- The Time Value of Money

Содержание

- 2. Key Points Understanding The Timing of Returns Cash Flows Risk and Return Time Value of Money

- 3. Introduction You may have learned from your studies of economics that the goal of the business

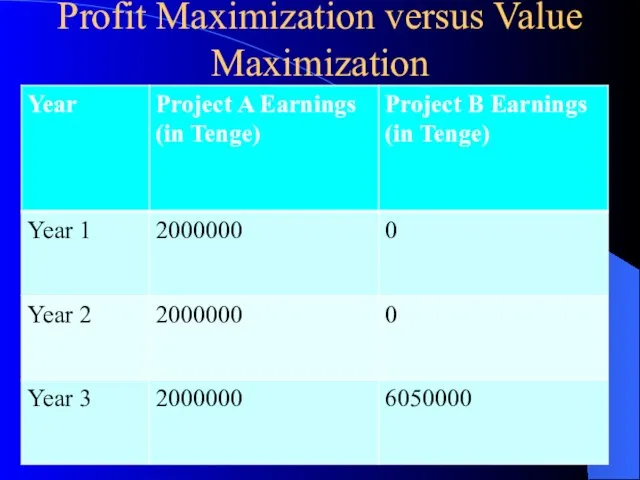

- 4. Profit Maximization versus Value Maximization

- 5. Profit Maximizing Versus Value Maximizing Profit maximization would dictate the choice of Project B, as it

- 6. Cash Flows Profits do not represent cash flows. Although profits may be used as the traditional

- 7. Risk The objective of profit maximization also ignores the concept of risk, which, for our purposes

- 8. Risk Clearly Project B, in this scenario, would be the higher risk investment and therefore its

- 9. Core Concepts of Financial Management In making financial decisions, the financial manager will be guided and

- 10. Core Concepts of FM We can now proceed to examine the core concepts of financial management,

- 11. Cash Flow ‘Cash generation is the foundation of creative value for shareholders’ (J Sainsbury Plc, Annual

- 12. Profit versus Cash Flow Profit is an accounting concept whereas cash is a financial management concept,

- 13. Profit versus Cash Flow Wild Rover Joinery is a small company which designs and manufactures interior

- 14. Profit versus Cash Flow Accounting perspective-If the costs figure includes the costs of manufacture (wages, materials,

- 15. Measuring Cash Flow A firm’s net cash flow is USUALLY calculated by deducting cash payments from

- 16. Measuring Cash Flow However, the important point is that depreciation is not a cash expense. For

- 17. Measuring Cash Flow This measurement of cash flow shows the discretionary cash remaining after making the

- 18. Measuring Cash Flow However it is measured or defined, cash flow generation is the true test

- 19. Cash Inflows and Outflows

- 20. Risk and Return The motivation for undertaking an investment decision is the expectation of gaining a

- 21. Risk and Return In the context of financial management by risk we mean the chance that

- 22. Risk and Return This allows the decision-maker to create probability weightings for a range of possible

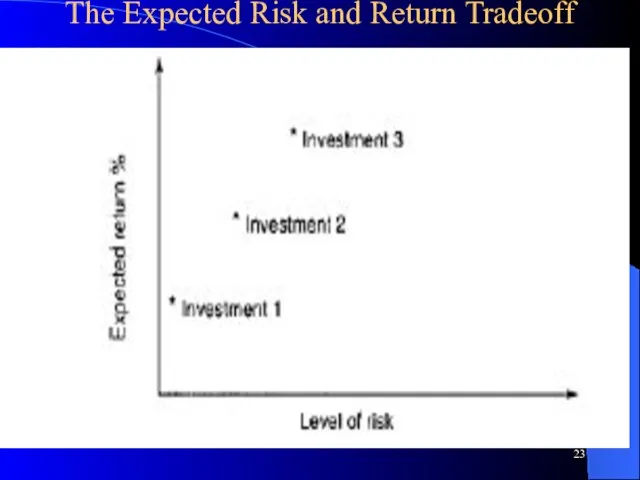

- 23. The Expected Risk and Return Tradeoff

- 24. Risk and Return The risk of investing in a bank or building society savings account (Investment

- 25. The investor’s propensity for risk-taking Figure shows, other things being equal, the positive relationship (correlation) between

- 26. The investor’s propensity for risk-taking Individuals and corporations are generally considered to be risk-averse, in the

- 27. Time Value of Money Cash flows which are to be received at some time in the

- 28. Time Value of Money Not only is the concept of measuring returns in terms of cash

- 29. The Time Value of Money Obviously, $1,000 today. Money received sooner rather than later allows one

- 30. INFLATION You may have wondered about the role inflation plays in the time value of money.

- 31. Why TIME? Observe that the concepts of future value and present value are inversely related. Over

- 32. How can one compare amounts in different time periods? One can adjust values from different time

- 33. Compound Interest When interest is paid on not only the principal amount invested, but also on

- 34. Future Value (Graphic) If you invested $2,000 today in an account that pays 6% interest, with

- 35. Future Value (Formula) FV1 = PV (1+i)n = $2,000 (1.06)2 = $2,247.20 FV = future value,

- 36. Future Value Example John wants to know how large his $5,000 deposit will become at an

- 37. Future Value Solution Calculator keystrokes: 1.08 2nd yx x 5000 = Calculation based on general formula:

- 38. Double Your Money!!! Quick! How long does it take to double $2,000 at a compound rate

- 39. The “Rule-of-72” Quick! How long does it take to double $2,000 at a compound rate of

- 40. Present Value Since FV = PV(1 + i)n. PV = FV / (1+i)n. Discounting is the

- 41. Present Value (Graphic) Assume that you need to have exactly $4,000 saved 10 years from now.

- 42. Present Value (Formula) PV0 = FV / (1+i)2 = $4,000 / (1.06)10 = $2,233.58 0 5

- 43. Present Value Example Joann needs to know how large of a deposit to make today so

- 44. Present Value Solution Calculation based on general formula: PV0 = FVn / (1+i)n PV0 = $2,500/(1.04)5

- 45. Finding “n” or “i” when one knows PV and FV(6/8.5) If one invests $2,000 today and

- 46. Frequency of Compounding General Formula: FVn = PV0(1 + [i/m])mn n: Number of Years m: Compounding

- 47. Frequency of Compounding Example Suppose you deposit $1,000 in an account that pays 12% interest, compounded

- 48. Solution based on formula: FV= PV (1 + i)n = 1,000(1.03)32 = 2,575.10 Calculator Keystrokes: 1.03

- 49. Annuities An annuity is a special cash flow pattern in which, as its name implies, a

- 50. Annuities

- 51. Annuities-Examples Example 8 —The future value of an annuity Anna would like to know how much

- 52. FV of an Annuities-Examples

- 53. FV of an Annuities-Examples Notice that since the first £1,000 is invested at the end of

- 54. FV of an Annuities-Examples For example, if you know that you will need £10,000 in eight

- 56. Скачать презентацию

Слайд 3Introduction

You may have learned from your studies of economics that the

Introduction

You may have learned from your studies of economics that the

Слайд 4Profit Maximization versus Value Maximization

Profit Maximization versus Value Maximization

Слайд 5Profit Maximizing Versus Value Maximizing

Profit maximization would dictate the choice of Project

Profit Maximizing Versus Value Maximizing

Profit maximization would dictate the choice of Project

Слайд 6Cash Flows

Profits do not represent cash flows. Although profits may be used

Cash Flows

Profits do not represent cash flows. Although profits may be used

Слайд 7Risk

The objective of profit maximization also ignores the concept of risk, which,

Risk

The objective of profit maximization also ignores the concept of risk, which,

Слайд 8Risk

Clearly Project B, in this scenario, would be the higher risk investment

Risk

Clearly Project B, in this scenario, would be the higher risk investment

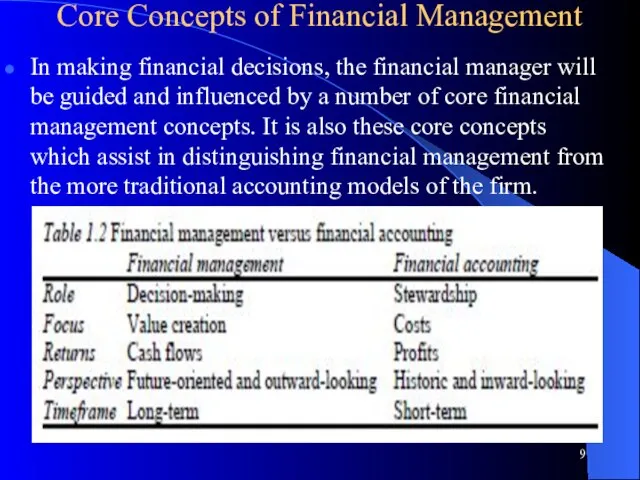

Слайд 9Core Concepts of Financial Management

In making financial decisions, the financial manager will

Core Concepts of Financial Management

In making financial decisions, the financial manager will

Слайд 10Core Concepts of FM

We can now proceed to examine the core concepts

Core Concepts of FM

We can now proceed to examine the core concepts

Слайд 11Cash Flow

‘Cash generation is the foundation of creative value for shareholders’ (J

Cash Flow

‘Cash generation is the foundation of creative value for shareholders’ (J

Слайд 12Profit versus Cash Flow

Profit is an accounting concept whereas cash is a

Profit versus Cash Flow

Profit is an accounting concept whereas cash is a

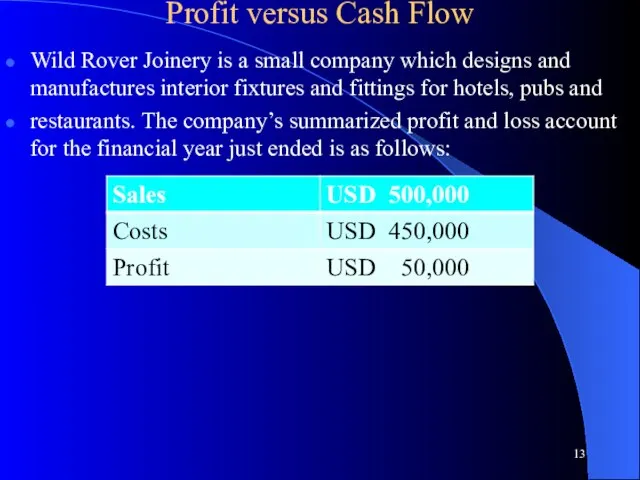

Слайд 13Profit versus Cash Flow

Wild Rover Joinery is a small company which designs

Profit versus Cash Flow

Wild Rover Joinery is a small company which designs

Слайд 14Profit versus Cash Flow

Accounting perspective-If the costs figure includes the costs of

Profit versus Cash Flow

Accounting perspective-If the costs figure includes the costs of

Слайд 15Measuring Cash Flow

A firm’s net cash flow is USUALLY calculated by deducting

Measuring Cash Flow

A firm’s net cash flow is USUALLY calculated by deducting

Слайд 16Measuring Cash Flow

However, the important point is that depreciation is not a

Measuring Cash Flow

However, the important point is that depreciation is not a

Слайд 17Measuring Cash Flow

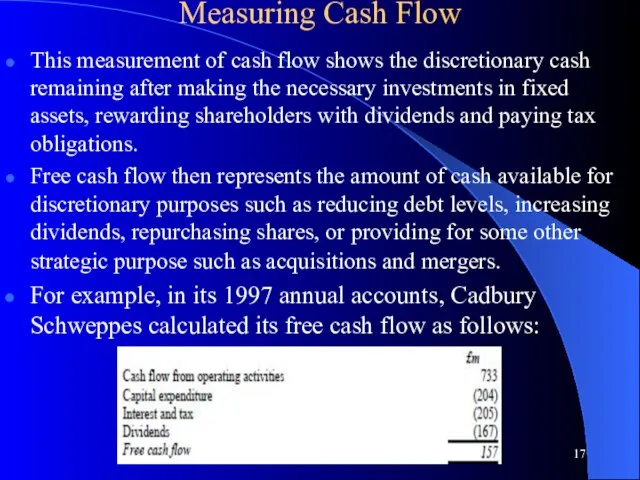

This measurement of cash flow shows the discretionary cash remaining

Measuring Cash Flow

This measurement of cash flow shows the discretionary cash remaining

Слайд 18Measuring Cash Flow

However it is measured or defined, cash flow generation is

Measuring Cash Flow

However it is measured or defined, cash flow generation is

Слайд 19Cash Inflows and Outflows

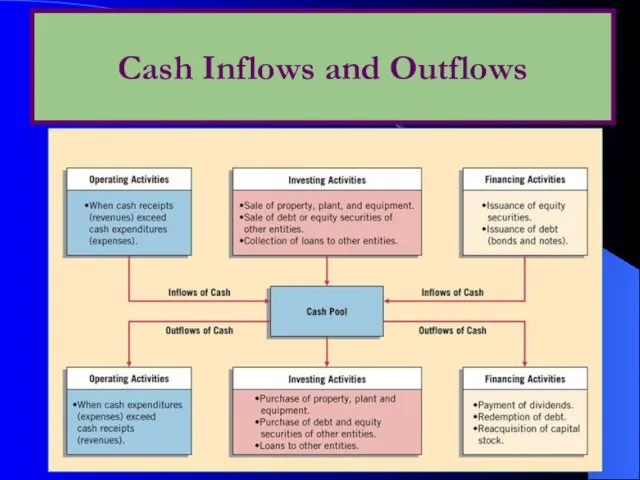

Cash Inflows and Outflows

Слайд 20Risk and Return

The motivation for undertaking an investment decision is the expectation

Risk and Return

The motivation for undertaking an investment decision is the expectation

Слайд 21Risk and Return

In the context of financial management by risk we mean

Risk and Return

In the context of financial management by risk we mean

Слайд 22Risk and Return

This allows the decision-maker to create probability weightings for a

Risk and Return

This allows the decision-maker to create probability weightings for a

Слайд 23The Expected Risk and Return Tradeoff

The Expected Risk and Return Tradeoff

Слайд 24Risk and Return

The risk of investing in a bank or building society

Risk and Return

The risk of investing in a bank or building society

Слайд 25

The investor’s propensity for risk-taking

Figure shows, other things being equal, the positive

The investor’s propensity for risk-taking

Figure shows, other things being equal, the positive

Слайд 26

The investor’s propensity for risk-taking

Individuals and corporations are generally considered to be

The investor’s propensity for risk-taking

Individuals and corporations are generally considered to be

Слайд 27

Time Value of Money

Cash flows which are to be received at some

Time Value of Money

Cash flows which are to be received at some

Слайд 28

Time Value of Money

Not only is the concept of measuring returns in

Time Value of Money

Not only is the concept of measuring returns in

Слайд 29The Time Value of Money

Obviously, $1,000 today.

Money received sooner rather than

The Time Value of Money

Obviously, $1,000 today.

Money received sooner rather than

Слайд 30INFLATION

You may have wondered about the role inflation plays in the time

INFLATION

You may have wondered about the role inflation plays in the time

Слайд 31Why TIME?

Observe that the concepts of future value and present value

Why TIME?

Observe that the concepts of future value and present value

Слайд 32How can one compare amounts in different time periods?

One can adjust values

How can one compare amounts in different time periods?

One can adjust values

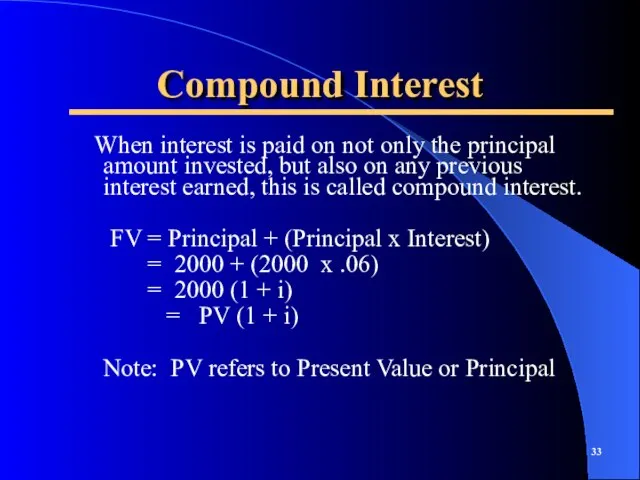

Слайд 33Compound Interest

When interest is paid on not only the principal amount

Compound Interest

When interest is paid on not only the principal amount

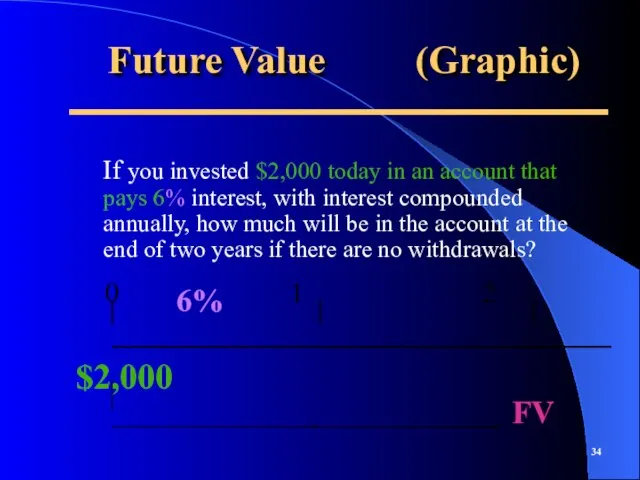

Слайд 34Future Value (Graphic)

If you invested $2,000 today in an account that pays

Future Value (Graphic)

If you invested $2,000 today in an account that pays

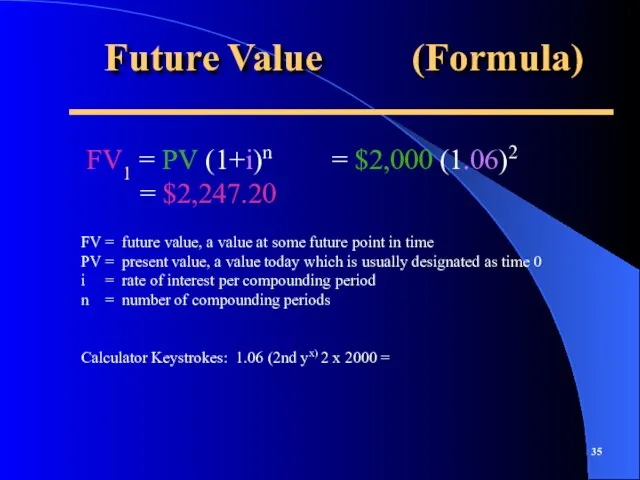

Слайд 35Future Value (Formula)

FV1 = PV (1+i)n = $2,000 (1.06)2 = $2,247.20

FV =

Future Value (Formula)

FV1 = PV (1+i)n = $2,000 (1.06)2 = $2,247.20

FV =

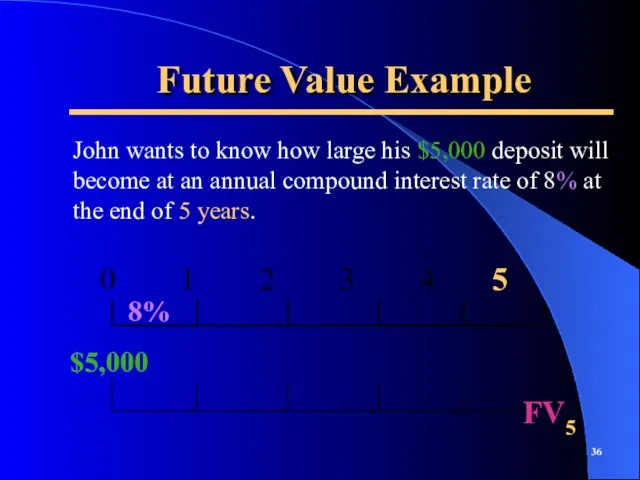

Слайд 36Future Value Example

John wants to know how large his $5,000 deposit will

Future Value Example

John wants to know how large his $5,000 deposit will

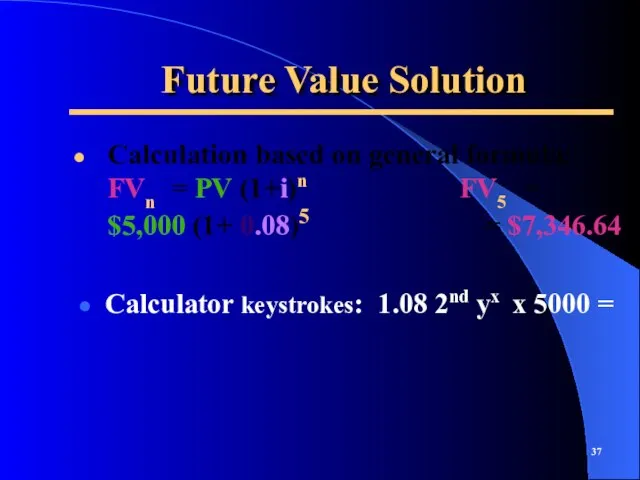

Слайд 37Future Value Solution

Calculator keystrokes: 1.08 2nd yx x 5000 =

Calculation based on

Future Value Solution

Calculator keystrokes: 1.08 2nd yx x 5000 =

Calculation based on

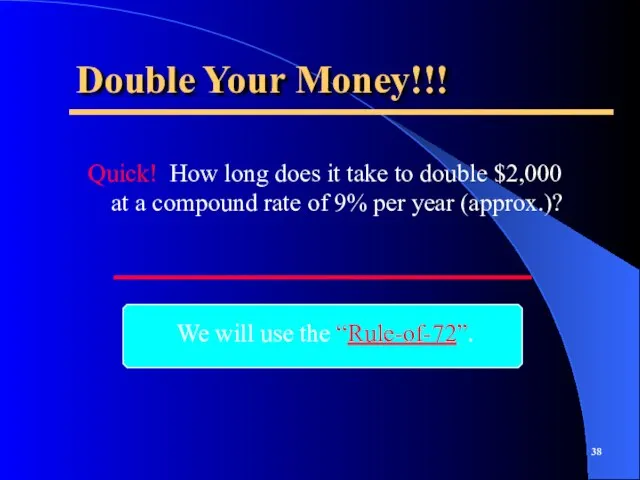

Слайд 38Double Your Money!!!

Quick! How long does it take to double $2,000 at

Double Your Money!!!

Quick! How long does it take to double $2,000 at

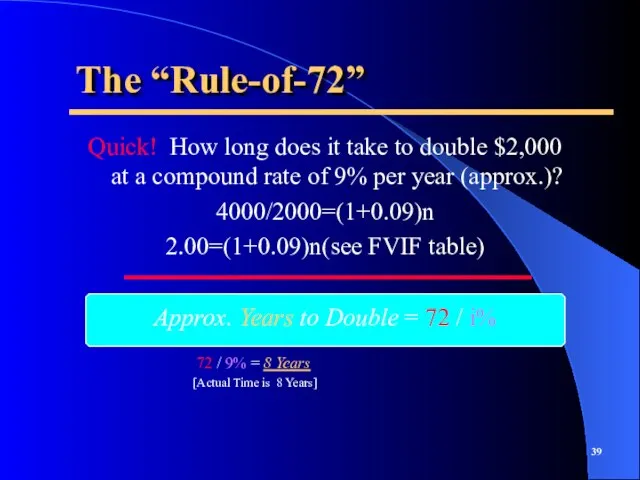

Слайд 39The “Rule-of-72”

Quick! How long does it take to double $2,000 at a

The “Rule-of-72”

Quick! How long does it take to double $2,000 at a

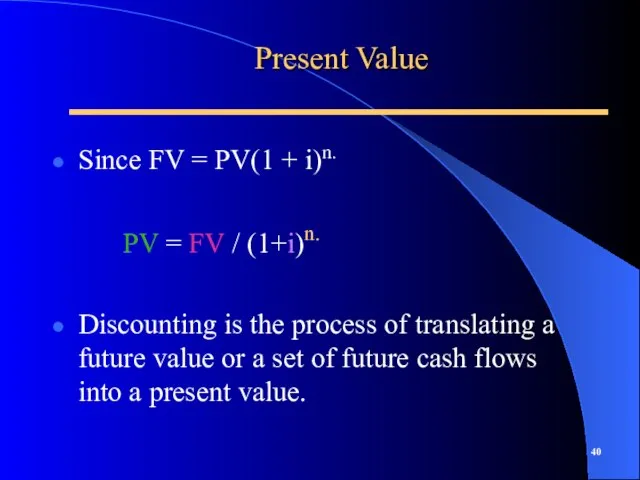

Слайд 40Present Value

Since FV = PV(1 + i)n.

PV = FV / (1+i)n.

Discounting

Present Value

Since FV = PV(1 + i)n.

PV = FV / (1+i)n.

Discounting

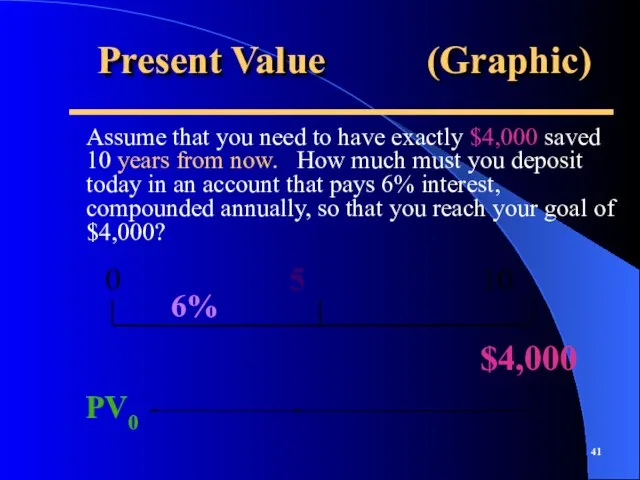

Слайд 41Present Value (Graphic)

Assume that you need to have exactly $4,000 saved 10

Present Value (Graphic)

Assume that you need to have exactly $4,000 saved 10

Слайд 42Present Value (Formula)

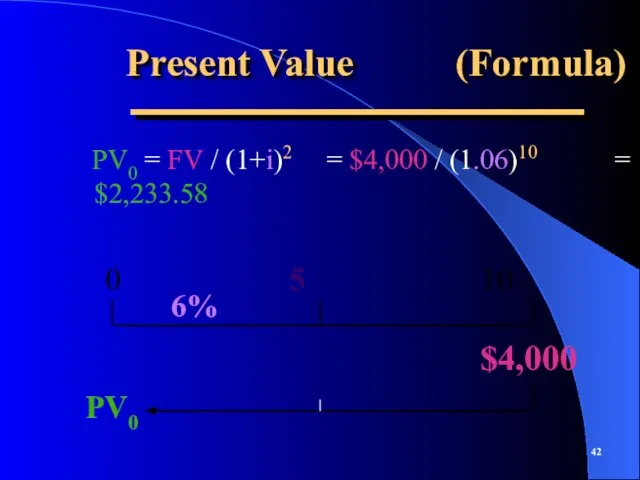

PV0 = FV / (1+i)2 = $4,000 / (1.06)10

Present Value (Formula)

PV0 = FV / (1+i)2 = $4,000 / (1.06)10

Слайд 43Present Value Example

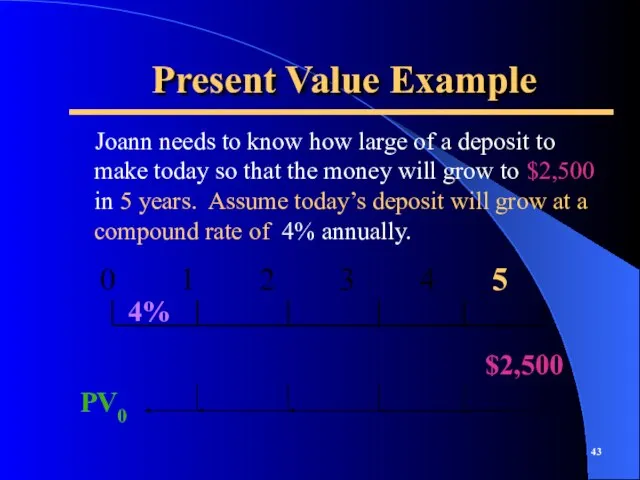

Joann needs to know how large of a deposit

Present Value Example

Joann needs to know how large of a deposit

Слайд 44Present Value Solution

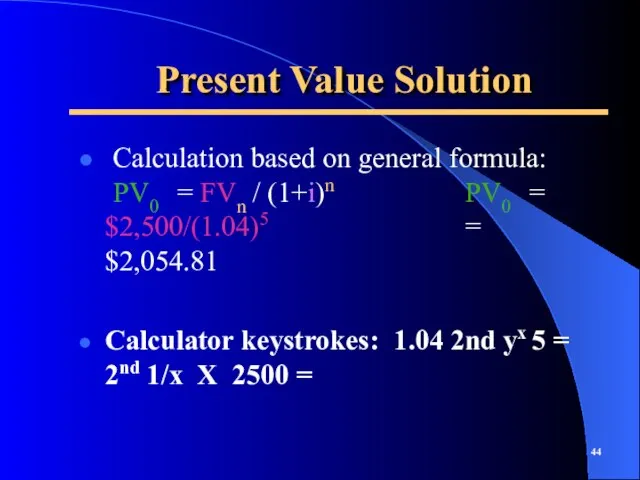

Calculation based on general formula: PV0 = FVn / (1+i)n

Present Value Solution

Calculation based on general formula: PV0 = FVn / (1+i)n

Слайд 45Finding “n” or “i” when one knows PV and FV(6/8.5)

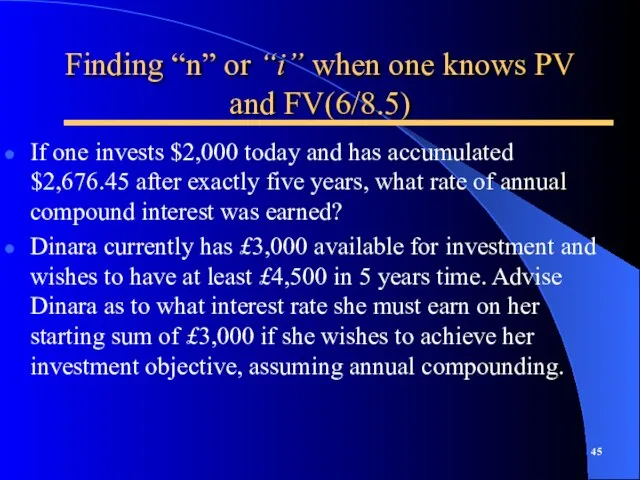

If one invests

Finding “n” or “i” when one knows PV and FV(6/8.5)

If one invests

Слайд 46Frequency of Compounding

General Formula:

FVn = PV0(1 + [i/m])mn

n: Number of Years

m:

Frequency of Compounding

General Formula:

FVn = PV0(1 + [i/m])mn

n: Number of Years

m:

![Frequency of Compounding General Formula: FVn = PV0(1 + [i/m])mn n: Number](/_ipx/f_webp&q_80&fit_contain&s_1440x1080/imagesDir/jpg/376780/slide-45.jpg)

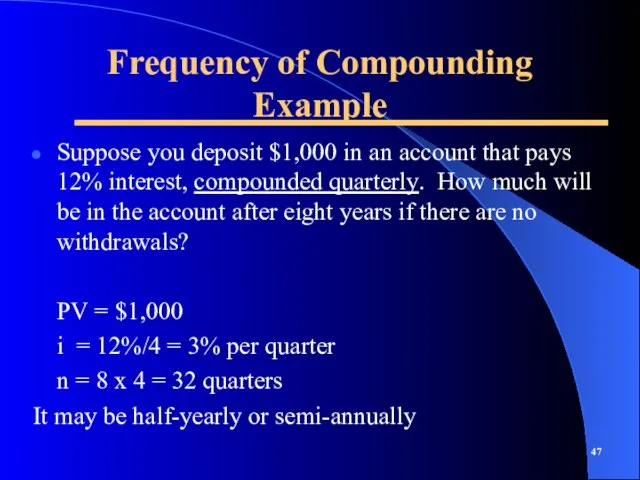

Слайд 47Frequency of Compounding Example

Suppose you deposit $1,000 in an account that pays

Frequency of Compounding Example

Suppose you deposit $1,000 in an account that pays

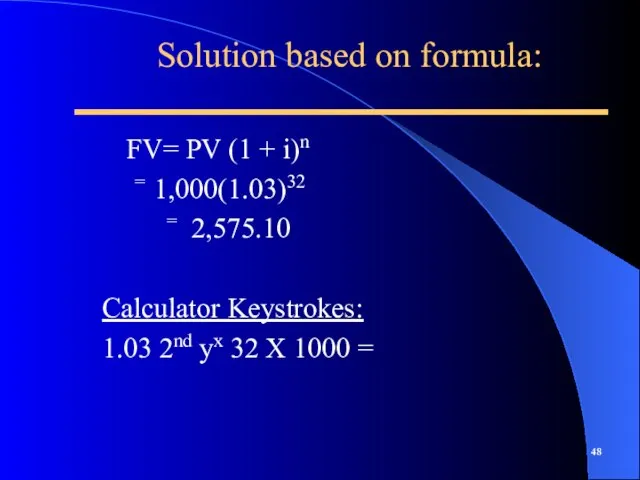

Слайд 48Solution based on formula:

FV= PV (1 + i)n

= 1,000(1.03)32

= 2,575.10

Calculator

Solution based on formula:

FV= PV (1 + i)n

= 1,000(1.03)32

= 2,575.10

Calculator

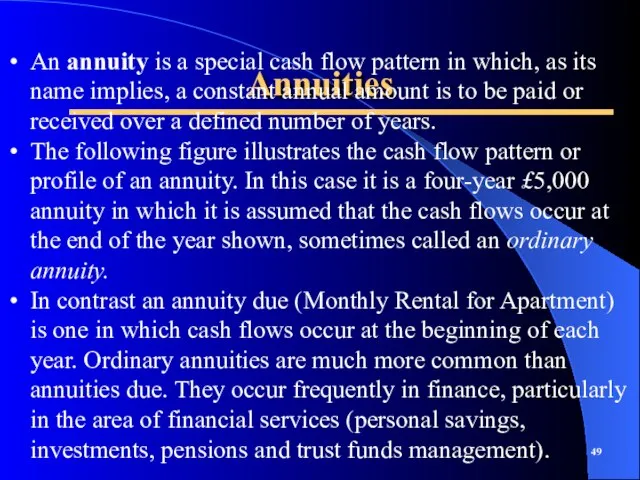

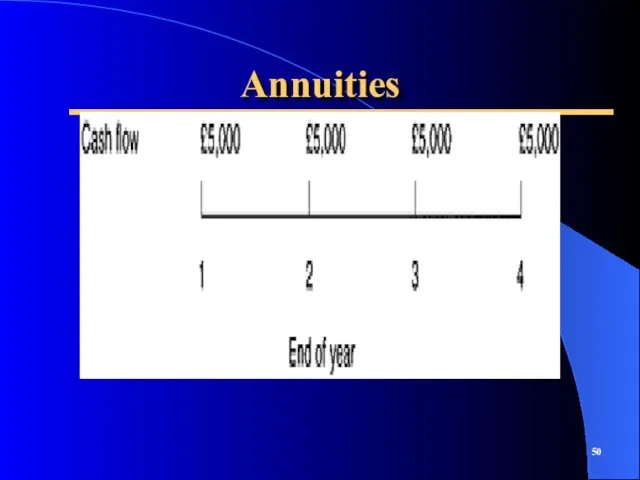

Слайд 49Annuities

An annuity is a special cash flow pattern in which, as its

Annuities

An annuity is a special cash flow pattern in which, as its

Слайд 50Annuities

Annuities

Слайд 51Annuities-Examples

Example 8 —The future value of an annuity

Anna would like to know

Annuities-Examples

Example 8 —The future value of an annuity

Anna would like to know

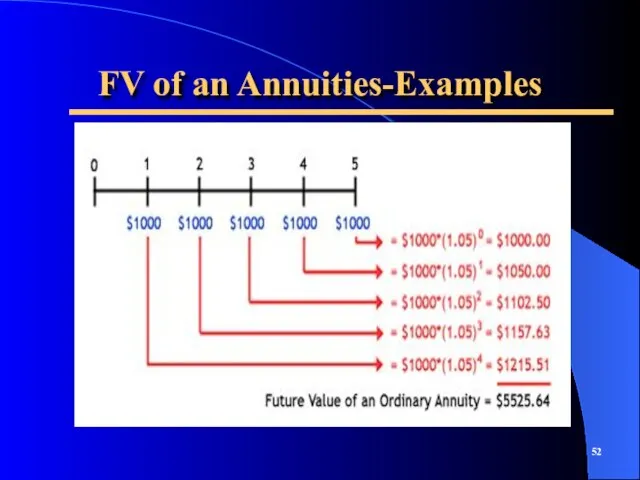

Слайд 52FV of an Annuities-Examples

FV of an Annuities-Examples

Слайд 53FV of an Annuities-Examples

Notice that since the first £1,000 is invested at

FV of an Annuities-Examples

Notice that since the first £1,000 is invested at

Слайд 54FV of an Annuities-Examples

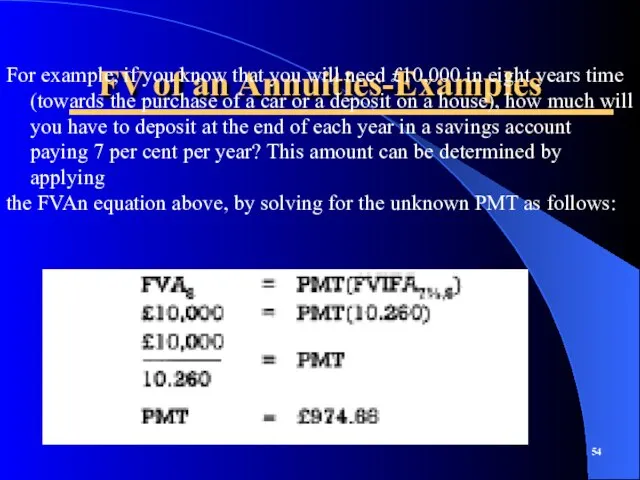

For example, if you know that you will need

FV of an Annuities-Examples

For example, if you know that you will need

Black English (Афроамериканский английский )

Black English (Афроамериканский английский ) Презентация на тему Корень. Родственные слова. Два признака родственных слов

Презентация на тему Корень. Родственные слова. Два признака родственных слов Презентация на тему Русские народные танцы (8 класс)

Презентация на тему Русские народные танцы (8 класс) Первые блюда. Супы

Первые блюда. Супы «Загрязнение атмосферного воздуха посёлка «Магистральный» выбросами автотранспорта и влияние отработанных газовна здоровье

«Загрязнение атмосферного воздуха посёлка «Магистральный» выбросами автотранспорта и влияние отработанных газовна здоровье  Создание рабочих мест

Создание рабочих мест С:ЕНКО MEN

С:ЕНКО MEN Традиции модернизма в искусстве 2-й пол. ХХ века

Традиции модернизма в искусстве 2-й пол. ХХ века Многогранники в живой природе

Многогранники в живой природе Sale 30% Bestia

Sale 30% Bestia ВЫСТУПЛЕНИЕ ПЕРВОГО ВИЦЕ-ПРЕЗИДЕНТА ОАО «РЖД»В.Н.МОРОЗОВА на VII Международной конференции «Рынок транспортных услуг: взаимодейс

ВЫСТУПЛЕНИЕ ПЕРВОГО ВИЦЕ-ПРЕЗИДЕНТА ОАО «РЖД»В.Н.МОРОЗОВА на VII Международной конференции «Рынок транспортных услуг: взаимодейс Эффективный нападающий удар в волейболе

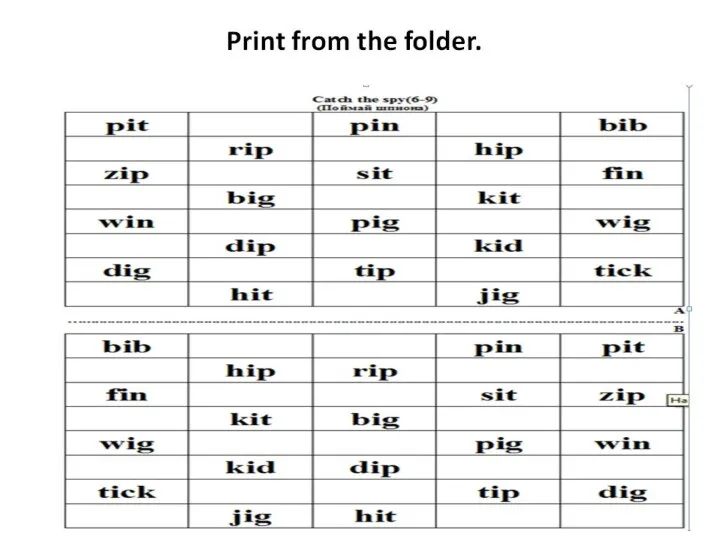

Эффективный нападающий удар в волейболе Print from the folder

Print from the folder Шаровая Молния.

Шаровая Молния. МОУ Голицынская СОШ №1 Презентация на тему : «Александр Невский – Патриот Земли Русской»

МОУ Голицынская СОШ №1 Презентация на тему : «Александр Невский – Патриот Земли Русской» Отделение дополнительного образования детей ГОУ школы №20

Отделение дополнительного образования детей ГОУ школы №20 Это мы, здравствуйте! 6 «Б» класс

Это мы, здравствуйте! 6 «Б» класс Потребности и способности

Потребности и способности a4c02c41e02991ba9d4f7fdd7cfefa1c

a4c02c41e02991ba9d4f7fdd7cfefa1c Собрание родителей и обучающихся 11 классов

Собрание родителей и обучающихся 11 классов Анализ и оценка организационных структур управления

Анализ и оценка организационных структур управления Органы государственной власти по Конституции 1918 г

Органы государственной власти по Конституции 1918 г Азбука потребителя

Азбука потребителя Совещание с грузоотправителями Калининградской железной дороги

Совещание с грузоотправителями Калининградской железной дороги Орудия труда

Орудия труда Полупроводниковые приборы

Полупроводниковые приборы Презентация на тему Гора Рашмор

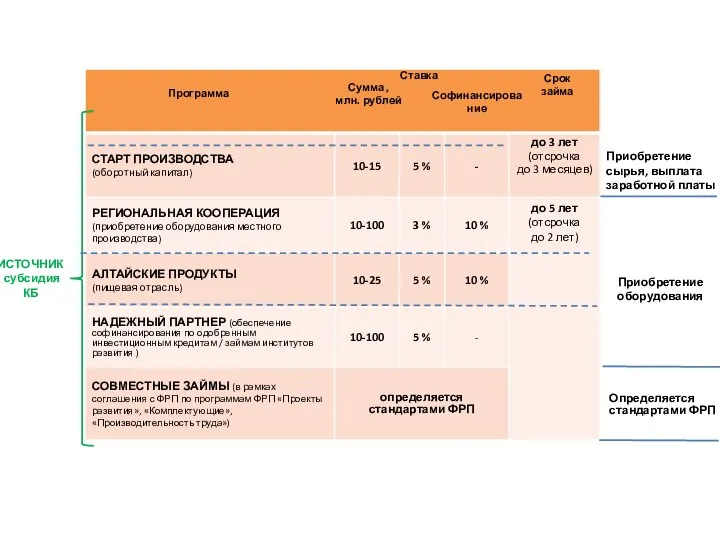

Презентация на тему Гора Рашмор Программы государственной поддержки малого предпринимательства на селе в Республике Карелия

Программы государственной поддержки малого предпринимательства на селе в Республике Карелия