- Are Financial Markets Effcient

Содержание

- 2. Roadmap The Efficient Market Hypothesis Stronger Version of Efficient Market Hypothesis Evidence on the Efficient Market

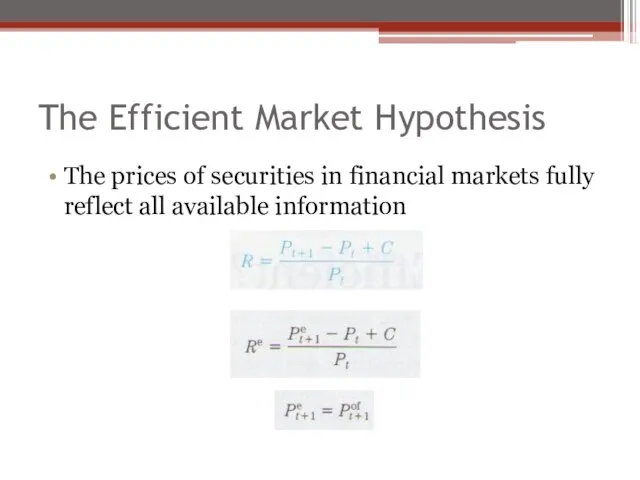

- 3. The Efficient Market Hypothesis The prices of securities in financial markets fully reflect all available information

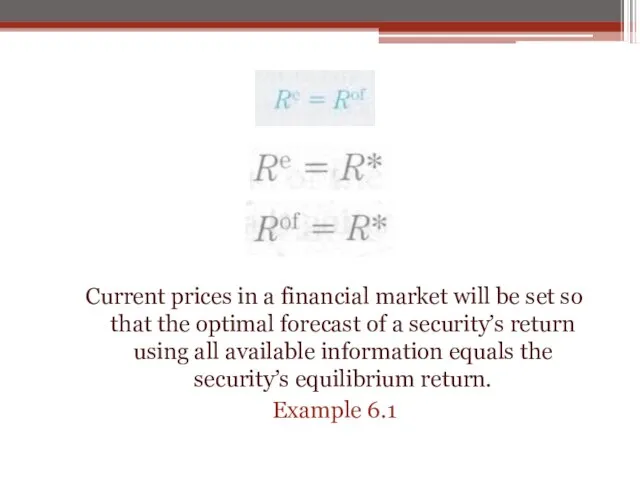

- 4. Current prices in a financial market will be set so that the optimal forecast of a

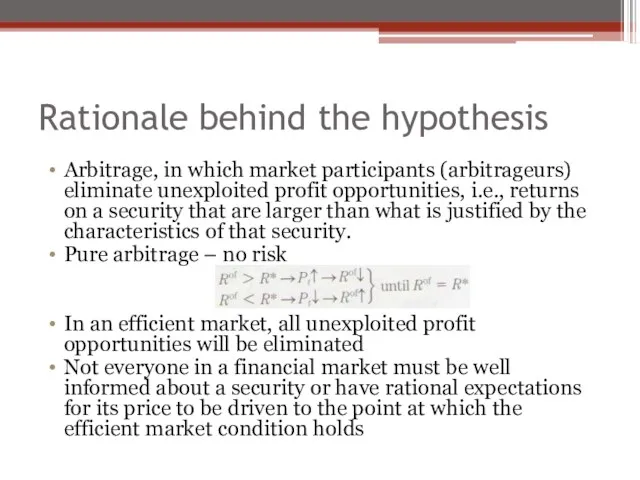

- 5. Rationale behind the hypothesis Arbitrage, in which market participants (arbitrageurs) eliminate unexploited profit opportunities, i.e., returns

- 6. Stronger Version of the Efficient Market Hypothesis Not only do scientists define an efficient market as

- 7. Implications of the above In an eff. market one investment is as good as any other

- 8. Evidence on the Efficient Market Hypothesis Evidence in favour of Market Efficiency Performance of investment analysts

- 9. Evidence on the Efficient Market Hypothesis Do stock prices reflect publically available information? Favourable stock announcements

- 10. Evidence Against Market Efficiency Small firm effect Due to rebalancing of portfolios by institutional investors, low

- 11. Evidence Against Market Efficiency Excessive volatility Fluctuations in stock prices may be much greater than is

- 12. Evidence Against Market Efficiency New information is not always immediately incorporated into stock prices On average

- 13. Overview of the Evidence on the EMH How valuable are publishable reports by Investment Advisors? We

- 14. Overview of the Evidence on the EMH Should you be skeptical of hot tips? If this

- 15. Overview of the Evidence on the EMH Efficient market prescription for an investor Hot tips, investment

- 17. Скачать презентацию

Слайд 2Roadmap

The Efficient Market Hypothesis

Stronger Version of Efficient Market Hypothesis

Evidence on the Efficient

Roadmap

The Efficient Market Hypothesis

Stronger Version of Efficient Market Hypothesis

Evidence on the Efficient

Слайд 3The Efficient Market Hypothesis

The prices of securities in financial markets fully reflect

The Efficient Market Hypothesis

The prices of securities in financial markets fully reflect

Слайд 4

Current prices in a financial market will be set so that the

Current prices in a financial market will be set so that the

Слайд 5Rationale behind the hypothesis

Arbitrage, in which market participants (arbitrageurs) eliminate unexploited profit

Rationale behind the hypothesis

Arbitrage, in which market participants (arbitrageurs) eliminate unexploited profit

Слайд 6Stronger Version of the Efficient Market Hypothesis

Not only do scientists define an

Stronger Version of the Efficient Market Hypothesis

Not only do scientists define an

Слайд 7Implications of the above

In an eff. market one investment is as good

Implications of the above

In an eff. market one investment is as good

Слайд 8Evidence on the Efficient Market Hypothesis

Evidence in favour of Market Efficiency

Performance of

Evidence on the Efficient Market Hypothesis

Evidence in favour of Market Efficiency

Performance of

Слайд 9Evidence on the Efficient Market Hypothesis

Do stock prices reflect publically available information?

Favourable

Evidence on the Efficient Market Hypothesis

Do stock prices reflect publically available information?

Favourable

Слайд 10Evidence Against Market Efficiency

Small firm effect

Due to rebalancing of portfolios by institutional

Evidence Against Market Efficiency

Small firm effect

Due to rebalancing of portfolios by institutional

Слайд 11Evidence Against Market Efficiency

Excessive volatility

Fluctuations in stock prices may be much greater

Evidence Against Market Efficiency

Excessive volatility

Fluctuations in stock prices may be much greater

Слайд 12Evidence Against Market Efficiency

New information is not always immediately incorporated into stock

Evidence Against Market Efficiency

New information is not always immediately incorporated into stock

Слайд 13Overview of the Evidence on the EMH

How valuable are publishable reports by

Overview of the Evidence on the EMH

How valuable are publishable reports by

Слайд 14Overview of the Evidence on the EMH

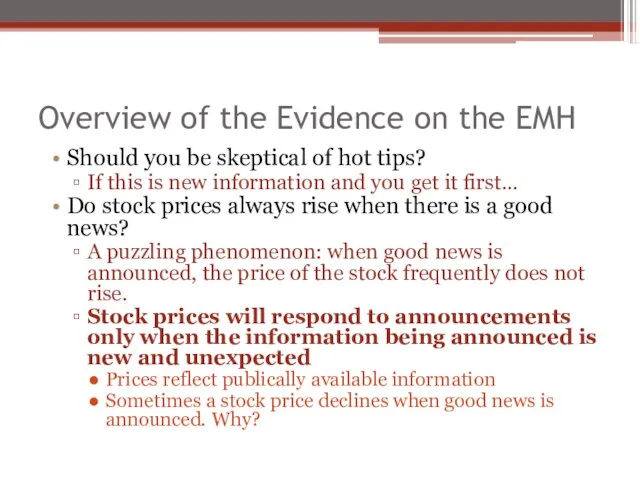

Should you be skeptical of hot

Overview of the Evidence on the EMH

Should you be skeptical of hot

Слайд 15Overview of the Evidence on the EMH

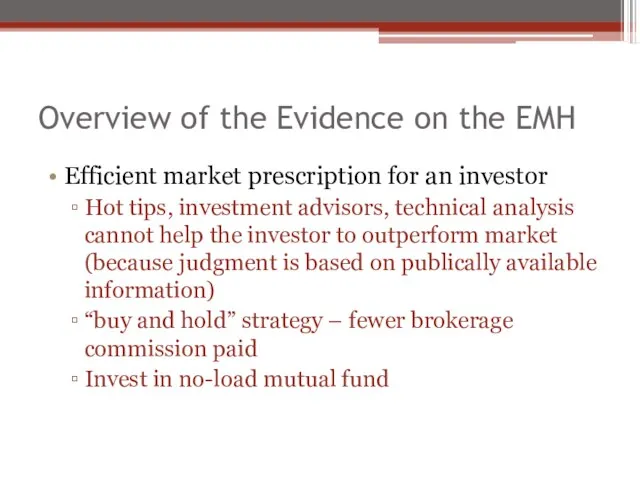

Efficient market prescription for an investor

Hot

Overview of the Evidence on the EMH

Efficient market prescription for an investor

Hot

Исторические типы культуры

Исторические типы культуры Бизнес план Кролиководческое хозяйство

Бизнес план Кролиководческое хозяйство  Ставропольское культурологическое общество

Ставропольское культурологическое общество Оценочный лист

Оценочный лист Волшебная строчка

Волшебная строчка Культурологический подход к преподаванию курса ОПК

Культурологический подход к преподаванию курса ОПК «Цветы» - это замечательное слово на планете

«Цветы» - это замечательное слово на планете A monopoly is a market envir onment where there is only one provider of a certain economic good or service

A monopoly is a market envir onment where there is only one provider of a certain economic good or service Машины для выполнения ветеринарносанитарных работ на фермах и комплексах

Машины для выполнения ветеринарносанитарных работ на фермах и комплексах Современные исследовательские университеты

Современные исследовательские университеты Презентация без названия

Презентация без названия Институт Пищевых Производств

Институт Пищевых Производств 20141104_vodyanoy_par

20141104_vodyanoy_par Мировая практика применения индекса цитирования при проведении и оценке научных исследованийчасть 2

Мировая практика применения индекса цитирования при проведении и оценке научных исследованийчасть 2 Государственная (итоговая) аттестация в 9 классе по русскому языку

Государственная (итоговая) аттестация в 9 классе по русскому языку Реакция якоря синхронных машин

Реакция якоря синхронных машин ЭКОНОМИЧЕСКИЙ КАЛЕЙДОСКОП

ЭКОНОМИЧЕСКИЙ КАЛЕЙДОСКОП Международные исследования качества образования (PISA) как фактор развития компетенции педагога

Международные исследования качества образования (PISA) как фактор развития компетенции педагога Проект Б.А.Р.С

Проект Б.А.Р.С Специальное обучение по охране труда работников АО Группа Илим в г. Братске. Общие вопросы охраны труда

Специальное обучение по охране труда работников АО Группа Илим в г. Братске. Общие вопросы охраны труда Данные о деятельности крупнейших компаний США. Семинар 16

Данные о деятельности крупнейших компаний США. Семинар 16 Северное Возрождение III часть

Северное Возрождение III часть Lux Express Group

Lux Express Group Анализ поведения затрат и взаимосвязи объема, себестоимости и прибыли

Анализ поведения затрат и взаимосвязи объема, себестоимости и прибыли За здоровый образ жизни

За здоровый образ жизни Специальность: управление, эксплуатация и обслуживание многоквартирного дома

Специальность: управление, эксплуатация и обслуживание многоквартирного дома Денежная реформа Елены Глинской

Денежная реформа Елены Глинской Литературное чтение 3 класс

Литературное чтение 3 класс