- Macroeconomics_1

Содержание

- 2. Macroeconomics The Teacher: Ivan Vadimovich Rozmainsky [email protected] [email protected] https://vk.com/ivan_roz https://www.hse.ru/org/persons/915797 Telegram +79811481639

- 3. Macroeconomics Themes of Lectures Capitalism, money, banking and monetary policy (Lecture #1) Determination of GDP under

- 4. Macroeconomics Themes of Classes Calculation of GDP by 3 Methods (Class #1) Keynesian Cross model (Class

- 5. Macroeconomics Lecture 1. Capitalism, money, banking and monetary policy

- 6. What is Capitalism? This is the special economic system analyzed by Macroeconomics! Features of Capitalism include:

- 7. What is Money? Money is what money does! That is: any asset performing all functions of

- 8. In other words: Money is… Money is the set of assets in the economy that people

- 9. The brief history of money First, there was barter Then, there was commodity money This money

- 10. The types of contemporary money Currency is the paper bills and coins in the hands of

- 11. The story about monetary aggregates Monetary Aggregates are broad categories that measure the money supply in

- 12. The simplest structure of contemporary money supply The money supply equals currency plus demand (checking account)

- 13. Some basic concepts of Banking Reserves (R ): the portion of deposits that banks have not

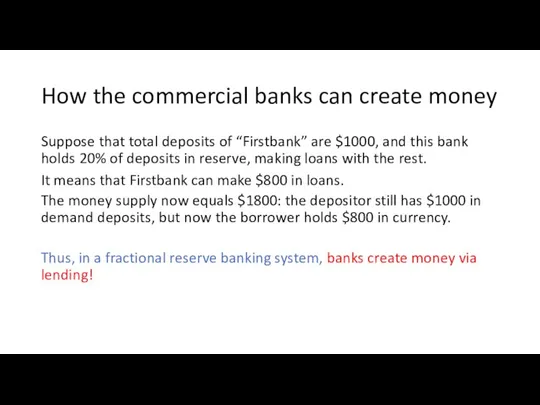

- 14. How the commercial banks can create money Suppose that total deposits of “Firstbank” are $1000, and

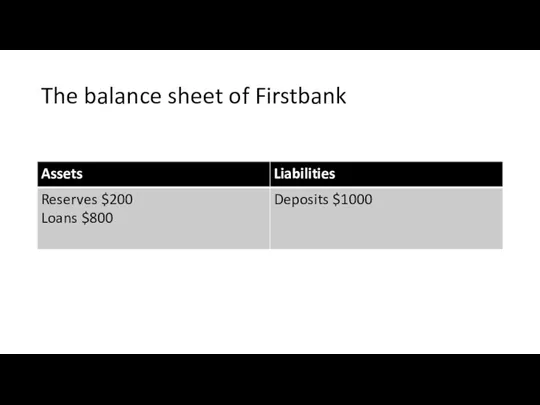

- 15. The balance sheet of Firstbank

- 16. The story continues… Suppose the borrower deposits the $800 in Secondbank. But then Secondbank will loan

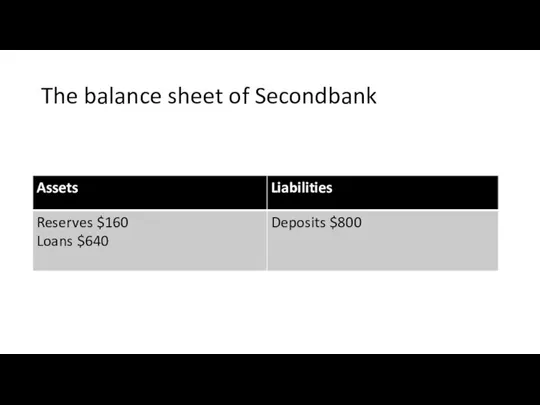

- 17. The balance sheet of Secondbank

- 18. The next stage of this story… If this $640 is eventually deposited in Thirdbank then Thirdbank

- 19. The balance sheet of Thirdbank

- 20. Finding the total money supply Original deposit = $1000 + Firstbank lending = $ 800 +

- 21. Some important conclusions about the role of banks in the money-creating process - A fractional reserve

- 22. What is monetary policy? Monetary policy is policy adopted by the monetary authority of a nation

- 23. Monetary policy can be expansionary or restrictive Monetary policy is expansionary if the central bank tries

- 24. The main instruments of monetary policy Reserve requirements. Discount rate/base rate Open market operations

- 25. Reserve requirements The reserve requirement is regulation that sets the minimum amount of reserves that must

- 26. The discount rate/base rate The discount rate/base rate is price of borrowing money from the central

- 27. Open market operations Open market operations are an activity by a central bank to give (or

- 28. If the central bank wants to make expansionary policy that it will Soften reserve requirements. Reduce

- 29. If the central bank wants to make restrictive policy that it will Tighten reserve requirements. Increase

- 30. Something about the demand for money The effectiveness of monetary policy depends on – other things

- 31. The price level as a factor of the demand for money A rise in the price

- 32. The interest rate as a factor of the demand for money The interest rate is the

- 33. The real GDP as a factor of the demand for money The idea is that people

- 34. Financial innovations as a factor of the demand for money Financial innovation that lowers the cost

- 35. The money supply and the demand for money together Economists usually prefer to construct macroeconomic models

- 36. The money market equilibrium

- 37. The consequences of an increase in the nominal money supply

- 38. The consequences of an increase in the price level

- 40. Скачать презентацию

Слайд 2Macroeconomics

The Teacher: Ivan Vadimovich Rozmainsky

[email protected]

[email protected]

https://vk.com/ivan_roz

https://www.hse.ru/org/persons/915797

Telegram +79811481639

Macroeconomics

The Teacher: Ivan Vadimovich Rozmainsky

[email protected]

[email protected]

https://vk.com/ivan_roz

https://www.hse.ru/org/persons/915797

Telegram +79811481639

Слайд 3Macroeconomics

Themes of Lectures

Capitalism, money, banking and monetary policy (Lecture #1)

Determination of

Macroeconomics

Themes of Lectures

Capitalism, money, banking and monetary policy (Lecture #1)

Determination of

Слайд 4Macroeconomics

Themes of Classes

Calculation of GDP by 3 Methods (Class #1)

Keynesian Cross

Macroeconomics

Themes of Classes

Calculation of GDP by 3 Methods (Class #1)

Keynesian Cross

Слайд 5Macroeconomics

Lecture 1.

Capitalism, money, banking and monetary policy

Macroeconomics

Lecture 1.

Capitalism, money, banking and monetary policy

Слайд 6What is Capitalism?

This is the special economic system analyzed by Macroeconomics!

Features of

What is Capitalism?

This is the special economic system analyzed by Macroeconomics!

Features of

Слайд 7What is Money?

Money is what money does!

That is: any asset performing all

What is Money?

Money is what money does!

That is: any asset performing all

Слайд 8In other words: Money is…

Money is the set of assets in the

In other words: Money is…

Money is the set of assets in the

Слайд 9The brief history of money

First, there was barter

Then, there was commodity money

The brief history of money

First, there was barter

Then, there was commodity money

Слайд 10The types of contemporary money

Currency is the paper bills and coins in

The types of contemporary money

Currency is the paper bills and coins in

Слайд 11The story about monetary aggregates

Monetary Aggregates are broad categories that measure the

The story about monetary aggregates

Monetary Aggregates are broad categories that measure the

Слайд 12The simplest structure of contemporary money supply

The money supply equals currency plus

The simplest structure of contemporary money supply

The money supply equals currency plus

Слайд 13Some basic concepts of Banking

Reserves (R ): the portion of deposits that

Some basic concepts of Banking

Reserves (R ): the portion of deposits that

Слайд 14How the commercial banks can create money

Suppose that total deposits of “Firstbank”

How the commercial banks can create money

Suppose that total deposits of “Firstbank”

Слайд 15The balance sheet of Firstbank

The balance sheet of Firstbank

Слайд 16The story continues…

Suppose the borrower deposits the $800 in Secondbank.

But then Secondbank

The story continues…

Suppose the borrower deposits the $800 in Secondbank.

But then Secondbank

Слайд 17The balance sheet of Secondbank

The balance sheet of Secondbank

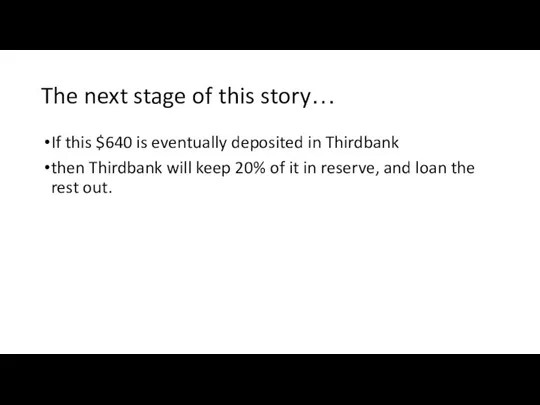

Слайд 18The next stage of this story…

If this $640 is eventually deposited in

The next stage of this story…

If this $640 is eventually deposited in

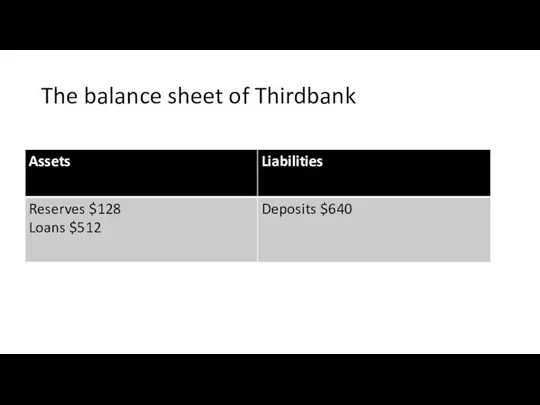

Слайд 19The balance sheet of Thirdbank

The balance sheet of Thirdbank

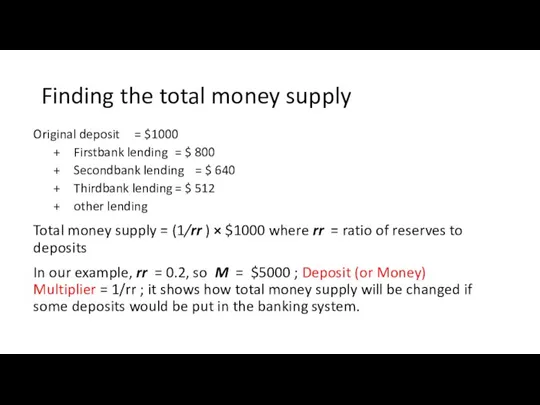

Слайд 20Finding the total money supply

Original deposit = $1000

+ Firstbank lending = $ 800

+

Finding the total money supply

Original deposit = $1000

+ Firstbank lending = $ 800

+

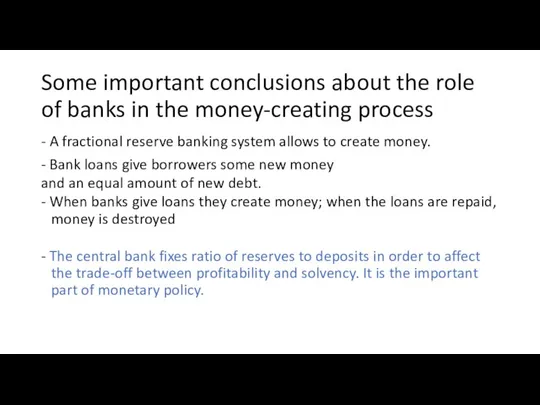

Слайд 21Some important conclusions about the role of banks in the money-creating process

-

Some important conclusions about the role of banks in the money-creating process

-

Слайд 22What is monetary policy?

Monetary policy is policy adopted by the monetary authority of

What is monetary policy?

Monetary policy is policy adopted by the monetary authority of

Слайд 23Monetary policy can be expansionary or restrictive

Monetary policy is expansionary if the

Monetary policy can be expansionary or restrictive

Monetary policy is expansionary if the

Слайд 24The main instruments of monetary policy

Reserve requirements.

Discount rate/base rate

Open market operations

The main instruments of monetary policy

Reserve requirements.

Discount rate/base rate

Open market operations

Слайд 25Reserve requirements

The reserve requirement is regulation that sets the minimum amount of reserves that

Reserve requirements

The reserve requirement is regulation that sets the minimum amount of reserves that

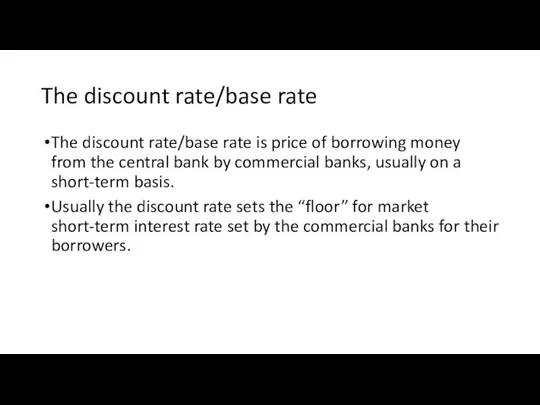

Слайд 26The discount rate/base rate

The discount rate/base rate is price of borrowing money

The discount rate/base rate

The discount rate/base rate is price of borrowing money

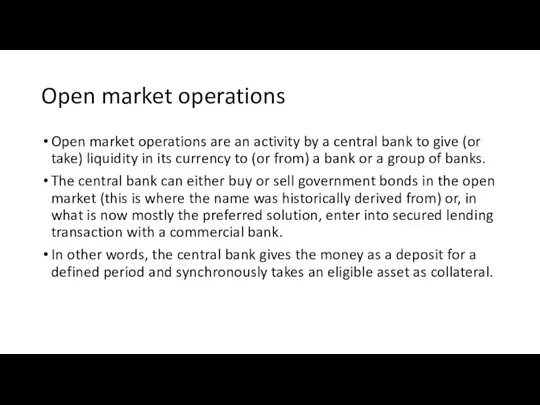

Слайд 27Open market operations

Open market operations are an activity by a central bank to give (or

Open market operations

Open market operations are an activity by a central bank to give (or

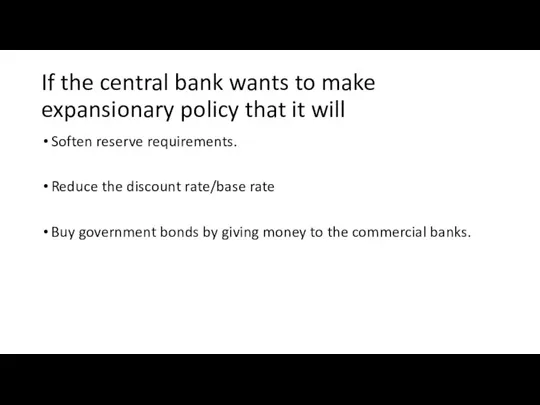

Слайд 28If the central bank wants to make expansionary policy that it will

Soften

If the central bank wants to make expansionary policy that it will

Soften

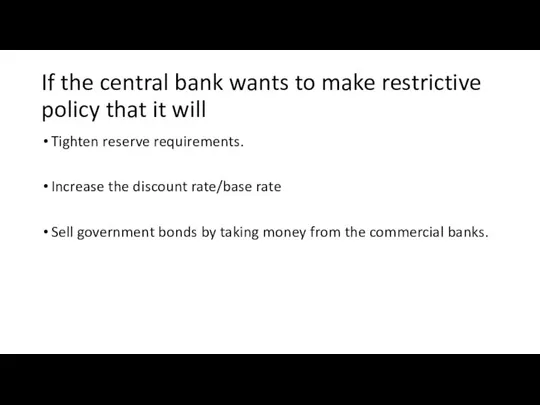

Слайд 29If the central bank wants to make restrictive policy that it will

Tighten

If the central bank wants to make restrictive policy that it will

Tighten

Слайд 30Something about the demand for money

The effectiveness of monetary policy depends on

Something about the demand for money

The effectiveness of monetary policy depends on

Слайд 31The price level as a factor of the demand for money

A rise

The price level as a factor of the demand for money

A rise

Слайд 32The interest rate as a factor of the demand for money

The interest

The interest rate as a factor of the demand for money

The interest

Слайд 33The real GDP as a factor of the demand for money

The idea

The real GDP as a factor of the demand for money

The idea

Слайд 34Financial innovations as a factor of the demand for money

Financial innovation that

Financial innovations as a factor of the demand for money

Financial innovation that

Слайд 35The money supply and the demand for money together

Economists usually prefer to

The money supply and the demand for money together

Economists usually prefer to

Слайд 36The money market equilibrium

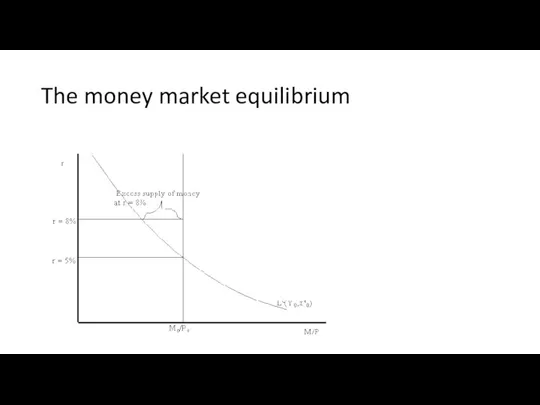

The money market equilibrium

Слайд 37The consequences of an increase in the nominal money supply

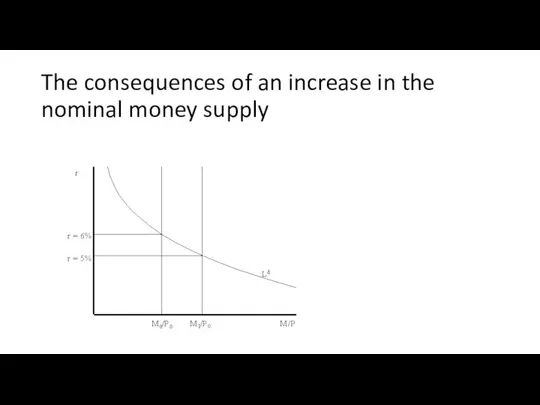

The consequences of an increase in the nominal money supply

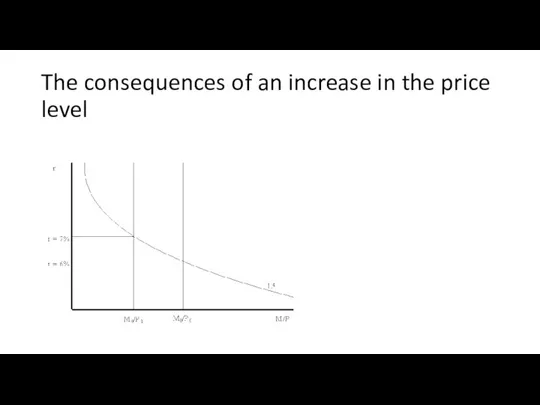

Слайд 38The consequences of an increase in the price level

The consequences of an increase in the price level

20141110_prezentatsiya8

20141110_prezentatsiya8 Объекты для Субъектов МСП, включенные в перечень муниципального имущества г.о. Новокуйбышевск

Объекты для Субъектов МСП, включенные в перечень муниципального имущества г.о. Новокуйбышевск ДОКЛАД О СОСТОЯНИИ И РЕЗУЛЬТАТАХ ДЕЯТЕЛЬНОСТИ за 2010-2011 учебный год

ДОКЛАД О СОСТОЯНИИ И РЕЗУЛЬТАТАХ ДЕЯТЕЛЬНОСТИ за 2010-2011 учебный год ОТЕЧЕСТВЕННАЯ ВОЙНА 1812года.

ОТЕЧЕСТВЕННАЯ ВОЙНА 1812года. Презентация на тему «Основы стереометрии»

Презентация на тему «Основы стереометрии» Логистика как инструмент снижения издержек

Логистика как инструмент снижения издержек  Hollywood, 9 классе

Hollywood, 9 классе Кукла Травница. Оберег

Кукла Травница. Оберег ПРОГРЕССТЕХ

ПРОГРЕССТЕХ Упражнения на гимнастических скамейках

Упражнения на гимнастических скамейках Азбука этикета

Азбука этикета Эритроциты

Эритроциты Panda Meetup Анна Панферова

Panda Meetup Анна Панферова Соревновательная деятельность теннисистов и аспекты ее оптимизации

Соревновательная деятельность теннисистов и аспекты ее оптимизации Лоу-Кост по Европе

Лоу-Кост по Европе Магистерская программа "Социальная философия"

Магистерская программа "Социальная философия" Срочно требуются грузчики-комплектовщики!!!

Срочно требуются грузчики-комплектовщики!!! Презентація(3)(1)

Презентація(3)(1) Презентация на тему Строение вещества

Презентация на тему Строение вещества История развития олимпийского движения в России

История развития олимпийского движения в России Пример внедрения в крупной розничной сети. "1С:Магазин одежды и обуви"

Пример внедрения в крупной розничной сети. "1С:Магазин одежды и обуви" Методологические и методические основы преподавания истории. (Тема 3)

Методологические и методические основы преподавания истории. (Тема 3) Педагогический совет:

Педагогический совет: Нужен ли нашему городу экологически чистый транспорт

Нужен ли нашему городу экологически чистый транспорт ПОИСК ПЕРСОНАЛА В СЕТИ ИНТЕРНЕТ

ПОИСК ПЕРСОНАЛА В СЕТИ ИНТЕРНЕТ Салаты из свежих овощей

Салаты из свежих овощей Ivan

Ivan Занимательные прищепки

Занимательные прищепки