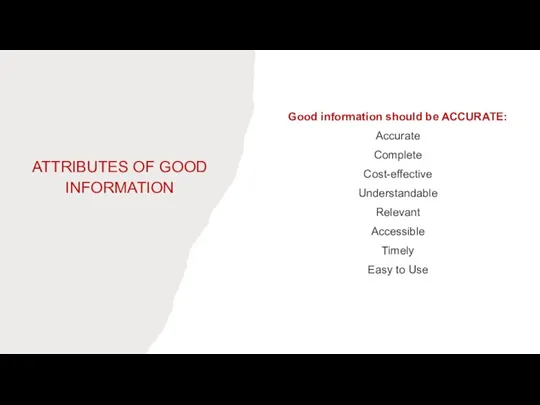

- 24. ATTRIBUTES OF GOOD INFORMATION Good information should be ACCURATE: Accurate Complete Cost-effective Understandable Relevant Accessible Timely

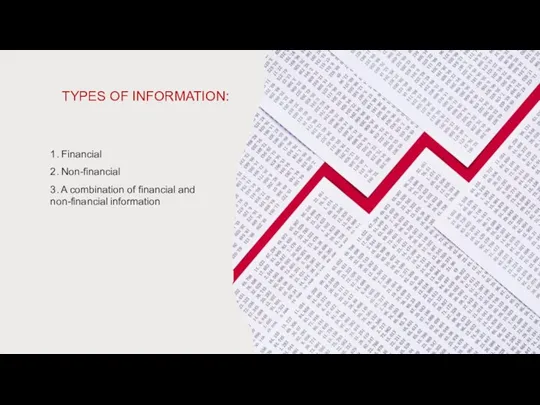

- 25. TYPES OF INFORMATION: 1. Financial 2. Non-financial 3. A combination of financial and non-financial information

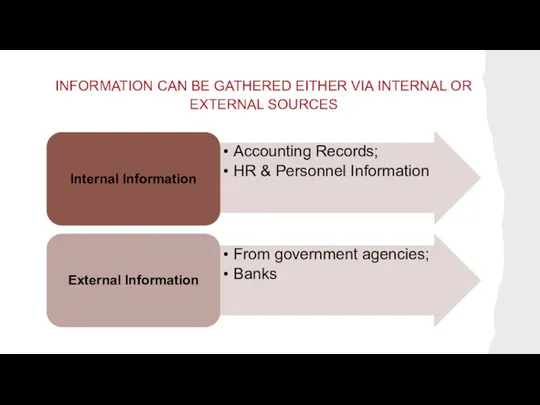

- 26. INFORMATION CAN BE GATHERED EITHER VIA INTERNAL OR EXTERNAL SOURCES

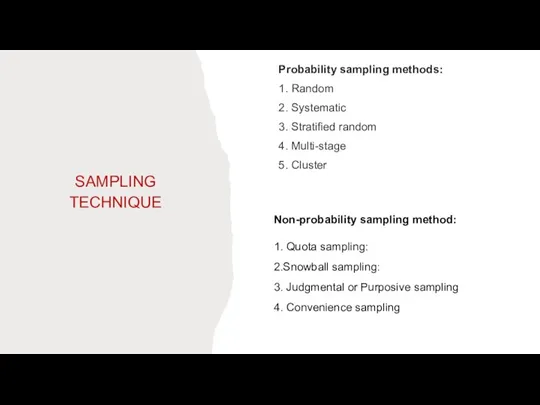

- 27. SAMPLING TECHNIQUE Probability sampling methods: 1. Random 2. Systematic 3. Stratified random 4. Multi-stage 5. Cluster

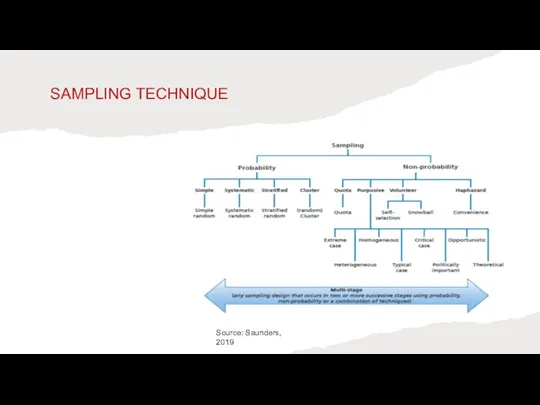

- 28. SAMPLING TECHNIQUE Source: Saunders, 2019

- 29. PRESENTING INFORMATION 1. Written reports; 2. Tables, charts and graphs (need interpretation).

- 30. IMA STATEMENT OF ETHICAL PROFESSIONAL PRACTICE PRINCIPLES Honesty Fairness Objectivity Responsibility

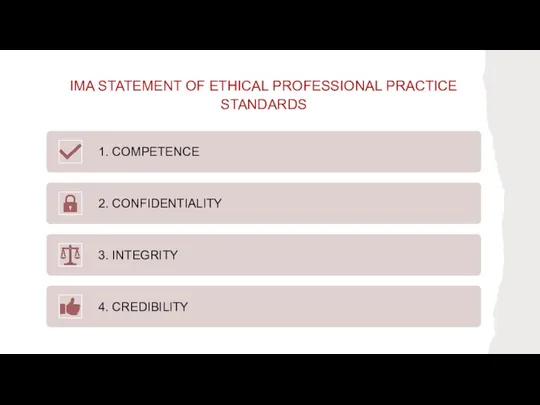

- 31. IMA STATEMENT OF ETHICAL PROFESSIONAL PRACTICE STANDARDS

- 32. PROFESSIONAL QUALIFICATIONS AND PROFESSIONAL BODIES

- 33. LITERATURE Srikant M. Datar, Madhav V. Rajan (2018), Horngren's Cost Accounting: A Managerial Emphasis,16th Edition; Pearson.

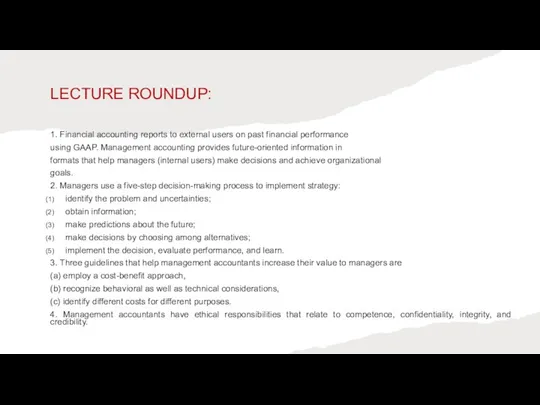

- 34. LECTURE ROUNDUP: 1. Financial accounting reports to external users on past financial performance using GAAP. Management

- 35. LECTURE ROUNDUP: 5. Data is the raw material for data processing. Data relates to facts, events

- 36. LECTURE ROUNDUP: 9. A non-probability sampling method is a sampling method in which the chance of

- 38. Скачать презентацию

Слайд 3MODULE DETAILS

[email protected]

Office hours: Friday, 3pm-5pm

MAccWIUT2022-2023

(Telegram channel)

Quickly Join!

MODULE DETAILS

[email protected]

Office hours: Friday, 3pm-5pm

MAccWIUT2022-2023

(Telegram channel)

Quickly Join!

Слайд 4MODULE LEARNING OUTCOMES:

Upon completion of the module, successful students will be able

MODULE LEARNING OUTCOMES:

Upon completion of the module, successful students will be able

Слайд 5

ASSESSMENT METHODS AND WEIGHTINGS

ASSESSMENT METHODS AND WEIGHTINGS

Слайд 6

TOTAL STUDENTS’ LEARNING AND TEACHING HOURS

TOTAL STUDENTS’ LEARNING AND TEACHING HOURS

Слайд 7

FLIPPED CLASSROOM

(PRIOR PREPARATION BEFORE THE SEMINAR)

FLIPPED CLASSROOM

(PRIOR PREPARATION BEFORE THE SEMINAR)

Слайд 8

LECTURE 1

INTRODUCTION TO MANAGEMENT ACCOUNTING

LECTURE 1

INTRODUCTION TO MANAGEMENT ACCOUNTING

Слайд 9LECTURE 1. LEARNING OUTCOMES:

Identify the purpose and role of management accounting within

LECTURE 1. LEARNING OUTCOMES:

Identify the purpose and role of management accounting within

Слайд 10Management accounting is the 'application of the principles of accounting and financial

Management accounting is the 'application of the principles of accounting and financial

Слайд 11A CASE FROM MANUFACTURING SECTOR

A CASE FROM MANUFACTURING SECTOR

Слайд 12RESPONSIBILITIES OF MANAGERIAL

ACCOUNTANTS:

Gather and analyze financial information for internal use;

Support budgeting and

RESPONSIBILITIES OF MANAGERIAL

ACCOUNTANTS:

Gather and analyze financial information for internal use;

Support budgeting and

Слайд 13MANAGERIAL ACCOUNTANTS IN THE ORGANIZATION

MANAGERIAL ACCOUNTANTS IN THE ORGANIZATION

Слайд 14COMPARISON OF FA AND MA

COMPARISON OF FA AND MA

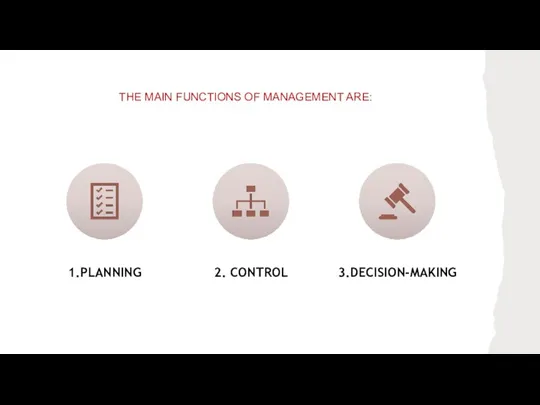

Слайд 15THE MAIN FUNCTIONS OF MANAGEMENT ARE:

THE MAIN FUNCTIONS OF MANAGEMENT ARE:

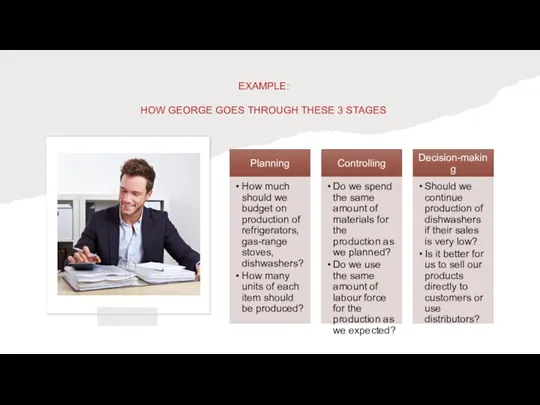

Слайд 16EXAMPLE:

HOW GEORGE GOES THROUGH THESE 3 STAGES

EXAMPLE:

HOW GEORGE GOES THROUGH THESE 3 STAGES

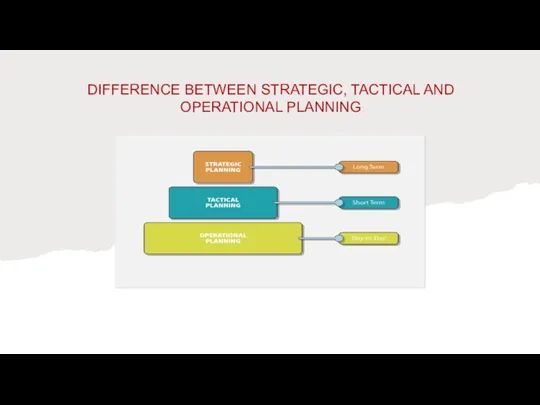

Слайд 17DIFFERENCE BETWEEN STRATEGIC, TACTICAL AND OPERATIONAL PLANNING

DIFFERENCE BETWEEN STRATEGIC, TACTICAL AND OPERATIONAL PLANNING

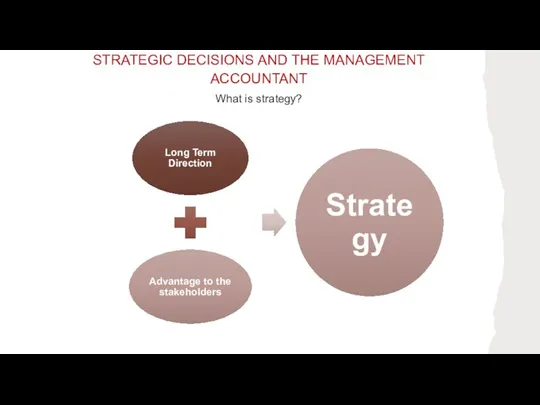

Слайд 18STRATEGIC DECISIONS AND THE MANAGEMENT ACCOUNTANT

What is strategy?

STRATEGIC DECISIONS AND THE MANAGEMENT ACCOUNTANT

What is strategy?

Слайд 19EXAMPLES FOR STRATEGIES

1. Cost leadership strategy

2. Product differentiation

EXAMPLES FOR STRATEGIES

1. Cost leadership strategy

2. Product differentiation

Слайд 20FIVE-STEP DECISION-MAKING PROCESS:

3. Make predictions about the future;

4. Make decisions by choosing

FIVE-STEP DECISION-MAKING PROCESS:

3. Make predictions about the future;

4. Make decisions by choosing

Слайд 21EXAMPLE:

HOW GEORGE GOES THROUGH THESE 5 STAGES

1. Identify the problem and uncertainties.

(Revenue

EXAMPLE:

HOW GEORGE GOES THROUGH THESE 5 STAGES

1. Identify the problem and uncertainties.

(Revenue

Слайд 223 MANAGEMENT ACCOUNTING GUIDELINES:

3 MANAGEMENT ACCOUNTING GUIDELINES:

Слайд 23SOURCES OF DATA

Data is the raw material for data processing.

Information is data that

SOURCES OF DATA

Data is the raw material for data processing.

Information is data that

Слайд 24ATTRIBUTES OF GOOD INFORMATION

Good information should be ACCURATE:

Accurate

Complete

Cost-effective

Understandable

Relevant

Accessible

Timely

Easy to Use

ATTRIBUTES OF GOOD INFORMATION

Good information should be ACCURATE:

Accurate

Complete

Cost-effective

Understandable

Relevant

Accessible

Timely

Easy to Use

Слайд 25TYPES OF INFORMATION:

1. Financial

2. Non-financial

3. A combination of financial and non-financial information

TYPES OF INFORMATION:

1. Financial

2. Non-financial

3. A combination of financial and non-financial information

Слайд 26INFORMATION CAN BE GATHERED EITHER VIA INTERNAL OR EXTERNAL SOURCES

INFORMATION CAN BE GATHERED EITHER VIA INTERNAL OR EXTERNAL SOURCES

Слайд 27SAMPLING TECHNIQUE

Probability sampling methods:

1. Random

2. Systematic

3. Stratified random

4. Multi-stage

5. Cluster

Non-probability sampling

SAMPLING TECHNIQUE

Probability sampling methods:

1. Random

2. Systematic

3. Stratified random

4. Multi-stage

5. Cluster

Non-probability sampling

Слайд 28SAMPLING TECHNIQUE

Source: Saunders, 2019

SAMPLING TECHNIQUE

Source: Saunders, 2019

Слайд 29PRESENTING INFORMATION

1. Written reports;

2. Tables, charts and graphs (need interpretation).

PRESENTING INFORMATION

1. Written reports;

2. Tables, charts and graphs (need interpretation).

Слайд 30IMA STATEMENT OF ETHICAL PROFESSIONAL PRACTICE PRINCIPLES

Honesty

Fairness

Objectivity

Responsibility

IMA STATEMENT OF ETHICAL PROFESSIONAL PRACTICE PRINCIPLES

Honesty

Fairness

Objectivity

Responsibility

Слайд 31IMA STATEMENT OF ETHICAL PROFESSIONAL PRACTICE

STANDARDS

IMA STATEMENT OF ETHICAL PROFESSIONAL PRACTICE

STANDARDS

Слайд 32PROFESSIONAL QUALIFICATIONS AND PROFESSIONAL BODIES

PROFESSIONAL QUALIFICATIONS AND PROFESSIONAL BODIES

Слайд 33LITERATURE

Srikant M. Datar, Madhav V. Rajan (2018), Horngren's Cost Accounting: A Managerial

LITERATURE

Srikant M. Datar, Madhav V. Rajan (2018), Horngren's Cost Accounting: A Managerial

Слайд 34LECTURE ROUNDUP:

1. Financial accounting reports to external users on past financial performance

using

LECTURE ROUNDUP:

1. Financial accounting reports to external users on past financial performance

using

Слайд 35LECTURE ROUNDUP:

5. Data is the raw material for data processing. Data relates

LECTURE ROUNDUP:

5. Data is the raw material for data processing. Data relates

Слайд 36LECTURE ROUNDUP:

9. A non-probability sampling method is a sampling method in which

LECTURE ROUNDUP:

9. A non-probability sampling method is a sampling method in which

Система права

Система права Азбука общения: Почему ты нравишься окружающим или нет

Азбука общения: Почему ты нравишься окружающим или нет Парадоксы бесконечности

Парадоксы бесконечности Берестяные плетёнки

Берестяные плетёнки Огневая подготовка. Правила стрельбы

Огневая подготовка. Правила стрельбы Финансовое обеспечение программы

Финансовое обеспечение программы Характерные проблемы внедрения автоматизированной системы управления персоналом на производственном предприятии

Характерные проблемы внедрения автоматизированной системы управления персоналом на производственном предприятии Как помочь волшебнику

Как помочь волшебнику Презентация на тему Политика и литература 20-30-х годов XX века

Презентация на тему Политика и литература 20-30-х годов XX века Бионика – прикладная наука,

Бионика – прикладная наука, Презентация Microsoft Office PowerPoint

Презентация Microsoft Office PowerPoint Презентация на тему Проблема свободы в романе Ф.М. Достоевского «Преступление и наказание»

Презентация на тему Проблема свободы в романе Ф.М. Достоевского «Преступление и наказание» Описание памятника архитектуры

Описание памятника архитектуры Создание детского кукольного театра на магнитах по мотивам самарского фольклора с использованием лубочной росписи

Создание детского кукольного театра на магнитах по мотивам самарского фольклора с использованием лубочной росписи Психологические возрастные особенности подростка

Психологические возрастные особенности подростка Класификация товаров

Класификация товаров Просвещение участников образовательного процесса специалистами в инклюзивном и специальном образовании

Просвещение участников образовательного процесса специалистами в инклюзивном и специальном образовании Мачты. Монтаж башен и мачт

Мачты. Монтаж башен и мачт Отделка тканей

Отделка тканей Как научить первоклассника кататься на лыжах

Как научить первоклассника кататься на лыжах Подслушано — кроссплатформенный социальный развлекательный проект

Подслушано — кроссплатформенный социальный развлекательный проект Формулы суммы и разности синуса и косинуса

Формулы суммы и разности синуса и косинуса Баланс-2: подготовка и сдача отчетности (Баланс-2W)

Баланс-2: подготовка и сдача отчетности (Баланс-2W) lektsia_6

lektsia_6 Теория литературы. Роды и жанры

Теория литературы. Роды и жанры Авторское право и смежные права

Авторское право и смежные права  Соли, привычная и поваренная соль

Соли, привычная и поваренная соль Милли ризыклар

Милли ризыклар