- Organizing Production

Содержание

- 2. After studying this chapter you will be able to Explain what a firm is and describe

- 3. The invention of the World Wide Web has paved the way for the creation of thousands

- 4. The Firm and Its Economic Problem A firm is an institution that hires factors of production

- 5. Accounting Profit Accountants measure a firm’s profit to ensure that the firm pays the correct amount

- 6. Economic Profit Economists measure a firm’s profit to enable them to predict the firm’s decisions, and

- 7. A Firm’s Opportunity Cost of Production A firm’s opportunity cost of production is the value of

- 8. Resources Bought in the Market The amount spent by a firm on resources bought in the

- 9. Resources Owned by the Firm If the firm owns capital and uses it to produce its

- 10. The implicit rental rate of capital is made up of 1. Economic depreciation 2. Interest forgone

- 11. Resources Supplied by the Firm’s Owner The owner might supply both entrepreneurship and labor. The return

- 12. In addition to supplying entrepreneurship, the owner might supply labor but not take as wage. The

- 13. The Firm and Its Economic Problem

- 14. The Firm’s Decisions To maximize profit, a firm must make five basic decisions: 1. What to

- 15. The Firm’s Constraints The firm’s profit is limited by three features of the environment: Technology constraints

- 16. Technology Constraints Technology is any method of producing a good or service. Technology advances over time.

- 17. Information Constraints A firm never possesses complete information about either the present or the future. It

- 18. Market Constraints What a firm can sell and the price it can obtain are constrained by

- 19. Technology and Economic Efficiency Technological Efficiency Technological efficiency occurs when a firm produces a given level

- 20. Technology and Economic Efficiency Table 10.2 sets out the labor and capital required to produce 10

- 21. Economic Efficiency Economic efficiency occurs when the firm produces a given level of output at the

- 22. An economically efficient production process also is technologically efficient. A technologically efficient process may not be

- 23. Technology and Economic Efficiency When the wage rate is $75 a day and the rental rate

- 25. Information and Organization A firm organizes production by combining and coordinating productive resources using a mixture

- 26. Command Systems A command system uses a managerial hierarchy. Commands pass downward through the hierarchy and

- 27. Incentive Systems An incentive system is a method of organizing production that uses a market-like mechanism

- 28. Mixing the Systems Most firms use a mix of command and incentive systems to maximize profit.

- 29. The Principal–Agent Problem The principal–agent problem is the problem of devising compensation rules that induce an

- 30. Coping with the Principal–Agent Problem Three ways of coping with the principal–agent problem are Ownership Incentive

- 31. Ownership, often offered to managers, gives the managers an incentive to maximize the firm’s profits, which

- 32. Types of Business Organization There are three types of business organization: Proprietorship Partnership Corporation Information and

- 33. Proprietorship A proprietorship is a firm with a single owner who has unlimited liability, or legal

- 34. Partnership A partnership is a firm with two or more owners who have unlimited liability. Partners

- 35. Corporation A corporation is owned by one or more stockholders with limited liability, which means the

- 36. Pros and Cons of Different Types of Firms Each type of business organization has advantages and

- 38. Proprietorships Are easy to set up Managerial decision making is simple Profits are taxed only once

- 39. Partnerships Are easy to set up Employ diversified decision-making processes Can survive the withdrawal of a

- 40. Corporation Limited liability for its owners Large-scale and low-cost capital that is readily available Professional management

- 41. Markets and the Competitive Environment Economists identify four market types: 1. Perfect competition 2. Monopolistic competition

- 42. Perfect competition is a market structure with Many firms Each sells an identical product Many buyers

- 43. Monopolistic competition is a market structure with Many firms Each firm produces similar but slightly different

- 44. Oligopoly is a market structure in which A small number of firms compete. The firms might

- 45. Monopoly is a market structure in which One firm produces the entire output of the industry.

- 46. Measures of Concentration Economists use two measures of market concentration: The four-firm concentration ratio The Herfindahl–Hirschman

- 47. The Four-Firm Concentration Ratio The four-firm concentration ratio is the percentage of the total industry sales

- 48. Markets and the Competitive Environment

- 49. The Herfindahl–Hirschman Index The Herfindahl–Hirschman index (HHI) is the square of percentage market share of each

- 50. Markets and the Competitive Environment Concentration Measures for the U.S. Economy Figure 9.2 shows some concentration

- 51. Markets and the Competitive Environment Figure 10.2 shows the four-firm concentration ratio for various industries in

- 53. Limitations of Concentration Measures The main limitations of only using concentration measure as determinants of market

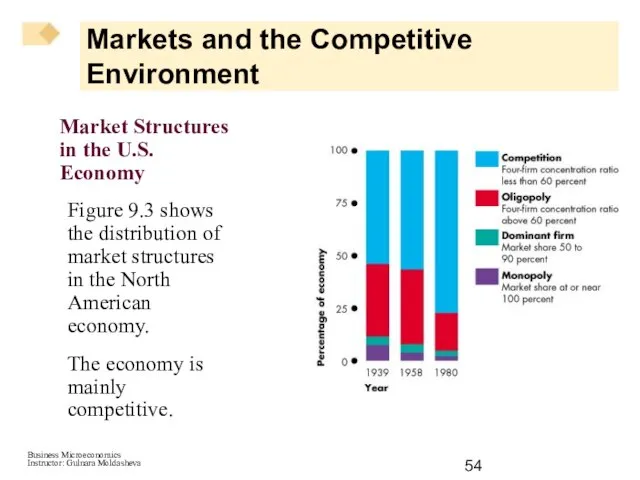

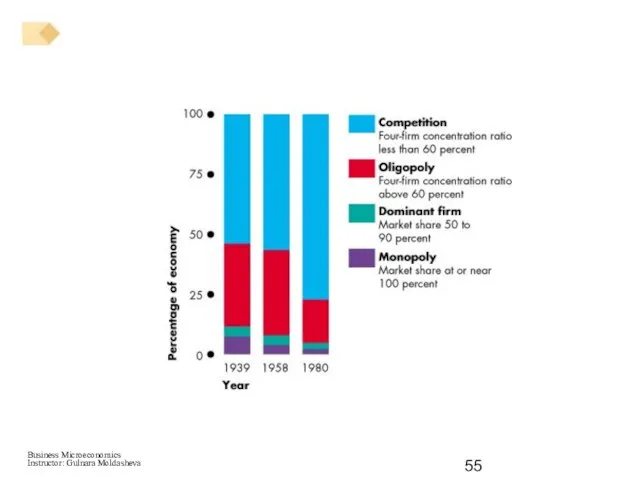

- 54. Markets and the Competitive Environment Market Structures in the U.S. Economy Figure 9.3 shows the distribution

- 56. Markets and Firms Market Coordination Markets both coordinate production. Chapter 3 explains how demand and supply

- 57. Why Firms? Firms coordinate production when they can do so more efficiently than a market. Four

- 58. Transactions costs are the costs arising from finding someone with whom to do business, reaching agreement

- 59. Terms Along the Way firm corporation stock bond profit (economic profit) total revenue total cost explicit

- 60. Test Yourself 1.Which is not a legal form of business? Sole proprietorship. Partnership. Corporation. Limited liability.

- 61. Test Yourself 2. The stock exchanges are an example of a primary market. secondary market. sole

- 63. Скачать презентацию

Слайд 3The invention of the World Wide Web has paved the way for

The invention of the World Wide Web has paved the way for

Слайд 4The Firm and Its Economic Problem

A firm is an institution that hires

The Firm and Its Economic Problem

A firm is an institution that hires

Слайд 5Accounting Profit

Accountants measure a firm’s profit to ensure that the firm pays

Accounting Profit

Accountants measure a firm’s profit to ensure that the firm pays

Слайд 6Economic Profit

Economists measure a firm’s profit to enable them to predict the

Economic Profit

Economists measure a firm’s profit to enable them to predict the

Слайд 7A Firm’s Opportunity Cost of Production

A firm’s opportunity cost of production is

A Firm’s Opportunity Cost of Production

A firm’s opportunity cost of production is

Слайд 8Resources Bought in the Market

The amount spent by a firm on resources

Resources Bought in the Market

The amount spent by a firm on resources

Слайд 9Resources Owned by the Firm

If the firm owns capital and uses it

Resources Owned by the Firm

If the firm owns capital and uses it

Слайд 10The implicit rental rate of capital is made up of

1. Economic depreciation

2.

The implicit rental rate of capital is made up of

1. Economic depreciation

2.

Слайд 11Resources Supplied by the Firm’s Owner

The owner might supply both entrepreneurship and

Resources Supplied by the Firm’s Owner

The owner might supply both entrepreneurship and

Слайд 12In addition to supplying entrepreneurship, the owner might supply labor but not

In addition to supplying entrepreneurship, the owner might supply labor but not

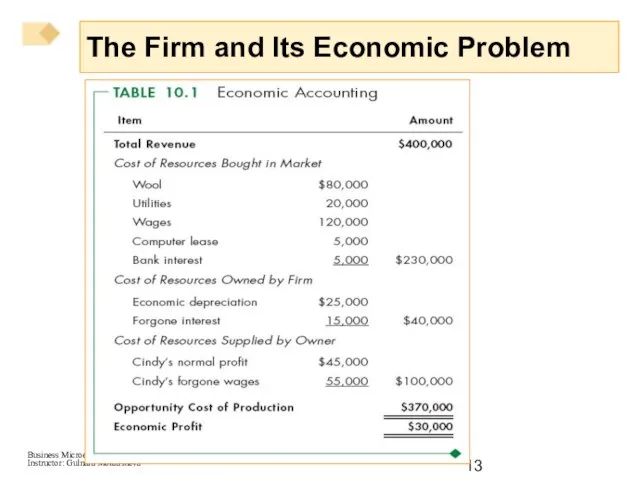

Слайд 13The Firm and Its Economic Problem

The Firm and Its Economic Problem

Слайд 14The Firm’s Decisions

To maximize profit, a firm must make five basic decisions:

1.

The Firm’s Decisions

To maximize profit, a firm must make five basic decisions:

1.

Слайд 15The Firm’s Constraints

The firm’s profit is limited by three features of the

The Firm’s Constraints

The firm’s profit is limited by three features of the

Слайд 16Technology Constraints

Technology is any method of producing a good or service.

Technology Constraints

Technology is any method of producing a good or service.

Слайд 17Information Constraints

A firm never possesses complete information about either the present

Information Constraints

A firm never possesses complete information about either the present

Слайд 18Market Constraints

What a firm can sell and the price it can

Market Constraints

What a firm can sell and the price it can

Слайд 19Technology and Economic Efficiency

Technological Efficiency

Technological efficiency occurs when a firm produces a

Technology and Economic Efficiency

Technological Efficiency

Technological efficiency occurs when a firm produces a

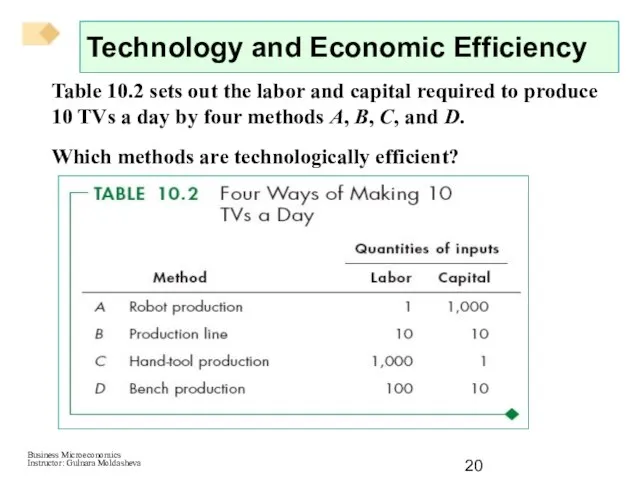

Слайд 20Technology and Economic Efficiency

Table 10.2 sets out the labor and capital required

Technology and Economic Efficiency

Table 10.2 sets out the labor and capital required

Слайд 21Economic Efficiency

Economic efficiency occurs when the firm produces a given level of

Economic Efficiency

Economic efficiency occurs when the firm produces a given level of

Слайд 22An economically efficient production process also is technologically efficient.

A technologically efficient process

An economically efficient production process also is technologically efficient.

A technologically efficient process

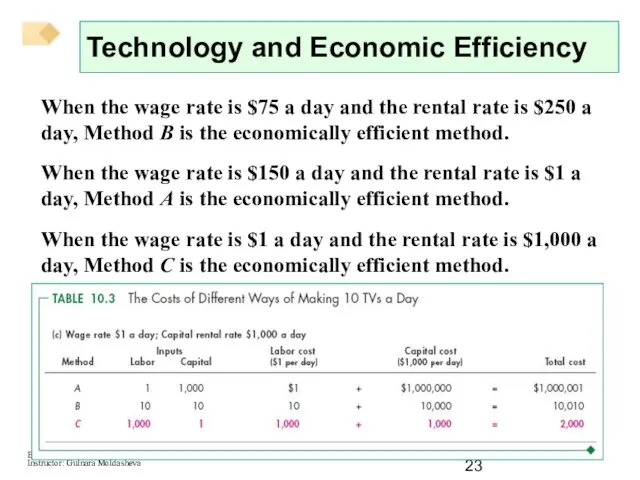

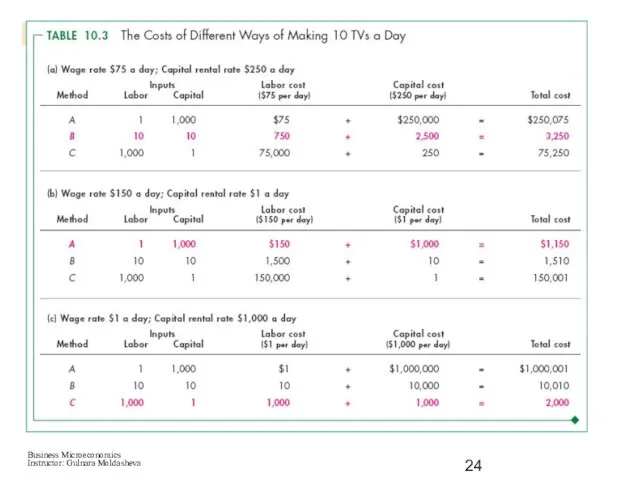

Слайд 23Technology and Economic Efficiency

When the wage rate is $75 a day and

Technology and Economic Efficiency

When the wage rate is $75 a day and

Слайд 25Information and Organization

A firm organizes production by combining and coordinating productive resources

Information and Organization

A firm organizes production by combining and coordinating productive resources

Слайд 26Command Systems

A command system uses a managerial hierarchy.

Commands pass downward through

Command Systems

A command system uses a managerial hierarchy.

Commands pass downward through

Слайд 27Incentive Systems

An incentive system is a method of organizing production that uses

Incentive Systems

An incentive system is a method of organizing production that uses

Слайд 28Mixing the Systems

Most firms use a mix of command and incentive systems

Mixing the Systems

Most firms use a mix of command and incentive systems

Слайд 29The Principal–Agent Problem

The principal–agent problem is the problem of devising compensation rules

The Principal–Agent Problem

The principal–agent problem is the problem of devising compensation rules

Слайд 30Coping with the Principal–Agent Problem

Three ways of coping with the principal–agent problem

Coping with the Principal–Agent Problem

Three ways of coping with the principal–agent problem

Слайд 31Ownership, often offered to managers, gives the managers an incentive to maximize

Ownership, often offered to managers, gives the managers an incentive to maximize

Слайд 32Types of Business Organization

There are three types of business organization:

Proprietorship

Partnership

Types of Business Organization

There are three types of business organization:

Proprietorship

Partnership

Слайд 33Proprietorship

A proprietorship is a firm with a single owner who has unlimited

Proprietorship

A proprietorship is a firm with a single owner who has unlimited

Слайд 34Partnership

A partnership is a firm with two or more owners who have

Partnership

A partnership is a firm with two or more owners who have

Слайд 35Corporation

A corporation is owned by one or more stockholders with limited

Corporation

A corporation is owned by one or more stockholders with limited

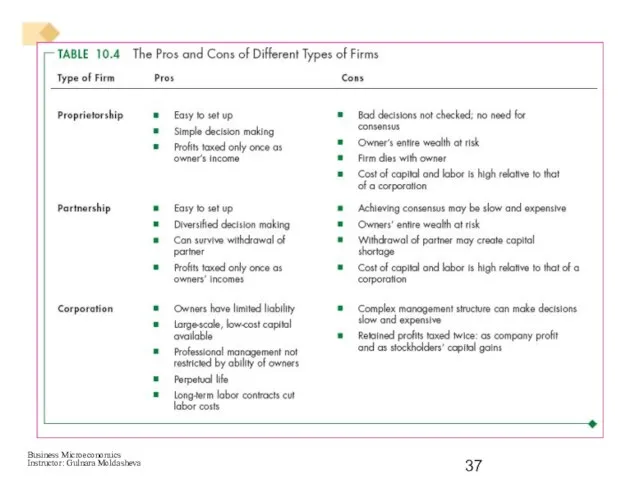

Слайд 36Pros and Cons of Different Types of Firms

Each type of business organization

Pros and Cons of Different Types of Firms

Each type of business organization

Слайд 38Proprietorships

Are easy to set up

Managerial decision making is simple

Profits are taxed only

Proprietorships

Are easy to set up

Managerial decision making is simple

Profits are taxed only

Слайд 39Partnerships

Are easy to set up

Employ diversified decision-making processes

Can survive the withdrawal of

Partnerships

Are easy to set up

Employ diversified decision-making processes

Can survive the withdrawal of

Слайд 40Corporation

Limited liability for its owners

Large-scale and low-cost capital that is readily

Corporation

Limited liability for its owners

Large-scale and low-cost capital that is readily

Слайд 41Markets and the Competitive Environment

Economists identify four market types:

1. Perfect competition

2. Monopolistic

Markets and the Competitive Environment

Economists identify four market types:

1. Perfect competition

2. Monopolistic

Слайд 42Perfect competition is a market structure with

Many firms

Each sells an identical product

Many

Perfect competition is a market structure with

Many firms

Each sells an identical product

Many

Слайд 43Monopolistic competition is a market structure with

Many firms

Each firm produces similar but

Monopolistic competition is a market structure with

Many firms

Each firm produces similar but

Слайд 44Oligopoly is a market structure in which

A small number of firms compete.

The

Oligopoly is a market structure in which

A small number of firms compete.

The

Слайд 45Monopoly is a market structure in which

One firm produces the entire output

Monopoly is a market structure in which

One firm produces the entire output

Слайд 46Measures of Concentration

Economists use two measures of market concentration:

The four-firm

Measures of Concentration

Economists use two measures of market concentration:

The four-firm

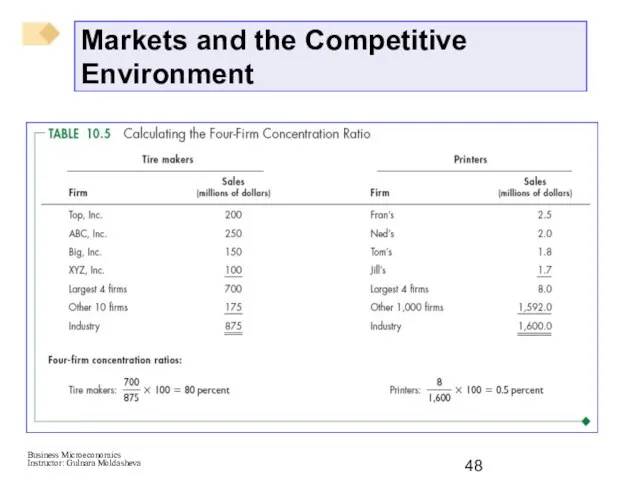

Слайд 47The Four-Firm Concentration Ratio

The four-firm concentration ratio is the percentage of the

The Four-Firm Concentration Ratio

The four-firm concentration ratio is the percentage of the

Слайд 48Markets and the Competitive Environment

Markets and the Competitive Environment

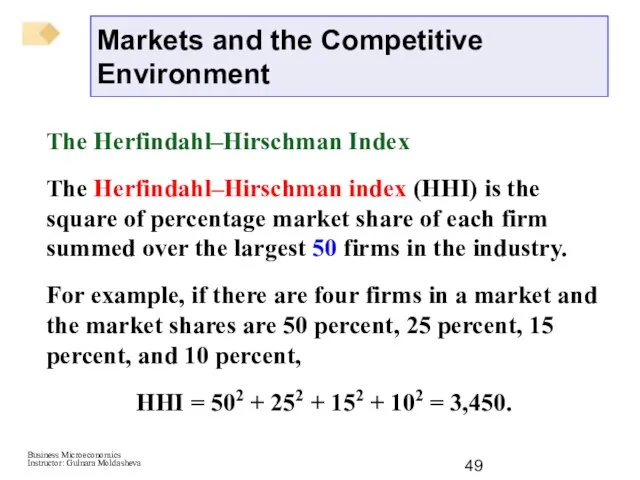

Слайд 49The Herfindahl–Hirschman Index

The Herfindahl–Hirschman index (HHI) is the square of percentage

The Herfindahl–Hirschman Index

The Herfindahl–Hirschman index (HHI) is the square of percentage

Слайд 50Markets and the Competitive Environment

Concentration Measures for the U.S. Economy

Figure 9.2 shows

Markets and the Competitive Environment

Concentration Measures for the U.S. Economy

Figure 9.2 shows

Слайд 51Markets and the Competitive Environment

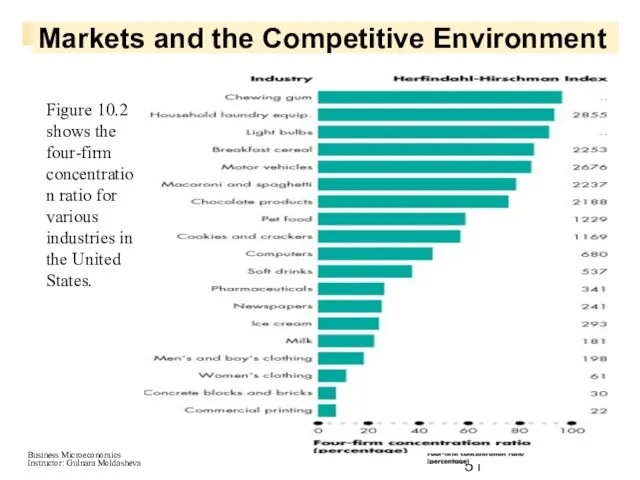

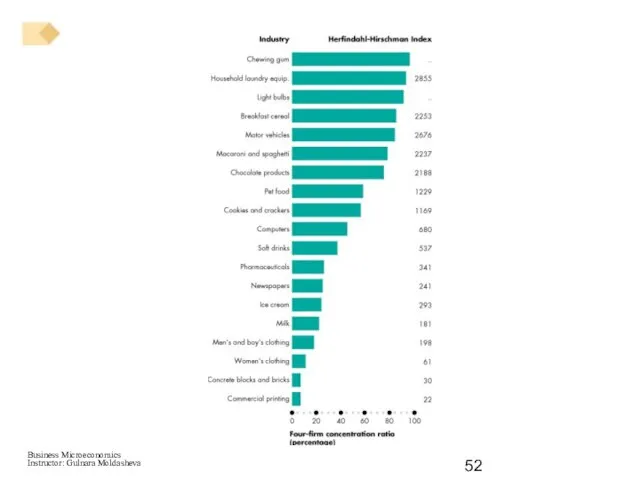

Figure 10.2 shows the four-firm concentration ratio for

Markets and the Competitive Environment

Figure 10.2 shows the four-firm concentration ratio for

Слайд 53Limitations of Concentration Measures

The main limitations of only using concentration measure as

Limitations of Concentration Measures

The main limitations of only using concentration measure as

Слайд 54Markets and the Competitive Environment

Market Structures in the U.S. Economy

Figure 9.3 shows

Markets and the Competitive Environment

Market Structures in the U.S. Economy

Figure 9.3 shows

Слайд 56Markets and Firms

Market Coordination

Markets both coordinate production.

Chapter 3 explains how demand and

Markets and Firms

Market Coordination

Markets both coordinate production.

Chapter 3 explains how demand and

Слайд 57Why Firms?

Firms coordinate production when they can do so more efficiently than

Why Firms?

Firms coordinate production when they can do so more efficiently than

Слайд 58Transactions costs are the costs arising from finding someone with whom to

Transactions costs are the costs arising from finding someone with whom to

Слайд 59Terms Along the Way

firm

corporation

stock

bond

profit (economic profit)

total revenue

total cost

explicit cost

implicit opportunity cost (implicit

Terms Along the Way

firm

corporation

stock

bond

profit (economic profit)

total revenue

total cost

explicit cost

implicit opportunity cost (implicit

Слайд 60Test Yourself

1.Which is not a legal form of business?

Sole proprietorship.

Partnership.

Corporation.

Limited liability.

Test Yourself

1.Which is not a legal form of business?

Sole proprietorship.

Partnership.

Corporation.

Limited liability.

Слайд 61Test Yourself

2. The stock exchanges are an example of a

primary market.

secondary market.

sole

Test Yourself

2. The stock exchanges are an example of a

primary market.

secondary market.

sole

Нашествие с Востока на Русь

Нашествие с Востока на Русь От пера к компьютеру

От пера к компьютеру Мощный инструмент управления персоналом

Мощный инструмент управления персоналом Потерянные слова Missed Words

Потерянные слова Missed Words Масленица. Празднование масленицы

Масленица. Празднование масленицы 2209 кейс Софии

2209 кейс Софии Изменения в культуре и быте в первой четверти XVIII века

Изменения в культуре и быте в первой четверти XVIII века Создание проблемных ситуаций на уроках математики

Создание проблемных ситуаций на уроках математики Борьба с агрессией крестоносцев в XIII-XVI вв

Борьба с агрессией крестоносцев в XIII-XVI вв gtz

gtz Результаты деятельности по направлению ОТ и ПБ на проекте Карьер АО СГОК 09.11.2021

Результаты деятельности по направлению ОТ и ПБ на проекте Карьер АО СГОК 09.11.2021 ОРГАНИЗАЦИЯ ОБЩЕЙ ВРАЧЕБНОЙ ПРАКТИКИ (СЕМЕЙНОЙ МЕДИЦИНЫ) В УСЛОВИЯХ КРУПНОГО ГОРОДА

ОРГАНИЗАЦИЯ ОБЩЕЙ ВРАЧЕБНОЙ ПРАКТИКИ (СЕМЕЙНОЙ МЕДИЦИНЫ) В УСЛОВИЯХ КРУПНОГО ГОРОДА Западная Европа в 16-17 вв. Общая характеристика эпохи Раннего Нового времени

Западная Европа в 16-17 вв. Общая характеристика эпохи Раннего Нового времени Перечень инструкций по ОТ

Перечень инструкций по ОТ Зигмунд Фрейд

Зигмунд Фрейд Оборотные средства

Оборотные средства Прилагательные и наречия

Прилагательные и наречия Презентация на тему Интерактивный грамматический тест

Презентация на тему Интерактивный грамматический тест  Золотое сечение в пропорциях тела человека

Золотое сечение в пропорциях тела человека Советско-афганская война1979-1989 гг.

Советско-афганская война1979-1989 гг. Урок 15

Урок 15 Долг и совесть (8 класс)

Долг и совесть (8 класс) Ярмарочное гулянье

Ярмарочное гулянье Epr.electrolux.com

Epr.electrolux.com Как жили земледельцы и ремесленники в Египте

Как жили земледельцы и ремесленники в Египте Карлсон

Карлсон Уход за кожей лица в течении суток

Уход за кожей лица в течении суток Электронные таблицы Microsoft Excel

Электронные таблицы Microsoft Excel