- Transfer prices

Содержание

- 2. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Significance About 50

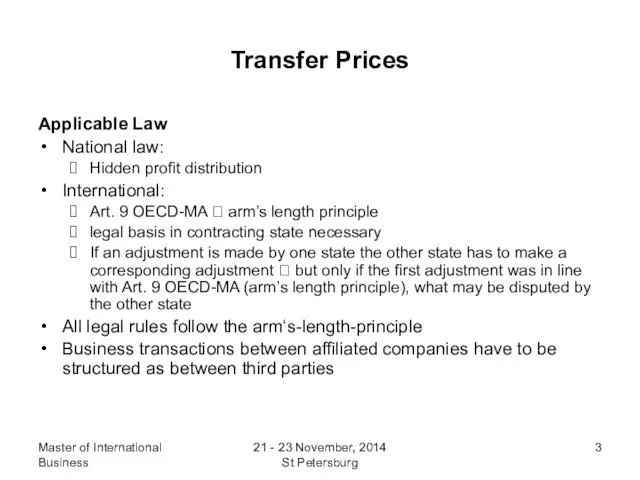

- 3. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Applicable Law National

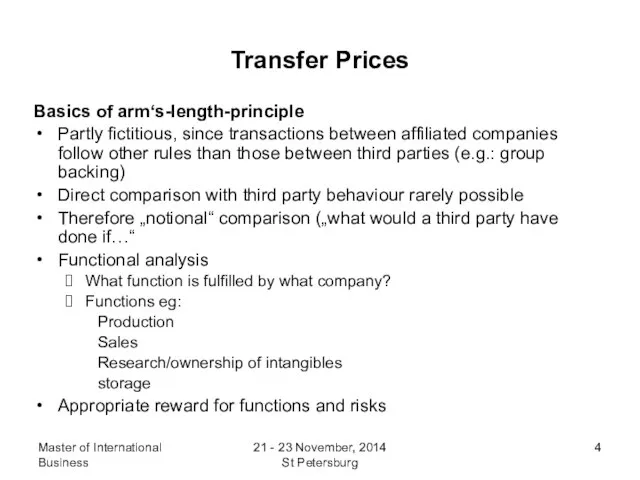

- 4. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Basics of arm‘s-length-principle

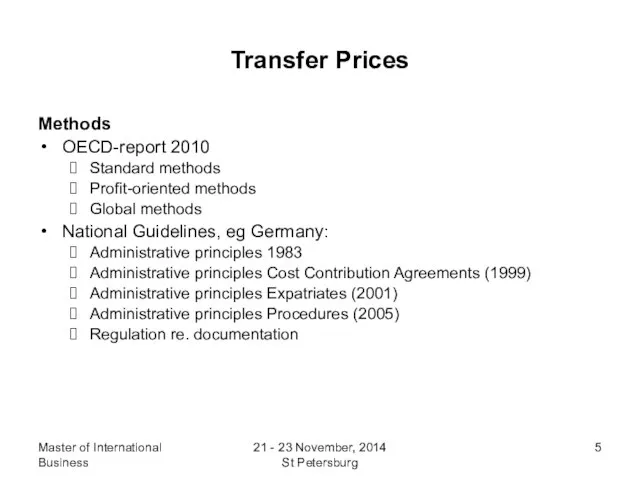

- 5. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Methods OECD-report 2010

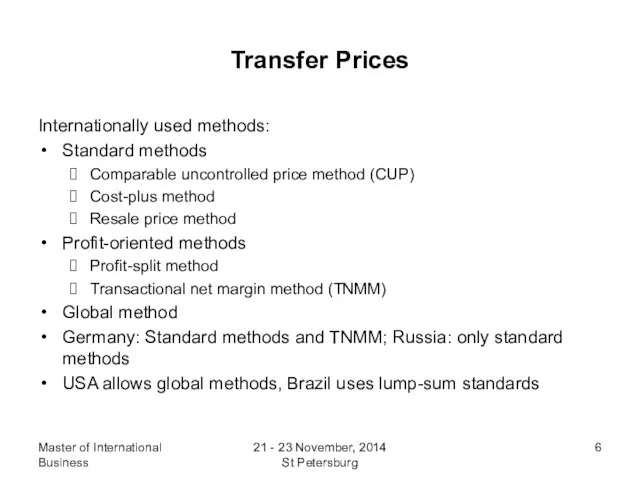

- 6. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Internationally used methods:

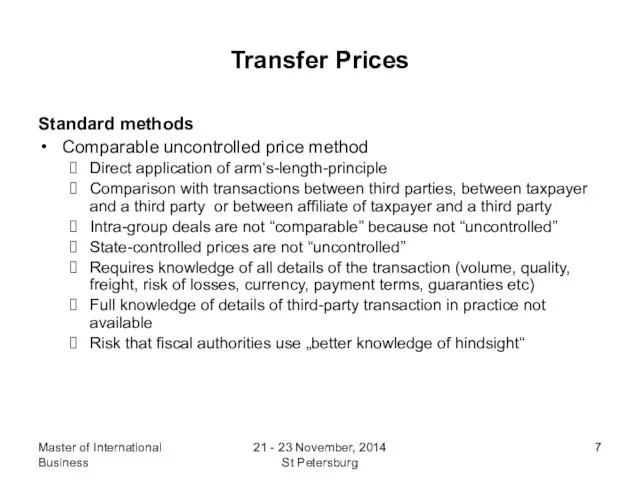

- 7. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Standard methods Comparable

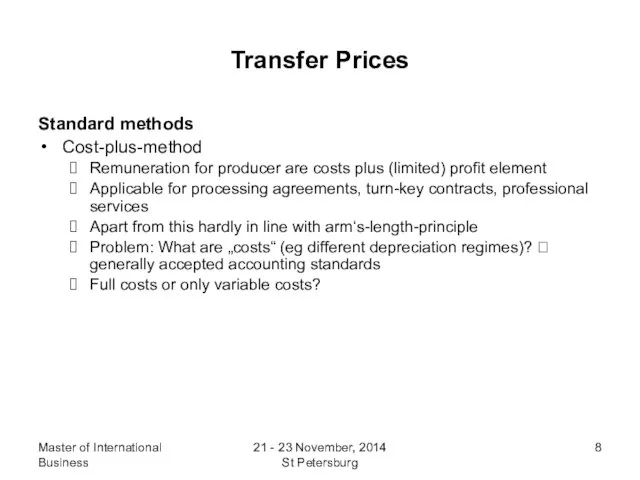

- 8. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Standard methods Cost-plus-method

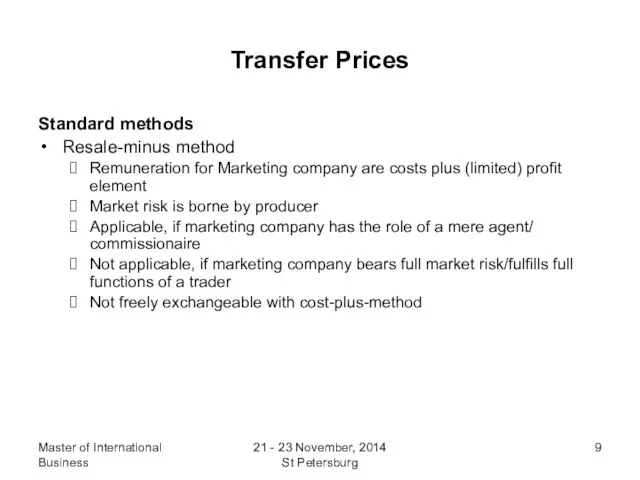

- 9. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Standard methods Resale-minus

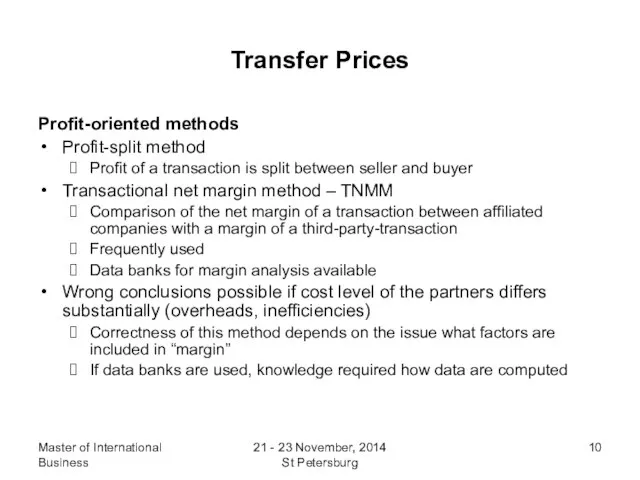

- 10. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Profit-oriented methods Profit-split

- 11. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Global methods Total

- 12. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Price range Special

- 13. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Transfer of goods

- 14. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Services Comparable prices

- 15. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Control- and Coordination

- 16. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Intangible assets OECD-report

- 17. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Financing Market interests

- 18. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Documentation Internationally widely

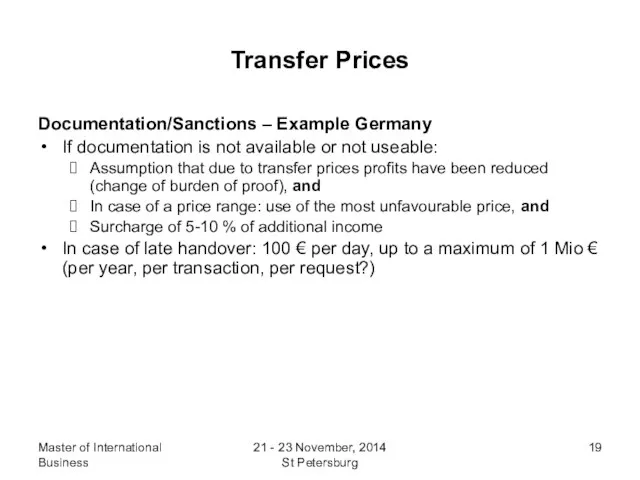

- 19. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Documentation/Sanctions – Example

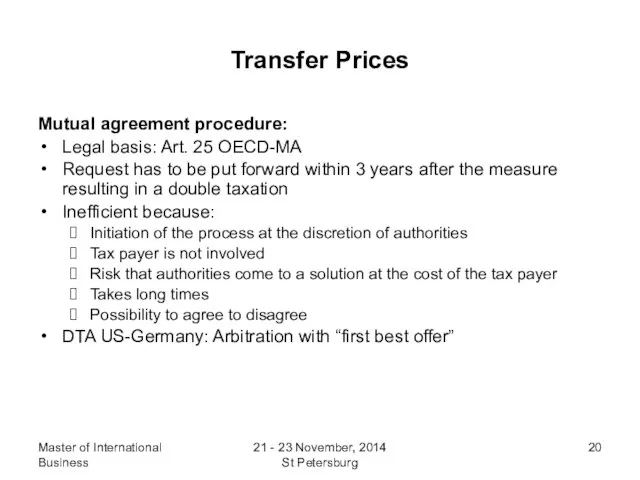

- 20. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Mutual agreement procedure:

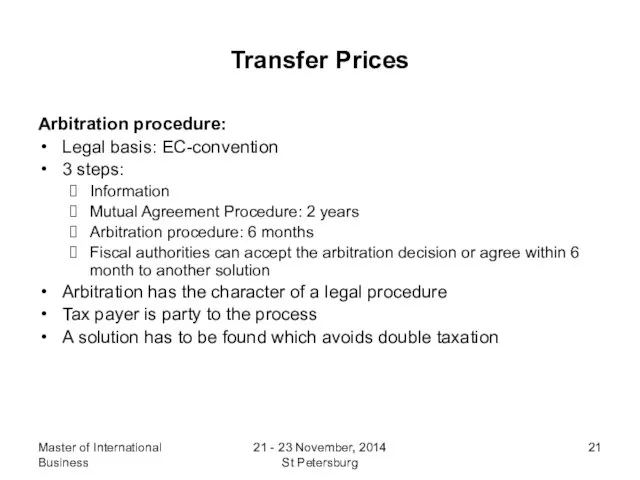

- 21. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Arbitration procedure: Legal

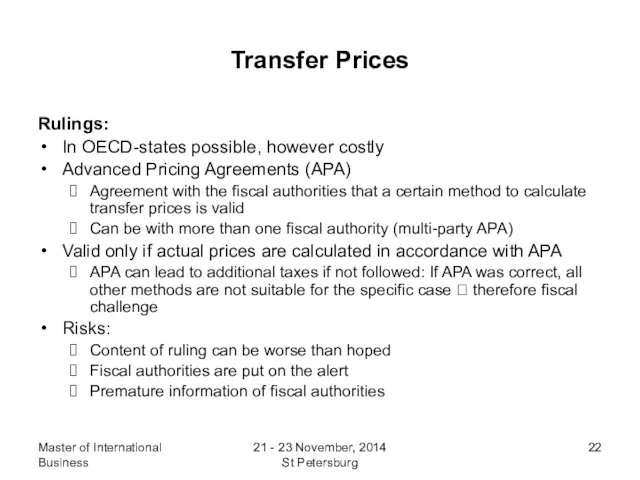

- 22. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Rulings: In OECD-states

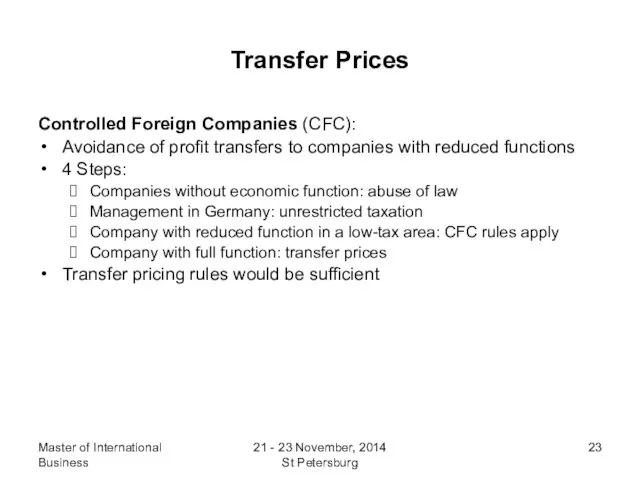

- 23. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices Controlled Foreign Companies

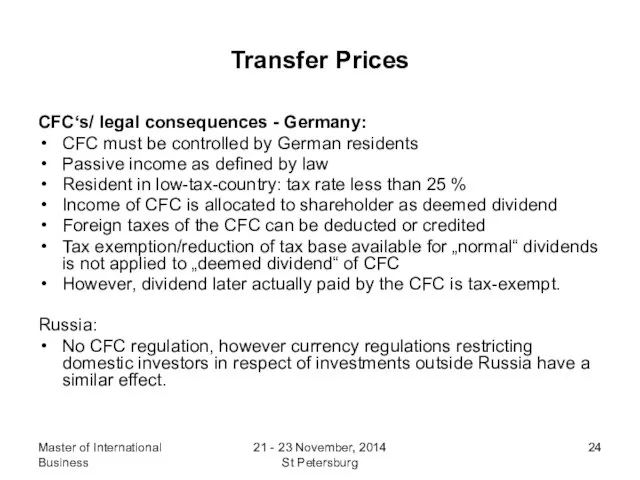

- 24. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices CFC‘s/ legal consequences

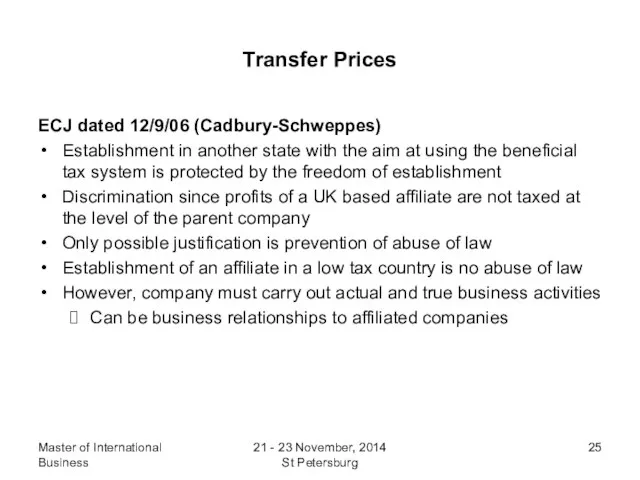

- 25. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices ECJ dated 12/9/06

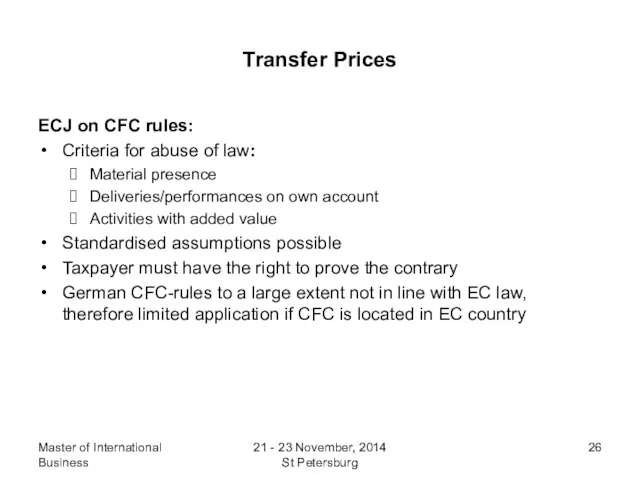

- 26. Master of International Business 21 - 23 November, 2014 St Petersburg Transfer Prices ECJ on CFC

- 28. Скачать презентацию

Слайд 2Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Significance

About 50

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Significance

About 50

Слайд 3Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Applicable Law

National

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Applicable Law

National

Слайд 4Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Basics of

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Basics of

Слайд 5Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Methods

OECD-report 2010

Standard

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Methods

OECD-report 2010

Standard

Слайд 6Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Internationally used

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Internationally used

Слайд 7Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Standard methods

Comparable

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Standard methods

Comparable

Слайд 8Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Standard methods

Cost-plus-method

Remuneration

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Standard methods

Cost-plus-method

Remuneration

Слайд 9Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Standard methods

Resale-minus

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Standard methods

Resale-minus

Слайд 10Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Profit-oriented methods

Profit-split

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Profit-oriented methods

Profit-split

Слайд 11Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Global methods

Total

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Global methods

Total

Слайд 12Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Price range

Special

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Price range

Special

Слайд 13Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Transfer of

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Transfer of

Слайд 14Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Services

Comparable prices

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Services

Comparable prices

Слайд 15Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

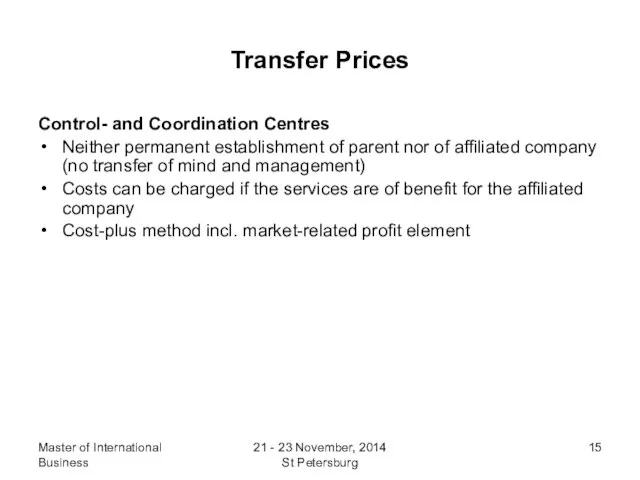

Control- and

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Control- and

Слайд 16Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

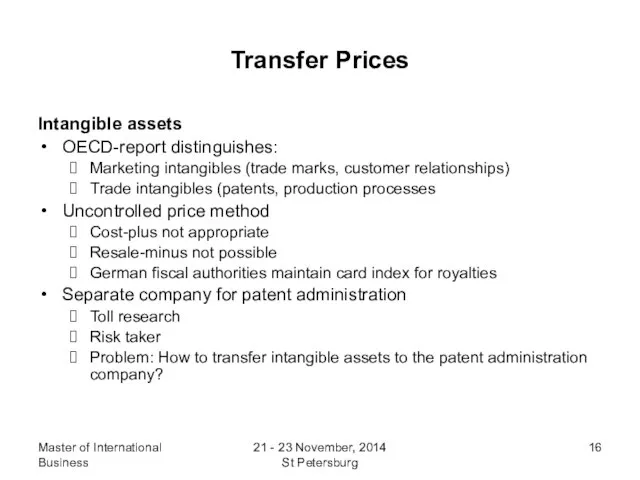

Intangible assets

OECD-report

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Intangible assets

OECD-report

Слайд 17Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

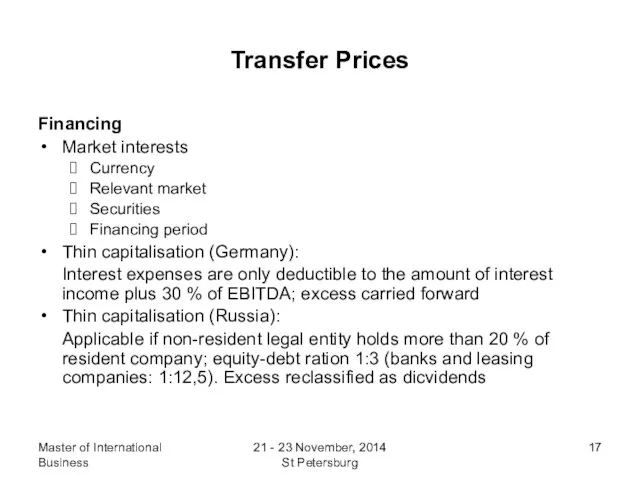

Financing

Market interests

Currency

Relevant

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Financing

Market interests

Currency

Relevant

Слайд 18Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

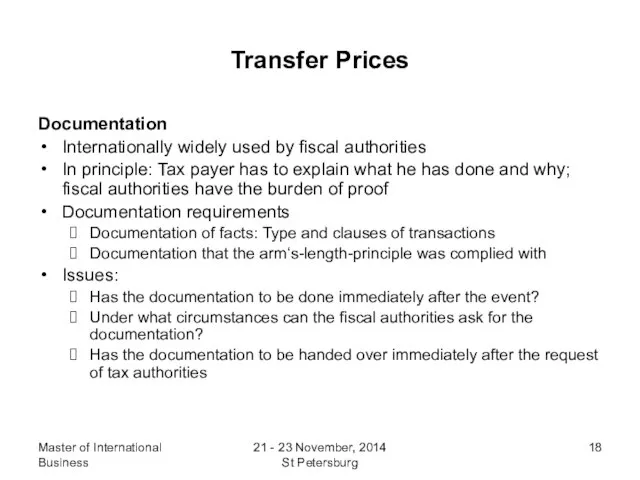

Documentation

Internationally widely

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Documentation

Internationally widely

Слайд 19Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Documentation/Sanctions –

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Documentation/Sanctions –

Слайд 20Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Mutual agreement

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Mutual agreement

Слайд 21Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Arbitration procedure:

Legal

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Arbitration procedure:

Legal

Слайд 22Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Rulings:

In OECD-states

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Rulings:

In OECD-states

Слайд 23Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Controlled Foreign

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

Controlled Foreign

Слайд 24Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

CFC‘s/ legal

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

CFC‘s/ legal

Слайд 25Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

ECJ dated

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

ECJ dated

Слайд 26Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

ECJ on

Master of International Business

21 - 23 November, 2014 St Petersburg

Transfer Prices

ECJ on

Основные виды организационных структур

Основные виды организационных структур ПРОГРАММА профилактики детского электротравматизма ОАО «Кубаньэнерго» Тематический урок «Основы электробезопасности» (для у

ПРОГРАММА профилактики детского электротравматизма ОАО «Кубаньэнерго» Тематический урок «Основы электробезопасности» (для у Брендинг в индустрии моды

Брендинг в индустрии моды Профориентация: новые форматы, ГАУ ДПО СОИРО

Профориентация: новые форматы, ГАУ ДПО СОИРО Традиционный бурятский мужской костюм

Традиционный бурятский мужской костюм Добор опоздавших на регистрацию пассажиров

Добор опоздавших на регистрацию пассажиров ФСКН Молодёжи

ФСКН Молодёжи Рамы переменного сечения

Рамы переменного сечения 568120

568120 Добро пожаловать в ВГПУ!

Добро пожаловать в ВГПУ! Управление коллективом исполнителей

Управление коллективом исполнителей Интерьер, который мы создаем. Дизайн. Моделирование

Интерьер, который мы создаем. Дизайн. Моделирование В гостях у Барбариков

В гостях у Барбариков Функции и структура ЛЭС. Оформление трассы

Функции и структура ЛЭС. Оформление трассы Сборы с носителей информации и оборудования

Сборы с носителей информации и оборудования «1С:Документооборот 8»

«1С:Документооборот 8» Вопросы проверки и перепроверки экзаменационных работ в условиях формирования независимой оценки качества образования

Вопросы проверки и перепроверки экзаменационных работ в условиях формирования независимой оценки качества образования Творчество Евгения Рачёва

Творчество Евгения Рачёва Презентация_Касимов

Презентация_Касимов Бесстрашный рыцарь неба

Бесстрашный рыцарь неба энн

энн Инновационные приоритеты в высокотехнологичной области Дмитрий Конаш, Региональный Директор Intel в странах СНГ

Инновационные приоритеты в высокотехнологичной области Дмитрий Конаш, Региональный Директор Intel в странах СНГ Символы России. Государственный флаг

Символы России. Государственный флаг Презентация на тему ЛАТВИЯ

Презентация на тему ЛАТВИЯ Новые люди

Новые люди Горы мира

Горы мира Photoshop. Конкурс. Supermen - GGG

Photoshop. Конкурс. Supermen - GGG Презентация

Презентация