- The International Monetary System

Содержание

- 2. What is special about international finance? Foreign exchange risk E.g., an unexpected devaluation adversely affects your

- 3. The Monetary System Bimetallism: Before 1875 Free coinage was maintained for both gold and silver Gresham’s

- 4. The Monetary System Interwar period: 1915-1944 World War I ended the classical gold standard in 1914

- 5. The Monetary System Jamaica Agreement (1976) Central banks were allowed to intervene in the foreign exchange

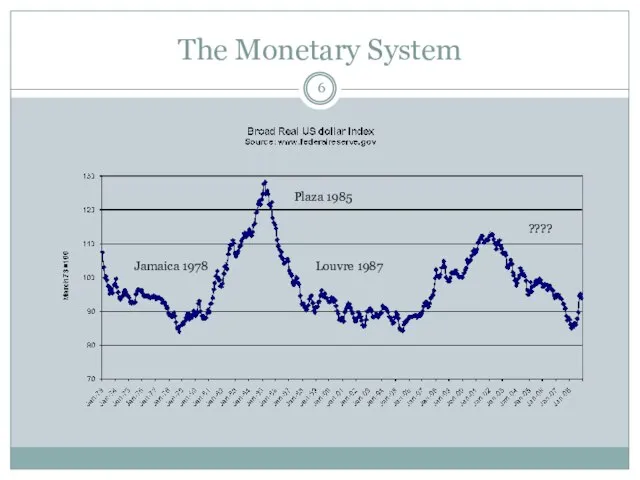

- 6. The Monetary System Jamaica 1978 Plaza 1985 Louvre 1987 ????

- 7. Current Exchange Rate Arrangements 36 major currencies, such as the U.S. dollar, the Japanese yen, the

- 8. The Euro Product of the desire to create a more integrated European economy. Eleven European countries

- 9. The Euro Nowadays the euro (€) is the official currency of 17 out of 27 EU

- 10. Will the UK (Sweden) join the Euro? Think about: Potential benefits and costs of adopting the

- 11. THE ORGANIZATION OF THE FOREIGN EXCHANGE MARKET THE SPOT MARKET THE FORWARD MARKET THE FOREIGN EXCHANGE

- 12. The organization of the Foreign Exchange Market Foreign exchange market - the market in which one

- 13. The organization of the Foreign Exchange Market An exchange rate is simply the price of one

- 14. The Foreign Exchange Market The FX market encompasses: Conversion of purchasing power from one currency to

- 15. Global Foreign Exchange Market Turnover Source: BIS Triennial Central Bank Survey of Foreign Exchange and Derivatives

- 16. BIS (Bank for International Settlements) Triennial Survey…

- 17. The Foreign Exchange Market The FX market is a two-tiered market: Interbank Market (Wholesale) Accounts for

- 18. Central Banking The U.S. monetary authorities occasionally intervene in the foreign exchange (FX) market to counter

- 19. The Foreign Exchange Market

- 20. Overview Currency Table

- 21. The Spot Market The spot market involves the immediate purchase or sale of foreign exchange Cash

- 22. The Spot Market – Direct Quotes US dollar price of 1 unit of foreign currency—$ are

- 23. The Spot Market – Indirect Quotes Foreign currency price of $1—$ are in the denominator (US

- 24. The Spot Market - Conventions Denote the spot rate as S For most currencies, use 4

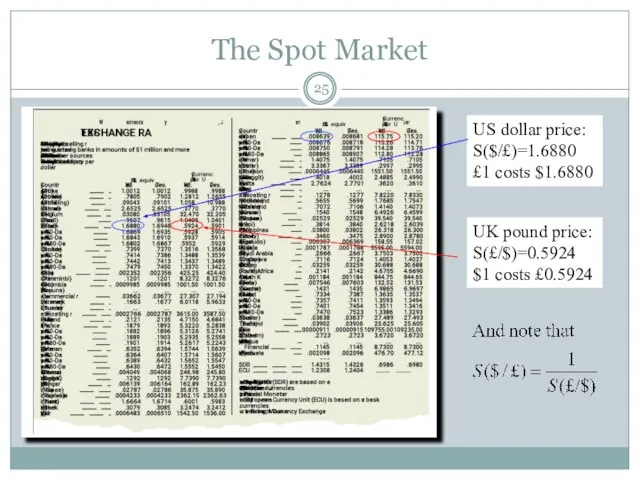

- 25. US dollar price: S($/£)=1.6880 £1 costs $1.6880 UK pound price: S(£/$)=0.5924 $1 costs £0.5924 The Spot

- 26. The current exchange, S($/€)=1.5000. In 1 month, it is S(€/$)=0.6689 Has the US dollar appreciated or

- 27. The exchange rate between 2 currencies where neither currency is the US dollar We know the

- 28. Cross-rates must be internally consistent; otherwise arbitrage profit opportunities exist. Suppose that: A profit opportunity exists.

- 29. Cross-Exchange Rates Example Bank1: S($/¥)=0.0084; Bank2: S($/€)=1.0500; Bank3: S(€/¥)=0.0081. The implied cross rate between Bank 1

- 30. The Forward Market Forward market involves contracting today for the future purchase or sale of foreign

- 31. The Forward Market For example, the spot exchange rate for the Swiss franc is SF 1

- 32. The foreign exchange market is by far the largest financial market in the world. Currency traders

- 33. Assignment Suppose you are Professor Paul Krugman (Princeton University Economics Professor and NYT columnist (Op-Ed Page)).

- 35. Скачать презентацию

Слайд 2What is special about international finance?

Foreign exchange risk

E.g., an unexpected devaluation adversely

What is special about international finance?

Foreign exchange risk

E.g., an unexpected devaluation adversely

Слайд 3The Monetary System

Bimetallism: Before 1875

Free coinage was maintained for both gold and

The Monetary System

Bimetallism: Before 1875

Free coinage was maintained for both gold and

Слайд 4The Monetary System

Interwar period: 1915-1944

World War I ended the classical gold standard

The Monetary System

Interwar period: 1915-1944

World War I ended the classical gold standard

Слайд 5The Monetary System

Jamaica Agreement (1976)

Central banks were allowed to intervene in the

The Monetary System

Jamaica Agreement (1976)

Central banks were allowed to intervene in the

Слайд 6The Monetary System

Jamaica 1978

Plaza 1985

Louvre 1987

????

The Monetary System

Jamaica 1978

Plaza 1985

Louvre 1987

????

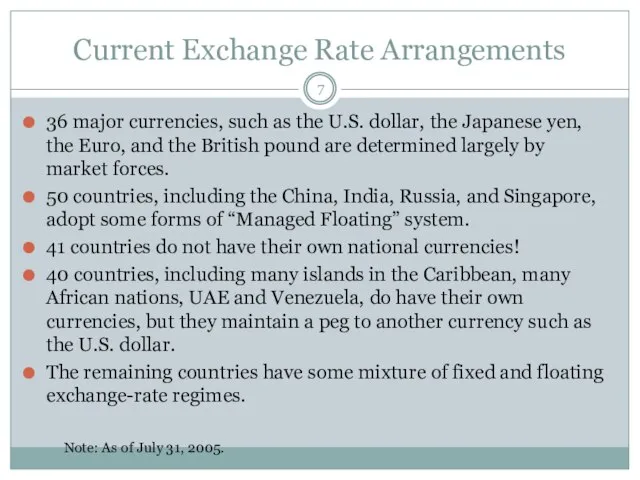

Слайд 7Current Exchange Rate Arrangements

36 major currencies, such as the U.S. dollar, the

Current Exchange Rate Arrangements

36 major currencies, such as the U.S. dollar, the

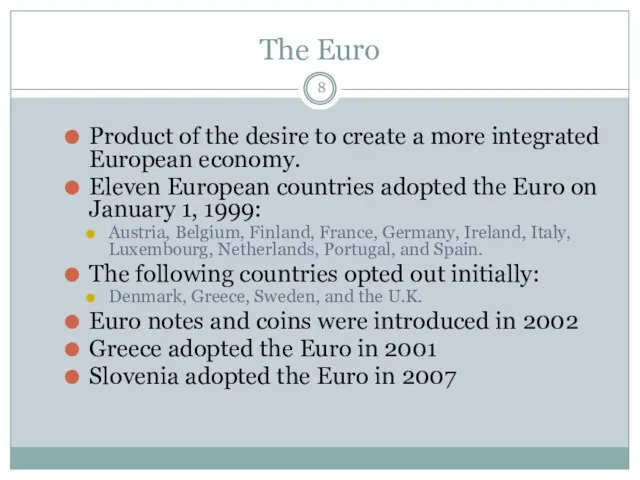

Слайд 8The Euro

Product of the desire to create a more integrated European economy.

Eleven

The Euro

Product of the desire to create a more integrated European economy.

Eleven

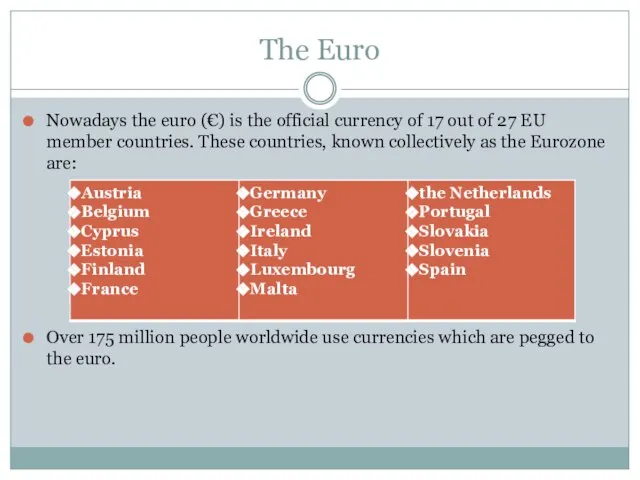

Слайд 9The Euro

Nowadays the euro (€) is the official currency of 17 out

The Euro

Nowadays the euro (€) is the official currency of 17 out

Слайд 10Will the UK (Sweden) join the Euro?

Think about:

Potential benefits and costs of

Will the UK (Sweden) join the Euro?

Think about:

Potential benefits and costs of

Слайд 11THE ORGANIZATION OF THE FOREIGN EXCHANGE MARKET

THE SPOT MARKET

THE FORWARD MARKET

THE FOREIGN

THE ORGANIZATION OF THE FOREIGN EXCHANGE MARKET

THE SPOT MARKET

THE FORWARD MARKET

THE FOREIGN

Слайд 12The organization of the Foreign Exchange Market

Foreign exchange market - the market

The organization of the Foreign Exchange Market

Foreign exchange market - the market

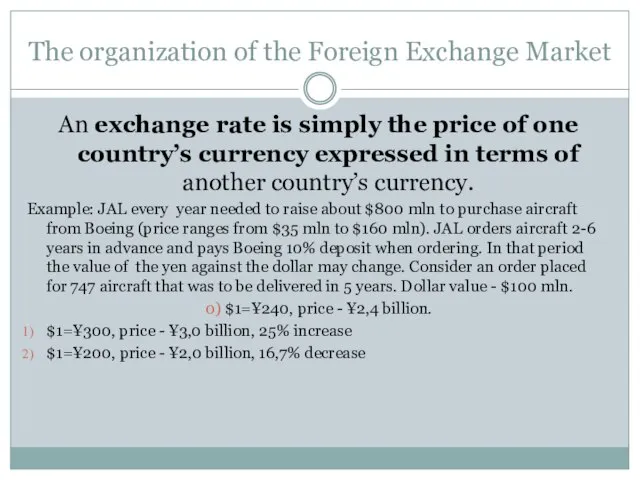

Слайд 13The organization of the Foreign Exchange Market

An exchange rate is simply the

The organization of the Foreign Exchange Market

An exchange rate is simply the

Слайд 14The Foreign Exchange Market

The FX market encompasses:

Conversion of purchasing power from one

The Foreign Exchange Market

The FX market encompasses:

Conversion of purchasing power from one

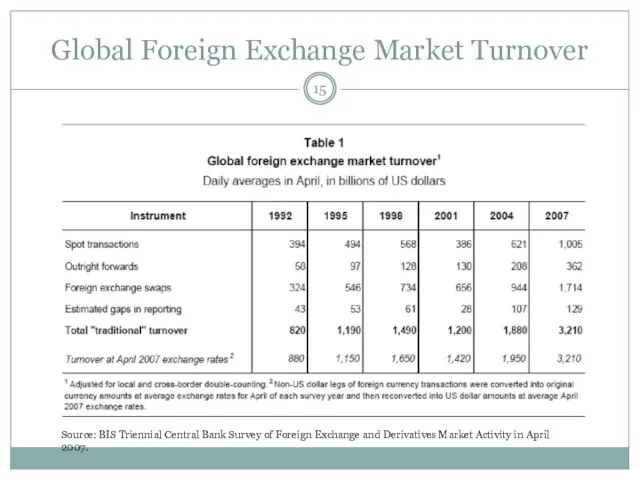

Слайд 15Global Foreign Exchange Market Turnover

Source: BIS Triennial Central Bank Survey of Foreign

Global Foreign Exchange Market Turnover

Source: BIS Triennial Central Bank Survey of Foreign

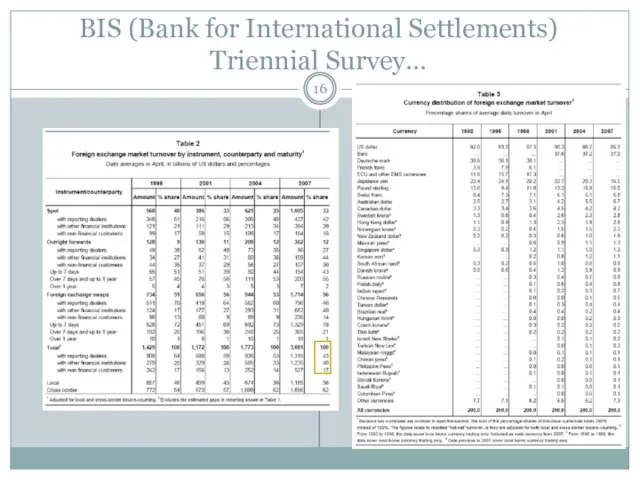

Слайд 16BIS (Bank for International Settlements) Triennial Survey…

BIS (Bank for International Settlements) Triennial Survey…

Слайд 17The Foreign Exchange Market

The FX market is a two-tiered market:

Interbank Market (Wholesale)

Accounts

The Foreign Exchange Market

The FX market is a two-tiered market:

Interbank Market (Wholesale)

Accounts

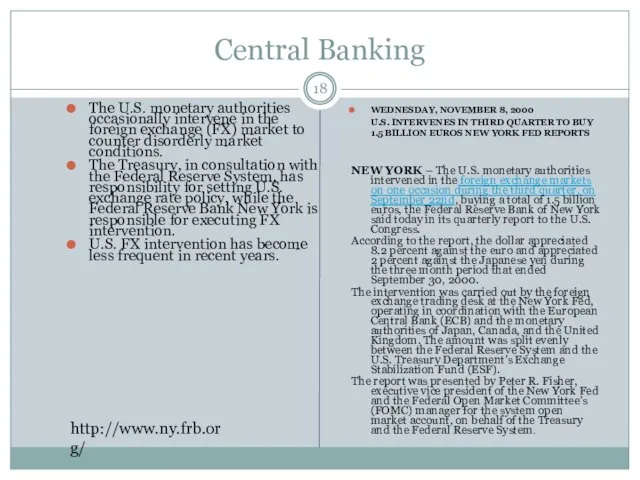

Слайд 18Central Banking

The U.S. monetary authorities occasionally intervene in the foreign exchange (FX)

Central Banking

The U.S. monetary authorities occasionally intervene in the foreign exchange (FX)

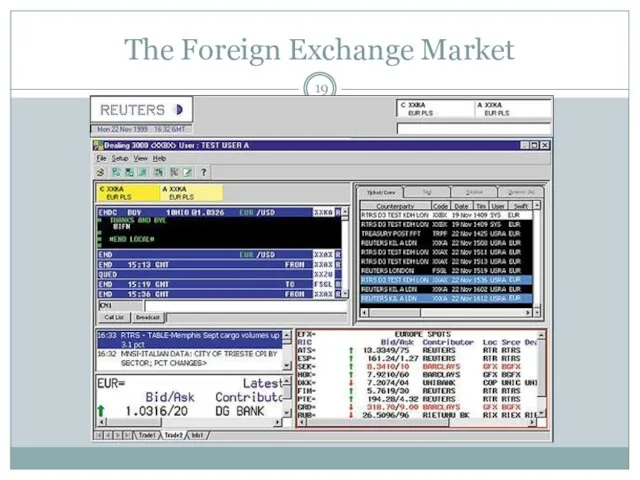

Слайд 19The Foreign Exchange Market

The Foreign Exchange Market

Слайд 20Overview

Currency Table

Overview

Currency Table

Слайд 21The Spot Market

The spot market involves the immediate purchase or sale of

The Spot Market

The spot market involves the immediate purchase or sale of

Слайд 22The Spot Market – Direct Quotes

US dollar price of 1 unit of

The Spot Market – Direct Quotes

US dollar price of 1 unit of

Слайд 23The Spot Market – Indirect Quotes

Foreign currency price of $1—$ are in

The Spot Market – Indirect Quotes

Foreign currency price of $1—$ are in

Слайд 24The Spot Market - Conventions

Denote the spot rate as S

For most currencies,

The Spot Market - Conventions

Denote the spot rate as S

For most currencies,

Слайд 25US dollar price:

S($/£)=1.6880

£1 costs $1.6880

UK pound price:

S(£/$)=0.5924

$1 costs £0.5924

The Spot Market

US dollar price:

S($/£)=1.6880

£1 costs $1.6880

UK pound price:

S(£/$)=0.5924

$1 costs £0.5924

The Spot Market

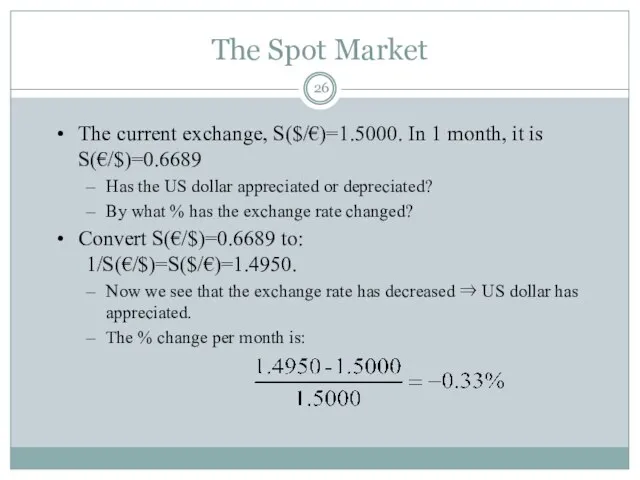

Слайд 26The current exchange, S($/€)=1.5000. In 1 month, it is S(€/$)=0.6689

Has the US

The current exchange, S($/€)=1.5000. In 1 month, it is S(€/$)=0.6689

Has the US

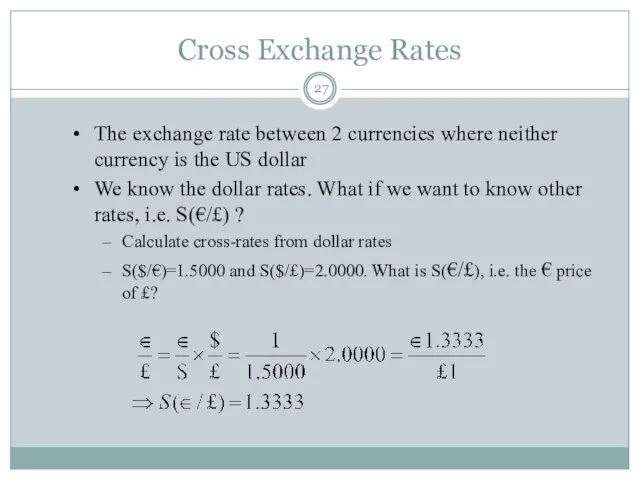

Слайд 27The exchange rate between 2 currencies where neither currency is the US

The exchange rate between 2 currencies where neither currency is the US

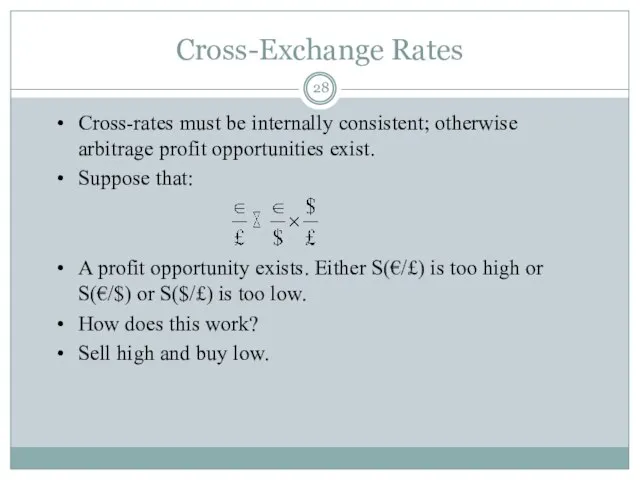

Слайд 28Cross-rates must be internally consistent; otherwise arbitrage profit opportunities exist.

Suppose that:

A profit

Cross-rates must be internally consistent; otherwise arbitrage profit opportunities exist.

Suppose that:

A profit

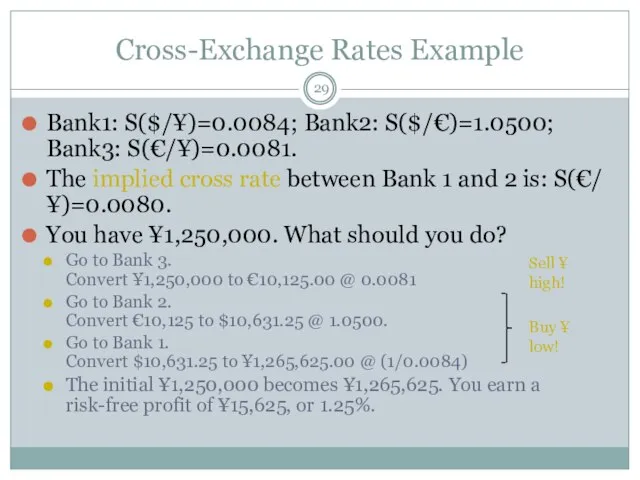

Слайд 29Cross-Exchange Rates Example

Bank1: S($/¥)=0.0084; Bank2: S($/€)=1.0500; Bank3: S(€/¥)=0.0081.

The implied cross rate between

Cross-Exchange Rates Example

Bank1: S($/¥)=0.0084; Bank2: S($/€)=1.0500; Bank3: S(€/¥)=0.0081.

The implied cross rate between

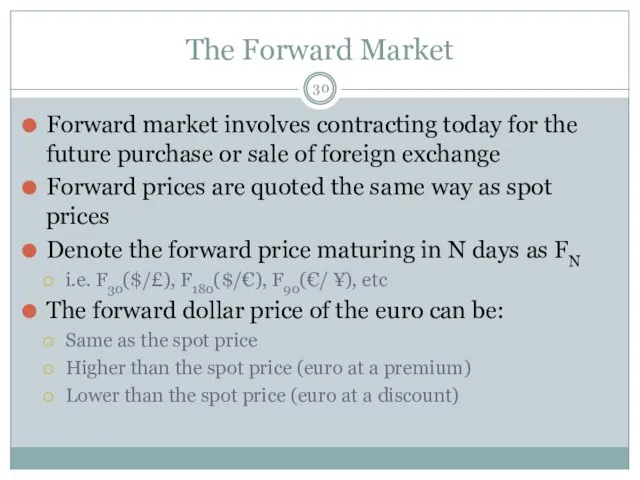

Слайд 30The Forward Market

Forward market involves contracting today for the future purchase or

The Forward Market

Forward market involves contracting today for the future purchase or

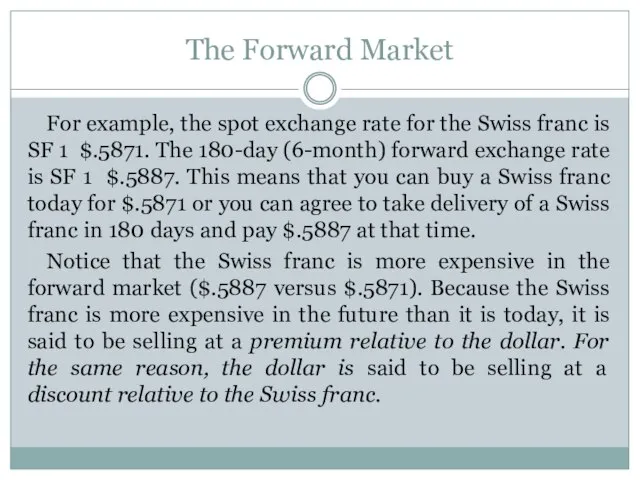

Слайд 31The Forward Market

For example, the spot exchange rate for the Swiss franc

The Forward Market

For example, the spot exchange rate for the Swiss franc

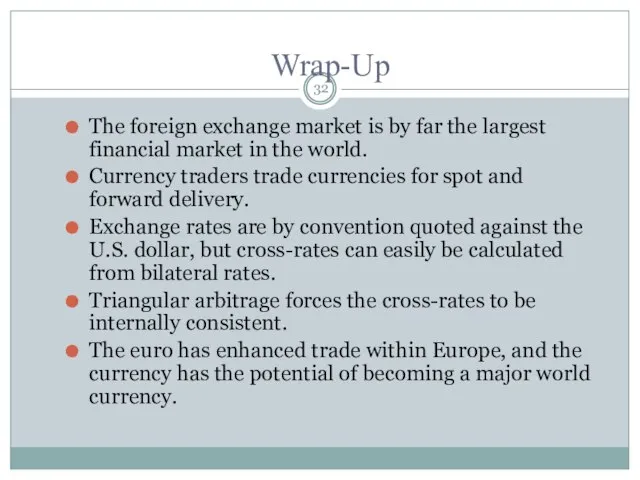

Слайд 32The foreign exchange market is by far the largest financial market in

The foreign exchange market is by far the largest financial market in

Слайд 33Assignment

Suppose you are Professor Paul Krugman (Princeton University Economics Professor and NYT

Assignment

Suppose you are Professor Paul Krugman (Princeton University Economics Professor and NYT

Удмуртский этнотуристический центр эштэрек

Удмуртский этнотуристический центр эштэрек Кладовщики. Должностная инструкция

Кладовщики. Должностная инструкция System administracji publicznej w Korei Północnej

System administracji publicznej w Korei Północnej Этикет и этика

Этикет и этика Что такое банк?

Что такое банк? Диагностика готовности первоклассников к обучению в школе

Диагностика готовности первоклассников к обучению в школе Сертификаты (1)

Сертификаты (1) «Не стоит село без праведника»

«Не стоит село без праведника» Магистерская диссертация:«Структурно-фазовое состояние титана, легированного под воздействием электронных пучков»

Магистерская диссертация:«Структурно-фазовое состояние титана, легированного под воздействием электронных пучков» Лизинговые сделки в Эстонии

Лизинговые сделки в Эстонии Молоко и его свойства. Блюда из молока

Молоко и его свойства. Блюда из молока Использование информационно-коммуникативных технологий для автоматизации рутинных операций образовательного процесса(на приме

Использование информационно-коммуникативных технологий для автоматизации рутинных операций образовательного процесса(на приме Nicaragua

Nicaragua Маку в мешочке насыпано, а не перетрясется.Маком по белой земле посеяно, далеко вожено, а куда пришло, там взошло.

Маку в мешочке насыпано, а не перетрясется.Маком по белой земле посеяно, далеко вожено, а куда пришло, там взошло. Безопасный Город международная практика

Безопасный Город международная практика Отчёт детской молодёжной организации «Мы – ростовчане» МОУ «СОШ № 70 Ленинского района г. Ростова-на-Дону», военно-патриотического

Отчёт детской молодёжной организации «Мы – ростовчане» МОУ «СОШ № 70 Ленинского района г. Ростова-на-Дону», военно-патриотического «Юный математик»

«Юный математик» ПРОГРАММА по изобразительному искусству “Воспитание мира чувств” по изобразительному искусству

ПРОГРАММА по изобразительному искусству “Воспитание мира чувств” по изобразительному искусству Дмитровский рыбохозяйственный технологический институт. Специальности и направления

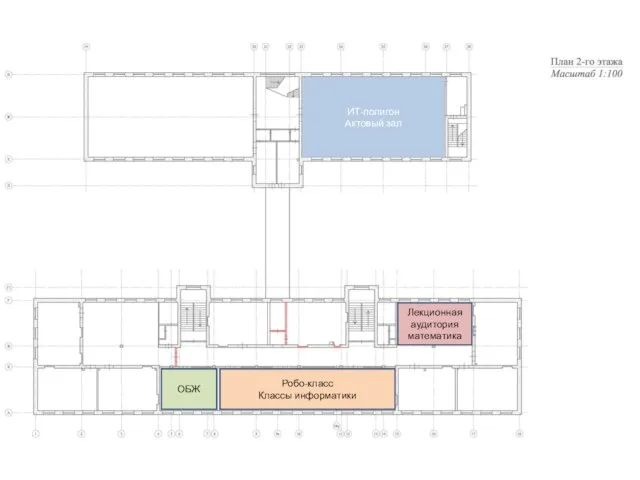

Дмитровский рыбохозяйственный технологический институт. Специальности и направления ИТ-полигон. Робо-класс. Планировочное решение

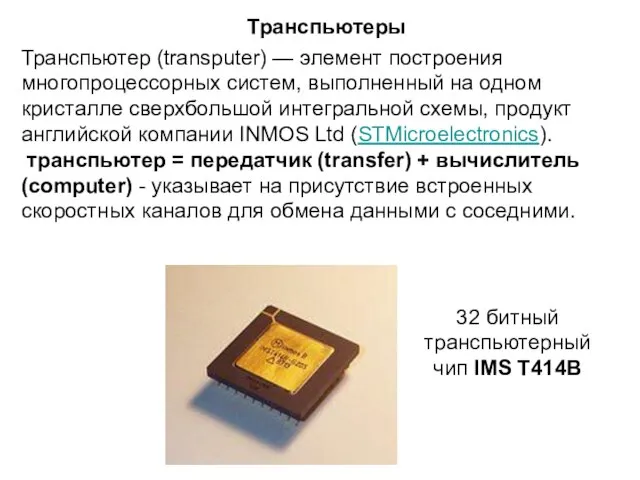

ИТ-полигон. Робо-класс. Планировочное решение Транспьютеры

Транспьютеры Результаты анонимного тестирования Скажем коррупции нет

Результаты анонимного тестирования Скажем коррупции нет Презентация на тему: В тридевятом царстве

Презентация на тему: В тридевятом царстве День молодого избирателя

День молодого избирателя Япония презентация. 日本

Япония презентация. 日本 «Фестиваль тюнинга в Томске»

«Фестиваль тюнинга в Томске» Дополнительные взыскания и порядок их применения по трудовому законодательству РФ

Дополнительные взыскания и порядок их применения по трудовому законодательству РФ Презентация на тему Роль инновационных технологий в повышении качества образования

Презентация на тему Роль инновационных технологий в повышении качества образования