- Macroeconomics 5

Содержание

- 2. What are business cycles? Perhaps, you know something from the introductory level… The business cycles occur

- 3. Phases of business cycles In other words, Business Cycles are alternating periods of economic expansion and

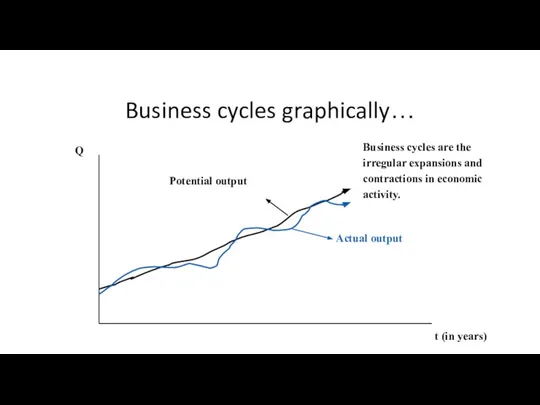

- 4. Business cycles graphically… Potential output Actual output Business cycles are the irregular expansions and contractions in

- 5. Business cycles and unemployment dynamics Recessions cause the unemployment rate to increase. We should remember about

- 6. The most important recent recessions 1974/75: Oil price shock caused by OPEC. 1982/83: High real wages

- 7. How to explain business cycles? ?

- 8. The multiplier-accelerator model as the oldest formalized model of cycle Initial points The model is a

- 9. What is the accelerator? Firms need a given quantity of capital to produce the current level

- 10. About constancy of the capital-output ratio If we do not allow for productivity boosting technical change,

- 11. Example of the accelerator principle We assume that ν = 3. That is, it takes 3

- 12. Formalizing the model (Part 1) If the economy is in equilibrium, then output supplied (Y) is

- 13. Formalizing the model (Part 2) The consumption function is given by: We assume that investment in

- 14. Combining these equations, we will receive: To simplify, we ignore the constant To get a standardized

- 15. Some essential ideas Change in investment affects output/income. Change in output/income affects (with delay) investment. Higher

- 16. Some conclusions (derived from the fundamental mathematical principles) There will be cyclical fluctuations in the time

- 17. Explosive oscillations B > 1 and A2 > 4B

- 18. Limitations of the multiplier-accelerator model This model is based on a crude theory of investment. There

- 19. New Keynesian approach New Keynesian economists (Mankiw, Stiglitz, Akerlof and others) believe that short-run fluctuations in

- 20. Top reasons for sticky prices – Results from surveys of managers (in the U.S.) (Mankiw, 2007)

- 21. The Real Business Cycle model All prices are flexible, even in short run: thus, money is

- 22. Intertemporal substitution of labor In the RBC model, workers are willing to reallocate labor over time

- 23. The mechanism of cycles in the RBC model In the RBC model, productivity shocks cause fluctuations

- 24. Are prices/wages flexible? The RBC model assumes that wages and prices are completely flexible, so markets

- 25. The financial fragility hypothesis (aka the financial instability hypothesis) Financial fragility hypothesis – developed by Hyman

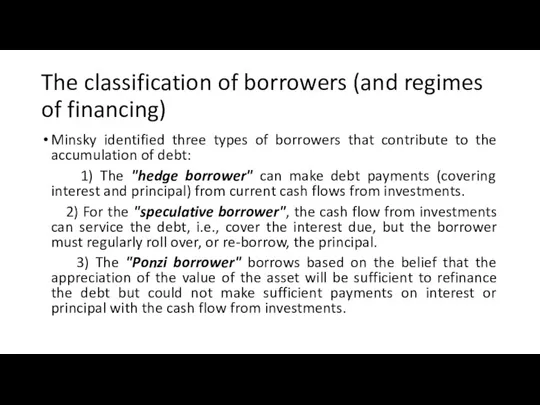

- 26. The classification of borrowers (and regimes of financing) Minsky identified three types of borrowers that contribute

- 27. Reasons for the name “Ponzi finance” or “Ponzi regime” Named after Charles Ponzi (1882-1949), an Italian

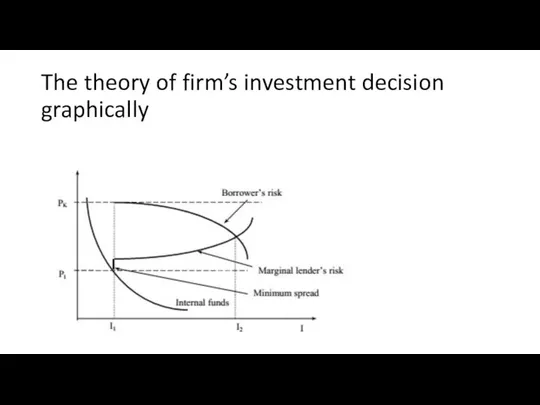

- 28. The theory of firm’s investment decision graphically

- 29. Some explanations I is investment PK is the demand price of investment (willingness to pay some

- 30. More explanations As business expansion takes place, all relevant curves shift to the right. Both total

- 31. The business expansion based on the accumulation of financial fragility graphically

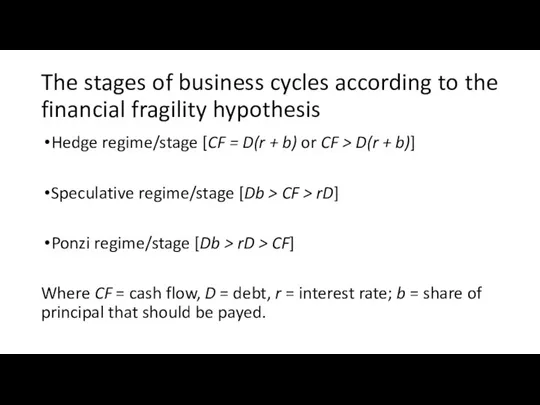

- 32. The stages of business cycles according to the financial fragility hypothesis Hedge regime/stage [CF = D(r

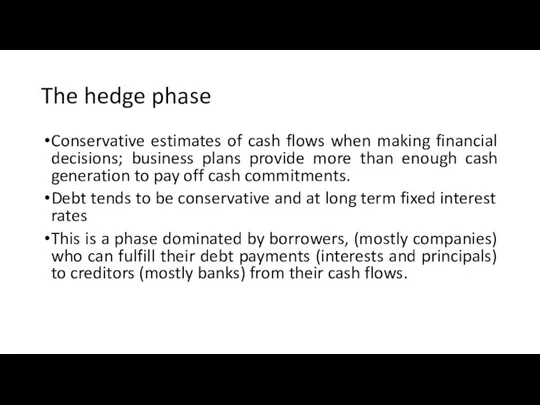

- 33. The hedge phase Conservative estimates of cash flows when making financial decisions; business plans provide more

- 34. The speculative phase Estimates of cash flows are more aggressive - expected cash inflows provide just

- 35. The “Ponzi” stage Estimates of cash generation not expected to cover cash commitments. Debt is short

- 36. The Minsky moment and financial crisis If the use of Ponzi finance is general enough in

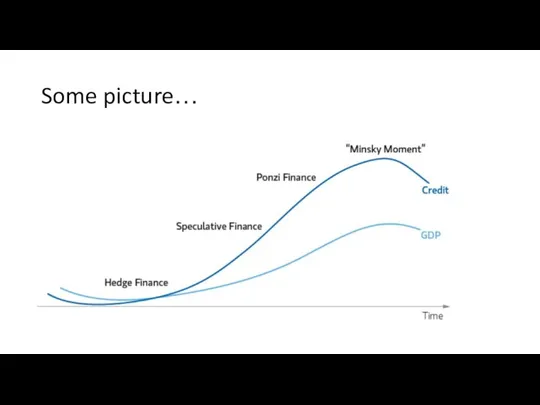

- 37. Some picture…

- 38. Quote from paper by Roncaglia (2013)

- 39. Minsky about the policy Minsky observes that the government intervention (proper fiscal policy measures) are necessary

- 40. More about the “proper” fiscal policy Fiscal policy may have a discretionary component, such as the

- 41. The fiscal policy may not be enough Governments alone may not be enough to stabilize the

- 42. Paradox of tranquility Government intervention is needed to stabilize the economy... If policies are successful, the

- 43. What about the monetary policy? Monetary policy can constrain undue expansion and inflation operates by way

- 44. More about the monetary policy The Central Bank will generally be taking up the role of

- 45. Results of the active government intervention for the U.S. economy (Tymoigne, 2008)

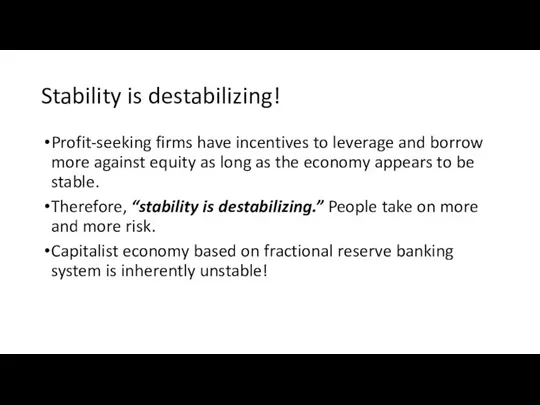

- 46. Stability is destabilizing! Profit-seeking firms have incentives to leverage and borrow more against equity as long

- 47. Let me give examples of three empirical studies of the financial fragility’s evolution in different countries

- 48. Empirical analysis of the Greek companies’ financing regimes on the base of the financial fragility hypothesis

- 49. Some details about this analysis and this index The ASE General Index includes 60 of the

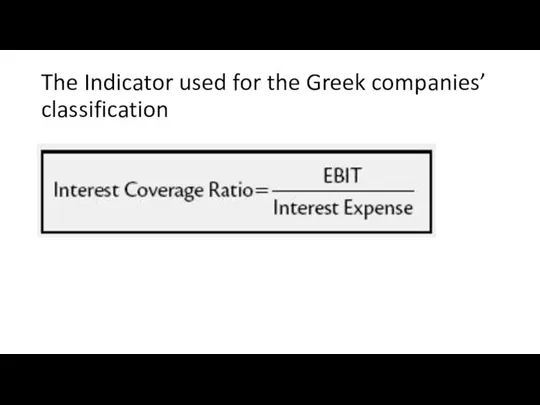

- 50. The Indicator used for the Greek companies’ classification

- 51. Explanation of the Indicator EBIT = earnings before interest and taxes Interest Coverage Ratio (ICR) =

- 52. The Principles of The Greek companies’ classification ICR>=3 treated as a financially “healthy” company or as

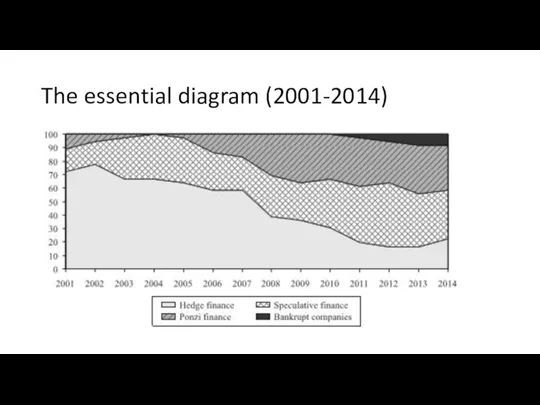

- 53. The dynamics of 36 Greek companies during the period in question After 2001 the number of

- 54. The essential diagram (2001-2014)

- 55. Some Conclusions Experience of the Greek economy is consistent with the FIH. In the 2000s, the

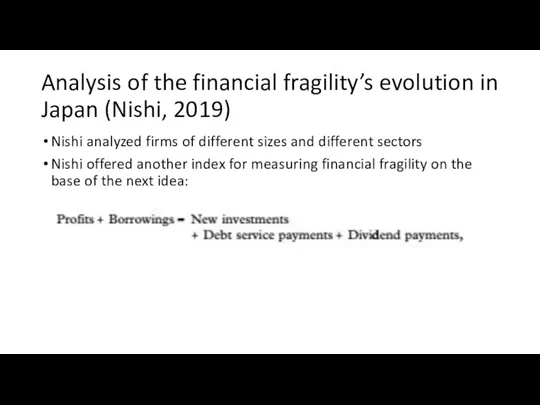

- 56. Analysis of the financial fragility’s evolution in Japan (Nishi, 2019) Nishi analyzed firms of different sizes

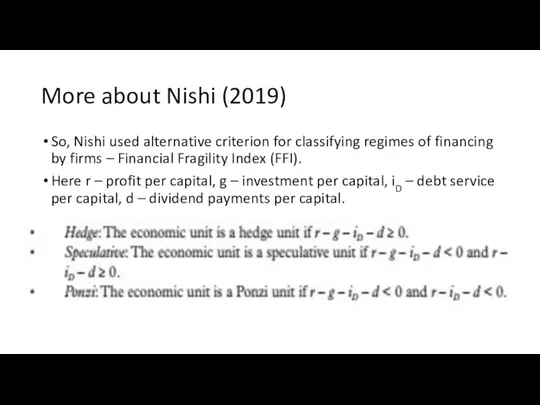

- 57. More about Nishi (2019) So, Nishi used alternative criterion for classifying regimes of financing by firms

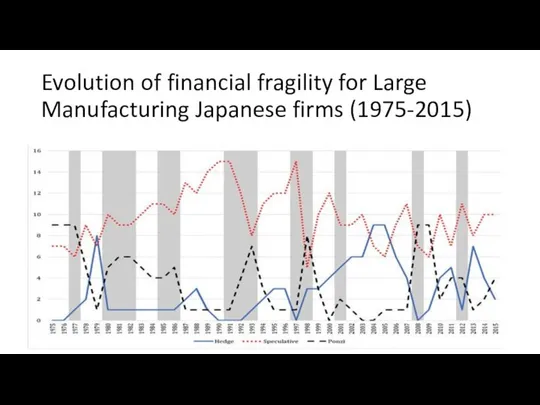

- 58. Evolution of financial fragility for Large Manufacturing Japanese firms (1975-2015)

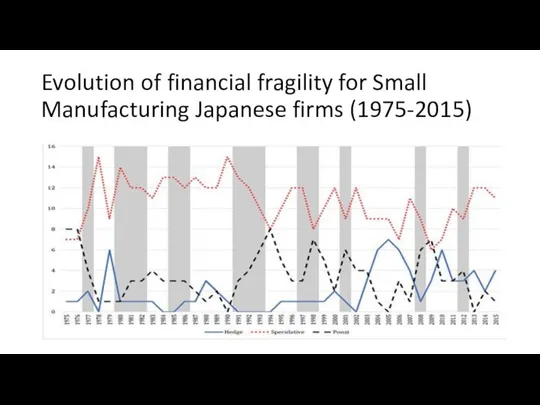

- 59. Evolution of financial fragility for Small Manufacturing Japanese firms (1975-2015)

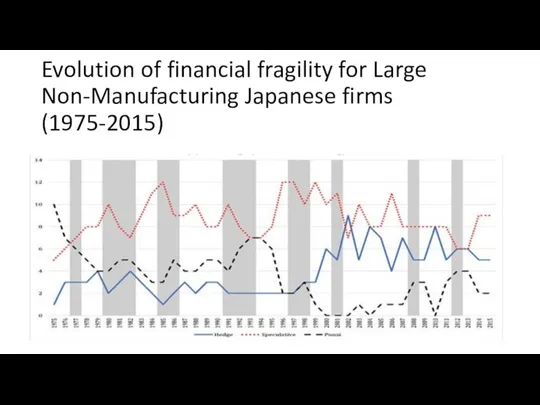

- 60. Evolution of financial fragility for Large Non-Manufacturing Japanese firms (1975-2015)

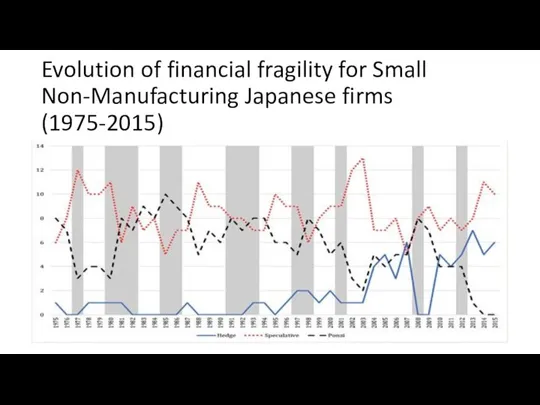

- 61. Evolution of financial fragility for Small Non-Manufacturing Japanese firms (1975-2015)

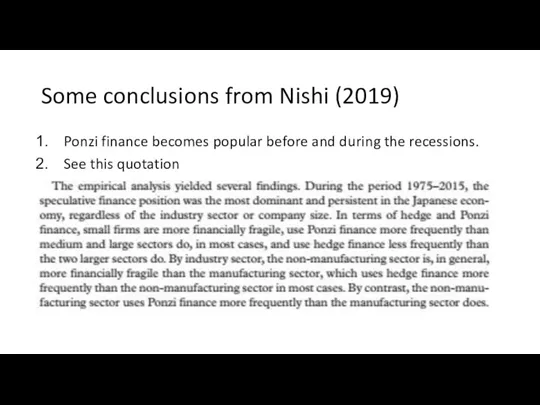

- 62. Some conclusions from Nishi (2019) Ponzi finance becomes popular before and during the recessions. See this

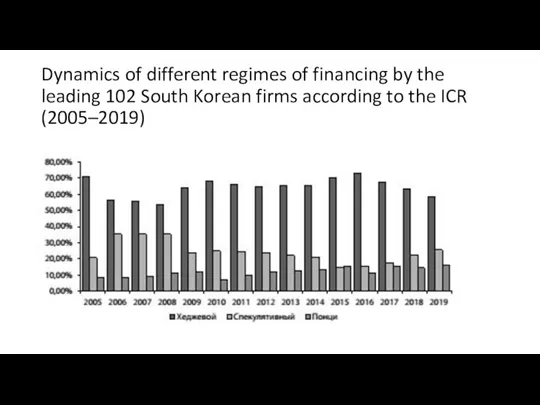

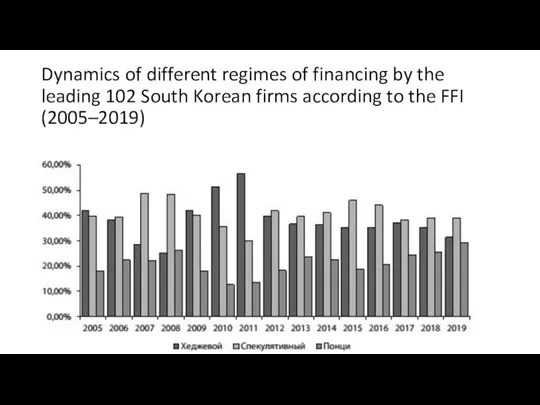

- 63. The example of latest research – for the South Korean private nonfinancial firms (Rozmainsky, Selitsky, 2021)

- 64. Dynamics of different regimes of financing by the leading 102 South Korean firms according to the

- 65. Dynamics of different regimes of financing by the leading 102 South Korean firms according to the

- 67. Скачать презентацию

Слайд 3Phases of business cycles

In other words, Business Cycles are alternating periods of

Phases of business cycles

In other words, Business Cycles are alternating periods of

Слайд 4Business cycles graphically…

Potential output

Actual output

Business cycles are the

irregular expansions and

contractions in economic

Business cycles graphically…

Potential output

Actual output

Business cycles are the

irregular expansions and

contractions in economic

Слайд 5Business cycles and unemployment dynamics

Recessions cause the unemployment rate to increase. We

Business cycles and unemployment dynamics

Recessions cause the unemployment rate to increase. We

Слайд 6The most important recent recessions

1974/75: Oil price shock caused by OPEC.

The most important recent recessions

1974/75: Oil price shock caused by OPEC.

Слайд 7How to explain business cycles?

?

How to explain business cycles?

?

Слайд 8The multiplier-accelerator model as the oldest formalized model of cycle

Initial points

The model

The multiplier-accelerator model as the oldest formalized model of cycle

Initial points

The model

Слайд 9What is the accelerator?

Firms need a given quantity of capital to produce

What is the accelerator?

Firms need a given quantity of capital to produce

Слайд 10About constancy of the capital-output ratio

If we do not allow for productivity

About constancy of the capital-output ratio

If we do not allow for productivity

Слайд 11Example of the accelerator principle

We assume that ν = 3. That is,

Example of the accelerator principle

We assume that ν = 3. That is,

Слайд 12Formalizing the model (Part 1)

If the economy is in equilibrium,

then output

Formalizing the model (Part 1)

If the economy is in equilibrium,

then output

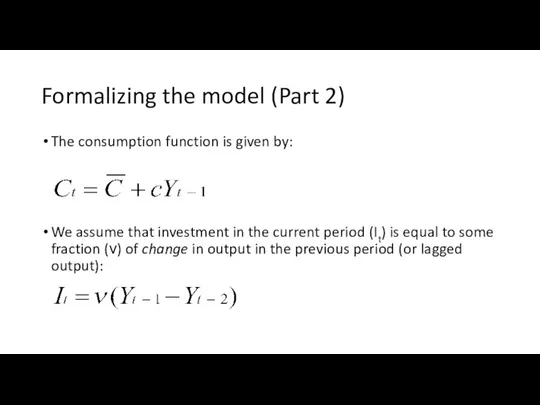

Слайд 13Formalizing the model (Part 2)

The consumption function is given by:

We assume that

Formalizing the model (Part 2)

The consumption function is given by:

We assume that

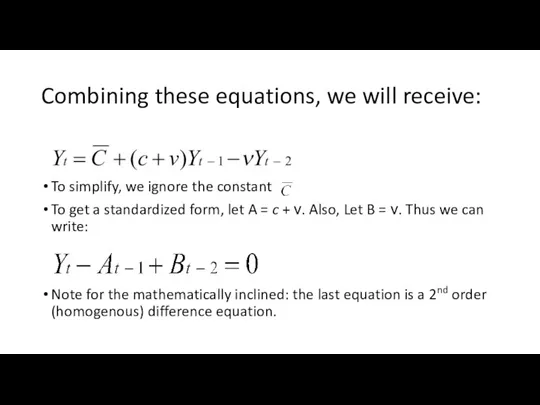

Слайд 14Combining these equations, we will receive:

To simplify, we ignore the constant

To

Combining these equations, we will receive:

To simplify, we ignore the constant

To

Слайд 15Some essential ideas

Change in investment affects output/income.

Change in output/income affects (with delay)

Some essential ideas

Change in investment affects output/income.

Change in output/income affects (with delay)

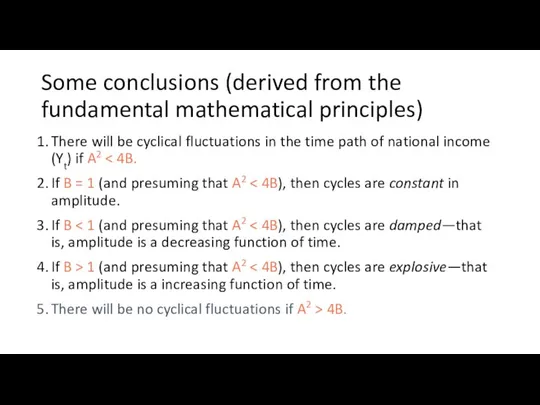

Слайд 16Some conclusions (derived from the fundamental mathematical principles)

There will be cyclical fluctuations

Some conclusions (derived from the fundamental mathematical principles)

There will be cyclical fluctuations

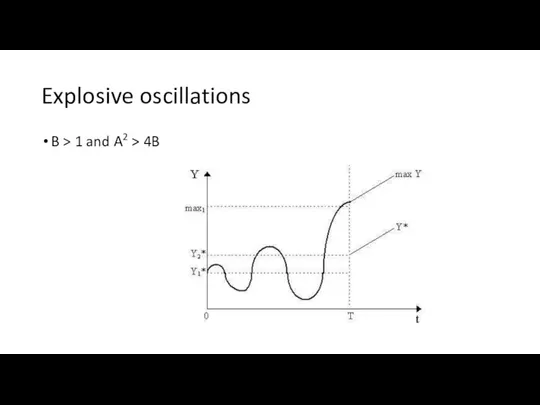

Слайд 17Explosive oscillations

B > 1 and A2 > 4B

Explosive oscillations

B > 1 and A2 > 4B

Слайд 18Limitations of the multiplier-accelerator model

This model is based on a crude theory

Limitations of the multiplier-accelerator model

This model is based on a crude theory

Слайд 19New Keynesian approach

New Keynesian economists (Mankiw, Stiglitz, Akerlof and others) believe that

New Keynesian approach

New Keynesian economists (Mankiw, Stiglitz, Akerlof and others) believe that

Слайд 20Top reasons for sticky prices – Results from surveys of managers (in

Top reasons for sticky prices – Results from surveys of managers (in

Слайд 21The Real Business Cycle model

All prices are flexible, even in short run:

thus,

The Real Business Cycle model

All prices are flexible, even in short run:

thus,

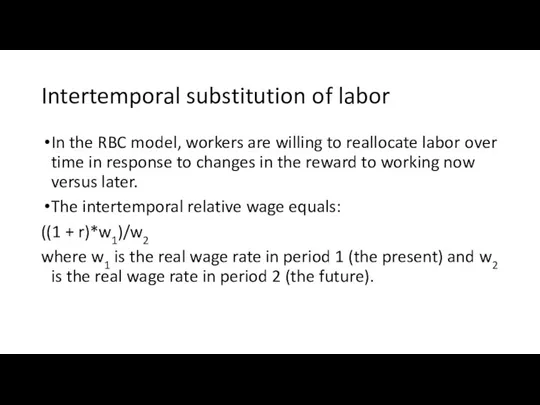

Слайд 22Intertemporal substitution of labor

In the RBC model, workers are willing to

Intertemporal substitution of labor

In the RBC model, workers are willing to

Слайд 23The mechanism of cycles in the RBC model

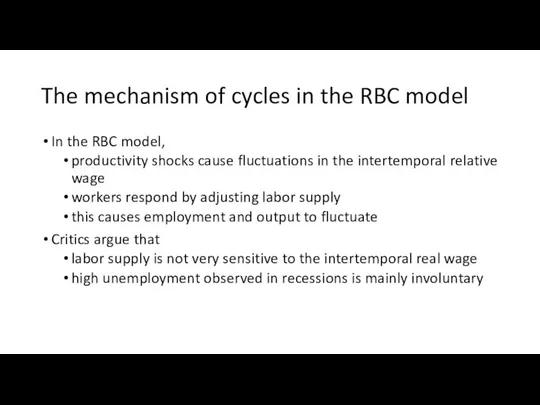

In the RBC model,

productivity

The mechanism of cycles in the RBC model

In the RBC model,

productivity

Слайд 24Are prices/wages flexible?

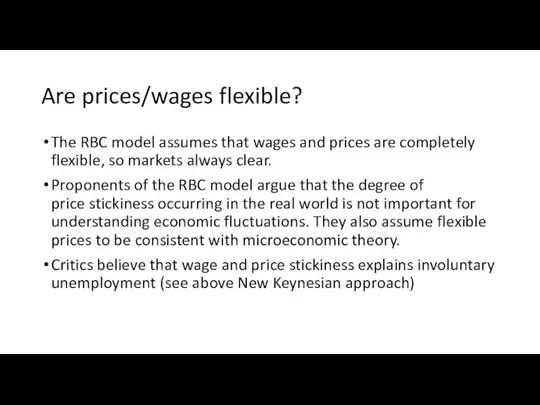

The RBC model assumes that wages and prices are completely

Are prices/wages flexible?

The RBC model assumes that wages and prices are completely

Слайд 25The financial fragility hypothesis (aka the financial instability hypothesis)

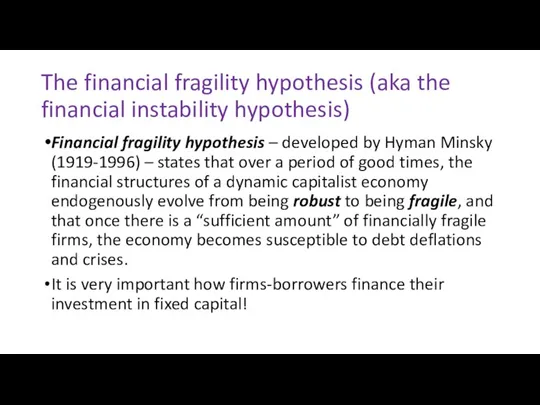

Financial fragility hypothesis –

The financial fragility hypothesis (aka the financial instability hypothesis)

Financial fragility hypothesis –

Слайд 26The classification of borrowers (and regimes of financing)

Minsky identified three types of

The classification of borrowers (and regimes of financing)

Minsky identified three types of

Слайд 27Reasons for the name “Ponzi finance” or “Ponzi regime”

Named after Charles Ponzi

Reasons for the name “Ponzi finance” or “Ponzi regime”

Named after Charles Ponzi

Слайд 28The theory of firm’s investment decision graphically

The theory of firm’s investment decision graphically

Слайд 29Some explanations

I is investment

PK is the demand price of investment (willingness

Some explanations

I is investment

PK is the demand price of investment (willingness

Слайд 30More explanations

As business expansion takes place, all relevant curves shift to the

More explanations

As business expansion takes place, all relevant curves shift to the

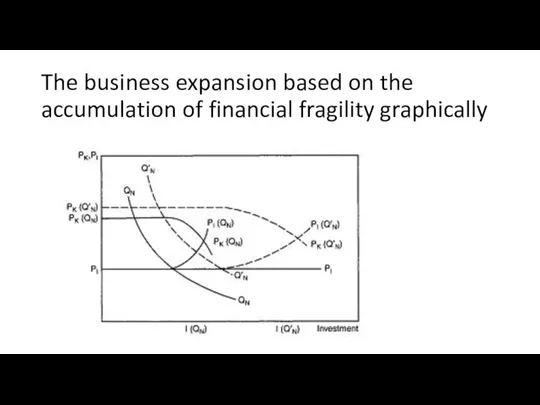

Слайд 31The business expansion based on the accumulation of financial fragility graphically

The business expansion based on the accumulation of financial fragility graphically

Слайд 32The stages of business cycles according to the financial fragility hypothesis

Hedge regime/stage

The stages of business cycles according to the financial fragility hypothesis

Hedge regime/stage

Слайд 33The hedge phase

Conservative estimates of cash flows when making financial decisions; business

The hedge phase

Conservative estimates of cash flows when making financial decisions; business

Слайд 34The speculative phase

Estimates of cash flows are more aggressive - expected cash

The speculative phase

Estimates of cash flows are more aggressive - expected cash

Слайд 35The “Ponzi” stage

Estimates of cash generation not expected to cover cash commitments.

The “Ponzi” stage

Estimates of cash generation not expected to cover cash commitments.

Слайд 36The Minsky moment and financial crisis

If the use of Ponzi finance is

The Minsky moment and financial crisis

If the use of Ponzi finance is

Слайд 37Some picture…

Some picture…

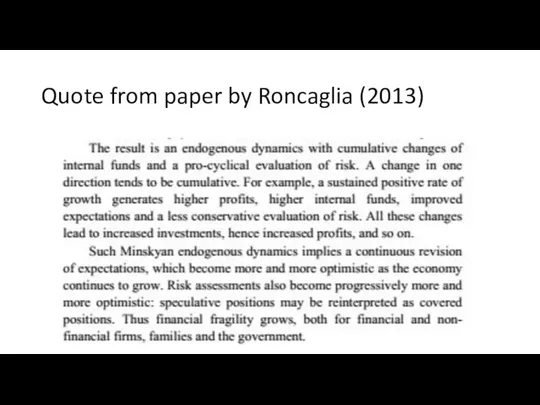

Слайд 38Quote from paper by Roncaglia (2013)

Quote from paper by Roncaglia (2013)

Слайд 39Minsky about the policy

Minsky observes that the government intervention (proper fiscal policy

Minsky about the policy

Minsky observes that the government intervention (proper fiscal policy

Слайд 40More about the “proper” fiscal policy

Fiscal policy may have a discretionary component,

More about the “proper” fiscal policy

Fiscal policy may have a discretionary component,

Слайд 41The fiscal policy may not be enough

Governments alone may not be enough

The fiscal policy may not be enough

Governments alone may not be enough

Слайд 42Paradox of tranquility

Government intervention is needed to stabilize the economy...

Paradox of tranquility

Government intervention is needed to stabilize the economy...

Слайд 43What about the monetary policy?

Monetary policy can constrain undue expansion and inflation

What about the monetary policy?

Monetary policy can constrain undue expansion and inflation

Слайд 44More about the monetary policy

The Central Bank will generally be taking up

More about the monetary policy

The Central Bank will generally be taking up

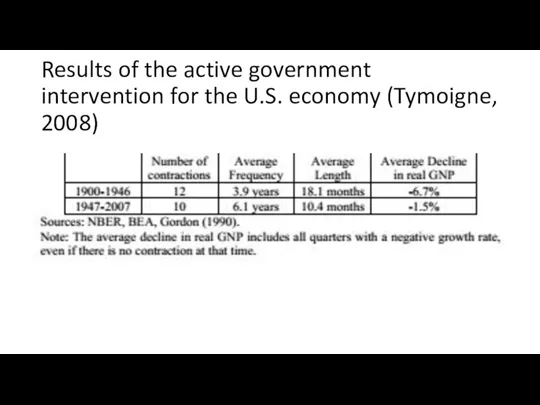

Слайд 45Results of the active government intervention for the U.S. economy (Tymoigne, 2008)

Results of the active government intervention for the U.S. economy (Tymoigne, 2008)

Слайд 46Stability is destabilizing!

Profit-seeking firms have incentives to leverage and borrow more against

Stability is destabilizing!

Profit-seeking firms have incentives to leverage and borrow more against

Слайд 47Let me give examples of three empirical studies of the financial fragility’s

Let me give examples of three empirical studies of the financial fragility’s

Слайд 48Empirical analysis of the Greek companies’ financing regimes on the base of

Empirical analysis of the Greek companies’ financing regimes on the base of

Слайд 49Some details about this analysis and this index

The ASE General Index includes

Some details about this analysis and this index

The ASE General Index includes

Слайд 50The Indicator used for the Greek companies’ classification

The Indicator used for the Greek companies’ classification

Слайд 51Explanation of the Indicator

EBIT = earnings before interest and taxes

Interest Coverage Ratio

Explanation of the Indicator

EBIT = earnings before interest and taxes

Interest Coverage Ratio

Слайд 52The Principles of The Greek companies’ classification

ICR>=3 treated as a financially “healthy”

The Principles of The Greek companies’ classification

ICR>=3 treated as a financially “healthy”

Слайд 53The dynamics of 36 Greek companies during the period in question

After

The dynamics of 36 Greek companies during the period in question

After

Слайд 54The essential diagram (2001-2014)

The essential diagram (2001-2014)

Слайд 55Some Conclusions

Experience of the Greek economy is consistent with the FIH.

In the

Some Conclusions

Experience of the Greek economy is consistent with the FIH.

In the

Слайд 56Analysis of the financial fragility’s evolution in Japan (Nishi, 2019)

Nishi analyzed firms

Analysis of the financial fragility’s evolution in Japan (Nishi, 2019)

Nishi analyzed firms

Слайд 57More about Nishi (2019)

So, Nishi used alternative criterion for classifying regimes of

More about Nishi (2019)

So, Nishi used alternative criterion for classifying regimes of

Слайд 58Evolution of financial fragility for Large Manufacturing Japanese firms (1975-2015)

Evolution of financial fragility for Large Manufacturing Japanese firms (1975-2015)

Слайд 59Evolution of financial fragility for Small Manufacturing Japanese firms (1975-2015)

Evolution of financial fragility for Small Manufacturing Japanese firms (1975-2015)

Слайд 60Evolution of financial fragility for Large Non-Manufacturing Japanese firms (1975-2015)

Evolution of financial fragility for Large Non-Manufacturing Japanese firms (1975-2015)

Слайд 61Evolution of financial fragility for Small Non-Manufacturing Japanese firms (1975-2015)

Evolution of financial fragility for Small Non-Manufacturing Japanese firms (1975-2015)

Слайд 62Some conclusions from Nishi (2019)

Ponzi finance becomes popular before and during the

Some conclusions from Nishi (2019)

Ponzi finance becomes popular before and during the

Слайд 63The example of latest research – for the South Korean private nonfinancial

The example of latest research – for the South Korean private nonfinancial

Слайд 64Dynamics of different regimes of financing by the leading 102 South Korean

Dynamics of different regimes of financing by the leading 102 South Korean

Слайд 65Dynamics of different regimes of financing by the leading 102 South Korean

Dynamics of different regimes of financing by the leading 102 South Korean

План расширения программы ОЗТ

План расширения программы ОЗТ Использование ИТ в проектировании предметно-пространственной среды Руководители: Шишко С.М. Баженова О.Д.

Использование ИТ в проектировании предметно-пространственной среды Руководители: Шишко С.М. Баженова О.Д. Sieben Fliegen blieben liegen Sieben Fliegen fliegen weg!

Sieben Fliegen blieben liegen Sieben Fliegen fliegen weg! Презентация на тему Виды информационных технологий

Презентация на тему Виды информационных технологий Центральная Россия

Центральная Россия  Подвиги в годы Виликой Отечественной Войны

Подвиги в годы Виликой Отечественной Войны Пасхальные традиции

Пасхальные традиции Бейджи. Раскладка

Бейджи. Раскладка ТЕХНИЧЕСКАЯ ДИАГНОСТИКА АВТОМОБИЛЕЙ

ТЕХНИЧЕСКАЯ ДИАГНОСТИКА АВТОМОБИЛЕЙ Память о Холокосте – путь к толерантности

Память о Холокосте – путь к толерантности Математика в природе

Математика в природе 7кл технические открытия

7кл технические открытия Коммуникативные универсальные учебные действия

Коммуникативные универсальные учебные действия Презентация на тему Учебный план основного общего образования как один из основных механизмов реализации основной образовательн

Презентация на тему Учебный план основного общего образования как один из основных механизмов реализации основной образовательн Итоги реализации КПМО в Шелаболихинском районе: эффекты,проблемы, перспективы

Итоги реализации КПМО в Шелаболихинском районе: эффекты,проблемы, перспективы Прощание с первым классом

Прощание с первым классом Антигитлеровская коалиция и итоги Второй мировой войны

Антигитлеровская коалиция и итоги Второй мировой войны Японская экономическая модель: содержание и направления развития

Японская экономическая модель: содержание и направления развития ОБУЧЕНИЕ И ПЕРЕОБУЧЕНИЕ В УСЛОВИЯХ КРИЗИСА

ОБУЧЕНИЕ И ПЕРЕОБУЧЕНИЕ В УСЛОВИЯХ КРИЗИСА Господь, любви Твоей свет сияет, Горит огнём среди тьмы и мрака, Иисус, свет мира, сияет над нами Истинным словом освобождая Сияй над

Господь, любви Твоей свет сияет, Горит огнём среди тьмы и мрака, Иисус, свет мира, сияет над нами Истинным словом освобождая Сияй над АНАЛИЗ МНОГОЗНАЧНОСТЕЙВ ЕСТЕСТВЕННО-ЯЗЫКОВЫХ ТЕКСТАХ

АНАЛИЗ МНОГОЗНАЧНОСТЕЙВ ЕСТЕСТВЕННО-ЯЗЫКОВЫХ ТЕКСТАХ Черная металлургия мира

Черная металлургия мира Концепция благоустройства города Полевской

Концепция благоустройства города Полевской Сечения

Сечения Запах веществ

Запах веществ Подводим итоги Фестиваля проектов - 2012

Подводим итоги Фестиваля проектов - 2012 Коммерческое предложение

Коммерческое предложение Новоюласинская средняя школа…

Новоюласинская средняя школа…