- Perfect Competition

Содержание

- 3. Airlines and automobile producers are facing tough times: Prices are being slashed to drive sales and

- 4. What Is Perfect Competition? Perfect competition is an industry in which Many firms sell identical products

- 5. How Perfect Competition Arises Perfect competition arises: When firm’s minimum efficient scale is small relative to

- 6. Price Takers In perfect competition, each firm is a price taker. A price taker is a

- 7. Economic Profit and Revenue The goal of each firm is to maximize economic profit, which equals

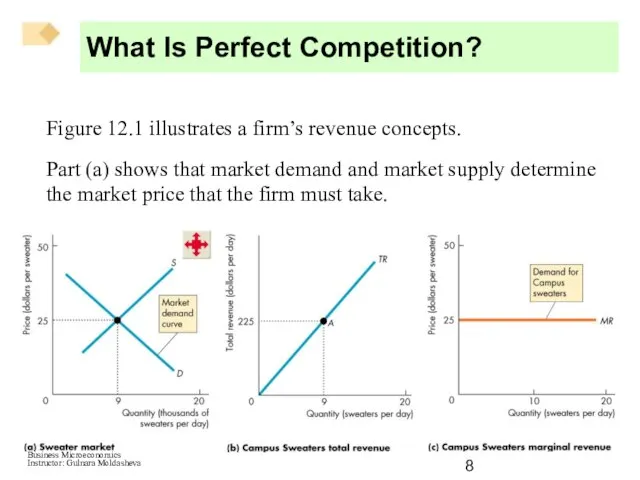

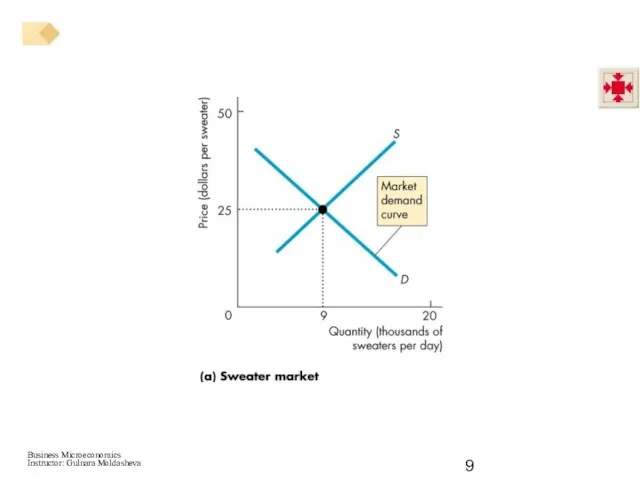

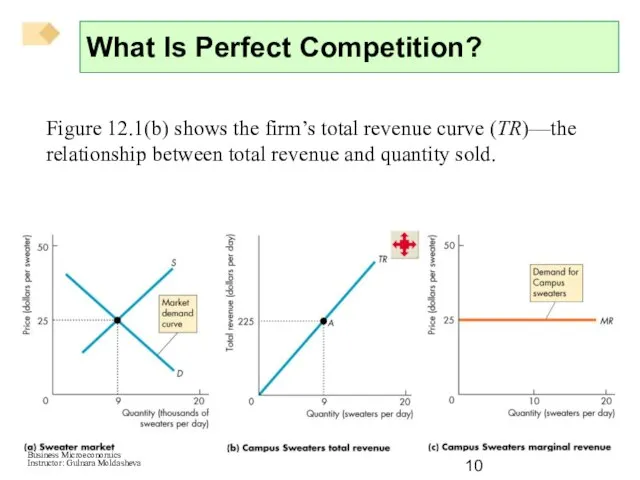

- 8. Figure 12.1 illustrates a firm’s revenue concepts. Part (a) shows that market demand and market supply

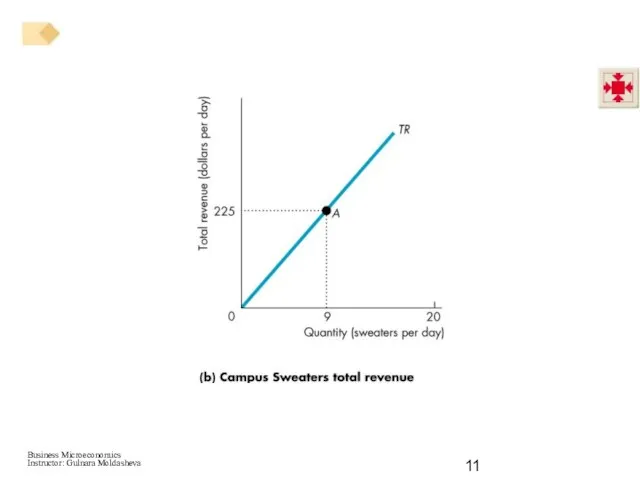

- 10. Figure 12.1(b) shows the firm’s total revenue curve (TR)—the relationship between total revenue and quantity sold.

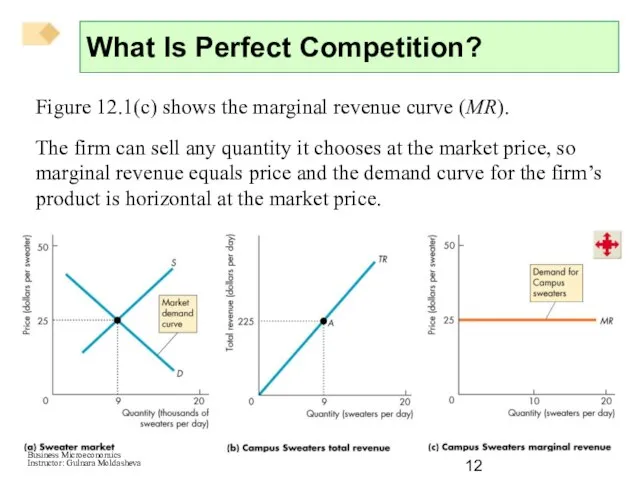

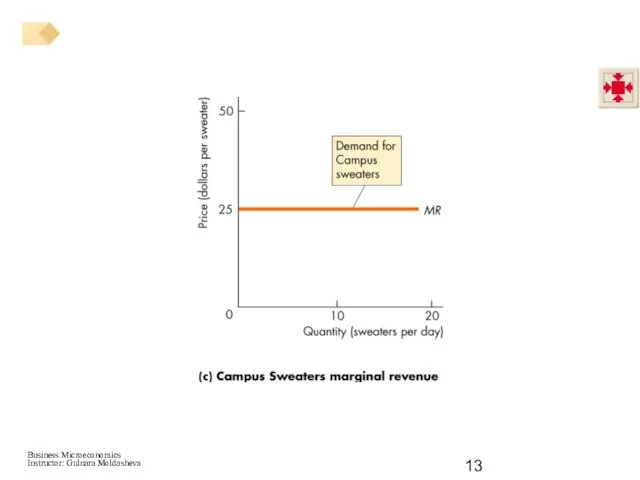

- 12. Figure 12.1(c) shows the marginal revenue curve (MR). The firm can sell any quantity it chooses

- 14. The demand for a firm’s product is perfectly elastic because one firm’s sweater is a perfect

- 15. A perfectly competitive firm’s goal is to make maximum economic profit, given the constraints it faces.

- 16. Profit-Maximizing Output A perfectly competitive firm chooses the output that maximizes its economic profit. One way

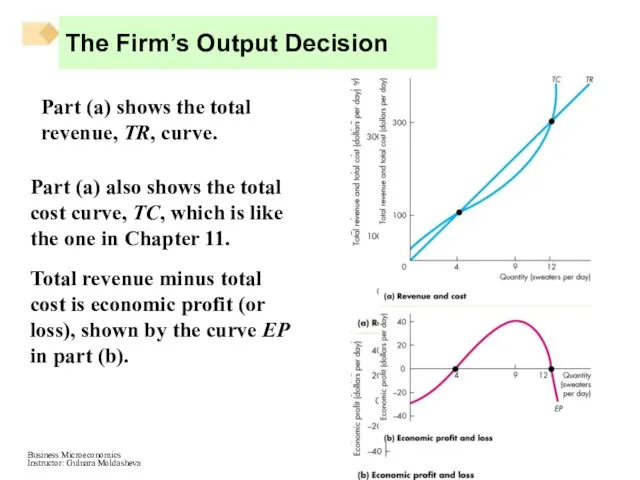

- 17. Part (a) shows the total revenue, TR, curve. Part (a) also shows the total cost curve,

- 19. At low output levels, the firm incurs an economic loss—it can’t cover its fixed costs. At

- 20. At high output levels, the firm again incurs an economic loss—now the firm faces steeply rising

- 21. Marginal Analysis and Supply Decision The firm can use marginal analysis to determine the profit-maximizing output.

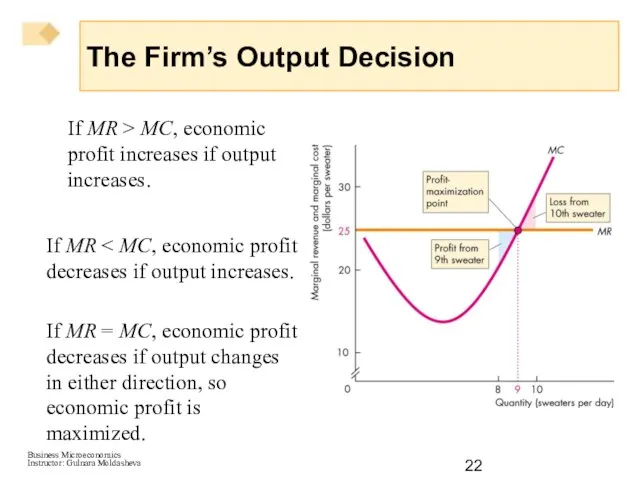

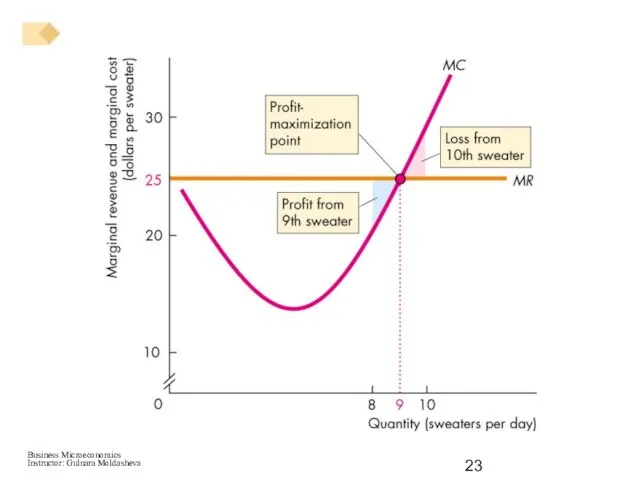

- 22. If MR > MC, economic profit increases if output increases. If MR If MR = MC,

- 24. Temporary Shutdown Decision If the firm makes an economic loss it must decide to exit the

- 25. Loss Comparison The firm’s loss equals total fixed cost (TFC) plus total variable cost (TVC) minus

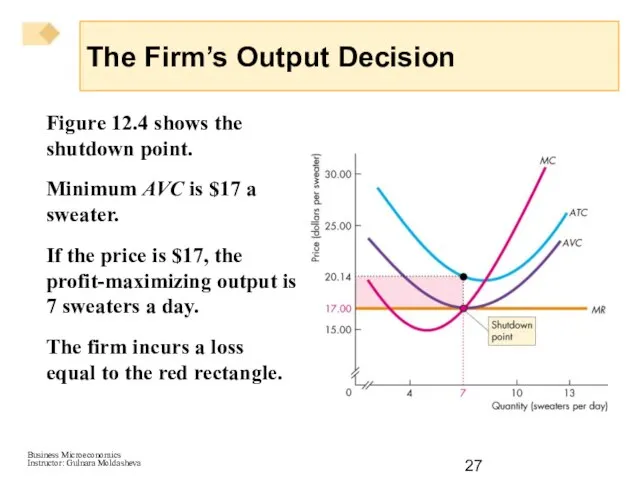

- 26. A firm’s shutdown point is the price and quantity at which it is indifferent between producing

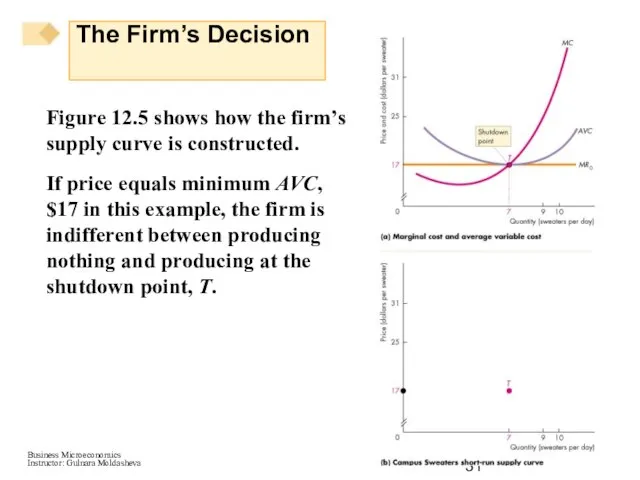

- 27. Figure 12.4 shows the shutdown point. Minimum AVC is $17 a sweater. If the price is

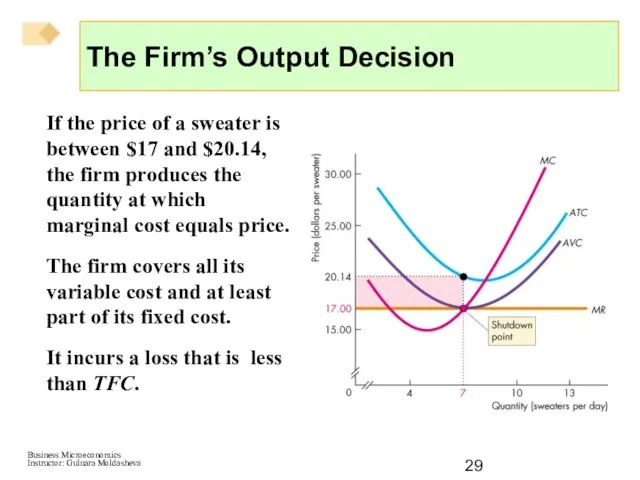

- 29. If the price of a sweater is between $17 and $20.14, the firm produces the quantity

- 30. The Firm’s Supply Curve A perfectly competitive firm’s supply curve shows how the firm’s profit-maximizing output

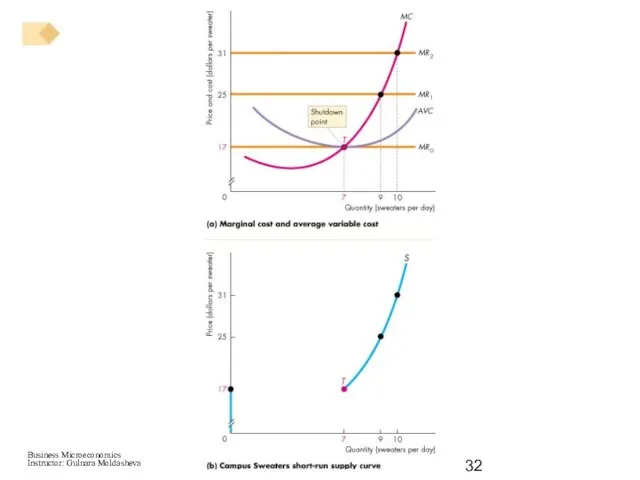

- 31. Figure 12.5 shows how the firm’s supply curve is constructed. If price equals minimum AVC, $17

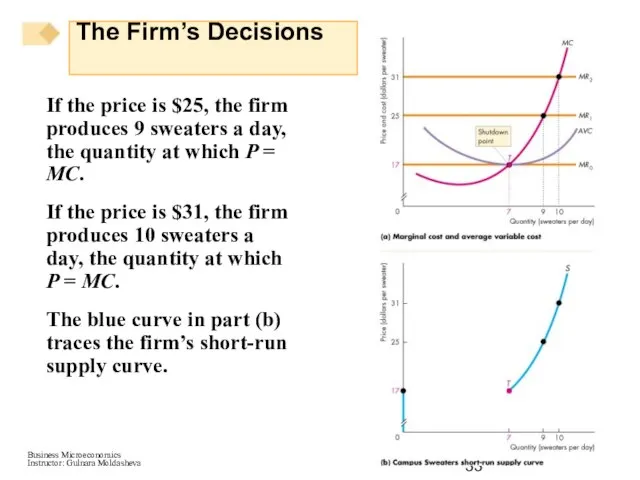

- 33. If the price is $25, the firm produces 9 sweaters a day, the quantity at which

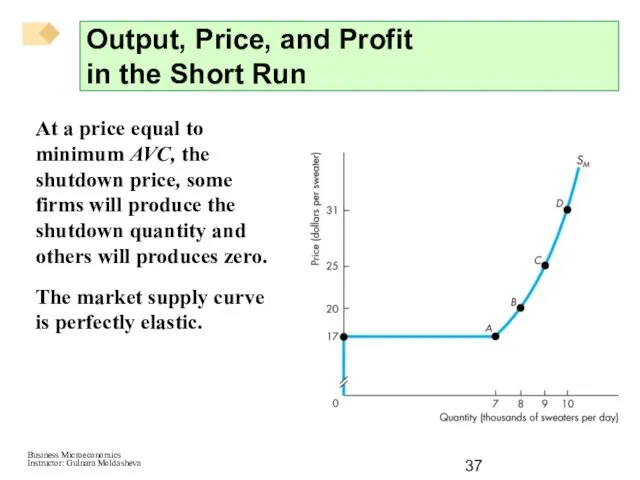

- 34. Market Supply in the Short Run The short-run market supply curve shows the quantity supplied by

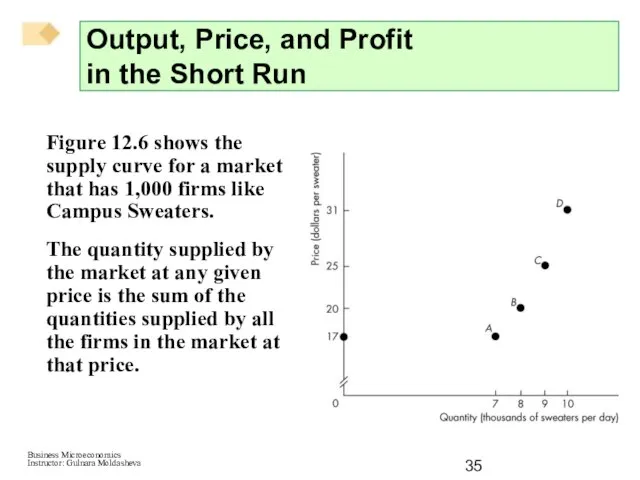

- 35. Figure 12.6 shows the supply curve for a market that has 1,000 firms like Campus Sweaters.

- 37. At a price equal to minimum AVC, the shutdown price, some firms will produce the shutdown

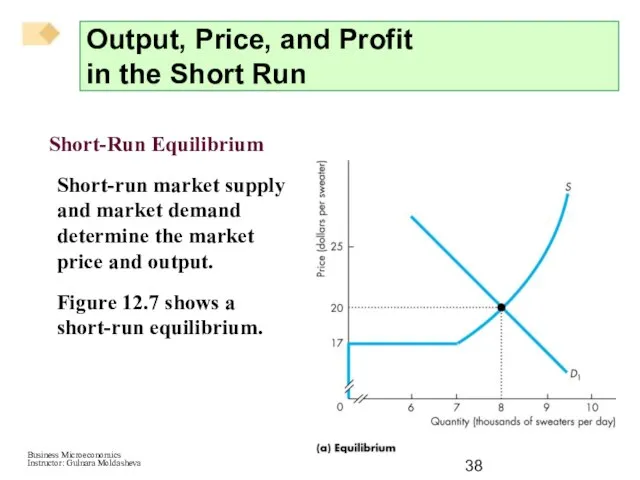

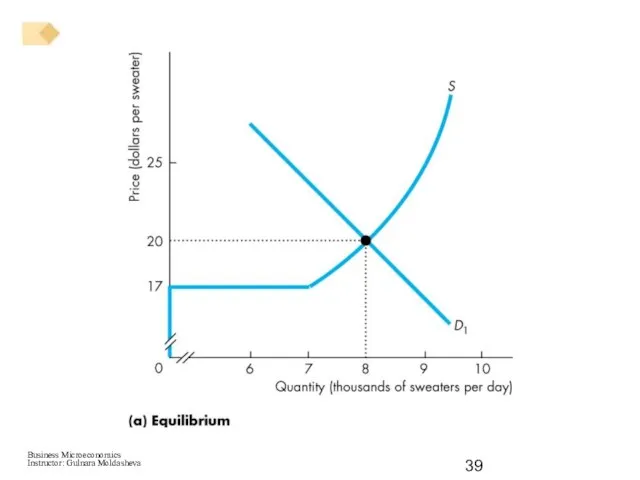

- 38. Short-Run Equilibrium Short-run market supply and market demand determine the market price and output. Figure 12.7

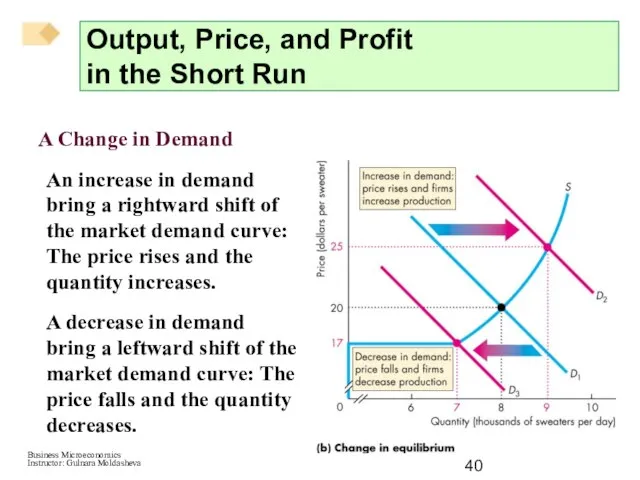

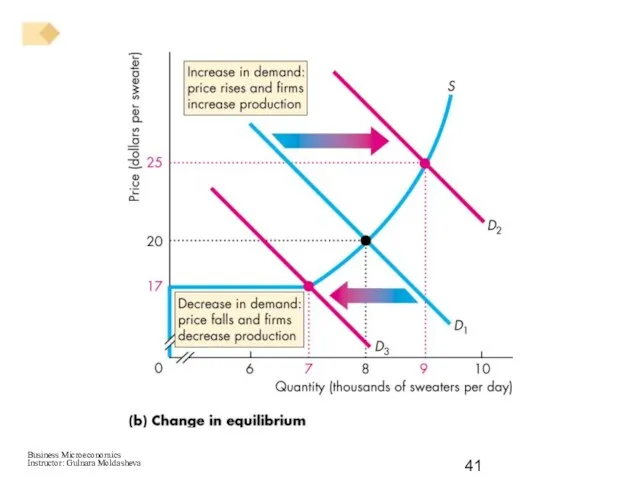

- 40. A Change in Demand An increase in demand bring a rightward shift of the market demand

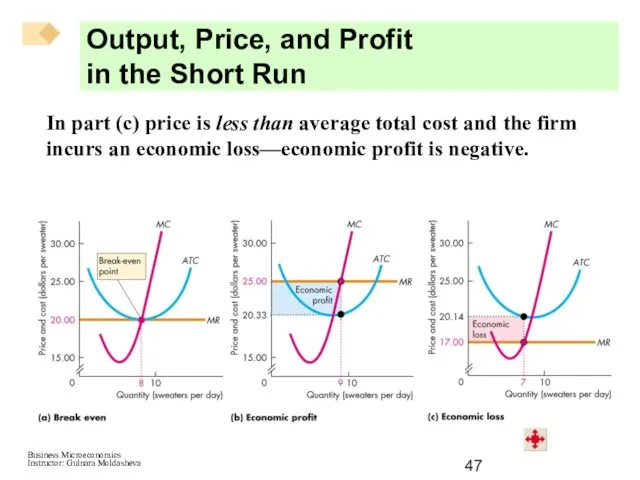

- 42. Profits and Losses in the Short Run Maximum profit is not always a positive economic profit.

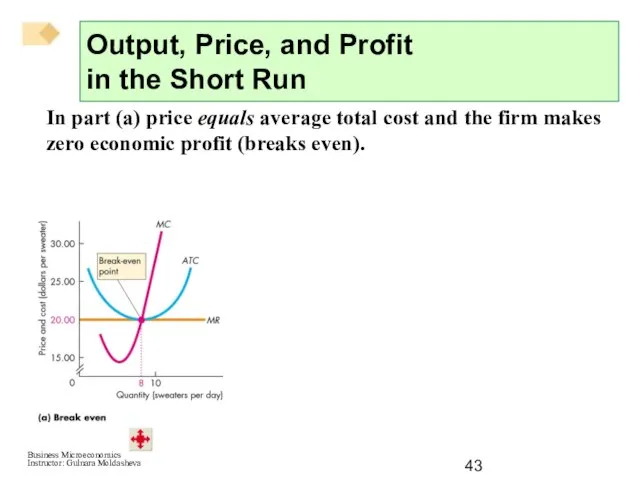

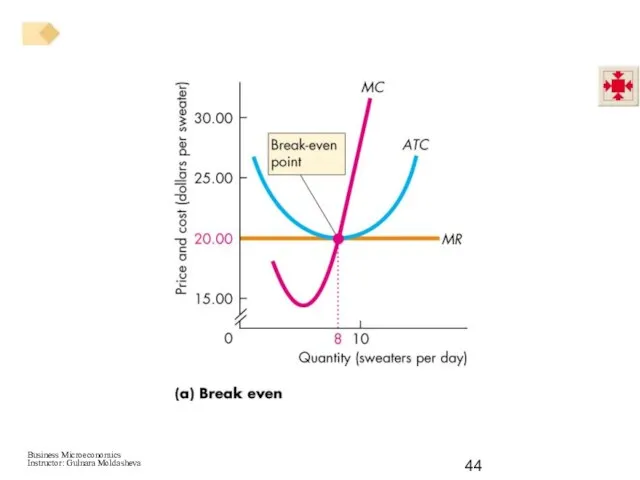

- 43. In part (a) price equals average total cost and the firm makes zero economic profit (breaks

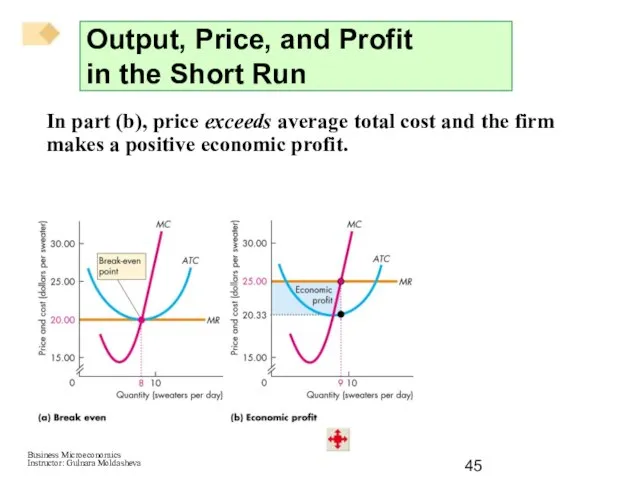

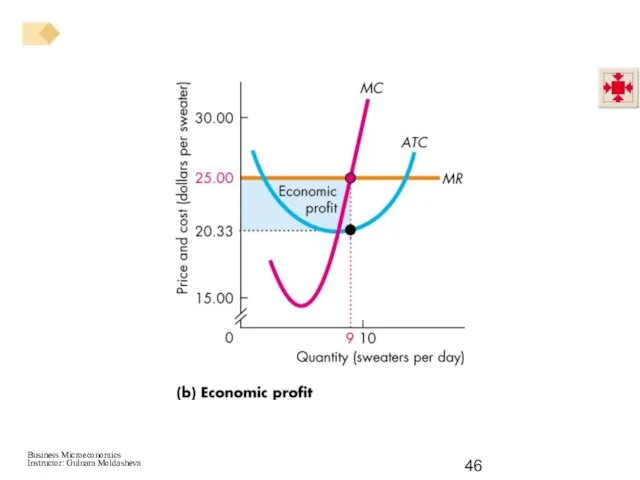

- 45. In part (b), price exceeds average total cost and the firm makes a positive economic profit.

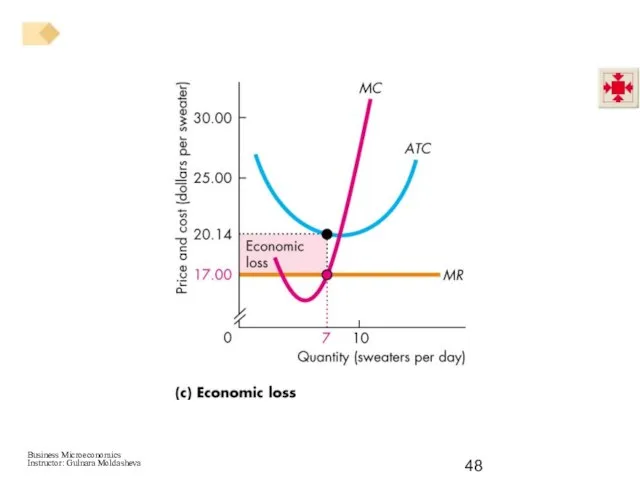

- 47. In part (c) price is less than average total cost and the firm incurs an economic

- 49. In short-run equilibrium, a firm may make an economic profit, break even, or incur an economic

- 50. Entry and Exit New firms enter an industry in which existing firms make an economic profit.

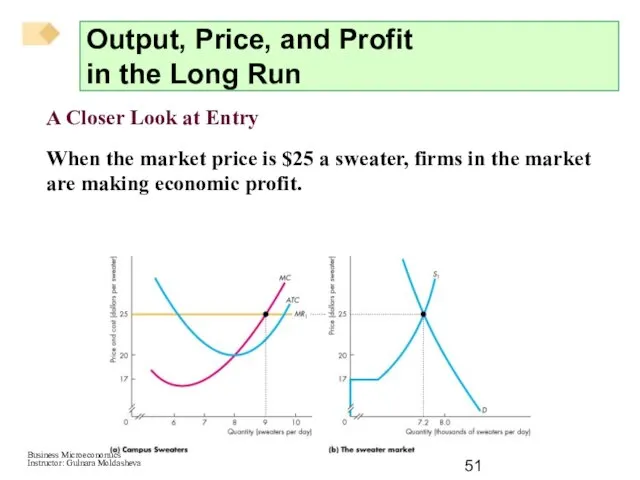

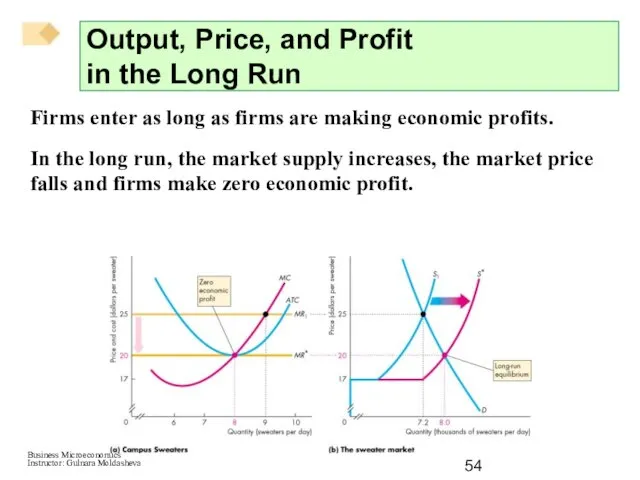

- 51. A Closer Look at Entry When the market price is $25 a sweater, firms in the

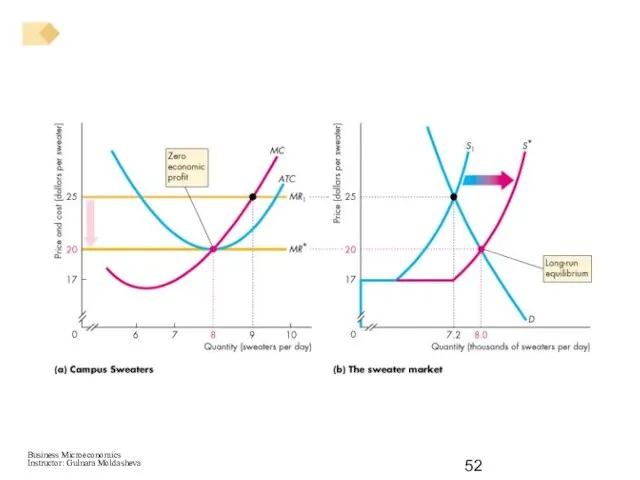

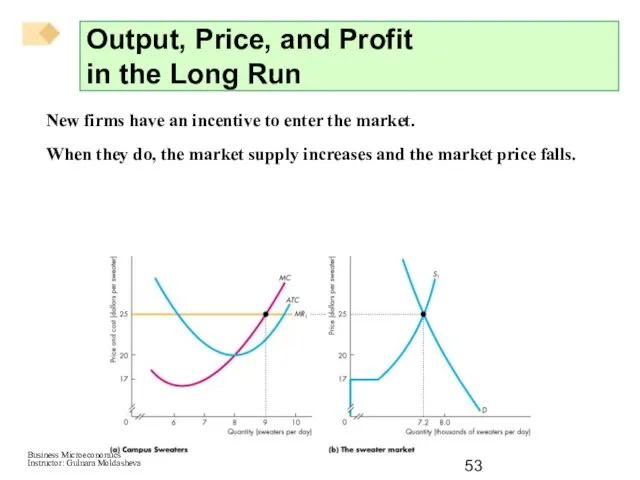

- 53. New firms have an incentive to enter the market. When they do, the market supply increases

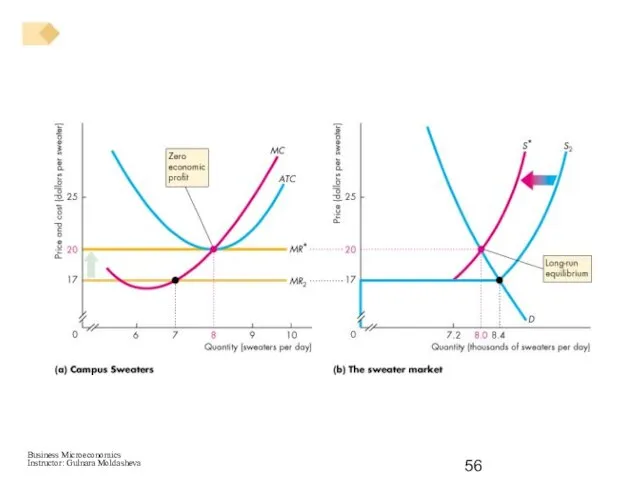

- 54. Firms enter as long as firms are making economic profits. In the long run, the market

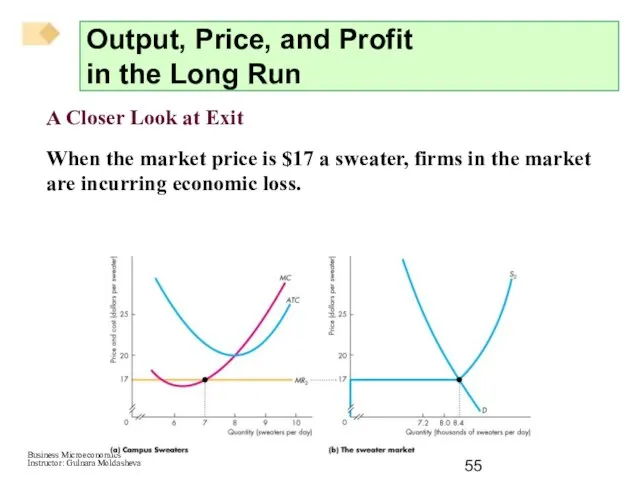

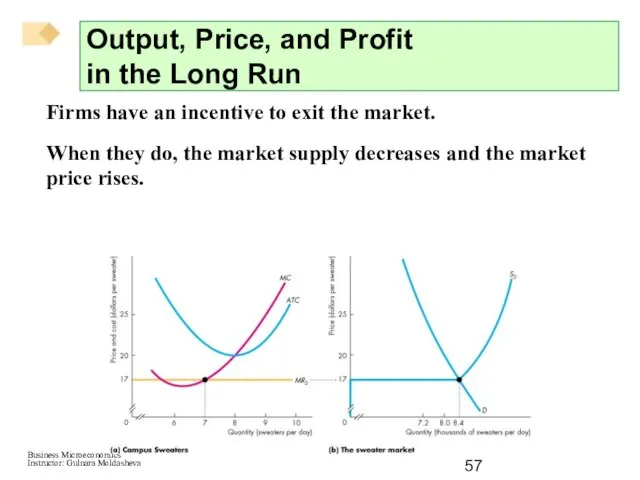

- 55. A Closer Look at Exit When the market price is $17 a sweater, firms in the

- 57. Firms have an incentive to exit the market. When they do, the market supply decreases and

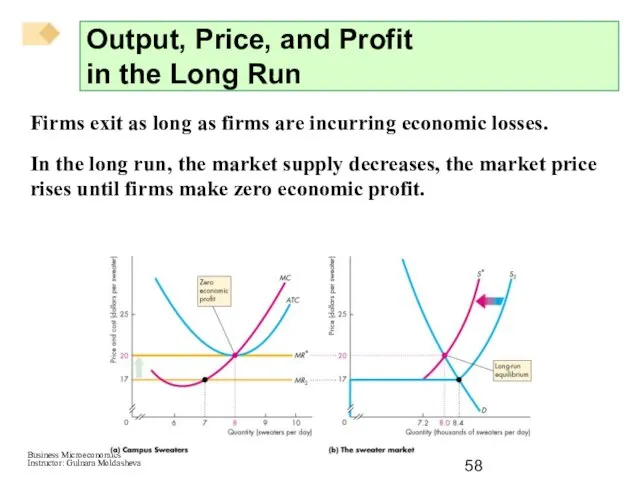

- 58. Firms exit as long as firms are incurring economic losses. In the long run, the market

- 59. Changing Tastes and Advancing Technology A Permanent Change in Demand A decrease in demand shifts the

- 60. A decrease in demand shifts the market demand curve leftward. The market price falls, and each

- 62. The market price is now below each firm’s minimum average total cost, so firms incur economic

- 63. Economic losses induce some firms to exit in the long run, which decreases the market supply

- 64. As the price rises, the quantity produced by all firms continues to decrease as more firms

- 65. A new long-run equilibrium occurs when the price has risen to equal minimum average total cost.

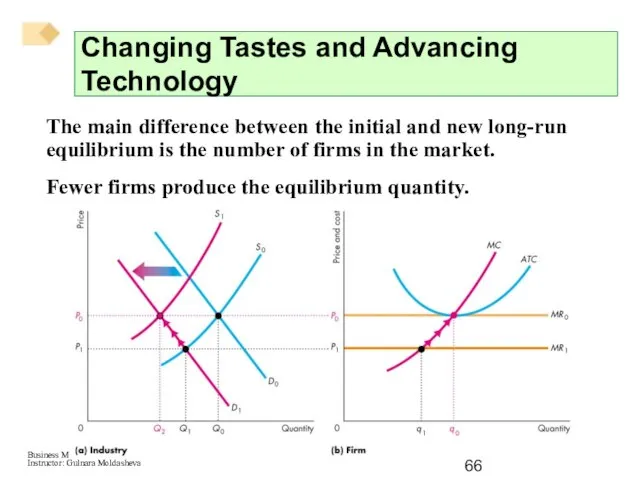

- 66. The main difference between the initial and new long-run equilibrium is the number of firms in

- 67. A permanent increase in demand has the opposite effects to those just described and shown in

- 68. With a falling price, each firm decreases its output as it moves along its marginal cost

- 69. External Economics and Diseconomies The change in the long-run equilibrium price following a permanent change in

- 70. In the absence of external economies or external diseconomies, a firm’s costs remain constant as the

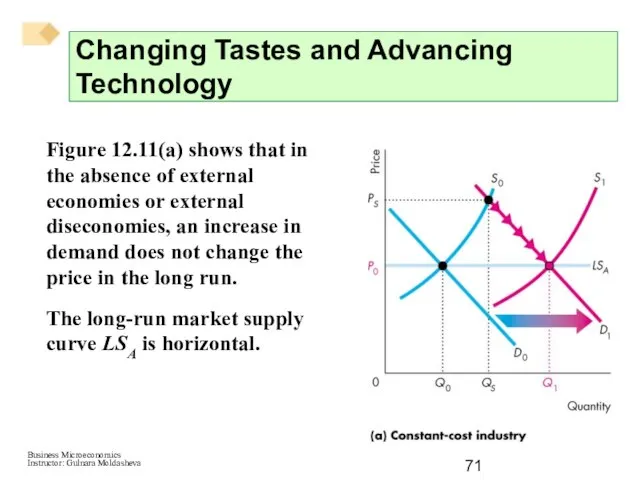

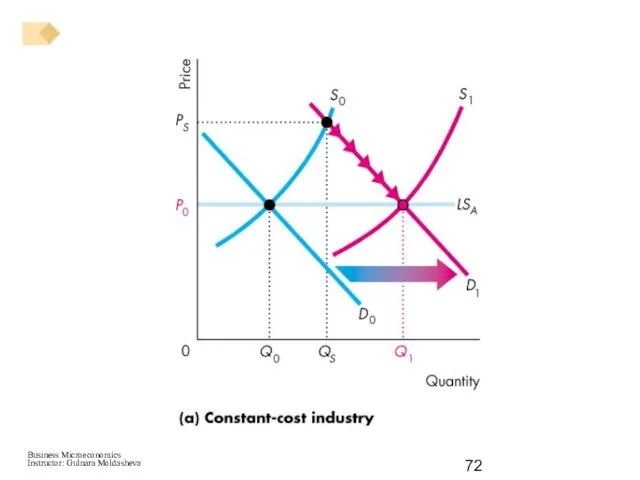

- 71. Figure 12.11(a) shows that in the absence of external economies or external diseconomies, an increase in

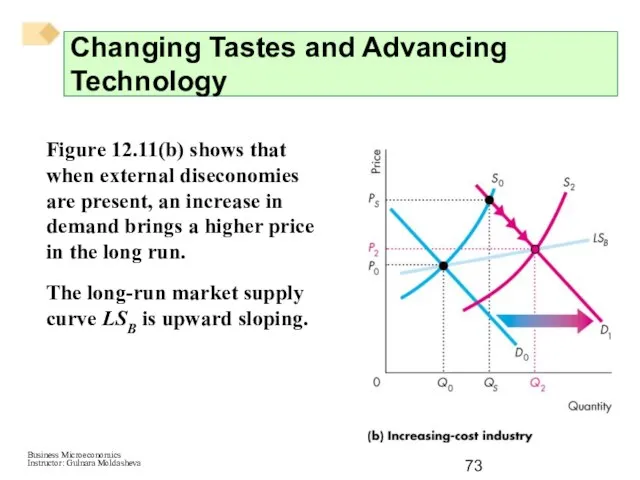

- 73. Figure 12.11(b) shows that when external diseconomies are present, an increase in demand brings a higher

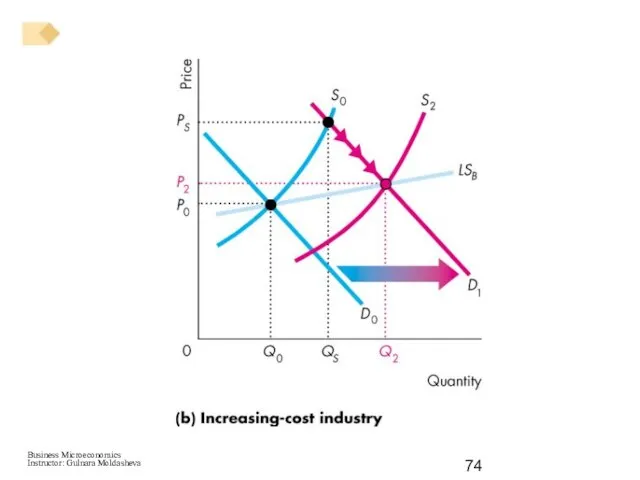

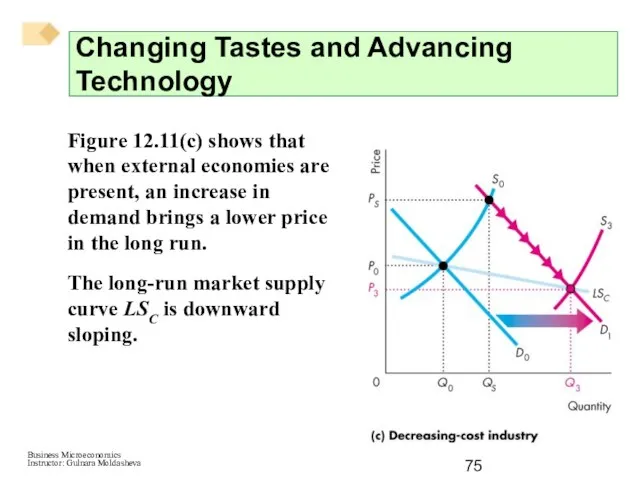

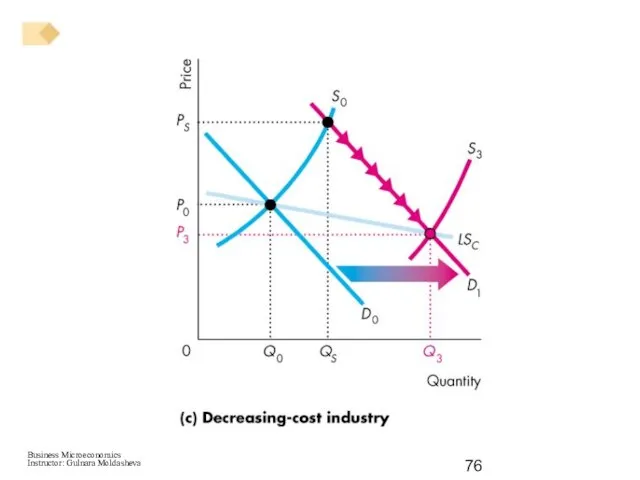

- 75. Figure 12.11(c) shows that when external economies are present, an increase in demand brings a lower

- 77. Technological Change New technologies are constantly discovered that lower costs. A new technology enables firms to

- 78. New-technology firms enter and old-technology firms either exit or adopt the new technology. Industry supply increases

- 79. Competition and Efficiency Efficient Use of Resources Resources are used efficiently when no one can be

- 80. Choices, Equilibrium, and Efficiency We can describe an efficient use of resources in terms of the

- 81. A competitive firm’s supply curve shows how the profit-maximizing quantity changes as the price of a

- 82. Equilibrium and Efficiency In competitive equilibrium, resources are used efficiently—the quantity demanded equals the quantity supplied,

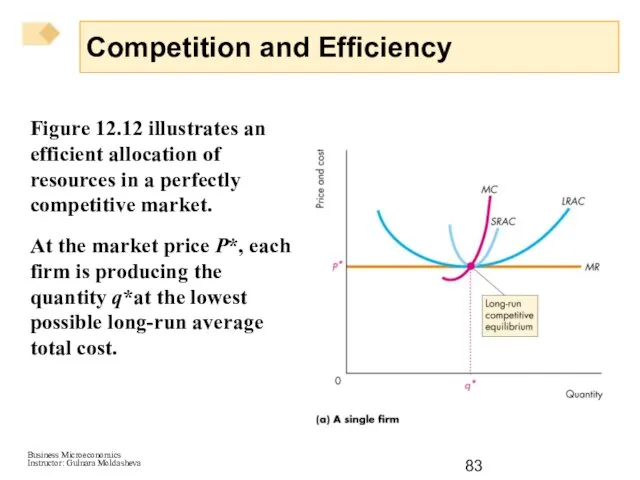

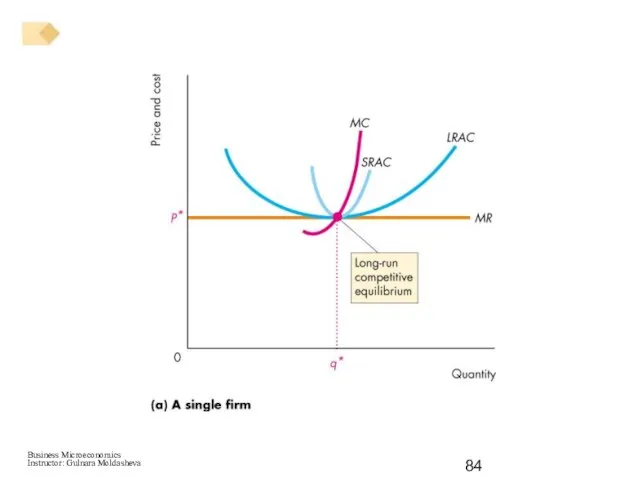

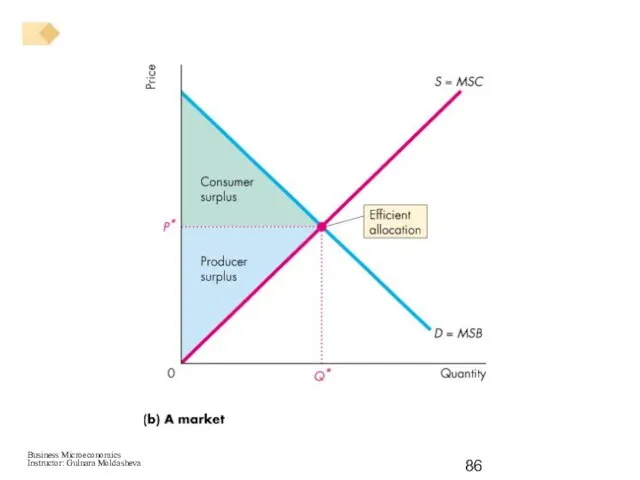

- 83. Figure 12.12 illustrates an efficient allocation of resources in a perfectly competitive market. At the market

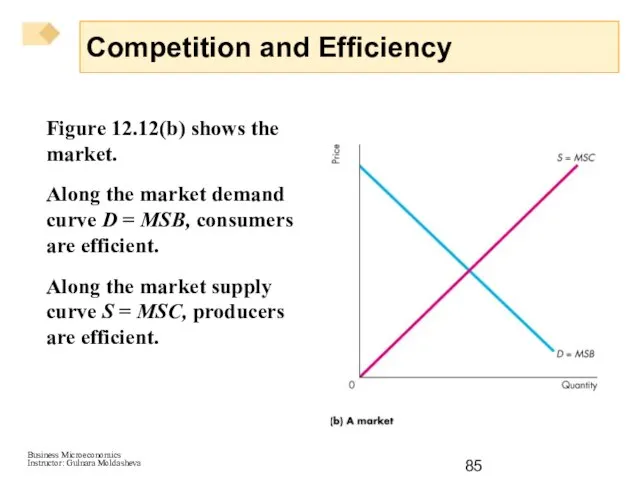

- 85. Figure 12.12(b) shows the market. Along the market demand curve D = MSB, consumers are efficient.

- 88. Скачать презентацию

Слайд 3Airlines and automobile producers are facing tough times: Prices are being slashed

Airlines and automobile producers are facing tough times: Prices are being slashed

Слайд 4What Is Perfect Competition?

Perfect competition is an industry in which

Many firms

What Is Perfect Competition?

Perfect competition is an industry in which

Many firms

Слайд 5How Perfect Competition Arises

Perfect competition arises:

When firm’s minimum efficient scale is small

How Perfect Competition Arises

Perfect competition arises:

When firm’s minimum efficient scale is small

Слайд 6Price Takers

In perfect competition, each firm is a price taker.

A price taker

Price Takers

In perfect competition, each firm is a price taker.

A price taker

Слайд 7Economic Profit and Revenue

The goal of each firm is to maximize economic

Economic Profit and Revenue

The goal of each firm is to maximize economic

Слайд 8Figure 12.1 illustrates a firm’s revenue concepts.

Part (a) shows that market demand

Figure 12.1 illustrates a firm’s revenue concepts.

Part (a) shows that market demand

Слайд 10Figure 12.1(b) shows the firm’s total revenue curve (TR)—the relationship between total

Figure 12.1(b) shows the firm’s total revenue curve (TR)—the relationship between total

Слайд 12Figure 12.1(c) shows the marginal revenue curve (MR).

The firm can sell any

Figure 12.1(c) shows the marginal revenue curve (MR).

The firm can sell any

Слайд 14The demand for a firm’s product is perfectly elastic because one firm’s

The demand for a firm’s product is perfectly elastic because one firm’s

Слайд 15A perfectly competitive firm’s goal is to make maximum economic profit, given

A perfectly competitive firm’s goal is to make maximum economic profit, given

Слайд 16Profit-Maximizing Output

A perfectly competitive firm chooses the output that maximizes its economic

Profit-Maximizing Output

A perfectly competitive firm chooses the output that maximizes its economic

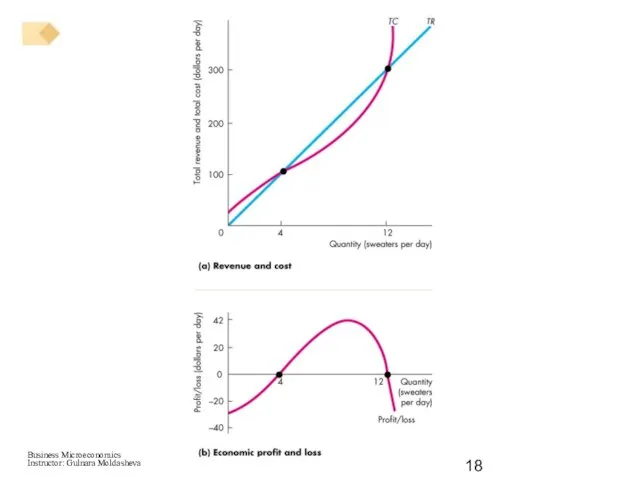

Слайд 17Part (a) shows the total revenue, TR, curve.

Part (a) also shows the

Part (a) shows the total revenue, TR, curve.

Part (a) also shows the

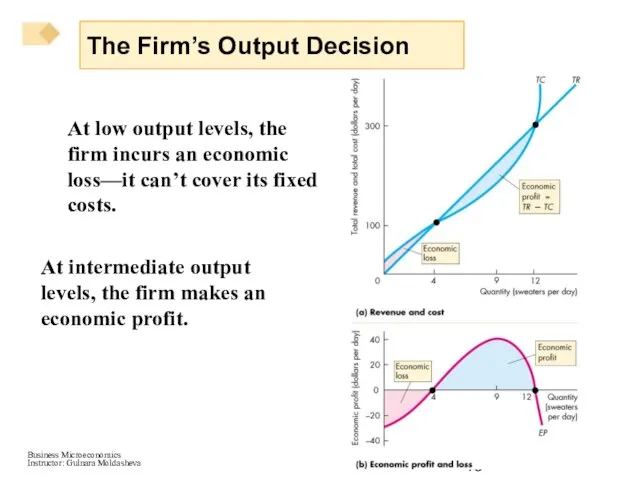

Слайд 19At low output levels, the firm incurs an economic loss—it can’t cover

At low output levels, the firm incurs an economic loss—it can’t cover

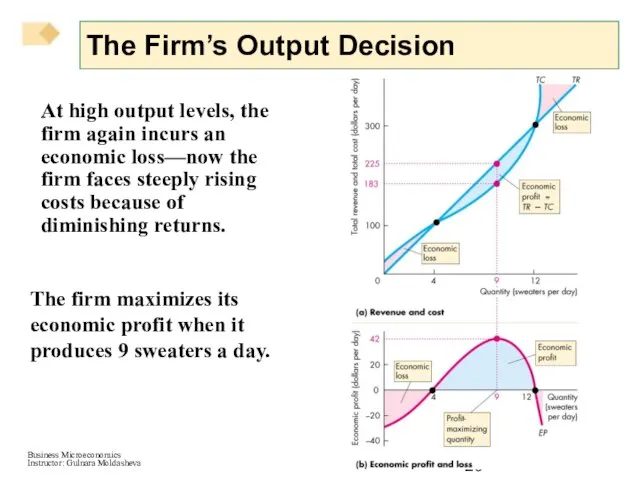

Слайд 20At high output levels, the firm again incurs an economic loss—now the

At high output levels, the firm again incurs an economic loss—now the

Слайд 21Marginal Analysis and Supply Decision

The firm can use marginal analysis to determine

Marginal Analysis and Supply Decision

The firm can use marginal analysis to determine

Слайд 22If MR > MC, economic profit increases if output increases.

If MR <

If MR > MC, economic profit increases if output increases.

If MR <

Слайд 24Temporary Shutdown Decision

If the firm makes an economic loss it must decide

Temporary Shutdown Decision

If the firm makes an economic loss it must decide

Слайд 25Loss Comparison

The firm’s loss equals total fixed cost (TFC) plus total variable

Loss Comparison

The firm’s loss equals total fixed cost (TFC) plus total variable

Слайд 26A firm’s shutdown point is the price and quantity at which it

A firm’s shutdown point is the price and quantity at which it

Слайд 27Figure 12.4 shows the shutdown point.

Minimum AVC is $17 a sweater.

If the

Figure 12.4 shows the shutdown point.

Minimum AVC is $17 a sweater.

If the

Слайд 29If the price of a sweater is between $17 and $20.14, the

If the price of a sweater is between $17 and $20.14, the

Слайд 30The Firm’s Supply Curve

A perfectly competitive firm’s supply curve shows how the

The Firm’s Supply Curve

A perfectly competitive firm’s supply curve shows how the

Слайд 31Figure 12.5 shows how the firm’s supply curve is constructed.

If price equals

Figure 12.5 shows how the firm’s supply curve is constructed.

If price equals

Слайд 33If the price is $25, the firm produces 9 sweaters a day,

If the price is $25, the firm produces 9 sweaters a day,

Слайд 34Market Supply in the Short Run

The short-run market supply curve shows the

Market Supply in the Short Run

The short-run market supply curve shows the

Слайд 35Figure 12.6 shows the supply curve for a market that has 1,000

Figure 12.6 shows the supply curve for a market that has 1,000

Слайд 37At a price equal to minimum AVC, the shutdown price, some firms

At a price equal to minimum AVC, the shutdown price, some firms

Слайд 38Short-Run Equilibrium

Short-run market supply and market demand determine the market price and

Short-Run Equilibrium

Short-run market supply and market demand determine the market price and

Слайд 40A Change in Demand

An increase in demand bring a rightward shift

A Change in Demand

An increase in demand bring a rightward shift

Слайд 42Profits and Losses in the Short Run

Maximum profit is not always a

Profits and Losses in the Short Run

Maximum profit is not always a

Слайд 43In part (a) price equals average total cost and the firm makes

In part (a) price equals average total cost and the firm makes

Слайд 45In part (b), price exceeds average total cost and the firm makes

In part (b), price exceeds average total cost and the firm makes

Слайд 47In part (c) price is less than average total cost and the

In part (c) price is less than average total cost and the

Слайд 49In short-run equilibrium, a firm may make an economic profit, break even,

In short-run equilibrium, a firm may make an economic profit, break even,

Слайд 50Entry and Exit

New firms enter an industry in which existing firms make

Entry and Exit

New firms enter an industry in which existing firms make

Слайд 51A Closer Look at Entry

When the market price is $25 a sweater,

A Closer Look at Entry

When the market price is $25 a sweater,

Слайд 53New firms have an incentive to enter the market.

When they do, the

New firms have an incentive to enter the market.

When they do, the

Слайд 54Firms enter as long as firms are making economic profits.

In the

Firms enter as long as firms are making economic profits.

In the

Слайд 55A Closer Look at Exit

When the market price is $17 a sweater,

A Closer Look at Exit

When the market price is $17 a sweater,

Слайд 57Firms have an incentive to exit the market.

When they do, the market

Firms have an incentive to exit the market.

When they do, the market

Слайд 58Firms exit as long as firms are incurring economic losses.

In the

Firms exit as long as firms are incurring economic losses.

In the

Слайд 59Changing Tastes and Advancing Technology

A Permanent Change in Demand

A decrease in demand

Changing Tastes and Advancing Technology

A Permanent Change in Demand

A decrease in demand

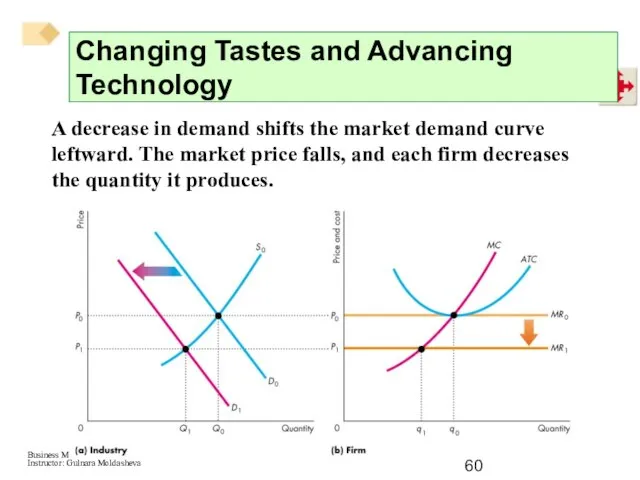

Слайд 60A decrease in demand shifts the market demand curve leftward. The market

A decrease in demand shifts the market demand curve leftward. The market

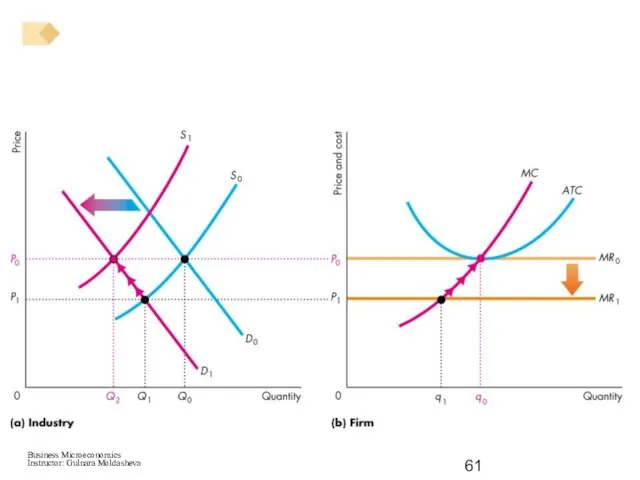

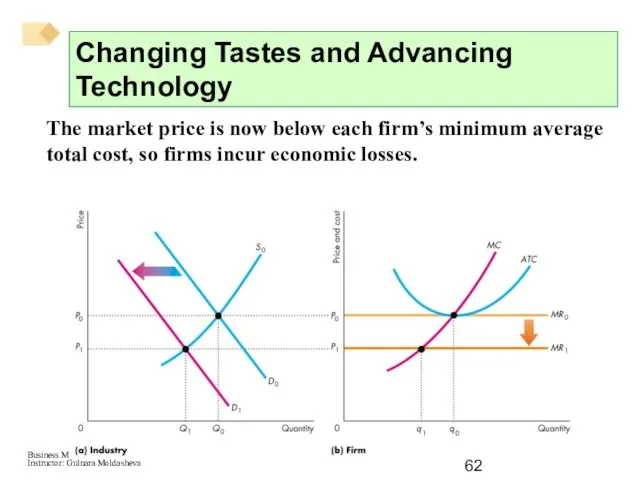

Слайд 62The market price is now below each firm’s minimum average total cost,

The market price is now below each firm’s minimum average total cost,

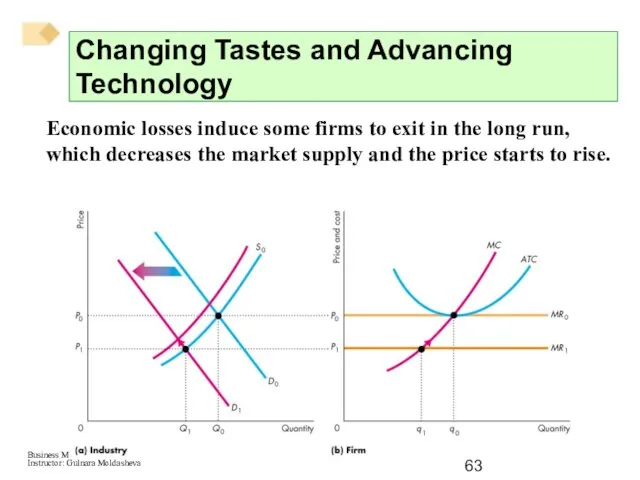

Слайд 63Economic losses induce some firms to exit in the long run, which

Economic losses induce some firms to exit in the long run, which

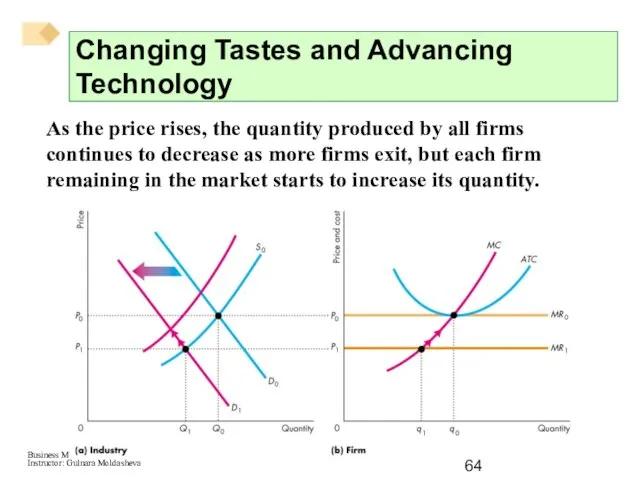

Слайд 64As the price rises, the quantity produced by all firms continues to

As the price rises, the quantity produced by all firms continues to

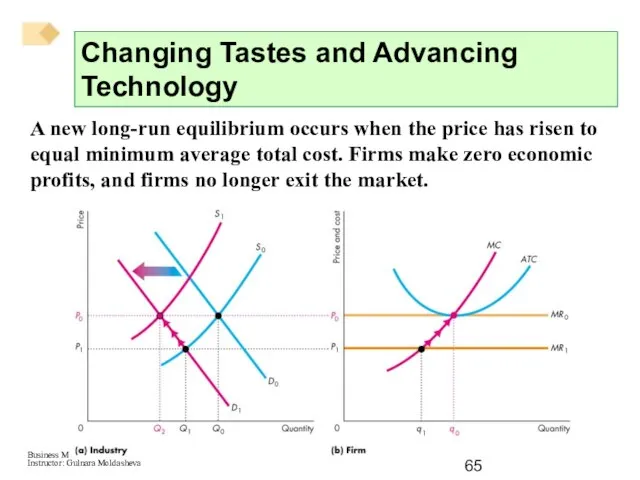

Слайд 65A new long-run equilibrium occurs when the price has risen to equal

A new long-run equilibrium occurs when the price has risen to equal

Слайд 66The main difference between the initial and new long-run equilibrium is the

The main difference between the initial and new long-run equilibrium is the

Слайд 67A permanent increase in demand has the opposite effects to those just

A permanent increase in demand has the opposite effects to those just

Слайд 68With a falling price, each firm decreases its output as it moves

With a falling price, each firm decreases its output as it moves

Слайд 69External Economics and Diseconomies

The change in the long-run equilibrium price following a

External Economics and Diseconomies

The change in the long-run equilibrium price following a

Слайд 70In the absence of external economies or external diseconomies, a firm’s costs

In the absence of external economies or external diseconomies, a firm’s costs

Слайд 71Figure 12.11(a) shows that in the absence of external economies or external

Figure 12.11(a) shows that in the absence of external economies or external

Слайд 73Figure 12.11(b) shows that when external diseconomies are present, an increase in

Figure 12.11(b) shows that when external diseconomies are present, an increase in

Слайд 75Figure 12.11(c) shows that when external economies are present, an increase in

Figure 12.11(c) shows that when external economies are present, an increase in

Слайд 77Technological Change

New technologies are constantly discovered that lower costs.

A new technology enables

Technological Change

New technologies are constantly discovered that lower costs.

A new technology enables

Слайд 78New-technology firms enter and old-technology firms either exit or adopt the new

New-technology firms enter and old-technology firms either exit or adopt the new

Слайд 79Competition and Efficiency

Efficient Use of Resources

Resources are used efficiently when no one

Competition and Efficiency

Efficient Use of Resources

Resources are used efficiently when no one

Слайд 80Choices, Equilibrium, and Efficiency

We can describe an efficient use of resources in

Choices, Equilibrium, and Efficiency

We can describe an efficient use of resources in

Слайд 81A competitive firm’s supply curve shows how the profit-maximizing quantity changes as

A competitive firm’s supply curve shows how the profit-maximizing quantity changes as

Слайд 82Equilibrium and Efficiency

In competitive equilibrium, resources are used efficiently—the quantity demanded equals

Equilibrium and Efficiency

In competitive equilibrium, resources are used efficiently—the quantity demanded equals

Слайд 83Figure 12.12 illustrates an efficient allocation of resources in a perfectly competitive

Figure 12.12 illustrates an efficient allocation of resources in a perfectly competitive

Слайд 85Figure 12.12(b) shows the market.

Along the market demand curve D = MSB,

Figure 12.12(b) shows the market.

Along the market demand curve D = MSB,

ОБЩ 5.1

ОБЩ 5.1 Презентация на тему Философы Японии. Нисида Китаро

Презентация на тему Философы Японии. Нисида Китаро  База отдыха Борвиха

База отдыха Борвиха Лекция 2. «Программно-методическое обеспечение обучения в воскресной школе»

Лекция 2. «Программно-методическое обеспечение обучения в воскресной школе» Презентация на тему”День космонавтики»

Презентация на тему”День космонавтики» Что такое красота?

Что такое красота? Национальные традиции, обычаи, культура народов нашего края

Национальные традиции, обычаи, культура народов нашего края Что мы знаем о молоке?

Что мы знаем о молоке? Кибербуллинг

Кибербуллинг Политические институты. Международные институты. Лекция 7

Политические институты. Международные институты. Лекция 7 Квітка Цісик (1953-1998рр) Нью-Йорк, США

Квітка Цісик (1953-1998рр) Нью-Йорк, США Профессиональное командное соревнование молодежных команд

Профессиональное командное соревнование молодежных команд Софт скиллз… Это для меня?

Софт скиллз… Это для меня? Мышление. Тест Какой у вас тип мышления

Мышление. Тест Какой у вас тип мышления Презентация на тему Атмосферные осадки

Презентация на тему Атмосферные осадки  Стихийные бедствия

Стихийные бедствия Яна

Яна Симметрия и правила её построения в рисунке

Симметрия и правила её построения в рисунке ООО ЭКОЭРЭ производство инфракрасных обогревателей ERES

ООО ЭКОЭРЭ производство инфракрасных обогревателей ERES Теория управления. Лекция 3. Системный подход в управлении

Теория управления. Лекция 3. Системный подход в управлении Контакт-центр

Контакт-центр Будущий ученик - "Новой школы"

Будущий ученик - "Новой школы" Презентация Центра систем альтернативной энергетики Партнерский проект ООО «Системы Альтернативной Энергетики» и AXEPTOR AG

Презентация Центра систем альтернативной энергетики Партнерский проект ООО «Системы Альтернативной Энергетики» и AXEPTOR AG Measuring perfomance

Measuring perfomance Греческий ордер

Греческий ордер Строение человека

Строение человека Асимметрия головного мозга

Асимметрия головного мозга Konstytucja RP. Art. 66. „Każdy ma prawo do bezpiecznych i higienicznych warunków pracy”

Konstytucja RP. Art. 66. „Każdy ma prawo do bezpiecznych i higienicznych warunków pracy”