- Project Analysis and Evaluation

Содержание

- 2. EVALUATING ESTIMATES NPV> 0 PBP - as short as possible IRR - as high as possible

- 3. SCENARIO AND OTHER WHAT-IF ANALYSES Scenario analysis is the determination of what happens to NPV estimates

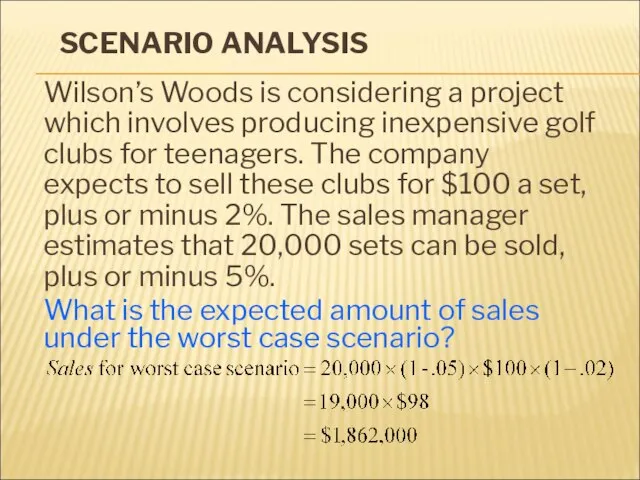

- 4. SCENARIO ANALYSIS Wilson’s Woods is considering a project which involves producing inexpensive golf clubs for teenagers.

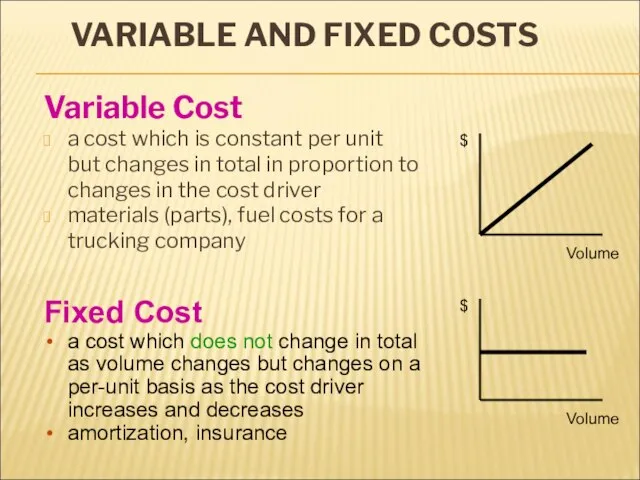

- 5. VARIABLE AND FIXED COSTS Variable Cost a cost which is constant per unit but changes in

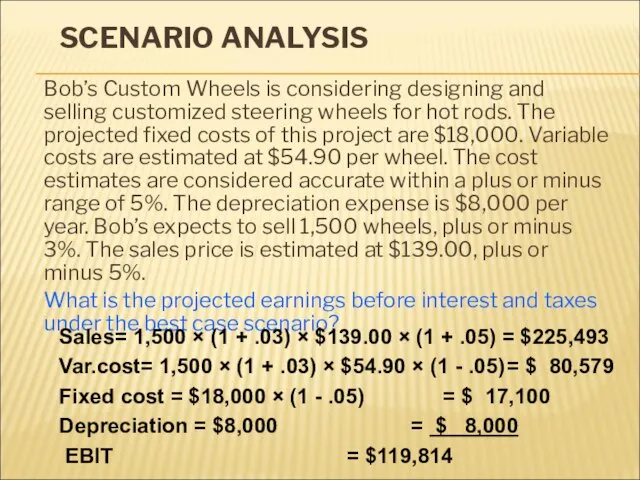

- 6. SCENARIO ANALYSIS Bob’s Custom Wheels is considering designing and selling customized steering wheels for hot rods.

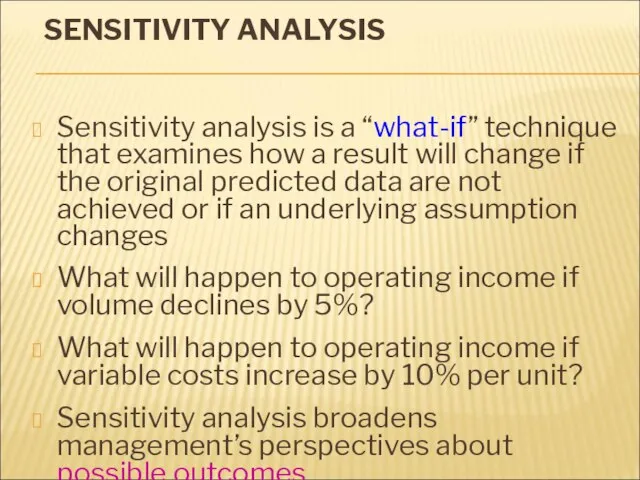

- 7. SENSITIVITY ANALYSIS Sensitivity analysis is a “what-if” technique that examines how a result will change if

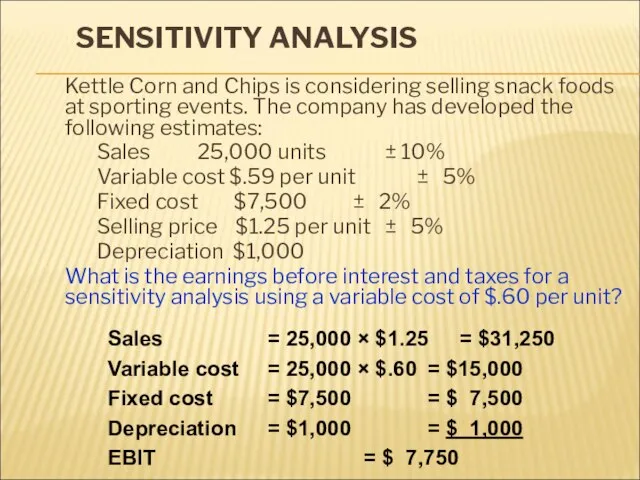

- 8. SENSITIVITY ANALYSIS Kettle Corn and Chips is considering selling snack foods at sporting events. The company

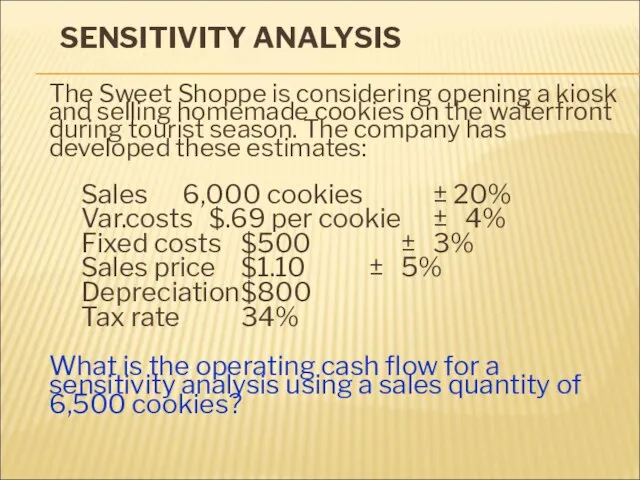

- 9. SENSITIVITY ANALYSIS The Sweet Shoppe is considering opening a kiosk and selling homemade cookies on the

- 10. SENSITIVITY ANALYSIS Sales = 6,500 × $1.10 = $7,150 Variable cost = 6,500 × $.69 =

- 11. TOTAL COST Sandwiches To Go sells 500 sandwiches per day. The company pays $1,200 a month

- 12. AVERAGE VS. MARGINAL COST Daisy’s Flowers raises and sells 36,000 bouquets of fresh cut flowers each

- 13. CONTRIBUTION MARGIN Contribution margin is equal to the difference between total revenue and total variable costs

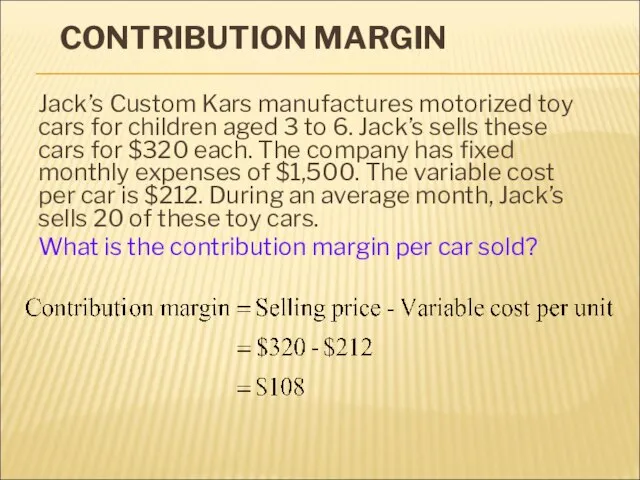

- 14. CONTRIBUTION MARGIN Jack’s Custom Kars manufactures motorized toy cars for children aged 3 to 6. Jack’s

- 15. COST-VOLUME-PROFIT (BREAKEVEN) GRAPH $10,000 $8,000 $6,000 $4,000 $2,000 $0 0 10 20 30 40 50 Units

- 16. BREAKEVEN POINT Quantity of output where total revenues equal total costs the point where operating income

- 17. BREAKEVEN POINTS General BE expression – relation between OCF (ignoring taxes) and quantity of output or

- 18. BREAKEVEN POINTS Financial BE – the sales level that results in a zero NPV Q= (FC+

- 19. ACCOUNTING BREAK-EVEN You are considering a new project. The projections include a sales price of $11.99,

- 20. ACCOUNTING BREAK-EVEN Katie’s Kites is considering a project with estimated fixed costs of $2,100, depreciation expense

- 21. CASH BREAK-EVEN Pretzels N’ More is considering adding a new retail outlet. Fixed costs are estimated

- 22. CASH BREAK-EVEN Tight-Wad Willsen is reviewing a proposal that has fixed costs of $12,500, depreciation expense

- 23. FINANCIAL BREAK-EVEN You are considering a new project that has an operating cash flow of $22,600

- 24. OPERATING LEVERAGE Operating leverage – the degree to which a firms or project relies on fixed

- 25. DEGREE OF OPERATING LEVERAGE Def: DOL is change in OCF relative to % change in quantity

- 26. DEGREE OF OPERATING LEVERAGE Martha’s Linens, Etc. has a 2.5 degree of operating leverage. Sales are

- 28. Скачать презентацию

Слайд 3SCENARIO AND OTHER WHAT-IF ANALYSES

Scenario analysis is the determination of what

SCENARIO AND OTHER WHAT-IF ANALYSES

Scenario analysis is the determination of what

Слайд 4SCENARIO ANALYSIS

Wilson’s Woods is considering a project which involves producing inexpensive golf

SCENARIO ANALYSIS

Wilson’s Woods is considering a project which involves producing inexpensive golf

Слайд 5VARIABLE AND FIXED COSTS

Variable Cost

a cost which is constant per unit but

VARIABLE AND FIXED COSTS

Variable Cost

a cost which is constant per unit but

Слайд 6SCENARIO ANALYSIS

Bob’s Custom Wheels is considering designing and selling customized steering wheels

SCENARIO ANALYSIS

Bob’s Custom Wheels is considering designing and selling customized steering wheels

Слайд 7SENSITIVITY ANALYSIS

Sensitivity analysis is a “what-if” technique that examines how a result

SENSITIVITY ANALYSIS

Sensitivity analysis is a “what-if” technique that examines how a result

Слайд 8SENSITIVITY ANALYSIS

Kettle Corn and Chips is considering selling snack foods at sporting

SENSITIVITY ANALYSIS

Kettle Corn and Chips is considering selling snack foods at sporting

Слайд 9SENSITIVITY ANALYSIS

The Sweet Shoppe is considering opening a kiosk and selling homemade

SENSITIVITY ANALYSIS

The Sweet Shoppe is considering opening a kiosk and selling homemade

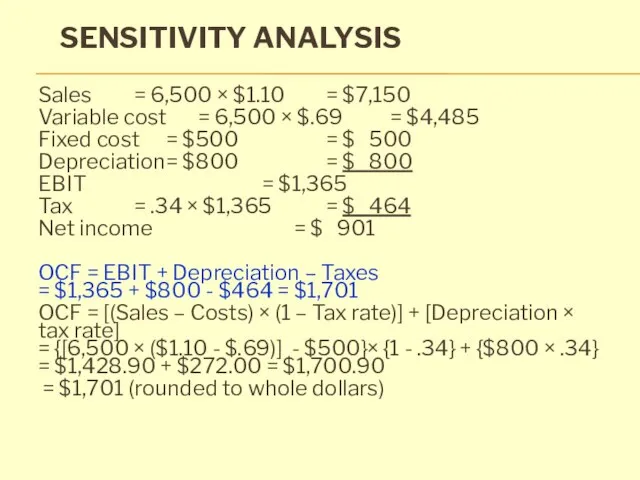

Слайд 10SENSITIVITY ANALYSIS

Sales = 6,500 × $1.10 = $7,150

Variable cost = 6,500 × $.69 = $4,485

Fixed cost =

SENSITIVITY ANALYSIS

Sales = 6,500 × $1.10 = $7,150

Variable cost = 6,500 × $.69 = $4,485

Fixed cost =

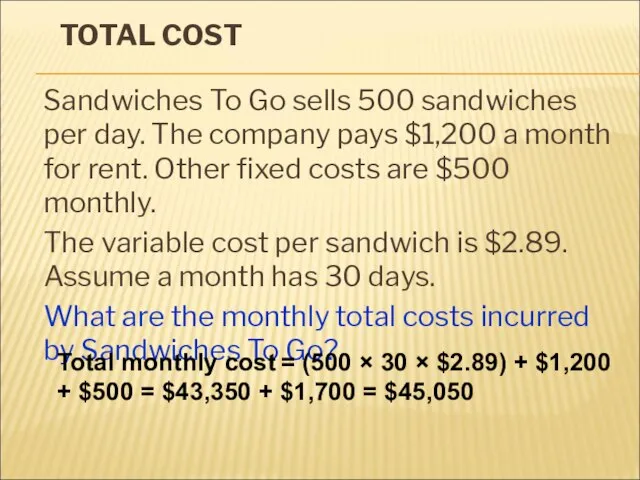

Слайд 11TOTAL COST

Sandwiches To Go sells 500 sandwiches per day. The company pays

TOTAL COST

Sandwiches To Go sells 500 sandwiches per day. The company pays

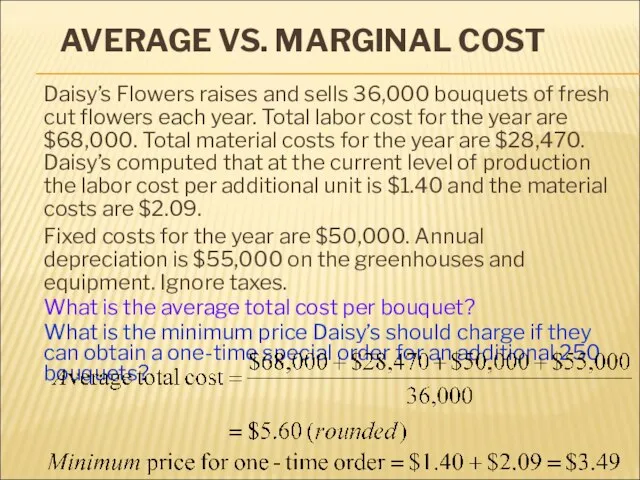

Слайд 12AVERAGE VS. MARGINAL COST

Daisy’s Flowers raises and sells 36,000 bouquets of fresh

AVERAGE VS. MARGINAL COST

Daisy’s Flowers raises and sells 36,000 bouquets of fresh

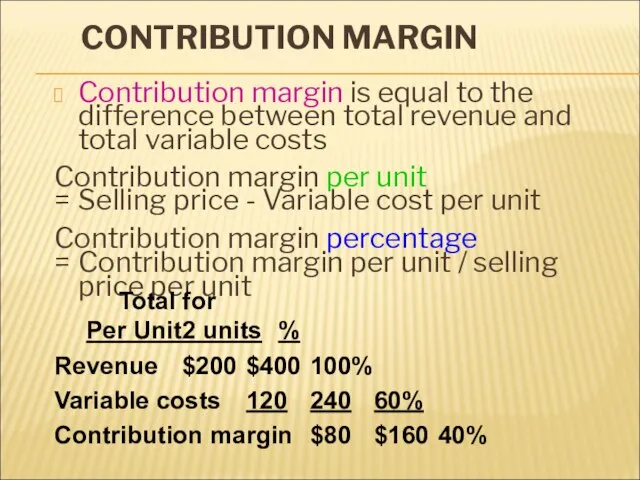

Слайд 13CONTRIBUTION MARGIN

Contribution margin is equal to the difference between total revenue and

CONTRIBUTION MARGIN

Contribution margin is equal to the difference between total revenue and

Слайд 14CONTRIBUTION MARGIN

Jack’s Custom Kars manufactures motorized toy cars for children aged 3

CONTRIBUTION MARGIN

Jack’s Custom Kars manufactures motorized toy cars for children aged 3

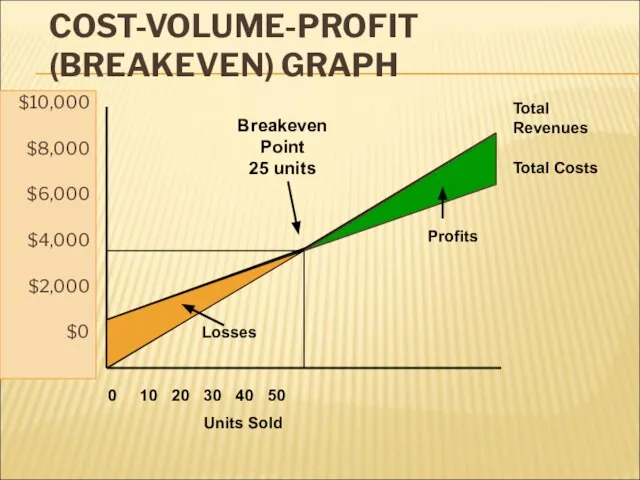

Слайд 15COST-VOLUME-PROFIT (BREAKEVEN) GRAPH

$10,000

$8,000

$6,000

$4,000

$2,000

$0

0 10 20 30 40 50

Units Sold

Total

Revenues

Total Costs

Breakeven

Point

25 units

Profits

Losses

COST-VOLUME-PROFIT (BREAKEVEN) GRAPH

$10,000

$8,000

$6,000

$4,000

$2,000

$0

0 10 20 30 40 50

Units Sold

Total

Revenues

Total Costs

Breakeven

Point

25 units

Profits

Losses

Слайд 16BREAKEVEN POINT

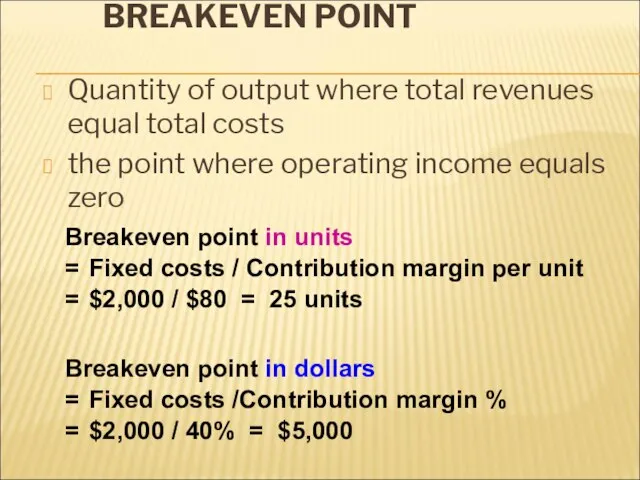

Quantity of output where total revenues equal total costs

the point where

BREAKEVEN POINT

Quantity of output where total revenues equal total costs

the point where

Слайд 17BREAKEVEN POINTS

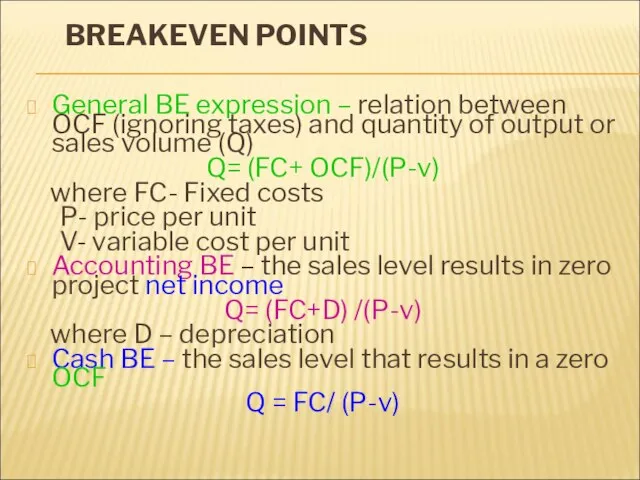

General BE expression – relation between OCF (ignoring taxes) and quantity

BREAKEVEN POINTS

General BE expression – relation between OCF (ignoring taxes) and quantity

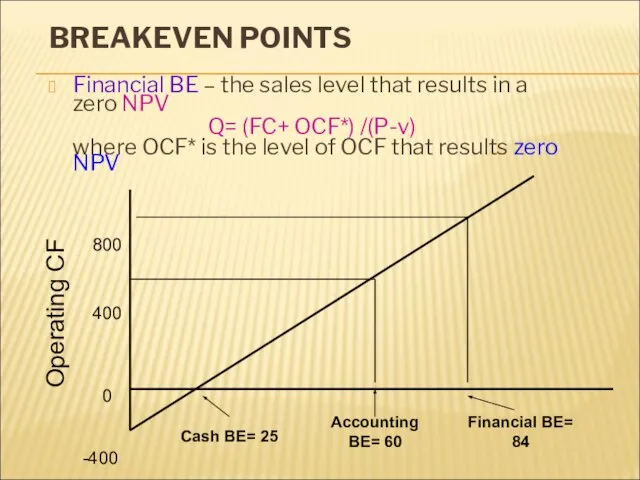

Слайд 18BREAKEVEN POINTS

Financial BE – the sales level that results in a zero

BREAKEVEN POINTS

Financial BE – the sales level that results in a zero

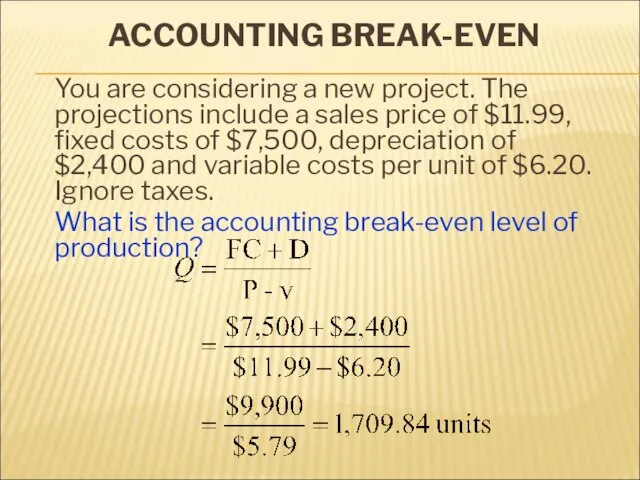

Слайд 19ACCOUNTING BREAK-EVEN

You are considering a new project. The projections include a sales

ACCOUNTING BREAK-EVEN

You are considering a new project. The projections include a sales

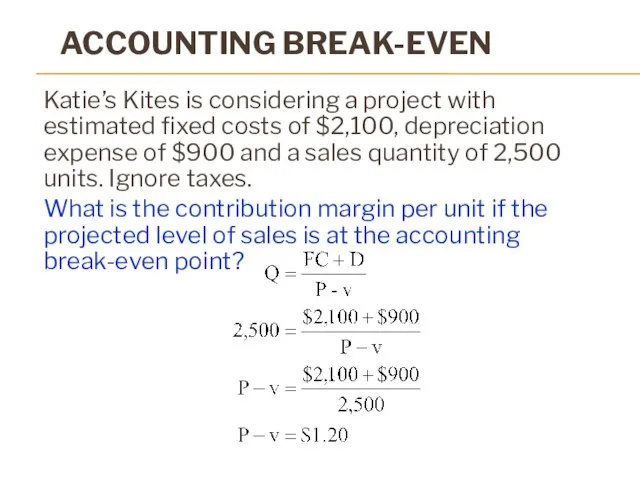

Слайд 20ACCOUNTING BREAK-EVEN

Katie’s Kites is considering a project with estimated fixed costs of

ACCOUNTING BREAK-EVEN

Katie’s Kites is considering a project with estimated fixed costs of

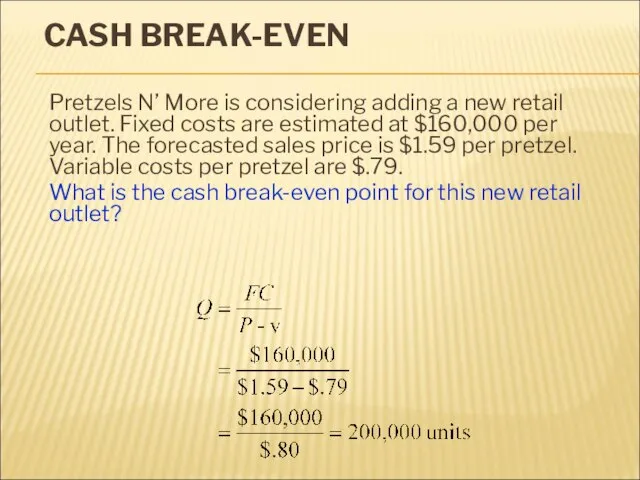

Слайд 21CASH BREAK-EVEN

Pretzels N’ More is considering adding a new retail outlet. Fixed

CASH BREAK-EVEN

Pretzels N’ More is considering adding a new retail outlet. Fixed

Слайд 22CASH BREAK-EVEN

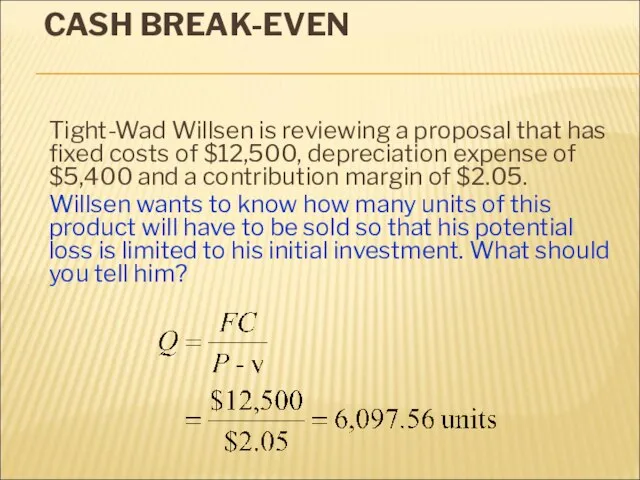

Tight-Wad Willsen is reviewing a proposal that has fixed costs of

CASH BREAK-EVEN

Tight-Wad Willsen is reviewing a proposal that has fixed costs of

Слайд 23 FINANCIAL BREAK-EVEN

You are considering a new project that has an operating

FINANCIAL BREAK-EVEN

You are considering a new project that has an operating

Слайд 24OPERATING LEVERAGE

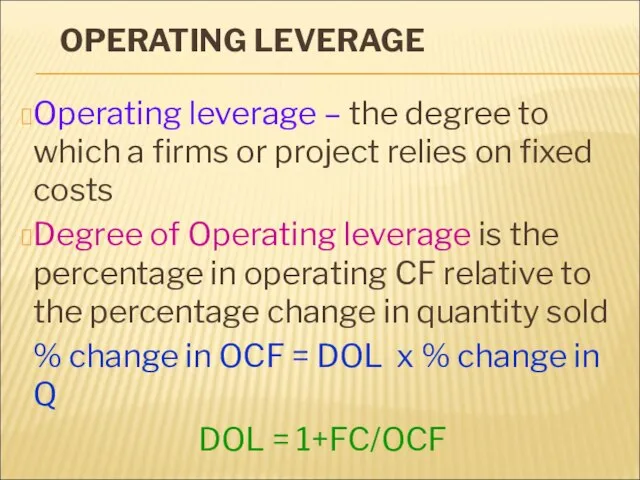

Operating leverage – the degree to which a firms or project

OPERATING LEVERAGE

Operating leverage – the degree to which a firms or project

Слайд 25DEGREE OF OPERATING LEVERAGE

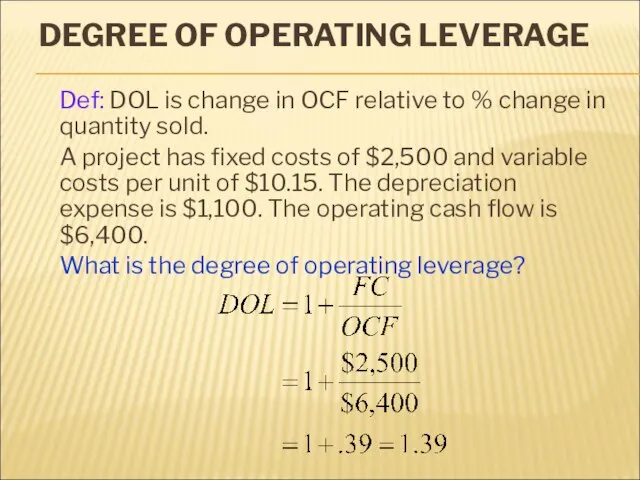

Def: DOL is change in OCF relative to %

DEGREE OF OPERATING LEVERAGE

Def: DOL is change in OCF relative to %

Слайд 26DEGREE OF OPERATING LEVERAGE

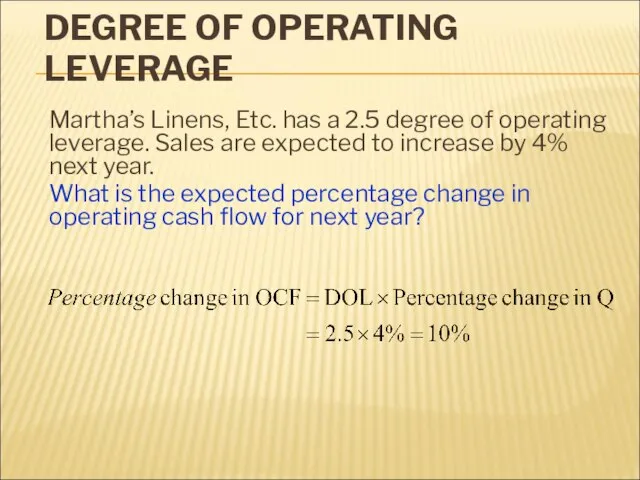

Martha’s Linens, Etc. has a 2.5 degree of operating

DEGREE OF OPERATING LEVERAGE

Martha’s Linens, Etc. has a 2.5 degree of operating

Основні і оборотні фонди залізничного тарнспорту. Лекція 7

Основні і оборотні фонди залізничного тарнспорту. Лекція 7 Педагогика лек 7 -2022

Педагогика лек 7 -2022 Информационное обеспечение системы обязательного медицинского страхования

Информационное обеспечение системы обязательного медицинского страхования Презентация на тему Основные понятия генетики

Презентация на тему Основные понятия генетики Азбука плавания

Азбука плавания Современные и перспективные технологии разработки прикладных систем

Современные и перспективные технологии разработки прикладных систем Профориентационная работа Профориентационная работа с учащимися.

Профориентационная работа Профориентационная работа с учащимися. Как возникло франкское государство

Как возникло франкское государство Презентация на тему 300 лет Нижегородской губернии

Презентация на тему 300 лет Нижегородской губернии  Презентация на тему Моя будущая профессия

Презентация на тему Моя будущая профессия  Мощные производители из наиболее развитых провинций - Цзянсу

Мощные производители из наиболее развитых провинций - Цзянсу Права человека

Права человека Презентация на тему Электроёмкость

Презентация на тему Электроёмкость KazakhParty-ға қош келдіңіз. Үйлену тойы

KazakhParty-ға қош келдіңіз. Үйлену тойы ДискретизацияСверткаДПФ

ДискретизацияСверткаДПФ Использование компьютерного тестирования на уроках английского языка

Использование компьютерного тестирования на уроках английского языка Микропроцессоры

Микропроцессоры Дети@Mail.Ru

Дети@Mail.Ru Печенье Oreo

Печенье Oreo Пути активизации устной речи на уроках английского языка в рамках коммуникативной методики обучения

Пути активизации устной речи на уроках английского языка в рамках коммуникативной методики обучения Загадки деда мороза

Загадки деда мороза Chanel- один из самых влиятельных французских домов моды

Chanel- один из самых влиятельных французских домов моды психология упр 2

психология упр 2 Регламент на автовыставку

Регламент на автовыставку Результаты учебной деятельности за 2010-2011 учебный год

Результаты учебной деятельности за 2010-2011 учебный год Экологические кризисы 9 класс

Экологические кризисы 9 класс Обеспечение безопасности детей при работе в Интернет

Обеспечение безопасности детей при работе в Интернет Управление бизнес-проектами в коммуникациях

Управление бизнес-проектами в коммуникациях