- The accouting process

Содержание

- 2. THE ACCOUNTING PROCESS After studying this chapter you should be able to: explain the nature and

- 3. WHAT IS ACCOUNTING? Accounting was defined by Paul F. Grady as: … the body of knowledge

- 4. WHAT IS ACCOUNTING? The four facets of the accounting process: Design of the accounting information system

- 5. WHY IS FINANCIAL INFORMATION IMPORTANT? Financial information: Measures the economic health of a business Provides information

- 6. WHO USES THE INFORMATION? Internal users: Those working within the business who create the information External

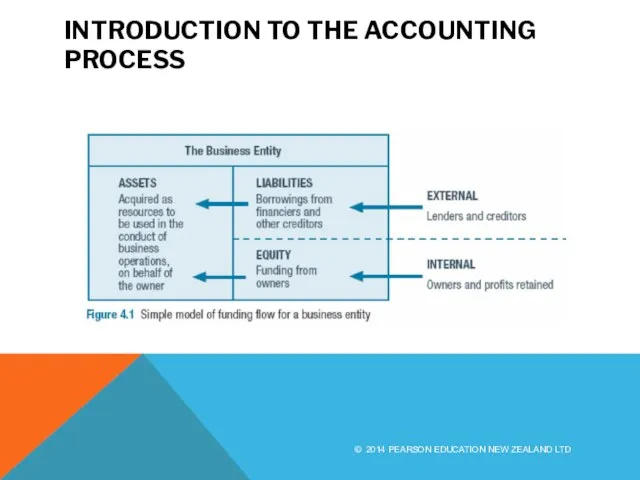

- 7. INTRODUCTION TO THE ACCOUNTING PROCESS The entity concept The affairs of a business entity are kept

- 8. INTRODUCTION TO THE ACCOUNTING PROCESS © 2014 PEARSON EDUCATION NEW ZEALAND LTD

- 9. INTRODUCTION TO THE ACCOUNTING PROCESS The accounting equation Assets = Liabilities + Equity Benefits = Obligations

- 10. PRINCIPLE OF DOUBLE ENTRY For each transaction there must be balancing debit and credit entries made

- 11. THE BASIS FOR RECORDING FINANCIAL TRANSACTIONS Monetary convention – the expressing of financial transactions in a

- 12. CONTROLLABLE AND NON-CONTROLLABLE EVENTS Controllable events Transactions undertaken by the business that have an impact on

- 13. THE ROLE OF SOURCE DOCUMENTS A source document identifies the transaction and gives it a monetary

- 14. CONTROL DOCUMENTS Control documents establish authorisation to initiate business events and source documents. They provide an

- 15. STEPS IN THE ACCOUNTING PROCESS There are four essential steps in the accounting process. Collection Processing

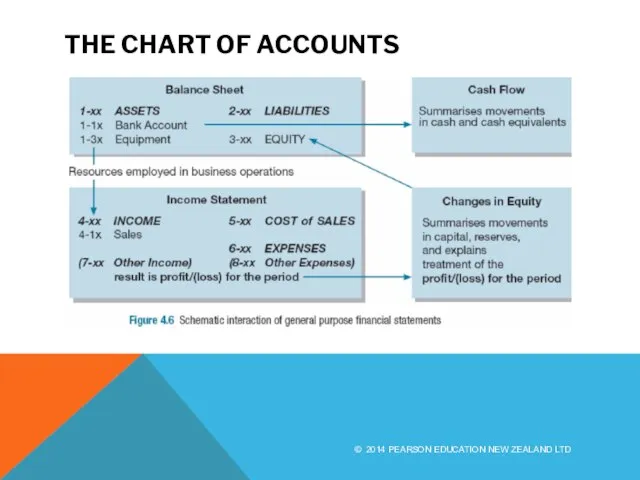

- 16. THE CHART OF ACCOUNTS Chart of Accounts: is a numerical list of all the ledger accounts

- 17. THE CHART OF ACCOUNTS Links the four principle accounting statements: Balance sheet, Income statement, Statement of

- 18. THE CHART OF ACCOUNTS © 2014 PEARSON EDUCATION NEW ZEALAND LTD

- 19. INTERNAL CONTROL Internal control - policies and procedures that inform management as to whether operational objectives

- 20. INTERNAL CONTROL For internal control strategies to work as intended, five principles: Attitude, Assessment, Activity, Advice,

- 21. INTERNAL CONTROL Practical internal control measures include: Establishment of responsibility Segregation of duties Documentation procedures Physical,

- 23. Скачать презентацию

Слайд 3WHAT IS ACCOUNTING?

Accounting was defined by Paul F. Grady as:

… the

WHAT IS ACCOUNTING?

Accounting was defined by Paul F. Grady as:

… the

Слайд 4WHAT IS ACCOUNTING?

The four facets of the accounting process:

Design of the accounting

WHAT IS ACCOUNTING?

The four facets of the accounting process:

Design of the accounting

Слайд 5WHY IS FINANCIAL INFORMATION IMPORTANT?

Financial information:

Measures the economic health of a business

Provides

WHY IS FINANCIAL INFORMATION IMPORTANT?

Financial information:

Measures the economic health of a business

Provides

Слайд 6WHO USES THE INFORMATION?

Internal users:

Those working within the business who

WHO USES THE INFORMATION?

Internal users:

Those working within the business who

Слайд 7INTRODUCTION TO THE ACCOUNTING PROCESS

The entity concept

The affairs of a business entity

INTRODUCTION TO THE ACCOUNTING PROCESS

The entity concept

The affairs of a business entity

Слайд 8INTRODUCTION TO THE ACCOUNTING PROCESS

© 2014 PEARSON EDUCATION NEW ZEALAND LTD

INTRODUCTION TO THE ACCOUNTING PROCESS

© 2014 PEARSON EDUCATION NEW ZEALAND LTD

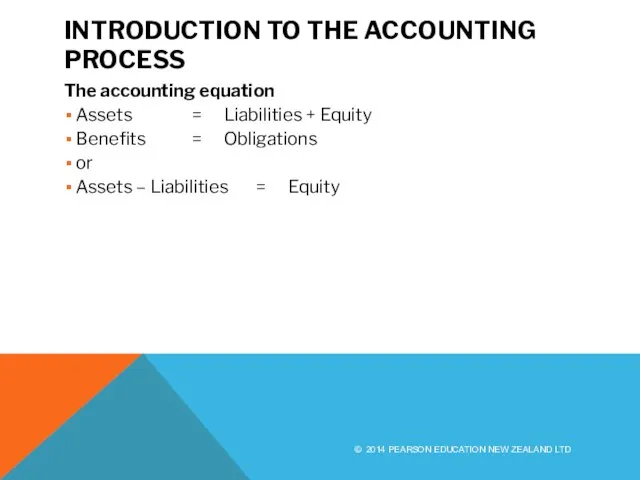

Слайд 9INTRODUCTION TO THE ACCOUNTING PROCESS

The accounting equation

Assets = Liabilities + Equity

Benefits = Obligations

or

Assets – Liabilities =

INTRODUCTION TO THE ACCOUNTING PROCESS

The accounting equation

Assets = Liabilities + Equity

Benefits = Obligations

or

Assets – Liabilities =

Слайд 10PRINCIPLE OF DOUBLE ENTRY

For each transaction there must be balancing debit and

PRINCIPLE OF DOUBLE ENTRY

For each transaction there must be balancing debit and

Слайд 11THE BASIS FOR RECORDING FINANCIAL TRANSACTIONS

Monetary convention – the expressing of financial

THE BASIS FOR RECORDING FINANCIAL TRANSACTIONS

Monetary convention – the expressing of financial

Слайд 12CONTROLLABLE AND NON-CONTROLLABLE EVENTS

Controllable events

Transactions undertaken by the business that have an

CONTROLLABLE AND NON-CONTROLLABLE EVENTS

Controllable events

Transactions undertaken by the business that have an

Слайд 13THE ROLE OF SOURCE DOCUMENTS

A source document identifies the transaction and gives

THE ROLE OF SOURCE DOCUMENTS

A source document identifies the transaction and gives

Слайд 14CONTROL DOCUMENTS

Control documents establish authorisation to initiate business events and source documents.

They

CONTROL DOCUMENTS

Control documents establish authorisation to initiate business events and source documents.

They

Слайд 15STEPS IN THE ACCOUNTING PROCESS

There are four essential steps in the accounting

STEPS IN THE ACCOUNTING PROCESS

There are four essential steps in the accounting

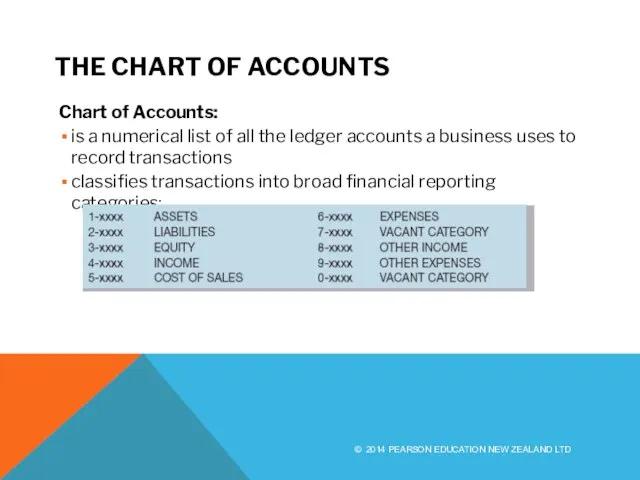

Слайд 16THE CHART OF ACCOUNTS

Chart of Accounts:

is a numerical list of all the

THE CHART OF ACCOUNTS

Chart of Accounts:

is a numerical list of all the

Слайд 17THE CHART OF ACCOUNTS

Links the four principle accounting statements:

Balance sheet,

Income statement,

Statement of

THE CHART OF ACCOUNTS

Links the four principle accounting statements:

Balance sheet,

Income statement,

Statement of

Слайд 18THE CHART OF ACCOUNTS

© 2014 PEARSON EDUCATION NEW ZEALAND LTD

THE CHART OF ACCOUNTS

© 2014 PEARSON EDUCATION NEW ZEALAND LTD

Слайд 19INTERNAL CONTROL

Internal control - policies and procedures that inform management as to

INTERNAL CONTROL

Internal control - policies and procedures that inform management as to

Слайд 20INTERNAL CONTROL

For internal control strategies to work as intended, five principles:

Attitude,

Assessment,

INTERNAL CONTROL

For internal control strategies to work as intended, five principles:

Attitude,

Assessment,

Слайд 21INTERNAL CONTROL

Practical internal control measures include:

Establishment of responsibility

Segregation of duties

Documentation procedures

Physical, mechanical

INTERNAL CONTROL

Practical internal control measures include:

Establishment of responsibility

Segregation of duties

Documentation procedures

Physical, mechanical

Собор Парижской Богоматери. Франция - родина готической архитектуры

Собор Парижской Богоматери. Франция - родина готической архитектуры Паркет Europa

Паркет Europa О подготовке образовательных учреждений города Лангепаса к началу 2012-2013 учебного года

О подготовке образовательных учреждений города Лангепаса к началу 2012-2013 учебного года Тайна Шекспира

Тайна Шекспира Торнадо любви. Направление Личные Цели

Торнадо любви. Направление Личные Цели Who took the cookie from the cookie jar

Who took the cookie from the cookie jar Сказка «Волшебное число»

Сказка «Волшебное число» My giant nerd boyfriend

My giant nerd boyfriend Роль системы развития персонала организации

Роль системы развития персонала организации Цифровая подстанция - важный элемент интеллектуальной энергосистемы

Цифровая подстанция - важный элемент интеллектуальной энергосистемы Как работают экономисты

Как работают экономисты «Вода – капля жизни» Участники: Дети и родители Воспитатели: Андреева Янина Евгеньевна

«Вода – капля жизни» Участники: Дети и родители Воспитатели: Андреева Янина Евгеньевна Жемчужины Республики Марий Эл

Жемчужины Республики Марий Эл Социальная напряжённость

Социальная напряжённость Метрологическое обеспечение технологического процесса изготовления продукции

Метрологическое обеспечение технологического процесса изготовления продукции Технологии разработки проектов, программ и требования к их реализации

Технологии разработки проектов, программ и требования к их реализации Построение чертежа фартука

Построение чертежа фартука Финансовая отчетностьв реальном времени.

Финансовая отчетностьв реальном времени. Кислоты 11 класс

Кислоты 11 класс Внутреннее строение рыб

Внутреннее строение рыб Автоматизация АОСЧ

Автоматизация АОСЧ М.А.Шолохов

М.А.Шолохов Гармония образа

Гармония образа Словарик горнорудных профессий

Словарик горнорудных профессий План «Барбаросса» предполагал «блицкриг» - т.е. рассчитан на молниеносную войну в течение нескольких месяцевБарбароссаблицкриг.

План «Барбаросса» предполагал «блицкриг» - т.е. рассчитан на молниеносную войну в течение нескольких месяцевБарбароссаблицкриг. Гражданское общество и правовое государство. 9 класс

Гражданское общество и правовое государство. 9 класс Конкурс чтецов, посвящённый творчеству Э. Асадова

Конкурс чтецов, посвящённый творчеству Э. Асадова СГУ им. Чернышевского

СГУ им. Чернышевского