- Stakeholder management

Содержание

- 2. Objectives Define stake and stakeholder Differentiate between production, managerial, and stakeholder views of the firm Discuss

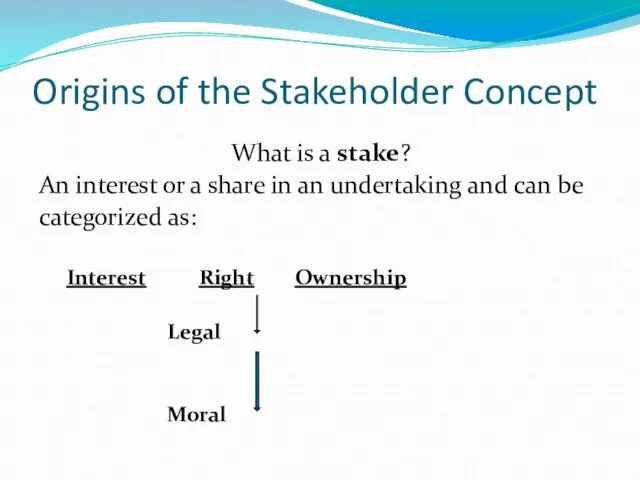

- 3. Origins of the Stakeholder Concept Who Are Business’s Stakeholders? Strategic, Multifiduciary, and Synthesis Views Three Values

- 4. Stakeholders Individuals and groups with a multitude of interests, expectations, and demands as to what business

- 5. Origins of the Stakeholder Concept What is a stake? An interest or a share in an

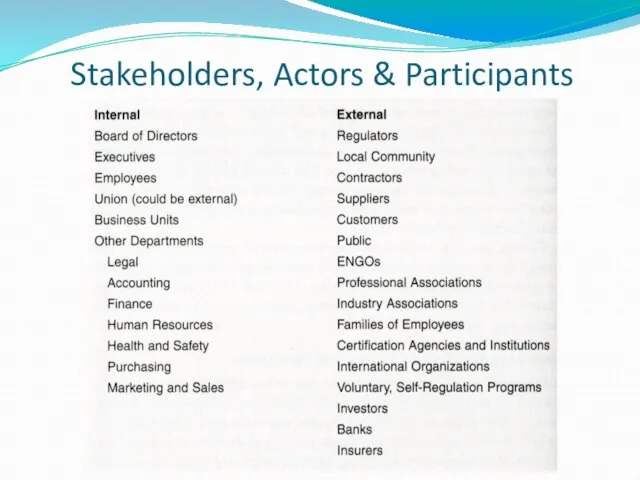

- 6. Stakeholders, Actors & Participants

- 7. Identifying Stakeholders, Actors and Participants These are people directly or indirectly involved in environmental management People

- 8. Wide range of stakeholders Internal or external Directly or indirectly involved Relationship can be formal (regulated,

- 9. Who Are Business Stakeholders?

- 10. Who Are Business Stakeholders? Evolution and Development of the Stakeholder Concept Views of the Firm Production

- 11. Who Are Business Stakeholders? Production and Managerial Views

- 12. Who Are Business Stakeholders?

- 13. Who Are Business Stakeholders? Primary and Secondary Stakeholders Primary stakeholders are those stakeholders that have a

- 14. Who Are Business Stakeholders? Core, Strategic, and Environmental Stakeholders Core stakeholders are essential to the survival

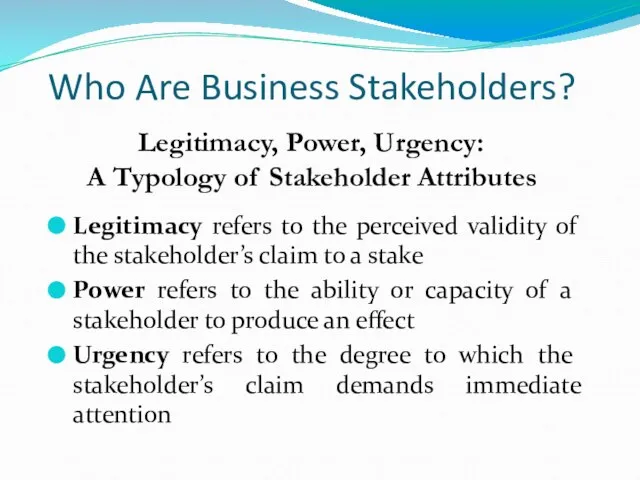

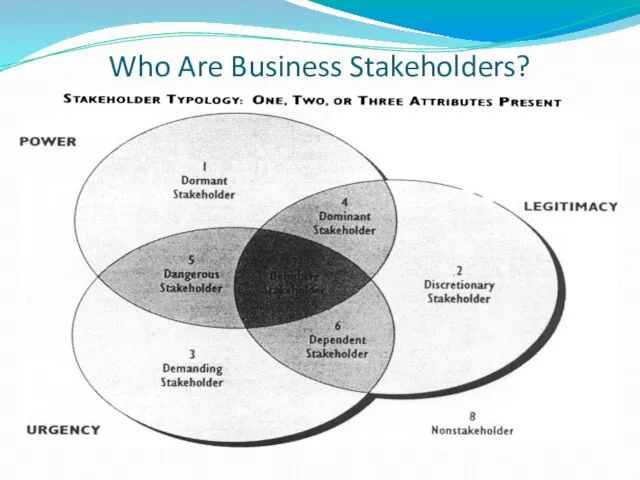

- 15. Who Are Business Stakeholders? Legitimacy refers to the perceived validity of the stakeholder’s claim to a

- 16. Who Are Business Stakeholders?

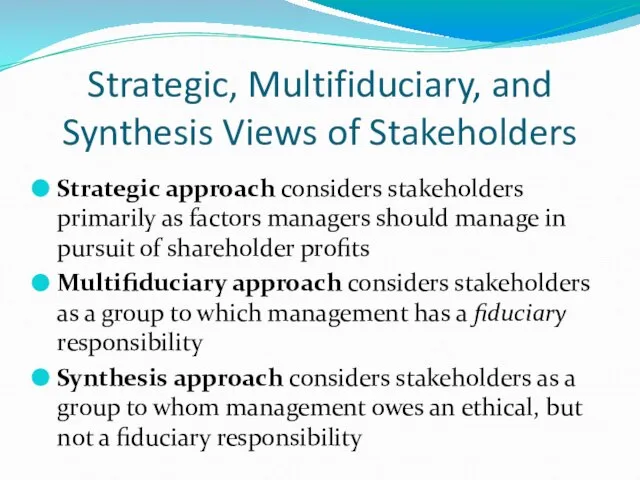

- 17. Strategic, Multifiduciary, and Synthesis Views of Stakeholders Strategic approach considers stakeholders primarily as factors managers should

- 18. Three Values of the Stakeholder Model Descriptive Instrumental Normative

- 19. Key Questions In Stakeholder Management Who are our stakeholders? What are our stakeholders’ stakes? What opportunities

- 20. Key Questions In Stakeholder Management Who are our stakeholders Management must identify generic stakeholder groups and

- 21. Key Questions In Stakeholder Management

- 22. Key Questions In Stakeholder Management What are our stakeholders’ stakes? Determine the nature/legitimacy of a group’s

- 23. Key Questions In Stakeholder Management What opportunities and challenges do stakeholders present? Opportunities are to build

- 24. Key Questions In Stakeholder Management

- 25. Key Questions In Stakeholder Management What economic, legal, ethical, and philanthropic responsibilities does our firm have

- 26. Key Questions In Stakeholder Management Stakeholder/Responsibility Matrix

- 27. Key Questions In Stakeholder Management What strategies or actions should our firm take to best manage

- 28. Key Questions In Stakeholder Management Types of Stakeholders

- 29. Effective Stakeholder Management Careful assessment of the five core questions: Who are our stakeholders? What are

- 30. Effective Stakeholder Management Stakeholder Management Capability Rational level Process level Transaction level

- 31. Effective Stakeholder Management Stakeholder Corporation Stakeholder inclusiveness Stakeholder symbiosis

- 32. Stakeholder Power: Four Gates of Engagement Awareness Knowledge Admiration Action

- 33. Principles of Stakeholder Management Acknowledge Monitor Listen Communicate Adopt Recognize Work Avoid Acknowledge conflict

- 34. Principles of Stakeholder Management

- 35. Core Stakeholders Environmental Stakeholders Legitimacy Managerial view of the firm Power Principles of stakeholder management Process

- 36. Environmental reporting Refers to the issuance of any report containing information of an environmental nature, from

- 37. History of Corporate Environmental Reporting (CER) First corporate environmental reports were released in 1990s issuing reports

- 38. Evolution of environmental reporting to meet stakeholders information needs. Source: adapted from the UN Environmental Programme,

- 39. Processes of preparing an environmental report GRI=Global reporting initiative

- 40. Reliability of the data At any time in a corporation, different performance measurement processes will be

- 41. Reporting and verification, measurement processes & reliable data

- 42. Frame of reference for reporting based on reliability of data and relevance to stakeholders Can be

- 43. Audiences for Environmental Reports Targeting their audiences, report makers may address the noisiest stakeholders Other consider

- 44. Driving forces for external assurance 1. The nature of information being reviewed: is the information mainly

- 45. Types of assurance Review & endorsement of company policies & performances – what does the external

- 46. Interpretation of performance data – what does all environmental data mean? How does this company compare

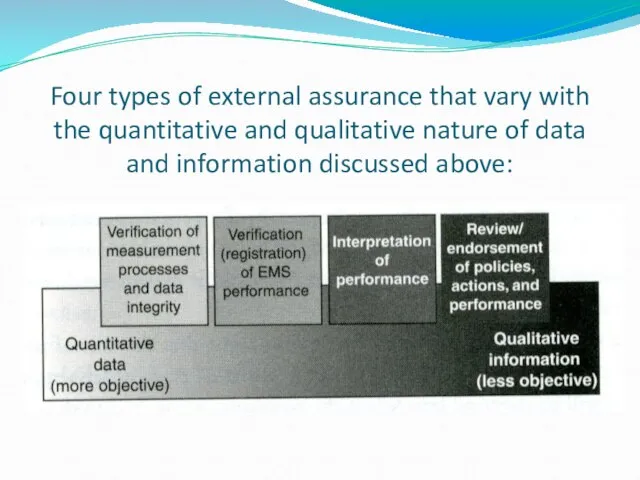

- 47. Four types of external assurance that vary with the quantitative and qualitative nature of data and

- 49. Скачать презентацию

Слайд 2Objectives

Define stake and stakeholder

Differentiate between production, managerial, and stakeholder views of the

Objectives

Define stake and stakeholder

Differentiate between production, managerial, and stakeholder views of the

Слайд 3Origins of the Stakeholder Concept

Who Are Business’s Stakeholders?

Strategic, Multifiduciary, and Synthesis Views

Three

Origins of the Stakeholder Concept

Who Are Business’s Stakeholders?

Strategic, Multifiduciary, and Synthesis Views

Three

Слайд 4Stakeholders

Individuals and groups with a multitude of interests, expectations, and demands as

Stakeholders

Individuals and groups with a multitude of interests, expectations, and demands as

Слайд 5Origins of the Stakeholder Concept

What is a stake?

An interest or a share

Origins of the Stakeholder Concept

What is a stake?

An interest or a share

Слайд 6Stakeholders, Actors & Participants

Stakeholders, Actors & Participants

Слайд 7Identifying Stakeholders, Actors and Participants

These are people directly or indirectly involved in

Identifying Stakeholders, Actors and Participants

These are people directly or indirectly involved in

Слайд 8Wide range of stakeholders

Internal or external

Directly or indirectly involved

Relationship can be formal

Wide range of stakeholders

Internal or external

Directly or indirectly involved

Relationship can be formal

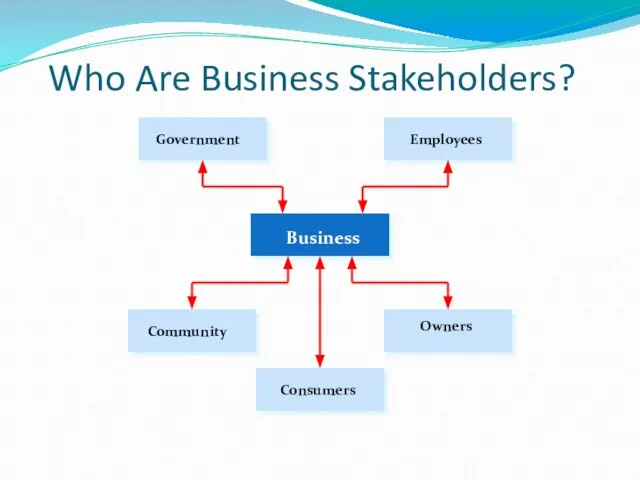

Слайд 9Who Are Business Stakeholders?

Who Are Business Stakeholders?

Слайд 10Who Are Business Stakeholders?

Evolution and Development of the

Stakeholder Concept

Views of the

Who Are Business Stakeholders?

Evolution and Development of the

Stakeholder Concept

Views of the

Слайд 11Who Are Business Stakeholders?

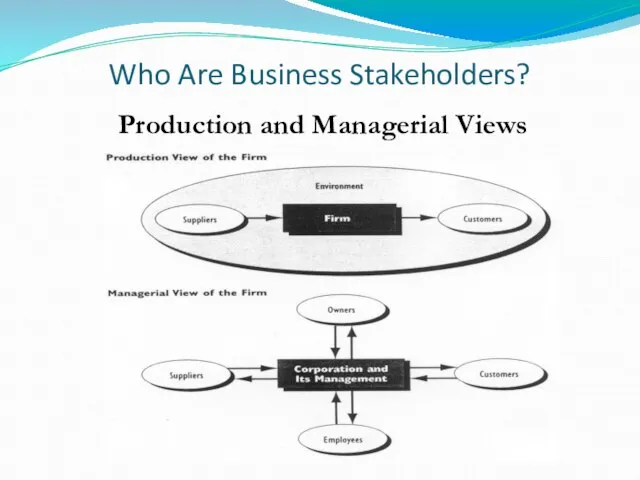

Production and Managerial Views

Who Are Business Stakeholders?

Production and Managerial Views

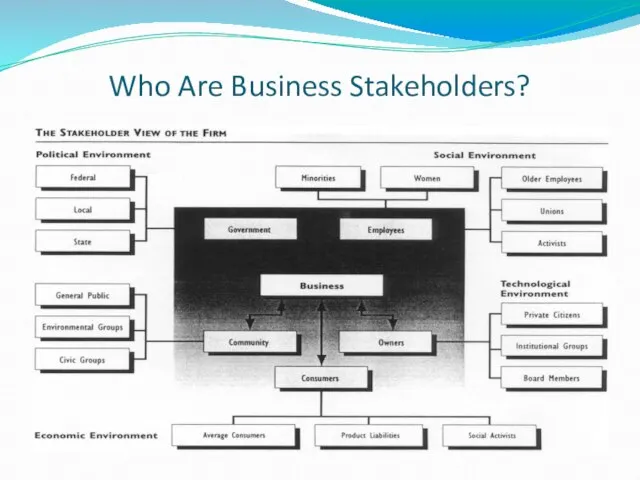

Слайд 12Who Are Business Stakeholders?

Who Are Business Stakeholders?

Слайд 13Who Are Business Stakeholders?

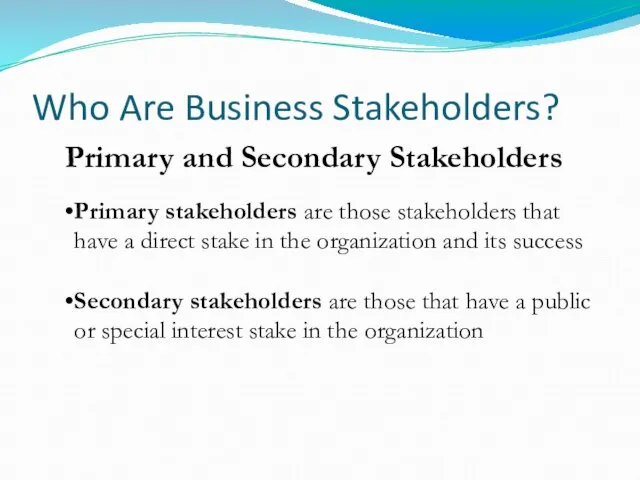

Primary and Secondary Stakeholders

Primary stakeholders are those stakeholders that

Who Are Business Stakeholders?

Primary and Secondary Stakeholders

Primary stakeholders are those stakeholders that

Слайд 14Who Are Business Stakeholders?

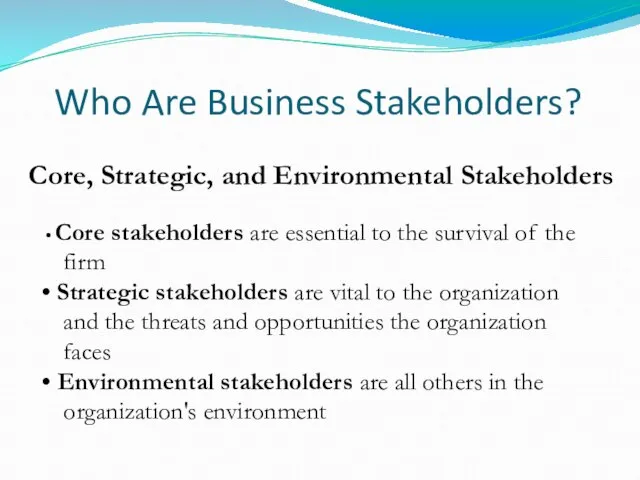

Core, Strategic, and Environmental Stakeholders

Core stakeholders are essential

Who Are Business Stakeholders?

Core, Strategic, and Environmental Stakeholders

Core stakeholders are essential

Слайд 15Who Are Business Stakeholders?

Legitimacy refers to the perceived validity of the stakeholder’s

Who Are Business Stakeholders?

Legitimacy refers to the perceived validity of the stakeholder’s

Слайд 16Who Are Business Stakeholders?

Who Are Business Stakeholders?

Слайд 17Strategic, Multifiduciary, and Synthesis Views of Stakeholders

Strategic approach considers stakeholders primarily as

Strategic, Multifiduciary, and Synthesis Views of Stakeholders

Strategic approach considers stakeholders primarily as

Слайд 18Three Values of the Stakeholder Model

Descriptive

Instrumental

Normative

Three Values of the Stakeholder Model

Descriptive

Instrumental

Normative

Слайд 19Key Questions In

Stakeholder Management

Who are our stakeholders?

What are our stakeholders’ stakes?

What

Key Questions In

Stakeholder Management

Who are our stakeholders?

What are our stakeholders’ stakes?

What

Слайд 20Key Questions In Stakeholder Management

Who are our stakeholders

Management must identify generic stakeholder

Key Questions In Stakeholder Management

Who are our stakeholders

Management must identify generic stakeholder

Слайд 21Key Questions In Stakeholder Management

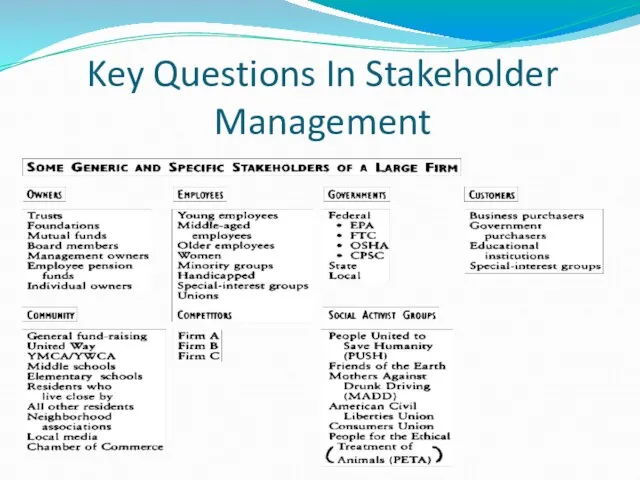

Key Questions In Stakeholder Management

Слайд 22Key Questions In Stakeholder Management

What are our stakeholders’ stakes?

Determine the nature/legitimacy of

Key Questions In Stakeholder Management

What are our stakeholders’ stakes?

Determine the nature/legitimacy of

Слайд 23Key Questions In Stakeholder Management

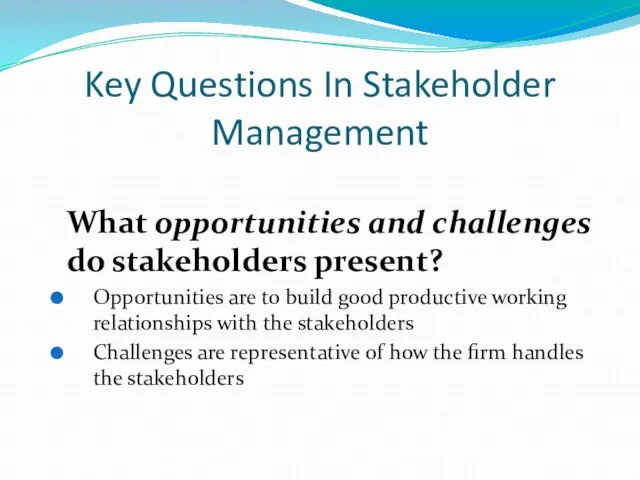

What opportunities and challenges do stakeholders present?

Opportunities

Key Questions In Stakeholder Management

What opportunities and challenges do stakeholders present?

Opportunities

Слайд 24Key Questions In Stakeholder Management

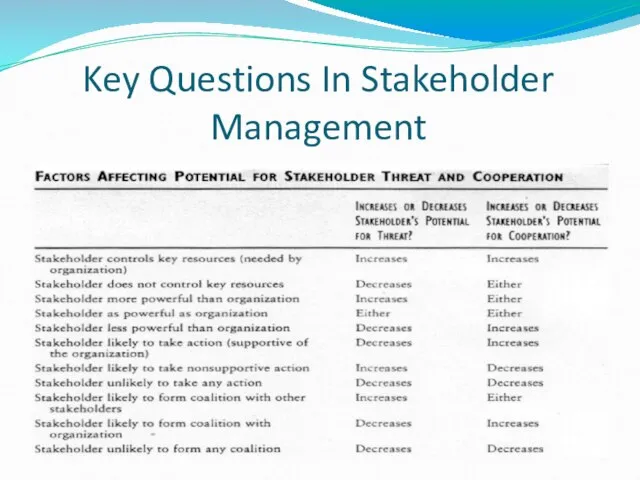

Key Questions In Stakeholder Management

Слайд 25Key Questions In Stakeholder Management

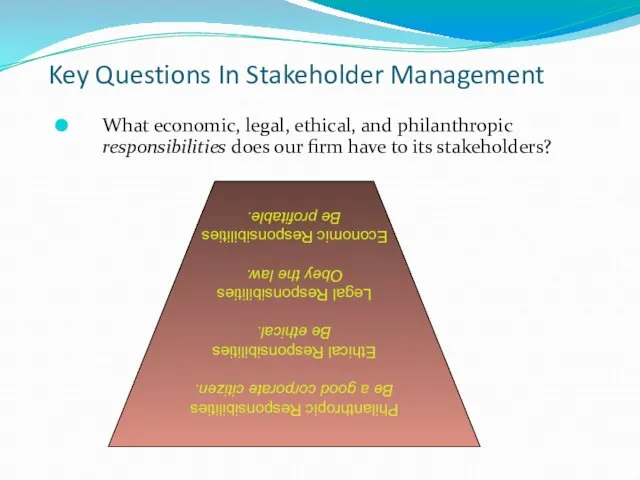

What economic, legal, ethical, and philanthropic responsibilities does

Key Questions In Stakeholder Management

What economic, legal, ethical, and philanthropic responsibilities does

Слайд 26Key Questions In Stakeholder Management

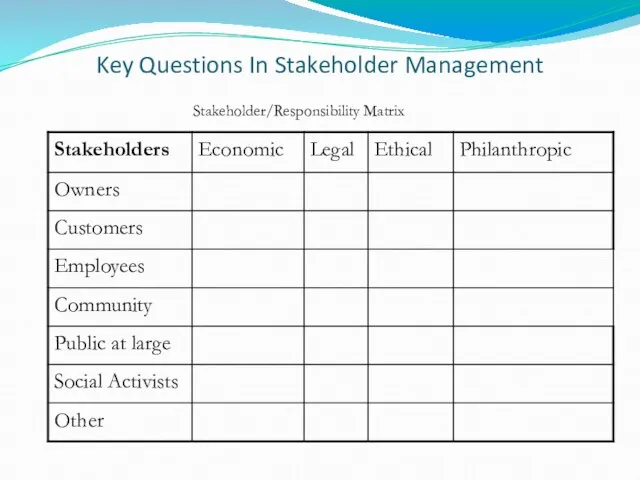

Stakeholder/Responsibility Matrix

Key Questions In Stakeholder Management

Stakeholder/Responsibility Matrix

Слайд 27Key Questions In Stakeholder Management

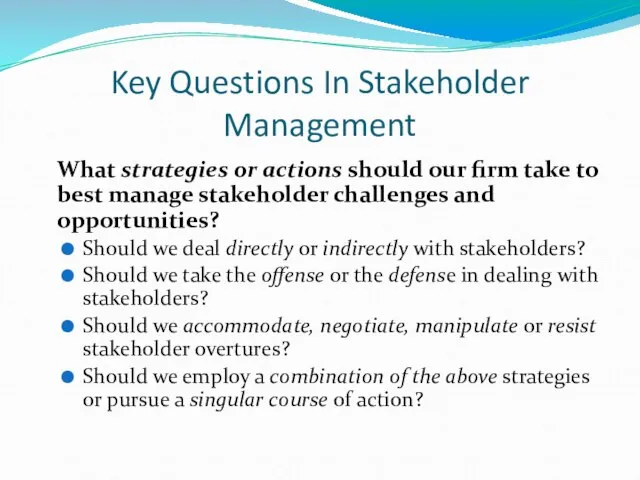

What strategies or actions should our firm take

Key Questions In Stakeholder Management

What strategies or actions should our firm take

Слайд 28Key Questions In Stakeholder Management

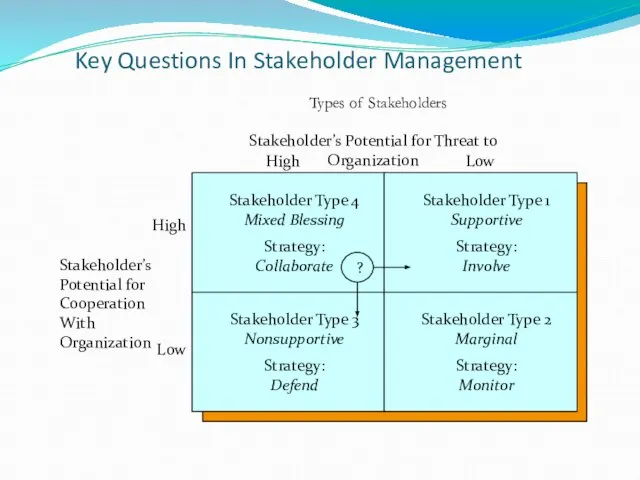

Types of Stakeholders

Key Questions In Stakeholder Management

Types of Stakeholders

Слайд 29Effective Stakeholder Management

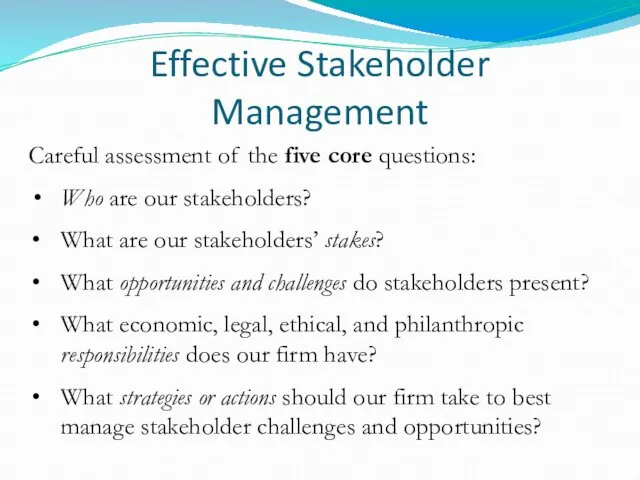

Careful assessment of the five core questions:

Who are our stakeholders?

What

Effective Stakeholder Management

Careful assessment of the five core questions:

Who are our stakeholders?

What

Слайд 30Effective Stakeholder Management

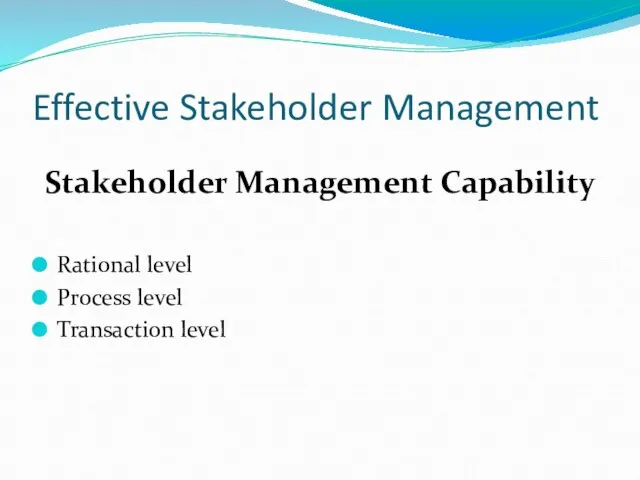

Stakeholder Management Capability

Rational level

Process level

Transaction level

Effective Stakeholder Management

Stakeholder Management Capability

Rational level

Process level

Transaction level

Слайд 31Effective Stakeholder Management

Stakeholder Corporation

Stakeholder inclusiveness

Stakeholder symbiosis

Effective Stakeholder Management

Stakeholder Corporation

Stakeholder inclusiveness

Stakeholder symbiosis

Слайд 32Stakeholder Power:

Four Gates of Engagement

Awareness

Knowledge

Admiration

Action

Stakeholder Power:

Four Gates of Engagement

Awareness

Knowledge

Admiration

Action

Слайд 33Principles of Stakeholder Management

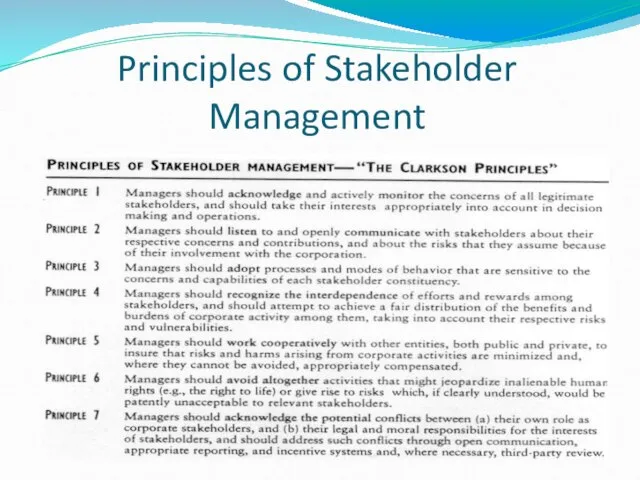

Acknowledge

Monitor

Listen

Communicate

Adopt

Recognize

Work

Avoid

Acknowledge conflict

Principles of Stakeholder Management

Acknowledge

Monitor

Listen

Communicate

Adopt

Recognize

Work

Avoid

Acknowledge conflict

Слайд 34Principles of Stakeholder Management

Principles of Stakeholder Management

Слайд 35Core Stakeholders

Environmental Stakeholders

Legitimacy

Managerial view of

the firm

Power

Principles of stakeholder management

Process level

Production view

Core Stakeholders

Environmental Stakeholders

Legitimacy

Managerial view of

the firm

Power

Principles of stakeholder management

Process level

Production view

Слайд 36Environmental reporting

Refers to the issuance of any report containing information of

Environmental reporting

Refers to the issuance of any report containing information of

Слайд 37History of Corporate Environmental Reporting (CER)

First corporate environmental reports were released in

History of Corporate Environmental Reporting (CER)

First corporate environmental reports were released in

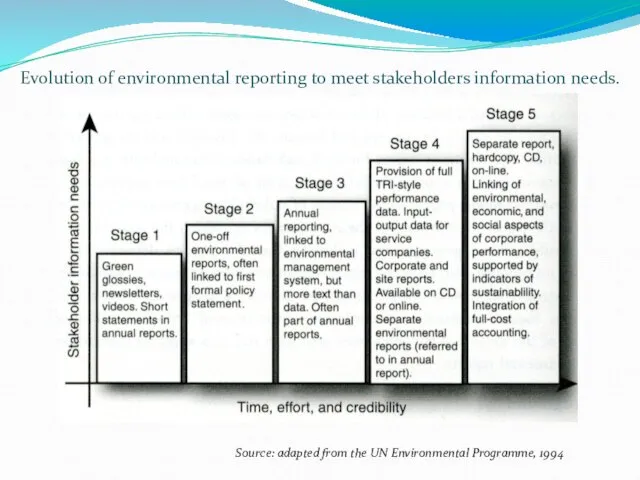

Слайд 38Evolution of environmental reporting to meet stakeholders information needs.

Source: adapted from the

Evolution of environmental reporting to meet stakeholders information needs.

Source: adapted from the

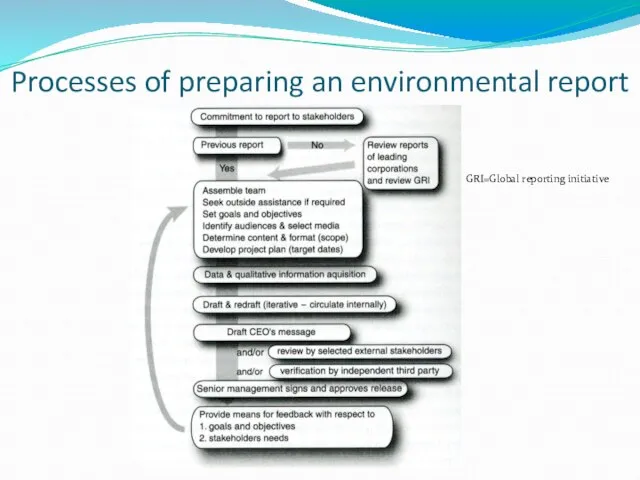

Слайд 39Processes of preparing an environmental report

GRI=Global reporting initiative

Processes of preparing an environmental report

GRI=Global reporting initiative

Слайд 40Reliability of the data

At any time in a corporation, different performance measurement

Reliability of the data

At any time in a corporation, different performance measurement

Слайд 41Reporting and verification, measurement processes & reliable data

Reporting and verification, measurement processes & reliable data

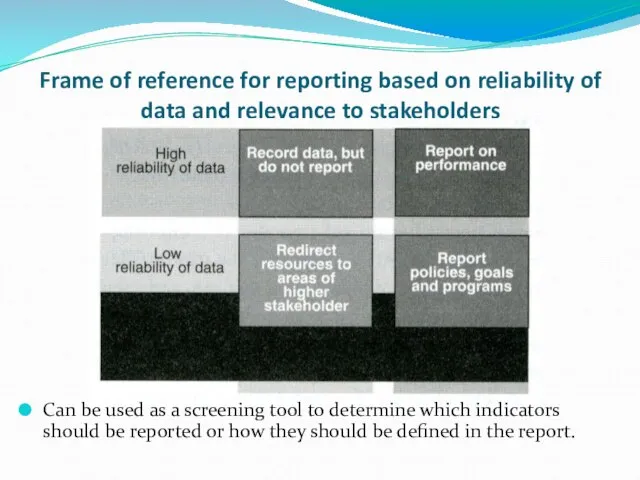

Слайд 42Frame of reference for reporting based on reliability of data and relevance

Frame of reference for reporting based on reliability of data and relevance

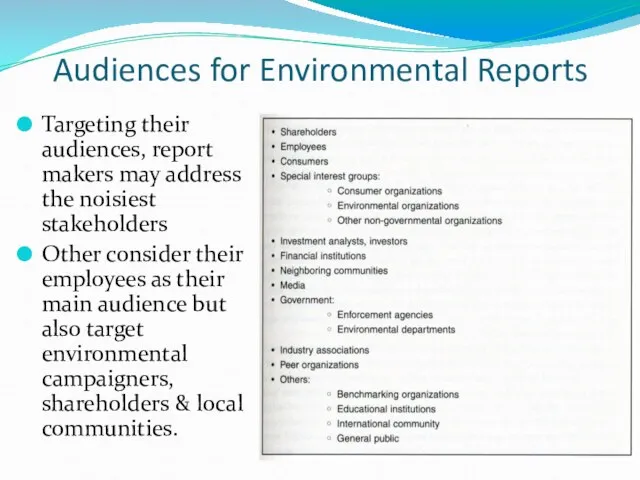

Слайд 43Audiences for Environmental Reports

Targeting their audiences, report makers may address the noisiest

Audiences for Environmental Reports

Targeting their audiences, report makers may address the noisiest

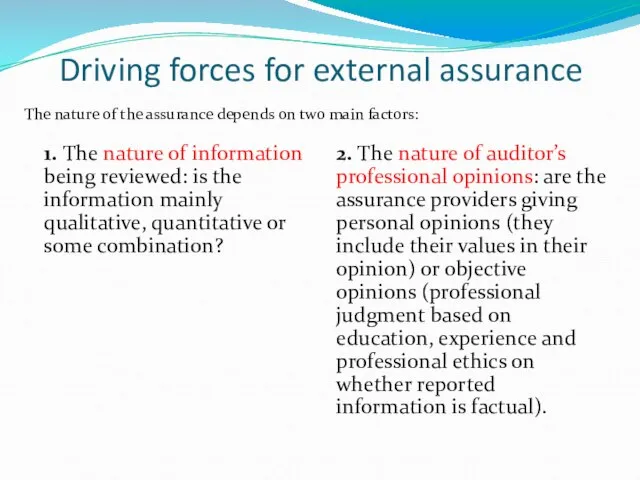

Слайд 44Driving forces for external assurance

1. The nature of information being reviewed: is

Driving forces for external assurance

1. The nature of information being reviewed: is

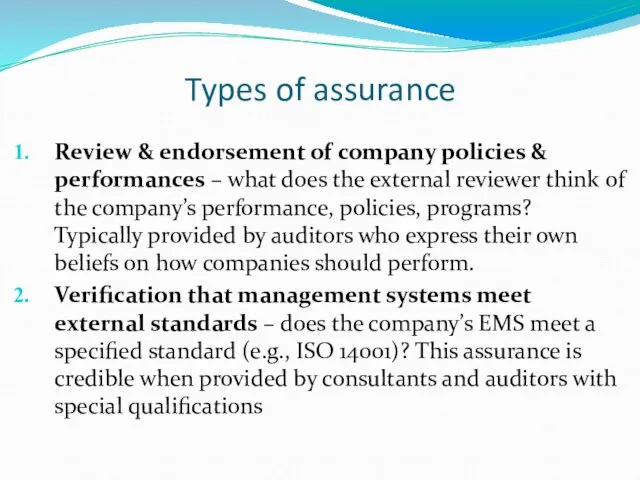

Слайд 45Types of assurance

Review & endorsement of company policies & performances – what

Types of assurance

Review & endorsement of company policies & performances – what

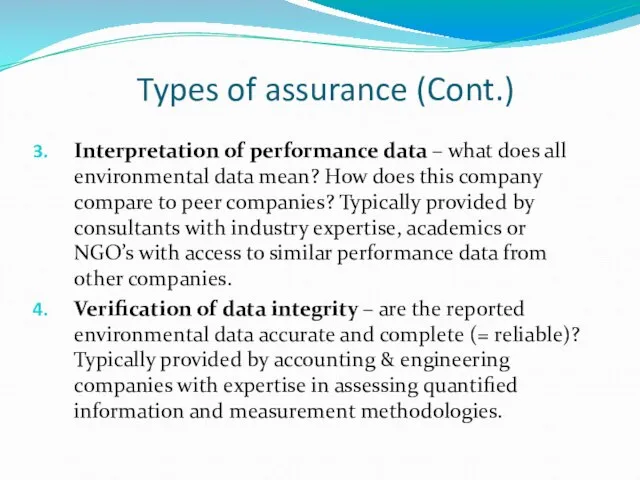

Слайд 46Interpretation of performance data – what does all environmental data mean? How

Interpretation of performance data – what does all environmental data mean? How

Слайд 47Four types of external assurance that vary with the quantitative and qualitative

Four types of external assurance that vary with the quantitative and qualitative

Собор Парижской Богоматери. Франция - родина готической архитектуры

Собор Парижской Богоматери. Франция - родина готической архитектуры Паркет Europa

Паркет Europa О подготовке образовательных учреждений города Лангепаса к началу 2012-2013 учебного года

О подготовке образовательных учреждений города Лангепаса к началу 2012-2013 учебного года Тайна Шекспира

Тайна Шекспира Торнадо любви. Направление Личные Цели

Торнадо любви. Направление Личные Цели Who took the cookie from the cookie jar

Who took the cookie from the cookie jar Сказка «Волшебное число»

Сказка «Волшебное число» My giant nerd boyfriend

My giant nerd boyfriend Роль системы развития персонала организации

Роль системы развития персонала организации Цифровая подстанция - важный элемент интеллектуальной энергосистемы

Цифровая подстанция - важный элемент интеллектуальной энергосистемы Как работают экономисты

Как работают экономисты «Вода – капля жизни» Участники: Дети и родители Воспитатели: Андреева Янина Евгеньевна

«Вода – капля жизни» Участники: Дети и родители Воспитатели: Андреева Янина Евгеньевна Жемчужины Республики Марий Эл

Жемчужины Республики Марий Эл Социальная напряжённость

Социальная напряжённость Метрологическое обеспечение технологического процесса изготовления продукции

Метрологическое обеспечение технологического процесса изготовления продукции Технологии разработки проектов, программ и требования к их реализации

Технологии разработки проектов, программ и требования к их реализации Построение чертежа фартука

Построение чертежа фартука Финансовая отчетностьв реальном времени.

Финансовая отчетностьв реальном времени. Кислоты 11 класс

Кислоты 11 класс Внутреннее строение рыб

Внутреннее строение рыб Автоматизация АОСЧ

Автоматизация АОСЧ М.А.Шолохов

М.А.Шолохов Гармония образа

Гармония образа Словарик горнорудных профессий

Словарик горнорудных профессий План «Барбаросса» предполагал «блицкриг» - т.е. рассчитан на молниеносную войну в течение нескольких месяцевБарбароссаблицкриг.

План «Барбаросса» предполагал «блицкриг» - т.е. рассчитан на молниеносную войну в течение нескольких месяцевБарбароссаблицкриг. Гражданское общество и правовое государство. 9 класс

Гражданское общество и правовое государство. 9 класс Конкурс чтецов, посвящённый творчеству Э. Асадова

Конкурс чтецов, посвящённый творчеству Э. Асадова СГУ им. Чернышевского

СГУ им. Чернышевского